FROM a shack to a formal home: without a title deed this process is almost impossible. |

LALI/BIGGER

FROM a shack to a formal home: without a title deed this process is almost impossible. |

LALI/BIGGER

VIVIAN WARBY

I

N A small office in Khayelitsha a woman is poring over some documents.

The documents belong to another woman who bought a home informally, paid cash for it with money she had diligently saved as a nurse over the years, then she renovated the small place, adding on rooms and renting them out. She now wants to get the title deeds for the property into her name but is being told by the original seller, who still has the title deed, to pay him more money since the property is now worth more.

It’s a dire situation and the woman’s life savings, which she ploughed into fixing the property, are threatened.

This is one of thousands of

stories that the team at the Tenure Support Centre in Khayelitsha, whose main job it is to solve the title deed problems through legal formal channels, hear.

Some people wait up to 20 years to get the title deeds in their names. This means that the home has to be traded informally and for cash, often at well below market value, or it sits as dead equity unable to be traded in the formal sector. It also means that these homes cannot be used as collateral.

Sadly, people at the lower end of South Africa’s property market, because of issues such as lack of title deeds, among others, just can’t get their foot on the formal property ladder to use their homes as viable assets, earn a sizeable income and return from their bricks and mortar and

build generational wealth for their families.

If they could, the results would be bigger than any broad-based black economic empowerment (B-BBEE) project to date to create wealth for South Africans left out of the economic fold, say the experts.

The situation, however, is bad, with many RDP and other homes lacking title deeds. While the RDP homes are seen as subsidised homes, as soon as they are sold they become part of the affordable housing market, broadening supply to this sector where it is in critical need.

The market is thus further stymied by laws that prohibit the selling of RDP homes for the first eight years.

Some homes are also being built and renovations done without approved plans - you can’t get

approval to build without a title deed - putting this market further out of the formal structures where these properties could realise their true value and where there could be economic progress. All these stumbling blocks also keep the market out of formal financing.

Players in the sector say the government and many big players just don’t see the lower end as part of the property market even though the affordable market makes up well over 70% of the entire property market.

The informality is well and good until someone disputes ownership, and many have lost their hard-earned homes because of this.

Yet the government is missing out on what could be their biggest B-BBEE effort to date - giving people at the lower end of the

property market, through better laws and title deeds, the right to use their homes as an asset and accumulate wealth, says housing specialist Kecia Rust, executive director and founder of the Centre for Affordable Housing Finance in Africa (CAHF).

Property economist Professor Francois Viruly, who has spent over 25 years in the analysis of the South African property market, says “a lot of value is sitting in these segments of the property market that is just not being unleashed”.

Rust says that what the government’s housing policy fails to do, and continues to fail to do, is engage with the housing market. Rust has been working in the sector since the early 1990s.

Continued on Page 3

THE buy-to-let investment strategy has faced challenges across South Africa due to rising interest rates, economic shifts and escalating property prices. Investors are under pressure to ensure that rental income can cover the higher costs of financing properties. Despite the challenges, Cape Town and the broader Western Cape continue to offer promising opportunities for buy-to-let investors.

Cape Town’s vibrant urban centres, scenic coastal towns and robust rental market have kept the region’s property market resilient. Semigration, where individuals relocate from other provinces to the Western Cape in search of better lifestyles and security, has been a key factor in maintaining high demand for rental properties.

“As migration to the Western Cape intensifies, the demand for rental properties continues to grow, making the buy-to-let market in Cape Town an appealing option for savvy investors,” says Odette Maartens, the head of rentals at DG Properties.

Here is why buy-to-let is still profitable in Cape Town. Rising demand

The semigration trend has led to a booming rental market. Many semigrants rent properties while they evaluate longterm settlement options. This has created sustained rental demand in high-demand areas.

According to Statistics SA’s Household Survey, the number of households renting has increased from 17.7% in 2020 to 23.9%, highlighting a preference for renting as property prices rise. Furthermore, ooba Home Loans data shows that 32.9% of the Western Cape’s property demand stemmed from buy-tolet applications in June last year, up from 21.5% in March 2020. The surge is largely driven by

the semigration trend, creating a shortage of properties.

Capital growth

Cape Town continues to see property price growth, particularly in areas like Sea Point and Claremont, offering investors attractive rental yields and long-term capital growth. Despite the Western Cape having the highest average purchase price for homes, buyto-let investments are surging, as foreign investors compete for limited available properties. Rising house prices are also pushing more people into the rental market.

According to the Vacancy Survey for the first quarter of this year, vacancy rates in the Western Cape have dropped to their lowest levels since 2016, recording a mere 4.42%.

This reflects the strong demand for rental properties, making the region a solid investment for landlords.

Prime locations

Investors looking to capitalise on Cape Town’s rental market should carefully consider the location. Some prime areas for buy-to-let investments:

The Atlantic Seaboard: Areas like Sea Point, Green Point and Mouille Point are sought after for their vibrant lifestyle and proximity to the ocean and CBD. The areas attract local and international tenants, particularly semigrants, creating strong rental demand. Although

entry prices can be high, yields in the areas are attractive.

City Bowl: The City Bowl area, encompassing Gardens, Vredehoek and Tamboerskloof, is popular among young professionals and creative entrepreneurs. Its proximity to the CBD, along with easy access to major transport routes and a vibrant cultural and social scene, makes it a top choice for renters. The area’s scenic views of Table Mountain and the harbour, along with trendy cafés, restaurants and entertainment hubs, draw tenants looking for an urban lifestyle with a touch of nature. Rental demand remains strong, with solid yield potential.

Southern suburbs: Neighbourhoods like Claremont, Rondebosch and Newlands are favoured by families and students for their proximity to top-tier schools and universities. The southern suburbs have remained in demand, particularly among semigrant families. The areas offer stable rental income and solid capital growth. Key considerations

While Cape Town’s buyto-let market offers substantial opportunities, investors should consider several factors:

Interest Rates: The repo rate remains at its 2023 level of 8.25%, with a prime lending rate of 11.5%. The stable environment makes financing more predictable for investors.

Experts predict that interest rates might begin to drop by the end of the year.

Tenant Profiles: Semigrants are typically professionals or families looking for long-term leases. Selecting properties in secure, family-friendly neighbourhoods and performing thorough tenant vetting can help secure reliable rental income.

Property Management: Hiring a property management company can help with day-today operations such as tenant screening and rent collection. Potential pitfalls

Seasonal Vacancy Rates: Coastal towns experience higher occupancy during the holiday season and slower periods in the off-season. Investors should consider whether they prefer the higher returns of holiday rentals or the stability of long-term tenants.

Maintenance Costs: Properties near the coast require more maintenance due to exposure to sea air and weather.

Affordability: Cape Town remains one of South Africa’s most expensive regions. Investors need to ensure that rental yields justify the higher initial investment and ongoing costs.

For more information on DG Properties, call 021 433 2580 or Maartens at 073 190 5726 or visit www.dgproperties.co.za

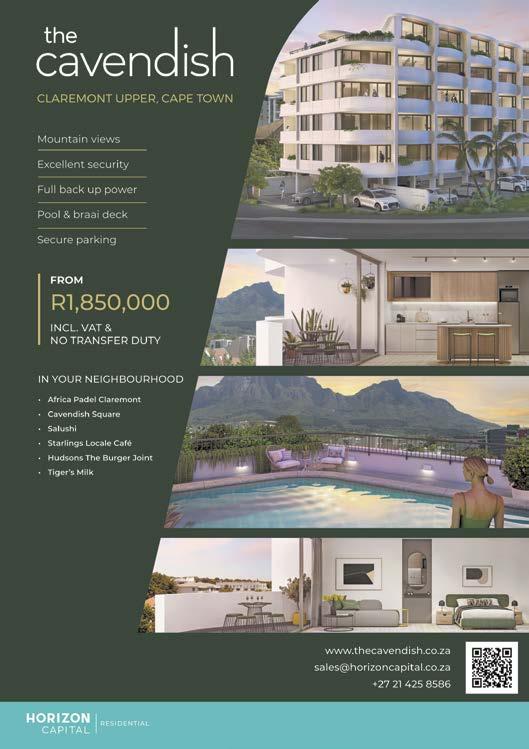

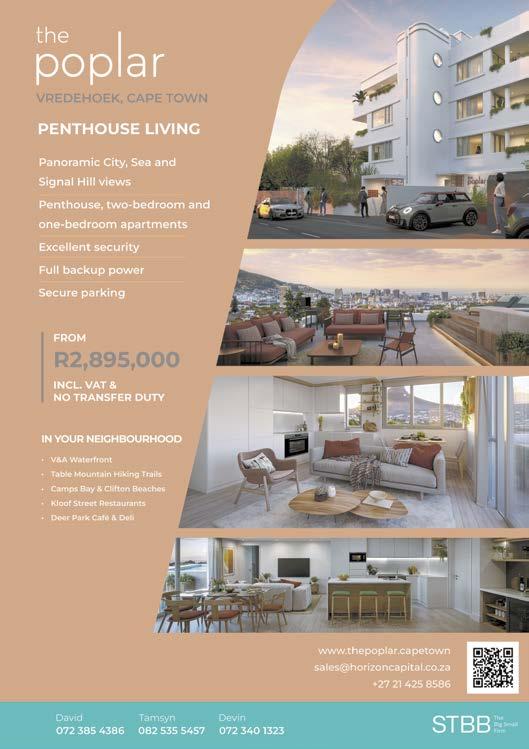

HORIZON Capital Residential is proud to present two boutique developments: The Cavendish in Claremont Upper and The Poplar in Vredehoek, both under construction.

The Cavendish, at 25 Cavendish Street, is a boutique collection of 32 apartments, making it a perfect investment for students and young professionals.

Nestled in the vibrant suburb of Claremont Upper, The Cavendish is surrounded by Cavendish Square shopping centre, Africa Padel courts and trendy coffee shops and restaurants. Residents will enjoy convenience and modern comfort.

The Cavendish offers a 5th floor communal roof and pool deck providing a picturesque location to take in the Mountain vistas and sunsets.

Completion is anticipated for December next year. The Cavendish promises a

lifestyle of ease in one of Cape Town’s most desirable neighbourhoods.

The Poplar, at 11 Davenport Road in Vredehoek, offers 14 high-end apartments on the slopes of Table Mountain. With breathtaking views of the mountain, City and sea, the apartments are a prime Airbnb opportunity, ideal for those looking to invest in the booming short-term rental market.

The Poplar has topped out after casting the 5th floor penthouse roof and is set for completion by the middle of next year.

Both developments reflect Horizon Capital’s commitment to quality, offering a rare opportunity to invest in Cape Town's prestigious suburbs with no Transfer Duty.

For more information, visit www.horizoncapital.co.za. Contact our team at sales@horizoncapital.co.za or 021 425 8586.

THE small West Coast towns and villages are no longer just for holidays and retirement, as more people are moving into areas such as Langebaan, Yzerfontein and further afield to St Helena Bay and Elands Bay, say agents from the Seeff Property Group.

The beautiful fishing villages, many with whitewashed Cape vernacular architecture have seen a strong shift in sales activities during the market boom of 2021/22. The migration of wealth to the West Coast is seeing prices of up to R5 million to R8m being paid for luxury homes in Langebaan.

Employees in Saldanha and Vredenburg and those who own businesses there, as well as those who come to the West Coast for contracts and other business reasons, often prefer to settle in places such as Langebaan.

This has boosted the Langebaan property market where transactions worth more than R1.3 billion were recorded for the 12 months to the end of last month, according to Lightstone data.

Given the proximity to Cape Town – less than a twohour drive – Langebaan is a popular weekend getaway. Many Capetonians own homes or rent Airbnbs. Families are also moving there, and now have access to a Curro School.

Places such as Malmesbury have benefited from the upgrades to the N7 Cape Town to Namibia Route that runs through the region. Given that it is only about a 40-minute drive from Cape Town, many people choose to settle there and commute daily, says the Seeff group.

Lightstone data shows the West Coast property markets boomed during the 2021/2 period, resulting in notable growth in median prices over the past five years, doubling in areas such as Yzerfontein and Paternoster, while areas such as Langebaan, Malmesbury and St Helena enjoyed a notable uptick. Most towns experienced growth of between 60% and 107% and some even 196% over the past 10 years. Yzerfontein boasts the highest average transaction price of R3.1m, followed by Langebaan at R2.3m.

Continued from Page 1

The housing sector, she says, is an asset to the country in terms of job creation and economic growth and is more than merely “roofs over heads”.

“A house should be an asset where owning it raises some appreciation and an inheritance for your children. It should also have a financial benefit as an income earning opportunity in a country with high unemployment. And if people are able to access mortgages, they can convert savings accounts into growth of capital.”

If 4 million unencumbered households could use their homes productively for economic activity, says Rust, it would go a long way towards the nation’s goals of B-BBEE. “We need to get our heads away from just delivery ... it is critical.”

Eight-year wait

But some things have to change to get the lower end of the market to work. For instance, waiting 8 years by law to be able to sell an RDP home “distorts the market”, says Viruly. “If you can’t sell your home, it restricts your ability to move up the housing ladder and further restricts the flow in the property market,” he says, adding that RDP homes should be freed up for sale sooner to allow flexibility and to make the market work more efficiently.

“The president says we are asset poor and yet there is great value that sits in those markets that has not been unleashed.”

Professor Ivan Turok, a professor of City-Region Economies at the University of Free State who has also worked in the sector for decades, says the 8-year rule “sounds great when you draw up a policy - but the government needs to get its feet on the ground - they are not connected to the everyday lives of people”.

“The 8-year rule stops the markets from working well. People’s circumstances change and they may want to sell their RDP home to move to a bigger home, or they may get a job in another province. “The rule creates rigidity in what should be a flexible market where there is also natural evolution.

“The minute a person sells their RDP home before the eight years is up they have broken the legal system and have to do the sale informally and are unable to pass on the title deed, and so the home - most people’s biggest asset - immediately becomes an inferior product.

“If the government would use its common sense it would see how certain rules create informality.”

While new builds are needed to address the affordable housing crisis, the sale of second-hand homes also go towards solving the problem, making getting this right crucial, says Turok.

Development Action Group (DAG) programme manager Zama Mgwatyu says the government needs to look at the township market with new eyes, “because some of the rules they have in place, and the backlog of title deeds, is preventing the market from flourishing”.

The property ladder

Instead billions of rands that could be circulating in a formal property market are lost.

Ideally, says Rust, the property ladder should start right at the bottom where someone who lives in a shack identifies an old RDP house for sale which they can afford in an existing township.

They then sell their shack for R10 000 - an informal transaction - and the person now has a deposit to formally buy the RDP home which could be R200 000 and under. They may even be eligible for a Flisp subsidy and mortgage finance.

The person who sold the RDP home now has R200 000 in their pocket, having benefited from getting an RDP home, and can now buy an improved RDP home, for say R400 000. Now the seller of the improved RDP home has a substantial deposit - equity - to go up the property ladder.

“If we could see the residential property market as a single market from right at the bottom upwards, it would work. However the split in South Africa - so well described as a house with two floors and no stairs to the second floor - creates a bifurcated property market where housing for some cannot be treated as an asset,” says Rust.

Khayelitsha estate agent Zola Wilfred Mekula, owner of agency Zolam Properties, says things are getting worse, not better.

“Most of the houses on the market need cash buyers. You will find the owner may have extended the home without getting approved plans, or they dealt with a dodgy architect who told them the plans were approved when they weren’t, and now while a buyer may be able to get a bond, they can’t get it for a home that doesn’t have approved plans.

“It then becomes a very expensive exercise to go the formal

route. We have even seen people who paid bribes to officials to turn a blind eye to their building, now unable to sell their homes because they don’t have the right documents.”

Ädded to that the backlog with title deeds hits the market - “it is killing the property market in the townships”.

“Townships can’t just be dormitory areas, we need to get them working as part of the formal economy and the government needs to come to the party to understand the township market,” says Mekula.

Both sellers and buyers are compromised in an informal transaction – but ultimately, it is the buyer who is most at risk.

Title deeds

The issue with title deeds is one of the biggest stumbling blocks to formalising the lower end of the property market. The government is aware of this and the Department of Human Settlements has made as one of its priorities a title deeds programme to ensure security of tenure for many South Africans who have never before owned a property.

It took DAG’s Mgwatyu, himself, 17 years to get the title deed to his RDP home.

“There are formalities built into the system, however, the very people making the laws are also the ones that gave RDP homes without title deeds. It is as though some parts of the market have been set up for informality.

“What really needs to happen is that there has to be a massive education roll-out by the government to people in the townships of how the property market works,” says Zama.

He says the informal market is fraught with deceptive “professionals” and when people try to do the right thing, they are often hoodwinked by these unscrupulous people, further cementing in their minds that it is easier to work with a street committee than go the formal route.

Viruly says with no title deeds it is, in effect, “denying South Africans the asset class components of properties. This has wide ramifications - people can’t get bonds to buy homes that have no title deeds and the city can find it difficult to bill for services”.

The Tenure Support Centre

One beacon of hope in acquiring a title deed is the Tenure Support Centre (TSC) situated in a First National Bank branch in

Khayelitsha.

The TSC began as an actionresearch project between the Centre for Affordable Housing Finance in Africa (CAHF) and 71point Consulting.

It has now been set up to help clients formalise tenure, regularising informal property market transactions that have taken place in the past, transferring properties out of deceased estates and securing primary transfer on properties that have never been formally transferred from the government to housing subsidy beneficiaries.

TSC attorney Lisa Hutsebaut and TSC client administrator Sona Nongqayi say in the short time it has been open, the TSC has assisted over 2 200 Khayelitsha residents with their title deeds issues.

“This is a difficult job,” says Nongqayo, who meets face to face with those seeking help, “Some days the painful stories get overwhelming.

“Some people arrive owning a home but they are the fourth person to have bought it without a title deed and no one knows who the original seller with the title deed is. The devastation is big, but on the day someone gets their title deed, after a long search and battle, the joy they feel knowing that this will change not just their lives but that of their families is unbelievable. It makes this worth it.”

Hutsebaut says by the time people end up at the TSC office “they have used all means, some have even got help from outside the formal structure”. Some never received title deeds, some have had a parent die decades ago and the title deed is still in the deceased’s name, for instance. “It is a complicated system to navigate and is also expensive. The TSC has funding and expertise so this makes it a simpler, cheaper route for those stuck in a horror story.”

Illana Melzer, engagement manager at 71point Consulting, who opened the TSC at first to get data of the biggest housing issues in the township, says the titling issue is “catastrophic”. “We are still trying to figure out how many people who received RDP homes didn’t get their title deeds in the first instance. Roughly it could be

about almost half a million people. Khayelitsha, a relatively new township, for instance, has over 40% of people in one area with no title deeds to the property they “own”, either because they never received title deeds, or there’s been a deceased estate, a divorce or an informal sale.

“Some of the ‘missing’ RDP title deeds are sitting in boxes in different municipalities and are just not being handed out - there seems to be an ambivalence about it, and yet without a title deed people are forced into an informal market where their asset’s potential will never be truly realised,” says Melzer.

It also shuts off formal financing. “There is very limited participation by the financial sector, they can’t give a secure loan if they don’t know who owns the home. Added to that, to get a title deed is a clunky, and long, process and can cost from R10 000 upwards, when you can “just go to a street committee and pay R300 to get a piece of paper saying the home is yours.”

The TSC has up to now been getting funding which makes the process of getting a title deed affordable to the lower end of the market.

“It is our hope to spread this operation throughout the country with funding. If we have more, it could be a game-changer, says Melzer.

The problems facing the lower end of the property market can feel overwhelming, catastrophic, unsolvable even, and those impacted may feel powerless - but for small pockets of hope like the TSC.

“We can’t give up hope,” says Turok. “It is a recipe for disaster. We have to see the positive things going on and build on those positives.”

The alternative, says Melzer, is to leave it, say it was a failure, and let people go and accumulate their wealth outside the townships in the suburbs where they can legally grow their assets.

“But that would be really sad.

“And while the situation is not a good one and will require a real effort to solve it… it is doable if we put our heads down.”

ELCOME to Wytham Estate, where retirement living is redefined with a blend of luxury, comfort and community. Situated in Cape Town’s southern suburbs, our estate is designed specifically for those over 60, offering an unparallelled living experience that combines elegance with practicality.

A new standard of living AT Wytham Estate, we offer a range of beautifully designed apartment-style units and mews homes, each crafted to meet the highest standards of comfort and style. Our residences feature spacious layouts, modern finishes and energy-efficient amenities, including solar power and battery storage. The elements are thoughtfully integrated to ensure your home is not only luxurious but also sustainable and cost-effective.

Each home is surrounded by meticulously landscaped

gardens, creating a serene and picturesque environment that enhances your living experience. Whether you’re enjoying a peaceful morning on your private balcony or strolling through our award-winning gardens, you’ll find that every aspect of Wytham Estate is designed to provide a tranquil and pleasant setting.

Exceptional amenities for a fulfilling lifestyle

Wytham Estate is more than just a place to live – it’s a community where you can thrive. Our estate boasts an array of amenities designed to cater to your every need and interest. The on-site restaurant and bar offer the perfect venue for socialising with friends and family, while our dedicated community spaces host a variety of events and activities that foster a vibrant and engaging atmosphere.

Health and wellness are

central to our offering. We provide tailored home-based health-care services that ensure you have access to the support you need while maintaining your independence.

Our premier security system adds an extra layer of comfort, giving you peace of mind and ensuring that you and your loved ones are safe.

A community like no other One of the most compelling features of Wytham Estate is our strong sense of community. We understand that retirement is not just about a beautiful home but also about living in a place where you feel connected and valued. Our community is designed to encourage interaction and engagement, with regular social events, clubs and activities that allow you to build lasting friendships and pursue your passions.

From fitness classes and hobby groups to

THE serene setting means residents can enjoy a peaceful morning on their private balcony or go for a stroll through the award-winning gardens.

cultural outings and social gatherings, there’s always something happening at Wytham Estate. Our residents enjoy a rich and fulfilling social life, all within the welcoming and supportive environment of our estate.

Convenience meets tranquillity Wytham Estate offers the perfect balance of tranquillity and convenience. Enjoy easy access to amenities, shopping and health-care facilities, all while being nestled in a peaceful, picturesque setting.

The prime location ensures that you have everything you need within reach, making everyday living convenient and enjoyable.

Your perfect retirement home awaits At Wytham Estate, we believe that your retirement years should be the best years of your life. With our luxurious homes, exceptional amenities and vibrant community, we provide an environment where you can live your life to the fullest.

We invite you to visit Wytham Estate and experience firsthand the exceptional living we offer. To learn more and schedule a tour, visit www.manor.life or contact us at sales@curaterealty.co.za or 063 707 2886. Discover how Wytham Estate can be the perfect setting for your next chapter. Your dream retirement lifestyle is within reach – come and make it a reality.