Banking news and stories to help you maximize the financial success of your business Q2 2023 IN THIS ISSUE Meet our Everett Team Steps to Green Your Business Business Banking Mentor: Cost Optimization a publication of EMERGENCY FOOD NETWORK + HERITAGE A partnership that demonstrates the power of people

Expanding into Boise, ID

We’re excited to announce the opening of our new commercial banking center in Boise, Idaho. The new team of bankers bring significant experience, integrity, skill and community focus that local businesses and customers can count on. We look forward to our continued growth in Idaho and delivering a diverse set of high-quality banking services.

- Michelle Douglas, CEO, Emergency Food Network

Dini

Trueba

© 2023 Heritage Bank, member FDIC, Equal Housing Lender. The information in this magazine is general education or marketing in nature and is not intended to be accounting, legal, tax, investment or financial advice. Although Heritage Bank believes this information to be accurate as of the date published, it cannot ensure that it will remain accurate. Statements of individuals are their own and do not necessarily reflect the position or ideas of Heritage Bank. Contact us at 800.455.6126 or visit HeritageBankNW.com to make an appointment with one of our local experienced relationship managers to discuss your individual business banking needs.

| Member FDIC

Business Profile: Emergency Food Network ......................................................... 2 Meet Our Everett Commercial Banking Team ....................................................... 8 Managing and Mitigating the Major Risks of Climate Change on Your Business ................................................................... 14 SECURE Act 2.0 Preview ........................................................................................ 13 Steps to Green Your Business 18 Business Start-Up Guide: Know Your ‘Why?’ 21 Solar Tax Credits 24 IN

Heritage Helps .................................... 12 Our community involvement is part of our company’s DNA and something we’re very proud of. In this section, we highlight the good we're doing in our communities. My Heritage ......................................... 16 Meet our relationship managers and learn about their heritage. Business Banking Mentor 22 Improve your bottom line by considering these factors for cost optimization. Cybersecurity 25 Take these steps to protect your business and finances from fraud. Financial Dictionary 25 Empowering you to make smart business decisions by demystifying banking terminology. Equal Housing Lender

Banking Business is a quarterly publication of Heritage Bank Director of Marketing Shaun

Editor-In-Chief Whitney

Creative

Erica

Stephanie

Contributors Paul

John

Mike

Cover

Olli

3615

800.455.6126 HeritageBankNW.com

Contents

EVERY ISSUE

Carson

Gibson

Director

Bolvin Managing Editor

Neurer

Stearns

photo

Tumelius

Pacific Avenue Tacoma, WA 98418

“The thing I appreciate about Heritage is they’ve recognized what we know: That everybody can have an impact on food insecurity in their community...”

Emergency Food Network

2 18 16

Vecteezy

Mike Trueba

In light of recent events, we want to assure you that your deposits are safe and secure at Heritage Bank. Check out page 7 for a full statement on the strength of Heritage.

As always, we are here to help. If you have any questions or concerns, please reach out to your banker. We also have resources available at HeritageBankNW.com and financial documents available at hf-wa.com.

Environmental, Social and Governance (ESG) is a framework that helps stakeholders understand how an organization is managing its environmental and social impacts. It’s a topic that’s been front of mind for several years now and increasingly important for all business leaders to consider.

The world is facing unprecedented environmental challenges, including climate change, pollution and resource depletion. As a result, consumers, employees, investors and regulators are expecting businesses to take action and adopt more sustainable practices. However, being environmentally conscious is not just about avoiding negative consequences. It is also about seizing opportunities to innovate, differentiate from competitors and create value for all stakeholders. By adopting green practices, we can reduce costs, improve efficiency, attract and retain employees and appeal to consumers who prioritize sustainability.

In this issue, we feature two articles that can help you get started on your green journey: Managing & Mitigating the Major Risks of Climate Change on Your Business (page 14) and Steps to Green Your Business (page 18). We also share briefly about Heritage’s investment in projects focused on conserving energy on page 24.

As CEO, I recognize that our business activities have a profound impact on the world around us, and we have a responsibility to act in a way that is both ethical and sustainable. By prioritizing ESG in our own business practices, we can build a better future for our company, our stakeholders and our communities.

Thank you for reading Banking Business and for trusting us as your banking partner.

Sincerely,

Jeff Deuel President and CEO

2 022

Jeff Deuel is chief executive officer at Heritage Bank. He has more than 39 years of banking experience. Prior to joining Heritage, he worked at JPMorgan Chase, WaMu, Bank United, First Union, CoreStates and First Pennsylvania Bank. Jeff is a past chair of the Washington Bankers Association. He currently serves on the board of the Oregon Bankers Association and Pacific Coast Banking School. He is an avid cyclist and has climbed to the top of Mt. Rainier.

A MESSAGE FROM OUR CEO

Heritage Bank

CORPORATE CITIZENSHIP

1 Equal Housing Lender | Member FDIC HeritageBankNW.com

Visit HeritageBankNW.com to read more of our business profiles, then make an appointment with a banker who knows your industry. Olli Tumelius 2 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

Big Bite Out of Hunger

IN PIERCE CO UNTY, W A

Emergency Food Network supplies 75 food pantries with millions of pounds of nutritious goodness every year.

ARTICLE BY JOHN STEARNS

MMichelle Douglas describes her organization as the backbone of the emergency food distribution system in Pierce County.

It’s an apt description for the supportive role the nonprofit Emergency Food Network (EFN) plays in combatting hunger throughout the sprawling county, Washington’s second most populous. It’s a county where an estimated one in 10 residents is hungry, or roughly 95,000 people, according to EFN.

The food bank distributed about 13 million pounds of food last year, largely through its network of 75 food pantry partners, according to Douglas, CEO of EFN, which is based in Lakewood, south of Tacoma. EFN is the main food supplier that allows the pantries to stock their shelves and to-go bags for the thousands of people relying on the pantries for their most basic of human needs: food. EFN provides that food at no cost.

EFN’s mission: To provide Pierce County with a consistent, diverse and nutritious food supply so that no person goes hungry.

Last year, two million visits were made to food pantries that EFN supports, a 43% increase from 2021, Douglas said, underscoring the need for EFN’s role supplying its pantry partners

to support their operations and the people they serve. EFN typically provides anywhere from 10% to 90% of the food a pantry hands out, she said. That food comes through bulk wholesale purchases by EFN that it then portions into family-size packages; food donations from several food supply partners, including companies like Fred Meyer and Del Monte; food drives by individuals and businesses; and area farms, including Mosby Farms in Auburn and EFN’s own cropland, the eight-acre Mother Earth Farm in the Puyallup Valley.

As the nerve center, or backbone, for receiving, storing, packaging and distributing that food, EFN relies on a vast network of 2,000 plus volunteers, said Douglas, who joined EFN in 2017 as deputy director and assumed the top staff role in October 2018. Previously, she served as executive director of the Rainbow Center in Tacoma and as operations manager at the Center for Dialogue & Resolution in Tacoma, and she also has an extensive background in the food industry, including catering, hospitality and service.

“We couldn’t do any of the work that we do without our volunteers,” Douglas said of the organization that traces its roots to 1982, first as a community emergency food program, before

becoming an independent 501(c)(3) nonprofit in 1991.

EFN’s volunteers—including residents, employees (from partner organizations like Heritage Bank) and others— supplement EFN’s 27-person staff in numerous ways: sorting and packing food, loading trucks, delivering food and tending the farm, among other tasks. Many EFN volunteers are seniors, who largely stayed home during the pandemic for safety precautions, she said.

“We saw about a 60% reduction (in volunteers) overnight during COVID,” Douglas said in mid-February. “We’ve definitely seen a lot of improvement since then, but we’re not back to our pre-COVID levels at this point for volunteers.”

Combine that with a dramatic increase in food need during the pandemic as people lost their jobs and schools closed, with 49% of students in Pierce County on free or reduced meal programs, and the situation was “fairly terrifying,” Douglas said. Also suffering are seniors, whose fixed incomes aren’t keeping up with inflation, and others whose rents and other costs are consuming more income, forcing some out of their homes.

As an essential business that never closed, EFN at one point was so low on

TAKING A 3 Equal Housing Lender | Member FDIC HeritageBankNW.com

staff due to COVID that it had to call in the Washington National Guard to help stay open, Douglas said.

“The story of EFN in the pandemic is bringing together partners that we’ve been with for a long time, partners that were brand new and partners that never knew they wanted to be our partners to figure out how to feed people in Pierce County,” she said. Douglas is grateful for partners like Heritage Bank and others that provide food, financial and labor support that EFN can leverage to serve the county’s significant food needs.

Heritage ‘not just a bank’

As EFN’s primary bank, Heritage was a huge help during the COVID crisis, Douglas said.

Importantly, the bank helped EFN get a Paycheck Protection Program (PPP) loan and navigate the paperwork associated with it at a time when EFN labor was stretched thin by the pandemic.

“We were already at our maximum operating capacity just trying to get food out the door, and so add in a complicated loan like that—we wouldn’t have gotten through it without Heritage,” Douglas said. “They were awesome.”

That loan was huge, coming as EFN feared its client load could double

and as future uncertainty upended earlier financial projections for 2020. The client increase was closer to 60%, but PPP funding was key to supporting EFN when its services were in high demand, she said.

The bank’s support goes beyond helping in emergencies. It’s there day to day, with guidance from Chad Maiuri on the EFN board of directors, and Kristy Willet on EFN’s ambassador Board. The ambassadors are young professionals who help raise awareness about hunger in the community, volunteer for programs and services and assist in fundraising.

“They’re a constant presence and a constant cheerleader for us, and businesses like ours can’t survive without that,” Douglas said of Heritage.

That presence extends to the front lines, too, with employees volunteering to help pack food bags for Pierce County students during winter, spring and fall breaks when they don’t have access to school meals. The “break bag program” distributes about 2,000 food bags per break, or roughly 6,000 per year, Douglas said. Each bag contains about 20 pounds of food and prioritizes food that kids can prepare themselves and also includes food for the whole family. Additionally, the bank conducts annual food drives and sponsors EFN events.

“They’re deeply committed to volunteer engagement as part of their company values,” she said.

“The thing I appreciate about Heritage is they’ve recognized what we know:

Emergency Food Network Heritage Bank

4 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

Heritage Bank

At left: Hundreds of bags packed and ready for local school children as part of EFN’s regular Break Bag events./ Lavina Reyes, program coordinator, with bags that are packed with food for home delivery./ Heritage Bank employees repack dried oats into smaller packages during Heritage’s all employee Volunteer Day in September.

Below: Caroline Crum, volunteer coordinator for EFN, distributes free vegetable starts for people to grow their own produce. / Heritage Bank employees repack potatoes for distribution to local food banks supported by EFN. / Izzi Ceccanti, farm assistant, harvests some of Mother Earth Farm’s bounty to be distributed to clients in need. EFN prioritizes getting the produce delivered quickly while it’s fresh.

That everybody can have an impact on food insecurity in their community, whether that’s through their job, as individuals or as a corporation,” Douglas said. “And that is not a problem that gets solved alone; it only gets solved in partnership, and the call to action is to be one of the partners.”

Her insight for other businesses considering working with Heritage?

“I found Heritage to be fast and responsive,” Douglas said. “I’ve also found them to be creative partners when we’ve needed help. They’re very willing to be a thought partner with me and with our board about long-term benefits or solutions. They’re just truly value added. They’re not just a bank.”

‘The power of people’

EFN normally has an annual operating budget of about $6 million and receives in-kind food donations worth anywhere from $20 million to $26 million annually, Douglas said. It’s also the distributor for all federal food in Pierce County through The Emergency Food Assistance Program (TEFAP), one of the largest federal commodities programs in the country. EFN serves as the TEFAP contractor distributing federal food through its 75 subcontractor food pantries.

EFN annually budgets about $1.3 million to $1.6 million to buy bulk commodities directly from food manufacturers, including truckloads of tuna, pallets of 50-pound bags of rice, large containers of pasta, oats, canned fruit and vegetables, frozen proteins like chicken and turkey and milk. It purchased 1.8 million pounds of food in 2022. Bulk purchases allow EFN to buy at a discount, after which EFN volunteers then sort the commodities into smaller, family-size packages inscribed with cooking instructions in the various languages spoken in Pierce County. It’s that repacking by volunteers that allows EFN to leverage every $1 in food donated or purchased into five meals. A truckload of rice in 50-pound bags is about $10,000 cheaper than a truckload

Emergency

Food Network

Emergency Food Network

Emergency

Food Network

Emergency Food Network

5 Equal Housing Lender | Member FDIC HeritageBankNW.com

Heritage Bank

of family-size packages, she said of stretching EFN’s dollars with volunteers who package the rice for families.

“When we look at those kinds of stats, what we realize is the power of people is really what makes that possible,” Douglas said.

Those savings have been key in recent years as EFN has purchased more food to cover declines in donated products.

When EFN has the money, it likes to buy “bonus items” outside of core staples, including peanut butter and canned chili that are protein rich, maybe don’t need heating and can go to people who are unhoused.

EFN’s logistics can be complicated

When it receives a large donation of food, EFN must store it then distribute it. Time is of the essence for perishables or produce, for example. EFN wants to get food to pantries and kitchen tables while it’s fresh. If it receives 25 pallets of fresh food, say a pineapple donation from Del Monte, EFN tries to distribute it within 48 hours.

“I often joke that we proactively prepare to be reactive— whether that’s having trucks available, or frozen space, or refrigerated space, or warehouse space—we’re always trying to be able to say, ‘Yes,’” Douglas said.

EFN has about 23,000 square feet of warehouse space in Lakewood where food is received and repacked, and includes storage, refrigeration and freezers. It also has what it refers to as its “rolling warehouse,” comprising the back of 13 semitrailers. Locally, EFN works a lot with Mosby Farms, which Douglas calls a great partner to the food pantry business, Whole Foods, Harvest Against Hunger, Fred Meyer, Del Monte and many others.

Oftentimes, if a grocer’s refrigerated truck has its cooling go offline for even 10 minutes, a grocer must reject the load, but the food is still perfectly good, Douglas said, happy to take the call for such items.

“The easiest thing is to walk out to the dumpster; it takes more work and more effort to coordinate with a food bank, but it has this ripple effect across communities when you are able to make that coordination,” Douglas said. “And I’m not talking about coordinating after the rot starts, I’m talking about coordinating when the product is still fresh and beautiful. That is the win. The symbiotic relationship between companies and food banks is when that understanding is in play of: ‘What’s the greatest good for that food?’”

EFN supplements donated food with its products grown at Mother Earth Farm, which includes a small orchard that annually produces more than 43 tons of fresh fruit, vegetables and herbs. The farm grows about 129 varieties of produce that its culturally diverse clients may not find elsewhere, Douglas said, and the food is typically distributed within 24 hours of picking.

“It is beautiful, beautiful food,” she said. “We have some food pantries that pick up from us out at the farm, and then we also use it for our own home delivery program. We’re able to put fresh, locally grown Pierce County food into our home delivery bags that go out to about 200 to 250 families a week.”

While home delivery is a relatively small portion of EFN’s business, about 45 volunteers use their personal vehicles to take fresh produce to people in far-flung parts of the county who may lack transportation. Every other week, volunteers take shelf stable food and a fresh bag of local produce to recipients. Once a month, clients get an additional bag with items like eggs, cheese, milk and meat.

“Our biggest business is distribution, but this home delivery program is pretty impactful in the county as well because we serve all of the outer regions,” Douglas said. “We have a lot of food pantries, for example, in Tacoma, but Eatonville, there’s only one out there. So, if people don’t have transportation, having somebody come to your door is incredible.”

Taking care of land and people

Meanwhile, at its farm, EFN continues to look for the best ways to grow food for its clients and the planet. It puts a quarter of its farmland to rest each year; uses a tremendous amount of cover crops; and does projects with Pierce Conservation District involving hedgerows, pollinating rows and more to increase bee production. EFN maintains multiple beehives, too.

“We are constantly looking for how to make that farm be more productive and better for the world,” Douglas said, including employing organic practices in growing. The farm, however, is not organically certified.

EFN also has a community garden at its Lakewood facility, and it’s constantly working to reduce food waste.

Overall, EFN and its pantry partners ensure that people who need food can get it.

“The lowest barrier program out there is designed to be the food system,” Douglas said. “Because what we know is when we can successfully get people fed, then they can participate in other systems; but if they’re not fed, they can’t. Think about the last time you were “hangry.” How great were you at your job? We can’t live without being able to eat, and so we’ve worked really hard to reduce barriers to food access. Whether you are documented or undocumented, whether you are housed or unhoused, whatever your situation is…if you self-identify that you need to go to the food pantry to be able to eat, we want you to be able to get service.”

6 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

ABOUT EFN’S RELATIONSHIP MANAGER, HAILEY WHEELER Hailey started her banking career as a float teller. Over the years, she’s worked as a teller, personal banker and now branch manager. She spends most of her time building relationships with local businesses and community members.

STRENGTH OF HERITAGE Your deposits are safe.

We understand recent events surrounding the failure of Silicon Valley Bank (SVB) has caused many people to worry about the security of their deposits. Rightfully so as this is the second largest bank failure in our history. This has potentially far-reaching ramifications for the financial industry, but we want to remind everyone that Heritage Bank is very different than SVB. We have a broad base of customers in a wide variety of businesses. Our conservative approach to banking has enabled us to weather many difficult events over the past 95 years, most recently managing well through the pandemic and PPP process. We have a long history of providing exceptional service and financial security to our customers, and we remain steadfast in our commitment to providing a safe and secure environment for your deposits.

In these uncertain times, we understand the importance of trust and transparency. We are committed to keeping you informed about any developments that may impact your relationship with Heritage Bank, and we encourage you to reach out to us if you have any questions or concerns.

Details about our financials and recently filed 10-k can be found on our website at hf-wa.com.

Strategies for maximizing FDIC coverage

The FDIC caps coverage at $250,000 for deposit accounts but you can significantly expand your coverage with these strategies:

• A joint account with your spouse or partner gives you each coverage for a total of $500,000.

• ICS and CDARS programs, available for personal and business customers, divide your deposits across multiple banks, increasing the funds that are covered while maintaining the simplicity of banking at one financial institution.

7 Equal Housing Lender | Member FDIC HeritageBankNW.com

HERITAGE BANK’S NEW EVERETT OFFICE UNITES COMMERCIAL AND RETAIL TEAMS

ARTICLE BY JOHN STEARNS

Heritage Bank’s commercial and retail teams in Everett, Washington, were looking forward to uniting under one roof in mid-February, when a new downtown office was scheduled to open.

“This new location in downtown Everett brings us back into the center of Snohomish County, and it’s closer to many of our clients and prospective clients that we’re looking to develop relationships with,” Paul Dini, senior vice president-commercial banking regional manager, said. “Also, we get to partner and collaborate day to day with our retail partners to support our existing customers and our broader Everett community, so we’re really excited to be in this new location.”

The new office is centrally located downtown at 2831 Colby Ave., a mile west of where U.S. Highway 2 meets Interstate 5.

Since 2020, the commercial team had been located in Heritage’s northern operations center in Lynnwood, where it relocated after its lease at the Everett Mall Way location expired. Meanwhile, the retail branch had been operating out of a building on Evergreen Way, about two and a half miles south of the new location. The Evergreen Way location closed mid-February.

The new combined hub of commercial and retail banking is technically known as the Everett Commercial Banking Center, but it includes the Everett retail branch for customers to visit for deposits, personal loans and other business, in addition housing Dini’s team for any commercial banking needs.

Dini oversees six other commercial bankers in Everett. Including him, the team has about 165 years of combined banking experience.

The Everett commercial bankers and their areas of expertise and focus are: Neil Sudra, SVP-commercial team leader, commercial & industrial (C&I) lending in the aircraft, food and beverage distribution, life science, maritime, manufacturing, practice and professional services industries, owner occupied and non-owneroccupied real estate loans, construction real estate loans; Sally Johnson, SVP-commercial banking officer, working capital lines of credit, real estate lending, service businesses and manufacturing; Diana Ortega, SVP-commercial

banking officer, dental practice acquisition/expansion and nonprofits; Kevin Codd, VP-commercial banking officer, owner-occupied real estate financing and governmentguaranteed loans; John Chambers, VP-commercial banking officer, owner-occupied real estate and working capital and equipment financing for manufacturing, distribution and service businesses; and Simona DeVries, SVP-commercial banking officer, investor real estate, owner-occupied real estate and working capital lines of credit for various industries, with an emphasis on manufacturing.

“I really like the mix of experience and market knowledge on this team,” said Dini, who’s been in commercial lending for 34 years, the last seven at Heritage.

“Collectively, our time in commercial lending, our community network and the industry expertise all make up the competitive advantage that we have. It’s why this group has been successful and will continue to be.”

Whilethe bankers lend across several industries, business sectors that are among their niches are aerospace and ancillary businesses related to it; health care, with a particular focus on dental practices such as dental acquisitions and practice expansions; and commercial real estate, including multifamily housing, mini storage and industrial real estate, he said.

The Everett team is actively developing relationships with potential new clients for Heritage across those industries and others.

Those include a business in the electrical contracting industry seeking a line of credit and financing its owneroccupied real estate, a company in the aviation industry seeking a line of credit and a nonprofit organization for which the bank hopes to bring over the organization’s full deposit relationship and line of credit, Dini said.

“The loans we do really reflect the community we serve in Snohomish County,” he said, including significant lending for owner-occupied real estate, leveraging the SBA 504 loan program and lines of credit and equipment loans.

Significant projects Heritage is involved within the county include construction financing for a new school

8 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

Everett’s commercial banking team, left to right: John Chambers, Paul Dini, Sally Johnson, Simona DeVries, Diana Ortega, Kevin Codd. Not pictured: Neil Sudra

Olli Tumelius 9 Equal Housing Lender | Member FDIC HeritageBankNW.com

in Lynnwood, financing purchase of an office building in Arlington and a client expanding their retail business through the acquisition of two new locations on the Kitsap Peninsula in Kitsap County. In the broader region, the team is financing a dental practice acquisition in Federal Way as well as two multifamily projects—one a purchase and the other a refinance and renovation, both in Seattle.

Dini also oversees two other commercial banking teams in the northern Puget Sound region: one based in Burlington, which includes some bankers on Whidbey Island, and a team in Bellingham.

Much of the Everett team’s business is focused in Snohomish County but loans in other counties occur as its clients grow their business in surrounding markets, he said. In the new Everett office, having all the Heritage commercial and retail operations under one roof should benefit prospective and existing customers even more, he said. Think of it as a one-stop shop allowing customers to easily engage with commercial and retail bankers for their deposit, lending or other financial services needs. The office has about 18 total staff, including five members of Heritage’s SBA lending team.

Outside the office, the Everett team, like Heritage bankers everywhere, is heavily involved in the community.

“We definitely, as a team, have a strong and active connection with our community and that’s reflected in the variety of organizations we’re involved in,” Dini said. Examples include team members on boards for the Imagine Children’s Museum and ChildStrive, said Dini, who serves on the board of trustees for Economic Alliance Snohomish County.

“There’s a bunch of other organizations that we support,” he said. “Some are clients, some are just places where our team members volunteer and are passionate about those organizations.”

Some of those include the Boys & Girls Clubs of Snohomish County, Work Opportunities, Housing Hope, the Everett Gospel Mission, Wonderland Child & Family Services and Center for Human Services.

Community involvement is central to Heritage’s culture as a bank, he said.

“It’s reflective of our values as an organization and our commitment to not only provide financial services to the individuals and businesses in our community but to really ensure that as an organization we are supporting the broader community through our participation in these nonprofits and other similar entities,” Dini said.

SNOHOMISH COUNTY BY THE NUMBERS

Major industries: manufacturing, aerospace, government, educational and health services, retail trade, professional and business services, leisure and hospitality, construction

Major employers: Boeing, Providence, The Everett Clinic, Naval Station Everett, The Tulalip Tribes, Washington State & Snohomish County governments, school districts

Notable company headquarters: Alaska Airlines, Amazon, Coinstar/Redbox, Costco, Expedia, Microsoft, Nintendo

#1 first in manufacturing jobs in Washington state

#1 highest concentration of aerospace jobs

#2 highest number of tech jobs

#4 best community college in Washington (Everett Community College)

60% of jobs associated with international commerce www.economicalliancesc.org/workforce/major-employers/ esd.wa.gov/labormarketinfo/county-profiles/snohomish

ABOUT OUR COMMERCIAL TEAM

Combined banker experience: 165 years

Areas of expertise: real estate lending, owner-occupied real estate, government-guaranteed loans, manufacturing, dental practice acquisition/expansion, nonprofits, equipment financing, capital lines of credit

Volunteer hours served in 2022: 209

Charitable giving in 2022: $91,400

Top nonprofits: The Salvation Army, Housing Hope, Center for Human Services, Boys & Girls Clubs of Snohomish County, Everett Gospel Mission, Rotary Club of Arlington, ChildStrive

CONTACT OR VISIT

2831 Colby Avenue Everett, WA 98201 425.355.7375

Staci Lindstrand

VP, Branch Relationship Manager

Staci has been a community banker for over 20 years and has experience in both the branch and back office. Her years of experience help her find solutions for her customers’ needs now and in the future. She’s focused on building and maintaining long-term relationships with her customers and helping them reach their goals. Just as she cares about her customers, she also cares about her community. She serves on the board of several local nonprofits including Lake Stevens Education Foundation and Lake Stevens Chamber of Commerce and is a former coach for youth volleyball at the local boys and girls club.

Kristina Canizales, Assistant Manager

10 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

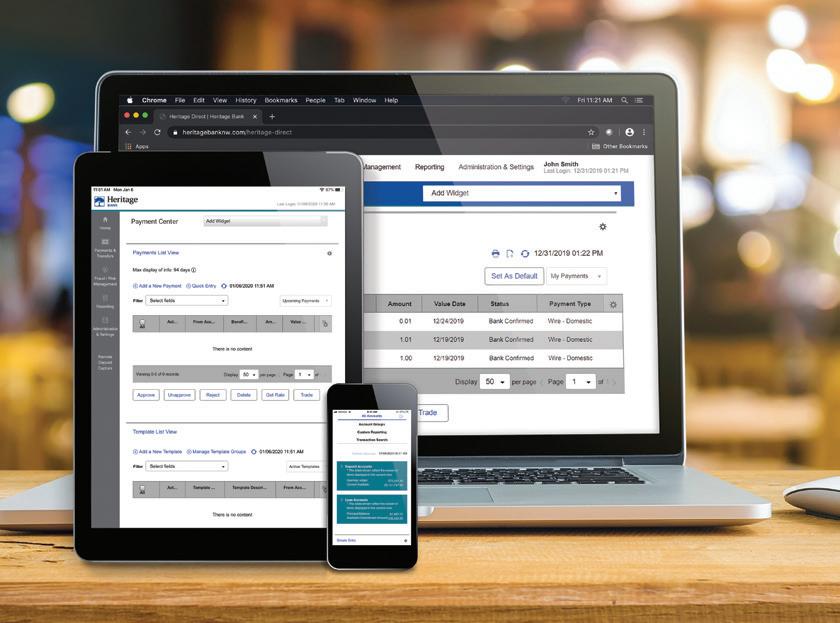

Scheduled Exports

A new Heritage Direct feature

Running reports on a regular basis? Now you don’t have to.

Define and schedule recurring exports* so they’re ready when you log in to Heritage Direct. This means less time spent on administrative tasks and more time growing your business.

File types available for export:

– BAI

– CSV

– QuickBooks

– Quicken

– TSV

Ask us how to get started.

*Currently only for balance and transaction history reports. For Heritage Direct Corporate users only.

11

HeritageBankNW.com

Equal Housing Lender | Member FDIC

MATCH GOOD

for

Here at Heritage, we are committed to continuously improving our community investment and giving. We’re proud to have team members involved in diverse and varied civic projects that serve and improve the places we call home. We want to celebrate and support their passions any way we can because what they care about, we care about.

“What a pleasant surprise! One thing RISE does is provide a mid-day meal every Saturday for homeless and low-income individuals. This will cover the cost of an additional five Saturdays.” – Quote from an employee who won an extra match

In 2018, we implemented a corporate match program as a way to further engage employees and amplify the impact of their donations. Through the program, employees can donate personal funds to organizations of their choice and receive a dollar-for-dollar match from the bank, up to $100 each year. Additionally, the bank hosts events throughout the year where employees’ donations are matched two-toone, with the chance to win additional matches through random drawings. During these events, the executive team pools their money to make a big impact at a local organization. Over the years, they’ve donated to Plymouth Housing, Junior Achievement, Community Roots Housing and The Wave Foundation. In total, they’ve given over $14,000. This year, their joint donation went to Financial Beginnings. Since launching the program, employees have donated over $66,000 and the bank has matched $120,000.

“Encompass is in the middle of a very large expansion, which Heritage Bank provided the funds! The center will house a Pediatric Center and Early Learning Center in Snoqualmie. Funds will be used for supplies for the new center. As our community grows, the need is far greater for children with needs as well as having children ready for elementary school.” – Quote from an employee

who won an extra match

Considering implementing an employee giving strategy at your own place of business? We highly recommend it! There are tons of advantages, and it can be beneficial for both your company and your employees. Programs focused around your employees and the causes they care about increases job satisfaction and attracts and retains talent. Plus, it can help you fulfill corporate social responsibility goals by demonstrating your commitment to community.

SECURE ACT 2.0: AN OVERVIEW

In the final days of 2022, Congress passed a new set of retirement rules designed to facilitate contribution to retirement plans and access to those funds earmarked for retirement.

The law is called SECURE 2.0 and it’s a follow up to the Setting Every Community Up for Retirement Enhancement (SECURE) Act passed in 2019. The sweeping legislation has dozens of significant provisions. Here are the major provisions of the new law.

New Distribution Rules

The required minimum distribution (RMD) age will rise to 73 years in 2023. By far, one of the most critical changes was increasing the age at which owners of retirement accounts must begin taking RMDs. Further, starting in 2033, RMDs may begin at age 75. If you’ve already turned 72, you must continue taking distributions. However, if you are turning 72 this year and have already scheduled your withdrawal, we may want to revisit your approach.1

Plan participants can use retirement funds in an emergency without penalty or fees. For example, beginning in 2024, an employee can take up to $1,000 from a retirement account for personal or family emergencies. Other emergency provisions exist for terminal illnesses and survivors of domestic abuse.2

Starting in 2023, if you miss an RMD for some reason, the penalty tax drops to 25% from 50%. If you promptly fix the mistake, the penalty may drop to 10%.3

New Accumulation Rules

From January 1, 2025, investors aged 60 through 63 years can make annual catch-up contributions of up

to $10,000 to workplace retirement plans. The catch-up amount for people aged 50 and older in 2023 is $7,500. However, the law applies certain stipulations to individuals with annual earnings more than $145,000.4

In 2025, the act requires employers to automatically enroll employees into workplace plans. However, employees can choose to opt-out.5

In 2024, companies can match employee student loan payments with retirement contributions. The rule change offers workers an extra incentive to save for retirement while paying off student loans.6

Revised Roth Rules

Starting in 2024, pending certain conditions, individuals can roll a 529 education savings plan into a Roth individual retirement account (IRA). Therefore, if your child receives a scholarship, goes to a less expensive school or doesn’t go to school, the money can get repositioned into a retirement account. However, rollovers are subject to the annual Roth IRA contribution limit. Roth IRA distributions must meet a five-year holding requirement and occur after age 59½ to qualify for the tax-free and penalty-free withdrawal of earnings. Tax-free and penalty-free withdrawals are also allowed under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.7

From 2023 on, employers can make Roth contributions to savings incentive match plans for employees (SIMPLE) or

simplified employee pension (SEP).8

The new legislation aligns the rules for Roth 401(k)s and Roth 403(b)s with Roth IRA rules. From 2024, the legislation no longer requires minimum distributions from Roth accounts in employer retirement plans.9

More Highlights

In 2023, the new law will increase the credit to help with the administrative costs of setting up a retirement plan. The credit increases to 100% from 50% for businesses with less than 50 employees. By boosting the credit, lawmakers hope to remove one of the most significant barriers for small businesses offering a workplace plan.10 From 2023 onward, qualified charitable donations (QCD) will adjust for inflation. The limit applies on an individual basis; for a married couple, each person who is 70½ years and older can make a QCD as long as it remains under the limit.11

The change in retirement rules does not mean adjusting your current strategy is appropriate. Each of your retirement assets plays a specific role in your overall financial strategy, so a change to one may require changes to another. Moreover, retirement rules can change without notice, and there is no guarantee that the treatment of specific rules will remain the same. This article intends to give you a broad overview of SECURE 2.0. It is not intended as a substitute for real-life advice. If changes are appropriate, your trusted financial professional can outline an approach and work with your tax and legal professionals, if applicable.

REFERENCES 1 Fidelity.com, December 23, 2022 / 2 CNBC.com, December 22, 2022 / 3 Fidelity.com, December 22, 2022 / 4 Fidelity.com, December 22, 2022 / 5 Paychex.com, December 30, 2022 / 6 PlanSponsor.com, December 27, 2022 / 7 CNBC.com, December 23, 2022 / 8 / Forbes.com, January 5, 2023 / 9 Forbes.com, January 5, 2023 / 10 Paychex.com, December 30, 2022 / 11 FidelityCharitable.org, December 29, 2022

This material is for information purposes only and not intended as an offer or solicitation with respect to the purchase or sale of any security. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss during periods of declining values. Neither the named representative, nor the named Broker-Dealer or Registered Investment Advisor, gives tax or legal advice. Past performance does not guarantee future results. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial professional for further information. These are the views of FMG Suite LLC, and not necessarily those of the named representative, Broker-Dealer, or Registered Investment Advisor, and should not be construed as investment advice.

Heritage Wealth Strategies is a marketing name of Cetera Investment Services. Securities and insurance products are offered through Cetera Investment Services LLC (doing insurance business in CA as CFG STC Insurance Agency LLC), member FINRA/ SIPC. Advisory services are offered through Cetera Investment Advisers LLC. Neither firm is affiliated with the financial institution where investment services are offered. Investments are: *Not FDIC/NCUSIF insured *May lose value *Not financial institution guaranteed *Not a deposit *Not insured by any federal government agency. 1000 SW Broadway, Suite 2170, Portland, OR 97205, (888) 360-0052.

13 Equal Housing Lender | Member FDIC HeritageBankNW.com

Almost all industries are threatened by the effects of climate change, either directly or indirectly, and most countries are working towards net zero carbon emissions by 2050. So, it’s important to understand how climate change could affect your business and what changes you need to make to reduce the impending impact.

Physical risks

It’s no surprise there are more extreme weather conditions than ever before, damaging property and disrupting supply chains. The implications for businesses include:

• The time and cost to put risk mitigation and disaster planning strategies in place, which can help solve issues such as critical buildings or production areas being unavailable, staff that can’t get to work or your operation going offline, leaving you unavailable to sell or service your customers for a period of time.

• The flow-on effect when certain industries either fail or face major financial stress. The agricultural sector is obviously exposed to flooding, drought and other weather fluctuations. If farmers stop purchasing, it affects the wider ecosystem around them.

• Tourism and the infrastructure that supports those operations will be hit hard if climate change eliminates industries that rely on year-round or seasonal tourists.

Increase in costs

Governments are painfully aware of balancing budgets, climate, productivity and staffing issues, often pulling from different directions. In addition, there will likely be increasing costs to businesses with the introduction of policy, laws and other regulations to manage climate change.

Insurance costs will increase as insurers work to shift the burden of loss from the few affected to the many that could be. Even if you live in an area that’s extremely unlikely to see a tornado, you could still see an increase in premiums.

With the push for greener energy sources, cities, towns and councils are also increasingly shifting to a reliance on renewable energy sources, demanding net zero carbon emissions from the businesses in their community.

Shutterstock 14 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

Reputational risk

As society changes its own view on ethical business practices, and sectors move away from activities that contribute to climate change, businesses risk being left with stranded assets (land, property or equipment) whose value has deteriorated. Customers may not want to see your fleet of trucks emitting diesel fumes, potentially causing the resale or residual value to plummet. Other reputational risks to your business include:

• If you fail to mitigate, disclose or comply with the changing legal and regulatory rules, you could face fines or, even worse, media coverage that highlights your failure to participate in avoiding climate change.

• Losing customers as people switch suppliers to those that do embrace climate change and can demonstrate their green credentials.

• Struggling to find employees who want to work for you or employees leave to a business that better fits their ideal business culture.

How to minimize climate change

It’s hard to change everything at once and possibly damaging to your business to upend your processes and supply chain overnight. First, identify the main risks your business faces with climate change, then work out over time how you can reduce the impact to your business.

Identify:

• The low-hanging fruit (low cost and fast to implement) and fix those things first.

• How to plan a net zero emissions strategy over the next 10 years.

• Changing your business model if there is a serious threat to your operation. An example is ski resorts developing summer tourist attractions as the winter seasons shorten.

• Who else you can work with? Other businesses (even competitors) will be in the same boat, so aim to work collectively to develop climate risk solutions leveraging the expertise of others. Connecting with your industry association to see what support they can offer is a good first step.

Next steps

If you don’t care about climate change, your customers will vote with their wallets. Taking action to reduce the impact on our climate is crucial, but it also makes good financial sense. Measure your carbon footprint and then start to reduce it.

Keep up to date on what’s happening with climate change in your industry and link to organizations driving change.

Shutterstock 15 Equal Housing Lender | Member FDIC HeritageBankNW.com

If you’re unsure what to do, seek help from experts and talk to other small business owners in a similar situation to discuss joint action.

BEST OF BOTH WORLDS

Growing Heritage in Idaho and my family at home

As someone born and raised in Idaho, opening Heritage Bank’s first branch in the state is a banker’s dream come true.

I joined the bank on December 1, 2022, to launch the Idaho expansion and take on this amazing opportunity to build something from the ground floor. It’s rewarding to bring an institution here that has the values and size that I think reflect this market. Speaking as someone who’s worked in banking for about 20 years, I know you don’t get these opportunities very often in your career, so I feel very fortunate and excited to establish Heritage’s Idaho home.

When interviewing for the job, I was impressed with Heritage’s senior leadership and the values they bring to the bank, which is reflected in Heritage’s culture and my own values. The bank has also supported me in hiring a great team for the Boise office. When fully staffed, we should have about 12 to 14 people.

The bank’s making a huge commitment to this market, and we’re building a full team, so it’s exciting to have that support and faith of Heritage’s executive management.

From our temporary location, we’ve already been transacting with prospective clients and establishing deposit accounts for other companies, and we can’t wait to get into our permanent location.

Ironically, building the Boise bank family coincides with building my family at home, where my wife, Desiree, and I last fall adopted two boys—Noah, 7, and Sha’dale, 9—from foster care in Texas. They joined our biological daughter, Eisley, 9, and son, Jack, 12. We welcomed them to our home November 18, 2022, and they have been an amazing addition to our family.

The transition has been great. All the kids get along super well, and we love our newly expanded family.

Sha’dale is nonverbal autistic. Noah was previously diagnosed on the autism spectrum, but we believe he is still autistic.

It’s been an adjustment trying to figure out Sha’dale and how to respond to his needs appropriately, but his foster mom of two and half years has been a phenomenal resource, and my wife talks with her often to learn how best to engage him. He’s a funny, sweet kid with a great sense of humor in his own way. It’s fascinating to see the wheels turning in his head.

Noah’s developmental delays are said to be mild. He can speak but acclimating with him has been unique, too. He’s very engaging with the family, the dogs and loves everybody in the house. He’s got the best laugh, he’s so happy, and he bounces everywhere he walks.

Desiree and I were several months into the adoption process when Texas officials told us the conditions of Sha’dale and Noah and provided the option to back out. Up until then, we were told they were loving, sweet and caring; loved dogs and trampolines; and that they wanted siblings and a forever home. That sounded perfect.

Learning their condition didn’t change our minds.

We had already decided their qualities were a good fit in our home and we determined their challenges should not

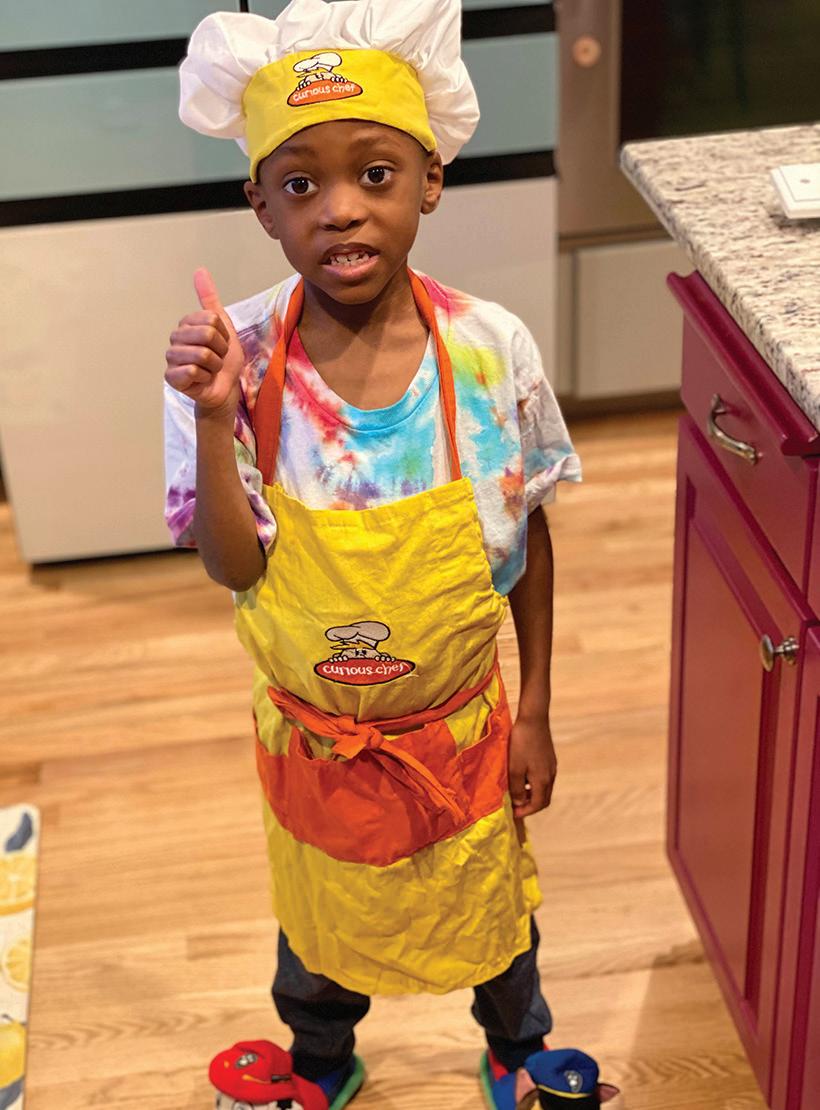

This page: The Trueba family (Des. Mike, Eisley. and Jack) in 2020 before it became a family of six in late-2022. / Mike and Desiree met Noah (left) and Sha’dale (right) for the first time at the Dallas Zoo in June 2022 and officially adopted them in November 2022. Here, Desiree gets to know the boys at the zoo. Facing page: Noah is ready to cook up some fun. / Sha’dale focuses on the task at hand.

This page: The Trueba family (Des. Mike, Eisley. and Jack) in 2020 before it became a family of six in late-2022. / Mike and Desiree met Noah (left) and Sha’dale (right) for the first time at the Dallas Zoo in June 2022 and officially adopted them in November 2022. Here, Desiree gets to know the boys at the zoo. Facing page: Noah is ready to cook up some fun. / Sha’dale focuses on the task at hand.

16 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

Photos courtesy of Mike Trueba

preclude them from a loving family. We saw no reason to give up on them because they would be more challenging to raise.

When you adopt from foster care, I don’t know that there is ever an easy or normal transition. I think it’s always challenging for a variety of reasons; these children have been through significant trauma in their life or they wouldn’t be in the situation they’re in.

So, I don’t think our situation’s unique, it’s just the specific factors that we’re dealing with make it our own unique situation. We knew we could provide Sha’dale and Noah a loving home and the resources and community they need to be the best versions of themselves. We figured we’d learn a lot, too, and have the opportunity to make everybody in our family better.

Desiree and I have always wanted a big family and long ago said we might adopt some day. While I only had one sibling, a brother who sadly died in 2021 at age 34 from a rare neurological condition, my dad had eight siblings, so I’ve always had a lot of aunts, uncles and cousins. Desiree is one of five kids. After my brother’s death and life’s uncertainties, we felt a calling not to delay adoption if we were ever going to do it.

Plus, we had a close call with Jack when he was young. He was diagnosed with leukemia at 18 months, an emotionally trying ordeal. A couple years after that diagnosis, we had Eisley. We wanted more kids and also knew a sibling would be the best bone marrow match for Jack if he ever needed that. Thankfully, Jack was cleared of cancer at 5 years old and has been healthy ever since.

With Jack and Eisley still young, we felt the time was right to adopt.

It’s very likely these two boys are never going to have a “normal” early adulthood and adulthood. Are we done

having more children? I don’t know, but I think we’re definitely going to be a lot more pragmatic about it because Sha’dale and Noah are probably around for the long haul. They’ve changed our perspective on what our future and potential retirement look like as they get older— and that’s okay.

In addition to family, I enjoy home projects or working on our vehicles. It’s a product of growing up with a father who was a skilled do-it-yourselfer.

He worked as a golf course superintendent, which took us from Boise to Gooding then Meridian. We then moved to Mountain Home, where he ran a potato and sugar beet farm, where I learned farming and how to fix farm equipment. Later, my dad ran an auto body shop in Mountain Home. In March 2022, I helped him buy his own business in Mountain Home, where he sells and services motor homes, trailers and powersports equipment. It’s called Terry’s Truck & RV.

After graduating high school in Mountain Home, I teamed up with three friends to form a rock band, Outside In. We moved to Boise and eventually recorded an album. We spent about five years living together, playing music and doing shows around the greater northwest, including in Boise, Portland, Seattle, Yakima and Spokane. I played bass.

We learned a lot, had wonderful experiences, met some incredible people and other bands and got to play fun shows. We played anywhere that a venue would have us: bars, clubs, events. The biggest venue we played was at Washington State University for Coug Fest, a spring event that drew maybe 10,000 people and included several other bands. We also headlined several times at what today is known as the Knitting Factory in Boise and played for maybe 1,000 people each time.

Eventually, we all kind of grew up and realized we weren’t going to be the Rolling Stones. We went our separate ways, but it was great while it lasted.

Throughout my life, I’ve had the opportunity professionally and personally to build meaningful relationships throughout Idaho. Banking is a relationship business and building relationships is the best part of what we do every day.

I’m thrilled to do that for Heritage in Boise as we build its presence in this incredible state.

ABOUT MIKE TRUEBA

17 Equal Housing Lender | Member FDIC HeritageBankNW.com

Mike is an experienced banker that will lead Heritage’s team in the newly expanded Boise, Idaho, market. Over the last 20 years, he’s held several leadership positions within the financial services industry, including retail, mortgage and commercial lending. This knowledge helps him build long-term trusting relationships. He listens to his clients’ goals, provides consistently reliable advice and tailors financial solutions to meet their needs.

Steps to Green Your Business Steps to Green Your Business

The obvious benefit of going green is that you’re helping to save the environment by reducing your carbon footprint. There will also be an increasing number of government and local council incentives (and penalties) to encourage change.

But there are also sensible business benefits to running a sustainable company, including saving money by reducing power bills, a healthier work environment for employees, strengthening the loyalty of existing customers and attracting new ecofriendly customers.

Here are some quick wins to start your green journey.

18 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

Vecteezy

Offer green transport incentives

Encourage employees to get to work using sustainable transportation methods, like walking, biking or taking public transportation. You can:

• Subsidize or buy public transport passes for your employees to make it cheaper to get to work and eliminate parking hassles.

• Provide secure bike storage or organize a carpooling system to encourage ride-share.

• Consider a location accessible to eco-friendly transit and close to bike lanes (if you ever move your business).

• Offer remote work options, which can have a massive impact on carbon emissions each year.

Make your office green

There are several obvious things you can do to make your office greener:

• Conserve energy by switching to LED lightbulbs, turning off electronics when they’re not in use, invest in light timers and take advantage of natural light by working near windows.

• Switch to natural and environmentally friendly cleaning supplies, use rechargeable batteries, only buy recycled paper and print double-sided.

• Give employees reusable water bottles to eliminate plastic, buy recycled ink cartridges and sprinkle live plants in the office to improve air quality.

• In the kitchen, swap disposable utensils and dishes for reusable ones, use fair-trade coffee and tea, avoid singleuse coffee pods or individually packaged snacks and upgrade to an energy efficient dishwasher and/or fridge.

Use sustainably sourced materials

Going green can be easier if you opt for green suppliers who:

• Use raw materials or their end products are sourced sustainably. Find out if they can prove they follow ethical, social and green rules.

• Use fair trade materials and, if imported, suppliers pay their employees fair and livable wages.

• Use renewable energy such as solar panels for climate control.

• Use materials that are recyclable, renewable and biodegradable (where possible), which includes ecofriendly packaging.

Plus, you can help the packaging dilemma if your packaging has a second use. For example, customers will often find a future use for a high-quality branded reusable drawstring bag, rather than a poor-quality cardboard box or plastic bag.

Do more online

There are ways to use the internet to limit your business footprint, even if you have a brick-and-mortar store.

Online marketing is one way to leverage the internet in an environmentally conscious way. Email marketing campaigns using automation software can replace print and social media can help you promote your business more efficiently than traditional advertising methods.

Adopt accounting software to send invoices online, limiting paper and postage, and help you get paid faster.

Store data online and replace on-site servers with a thirdparty cloud service to backup data, share files and make your business data accessible from anywhere, with very little environmental impact.

Green shipping

Think about your own shipping and packaging if you ship products to customers. Use boxes or bags as compact as possible to reduce the cost as well as the amount of space your product takes up in the carrier. This will result in fewer trips and fewer emissions.

You can also consolidate orders (if practical) so you’re shipping once to a destination and offer incentives for bulk purchases to reduce the number of times a customer orders each month.

Contribute back

You can actively support the environment by building into your marketing and community support ideas, such as planting a tree for each number of products sold or sales made. Some businesses donate a percentage of their profit to environmental causes.

Green business certification

By certifying your business as green, you’re better able to prove what you say. One way is to become B Corp certified, which means you not only practice being green but use sustainability throughout your business.

Next steps

Let everyone know about your green efforts. It’s a good look for your brand and demonstrates your commitment.

Finally, encourage your employees to buy into your greener world by incentivizing and rewarding good habits. Show appreciation for their efforts and ask for input on how you can make positive changes both in your workplace and your community. Set goals, celebrate your successes and consider setting up a person inside your business to champion the cause.

19 Equal Housing Lender | Member FDIC HeritageBankNW.com

Know your ‘why?’

If you dream of owning your own business, it’s important to make sure you cover all the business planning components to be able to start, grow and manage your business successfully.

Whether you want financial success or to turn your passion into a livelihood, transforming the idea of being your own boss into reality doesn’t have to be daunting.

We know that owner-operated businesses are the backbone of the economy, and every day, people like you talk to our bankers about getting into business for themselves.

As well as having the required level of skill, ability, knowledge and experience to run your business, you must be prepared to work hard and be clear about why you’re going into business.

Many people find the thought of working for themselves quite appealing. Being your own boss offers the freedom to:

• Work your own hours

• Make your own decisions

• Create your own lifestyle

However, establishing a successful business requires more than a great idea and a willingness to give it a go.

For example, you might be aiming to:

• Make more money than you could as an employee

• Be independent

• Represent a product or service you feel passionate about

• Create a business you can leave for family

• Build a business that you intend to sell

• Have a better work/life balance

Once you’re clear about why you’d like to be your own boss, it’s time to take a close look at yourself and determine if you have what it takes to run your own business.

Get our complete Business Start-Up Guide, designed to help you turn that desire to start your own business into a reality. Scan the QR code with your mobile device or, if you are reading the digital version of this publication, simply click or tap on the QR code to download the guide.

It contains important topics to review before you open your doors. By the time you’ve worked your way through the guide and have done your due diligence, you’ll be in a great position to consider whether you are able to launch your new business with as few roadblocks as possible.

HAVE QUESTIONS?

Remember that we’re always on hand to offer support. We want your business to succeed, so visit your local banking center or go to HeritageBankNW.com/business to connect with a business banking expert near you.

YOUR BUSINESS START-UP GUIDE

Shutterstock 21 Equal Housing Lender | Member FDIC HeritageBankNW.com

COST OPTIMIZATION

Improving your bottom line isn’t just about increasing your revenue but also comes down to reducing outgoings where you can. Reducing direct costs can dramatically increase your profit on each sale while eliminating unnecessary business overhead. Here are some things to consider for optimizing operational costs.

Lower the cost of purchases

Reducing what you pay for raw materials, components or employees who work directly on output will have a significant impact on optimizing your costs. This assumes of course that you can maintain the quality and service your customers expect. List your direct costs from the most to the least, select the top ten and then see if you can:

• Research and source cheaper suppliers.

• Ask your existing suppliers to renegotiate deals, offer early payment discounts or review more favorable terms. If you haven’t queried costs for some time, it’s never too late to ask and can be especially relevant for technology-based services, such as internet hosting and telco services (where costs drop each year).

• Buy in bulk, which often comes with a volume discount. Then consider where you can streamline expenses through larger, less

frequent, purchases.

• Consider whether switching out one ingredient or component for a more cost-efficient alternative is an option a customer may not notice or mind.

• Identify which of your products or services offer the slimmest margin for your business. Investigate alternatives, such as outsourcing or the use of contractors on an as-needed basis.

• Change your product mix and stop selling the things that are expensive to service or produce. If you can sell items that cost less to make or deliver, all things being equal, you’ll save costs.

• Use discounts from chambers or industry groups. For example, association memberships often provide supplier discounts to secure rates that are beyond the buying power of individual businesses.

• Look offshore to see if importing products or services will lower any direct costs.

BUSINESS BANKING

22 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

MENTOR

Lower the cost of expenses

At times it’s possible to lower your overhead while still operating effectively. Similar to reducing purchases, rank your most expensive costs in order and then start working your way down, applying cost-saving tactics in areas where you’ll see the most reward. You can try:

• Sub-contracting instead of having full-time overhead.

• Deleting a product line or service if it’s sold infrequently and is expensive to maintain or hold. For example, you may need extra warehouse space, dedicated employees or machinery that needs replacing.

• Auditing your operations to spot wastage from inefficient processes or shrinkage from theft or poor management of consumables.

• Switching manual processes to digital operations to cut down on things like paper, printing and stationery, not to mention labor and the cost of inefficient workflow. Ask yourself: where could you potentially streamline your business through digitization or automation?

• Pinpointing inefficient costs, such as cutting down on energy costs or getting rid of obvious overcapacity (unused phones, subscription costs, computer equipment, etc.).

• Measuring the impact of advertising and the return on investment. What may have worked in the past may not be bringing the returns it once did, and perhaps your marketing budget could be used in other channels with a more strategic approach.

Use technology to track and measure

Implement online accounting software to monitor your budget, track your payments and give visibility over your financials. Put robust systems in place that are checked frequently, such as using regular cash

flow forecasts, implementing clear payment terms and a robust payments process using online banking so you can catch inefficiencies early.

Call on your advisors

Lean on the expertise of your accountant who can help keep you accountable to financial targets, highlight any areas of concern and give you systems and benchmarks to keep you on track. Regularly

taking the time to review processes and activity within your business can help you reduce costs while still maintaining your brand integrity and the quality of your service.

Next steps

Benchmarking your business against similar companies may show that your performance is sub-standard. For example, your wastage levels might be higher than the industry average which is an opportunity to set goals to implement cost-saving solutions. Also, talk to your staff and get them involved in ways to cut costs. You might be surprised at some of their ideas. Give them an incentive to suggest cost-saving ideas and ask what causes them problems or wastes their time. Employees are more likely to cooperate with costcontrol initiatives if you explain the reasons for changes and the benefits to the business.

23 Equal Housing Lender | Member FDIC HeritageBankNW.com

SolarTa x Credits

The sun is a virtually limitless source of energy, and it’s not subject to price fluctuations or supply interruptions. It’s renewable, versatile and sustainable and can be used without depleting natural resources. Some of the benefits include:

• Doesn’t produce greenhouse gas emissions or other pollutants that contribute to climate change

• Lowers energy costs for businesses and individuals who invest in solar energy systems, resulting in longterm savings on energy costs

• Reduces dependency on traditional sources of energy (like coal, oil, natural gas, etc.)

• Improves grid security by reducing the risk of power outages caused by extreme weather events or other disruptions

• Can be used in remote areas where traditional power sources are not available or are unreliable

In addition to the positive environmental impacts, the solar industry has also seen considerable job growth, with a 5.4% increase from 2021 to 2022.2 The U.S. Department of Energy hopes to see the industry invest in education and training programs to help workers of all backgrounds advance their careers.

Inflation Reduction Act

The transformational Inflation Reduction Act (IRA) contains several provisions designed to entice a large number of community and regional banks to deploy capital into renewable energy projects across the U.S.

The act extends solar tax credits, or more broadly renewable energy investment tax credits (REITC), for at least 10 more years until greenhouse gas emissions are reduced by 70%. This extension and expansion of investment tax credits, along with other meaningful incentives included in the act, should result in a significant increase in renewable energy projects that are developed and constructed over the next decade.

Community banks are a logical source of project loans and REITCs, such as solar tax equity, in response to this expected flood of mid-size renewable projects. REITCs and the accelerated depreciation associated with a solar power project are fully recognized after it’s built and begins producing power. This is notably different from other tax credit investments (such as new markets tax credits, low-income housing tax credits and historic rehabilitation tax credits) where credits are recognized over the holding period of the investment and can take up to 15 years.

In 2022, Heritage invested $3.04 million in renewable energy tax credits to support a project that consists of a ground-mounted 3,024 kW solar voltaic energy system. Once complete, the land will be home to 5,600 solar panels that produce 5,788,000 kWh of clean energy and will support the operations of a local crop and cattle farm. We’re excited for the opportunity to invest in energy alternatives that are clean, renewable and reduce greenhouse gas emissions/pollutants. We hope this will be a catalyst for future projects that focus on reducing our collective carbon footprint and contribute to a more sustainable future.

“Clean energy creates good-paying jobs, stimulates our economy and protects our environment.”1

www.energy.gov/articles/doe-report-finds-energy-jobs-grew-faster-overall-us-employment-2021

1,2

24 Issue 9 | 2023 Q2 Banking Business a publication of Heritage Bank

Vecteezy

Avoiding Credit Card Fraud (part 1)

This is the first article in a two-part series. Look for the second article in the upcoming issue of Banking Business.

Safeguarding your business against fraud is important, particularly if your business is accepting credit cards. Credit card fraud is something that can never be eliminated but rather something that must be managed.

PREVENTING THE CAUSE OF FRAUD

If you can and it’s appropriate, avoid the chance of any credit card fraud by asking for and offering alternative payment options for customers. Ensure you’re equipped to process mail, telephone and/or internet orders prior to accepting credit card payments.

But chances are, credit card orders are part of your business model, either over the phone or online. So here are some things you can do to reduce the chance of fraud:

> Take extra care to validate the customer’s full name, address and contact details. Question any amendments a customer requests to their credit card details.

> Be wary if the address the goods are sent to differ from the cardholder’s address (especially if the credit card address and shipping destination are different countries).

> Question an order being shipped overseas if the customer could purchase the goods locally for a similar or lower price.

> Have deliveries made “signature required” with a courier of your choice to minimize the risk of carrier collusion, and never deliver goods to unattended premises.

> When receiving card payments ensure you never request for credit card numbers to be sent to your business by email. Email is not a secure channel and card details can easily be intercepted and used for criminal gains.

> For paper invoices and mail or telephone orders, use options such as click-topay invoicing solutions. They allow your business to create a payment order that can be copied into an email. This is a far safer why of processing card details.

> If you are an e-commerce merchant, using an approved outsourced third party to capture and process payments is the safest option.

> Be vigilant about unusual spending patterns or behavior could help you identify early warning signs that something may not be right. Visit HeritageBankNW.com for a full list of fraud prevention tools and resources.

FINANCIAL DICTIONARY

Community Development Entity

A Community Development Entity (CDE) is a domestic corporation with the ability to provide loans, investments or financial counseling in low-income communities. CDEs must obtain and maintain certification through the Community Development Financial Institutions (CDFI) Fund at the U.S. Department of Treasury. Eligible organizations must meet specific criteria to apply, which includes having a primary mission of serving low-income communities and maintaining accountability to the residents in those target markets. Certification as a CDE also allows organizations to participate (either directly or indirectly) in the New Markets Tax Credit (NMTC) Program, which incentivizes community development and economic growth through the use of tax credits that attract private investment in low-income communities. Heritage Bank was certified in 2021 and one of only a handful of CDEs in Washington and Oregon that’s able to facilitate these types of loans. Contact your banker if you’d like to learn more, are interested or have questions about your eligibility to apply.

ABOUT THE CONTRIBUTOR:

PAUL DINI

Paul has been in banking for over 30 years, and during that time, he’s held a number of leadership positions in commercial banking. As a commercial banking regional manager, Paul supports small and medium-sized businesses in his local market.

Shutterstock 25 Equal Housing Lender | Member FDIC HeritageBankNW.com

Go

– Ability to accept chip cards, PIN/debit cards and mobile payments

– Payment technology including smart terminals, in-person, online and tablet-based solutions

– 24/7/365 customer service and a dedicated account manager

– Solutions to help you protect your business from credit card fraud

– Loyalty programs to grow, retain and market your business

We may be able to save you money over your current merchant services provider. Ask us for more information today!

HeritageBankNW.com | 800.455.6126 | Equal Housing Lender | Member FDIC

green with digital payments made easy for you and your customers.