28 EXPRESS PHARMA TO HOSTTHE MAIDEN EDITION OFPHARMA LEADERSHIPAND INNOVATION CONCLAVE IN MUMBAI

28 HYDERABAD TO HOSTTHE SEVENTH EDITION OFPPLCONCLAVE 2025

MARKET

30 EVOLUTION AND COMMERCIALISATION OFCELLAND GENE THERAPIES

32 THE UNMISSABLE ASIAHEALTHCARE OPPORTUNITY

STRATEGY

37 PHARMA’S STRATEGIC PATH TO GROWTH IN THE NUTRAMAZE

39 2025: HEALTHCARE AND LIFESCIENCES INVESTMENT OUTLOOK

Regd.With RNI No.MAHENG/2005/21398.Postal Regd.No.MCS/164/2025 - 27.Printed and Published byVaidehi Thakar on behalf of The Indian Express (P) Limited and Printed at The Indian Express Press,Plot No.EL-208,TTC Industrial Area,Mahape,Navi Mumbai-400710 and Published at Mafatlal Centre,7th floor,Ramnath Goenka Marg,Nariman Point,Mumbai 400021.

Reproduction in anymanner,electronic or otherwise,in whole or in part,without prior written permission is prohibited.

Pg22

Trumping the Budget blues?

Perhaps the uncertainty of the Union Budget pales before the changes that US President Trump will make as he gets down to business in his second term

Even as industry braces for the impact of Union Budget 2026, there is a sense that Prime Minister Modi’s government makes announcements beyond the Budget. This could work both ways: additional funding or penalisation through more regulation or taxation.

Either way, there are some who now prefer a ‘bland budget’ as it makes for a more stable and predictive environment, apart from giving lobby groups more time to present their case to/influence policy makers, away from the spotlight.

Perhaps the uncertainty of the Union Budget pales before the changes that US President Trump will make as he gets down to business in his second term. He has already made big announcements (withdrawing funding to the WHO, pulling out of the Paris climate accord to name just two of them)

And while he has left the door open on resuming funding to the WHO, ("if they clean it up" as he put it in a rally in Las Vegas just days after his initial announcement) Trump 2.0 will clearly stick to his poll agenda of Make America Great Again (MAGA). Which is just another avatar of our very own Atmanirbhar Bharat. Let’s be fair, every national leader’s mandate is to put their people and nation first.

However, there are times when leaders need to think of the world as a global village. For instance, climate change impacts all countries.

Climate experts are correlating the Los Angeles wildfires of January to a decade of extreme drought, followed by two years of heavy rains, followed again by extremely dry ‘fire weather days’, which resulted in perfect conditions for wildfires to catch and spread. President Trump has another year before making good on his threat to leave the Paris agreement, so there is hope that he will reconsider his decision by then. Similarly, the COVID pandemic proved that viruses don’t respect country borders. Hoarding vaccines or prev enting the export of certain equipment critical to make vaccines resulted in a prolonged battle against the virus. Countries

Perhaps the uncertainty of the Union Budget pales before the changes that US President Trump will make as he gets down to business in his second term

which lacked the resources to make or buy vaccines were the last to be COVID free and remained a possible source of more virulent strains of the virus for longer than necessary.

Pharma leaders in India have been cautiously optimistic in their comments on Trump 2.0, choosing to focus on common goals. Sudarshan Jain, Secretary General, Indian Pharmaceutical Alliance points out that the relationship between India and the US has been growing from strength to strength over the years, Jain suggests that healthcare security and affordability are key priorities for the new Trump Administration. India and the US have an opportunity to collaborate in these areas to advance the healthcare agenda.

Highlighting the common goals, Jain says, “Together, India and the US recognise the importance of building a resilient and diversified pharma supply chain. India has already implemented the Production Linked Incentive Scheme for active pharmaceutical ingredients, and early results are promising. A synergistic effort from both countries can accelerate this initiative, strengthening self-reliance and enhancing healthcare security. As a supplier of quality-assured medicines, India plays a vital role in meeting the needs of the US and the global market.”

After three decades of tracking the pharma sector through Express Pharma and 24 years of spotlighting the healthcare sector through Express Healthcare, we add a new publication to our repertoire: Express Nutra.

To be launched at the upcoming VitaFoods 2025 this February and HADSA Annual conference in March, Express Nutra will partner with multiple stakeholders, and surf the sangam of science, shifting demographics, consumer-driven health trends, and a lot more. As always, we remain open to readers’ suggestions on stories, trends, etc. we should be covering in all three of our publications and websites.

Our vision is to make cutting-edge therapies accessible to Indian patients

Amit Mookim, CEO,Immuneel Therapeutics,discusses the launch of Qartemi,India’s first CAR T-cell therapy,and the company’s vision to make advanced cell and gene therapies accessible and affordable for Indian patients.He also shares insights on Immuneel’s growth strategies,partnerships,and plans to position India as a global hub for innovative cancer treatments,in an interview with Lakshmipriya

Immuneel recently launched Qartemi in India. How does its launch align with Immuneel’s broader vision for cell and gene therapies?

The launch of Qartemi, our CAR T-cell therapy for NonHodgkin’s Lymphoma, marks a pivotal moment in our journey to provide access to advanced cell and gene therapies in India.

Our vision is to make cuttingedge therapies accessible to Indian patients without compromising on global quality and standards. Qartemi is a testament to this vision, it’s not just a product, but a paradigm shift in how we approach cancer care. By bringing Qartemi to the Indian market, we’re not only providing renewed hope to patients but also paving the way for India to become a hub for affordable, innovative therapies in the global cell and gene therapy landscape.

What are Immuneel Therapeutics' immediate and long-term growth strategies to expand its portfolio and reach within India and globally?

Our immediate focus is on scaling access to Qartemi by establishing robust partnerships with leading hospitals and healthcare providers across India. We are also focusing on creating awareness, training physicians and the various stakeholders at the hospital/ infusion site, educating patients and caregivers about CAR T-cell therapy.

In the long term, we aim to expand our therapeutic portfolio by advancing our

Nair

Our immediate focus is on scaling access to Qartemi by establishing robust partnerships with leading hospitals and healthcare providers across India.In the long term,we aim to expand our therapeutic portfolio by advancing our research pipeline into other blood cancers

research pipeline into other blood cancers. Globally, we plan to explore partnerships with academic institutions, and healthcare systems to enhance our capabilities and expand

our footprint. Ultimately, our growth strategy revolves around innovation, accessibility, and sustainability.

Making advanced therapies

affordable is a significant challenge. So, how do you plan to make Qartemi more accessible and affordable?

Affordability is core to our mission, and we’ve taken a

multi-pronged approach to address it. First, we’ve developed a localised manufacturing model to significantly reduce costs while maintaining global quality standards. Second, we are actively pursuing collaborations with government bodies, insurance providers, and philanthropic organisations to ease the financial burden on patients. Additionally, our partnershipdriven PPP model aims to expand infrastructure and provide treatment to underserved regions, ensuring no patient is left behind due to cost constraints.

Are there any additional research or trials being planned to expand the application of Qartemi beyond Non-Hodgkin’s Lymphoma?

Yes, we are committed to broadening the scope of Qartemi’s application. The extension of IMAGINE clinical study for B-ALL patients will be commencing shortly. Preclinical studies and collaborations with global research networks are key steps in this direction.

Furthermore, we’re closely monitoring advancements in CAR T-cell technology to enhance its safety and efficacy.

What other therapeutic areas or diseases is Immuneel targeting in its pipeline?

Beyond Non-Hodgkin’s Lymphoma, our pipeline is focused on tackling other cancers and genetic disorders. Our R&D efforts are designed

to harness the full potential of immunotherapy.

What do you see as Immuneel’s most significant contribution to transforming cancer care in India, and how do you measure your impact?

Immuneel’s most significant contribution lies in its ability to bridge the gap between global innovation and local accessibility. We’ve made cutting-edge therapies available to Indian patients at a fraction of their international cost while maintaining uncompromised quality. Our impact is measured not only in clinical outcomes like improved response rates and survival but also in the hope we restore to patients and their families. Additionally, by creating a scalable and sustainable model, we are inspiring the broader healthcare ecosystem in India to prioritise innovation and accessibility.

Immuneel has partnered with hospitals like Narayana Health, Apollo Hospitals, and CMC Vellore. How will these collaborations enhance the delivery of CAR T-cell therapy?

These partnerships form the backbone of our delivery model. By working with institutions like Narayana Health, Apollo Hospitals, and CMC Vellore, we’ve been able to create centers of excellence for CAR T-cell therapy across India. These hospitals bring world-class infrastructure, medical expertise, and regional reach, ensuring that patients receive the highest standard of care.

Together, we’re building a comprehensive ecosystem, from patient identification and education to treatment delivery and post-therapy care, that makes advanced therapies more accessible and effective.

What is Immuneel’s longterm vision for India’s healthcare ecosystem?

Our long-term vision is to make India a global leader in advanced cell and gene therapies by creating an ecosystem that fosters

innovation, accessibility, and sustainability. We envision a future where no patient is denied treatment due to cost, geography, or awareness. By

building local capacity, advancing R&D, and fostering public-private partnerships, we aim to catalyse a healthcare transformation that prioritises

equitable access to lifesaving therapies. Ultimately, we want to redefine India’s position in the global healthcare landscape, not just as a

recipient of innovation, but as a pioneer driving change.

The group’s offerings range from over a billion injection doses annuallyto bespoke medical machinery

Rishad Dadachanji, MD,Dadachanji Group speaks on the company’s evolution from a pharma packaging company to a diversified solutions provider in biotechnology,automation, and sterile processing.He highlights strategic collaborations,sustainability initiatives,and the group’s vision for driving innovation in life sciences,in an interview with Express Pharma

How has the Dadachanji Group evolved from its inception in 1990 to its current diversified portfolio? How does the group ensure synergy between its diverse business verticals?

The Dadachanji Group has evolved significantly since its inception in 1990. Starting as Kaisha Manufacturers, which focused on pharma containers, the group gained prominence through innovation and a joint venture in 2008, becoming India’s largest producer of ampoules, vials, syringes, and cartridges under Schott Kaisha.

Following the divestment of this venture in 2021, the group diversified into multiple sectors, including biotechnology, medical devices, automation, robotics, and sterile processing, leveraging over 30 years of expertise to establish a broad and dynamic portfolio.

The synergy between the group’s diverse business verticals is achieved through its unwavering commitment to innovation, quality, and customer-centricity. By emphasising cutting-edge technology and understanding market needs, the group creates solutions that align with global standards while addressing local challenges. A unified approach, driven by its leadership, ensures that the expertise and innovation from one sector inform and

strengthen the others, creating an ecosystem of complementary capabilities and fostering growth across its varied ventures. With over 30 years of

expertise, the Dadachanji Group has established itself as a premium manufacturer of pharma products. Driven by innovation and cutting-edge technology, the group’s

offerings range from over a billion injection doses annually to bespoke medical machinery, emphasising both quality and scale.

In 2013, I joined as MD, leading the group into new territories and expanding its global footprint. The group now delivers products to over 50 countries and manufactures and distributes more than one billion injection doses annually.

The company prioritises evolving with customer needs. Understanding our clients’ requirements and consistently exceeding their expectations has always formed the foundation of our operations. By continually expanding its portfolio, the Dadachanji Group remains committed to delivering cutting-edge technology and exceptional solutions, ensuring leadership in an ever-evolving industry.

What role does collaboration—whether with industry partners, academia, or technology providers—play in your strategic vision? Are there any major partnerships in the offing?

Collaboration is a cornerstone of our strategic vision at the Dadachanji Group. Partnering with industry leaders, academic institutions, and technology providers allows us to stay ahead of the curve by fostering innovation, enhancing our capabilities, and effectively addressing

emerging market needs. These alliances not only accelerate our growth but also enable us to bring cuttingedge, affordable solutions to our customers globally. Currently, we are exploring partnerships in advanced biotechnology, automation, and sustainable manufacturing practices to further diversify our portfolio and strengthen our position in key sectors. Our focus is on synergistic collaborations that align with our mission to deliver high-quality, innovative products while driving long-term value for all stakeholders. There could be multiple ways of collaboration, including:

◆ Cross-industry synergies: Partnering with pharma companies for biotech research can lead to breakthroughs in drug development, while expertise in automation and robotics can enhance manufacturing efficiency and quality control.

◆ Academic and research partnerships: Collaborating with academic institutions and research centers can drive R&D efforts in biotech and pharma, fostering advancements in drug discovery, bioprocessing, and diagnostics. Academic collaborations also facilitate access to cutting-edge technologies and talent.

◆ Supply chain and packaging innovations: Working with packaging technology providers and

INTERVIEW

material science experts can enhance primary and secondary packaging solutions, ensuring compliance, safety, sustainability, and innovation tailored to the needs of pharma and medical devices.

◆ Technology providers and automation experts: Collaborating with robotics and AI firms can improve sterile processing, production efficiency, and quality checks while streamlining operations, optimising resources, and enabling predictive maintenance.

Additionally, joint initiatives with environmental technology companies can make manufacturing processes more sustainable, reducing waste and energy consumption.

Can you outline the strategic

vision of the Dadachanji Group of Companies in the life sciences sector?

In the life sciences sector, our decision to invest in and upgrade Sovereign Pharma was both strategic and swift.

Recognising a pressing need to enhance our capabilities, we enlisted an experienced external consultant from Europe to thoroughly evaluate our existing facility and identify critical gaps. Based on these insights, we committed to a comprehensive overhaul and modernisation of the site. This initiative positions us as one of the pioneers in the market, operating a state-ofthe-art facility dedicated exclusively to contract manufacturing. This specialisation gives us a distinct competitive advantage, allowing us to deliver superior value to our

clients.

Our overarching vision is clear: to achieve rapid growth, adhere to the highest compliance standards, and consistently offer innovative products that set a new benchmark in the industry. Supported by our integrated businesses, we have established a robust network that excels in innovation, customisation, product development, and high-quality dossier preparation. This ecosystem enables us to bring exceptional solutions to the market, addressing unmet needs while maintaining an unwavering commitment to excellence and compliance.

Sustainability has become a crucial focus in the industry—what significance does it hold for the Dadachanji Group, and what

initiatives have you implemented in this area?

At the core of the Dadachanji Group’s vision and operations lies a strong commitment to sustainability. As a pharma and biotech company, we acknowledge our responsibility to foster a healthier planet while providing life-saving solutions. Our dedication to sustainability permeates every aspect of our business, from product development to manufacturing and distribution.

We have launched various initiatives aimed at reducing our environmental impact. Our facilities are designed to enhance energy efficiency, minimise waste, and adopt renewable energy sources wherever feasible. In terms of packaging, we work closely with material science experts

to create eco-friendly, recyclable solutions that prioritise both safety and environmental stewardship. In our production processes, we adhere to green chemistry principles, actively seek to reduce water consumption, and emphasise sustainable sourcing of raw materials. Additionally, we are investing in strategies to lower our carbon footprint, including the transition to cleaner energy alternatives and the adoption of sustainable logistics practices.

For us, sustainability transcends being just a goal— it represents a continuous journey. By integrating environmentally responsible practices into our operations, we aspire to set industry benchmarks and inspire others to collaborate in building a sustainable future.

Consolidation has emerged as a major trend as the pharma industry seeks new avenues of growth and looks to expand its existing capabilities.Alook at the factors spurring M&A activity in the sector

By Kavita Jani

Navigating the complex terrain of the pharma industry demands constant adaptation and strategic manoeuvring. As the pharma market continues to grow and branch out, major players aim to expand and diversify to remain at the top of the game. Companies are eagerly engaging in strategic deal-making, probably more than ever before. The Indian pharma landscape has also witnessed significant expansion, punctuated by noteworthy acquisitions.

Global M&Alandscape of 2024

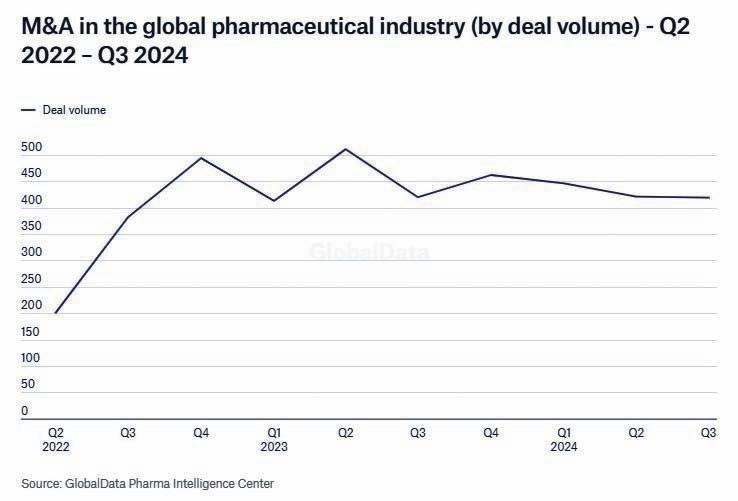

According to Aurojyoti Bose, Lead Analyst, GlobalData, the pharma industry's strategic alliances and M&A deal landscape presented a contrasting trend during 2024. There was an increase in the number of M&A deals announced in 2024 compared to the previous year but strategic alliances’ volume fell. While M&A deals volume registered a year-on-year growth of 17.7 per cent during 2024, announcement of strategic alliances fell by 17.2 per cent.

Globally, several pharma giants made alliances for the expansion and diversification of product portfolios, focusing on improving supply chains and strengthening manufacturing capacity acting as key rationales driving M&A strategies. Bose highlighted, “Many companies were seen going into a buying frenzy and we saw them announcing a spate of M&As during the year. Some notable companies that went for multiple M&A announcements during the year included Novartis AG, Novo Nordisk AS, Merck & Co, Sanofi, GSK plc, Johnson & Johnson and AstraZeneca Plc, among others.”

Bose stated that all the top three markets by M&A deal volume, the US, China and India registered growth in 2024. “Historically, the US has been the hotbed for M&A activity and the trend remains unchanged in 2024 as well. It continues to outpace its peers by a significant margin by

accounting for around 40 per cent of the total number of M&A deals announced globally during the last three years,” says Bose.

The US saw 2.4 per cent growth in M&A deal volume in 2024 compared to the previous year. The next two top markets by M&A deal volume, China and India also contributed to the overall growth. The number

The next two top markets by M&Adeal volume,China and India also contributed to the overall growth.The number of M&Adeals announced in China increased by 15.1 per cent in 2024 compared to 2024 while M&A deal volume for India was up by 42.5 per cent

Aurojyoti Bose Lead Analyst, GlobalData

Most large Indian pharma companies enjoy a healthy balance sheet,providing the ammunition to fund inorganic growth.Outside of India,some of the larger Indian diversified generics majors are eager to scale up their specialty businesses,especially in the US, through acquisitions and/or in-licensing

Subhakanta

Bal MD, Rothschild & Co

BSVacquisition is in line with our stated acquisition cases of high entry barrier business with long-run rate win for growth,specialty,R&D tech platform, solidifying our position offering in space like complementary drug portfolio with high potential OTXbrands

Rajeev

Juneja MD, Mankind Pharma

of M&A deals announced in China increased by 15.1 per cent in 2024 compared to 2024 while M&A deal volume for India was up by 42.5 per cent.

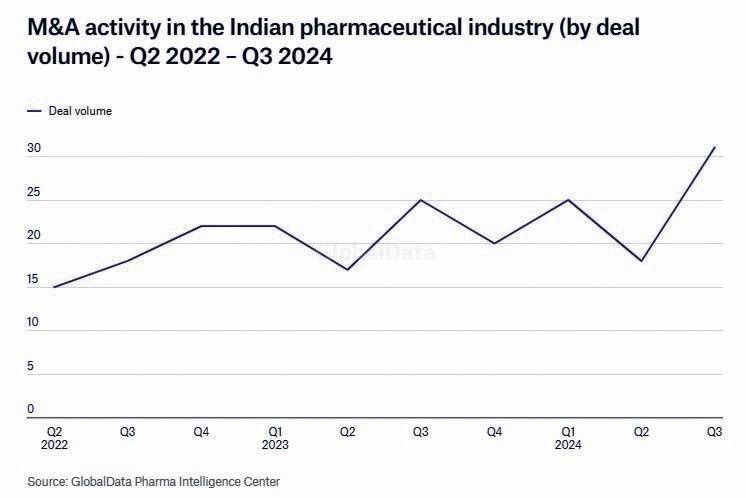

The India story

The Indian pharma industry had a robust 2024 in terms of M&A deals activity. According to GlobalData, the industry witnessed 31 M&A deals in

Q3 valued at $2.3 billion. The $1.6 billion BSV acquisition by Mankind Pharma was the biggest disclosed deal for the industry in 2024.

The report also states that M&A activity in India increased by 404 per cent in Q3 2024 compared to the previous quarter’s total of $456.2 million and rose by 53 per cent compared to Q3 2023 in terms of value. In terms

of volume, there was a sizeable increase of 72 per cent in Q3 2024 versus the previous quarter and was 24 per cent higher than in Q3 2023 (1).

Opportunities and key growth areas

A recent report by EY Parthenon – OPPI titled, “Viksit Bharat@2047: Transforming India from pharmacy of the world to pharma powerhouse for the world” highlighted the need for a unified vision for innovation, with a focus on building a collaborative ecosystem to define clear milestones and goals (2)

The industry gears up for a future driven by an increasing need to progress its biopharma capabilities, expand portfolios, and innovate new drugs and therapies, all while the demand for generics continues to grow.

Therefore, strategic imperatives like portfolio expansion, manufacturing prowess, and supply chain optimisation have made consolidation through M&As a burgeoning trend in the industry. It is now becoming a more ubiquitous method to amplify businesses, tap into nice markets, innovate and expand.

So, let’s examine the drivers of M&As in detail.

1. Looming patent expiries

Patent expirations have been a significant opportunity for the Indian pharma space that is dominated by generics and biosimilars manufacturing. 37 per cent of respondents in an EY-OPPI report view competition from generic drugs and biosimilars as a top trend, while 30 per cent cite the patent cliff as a significant concern (2). EY analysis of EvaluatePharma data indicates that the biopharma industry is facing a substantial loss of exclusivity, with more than $300 billion in sales at risk through 2030 due to expiring patents on high-revenue products. This looming patent expiration is likely to drive interest in mergers and acquisitions, with 77 per cent of

surveyed executives expecting M&A to increase in 2025.

2. Expanding portfolios

In order to grow their potential and expand market reach, pharma firms must diversify their product portfolios. While another EY analysis (2) indicates that smaller biotech firms were responsible for 55 per cent of all new NME approvals by the USFDA from 2015 to 2019. 37 large biopharma companies obtained the remaining 45 per cent. While 60 per cent of these NMEs were sourced externally through collaborations, acquisitions, deals/in-licensing, investments, or partnerships with smaller biotechs and academia.

So, major players in the generics and biosimilars space are likely to benefit by consoli-

dating if they find the right portfolio to enter niche markets and fill gaps within their existing portfolios.

Emphasising the high-potential areas of driving M&As in the pharma B2B space, industry Subhakanta Bal, MD, Rothschild & Co. explains that there has been strong M&A activity driven both by PE funds and corporates. “The industry continues to be fragmented, providing the opportunity for consolidation. PE activity has been led by funds doing platform investments and subsequent bolt-on acquisitions to acquire capabilities and scale up. Trade activity has been primarily driven by a desire to expand in high-growth segments such as high-potency APIs, oncology, peptides and injectables,” he says.

He adds that several strategic transactions have been in the form of brand/portfolio acquisitions to fill specific portfolio gaps or plug whitespaces within a certain therapy. In certain therapeutic areas, organic growth has been lower than expectations, making acquisitions a preferred alternative. The ability to eke out cost synergies through procurement efficiencies and SG&A cost optimisation are additional benefits,” he says.

3. Build integrated capabilities

Pharma companies are trying to build end-to-end capabilities to capture a larger share of the pharma value chain and enhance operational efficiencies.

Bal observes that there seems to be rising demand from customers for integrated service offerings, which would further drive companies to fill gaps in service offerings through acquisitions. “Given the supply chain disruptions faced during COVID-19, there is a greater awareness of the need to diversify the supply chain and avoid overreliance on one country. Outside of China, India and Italy are two of the major API manufacturing hubs, which is expected to further fuel the demand for APIs from India. This could also drive inbound activity with overseas companies looking to acquire assets, especially those with strong development capabilities, regulatory track record, and presence in high growth/complex segments,” explains Bal.

Thus, companies are directing substantial investments to acquire entities which will enhance their R&D and manufacturing capabilities beyond generics or small molecules.

4. Entering new markets

Acquiring companies in new markets allows Indian firms access to established distribution networks, local expertise, and regulatory knowledge in specific regions, thus overcoming entry barriers. This, in turn, has also resulted in a spate of M&As.

Bal conveys that many large domestic companies have been eager to enhance their presence beyond the Indian market. He adds, “Most large Indian pharma companies enjoy a healthy balance sheet, providing the ammunition to fund inorganic growth. Outside of India, some of the larger Indian diversified generics majors are eager to scale up their specialty businesses, especially in the US, through acquisitions and/or inlicensing. This trend is likely to continue as these companies continue to build a portfolio of branded specialty products and biosimilars.”

5. Technology-driven M&As

Technology-driven M&As are on the rise as companies look to strategically acquire targets with cutting-edge technologies to accelerate innovation, enhance drug development, and gain a competitive edge.

According to a report titled “Current Pharma M&A Trends” by Deloitte, a driving goal of pharma M&As is to embrace innovative and disruptive technologies to get ahead of the competition, instead of reinventing the wheel (4). This trend is fueled by the need to access advanced capabilities in areas like biologics, biosimilars, and digital health solutions. Companies specialising in novel drug delivery systems or AIdriven drug discovery pose as an attractive target for acquisi-

tions.

These deals not only provide access to intellectual property and talent but also enable companies to expand their portfolios and enter new therapeutic areas. The evolving regulatory landscape and increasing competition further drive this trend, as companies seek to leverage technology to improve efficiency and reduce costs.

A deal that exemplifies and reflects most of the industry dynamics mentioned earlier is Mankind Pharma’s acquisition of Bharat Serums and Vaccines in 2024. This deal was driven by Mankind’s aim to diversify its product portfolio and gain BSV’s biologics capabilities.

Deal overview

Mankind acquired a 100 per cent stake in BSV from PE investor Advent International, for an enterprise value of approximately Rs 13,630 crores. BSV’s leadership in biologics, immunoglobulins, and recombinant technology made it an ideal acquisition target for Mankind in order to strengthen its position in the specialty pharmaceuticals segment (5)

As per Makind’s BSV call transcripts, Rajeev Juneja, MD, Mankind Pharma states, “BSV acquisition is in line with our stated acquisition cases of high entry barrier business with long-run rate win for growth, specialty, R&D tech platform, solidifying our position offering in space like complementary

drug portfolio with high potential OTX brands, EBITDA margin accretive to Mankind’s margin, and unlock synergy by leveraging Mankind’s extensive reach to target rapidly growing highly underpenetrated markets, especially in fertility as well.”

BSV’s range of products covering fertility, pregnancy and post-pregnancy was a key focus area. Additionally, beyond product offering, BSV has a developed, robust, Specialty R&D tech platform with capabilities in recombinant, niche biologics, novel delivery and immunological immunoglobulins. Financially, the performance of BSV was another key factor for Mankind. With an adjusted EBITDA margin of 28 per cent and a strong growth trajectory in FY24, BSV demonstrated solid financial health.

What does the future behold?

According to Bal, consolidation is expected to continue in the pharma sector because M&As offer numerous strategic advantages in the form of revenue/cost synergies, increased scale, lower time to market (versus organic build-out) and filling specific portfolio gaps/whitespaces. He adds, “The scale and breadth of the portfolio, by itself, seem to have a meaningful influence on the bargaining power with customers/suppliers and other in-

dustry partners. The industry (both on the B2C and B2B side) continues to be highly fragmented, thereby providing the ingredient for continued M&A.”

The PwC 2025 Outlook on Global M&A Trends in the Healthcare Industry also points to the same trend. It states that as the macro and regulatory environment which slowed health industries' dealmaking in recent years begins to improve, dealmakers should be ready to act quickly on innovative assets when they hit the market. Development of interest rates should be watched closely along with policy changes arising from the new US administration. In particular, the anticipated easing of regulations may provide a tailwind to pharma and health industries' dealmaking, not just in the US, but also globally (6). Therefore, industry leaders who are already thinking several steps ahead and can successfully navigate remaining uncertainties will have a significant opportunity in 2025 to use M&A to accelerate their businesses for success.

As an incessant business, pharma firms will need to form deals to stay competitive. Looking ahead, the industry will witness sustained consolidation as companies grapple with competitive pressures, the looming patent cliff, and the relentless pursuit of innovation in a rapidly transform-

ing environment. Companies that proactively build the capabilities to acquire, divest and integrate the right assets have the potential to outperform the rest of the sector.

Express Pharma to host the maiden edition of Pharma Leadership and Innovation Conclave in Mumbai

This event will convene visionaries,decision-makers,and experts to drive insightful discussions, strategic collaborations,and innovative solutions that will define the next decade of India Pharma Inc

India’s pharmaceutical industry stands at a crossroads, poised for its next major leap. As traditional advantages like cost-effective manufacturing and reverse engineering face new global pressures, the sector must evolve. Intensifying global competition, regulatory challenges, stringent intellectual property (IP) frameworks, shrinking profit margins, and sustainability imperatives demand bold, forward-thinking leadership.

Recognising this need, Express Pharma presents the inaugural Pharma Leadership and Innovation Conclave 2024, a platform designed to empower pharma leaders across organisations and functions.

Set to held on February 21, 2025 at the Hilton Mumbai International Airport, this exclusive event will convene vision-

Under the overarching theme “Leadership for the next leap,”this conclave will focus on reshaping India’s pharma industry by fostering a balanced approach between innovation and responsibility, growth and sustainability,and profit and purpose

aries, decision-makers, and experts to drive insightful discussions, strategic collaborations, and inn ovative solutions that will define the next decade of India Pharma Inc.

Leadership for the next leap

Under the overarching theme

“Leadership for the next leap,” this conclave will focus on reshaping India’s pharma industry by fostering a balanced ap-

proach between innovation and responsibility, growth and sustainability, and profit and purpose. The event will serve as a catalyst for transformation, bringing together leaders to craft strategies that enhance India’s global competitiveness and future-proof the industry.

Keydiscussion areas

◆ The patient of the future: Shaping pharma’s next big opportunity

◆ Funding innovation: Unlocking investments in pharma

◆ Rewriting the pharma playbook: Faster, Smarter, Leaner

◆ India Pharma Inc’s next big frontiers: Complex generics, Biologics, APIs, and more

◆ IP and innovation: Strengthening India’s competitive edge

◆ Redefining pharma business models: From pills to platforms

WhyAttend?

◆ Gain insights from top

industry leaders who have transformed challenges into success stories.

◆ Understand how AI, big data, and automation are revolutionising the pharma landscape.

◆ Learn from real-world case studies on compliance, sustainability, and patient-first approaches.

◆ Build strategic partnerships with key decision-makers, innovators, and thought leaders.

As India Pharma Inc gears up for its next phase of leadership, this conclave will serve as the definitive forum to drive impactful discussions, foster collaborations, and set new benchmarks for the industry.

Join us in Mumbai and be part of the movement to unlock the true potential of India’s pharma sector!

Hyderabad to host the seventh edition of PPLConclave 2025

With the theme ‘Powering Innovation,Sustainability,Leadership,’PPLConclave 2025 will serve as a critical platform for thought leadership,knowledge exchange,and strategic networking

Pharma Packaging and Labelling (PPL) Conclave 2025, organised by Express Pharma, is scheduled to take place at Le Meridien on March 7-8, 2025.

The conclave will bring together over 100 industry leaders, innovators, and decision-makers to explore the latest advancements, challenges, and opportunities in the sector.

With the theme ‘Powering Innovation, Sustainability, Leadership,’ PPL Conclave 2025 will serve as a critical platform for thought leadership, knowledge exchange, and strategic networking.

Keythemes and topics

The event will feature keynote addresses, expert panels, and interactive sessions covering a range of pivotal topics:

◆ Smart packaging for the connected age

◆ Packaging for global markets: Navigating diverse regulatory landscapes

◆ Next-gen labelling solutions:

eLabelling and more

◆ Balancing cost and innovation in pharma packaging

◆ Anti-counterfeit packaging: Protecting patients and products

◆ Role of packaging in supply chain security

◆ Patient-centric packaging:

Safe, Smart, Secure

◆ Strategies to speed up serialisation

PPL Conclave 2025 will offer attendees a valuable opportunity to:

◆ Gain firsthand insights from leading experts in pharma, biotech, and packaging industries

◆ Explore innovative packaging solutions from top solution providers

◆ Engage in discussions on regulatory trends, market dynamics, and sustainability in pharma packaging

◆ Network with key stakeholders, fostering collaborations and business partnerships

◆ Demonstrate and discover cutting-edge packaging capabilities and technologies

The conclave will bring together a diverse set of stakeholders, including:

◆ Pharma packaging professionals – from R&D, quality assurance, and supply chain management.

◆ Regulatory and compliance experts – to discuss evolving guidelines and best practices.

◆ Technology providers –showcasing the latest innovations in smart and sustainable packaging.

◆ Industry leaders and decision-makers – sharing strate-

gic perspectives on market growth.

◆ Investors and policy makers – exploring new opportunities in the pharma packaging ecosystem.

With an impressive lineup of speakers, interactive discussions, and state-ofthe-art solutions on display, the conclave is poised to set new benchmarks in innovation, sustainability, and leadership within the industry.

Stay tuned for updates as we count down to PPL Conclave 2025 – the platform for the future of pharma packaging and labelling.

MARKET

Evolution and commercialisation of cell and gene therapies

Satyen Sanghavi, Founder & CSO,Regrow Biosciences traces the evolution of cell and gene therapies,highlighting global milestones,industry growth,and reimbursement models.

Emphasising the transformative potential of these therapies,he calls for stronger regulatory and financial backing to ensure wider accessibility

The field of cell and gene therapy has experienced remarkable progress since the early 2000s. A pivotal milestone was the USFDA's approval of Carticel by Genzyme in 1997, marking the first cell therapy approved in the U.S. for the treatment of cartilage defects in the knee. This groundbreaking achievement paved the way for the development of autologous cell therapies targeting multiple medical conditions. As of 2024, there are over 68 non-genetically modified cell therapies and 32 gene therapies approved for clinical use worldwide, with the US, EU, and Japan playing key roles in regulatory and commercial approvals. The industry has also seen substantial growth in the number of companies dedicated to cell and gene therapy development, with over 100 companies globally actively contributing to this transformative sector.

Concurrently, 1,221 clinical trials for cell and gene therapies are ongoing worldwide, spanning in various stages, including 342 in Phase 1/1b, 525 in Phase 2/2b, and 254 in Phase 3, highlighting the sector's robust development pipeline.

In India, the shift from clinical trials to commercial-scale production of cell and gene therapies has been led by companies like Regrow Biosciences, Stempeutics, ImmunoACT, Eyestem, and Aurigene Oncology. Regrow Biosciences has successfully launched three commercial autologous cell therapy products, targeting tissue damage in bone, cartilage and the urethra. Meanwhile, Stempeutics, focuses on the development of stem cellbased products, including Stempeucel, a therapy designed to treat critical limb ischemia and

As of 2024,there are over 68 nongenetically modified cell therapies and 32 gene therapies approved for clinical use worldwide,with the US,EU,and Japan playing key roles in regulatory and commercial approvals

osteoarthritis. Similarly, Eyestem is advancing its development of Eyecyte-RPE, a novel cell therapy aimed at treating age-related macular degeneration. Aurigene Oncology is advancing its first-in-class autologous CAR-T therapy, Ribrecabtagene autoleucel (DRL-1801), for the treatment of

multiple myeloma, reflecting the growing momentum within India's clinical-stage cell and gene therapy pipeline.

The commercialisation of cell and gene therapies globally has seen substantial financial impact, with several therapies generating significant revenue. For instance, Yescarta (Gilead

Sciences) is projected to achieve $966 million in US revenue and $321 million in Europe in 2024. Similarly, Carvykti (Ciltacabtagene Autoleucel) reported $286 million in sales in a single quarter, while Elevidys, Sarepta Therapeutics’ gene therapy for Duchenne Muscular Dystrophy, is forecast to achieve over $1 billion in 2024, with peak sales expected to exceed $6 billion by 2027. On the autologous front, Vericel's MACI, an autologous chondrocyte implantation (ACI) for knee cartilage repair, recorded $164.8 million in revenue in 2023, representing a 25 per cent year-on-year growth. Similarly, Epicel, a therapy for patients with severe burns, generated $31.6 million in revenue in the same year, underscoring the rising demand for autologous cellular therapies in regenerative medicine.

Reimbursement models in the US,EU and Japan

Reimbursement models for cell and gene therapies have evolved significantly in recent years to improve patient access and reduce financial strain on healthcare systems. Given the high cost of such therapies, regulatory authorities and health agencies have adopted innovative payment models to balance affordability with industry sustainability.

In the US, the Centers for Medicare & Medicaid Services (CMS) have implemented outcomes-based agreements to reimburse companies for therapies only when they achieve clinical efficacy. This has been adopted for products like Zolgensma (for spinal muscular atrophy) and Luxturna (for inherited retinal disease). Pay-for-performance models

link payments to treatment outcomes, ensuring that reimbursement only occurs when the therapy delivers measurable benefits to the patient. Medicaid Best Price Exclusion is another mechanism that allows states to negotiate reimbursement terms directly with manufacturers for innovative therapies.

In the EU, reimbursement for cell and gene therapies is managed through Managed Entry Agreements (MEAs). This approach enables payers to mitigate the uncertainty around clinical outcomes. Countries like Germany, Italy, and the UK have used MEAs to allow for costsharing between public health systems and manufacturers. NHS England, for example, has implemented the outcomebased reimbursement for Kymriah (CAR-T therapy) and Zynteglo (gene therapy for beta-thalassemia). These agreements ensure that manufacturers share part of the financial risk if the therapy fails to meet its intended clinical targets.

Japan has taken a progressive approach with its SAKIGAKE Designation, a system similar to the US's RMAT (Regenerative Medicine Advanced Therapy) designation. The SAKIGAKE framework provides conditional and time-limited approval for regenerative products with an option for post-marketing data collection. This allows therapies to enter the market faster, with subsequent data collected to support long-term efficacy and safety claims. Notably, the approval of Temcell for graft-versus-host disease (GvHD) and other therapies for rare diseases has been possible under this system. Outcome-based payments are also used in Japan, with hospitals be-

ing reimbursed only if patients demonstrate positive health outcomes.

Indian landscape:

Ayushman Bharat and health insurance

Government support and health policy play an instrumental role in the broader adoption of cell and gene therapies. India's Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY), launched in 2018, aims to provide health coverage of up to Rs 5 lakh per family annually, offering financial protection to economically weaker sections of society. As of March 2023, over 21 crore Ayushman Bharat cards have been issued, facilitating over 6.2 crore hospital admissions worth approximately Rs 79,000 crore. In September 2024, the Union Cabinet expanded the scheme to cover all senior citizens aged 70 and above, regardless of income, potentially benefiting an additional six crore people. Inclusion of cell and gene therapies under this scheme could significantly improve patient access, particularly for low-income populations in need of transformative therapies.

In addition to government initiatives, India's growing middle and upper classes are increasingly turning to private health insurance to access innovative treatments. As of 2023, approximately 51 per cent of India's population had health insurance coverage, with 35 per cent under government schemes (like Ayushman Bharat), 12 per cent through private health insurance, and four per cent through employer-provided insurance. The Insurance Regulatory and Development Authority of India (IRDAI) has been instrumental in driving health insurance coverage, and the average sum insured rose from Rs 5 lakh in 2020 to Rs 7.5 lakh in 2023. If private insurance schemes begin to cover advanced therapies like cell and gene therapy, patients will have broader access to curative therapies that were previously unaffordable. Moreover, this move would incentivise the commercial sector to offer more affordable options, ultimately driving demand for innovative therapies within India's growing health insurance landscape.

CONTRIBUTOR’S CHECKLIST

❒ Express Pharma accepts editorial material for regular columns and from pre-approved contributors / columnists.

❒ Express Pharma has a strict non-tolerance policy of plagiarism and will blacklist all authors found to have used/refered to previously published material in any form,without giving due credit in the industryaccepted format.All authors have to declare that the article/column is an original piece of work and if not, they will bear the onus of taking permission for re-publishing in Express Pharma.

❒ Express Pharma's prime audience is senior management and pharma professionals in the industry.Editorial material addressing this audience would be given preference.

❒ The articles should cover technology and policy trends and business related discussions.

❒ Articles for columns should talk about concepts or trends without being too company or product specific.

❒ Article length for regular columns: Between 12001500 words.These should be accompanied by diagrams,illustrations,tables and photographs, wherever relevant.

❒ We welcome information on new products and services introduced by your organisation for our various sections: Pharma Ally (News,Products,Value

Hopeful future: Transformational therapies redefining lives and society

As we look toward the future, it is clear that cell and gene therapies are not just scientific marvels — they are lifelines of hope for millions of people suffering from chronic, debilitating, and life-threatening diseases. These therapies go beyond symptomatic relief, offering the potential for lasting cures that restore health, dignity, and independence. Patients who were once burdened with the daily struggles of genetic disorders, cancer, and tissue degeneration can now envision a future free from pain, dependence, and the constant uncertainty of disease progression. For the first time, children born with rare genetic mutations have a chance to lead normal lives.

The societal impact of these therapies extends far beyond individual patients. When a father who was once unable to walk can return to work and support his family, or when a child can see the world clearly after receiving gene therapy for vision loss, the benefits are felt by entire families, communities, and

economies. These ripple effects reduce the long-term burden on healthcare systems, minimise hospitalisations, and reduce the need for chronic medical support. Countries that embrace these innovative therapies see a healthier, more productive population that can contribute meaningfully to society and the economy.

However, this journey is not without its challenges. Regulatory hurdles, lack of financial support, and limited insurance coverage have slowed the adoption of transformational therapies. Unlike conventional pharmaceuticals, the development of cell and gene therapies requires sophisticated infrastructure, longer development cycles, and stringent oversight to ensure safety and efficacy. Stronger regulatory support, targeted government incentives, and inclusion in national health programs like Ayushman Bharat can catalyse faster adoption.

As society steps into the future driven by personalised, regenerative medicine, it is essential for stakeholders — from regulators to healthcare providers — to recognise the profound potential of these ther-

Add),Pharma Packaging and Pharma Technology Review sections.Related photographs and brochures must accompany the information.

❒ Besides the regular columns,each issue will have a special focus on a specific topic of relevance to the Indian market.

❒ In e-mail communications,avoid large document attachments (above 1MB) as far as possible.

❒ Articles may be edited for brevity,style,and relevance.

❒ Do specify name,designation,company name, department and e-mail address for feedback,in the article.

❒ We encourage authors to send their photograph. Preferably in colour,postcard size and with a good contrast.

apies. Policymakers must view them not as experimental luxuries but as essential tools to improve population health. By bridging the gap between research, regulation, and access, governments can empower millions of patients to experience life-changing treatment.

Hope is a powerful thing, and cell and gene therapies embody that hope. They remind us that diseases we once feared as "incurable" can now be confronted head-on. With proper support, these therapies can create a future where people no longer live at the mercy of genetic fate, where healthcare becomes preventive rather than reactive, and where patients regain control of their lives.

This is a pivotal moment in the history of medicine. If governments, investors, regulators, and healthcare providers come together, they can create a future where transformational therapies are accessible to all. By doing so, we ensure that "no patient is left behind." These therapies promise to be more than just medical breakthroughs; they are stories of resilience, courage, and a profound belief in the human spirit.

Email your contribution to: The Editor, Express Pharma, Business Publications Division,The Indian Express (P) Ltd, Mafatlal Centre,7th floor,Ramnath Goenka Marg, Nariman Point,Mumbai 400021 viveka.r@expressindia.com viveka.roy3@gmail.com

The unmissable Asia healthcare opportunity

BCG’s latest report,The Unmissable Asia Healthcare Opportunity,highlights the region’s $5 trillion healthcare market potential by 2030,driven by demographic shifts,investment,and innovation.This article includes key excerpts from the report,offering insights into growth drivers,investment opportunities,and the evolving healthcare landscape in Asia

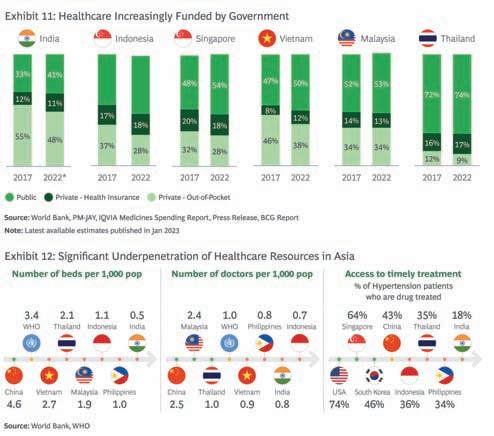

The healthcare (HC) markets across Asia are highly heterogeneous, reflecting wide variations in government spending and HC

infrastructure. For instance, Indonesia spends only 3.7 per cent of its GDP on HC compared to more developed markets like Singapore at 5.5 per cent. An-

other metric that proves this disparity is HC spending per capita, with countries like India spending only $74 per capita, falling significantly behind nations such as Thailand and Malaysia, spending $364 and $487 per capita respectively. (Refer to Exhibit 11)

Some countries lagging in WHO standards as compared to their developed counterparts have massive gaps in capacity and manpower to fill. For example, only 18 per cent of Indonesia’s hypertensive patients receive drug treatment, far below the 74 per cent treatment rate in the United States. Other markets such as the Philippines (34 per cent) and Thailand (35 per cent) also face significant treatment gaps. Countries like India and Indonesia have fewer HC resources, with just 0.8 and 0.7 doctors per 1,000 people, respectively, compared to the WHO recommendation of 2.5. ( Refer to Exhibit 12)

These differences underscore the need for tailored HC service models and investment strategies that consider each country’s unique economic and demographic landscape.

To be able to unlock its superpower status, Asian nations must do away with the social dis-

advantage to marginalised populations caused by lack of access to HC. There is a unique double bottomline opportunity for impact capital to penetrate HC within Asia, across all its delivery channels.

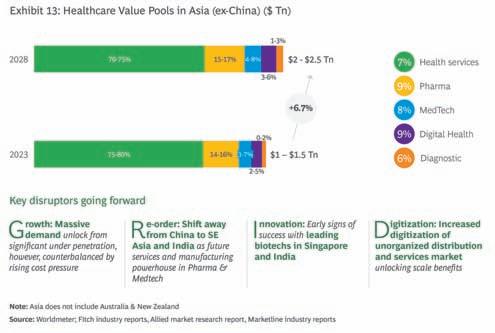

Health services largest value pool followed by pharma

HC services are the largest value pool in Asia, projected to grow

between grow from $1.0-1.5 trillion currently to $2.0-2.5 trillion by 2028.

The pharmaceutical and MedTech sectors are also expected to see significant growth of 7 per cent and 9 per cent, respectively, over the next five years. Digital health (growing at 9 per cent) and diagnostic services (growing at 6 per cent), are also promising investment opportunities. Furthermore, the

MARKET

shift of manufacturing from China to Southeast Asia and India is anticipated to create a new centre of gravity for pharma and MedTech production, providing strategic investment opportunities to be leveraged in these regions. (Refer to Exhibit 13)

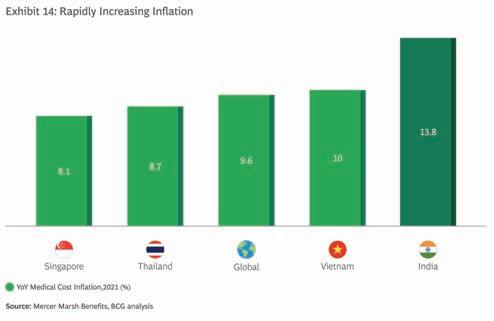

Rising medical inflation, shifting value pools and increased pricing pressure driving shift in business models in healthcare

Rising medical inflation is a key challenge for Asian HC systems, driven by shifting value pools and increasing demand. While government funding for HC is

services. This is possible only with innovation and a shift in approach, from delivering healthcare to health, from focussing on curative to preventive and cost management to outcomes.(Refer to Exhibit 14: Rapidly Increasing Inflation on the first page for a detailed overview)

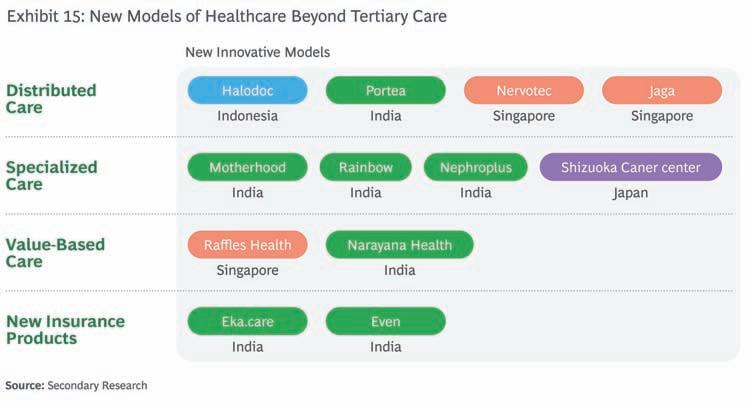

To succeed in this shift in approach, players are adapting and we see emergence of innovative business models such as: ( Refer to Exhibit 15: New Models of Healthcare Beyond Tertiary Care, on the first page for a detailed overview)

◆ Distributed care: The HC delivery is becoming increasingly

rising across countries like India, Vietnam and Thailand (they contribute to 40-50 per cent of HC spending), private HC costs continues to remain high, with a significant portion (38 per cent to 48 per cent) of expenses still covered out-of-pocket.

Public health schemes like PM-JAY in India are expanding now and covering ~ 550 million beneficiaries, but at the same time, private insurance is also growing as middle-class populations demand better and faster access to HC. Providers, on the other hand, are looking to streamline operations, reduce costs, and focus on delivering specialised and value-added

decentralised, with services distributed across various points of care, including primary care clinics, telemedicine platforms, pharmacies, and even homebased care. Notable example is Halodoc, with 4.4 million monthly active users, a leading telemedicine platform in Indonesia, providing distributed HC by offering remote consultations, digital prescriptions, and home delivery of medications, making HC accessible across urban and rural regions.

◆ Specialised care: We see emergence of specialised models of healthcare delivery that have created focused business models at greater efficiency and

lower costs compared to large multi-speciality hospitals. Notable examples from India is Aravind Eye Care which has pioneered a cost-efficient model for eye surgeries and treatments, making eye care accessible to low-income populations. There is also Nephroplus, which operates India’s largest chain of dialysis centers with ~135 centers and a revenue of $65 million in 2024 and, focusing on providing highquality, cost-effective renal care. At roughly $25 per treatment, NephroPlus prices are 30 to 40 percent lower than large hospitals in India.

◆ Value-based care: Value based healthcare is gaining traction as payers and providers look to move away from the traditional fee-for-service model, which promotes volume over outcomes. Raffles Health Group (in Singapore) implements value-based care by continually reviewing and auditing interventions & associated costs to ensure delivery of evidence-based high standard clinical care. This is made possible through the use of state-of-the-art technology, combined with a multi-disciplinary team work and a focus on integrated care.

◆ Flexible insurance products: Insurers are also developing new insurance products that offer greater flexibility, affordability, and coverage for specific HC needs. These products are designed to fit into the distributed and specialised care models discussed above. Notable example is Eka Care (in India) that offers integrated digital health platforms with insurance products tailored to chronic disease management and preventive care.

◆ Emergence of mid-market players: Evolving healthcare models have also led to the emergence of middle-market providers with affordable pricing structures, focusing on the middle income consumers rather than the elite segment. An example in the mid-market segment, offering affordable pricing structures is the Xuyen

A General Hospital chain in Vietnam, a private chain is established in 2012. It now has four hospitals across the country.

Xuyen A was a market pioneer, expanding operations in faraway

Tier 2 markets in Mekong Delta and Central Highlands rather than just focusing on metros and Tier 1 cities like other premium private chains. Xuyen A is reputed for its oncology practice. Its newly launched oncology center of excellence offers a full suite of services, including chemotherapy, radiotherapy, and surgical oncology.

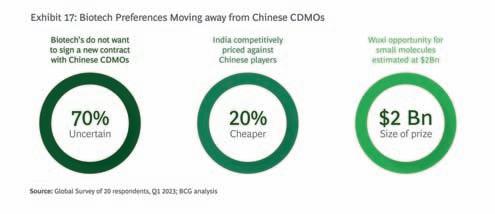

Rapidlygrowing pharma services market driven by China+1

The pharma services (contract research, clinical trials, patient therapy monitoring etc.) market in Asia is still relatively small but growing rapidly, offering an opportunity for countries like India to capitalise on the China+1 strategy.

In a survey conducted by BCG in Q1 2023, 70 per cent of biotechs indicated hesitation to

sign new contracts with Chinese manufacturers. The opportunity becomes more tangible in the wake of the Biosecure Act being passed in the House of Representatives in the US. Indian Contract Development and Manufacturing Organisations (CDMOs) stand to benefit as they are already well-established in the global Active Pharmaceutical Ingredient (API) and generic drug manufacturing space and offer competitive costeffective alternatives to China. Case in point is the 50 per cent YoY growth in RFPs for some Indian CDMOs in 2024.

As pharmaceutical companies look to diversify their investments and manufacturing operations beyond China, Indian players are capitalising on this opportunity. Indian pharma services are priced 20 per cent cheaper than their Chinese

MARKET

counterparts. The CDMO market in India is expected to grow from $7 billion to $14 billion by 2028, capturing 4-5 per cent of the global market. There is also a significant opportunity for other Asian countries like Philippines to step up their participation in pharma services and for Malaysia to emerge as a medical device outsourcing destination.

(Exhibit 16 and Exhibit 17 for a

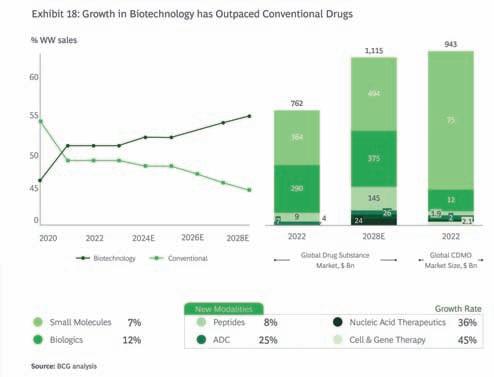

and gene therapy, antibody-drug conjugates (ADCs), and nucleic acid therapeutics are expected to see growth rates as high as 45 per cent, 25 per cent, and 36 per cent, respectively. These modalities are driving the rapid expansion of the biotechnology sector, with the global CDMO market for new modalities projected to reach $20 billion by 2028. As new treatments gain traction,

detailed overview)

The exciting opportunityin newmodalities

The biopharmaceutical sector is experiencing a shift towards new drug modalities, which are

conventional small-molecule drugs will grow at a slower rate, fueling the need for innovation in the pharmaceutical industry.

Asian CDMO players will have the opportunity to emerge

projected to outpace conventional drugs over the next decade. New modalities like cell

as low-cost scalable outsourcing destination with growing expertise in novel modalities. (Refer to

Exhibit 18for a detailed overview)

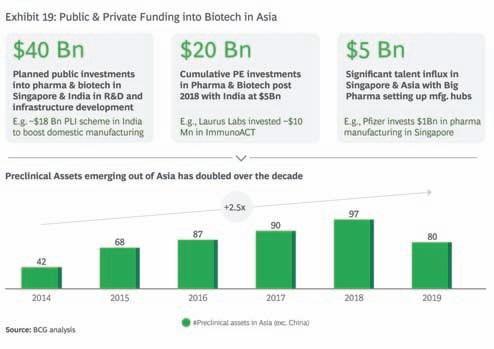

Unleashing biotech: Biopharma innovation in Asia starts showing returns Decades of investment in biotech and biopharma are starting to yield tangible results. Public and private investments are pouring into the sector in countries like India and Singapore. In particular, India’s $18 billion Production Linked Incentive (PLI) scheme is aimed at boosting domestic manufacturing.

Cumulative PE investments in India’s pharma and biotech sectors have reached $5 billion since 2018. These investments are leading to an increase in preclinical assets, with the number of assets in Asia (excluding China) more than doubling in the past decade.

Several Indian CDMOs are building capabilities in new modalities inorganically. Examples include Suven Pharma and Piramal Pharma. Suven recently announced a merger with Cohance Lifesciences to gain capability in Antibody Drug Conjugates (ADCs). It has also entered the oligonucleotides and nucleic acid therapeutics space with the acquisition of Sapala Lifesciences. Piramal Pharma’s series of acquisitions to bolster its ADC and High Potency API offerings through the acquisition of Ash Stevens in USA and Hemmo Pharma in India are also significant.

There are early signals of Asian biotechs and startups offering new therapies. ImmunoACT is an innovative biotech company from India, specialising in CAR-T cell therapies for cancer treatment. Their lead product, NexCAR19, is India’s first indigenous CAR-T therapy. This therapy is available at a fraction of the cost— $50,000 in India versus $500,000 internationally, making cutting-edge treatment far more accessible. ImmunoACT has already treated over 100 patients, and startups are entering key out-licensing deals, including a $430 million deal for further development.

Similarly, Hummingbird Bioscience, based out of Singapore, combines advanced computational biology and systems biology to identify novel, previously ‘undruggable’ cancer targets,

and develop treatments for hard-to-target cancer epitopes. Hummingbird has also secured a $430 million out-licensing deal with Endeavor Biomedicines, further validating its approach. (Refer to Exhibit 19 for a detailed overview)

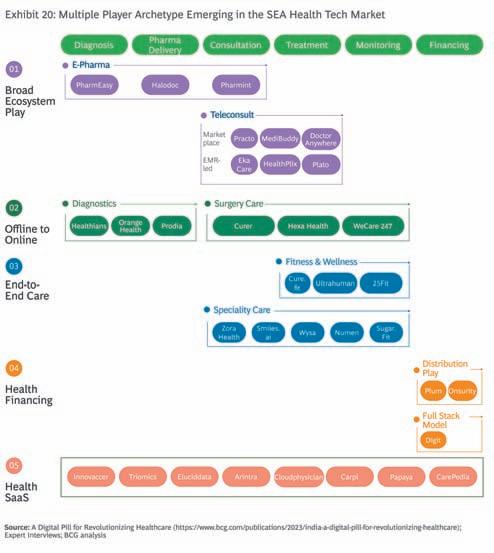

Health tech: Exciting market,though with longer trajectory

The Indian and South-East Asian health tech market is evolving rapidly, with multiple archetypes of players emerging.

across the region.

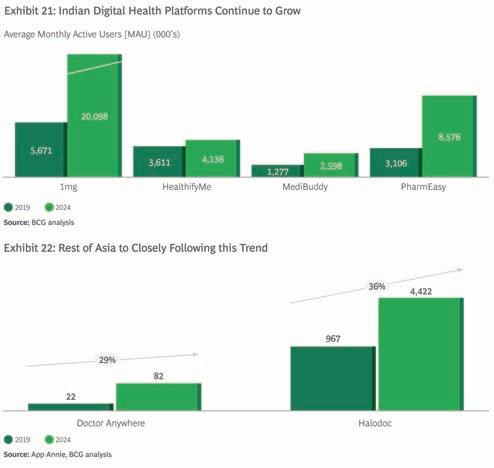

Digital health adoption, which promotes self-monitoring and management of health is accelerating, with platforms like 1mg, HealthifyMe, and PharmEasy in India, seeing their monthly active users (MAUs) rise significantly. These platforms continue to experience substantial growth, with India leading the region in digital health adoption. For example, MediBuddy has seen its MAUs grow from two million in 2019 to 8.5 million in 2024. As the digital

These range from digital HC platforms like PharmEasy and Halodoc to companies offering specialised care services via apps such as Healofy and Sugar.Fit.

We see different archetypes of players emerging, across the health tech ecosystem, including end-to-end care providers, specialty care providers, and health financing platforms. This diversity reflects the broader trend of digital transformation in HC, where technology is used to deliver myriad, non-traditional services more efficiently and reach underserved populations

health ecosystem in India matures, other Asian markets, including Indonesia and Vietnam, are expected to follow closely, driving the digital transformation of HC delivery across the region. (Refer to Exhibit 20, Exhibit 21, Exhibit 22)

An investment lens into Asia healthcare opportunity

Preliminary investments have already flown into the HC spectrum; but this is just a drop in the ocean. Given that yielding strong financial returns in the

MARKET

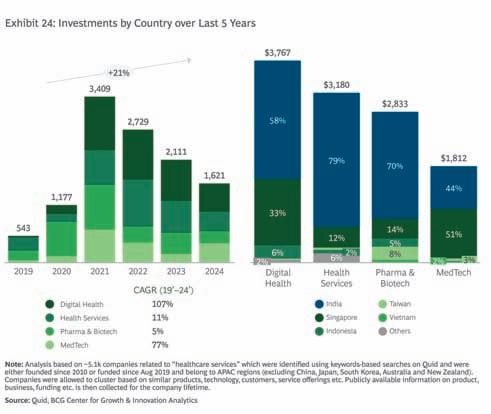

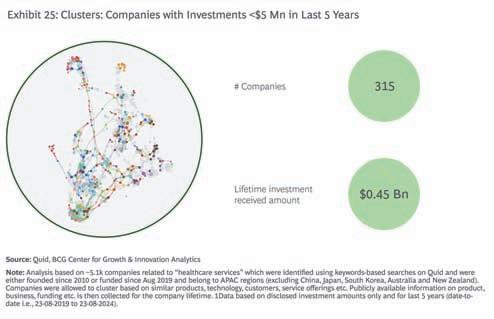

health sector and simultaneously driving social impact would go hand in hand, the path to achieving true health security in Asia would mean evaluating the impact of the ‘early dollars’ and what we can learn from the ROI generated so far. We leverage Quid (a tool that uses Natural Language Processing (NLP) to cluster HC investments in different areas) to analyse where investment dollars have gone in last five years. Since 2010, over $29.5 billion has been invested in approximately 5,100 companies in the region. ( Refer to Exhibit 23 for a detailed overview)

Big ticket investments have flown towards digital health,pharma,and health services as expected The overall trends are positive. There has been a steady increase in investment flows, with a 21 per cent compound annual growth rate (CAGR) from 2019 to 2024. Investment peaked in 2021 at $3.4 billion, following a significant surge compared to earlier years. This spike reflects the impetus to HC innovation, largely driven by the COVID-19 pandemic, which accelerated demand for digital health solutions, remote care platforms, and innovations in HC infrastructure. We see four major sectors for investment: Health Services, Pharma and Biotech, Digital Health and MedTech. Of the total investment, $9.5 billion has gone into pharma and biotech, while health services have received $12.1 billion in funding. Notably, digital health has seen strong growth in recent years, receiving $4.6 billion in investments, with $3.8 billion of that amount occurring in just the last five years. Singapore and India are leading the region in attracting HC investments, further cementing their roles as hubs for HC innovation.

Health Services exhibit a steady 11 per cent CAGR, representing ongoing investment in hospital chains, diagnostic services, and primary care facilities, driven by the increasing demand for accessible, quality HC for Asia’s growing middle-class population.

Digital Health shows the highest growth rate with a staggering 107 per cent CAGR, high-

lighting the rapid digitisation of HC services. This includes telemedicine, online pharmacies,

digital diagnostics, and health monitoring apps, which have seen explosive growth due to in-

creasing internet penetration, smartphone adoption, and demand for remote HC. ( Refer to Exhibit 24 for a detailed overview)

Small ticket investments: digital,AI and telehealth emerge as winners

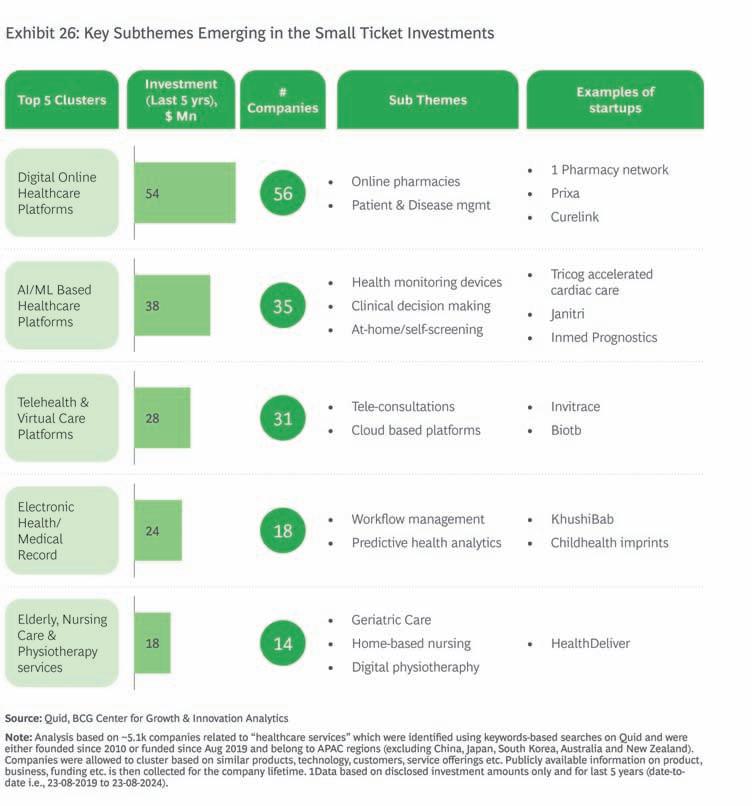

A deep dive into the small-ticket investments (less than $5 million) reveals sub-themes that are driving innovation across digital health platforms, patient monitoring devices, and homebased nursing care services. For instance, 56 companies have emerged in the online pharmacy and disease management space, with many focused on providing affordable, accessible HC solutions. These companies have the potential to create scalable HC models that can address the unique needs of populations in underserved markets. ( Refer to Exhibit 25 and Exhibit 26 for a detailed overview)

Conclusion

The unique interplay of megaforces will grow Asian HC exponentially.

To reiterate, we are in the middle of rapidly shifting mega forces that are interacting with each other to create disruption. The convergence of demographic shifts, technological adoption, and shifting consumer behavior, makes the HC sector in Asia ripe for investment.

For consumers, it is their preference for on-demand localised services, that is driving a digital shift. This is also driving the mainstreaming of telemedicine, remote diagnostics and enhanced engagement. The ‘pandemic-accentuated’ need to de-risk the supply chain, be selfsufficient with respect to essential medical products and services, is also a very powerful force arising from the demand side. For providers, Asian HC is an unparalleled hotbed for the innovative use of capital. New models of distributed care, specialised care, and value-based HC are already emerging and will consolidate.

A few broad trends are visible; within health services, midmarket single-specialty players such as ophthalmology or IVF centers–catering to niche highdemand treatments and elderly care services–will drive future growth. Similarly, the rise of digital health platforms—from e-pharmacies to employee wellness programs—presents a strong investment case as patients increasingly seek more convenient, tech-enabled HC options.

Lastly, the biotech and pharma sector offers long-term value, especially in emerging areas such as AI-based drug discovery and CRDMO services for new therapeutic modalities. The shift away from China, highlighted by trends like the “China+1” strategy, opens doors for other Asian countries like India to capture a larger share of global pharma manufacturing, expanding beyond generics. Advancements in stem cell research and AI-based drug development are creating new frontiers in personalised medicine, aligning with the broader trend toward precision HC.

This ‘Asia Healthcare Opportunity’ is the most lucrative bandwagon to have come along in a while.

STRATEGY

Pharma’s strategic path to growth in the nutra maze

The nutraceutical market is a thriving ecosystem of opportunities.For pharma companies,it’s a space where the allure of a $11.55 billion pie by 2030 is tempered by a maze of regulatory grey zones,stiff competition,and trust-eroding marketing practices.Still,with research expertise and consumer trust,they can thrive—if they play their cards right

The nutraceutical market is expanding rapidly, valued at $6.11 billion in 2024 and projected to reach $11.55 billion by 2030, according to a GlobeNewsWire report. However, pharma companies eager to tap into this growth, face a complex road ahead. Regulatory ambiguity, for instance, serves as a double-edged sword. On the one hand, relatively less regulatory control eases market entry; on the other, they expose pharma players to intense competition from both established FMCG brands and agile startups, quick to respond to shifting consumer preferences.

Adding to these challenges, unethical marketing practices continue to undermine consumer trust with misleading claims about product efficacy and outcomes. Despite these obstacles, opportunities remain significant, particularly given pharma companies' strong foundation in clinical research and established consumer trust. The question remains—how can they navigate these challenges and build strategies that foster long-term credibility and growth in the nutra sector?

Industrytug-of-war

Recent developments in India’s nutra sector have been nothing short of a rollercoaster ride from the pharma industry’s perspective. On one hand, the Indian government has taken proactive steps to explore bringing nutra products under the purview of the Central Drugs Standard Control Organisation (CDSCO) by setting up a government-constituted panel in February 2024. This move has been largely welcomed by pharma players as a step towards stricter oversight and standardised practices.

On the other hand, the recent revisions to Schedule M—which ban the production of nutra

Ethical marketing focuses on education rather than exaggeration, empowering consumers with accurate information about product benefits.By staying true to their reputation for reliability and putting consumer well-being first,pharma companies can build lasting credibility in the nutra space

Nandini Piramal Chairperson,Piramal Pharma

The strategy should focus on two aspects: understanding market dynamics and innovating according to consumer needs,while executing these competencies through the core principles of the 4Ps of marketing— Product,Price,Place,and Promotion

Kalka Prasad

AVP– Marketing, Crius Life, Crius Group

With increased awareness among consumers about health benefits, pharma industry involvement in nutra will help redefine rules and regulations

Antony Prashant Partner, Deloitte India

products in drug-licensed facilities to prevent cross-contamination—have ignited a heated debate. While these changes aim to enhance product safety and delineate clear boundaries between pharma and nutra manufacturing. However, they impose significant operational hurdles for pharma companies that also produce nutraceuticals. Meanwhile, standalone nutra manufacturers see this as an opportunity to compete on more equal footing.

Adding to the uncertainty, the Karnataka High Court’s temporary stay on the revised Schedule M has provided manufacturers with a momentary reprieve, leaving the sector in a state of limbo.

For pharma players, the situation underscores not only the need for balanced regulations that safeguard public health while fostering the coexistence of both industries but also serves as a clear call to action. It’s a pivotal moment for pharma companies to strategically assess their position, adapt to evolving dynamics, and carve a sustainable path in the rapidly growing nutra sector.

Guideline gaps

One of the major challenges in the current regulatory landscape is the ambiguity surrounding guidelines and the prevalence of low-quality benchmarks in the nutra sector.

Antony Prashant, Partner, Deloitte India, explains, "The nutra market currently lacks the regulations found in the pharma industry. This significantly impacts product quality and safety, with potential for adulteration. Nutra products may interact with medications, increasing the need for regulation and consultation by healthcare professionals. The Ministry of Health and Family Welfare is planning to

STRATEGY

bring these products under the supervision of the Central Drugs Standard Control Organisation (CDSCO)."

Giving insights on the value that pharma companies can bring to this segment, Nandini Piramal, Chairperson, Piramal Pharma outlines, “Navigating regulatory challenges in the nutra sector requires a clear focus on quality and transparency. Pharma companies can lead the way by applying their research and quality control expertise to create safe, effective products that consumers can trust".

Piramal also suggests that building strong relationships with regulatory bodies like FSSAI and actively participating in industry associations can help address these challenges. “By prioritising quality and collaboration, pharma companies can not only tackle regulatory hurdles but also set a higher benchmark for the entire industry,” she opines.

Kalka Prasad, AVP – Marketing, Crius Life, Crius Group, advocates for stricter regulations, particularly in India, where nutra standards are still evolving. He stresses the need for a collaborative effort between industry players and regulatory bodies to establish clear guidelines that ensure the safety and efficacy of products. "It is not justifiable to compare pharma products, where a lot of work has already been done and well-documented with international harmonisation (e.g., USP, EP, IP) on quality standards, with nutra products, which are still in their native stage and offer much scope for

improvement. A collaborative effort from both industry and governing bodies is needed to bring about the drastic change," he opines.

R&D

advantage

Looking at the sunny side, pharma companies' established expertise in R&D, clinical trials, and regulatory compliance can give them a distinct competitive edge in the nutra market. Piramal believes that pharma companies are well-positioned to create high-quality, sciencebacked products in a sector where quality standards can be inconsistent. "Their ability to validate health claims with rigorous trials and meet strict quality requirements builds trust and sets them apart," she says. Prashant shares a similar sentiment, noting that pharma companies have the advantage of well-established R&D capabilities. These capabilities allow them to create nutra products that cater to specific health needs while adhering to higher standards. "Pharma industries can leverage their R&D capabilities to innovate and develop products targeting specific diseases," says Prashant. "With increased pharma involvement in the nutraceutical domain, this will help streamline process compliance, raise product quality standards, and provide safety labeling, which will enhance consumer awareness and acceptance, ultimately fueling sector growth," he adds.

Evidence-based marketing: An imperative

Amid growing concerns over misleading marketing, pharma companies face challenges in the market where smaller or new entrants can quickly compete by making false claims, often blurring the lines of credibility and trust.

Piramal stresses the importance of education-driven marketing to foster consumer trust. "Ethical marketing focuses on education rather than exaggeration, empowering consumers with accurate information about product benefits. By staying true to their reputation for reliability and putting consumer well-being first, pharma companies can build lasting credibility in the nutra space," says Piramal.