17 minute read

Marketing: When You’ve Tried It All And Nothing Works!

When you think about ways to connect with younger generations, it may be helpful to consider these tips.

Commit to a strategy and be consistent in order to be successful in marketing to new clients.

By Julie Genjac

Financial professionals often feel as though nothing works when it pertains to a seamless marketing strategy that attracts new clients to their practice. I have heard “I’ve tried it all and nothing really works!” more times than I can count.

My team at Hartford Funds and I recently conducted a study that examines how investors of different genders and generations want to receive financial advice and marketing materials. We understand that the next generation of clients has more options than ever when it comes to financial advice, so it is important for financial professionals to have a buttoned-up approach.

To create an organized marketing plan that will attract younger generations of clients, consider the following tips.

Commit To A Strategy

This is a phrase that I repeat multiple times per day. I am a true believer that financial professionals can work to enhance their email marketing and social media plans by truly focusing on and committing to one strategy.

I recently had a conversation with a team whose members felt as though nothing was working with the plans they put into place, so I asked them to describe their strategy to me. It was a little bit of this, a touch of that, a pause, then a restart. This was then

followed by some talk of using LinkedIn, some website and some email. What their strategy didn’t have was consistency.

Here’s the analogy I used with this team: If you set out to lose 10 pounds and you work out for one day, don’t work out the next day, do half a workout on the third, binge on cake on the fourth, and then go back to a light workout on the fifth (and repeat), you will be frustrated at the end of the month when you either haven’t lost a pound or have actually gained one or two. Consistency is key. Apply this same thinking to your business plans. Consistent, repeated implementation is crucial to ultimate success.

For example, when you think about ways to connect with younger generations, it may be helpful to consider some of our findings. We found that 42% of younger consumers are attracted to lifestyleoriented materials that highlight how

sound investment advice and decisions can support their lifestyle goals. This compares to 25% of older consumers. Could a member of your team focus on engagement activities related to life, balance or leisure to attract young adults?

In addition, our study found that design is also important. Content that is colorful and engaging resonates with 28% of younger consumers, compared to only 10% of those from older generations. Although these details are just that — details — they ultimately can impact your marketing strategy’s reception.

Younger and older generations have both similarities and differences in the types of content that drive them to engage with a financial professional. Younger Generations

Older Generations

Easy to understand Lifestyle-oriented Focused on how a plan caters to individual needs

53% 42% 40%

Product- and performance-oriented

29%

Information-heavy

29%

Design-oriented (colorful and engaging) 28% Relationship-oriented

20% 52% 25% 36% 28% 23% 10% 15%

Source: Hartford Funds survey

Your Strategy Must Have Only One Owner

Now that you have your plan in place, who will take the lead? Do you have a teammate in mind to follow up on the next task? Do you have a main point of contact? These are important questions to discuss with your team before taking any next steps.

Assign one person on the team who is responsible and held accountable, even if it’s you. I always say the most dangerous word on a team is “we” because it is nearly impossible to hold “we” accountable: “We should do this.” “We should do that.” When those actions aren’t executed, it is easy to hide behind “we didn’t get it done.”

In order to take something from a great idea on paper to a great idea in execution, designate one person on your team to own it, and make the rest of the team aware of who is overseeing it. This way, the point person is the central repository for ideas, setting the strategy and executing, and each member of the team can articulate the plan.

I hear numerous success stories about how making this small change to the process has yielded results. It’s amazing how quickly something like marketing can be set aside when markets change, tax season arrives, client emails and phone calls increase, or any of the other peak times in a practice occur. Accountability and ownership are key elements of a successful strategy.

Be Patient With Your Strategy

Creating a seamless marketing plan takes time. We all are inundated with email messages, mail, phone calls, social media ads, etc. A name or a theme must be in front of people multiple times before it catches someone’s attention. And a haphazard, tryeverything-for-a-short-time approach will not capture the attention you want.

Commit to a certain period of time to execute your strategy. Will it be one quarter, six months, a year? Be sure to build a written plan, track the execution of activities and keep track of results. Be willing to adjust and be nimble, but don’t become frustrated if you don’t see overwhelming results immediately.

Use this time as a learning experience as well. For example, our study also showed that when it comes to receiving marketing or prospecting materials, consumers on both ends of the age spectrum rank email as their top choice (27% for younger generations vs. 32% for older generations). But beyond that, the desired channels for receiving materials ranked differently for younger vs. older consumers.

Do you have a team member who is interested in learning more about using social media for business or website design? If you’re looking to attract younger consumers, this may be the next step to take to achieve that goal. Giving yourself time to monitor results can help you better plan and shift your focus (if needed) to better engage with younger clients.

Persistence, repetition and consistency are essential to your approach. Those teams that see results will tell you that they went through their process time and time again before seeing those results. Had they given up early on in the process, they would have missed out on positive results in the longer term.

Committing, assigning ownership, and executing consistently for a period of time are the keys to marketing successes. Tapping into specific ideas through survey results and your team’s unique values is a key ingredient.

Sit down with your team and discuss all the things you’ve tried over the years. Did an element of a plan work, or did it work so well that you stopped doing it? We all have those elements in our life — those habits or processes that fall off the radar over time, just because. Be honest with yourself, and determine what approach excites you and your team. Having true passion and energy behind your strategy will make a significant difference in your team’s ability to stick with the plan.

Julie Genjac is a registered representative of Hartford Funds Distributors. She may be contacted at julie. genjac@innfeedback.com.

DI Coverage: Insuring The ‘Golden Goose’

Clients may not be aware that disability insurance is income protection insurance.

By Ann Baker Ronn

Discussing income protection insurance with clients isn’t always a main topic of conversation. Many advisors don’t address disability income insurance with their clients. One common reason may be because clients often decline coverage; they never imagine something will happen to them, often not making income protection insurance a priority. However, according to the Social Security Administration, one in four of today’s 20-year-olds can expect to be out of work for at least a year because of a disabling condition before they reach normal retirement age.

When broaching the subject to clients, I explain the importance of income protection insurance by asking this question: “How long can you financially sustain yourself without a paycheck?” Clients often state they could survive one or two weeks without a paycheck. This exercise helps them begin to grasp the importance of this protection.

Whether you are explaining the best form of personal income coverage to a new client or advising on current coverage with a long-term client, I encourage you to be properly educated on the topic to better serve your clients and equip them for future financial success.

When addressing income protection insurance with clients, explain it as income replacement if they’re too sick or too hurt to work. Coverage takes about 90 days to kick in. A general reference for the amount of coverage needed to replace income is 60%-70% of their take-home pay. If clients pay the premium after tax, benefits are received income tax free.

It’s helpful to mention to clients that this form of income kicks in if they are unable to complete the day-to-day duties of their occupation due to serious illness or injury. Not to be confused with critical illness insurance, income protection insurance is disbursed in monthly payments, whereas critical illness insurance is received as a lump sum upon diagnosis of a specific illness. Critical illness insurance is not defined by job duties but instead triggered by a specific qualifying illness.

Leverage Visuals To Boost Understanding

Beyond explaining what income protection insurance is and why clients might need it, it’s also helpful to use visual aids. To help put this topic in perspective, I often share an idea I learned at an MDRT annual meeting, leveraging a goose and her golden egg.

I have a toy goose with a golden egg that I pull out to display to clients. Then I tell them, “You are a goose, I am a goose. Think of yourself as a goose who lays golden eggs. The goose represents you and how hard you work every day to create golden eggs or, in your case, money that may be taken for granted. You purchase insurance for the valuable items in your life, such as your cars, jewelry and homes. If you total your car, you simply purchase another car with the golden eggs you keep laying. Yet if something were to happen to the goose, there is no other goose. That means there are no more golden eggs either.”

Visuals not only help clients understand complex subjects more easily but are also easier to remember than a verbal or written explanation. Explaining income protection insurance to clients with visuals such as this helps break down a more serious topic in a fun, lighthearted way. It also gets them thinking about what their family’s life might be like if something were to happen to the “goose.”

Convincing Clients It’s A Worthy Investment

into with clients is whether income protection insurance is a worthy investment. If a client is considering investing in income insurance protection, I use a chart to share with them how much money they will make while working by the time they reach 67. For example, if a client is currently 30 years old and earns an annual salary of $60,000, they will have earned at least $2,220,000 when they reach age 67.

However, if they didn’t invest in income protection insurance and were injured at age 30, their income wouldn’t be protected or replaced. Once a client sees a visual chart of their personal finances and understands how much money they will make while working — and how much they’ll miss out on if they can’t work — they realize income protection insurance not only insures them in their time of need but also ensures their financial trajectory isn’t derailed.

When assisting a client with their financial future, address the importance of having a stable income if they are unable to work. But also help your client focus on having the necessary resources to safely recover. For a client who is injured or ill, the recovery process can be arduous; they will need to focus on getting better physically, mentally and emotionally. Income protection insurance helps ensure clients have financial stability in the future while also providing peace of mind during uncertain times.

Ann Baker Ronn, CLU, ChFC, LUTCF, is the insurance director of AFP Group, an investment advisor representative with Ameritas Investment, and previously served as a member of the Ameritas Field Advisory Cabinet. Ann is the owner of Income Protection Solutions in Houston and a third-generation member of the insurance and financial profession. She has qualified for annual membership in MDRT and is a past Court of the Table member. She may be contacted at ann.baker.ronn@ innfeedback.com.

How Will Caregiving Impact A Career Or A Business?

Clients who are caregivers must be educated about options that work for them.

By Carroll S. Golden

Most statistics calling out the number of people involved in caregiving are rapidly becoming outdated. The necessity of being a caregiver can have significant financial implications for professionals, workers and, particularly, business owners. Financial professionals can help clients who are caregivers navigate these challenges. And as professionals and business owners themselves, these are challenges that advisors also may face.

The pandemic blurred the boundaries between the personal and the professional and fundamentally changed the social contract that governs today’s workplace. After seeing too many truly disturbing media images and hearing heart-wrenching stories, many people decidedly would prefer to age in place.

Arranging for care at home requires skills beyond those we may have acquired in our current employment. It is estimated that 95% of community-dwelling seniors today rely on help from unpaid family or friends. Being an employed caregiver, employing caregivers or living with a caregiver is quickly becoming the norm instead of the exception. Many businesses now employ a workforce that spans three, and in some cases, four generations — from career extenders to baby boomers to Generation X to millennials — many of whom are already involved in caregiving.

Planning Is Crucial

Juggling work and providing or supervising someone’s care is more complicated than just hiring someone to help (good luck finding a qualified, trained person). There also are the issues of wills, end of life directives and other documents (which no one really wants to discuss). Extended care and long-term care are expensive and can impact retirement savings. The time, energy and resources required to provide care can negatively impact a worker’s performance and can affect their own ability to retire comfortably.

Some 62% of caregivers who participated in an AgingCare.com survey say that the cost of caring for a parent has impacted their ability to plan for their own financial future. Family dynamics can add to stress and potential underperformance at work. Addressing the need and finding adequate and affordable options are challenging.

Solutions Are Available

In my recent book How Not To Tear Your Family Apart, I follow a fictitious family as they work to create a plan that will result in the main character, Jodi, finding options that will relieve her from the stressful juggling act of personal and professional responsibilities. As a member of the sandwich generation, Jodi has passed up a promotion and backs off from working on group projects since her time is not always her own. She stopped contributing to her 401(k) and instead started diverting those funds to a separate account dedicated to the cost of her parents’ care. She spends her lunch hour running errands related to her parents’ care and often shows up late to work looking exhausted.

Fortunately, she is not the business owner, for if she were, the impact on the confidence of her employees and clients likely would suffer as well. This case study uses this fictional family who works with an advisor/agent to explore various insurance, non-insurance and government programs. The study provides an overview of options to address extended and long-term care needs that work for employers, employees and family caregivers. It also covers strategies for initiating and sustaining difficult conversations that are necessary for good preparation.

Caregivers, especially those with additional professional responsibilities, must be prepared for the potential impact of caregiving on their lives and finances. It’s important to understand what resources are available and to have a plan in place that includes the entire family. Understanding how caregiving can affect the whole family, not only those receiving care, is an important part of any financial plan.

Since the pandemic, retaining the best employees includes caring about the physical and financial health of business owners and workers. To avoid the likelihood of extended and long-term care needs negatively impacting your clients’ careers or businesses, they must become educated about options that work for them. Offering solid guidance and advice is crucial to growing your business and protecting theirs.

Carroll S. Golden, CLU, ChFC, LTCP, CASL, FLMI, CLTC, is the executive director of NAIFA’s Limited and Extended Care Planning Center. She may be contacted at carroll.golden@ innfeedback.com.

A Path To Better Agent Retention

Seeking insights into the reasons why some advisors terminate while others remain and are successful.

By Kathleen Krozel

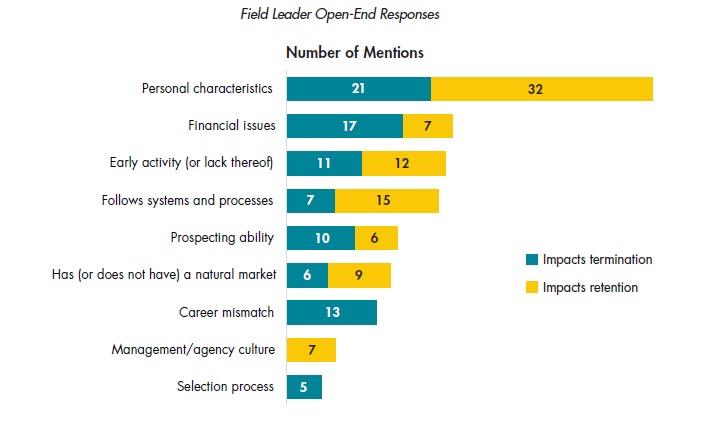

The life insurance industry has experienced a high turnover rate among financial professionals for many years. According to LIMRA research, in 2020, only 15% of full-time financial professionals remained with their hiring company after four years. The greatest portion of those terminations occur in years one and two.

To better understand the reasons behind low financial professional retention rates, LIMRA and Finseca surveyed field and home office leaders to gain insights into the reasons why some professionals terminate and why others remain and are successful.

Key Factors Affecting Retention

Our research finds a remarkable amount of agreement between home office and field leaders. Both groups identified five factors (out of a list of 12) they believe have the greatest positive effect on two-year retention: early activity (fast start), strong selection process prior to hire, joint field work, quality of sales skills training, and mentoring. This sends a strong signal that focusing on or investing more resources in these five areas could result in better outcomes for the industry.

It is no surprise that financial professionals who get off to a fast start are more likely to succeed. As a practical matter, less activity means fewer sales and lower income — a particularly high hurdle for new agents who lack a solid financial foundation coming into their careers. In fact, having a competitive financing plan, although rated below the “top five,” also is viewed as an important factor in overall success.

Field leaders frequently mentioned a set of personal characteristics they believe are key to an agent’s success or failure. They described these characteristics as drive, motivation, grit, self-discipline, work ethic and willingness to be coached.

However, personal characteristics can be hard to assess. The home office may be able to help field leaders objectively assess those attributes. If they are identifiable, it follows to invest more in recruits who demonstrate that they are coachable and have the drive to succeed by tracking and rewarding activities and the achievement of developmental milestones. Field leaders also believe that a lack of understanding about what the job entails can be a factor that contributes to termination. Considering most companies have a lengthy selection process (70% are longer than two months), it is particularly striking that field leaders cited this “career mismatch” as a significant reason for failure.

Perhaps precontract programs, which allow recruits to “try on” the career, are underused. Such a program could flag those who are clearly struggling with foundational aspects of the career such as prospecting and sales skills.

Another possibility is that recruiters’ narratives do not align with what the new candidate actually will be doing. In addition, younger generations may come in with a negative bias toward some of the industry’s terminology (for example, “insurance agent” or “commissions”). Using terms such as “financial professional” instead of “agent” or substituting “paid based on your performance” instead of “commission” may help with this. Spotlighting the “greater good” aspects of the career and moving away from a “sales job” mentality also could be beneficial.

While there is no one-size-fits-all solution to low financial professional retention rates, a combination of improved selection, early activity, quality sales training, and real-world experience through joint work and mentoring is likely to provide a pathway to success for new recruits.

Factors That Contribute to Financial Professional Termination and Retention

Personal characteristics Financial issues Early activity (or lack thereof) Follows systems and processes Prospecting ability Has (or does not have) a natural market Career mismatch Management/agency culture Selection process

Top 5 Factors Affecting Agent Retention

1. Early activity (fast start) 2. Strong selection process prior to hire 3. Joint field work 4. Quality of sales skill training 5. Mentoring

Kathleen Krozel, LLIF, FLMI, ARP, is research director, distribution research, with LIMRA. She may be contacted at kathleen.krozel@ innfeedback.com.