8 minute read

Annuities Provide Nourishment In An Income-Starved Environment

Adding an annuity to a client’s retirement portfolio can increase retirement sustainability as well as provide a legacy.

By Susan Rupe

Just as food sustains the body throughout its lifetime, an annuity sustains a client’s savings throughout their retirement. Just how important an income annuity is to the success of a retirement portfolio was the subject of a recent webinar by Tamiko Toland, director of retirement markets for CANNEX, and sponsored by the National Association for Fixed Annuities.

CANNEX looked at the use of annuity income incorporated into the fixed income allocation, and how that would affect the retirement portfolio sustainability. Among the findings: » The annuity improves the sustainability of savings throughout retirement.

» Characterizing the annuity as part of the fixed income portfolio can further benefit retirement outcomes, particularly when the portfolio allocation leans more toward the fixed income side.

» The annuity can increase retirement sustainability as well as legacy.

» Equity exposure contributes to both retirement sustainability and legacy.

These findings apply to any form of guaranteed lifetime income, Toland said, whether it comes from an income annuity or guaranteed lifetime withdrawal benefit.

The research looked at whether the retiree would run out of money over the course of retirement. In addition, the research looked at legacy, or how much money would be left over when the retiree dies.

Three different asset allocations were explored in the study.

» Conservative: 30% equity/70% fixed » Balanced: 60% equity/40% fixed » Aggressive: 70% equity/30% fixed

The researchers added annuity income in 5% increments starting at 0% and ending at 30%. Researchers looked at a scenario in which the annuity was separate from the remainder of the portfolio and a scenario in which the annuity was included as part of the fixed income allocation.

The percentage of annuity “based on the amount of money put into the annuity on the first day of retirement,” Toland said. “And for the purpose of the study, we used

single premium immediate annuities with a 2% inflation adjustment.”

The scenario considers a 65-year-old with $1 million in retirement savings who seeks a starting retirement income of $50,000. The income increases by 2% annually to account for inflation. The SPIA income amount is based on an average of the top three rates available at the time from a SPIA with a 2% cost-of-living adjustment a company rated at least A++ from AM Best. The rate using a $100,000 premium payment was $410 a month or $4,920 a year.

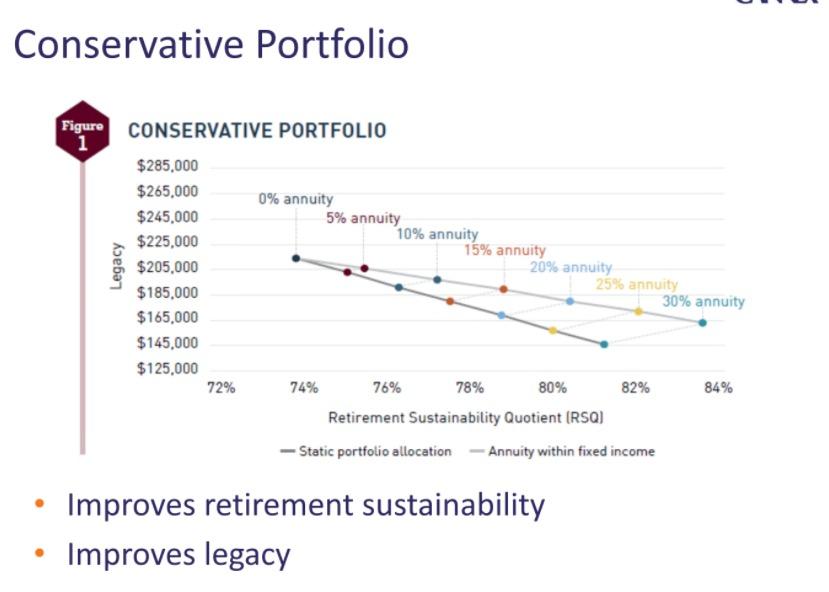

Conservative

In this scenario, the conservative portfolio has the highest allocation to fixed income, but it also benefits the most from adding the SPIA. Meanwhile, the SPIA reduces the financial legacy because it dedicates some starting assets to the lifetime income stream with no death benefit. “One of the things that I think is really important is the basic principle that by shifting the annuity into the fixed income allocation, you’re able to fully allocate the rest of that portfolio into equities, as opposed to if it’s outside,” Toland said. “Then it’s almost like doubling up on the fixed income component.”

Balanced

The balanced portfolio has twice the equity allocation of the conservative portfolio. As with the conservative portfolio, adding the SPIA as part of the fixed income allocation gives a noticeable improvement to the portfolio.

Aggressive

Although treating the annuity as part of the fixed income allocation has a noticeable improvement on both the conservative and the balanced portfolios, it has little effect on the aggressive portfolio.

Overall, the findings support the idea that it makes sense to include guaranteed annuity income as part of the fixed income allocation of a retirement portfolio, Toland said. One interesting note, she added, is that much of the effect of this approach shows up in the legacy component and not in the income sustainability component.

She said the findings consider the effect of the annuity purchase on both the strategy’s ability to provide the target income over a lifetime (retirement sustainability quotient, or RSQ) and the size of the legacy.

This is true when simply adding the annuity or counting the annuity as part of the fixed income allocation.

“What I really wanted to focus on is the idea that characterizing the annuity as part of the fixed income portfolio can further benefit outcomes, particularly when the portfolio allocation means towards more towards the fixed income side,” Toland said.

“A lot of good customers for annuities are people who are very conservative-leaning in their investments, and they don’t want to take a lot of chances. But this strategy of including the annuity as part of the fixed income allocation enables the client to be able to have a higher equity allocation. So I think that there’s a general understanding within the industry among people who really understand these products and understand the fundamental dynamics — that not having enough of an equity allocation in a retirement portfolio has its own risks and simply protecting assets alone is not the only thing to consider.

“But protecting assets does allow you to take that risk. And this study is very helpful, I think, in demonstrating how much of an effect that can have in terms of improving outcomes, particularly when clients are conservative in their investments.”

Susan Rupe is managing editor for InsuranceNewsNet. She formerly served as communications director for an insurance agents’ association and was an award-winning newspaper reporter and editor. Contact her at Susan.Rupe@innfeedback.com. Follow her on Twitter @INNsusan.

Health Ministry Leaves 10K Families On The Hook For Bills

About 10,000 families have ended up with more than $50 million in unpaid medical bills after their health sharing ministry shut down.

Sharity Ministries, formerly known as Trinity HealthShare, filed for bankruptcy in late 2021 and began the liquidation process. With so many outstanding claims against the ministry, it is unlikely that its members will receive the reimbursements they are owed.

Sharity Ministries operated as a nonprofit that offered an alternative to traditional health insurance. As a health care sharing ministry, members pay premiums and voluntarily agree to share their medical expenses in accordance with their Christian beliefs, according to the company’s previous website. Fifteen states and the District of Columbia have taken actions against Sharity.

administration to get rid of a Trump-era rule that expanded the duration of shortterm health plans.

A collection of more than 40 House Democrats wrote to Health and Human Services Secretary Xavier Becerra calling for the agency to pull the rule. The action comes after more than 20 advocacy groups wrote to Becerra back in January asking for the rule to be eliminated or modified.

HSAS CONTINUE TO TREND UPWARD

Proponents of health savings accounts say the vehicle could bridge the gap in health coverage, and an increasing number of Americans seem to agree. The Employee Benefit Research Institute has a database of 11 million HSAs, with assets totaling more than $32.9 billion as of the end of 2020.

EBRI noted an upward trend continuing over the past few years, with average HSA balances increasing once again

— to $3,622. The average individual contribution decreased slightly from the alltime high observed in 2019, and employer contributions declined slightly as well.

EBRI found that account holders who live in disproportionately white or Asian ZIP codes, for instance, had higher average balances and higher average contributions than their counterparts in disproportionately Black or Hispanic ZIP codes. Also, male account holders made higher contributions and had higher balances, on average, than their female counterparts.

FUTURE OF SHORT-TERM HEALTH PLANS IN QUESTION

Democratic lawmakers and advocacy groups are trying to convince the Biden

The Trump administration finalized the regulation in 2018 for short-term limited-duration plans that can bypass requirements under the Affordable Care Act to cover preexisting conditions and essential health benefits.

The rule said that the 12-month plans can be renewed for up to 36 months. At the time, HHS said the plans were necessary to give consumers options, as premiums on the ACA’s exchanges were too high. However,

the insurance industry and consumer advocates charged that the plans offer skimpy coverage and can deceive consumers into believing they are getting more robust benefits.

QUOTABLE

Agents and brokers want to help consumers, but they also have to keep their doors open. If they’re not earning commissions, they may not be able to help those consumers.

— Marcy Buckner, senior vice president for government affairs at the National Association of Health Underwriters

MORE STATES EYE LONG-TERM CARE TAX

Twelve states are currently considering a so-called long-term care tax in an attempt to address the skyrocketing need for care in the future.

California lawmakers passed CA AB 567, which established a task force in the California Department of Insurance to explore the feasibility of developing and implementing a statewide insurance program for longterm care services and support.

Alaska, Colorado, Hawaii, Oregon, Illinois, Michigan, Minnesota, New York, North Carolina and Utah are currently considering state-sponsored long-term care programs.

Although consumers may dislike the idea of additional taxes, this trend will help drive a much-needed conversation about the costs and responsibility for long-term care, financial experts say. The opportunity this provides is for working people and their financial or insurance advisors to plan and be proactive before legislation is passed.

DID YOU KNOW ?