Nobody delivers ag-friendly financing terms like AgDirect ®.

More than competitive rates, AgDirect delivers a broad selection of financing options, including flexible repayment terms and payment schedules that align with your customer's cash flow streams. That means AgDirect can help get your customers the equipment they want and save the working capital they need.

As low as $0 down * No prepayment penalties **

Financing terms from 2-7 years *

Delayed payments up to 15 months * Easy applications Fast credit decisions

888.525.9805 | agdirect.com

3 8

EXECUTIVE INSIGHT

Dive into this issue and begin with insights from Mark Hennessey, CEO, as he shares his perspective on the forecast and economic outlook in 2025 and beyond.

NEBRASKA FIELD REPORT

Join Phil Erdman as he summarizes key policy priorities coming from your state legislature and also what federal policy shifts and critical legislative discussions are on the horizon for 2025.

FEATURE 2025 – ECONOMIC OUTLOOK

Dive deep with AED and FCSA as they provide an essential guide to navigating the evolving political and economic landscape of 2025. Federal debates on tax reform, the Farm Bill, and corporate incentives are poised to reshape the financial outlook for businesses, families, and agricultural producers. At the state level, lawmakers are addressing diverse challenges such as tax reforms, paid sick leave policies, and UTV regulations. FCSA also highlights how these policy shifts align with a challenging economic climate, discussing the equipment industry’s strategies for managing rising input costs, fluctuating commodity prices, and tightening margins while redefining purchasing approaches. 11 4 16

IOWA FIELD REPORT

Read on as Jamie Mertz shares information on equipment pricing and current used equipment values from the last 20 years in the business. He also covers pricing trends and give his take on the future outlook.

12

FEATURE AGTECH

OUTLOOK 2025: RECOVERY, REALITY CHECKS, AND OPPORTUNITIES

Find out more about emerging opportunities driven by climatefocused investors, targeted innovations like generative AI, and strategic consolidation among smaller players suggesting 2025 could be a pivotal year for the ag tech industry.

EXPO DIRECTOR

Join Tom Junge, Expo Director, as he explores farmers’ insights into the cyclical nature of farming and agriculture, delving into production cost data and key indicators pointing toward potential future “cost reductions.”

MARKETING VIEW

Read along as Director of Marketing, Cindy Feldman, shares how you can increase dealership marketing success with more compelling headlines alongside your native advertising.

DEALER INFORMATION UPDATE:

In addition to receiving this Retailer magazine in print, INEDA will begin sending you more information in print––yes, you heard that right!

Currently, you can stay informed about events through the RoundUp eNewsletter, Retailer magazine, social media, email invites and on INEDA.com. Starting January 1st, however, we’ll also be promoting all events through print mailings.

We want to make sure you get information the way you prefer, and the choice is yours!

OFFICERS:

Jay Funke Chairman, Edgewood, IA

Kevin Clark Vice Chairman, Lincoln, NE

Tim Kayton Past Chairman, Alliance, NE

DIRECTORS:

Bruce Bowman Ankeny, IA

Kent Grosshans Central City, NE

Clay Haley Carroll, IA

Dave McCarthy Waterloo, NE

Mark Placek Alliance, NE

STAFF:

David Adelman IA Legislative Director

Phil Erdman Dir. of Dealer & Gov’t Rel.

Cindy Feldman Marketing Director

Laurie Haeder Ag Expo Coordinator

Mark Hennessey President/CEO

Tom Junge Expo Director

Tim Keigher NE Legislative Director

Cara Jicinsky Administrative Assistant

Jamie Mertz Dir. of Dealer & Gov’t Rel.

Gwen Parks Finance Director

subscriptions are available without charge to Association members. One-year subscriptions are available to all others for $30.00 (4 issues). Contact INEDA

This edition of the Retailer highlights the key trends from 2014 to 2024, explores economic impacts, and offers actionable insights for the future. While reflecting upon the past ten years, who would have predicted a black swan event called Covid-19. The disruption of supply chains was unprecedented throughout the world. Extreme highs and lows of product constraints, availability, and pricing were realized during these times. Today, we continue to see waves of this disruption. Dealers are forced to carefully manage their equipment inventories in light of economic slowdowns or uncertainty.

Over the past decade, inflation has evolved through distinct phases, shaping consumer behavior, business operations, and economic policy. For dealers, understanding these shifts is crucial for navigating pricing, inventory, operations and financing strategies. Keeping a close eye on policies of the incoming administration and ratification by congress will likely shape the next 5+ years.

Key trends that our equipment dealers may experience over the next ten years may include:

Moderate, but Persistent Inflation: Inflation rates are expected to stabilize at moderate levels, but supply chain disruptions, geopolitical tensions, and energy transitions could lead to occasional price surges.

Rising Interest Rates and Credit Tightening: The Federal Reserve may maintain higher interest rates to control inflation, leading to tighter credit conditions.

Technological Disruption and Automation: Increased adoption of AI, and automated customer service tools will redefine operations and customer interactions.

Demographic and Workforce Changes: Aging populations and shifts in workforce demographics will influence demand and operational practices. Training staff for new technologies, especially in service and parts management, will be a differentiator. AI will play a role.

Our equipment dealers have weathered many economic cycles, both in good times and rough times. The resiliency of equipment dealers throughout Iowa and Nebraska has shown that in spite of these uncertainties, our members find a way to adapt, innovate and overcome any challenges that are put in their path.

By embracing the changes that will occur over the next 10 years, we will undoubtedly face unexpected events that pose threats to our organizations, yet find new opportunities to grow and build bright futures, too.

Wishing all of you success in 2025 and many years to come.

Chief Executive Officer

PHIL ERDMAN Director of Dealer and Government Affairs [phile@ineda.com]

What to Expect from YOUR State Legislature

To avid sports fans, on either side of the Missouri River, this will not be news. The Hawkeyes have beaten the Huskers in 9 of the last 10 football games, while the lady Hawkeyes have never beat the lady Huskers in volleyball. Congrats to the Cyclones for making the Big 12 Football Championship.

The differences between Iowa and Nebraska are not only evident in sports, but in state politics and policy making.

The bicameral, partisan Iowa Legislature relies heavily on the leadership of the House and Senate to guide the process and determine what bills will have hearings as well as what is debated and passed.

The Unicameral Legislature in Nebraska is organized without party leadership – notice I didn’t say “nonpartisan” as Senators in Nebraska are all on a political team – and each Senator has the ability and right to introduce and debate as many of the issues that are introduced.

Iowa

All of the INEDA Iowa PAC candidates won their races. Thank you for your support of these candidates.

INEDA’S IOWA PAC Supported Candidates:

Iowa House

District 6 - Megan Jones

District 7 - Mike Sexton

District 10 - John Wills

District 26 - Austin Harris

District 28 - David Young

District 37 - Barb Kniff-Mcculla

District 54 - Josh Meggers

District 68 - Chad Ingels

District 76 - Derek Wulf

District 92 - Heather Hora

Nebraska

Iowa Senate

District 5 - Dave Rowley

District 9 - Tom Shipley

District 10 - Dan Dawson

District 12 - Amy Sinclair

District 19 - Ken Rozenboom

District 23 - Jack Whitver

District 27 - Annette Sweeney

District 34 - Dan Zumbach

District 41 - Kerry Gruenhagen

District 46 - Dawn Driscoll

Nebraska Equipment Dealers PAC (NED PAC) provided financial support to 27 candidates in 23 races. NED PAC supported candidates won 19 of those races. Thank you for your support in our efforts!

The party breakdown of the Legislature will keep Republicans with a 33-member majority but the support for specific issues may change based on the specific interests of those elected.

INEDA’S NEBRASKA PAC Winning Candidates:

District 1 - Bob Hallstrom

District 7 - Dunixi Guereca

District 9 - Sen. John Cavanaugh

District 11 - Sen. Terrell McKinney

District 15 - Dave Wordekemper

District 17 - Glen Meyer

District 19 - Sen. Robert Dover

District 21 - Sen. Beau Ballard

District 23 - Jared Storm

District 25 - Sen. Carolyn Bosn

District 27 - Jason Prokop

District 29 - Sen. Eliot Bostar

District 31 - Sen. Kathleen Kauth

District 33 - Dan Lonowski

District 37 - Stanley Clouse

District 39 - Tony Sorrentino

District 43 - Tanya Storer

District 45 - Sen. Rita Sanders

District 47 - Paul Strommen

An additional difference between the two states is that Nebraska voters have the ability to propose and pass referendums and initiatives.

Voters approved medicinal marijuana initiatives, repealed tax credits for scholarships for private schools, and rejected a constitutional amendment to remove all restrictions on abortion including parental notification in NE and instead approved a constitutional amendment that largely mirrors current state statues. Finally, Nebraskans voted overwhelmingly to require businesses to allow paid sick leave to be earned and used by employees. Businesses with 20 or fewer employees will be required to offer five days, or 40 hours, to be earned. Those with more than 20 workers will have to allow seven days, or 56 hours. This will go into effect on October 1, 2025.

2025 Legislative Session

Staff continue to gather intel on what to expect in the 2025 Legislative Session.

NEBRASKA – Governor Pillen continues to advocate for shifting more of the funding of local services from property taxes to sales tax. While many of the key advocates for his previous plan have been term limited out, the issue remains front and center. He is seeking to go after “low hanging fruit” to raise an additional $185 million in state revenue. We have been told that parts and agricultural equipment are not included at this time, but we will remain vigilant and active in these conversations. “Trust but verify.”

One issue that has been raised in conversation with dealers this summer and fall is the titling of Utility Vehicles (UTVs). Under current law, a machine must be less than 2000 pounds to be titled. Many of the newer machines either exceed the weight or length limits. We are currently working with manufacturers, Nebraska Department of Motor Vehicles, and County Treasurers to draft legislation that will narrowly and quickly resolve the matter and be introduced early in the session. Members will have the opportunity to submit testimony in support and if available attend the hearing in support once the bill has been introduced and the hearing date set.

IOWA – There is not any pending legislation at this time, however, we are diligently monitoring Iowa's legislative activity daily.

Upcoming Events

Legislative Reception

• February 5, 2025 – TBD pm – Iowa Events Center, HyVee Hall (Des Moines, IA)

Legislative Meeting and Golf Outings

• June 17, 2025 – 9:00 am – York Country Club (York, NE)

• June 19, 2025 – 10:00 am – Copper Creek Golf Club (Pleasant Hill, IA)

For more information on how you can get involved or if you have questions on state advocacy efforts, contact your Director of Dealer and Government Relations.

IOWA

Jamie Mertz, jamiem@ineda.com

NEBRASKA

Phil Erdman, phile@ineda.com

PHIL ERDMAN Director of Dealer and Government Affairs [phile@ineda.com]

Federal Tax Changes on the Horizon

With the 2024 in our rear-view mirror, many are anticipating what the new Congress and President Trump will do in the coming year.

Tax policy will be center stage as Congressional convenes in January due to the expiration of several key provisions from the Tax Cuts and Jobs Act (TCJA) of 2017. The TCJA, signed into law in December 2017, introduced sweeping changes to the U.S. tax code. However, many of its provisions were temporary, designed to sunset at the end of 2025 unless Congress acts to extend or modify them.

Among the key provisions set to expire are:

Individual Tax Rates and Standard Deductions

The TCJA reduced individual income tax rates across most brackets and significantly increased the standard deduction—a change that simplified tax filings for millions of Americans. Without legislative action, these rates will revert to their pre-2018 levels, likely leading to higher tax bills for individuals and families. The standard deduction will also decrease, potentially bringing more taxpayers into itemization territory.

Child Tax Credit (CTC)

The TCJA expanded the Child Tax Credit, increasing the maximum credit amount and making more families eligible. However, this expansion is set to expire, which could substantially reduce the credit available to middle- and low-income families. The resulting financial strain may disproportionately impact families with young children.

Other Individual Tax Provisions

Other expiring provisions include limits on state and local tax (SALT) deductions, changes to the alternative minimum tax (AMT), and adjustments to certain itemized deductions. The expiration of these measures could have varied impacts depending on taxpayers’ income levels and locations.

Potential Legislative Proposals:

With the sunset of the TCJA provisions looming, Congressional action will likely be required. Several proposals are already being floated:

Extension of TCJA Tax Cuts

Many Republican lawmakers and the incoming administration have expressed their intent to extend the TCJA tax cuts, citing concerns over potential economic slowdown and increased tax burdens. President-elect Donald Trump has indicated support for a broader tax reform package to make the 2017 cuts permanent, particularly for middle-income taxpayers.

Enhancements to Corporate Tax Incentives

The business community is closely watching discussions around corporate tax breaks. Proposals include reinstating full deductions for research and development expenses and maintaining immediate expensing for capital investments—measures that aim to boost innovation and economic growth (reinstating 100 percent bonus depreciation and business interest deduction cap at 30 percent of EBITDA).

Child Tax Credit Expansion

Both parties are seeking to champion the expansion of the Child Tax Credit. Proposals under consideration include increasing the credit’s maximum amount, tying it to inflation, and allowing families to calculate eligibility based on prior-year income. Such measures aim to reduce child poverty and provide more robust support for working families.

Looking Ahead

The next two years will be pivotal for U.S. tax policy. Congressman Smith (NE), Chair of the Rural America Tax Team for Ways and Means Committee Republicans, has been leading the effort to review the tax code ahead of Tax Cuts and Jobs Act reauthorization next year.

With significant economic and political stakes, debates in Congress are expected to be intense. As lawmakers balance fiscal responsibility with economic growth, we will continue to work closely with the federal delegation in Iowa and Nebraska along with our partners at Associated Equipment Dealers (AED) to strongly support making expiring (and expired) provisions from the Tax Cuts and Jobs Act (TCJA) permanent.

Farm Bill

Lawmakers have been unable to pass the Farm Bill but have extended the current law to allow them more time to develop a new policy for the next five years. Many in agriculture are encouraging leadership to strengthen the safety net for farmers, continue voluntary, incentive-based conservation programs that allow for producer flexibility, expand the use of agriculture-based biofuels, encourage adoption of the most precise, high-tech equipment, and invest in promoting U.S. commodities around the world. The passage of a new Farm Bill has been and remains a priority for the Iowa and Nebraska members of Congress.

Iowa Federal Delegation (Republicans)

Sen. Chuck Grassley

Sen. Joni Ernst

Rep. Mariannette Miller-Meeks (CD 1)

Rep. Ashley Hinson (CD 2)

Rep. Zach Nunn (CD 3)

Rep. Randy Feenstra (CD 4)

Nebraska Federal Delegation (Republicans)

Sen. Deb Fischer

Sen. Pete Ricketts

Rep. Mike Flood (CD 1)

Rep. Don Bacon (CD 2)

Rep. Adrian Smith (CD 3)

Washington DC Fly-In

INEDA members are invited to attend the annual Washington DC Fly-In planned for March 25-27, 2025. We will meet with industry leaders, including staff from AED during our visit prior to visits to members of the Federal Delegation from each state. If you are interested in attending, including the support that INEDA can provide to your dealership for you to attend, please contact your Director of Dealer and Government Relations:

Iowa

Nebraska

Jamie Mertz Phil Erdman jamiem@ineda.com phile@ineda.com

JAMIE MERTZ Director of Dealer and Government Affairs [jamiem@ineda.com]

Price Trends and Future Outlooks

As we conclude 2024, the agricultural equipment market has continued to evolve. New machinery prices have significantly increased, while the value of used equipment has shown a decrease in value due to factors such as high inventory levels and the use of auctions to manage those inventory levels. Every ten years Tom would come out with an article highlighting the increase in the price of new equipment and the price of the used equipment 10 years later to compare. Below is a chart showing the trend of equipment prices over the past 20 years. Here are some of the findings based off the prices available. The wholesale values were gotten off Iron Guides or by utilizing AuctionTime prices.

Following is a summary of the findings over the past 20 years.

• New Equipment – Since 2003 to present, the price of agricultura l equipment has significantly increased. New equipment in many categories has more than doubled over the past 20 years with the past ten years having more significant price hikes than the previous 10-year span.

• Used Equipment – Used equipment with certain equipment has remained relatively stable, while other equipment, such as used combines have taken much sharper declines in value. Used combines have taken such a steep decline because they are higher maintenance equipment and there have been many more of them on auctions in the past 10 years.

Some of the key drivers in the price dynamics we have seen over the past 20 years have been supply and demand and the advancements in technology on equipment which have shifted the preferences of farmers for more efficient machinery that will do more for them in less time. Looking ahead to the next 10 years technology will play an even more transformative role in the agricultural landscape. With the use of AI and other emerging technologies we will see enhanced automation, data analytics, and AI decision making tools on new equipment. The agricultural equipment market over the past twenty years has been influenced by innovation, market forces, and economic trends. The advancement in technology will continue to shape the agriculture equipment market and how farmers are utilizing the equipment for each of their operations. The opportunity for greater efficiency and sustainability with ag equipment is what will continue to drive the market.

Start-Up Showcase

The Nebraska Ag Expo, a trailblazer in advancing agricultural innovation and host of Innovation Hub – hosted their third Innovation After Hours event this month. Over 150 start-ups, investors, and executives from innovative ag companies and partners from across the country and beyond shared an evening of networking and innovation.

Nebraska Innovation After Hours is presented by Farm Credit Services of America, Iowa Nebraska Equipment Dealers Association, Invest Nebraska, The Combine, and Nebraska Innovation Campus.

This year, 6 companies competed for cash prizes during the Startup Showcase:

• AgZen (MA) – Revolutionize farming practices by providing real-time insights into droplet behavior. (agzen.com)

• ALA Engineering (NE) – Cutting-edge intelligence behind feedlot operations, combining advanced software, sensors, and computing power to autonomously feed cattle with precision and efficiency. (ala. engineering)

• Bio-Agtive Emissions Farming (CAN) – Rapidly builds soil organic matter, but it also empowers you to gain free nitrogen for your farm to eliminate costly inputs, notably synthetic nitrogen. (bioagtive.com)

• Grain Weevil (NE) – Grain bin safety and management robot that directly engages the surface of the grain. Grain bins are dirty, dangerous workplaces. (grainweevil.com)

• PathoScan (CAN) – Enables farmers to perform pathogen test for any crop, anywhere, without any technical background. (pathoscan.com)

• RhizeBio (NC) – Creators of a unique metagenomic method, coupled with machine learning and biostatistics, to test raw soil DNA sequencing data into user-friendly and informative soil health reports. (rhizebio.com)

Grain Weevil was named the Startup Showcase Winner and received a $5000 cash award from the Iowa Nebraska Equipment Dealers Association (INEDA). Pictured is Mark Hennessey, CEO of INEDA and Chad Johnson, CEO of Grain Weevil.

AgZen was named the “People’s Choice Award” and received a $1000 cash award from The Combine. Pictured is Josh DeMers of The Combine and Vishnu Jayaprakash, CEO of AgZen.

As 2025 unfolds, federal and state policy changes are poised to significantly impact industries and communities. On the federal level, key provisions of the 2017 Tax Cuts and Jobs Act are set to expire, prompting discussions on tax reform, the Farm Bill, and corporate incentives. These debates could reshape the financial landscape for businesses, families, and agriculturalproducers.

Meanwhile, state legislatures in Iowa and Nebraska are tackling diverse challenges, including tax reform, paid sick leave policies, and regulations for utility vehicles. The interplay of legislative priorities at both levels will shape the year ahead for policymakers and stakeholders alike.

For equipment dealers and farmers, these policy shifts coincide with a challenging economic outlook. Rising input costs, fluctuating commodity prices, and tight margins are redefining purchasing strategies for agricultural machinery. While interest in precision farming technologies grows, high borrowing costs and shrinking net farm incomes are driving cautious decision-making.

Together, these articles on the next several pages provide an essential guide to navigating the evolving political and economic terrain in 2025.

Stakes are High for Equipment

As the Trump administration gears up for its second term, the equipment industry stands at a critical juncture, navigating a landscape filled with both opportunities and uncertainties. Despite holding Republican majorities in both chambers of Congress, the party faces significant internal divisions. With razor-thin margins, achieving legislative progress will require strategic maneuvering and compromise. The challenges posed by narrow majorities and conflicting priorities—evident during the 118th Congress— underscore the risk of legislative gridlock. For the 119th Congress, pivotal issues like the Farm Bill, tax policy, and trade agreements will shape the future for equipment dealers, our customers, and our manufacturers, making the stakes higher than ever.

The Farm Bill: An Unfinished Agenda

The 2024 election ushered in significant changes in Washington, D.C., including a new Republican trifecta with a Republican-controlled Senate and an incoming Trump administration 2.0. However, the party’s slim majority in both the House and Senate will pose challenges in reaching consensus on major pieces of legislation. While Republicans now have an edge in negotiating priorities, slim margins will challenge GOP leaders trying to turn electoral successes into policy victories.

At the end of the 118th Congress, lawmakers approved an extension of the Farm Bill. The current Farm Bill, which was enacted in 2018 and expired on September 30, 2023, is in dire need of updating and modernization. While the extension offers a stopgap, the urgency remains to address the longterm needs of America’s rural communities and the agriculture sector.

Looking ahead to the 119th Congress, leadership changes will further influence the trajectory of the Farm Bill. A Republican-led Senate Agriculture Committee will take over, introducing new strategies and priorities. Senate Majority Leader Thune has indicated an initial focus on reconciliation bills addressing narrower issues, such as border security, energy

development, and tax priorities. These priorities could delay comprehensive Farm Bill discussions, potentially prolonging uncertainty for stakeholders.

Maintaining access to critical support programs is a priority for AED members and dealers who serve the agricultural sector. AED continues to advocate for provisions that ensure farmers have access to necessary lines of credit and crop insurance, which are vital to the success of the agricultural industry. Additionally, incentivizing investments in precision ag technologies will assist farmers in taking advantage of technological developments. These provisions and the bill’s broader objectives that support agriculture producers are crucial for creating a predictable policy environment that supports long-term investments in equipment and workforce development.

Tariff Policies: Uncertainty Looms

President Trump’s renewed rhetoric around tariffs has sparked concern among AED members. While intended to bolster domestic manufacturing, past tariffs have disrupted supply chains and increased costs for dealers. With the administration signaling potential 25 percent tariffs on imports from Canada and Mexico and an additional 10 percent tariff imposed on goods from China, the equipment industry, from manufacturers and dealers to end users, should pay close attention.

Current tariff rates range a great deal based on the product and the country of origin. Tariffs can be lower for countries with which the United States has trade agreements, such as the US-Mexico-Canada trade agreement, which allows most goods to move tariff-free among the three nations. However, there is much misinformation about who pays tariffs. While former President Trump often claimed foreign countries bear the cost, tariffs are actually paid by importers — American companies — with the revenue going to the U.S. Treasury. These companies typically pass higher costs onto consumers, meaning U.S. consumers ultimately foot the bill.

DANIEL FISHER, Associated Equipment Distributors (AED) Senior VP of Government and External Affairs [dfisher@aednet.org]

Dealers in the New Congress

Tariffs are intended to protect domestic industries by raising the price of imports, making home-grown manufacturers more competitive. However, they can provoke retaliation from other countries, further disrupting trade. During Trump’s first administration, China imposed retaliatory tariffs on U.S. commodity imports, significantly affecting soybean and corn exports and dealing a major blow to U.S. agricultural producers. Similar issues could reemerge, potentially exacerbating challenges for farmers and the dealers who support them.

While tariffs can serve as a tool to pressure foreign governments on broader issues, they often result in higher costs for consumers and businesses, and economists generally view them as self-defeating. Studies have shown that Trump’s tariffs failed to restore jobs to the American heartland and caused retaliatory measures that harmed U.S. farmers and manufacturers.

Tax Policy: The Future of the TCJA

The Tax Cuts and Jobs Act (TCJA) of 2017 provided significant benefits to AED members, particularly through 100 percent bonus depreciation, which has driven investments across the equipment industry. This provision allows businesses to fully deduct the cost of new and used equipment purchases upfront, freeing up cash flow for reinvestment. However, it began phasing out in 2023 and is set to fully expire by 2027, compounding the fiscal cliff created by the 2025 expiration of other TCJA benefits.

AED also advocates for the permanent extension of the Section 199A deduction, which expires at the end of 2025. Section 199A provides tax relief for pass-through businesses like S-corporations and LLCs, ensuring they can remain competitive with corporations taxed at the lower 21percent rate. Furthermore, AED supports tying the business interest deduction cap to EBITDA (earnings before interest, taxes, depreciation, and amortization), rather than

EBIT, to help businesses manage borrowing costs, especially in capital-intensive sectors like the equipment industry.

Preserving current estate tax exemptions and stepped-up basis is another priority for AED, as these provisions protect family-owned businesses from punitive double taxation when assets are transferred between generations. Without these measures, many businesses could face significant financial challenges and be forced to sell the company when the next generation takes over.

The debate over how to extend these provisions reflects broader tensions in Congress. GOP leadership will have to navigate narrow majorities and won’t be able to afford to lose any votes. Consequently, fiscal hawks, concerned with the $4.6 trillion cost of extending TCJA provisions without offsets, and Republicans from high-tax states, like California and New York clamoring for a more generous state and local tax deduction, must be satisfied.

While the Trump administration is expected to advocate for pro-business tax policies, it remains uncertain whether Congress will deliver permanent solutions or resort to temporary measures, such as in 2017. AED emphasizes the urgency of ensuring these provisions are not only extended but made permanent to safeguard industry growth and stability.

Conclusion

The 119th Congress will be pivotal for the equipment industry, with critical decisions on the Farm Bill, tariffs, and tax policy looming. It is imperative that dealers and manufacturers remain engaged with lawmakers by connecting with their members of Congress, hosting them at their businesses, and utilizing AED—the national association representing all equipment dealers in the nation’s capital.

FARM EQUIPMENT ECONOMICS

While nobody can predict what 2025 holds for agriculture, today’s economic trends and past cycles provide valuable insights for thinking about farm equipment purchases. AgDirect, powered by Farm Credit, looks at some of the key factors shaping on-farm income and decisions.

Equipment has gotten more expensive.

Price matters when purchasing new farm equipment. Since 1990, the average price of a new tractor has outpaced the rate of inflation. The average price of a 200-horsepower tractor has risen 287% and the price of a new 300-horsepower tractor, 275% -- double the rate of inflation from 1990 to 2024.

The margin squeeze is real.

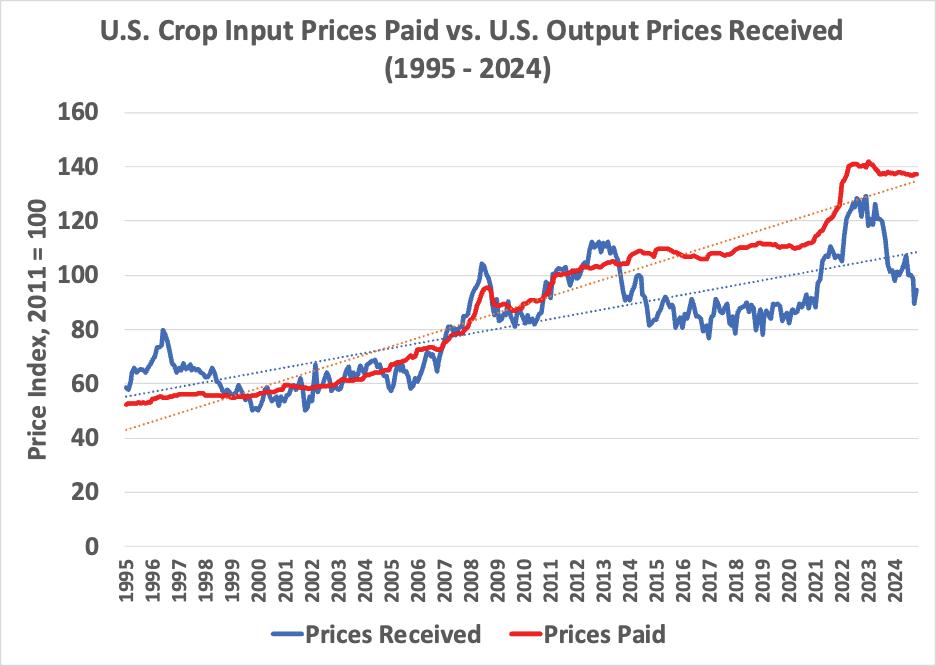

U.S. crop producers have experienced significant margin compression during the past year. Crop prices received by producers were volatile in 2024. As the chart below shows, crop prices received increased 9.5% in the first half of the year, followed by an 11.8% drop from June to November. In fact, crop prices in November were 5.4% lower than in January 2011.

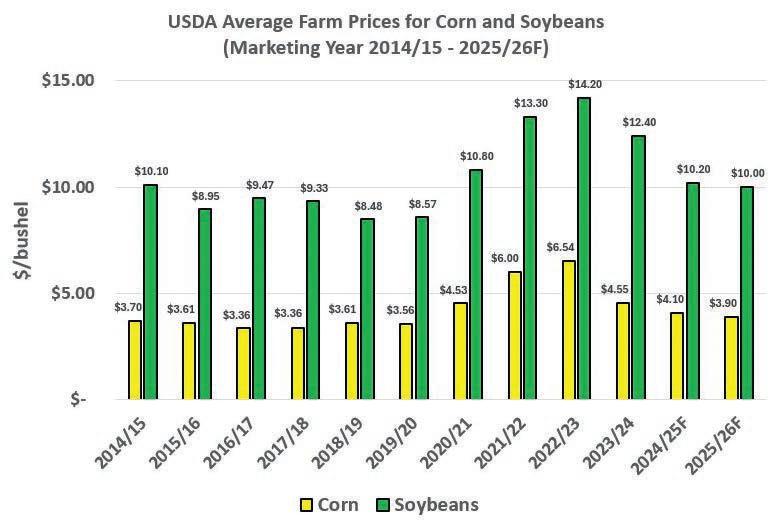

Average farm prices for corn and soybeans are projected to decline further for the 2025/2026 marketing year. Corn prices are expected to be around $3.90 per bushel and soybeans, $10 per bushel for marketing year 2025/26. This means margins will remain tight, and in some cases negative, for U.S. corn and soybean producers.

Input costs are higher.

The prices that U.S. crop producers pay for chemicals, fertilizer, farm machinery, fuels, seeds and other production costs have stayed relatively “sticky” since 2022. While crop prices at the end of the 2024 harvest were down more than 5% compared to January 2011, input prices paid were up 37.5% for the same time period.

Little relief on the interest rate front.

Meanwhile, the federal funds rate that shapes interest rates is expected to drop only 50 basis points in 2025, far less than the 150 basis points projected last fall. Interest rates are at more historically normal levels but have added to the cost of financing at a time when producers also face higher production costs.

Net cash farm income is down.

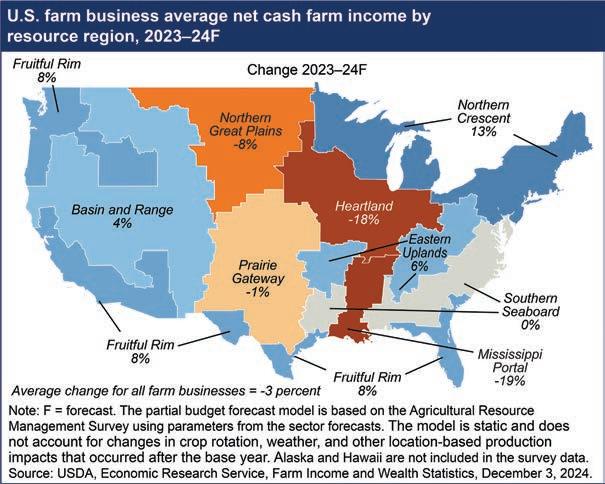

Net cash farm income is cash receipts from farming and cash from farm-related income (such as government payments) minus cash expenses. On an inflation-adjusted basis, average net cash income for farm businesses, USDA projects a decline of nearly 20% -- or $30,000 – from 2023 to 2024 for producers in the heartland region, as shown in the map above. If accurate, this would be the largest year-over-year decline in percentage terms since 2013 to 2014.

‘

A three-year rolling average for net cash farm income in the heartland region (graph below) offers yet another perspective. It is down, but by a relatively more modest 13%. It reflects positive cash receipts from farming, as well as significant government payments.

Producers entered the current downturn in the grain market with unprecedented levels of working capital and balance sheets are still positive. However, lower commodity prices and higher production costs likely will eat into working capital in 2025.

When adjusted for inflation, average net cash farm income nationally for corn and soybean producers is expected to be at its lowest level since 2010, the first year this data was collected. Average net cash farm income for all U.S. corn farms is forecast to be down 35% from 2023 to 2024, while income from soybeans is expected to decline 36% year-over-year.

What this means for equipment purchases in 2025.

While the economic outlook is challenging, proactive planning, strong risk management and strategic management can help farmers mitigate some of these pressures. But preserving working capital will be top of mind, and this will shape purchasing decisions.

Farm equipment sales in 2025 likely will be mixed as commodity price pressures impact producer margins.

Used Equipment Market: Producers may be hesitant to purchase new or used equipment until they get a handle of their working capital situation putting pressure on the new and used equipment market. Machine prices are expected to remain solid as inventory levels stabilize. This might suggest that demand for used equipment may be higher than the new equipment market, providing opportunities for farmers looking to upgrade without the high costs of new machinery.

New Equipment Sales: The outlook for the new equipment market is more cautious. Economic pressures, tight margins, and high input costs may lead farmers to delay purchasing new machinery. However, advancements in precision agriculture and smart farming technologies could drive interest in specific high-tech equipment.

Auction Market: The auction market may remain active, with many farmers considering retirement or restructuring their operations. This could lead to increased availability of used equipment at auctions, potentially at competitive prices.

Overall, new and used equipment sales might face some headwinds in 2025 due to tight margins. However, with the increase in equipment inventory over the past couple years along with lower producer demand, equipment prices may also be under pressure Farmers should carefully evaluate their needs and financial situation to make informed decisions about equipment investments in 2025.

Source: The analysis is provided by Matt Erickson, an economist for Farm Credit Services of America (FCSAmerica).

There are many questions to consider when making decisions about acquiring machinery. With higher borrowing costs and reduced net farm income challenging profitability, these decisions are even more critical. Before buying, set a realistic budget. Completing the following steps and involving trusted advisors early in the buying process can help you set expectations about your purchasing power and what you can comfortably afford.

1. Review production records to assess your working capital, cash flow and overall payment capacity

2. Conduct research to compare costs and establish a reasonable price point.

3. Reach out to your local dealer for additional information about pricing, product specifications and trade-in values.

4. Consult with your accountant or tax adviser to discuss tax benefits and liabilities.

5. Contact your lender to learn about the latest interest rates and your loan and lease options.

6. Factor in additional costs that may not be covered in the initial price, such as transportation costs or buyer’s fees.

7. Evaluate opportunities to share equipment or provide custom services to offset costs.

Compare Payment Options

Choosing between loans, leases, cash payments or an operating line of credit depends on your specific needs. Think about how each option impacts your ownership and operating expenses, cash flow and tax position.

For example, how many hours a year do you expect to use the equipment? Are you looking for the lowest possible initial investment and payment? Do you have built-up working capital? Is it best used toward machinery or other areas of your operation? Is it beneficial to keep your operating line open or retain liquidity for other expenses and future expansion opportunities?

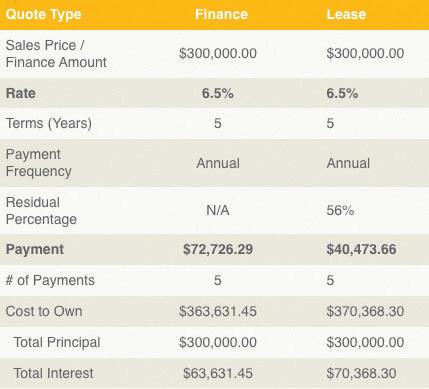

The following example compares an estimated loan versus lease payments for a new row crop tractor using a 5-year walk away lease agreement with a limit of 300 hours per year. In this comparison, the lease option lowers the annual payment by more than $32,000. The actual payment amount and residuals may vary depending on equipment brand, rate, closing date, asset valuation and other factors.

Loan vs. Lease Comparison

For more on ag equipment decisions in 2025, download AgDirect’s buyer guide at agdirect.com.

TOM JUNGE, Expo Director [tomj@ineda.com]

Word at the Expo was “Agriculture is Cyclical”

The Nebraska Ag Expo continues to thrive, drawing a full house of exhibitors with a long wait-list eager to join the show. The event attracted a vibrant mix of attendees spanning multiple generations, highlighting its broad appeal and enduring relevance to farmers and ranchers. The expanded Innovation Hub, featuring 73 exhibitors, became a standout destination, showcasing cutting-edge solutions and fostering exciting conversations about the future of agriculture while visitors were impressed by the superior educational ag talks, which offered valuable insights into industry trends and advancements.

Naturally, the recent downturn in commodity prices lowered near-term expectations from exhibitors at the Nebraska Ag Expo; however, exhibitors are optimistic that farmers, manufacturers and dealers will adjust like they did in the past.

History seems to repeat itself. 2013 was the last year for “high” grain prices and 2014 for cattle. 10 years later, 2023 was the last year of “high” grain prices and too early to tell, but maybe 2024 for cattle. If I remember correctly, it took 3 to 4 years for dealers and farmers to adjust to the “back-to-earth commodity prices”.

Reducing the cost of production will be key for farmers to purchase high ticket equipment again. Here are some indicators that farmers might be able to do such in the coming years.

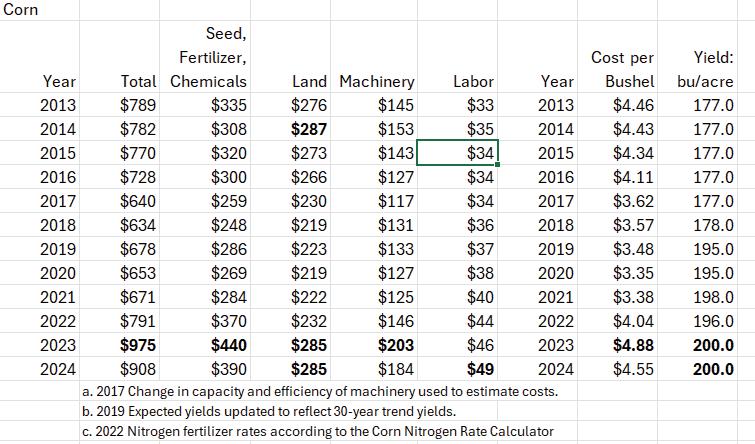

Cost of Production

Looking at data from Iowa State University, the cost of production of corn has already dropped from $974.60/acre in 2023 to $908.30/acre in 2024. On a per bushel basis, it dropped from $4.88 to $4.55. The biggest drop came from the seed, fertilizer and chemical category. Although the cost of production has dropped, it still needs to be lower to hit break-even at today’s cash price of $4.22 (Dec. 21). NOTE: After 2013’s peak, farmers were able to reduce their cost to $4.11/bushel by 2016.

Corn

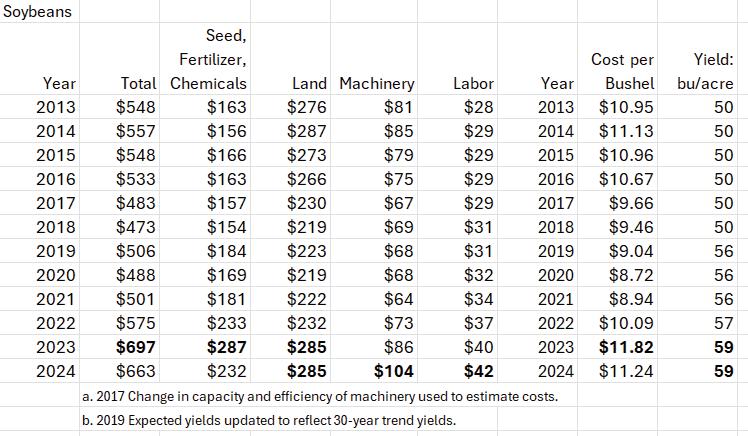

The cost of production of soybeans dropped from $697.40/acre to $663.10/acre. On a per bushel basis, it dropped from $11.82 to $11.24. Although it has dropped, it still has a long way to go to hit the breakeven cash price of $9.21 (Dec. 21).

The cost of chemicals, fertilizer, seed, land and machinery all hit their high in 2023. Labor hit a high in 2024. The exception was machinery for soybeans, which hit a high in 2024.

Indicators for Future Lower Production Cost

Land

The 2024 Iowa State University Land Value Survey reported a 3.1% decrease to $11,467 per acre for average Iowa farmland values from November 2023 to November 2024. This represents a decrease of $369 per acre from last year. Rent will likely lag this trend but will eventually follow.

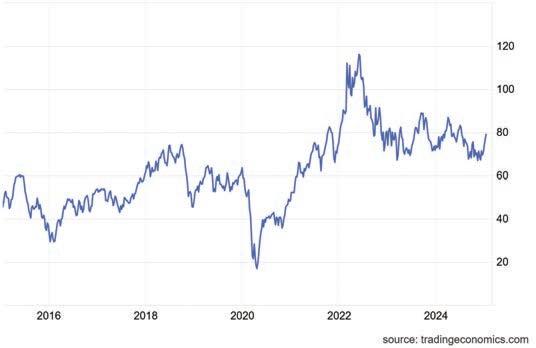

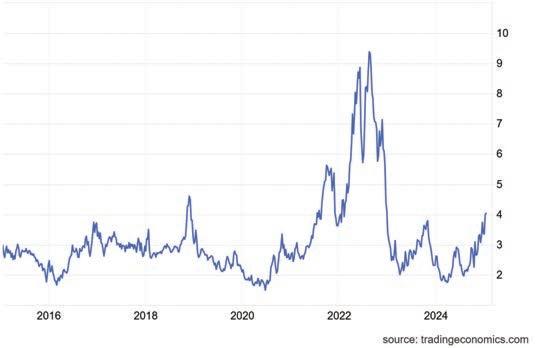

Diesel/Fertilizer

The price of crude oil is also an important component in the cost of production. It is the base for diesel fuel and so many other items such as chemicals, plastics, etc. Nitrogen-based fertilizers, relies on natural gas derived from oil. The good news is that both have peaked in 2022. Anhydrous Ammonia in December was $692/ton. In 2022, Anhydrous ammonia hit $1600/ton. Charts provided by Trading Economics.

Crude Oil

Natural Gas

Soybeans

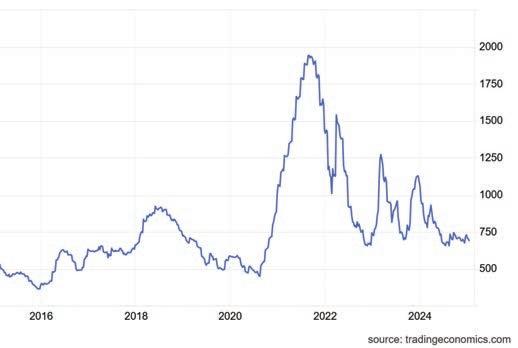

Steel Prices

Good news is possibly coming on equipment production cost, at least where steel is a major component. A couple Nebraska Ag Expo exhibitors mentioned that steel prices have dropped dramatically. Two of the livestock equipment exhibitors said their wholesale price has dropped which has allowed them to lower their cost to producers.

Hot-rolled steel has dropped from a high of $1,943/ton to $679/ton, a 65% drop since August 2021. Most exhibitors feel that steel companies will try to hold their prices to achieve a higher margin but will eventually be forced to lower them. The same could be said of equipment manufacturers. Eventually, lower steel prices will be passed down as price roll backs or program discounts.

Hot-Rolled Coil Steel

Interest Rates

After hitting a high in 2023, the Federal Reserve started cutting interest rates. As of now, the rate has been cut by .75%. Two additional cuts are planned for 2025. These additional cuts will provide some relief in farmer operating loan rates.

Growth on the Horizon: Agriculture’s Cyclical Comeback

History shows that agriculture is cyclical. It was a tough stretch after 2013/2014 for farmers and dealers alike, but over time economics improved. It appears farmers will be able to reduce their input cost in the coming years. Hopefully this turnaround will be shorter than a decade ago, but no one really knows.

The AgTech Outlook for 2025: Recovery, Reality Checks,

and Opportunities

Even though the AgTech sector in North America showed some growth this year, increasing in value from $9.26 billion in 2023 to an estimated $11.46 billion, it was still a turbulent 12 months. Constrained funding, uncertain economic conditions, and rising challenges for companies navigating the biological and crop protection landscape all contributed to a more restrained environment. However, there is reason for cautious optimism in the new year.

Investment trends are evolving, with investor expectations shifting. There are also opportunities emerging for those organizations that can deliver tangible value. To this end, we’ve identified five trends that will contribute to the AgTech outlook in the coming months. These will be shaped by macroeconomic conditions globally and particularly in the US, investor priorities, and technological innovation.

1. Recovery depends on macroeconomic stability

Sustainable growth in the AgTech sector in 2025 will be closely tied to macroeconomic stability, not just in the US but on a global scale. Trade tariffs, supply chain disruptions, and inflationary pressures remain key challenges, but much of the sector’s momentum hinges on decisions made by the incoming US and various European administrations. Policies surrounding climate initiatives, subsidies, and agricultural trade agreements will either create an enabling environment for investment or deepen market uncertainty.

A more stable global economic outlook, combined with supportive domestic policies, could restore investor confidence and unlock funding opportunities. Conversely, prolonged stagnation or unfavorable policies could extend the challenges seen throughout 2024. For the AgTech industry, stability is the foundation for growth, and 2025 will be a critical year in determining whether this balance can be achieved.

2. A new breed of investors with higher expectations

Additionally, the investor landscape for AgTech is changing. Many traditional AgTech venture funds, having struggled to secure strong exits, are unlikely to raise new rounds of funding. In their place, impact-focused and climate-centric VCs are stepping in, driven by the urgency to address climate change and its critical ties to agriculture. If anything, food and agriculture will be one of the most important components of this climate change focus. These investors bring with them a new set of priorities, placing greater emphasis on sustainability, measurable results, and long-term viability.

For startups, the bar has been raised. Investors are demanding clearer proof points, tighter unit economics, and scalable business models that can pass more intense scrutiny. While this shift may favor younger startups still in early growth stages, later-stage companies that have yet to demonstrate financial viability could face significant hurdles. Funding will likely flow to startups that can pass the ‘reality check’ on scalability and value creation. Even so, higher investor expectations will likely see lower valuations continue for the foreseeable future.

3. Big acquisitions are on hold — Smaller players will seize the opportunity

The financial challenges faced by major agrochemical companies suggest that large-scale acquisitions in the AgTech space will remain subdued in 2025. Many of the industry’s biggest players are focused on cost control and operational efficiency, leaving little appetite for major deals. This pause in acquisitions is likely to continue for the next three to four years as these companies manage their financial performances and recover from ongoing market pressures.

However, this shift presents opportunities for second-tier players and private equity firms to step into the vacuum. Smaller companies with strategic capital could take advantage of asset divestments and forced sales, acquiring distressed assets or undervalued technologies. The result may be a wave of roll-up strategies, where agile players consolidate assets and strengthen their market positions.

We anticipate that this will be one of the most interesting areas to watch in 2025. Companies with time-sensitive investors may be forced into sales at lower valuations, creating openings for strategic consolidations at a fraction of the value.

4. Generative AI will drive targeted innovation

Generative AI (GenAI) is emerging as one of the most transformative tools in agriculture, and its role in 2025 will be increasingly practical. The focus will no longer be on broad AI promises but rather on solving specific, high-value problems. Companies applying GenAI to targeted areas such as soil health monitoring, crop disease prediction, supply chain management, and biological innovation are well-positioned to attract significant funding.

The growing sophistication of AI models allows startups to identify solutions that unlock real efficiencies for farmers, streamline processes, and reduce costs. Investors will prioritize those organizations that can demonstrate measurable results, backed by comprehensive AI-driven processes.

5. The US recovery could outpace Europe but with caveats

While Europe’s regulatory consistency provides a foundation of resilience for AgTech investment, the US presents both greater potential and higher volatility. The sheer scale of the US market, combined with its innovation-driven ecosystem, positions it for a sharper recovery if favorable policies emerge. Climate-focused regulation, trade agreements, and incentives for sustainable agriculture could accelerate this rebound, fostering an environment where funding flows more readily to innovative companies.

However, this recovery is highly sensitive to political shifts. If climate policy is deprioritized or a more protectionist stance is adopted, the momentum could stall. Europe, in contrast, may lack the dynamism of the US market but offers steady progress driven by its long-term commitment to sustainability and stricter regulatory frameworks.

Potential for a new beginning

While macroeconomic uncertainty persists, the opportunities for companies to deliver measurable value in AgTech are growing. New investors, particularly those focused on climate and demonstratable impact, are entering the space with clear expectations, while technologies like GenAI are enabling practical, targeted innovation. At the same time, a pause in major acquisitions may create room for smaller players to consolidate and thrive.

For startups and innovators willing to navigate these evolving dynamics, 2025 could mark the beginning of a new and transformative chapter for AgTech.

Source: By Jeff Bell & Thomas Laurent | Micropep (globalagtechinitiative.com)

FTC Non-Compete Ban and Upcoming Practical Considerations for Employers

ISSUE

AUGUST 19, 2024 – Earlier in the year, Federal Trade Commission (FTC) issued a new rule which essentially bans non-compete limitations for workers in the United States. The rule banning non-competes is scheduled to take effect on September 4, 2024.

Although the business community has been anticipating a nationwide preliminary injunction to derail the ban, federal courts to date have only temporarily enjoined the FTC from enforcing the rule against Ryan LLC, a global tax services and software provider. The judge in Ryan LLC v Federal Trade Commission has refused to extend the scope of the preliminary injunction beyond applicability to Ryan. The judge in Ryan LLC has indicated she will release her final ruling by August 30th, which is mere days from the rule’s scheduled effective date.

POSSIBLE RELIEF

Notwithstanding the practical considerations for developing a plan of action for compliance, employers can still reasonably anticipate a protracted legal battle for the FTC to successfully implement this rule in its entirety. There are a number of other challenges in other jurisdictions and a court could still issue a broader nationwide injunction or vacate the rule in its entirety prior to the scheduled effective date.

ACTION

INEDA and Associated Equipment Distributors (AED) have a formal agreement to collaborate on federal advocacy efforts. Together we are advancing dealer interests in Washington, D.C.

AED joined comments on the proposed rule and urged the FTC to delay implementation to allow for judicial review in an industry letter. While AED is hopeful the courts will strike down the non-compete ban, employers should plan to comply with the mandate. If you have specific questions about the rule and its application to your company, please contact your attorney for further guidance.

UPDATE

AUGUST 21, 2024 – Yesterday, Judge Ada Brown of the U.S. District Court for the Northern District of Texas ruled that the Federal Trade Commission (FTC) lacks legal authority to implement its “non-compete” rule. As we alerted you in the below update, on April 23, 2024, the FTC ban on nearly all non-compete agreements was set to take effect on September 4. However, Judge Brown concluded that the FTC exceeded its statutory authority in promulgating the rule and that the rule itself was arbitrary and capricious. Therefore, the rule is considered unlawful and, for the moment, is now set aside (i.e., not enforceable).

The FTC will likely appeal the decision, opening the door to further review by higher courts. Nonetheless, at this time, the non-compete ban is not enforceable.

DEALER INFORMATION UPDATE:

These are the most recent “Regulatory ALERTS,” however, others can be found under the Dealer Resources tab on the INEDA website at https://ineda.com/regulatory-compliance-2/.

ISSUE

AUGUST 19, 2024 – Earlier in the year, Federal Trade Commission (FTC) issued a new rule which essentially bans non-compete limitations for workers in the United States. The rule banning non-competes is scheduled to take effect on September 4, 2024.

Although the business community has been anticipating a nationwide preliminary injunction to derail the ban, federal courts to date have only temporarily enjoined the FTC from enforcing the rule against Ryan LLC, a global tax services and software provider. The judge in Ryan LLC v Federal Trade Commission has refused to extend the scope of the preliminary injunction beyond applicability to Ryan. The judge in Ryan LLC has indicated she will release her final ruling by August 30th, which is mere days from the rule’s scheduled effective date.

POSSIBLE RELIEF

Notwithstanding the practical considerations for developing a plan of action for compliance, employers can still reasonably anticipate a protracted legal battle for the FTC to successfully implement this rule in its entirety. There are a number of other challenges in other jurisdictions and a court could still issue a broader nationwide injunction or vacate the rule in its entirety prior to the scheduled effective date.

ACTION

Custom Wealth Advice Driven By Your Needs

At Tax Favored Benefits, we serve as a partner in helping individuals, families and business owners achieve financial success.

Our experienced professionals are supported by world-class resources in providing a full suite of wealth, investment and retirement planning services to clients across the country.

We focus, first and foremost, on helping you achieve your personal financial goals. As financial professionals, we put your best interests first, at all times and in all situations. We succeed when you succeed.

Interested in learning more about how we can help you achieve your financial goals? Contact us to get started.

We look forward to getting to know you.

David

B. Wentz, J.D.,

dbw@tfbusa.com

EDUCATION

Career Exploration Event 2024

The Nebraska Ag Expo held December 10–12, 2024, hosted its 4th annual Career Exploration Event to educate middle and high school students about career opportunities in agriculture and construction. 344 students from 15 schools registered for the event.

Students participated in guided tours, led by local dealerships, to interactive presentations by eight companies, including John Deere, CaseIH, Bobcat, Stine, and Sukup about their history, operations, and career opportunities. Following the tours, students gathered for keynote presentations from industry leaders, educators, and company representatives. Speakers emphasized qualities employers value, such as a strong work ethic, positive attitude, and teamwork, and shared motivational insights about achieving success.

Mark Hennessey, CEO of the Iowa Nebraska Equipment Dealers Association which owns and operates the Nebraska Ag Expo, stressed the importance of personal responsibility and determination, encouraging students to adopt winning attitudes and behaviors to succeed in life and work.

Afterward, students explored the Expo independently and provided feedback through surveys on the event’s impact and their interests in the careers highlighted. The event continues to grow its reputation as a valuable resource for career education in Nebraska.

$1.8B Combined Gross Annual Revenue of Nebraska Equipment Dealerships

151 Dealers in Nebraska Sell Ag, Construction, and Outdoor Power Equipment

3,670 People Employed by Nebraska Dealers

MARKETING VIEW

CINDY FELDMAN, Marketing Director [cindyf@ineda.com]

MARKETING

WHY COMPELLING HEADLINES ARE CRITICAL FOR NATIVE ADVERTISING SUCCESS

In today’s digital landscape, native advertising (paid ad placement that appears in the same format and style as the non-paid content where it’s placed) has emerged as a powerful tool for marketers to reach their target audience seamlessly. According to research conducted by eMarketer, native advertising spend increased from about $100B in 2023 and is expected to hit over $110 billion in ad spend this year. And with good reason: native advertising offers a non-intrusive way to engage customers by blending in with surrounding content.

However, with the increasing volume of content bombarding users, it’s necessary to have compelling headlines to make sure your target audience is reading what you have to say

Here are a few tips that can help make you stand out…

• Consumers are often driven by their pain points and needs. By offering a solution in the headline, ag marketers can explicitly address these concerns, instantly capturing the attention of their target audience. “How X Product Can Increase Your Harvest Yield by 50%” is an example that promises a solution to a problem they are facing, and thus is more likely to have readers engage further with the content.

• You are probably well aware of content that uses headlines that start with “Top 10,” or “5 Reasons Why,” or “3 Pre-Trade Deadline Moves the Guardians Should Make,” (for example). Why do you see it so often? Because it works!

• People are more willing to check out content with a set number of key points because it provides a clear and structured format that is more likely easy to scan and comprehend quickly. The next time you’re preparing your native advertising content, make sure you have a set number of data points to share.

• It may sound simple, but calling out exactly who you want to reach is something that is underutilized and very powerful way to entice readers when it comes to native advertising. Even in specific markets where it’s very likely that your products and services are reaching your target buyers, you still want to make sure that it’s for them. For example, you can be broad with a headline like “Midwest Growers Use This Pesticide…” or as specific as “Seed Corn Growers Use This Pesticide…”, and you’ll know that any clicks you receive are likely the ones you want to target.

• Similar to understanding your ideal buyer, using your most enthusiastic customers as the voice for your content is a surefire way to get readers’ attention. FCSA is a great example of this recently by highlighting a hay producer in Nebraska that they then used his testimonial in their ad. Usually the metrics of this type of ad will greatly exceed the benchmarks against other native ads.

As native advertising continues to thrive and evolve, incorporating these strategies will help ensure that your message cuts through the noise and reaches the right people at the right time, delivering meaningful results for your dealership!