$ INFLUENTIAL VOICES IN October 2018 www.insightssuccess.com An Insight on the Opportunities in the Big Data Industry Industry Insight TheAge of Disruptive Banking through Digital Payment Solutions Digi-Payments

Simplifying Banking with a Distinctive Digital Solution

Brett

King Executive Chairman & Founder

Editor’s Note

The Better Option

Imagineanagedpersonfromlastcenturywhohaskepthisentirelifetime'searningsinhishouse.

Thereisnoonetolookafterhim,andthatholdingistheonlysourcetospendawealthylife ahead.Forsomereasons,onedayhewentoutofthetown,andtheretookplacearobberyor wildfire.Howwouldhesurvive?Eitherhehastorigorouslyworkinhisoldageorhavetoborrow somemoneydisowninghispridejustbecausehedoesnothaveanyotheroption.Hemaynothavea betteroptionbutwehave;TheBank.

Inthebelligerentperiodof21stcenturyeveryoneisnotblessedwitharichfriendwhocanhelp throughthebadfinancialtimes.Buttherearebankstodothetalking.Fromitsinceptionthebanking sectorhasbeenthehidden,vividlyunrecognizedfacilitatorbehindtherevolutionofmanyindustries. Wemaynotadmirebankloansbecauseoftheirburdeninginterestratesbutitisundeniablefactthatit isalmostimpossibletofulfillbusinessneedswithoutsignificantamountoffinancethatbank provides.Thesectorhastrulyembracedanincalculableamountofchangeinsociety.

Bankingisnotjustaboutlendingorborrowingthemoneybutmorespecificallyitisaboutmanaging, securingandmultiplyingyourmoney.Itsfinancialassistancehasbreathedasenseofcontrolinthe moneymatters.Whowouldhavethoughtthemoneycanbemultipliedbykeepingitinalockeror canbeexchanged,creditedordebitedfromanypartoftheworldwithoutkeepingitinapocket?The sectorhasboomedinfinitepossibilities.Itallowsmillionsofustopayforgoods,servicesandtransfer

moneywheneverandwhereverwewant.Providinglivelihoodsforhundredsofthousands familiesacrossthecountry.Inadditiontothisbankscontributebillionsofpoundsayeartoour publicservices,payingthesalariesofnurses,teachersandothervitalworkers.

Abovearethefewunquestionable,unparalleledbenefitsofbanking.However,wehaveto acceptthatbanksdidnotreceivedeservingadmirationfromthesocietyfortheircontributionto thelivelihood.Ifweareungeneroustowardsthecontributionofthesystem,whataboutits facilitators?Analyzingtheinefficiencyinfinancialmattersmanybankingenthusiastscameup withuniquenoteworthysolutions.Theirinfluencehassimplifiedseveralprocessesofbanking. Instigatingvarioustechnological,logisticaladvancementstheyhavetakenthefutureofbanking toanotherlevel.

Consideringtheirinnovationzenithanddedicatedeffortstowardsempoweringthebanking sectorInsightsSuccesshascomeupwithadistinctiveissue“The10MostInfluentialVoicesin Banking”whichrecognizestheincalculablecontributionofbankingenthusiastswhohas revolutionizedbankingprocesseswiththeirinventiveexcellence.

OurCoverFeatureadmirestheinspiringeffortsofBrettKing,anInternationalBestselling author,andExecutiveChairmanandFounderofMoven.Amobilefinancestrackingappthat updatesinrealtimeandonthego.Italsofunctionsasamobilebankthatallowsyoutoconduct instanttransactionsaroundtheworldusingyourphone.

Themagazinealsofeaturesworthareadcontributionofnineothervoicesinbankingwhose storiesandexpertisewillalsooverwhelmyou.Inadditionwehavealsoincludedarticlesfrom ourveryownin-houseeditorialteamandindustryexperts.Don'tforgettoflipthroughthatas well.

Let'sstartreading,shallwe?

Kedar Kulkarni

Digi-Payments The Age of Disruptive Banking through Digital Payment Solutions Simplifying Banking with a Distinctive Digital Solution Brett King What a tech CEO can teach your business about digital Industry Insight An Insight on the Opportunities in the Big Data Industry 48 Leader’s Desk Being confident about your future when your organization is designed for control Cover Story ARTICLE Unboxing banking Multiplying, Managing and Securing your Money Benchmarking Future 42 34 26

24 30 Alain Falys A Passionate Leader Empowering Banking Technic 22 Chris Skinner Demystifying the Financial World for You Joe Seunghyun Cho An Innovator in Banking Industry Matthias Kröner A Trendsetter Connecting Customers with Humanity and Transparency 38 Nektarios Liolios Advocating a Global Fintech Revolution40 Sankalp Shangari A Global Advisor for the Digitally Decentralized Financial Ecosystem 46 MessageSolution Technologies Compliance Transformation

sales@insightssuccess.com Corporate Ofces: October, 2018 Database Management Stella Andrew Technology Consultant David Stokes Circulation Managers Robert, Tanaji Research Analyst Chidiebere Moses Steve, Ben, Alan, Pranay Anish Miller Managing Editor Jenny Fernandes Art & Design Director Amol Kamble Associate Designer Kushagra Gupta Visualiser David King Senior Sales Manager Passi D. Business Development Executives Marketing Manager Ken Jones Executive Editor Assistant Editors Shubham Khampariya Art & Picture Editors Belin Paul Co-designer Vanshika Khanna Jayant John Mathew Business Development Manager Sales Executives David, Kevin, Mark, Ajinkya SME-SMO Executives Prashant Chevale, Uma Dhenge, Gemson, Irfan Online Marketing Strategists Alina Sege, Shubham, Vaibhav K Digital Marketing Manager Marry D’Souza Technical Specialists Amar, Aditya Technical Head Jacob Smile Copyright © 2018 Insights Success, All rights reserved. The content and images used in this magazine should not be reproduced or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior permission from Insights Success. Reprint rights remain solely with Insights Success. Follow us on : www.facebook.com/insightssuccess/ www.twitter.com/insightssuccess We are also available on : Insights Success Media Tech LLC 555 Metro Place North, Suite 100, Dublin, OH 43017, United States Phone - (614)-602-1754 Email: info@insightssuccess.com For Subscription: www.insightssuccess.com Insights Success Media and Technology Pvt. Ltd. Off. No. 513 & 510, 5th Flr., Rainbow Plaza, Shivar Chowk, Pimple Saudagar, Pune, Maharashtra 411017 Phone - India: +91 7410079881/ 82/ 83/ 84/ 85 Email: info@insightssuccess.in For Subscription: www.insightssuccess.in Kedar Kulkarni Contributing Editors Abhishaj Sajeev Hitesh Dhamani Editor-in-Chief Pooja M. Bansal

Brett King Executive Chairman and Founder Moven

Brett King Executive Chairman and Founder Moven

Cover Story

King

Simplifying Banking with a Distinctive Digital Solution Brett

You can be a bank without branches and without advisors today, but you cannot be a bank without technology.

Thereareveryfewpeoplewho

couldhonestlyclaimthatthey areincompletecontroloftheir finances.Whilethemajorityofushave usedbudgetingprogramsor applications,weoftendiscoverthat gettinginsightsfromthedataisnotas simpleasweareledtobelieve.

Untilnow,onemanisonamissionto makeyourmoneytalktoyou, whereveryouareandwhateveryou maybedoing.HisnameisBrettKing.

KingofFinancialInnovation

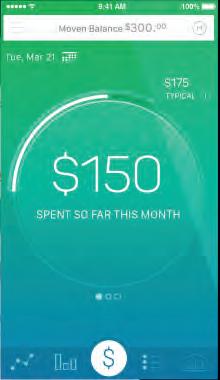

BrettKingistheExecutive ChairmanandFounderofMoven,a mobilebankingandfinancial managementappthatworksinreal time,evenforsigningup.Formany customersMovenfunctionsastheir day-to-daymobilebank,onethat allowsyoutoconductinstant transactionsaroundtheworldusing yourphone.

TheideaforMovencametoBrett,who isanInternationalBestsellingauthor, whenhewaspromotinghisfirstbook in2010.Thebooktitled Bank 2.0, dealtwiththeevolutionofthebank account,bankingingeneralandthe directiontheywereheaded.Whileon hisBank2.0booktour,askeptical seniorbankexecutivetoldBrettthatit waslikelynobankshadthecapacityor willtodeliverthetypesofserviceson whichthebooktouchedanytimesoon.

ThiswaswhereBrettfoundhis windowofopportunity.Healso recognizedthatamobileplatform mightallowhimtostrongly

One of the chief differences between Moven and the innumerable banking apps currently available is its focus on effecting real change in every user’s nancial habits.

differentiateanewsmartbankaccountaroundbehavior,financial health,digitalonboarding,andcustomeracquisition.Neverone toprocrastinate,Brettregisteredthedomain,MoveNBank.com (MoveandBank)thatverydayandcommencedworkonthefirst appprototype.

Movenwasestablishedthefollowingyearandthefirstseed roundin2012generated$2.5m.Theywentlivein2013with BrettastheCEO,apositionherecentlyrelinquishedtomove intotheroleofExecutiveChairman.Today,hecontinuestochart thestrategicdirectionofthecompanyandmaintainshisintimate involvementintheproductdesignprocess.

Thecompanyhasnowboughtinover$50minstrategicand venturefunding,createdadirectbankingserviceintheUSAand anenterprisesoftwarebusinessthatislicensingitstechnologyto banksacrosstheglobe,fromCanadatoNewZealand.Theyare currentlyfinalizingtheprocessofacquiringafullnationalbank charterintheU.S.

UnparalleledInsight

OneofthechiefdifferencesbetweenMovenandthe innumerablebankingappscurrentlyavailableisitsfocuson effectingrealchangeineveryuser’sfinancialhabits.

Thatisnotjustathrowawaymarketinglineorapipedream –statisticsrevealthatMovencustomerssaveanaverageof4-8% monthonmonthfromtheirpeersaftermigratingfromastandard debitcardissuedbyamainstreambank.

Rathercounterintuitively,thisisnotachievedthroughinterest ratesandpromotions,thetwomostcommontoolsusedby banks.Instead,Movenfocusesonunderstandingtheindividual andthenintelligentlyinjectingbehavioralpromptsand gamificationelementsintheapptoguidetheminsaving proactivelyonadailybasis.

Itisnotastaticprocess;theapplearnsasitinteractsandisable topredictthetimeofdayanddayoftheweekwhenauseris mostlikelytorespondpositivelytoaprompttosavebetter.In thisway,Moveniscreatingsmartsaverswhobecome progressivelyhealthierfinanciallythemoretheyusethe platform.

TheenterprisecomponentofMoventakestwoforms.Firstly, financialinstitutionscanuseitasthebasisonwhichtocreatea newstandaloneappormobilebankaccountofferingtohelptheir customersintheirquestforfinancialwellbeing.

Otherwise,theycantakeadvantageofMoven’sproprietaryapp components,convenientlycreatedasdiscretemodules,by

OnaverageMoven customerswhomigrate toourapp,saveabout 4-8%monthonmonth versusatypicaldebit cardfromamainstreambank.

insertingthemintotheirexistingapps.Thisgivestheir customersthesameremarkableinsightsintotheirfinancial behaviorenjoyedbyMovenusers.

PredictingtheFuture

Brettisabsolutelycategoricalinhisbeliefthatevery business,particularlyinthefinancesector,mustadopt technologytostayrelevantandcompetitive.

“Youcanbeabankwithoutbranchesandwithoutadvisors today,butyoucannotbeabankwithouttechnology,”he says,“Bankswhichrelyonbranchtrafficforrevenuewill beanendangeredspeciesby2025.”

Todemonstratethatthemarchtowardsatechnology-centric financialecosystemisinevitable,Brettcitestrendsfromthe pastfourdecades.

“WeintroducedtheATMmachinebackinthe‘80s,internet inthe‘90s,andmobilebankinginthe2000s.Thatisa steadyshifttowardsdigitaldistributionandengagementat thecoreofthebankingbusiness,andonewherewe’ve soughttoeliminatefrictionfromday-to-daymoney situations.”

“We’removingtoaworlddominatedbydigitalwitha focusonreal-time,low-latency,frictionlessdelivery.By 2025,morepeoplewillinteractwithabank’stechnology layerdailythantheydowithbranchesannually-if

branchesstillexist.Wewilljustexpectbankingtobe embeddedintheworldaroundusthroughtechnology, availablewhenandwhereweneedit.”

Brettalludestothisinhislatestbook, Bank 4.0: Banking th Everywhere, Never at a Bank,his6 bookandthethirdin theseriesbasedonthatfirstbookthatledtothefoundingof Moven.

“Centraltothefutureisthefactthatbankingisnolonger predominantlyaboutbeinggreatatbankingitselfbutrather aboutexcellingatbankingtechnology.”

Headds,“Aswemovetowardsembedded,ubiquitous banking,weareredesigningbankingbasedontechnologyledexperiencesandnottheproductsweusedtohaveata branch.Forexample,wedon’tneedplasticintheBank4.0 world.Youcanpaywithyourphone,sowhygetacustomer toapplyforaplasticcreditcard?”

“Insteadwe’lljustprovidecreditaccesswhenandwhere youneedit,instantly.”

However,Brettisquicktocautionthatitisnottechnology fortechnology’ssake,it’safundamentaltransformationof thebankingmodel.

“Thekeypillarsofthefuturereallyrevolvearound understandingwhenandwhereyourcustomerneedsyour platformandadviceasabank.Thiswillrequiretonsof data,artificialintelligence,andtechnologydelivery capability.”

“Muchofwhatwehaveconsidered‘core’tobanking–assetallocationandportfoliomanagement,riskprofiling, identity,frauddetection,smartcontractsfortradefinance, etc.–willbebuiltintoalgorithmsinthemediumterm.”

Theobviousconsequencewillbethatthebankerofthe futurewillbedistinctlydifferent,too.“Theskillsyouneed tobeasuccessfulbankerwillbereallyfocusedonbeing goodatthetechnologyofbanking.Thekeyrolesthatwill differentiatebankingtomorrowarethingslikemachine learning,datascience,behavioralpsychology,experience designandsoforth,”explainsBrett.

PersistenceandVision

WhilesomuchofwhatBretthaspredictedoverthecourse ofthepastfewyearsmayseemobviousinhindsight,his perspectiveandapproachcertainlyweren’tasreadily embracedwhenheintroducedthem.

Keypillarsofthe futurebankingreally revolvearound understandingwhen andwhereyour customerneeds yourplatformand adviceasabank.

Herevealsthathispitchesdidnotimmediatelyreceivethepositiveresponseithasnowbeenproventhattheydeserved.The factthatthenascentFintechsectorwassonewdidnothelp.

“Asastartup,therewereanumberofchallenges,thefirstofwhichwasraisingfinancing.I’dneverdonethisbeforesoitwas asuper-steeplearningcurve.”

“Secondly,findingtherightteamdynamicwasachallenge.Wehadissueswithteammemberswhowantedtochangethe strategicdirectionofthecompany.Thatthreatenedtodiluteourcentraldifferentiation;theyweretryingtoskatewherethe puckwastoday,nottomorrow.”

“Lastly,we’reinaregulatoryenvironmentintheU.S.thathasreallydonenothingtohelpFinTechplayers,sowe’vehadto breaknewgroundrepeatedlyalongtheway.Iguessthatisattheverycoreofbeinganinnovator!”

Nowthatthefirstseriesofspeedbumpshavebeenovercome,BrettandMovenfocusedfirmlyongrowthandexpansion. “Wehavepursuedbothachallengerbankmodelandanenterpriselicensingmodelwithonesingularobjective,togetourapp andexperiencesonasmanydevicesforasmanycustomersaspossible.Bytheendof2018,we’llhavemorethan5million usersacrosshalfadozencountries.By2019we’llmorethandoublethatagain.”

Headdssomeadviceforaspiringbankers,“Experientialdesignwilldramaticallyinfluencetheeverydayuseofembedded financialservicesandbankinginthenext10years.Youcanbecertainthatbankswillnotbecompetingagainstotherbanksin thisworld;theywillbecompetingagainsttechnologyplayers.”

Read my book Bank 4.0:

Banking Everywhere, Never at a Bank. It lays out a roadmap of key developments in the banking space over the next 10 years and how experiential design will dramatically inuence day to day use of embedded nancial services and banking.

Address : Country : City : State : Zip : Global Subscription Date : Name : Telephone : Email : READ IT FIRST Never Miss an Issue Yes, I would like to subscribe to Insights Success Magazine. SUBSCRIBE TODAY Check should be drawn in favor of: INSIGHTS SUCCESS MEDIA TECH LLC Insights Success Media Tech LLC 555 Metro Place North, Suite 100, Dublin, OH 43017, United States Phone: (614)-602-1754,(302)-319-9947 Email: info@insightssuccess.com For Subscription: www.insightssuccess.com CORPORATE OFFICE

CompanyName

FidorBank fidorbank.uk

Management Brief

MatthiasKröner CEO

LalaWorld lalaworld.io SankalpShangari Founder&CEO

FidorcomprisesofFidorBank,aEuropeanchallengerbank withacommunityconcept–FidorSolutions,atechnology partnerthathelpsbuildandrunbanksfromthegroundup–FidorFactory,anin-housecustomerengagementagency.

LALAWorldaimsatbuildingaGlobalDigitalDecentralized FinancialEcosystemtosupporttheinclusionoftheUnbanked, Undocumented,Micro-entrepreneurs,Studentsand everyoneelse.

LATTICE80 lattice80.com JoeSeunghyunCho Co-founder

Gavin meetgavin.com MatthijsNelemans Co-founder

MessageSolutions TechnologiesInc messagesolution.com

Movencorp moven.com

Startupbootcamp startupbootcamp.org

JoshLiang President

LATTICE80istheWorld’sLargestFintechHub.

Gavinisthefirstrisk-sharingserviceintheworld.Its technologicallyadvancedplatformensuresthatcustomerswon’t payanyup-frontpremiums,andclaimsaresettledrightaway.

MessageSolutionisanindustrytechnologyleaderincompliance archivingandeDiscoverysolutionsforon-premise,Cloud,and MSP/ISP-hostedmulti-tenantenvironments.

BrettKing Founder

NektariosLiolios CEO&Co-founder

Movenisamobilefinancestrackingappthatupdatesinrealtimeand onthego.Italsofunctionsasamobilebankthatallowstoconduct instanttransactionsaroundtheworldusingphone.

Startupbootcampelevatesstartupstoagloballevelbygiving themdirectaccesstoaninternationalnetworkofthemost relevantpartners,investors,andmentorsintheirsector.

FinanserLtd thefinanser.com

ChrisSkinner CEO

InternationalPrivate BankingSystems www.ipbs.com BruceG.Raine Owner

YoyoWallet yoyowallet.com AlainFalys Co-founder& Chairman

TheFinanseristheportaltotheknowledgebaseoftheFinancial ServicesClub.

InternationalPrivateBankingSystems,Ltd.providesprivate bankingandwealthmanagementsoftwarefortheprivate bankingsector.

YoyoWalletisafastestgrowingpaymentgatewaywith emergingbankingtechnic.

Pam Bateson is an expert coach and mentor in business, training others to Masters level qualifications and supervising coaches. She has worked within the healthcare, retail, hotels, construction, media, agencies, education and public sector. She specialises in Coaching, Mentoring, Employee Engagement, Change Management, Learning and Development and Organisational Design. She has worked with all levels in organisations from graduates to the CEO. She has designed change programmes that connect projects, outcomes, training and coaching. The performance outcomes have been outstanding. She is CEO and Co-Founder at Thrive Partners.

$ $ 18 October 2018|

About the Author

Pam Batesonset up Thrive

Partners, an on-demand coaching company, three years ago. In this article, she shares her point of view on how important humans are in a more digital world, what she’s learned as a tech CEO, and what this means when you’re looking to use tech in a way that’s both disruptive and works for customers.

$ $ 19 October 2018|

Benchmarking Future

InOctober2015,Igaveupasuccessful careerasamanagementconsultantand coachtosetupThrivePartners.Lotsof peoplethoughtIwascrazy.Iwas approaching50,withtwochildrenstill athome.Butforthedecaderunningup tothatdecision,I’dbeenthinking aboutabetterwaytodelivercoaching –supportedbydigital,tosharemore widelythecoachingtoolsI’dusedto helpclientsformanyyears.

ThiswasthebusinessIsetouttobuild threeyearsago. Today,we’reworking with25clientsonfivecontinents–deliveringourownbrandofondemandcoaching,backedwithinsights forthewholebusiness. Thelearning curvehasbeensteep–particularlyfor someonewho,bytheirown confession,didn’thavealotof experienceinlearningtechnology.So here,Iwantedtosharesomeofthe thingswe’velearned–andwhatit mightmeanforyourbusiness.

Dreambig

Ididn’treallysetouttobuilda businessthatwouldbeconsidered disruptive,butmybackgroundasa leanengineerandcoachdidmeanthat werippeduptherulebookwhenit cametothecoachingindustry. We scrappedtheideathatyouneededto meetfacetoface,andthatsessionshad tolastanhour,oreventwohours.And wemadeitaloteasierforpeopleto accessacoachtoanswerthequestions theyhadthereandthen–increasing accesssopeoplecouldchattoan expertwithinanhour.

Workingwithmyco-founder,wethen rebuilttheindustrybyaskingthe biggestquestionswecouldimaging. Whatifwecouldmakecoaching availabletowholeorganisations?What ifwecouldgetlisteningasvaluedas speaking?Andwhatifwecouldhelp organisationslearnasquicklyas individuals?

Ifoundthesequestionsirresistible:I wantedtodoforcoachingwhatUber haddoneforgettingataxi,Netflixhad doneforhomeentertainment,and

Tinderhaddonefordating.It’sthese bigdreamsthathavegalvanisedour successinthelastfewyears–and whichhassetusintherightdirection forthefuture.

Buildformodernusers

Despitebigdreams,we’vealsomade ourfairshareofmistakes! Alotof themmistakeshappenedwhenwetook ourattentionawayfromourend customers. Itsoundsobvioustoseeit thereonthepage.Butitcanbeeasyto losesightofthecustomersthatmatter most,especiallywhen,asatechCEO, sometimewegetpreoccupiedwitha shinypieceofnewtechnology.

So,whattoconsiderfirstwhenit comestousers?Themainthingtobear inmindisthattheyexpectexperiences thatareeasyandfasttoaccess–ashift broughtaboutbywhatwecallthe ‘AmazonPrimeMindset.’Inthisera, clunkyuserexperiencesreducethe chancesofuptakeofservices.Inshort, ifyourtechnologycan’tmatchor exceedthequalityofdigitalexperience peoplegetintheireverydaylives,then you’llneedtogobacktothedrawing board.

Createwinsforthemany So,ifuserscomefirst–whoelsecan weharnessthepoweroftechnology for?

Ouranswer?Everyoneelseinthe system.

Earlyoninthedevelopmentofour MyThriveplatform,werealisedthat deliveringdigitallywouldenableusto domorethanjustscaleandfacilitate coachinginglobalorganisations;it wouldalso meanwecouldspottrends andpatternswithincommunitiesof users,inorganisationsorsocietyat large. Justascarefullylisteninghasa powerfulandtransformativerolein one-to-onecoachingconversations, carefullylisteningtoandanalysing anonymisedversionofthe conversationswehosthasapowerful andtransformativerolewithinwhole organisations.

Thewhole-systeminsightswe producedhashelpedtomakesales processessmoother,improved communicationsandcreatedmore opportunitiesforpeopletolearn.

Keepithuman

Withsuicidebeingthebiggestkillerof menunder45,lonelinesssweeping throughdevelopedeconomiesin epidemicproportionsandathirdofall youngpeoplesufferingfromanxiety,I stronglybelievethatwehaveadutyto keeptalkingtoeachotherasasociety.

Webelievethatkeepingtheartof conversationaliveinthisdigitalageis essential;onlyhumanscanmaster creativity,empathy,humourand imaginationinawaythat’scompelling. Informationiseverywhere,sowe’re usingtechnologydifferently–tooffer realhumanexperiencesatscale,atany timeoftheday,wheneverourclients needaconversation,foreverything youcan’tGoogle.

Andwhatofthefuture? Curiously, eventhestructuresofartificial intelligenceandmachinelearninglook settomimichumanpatterns.It’sstill earlydays,butleadersinthisspace talkof‘deeplearning’withAI–by layeringupdifferenttoolsthatconnect inthesamewayasourbrain’sneural networks.

Andso,thenextthreeyears?

Myrecentexperienceshaveledusto askevenbiggerquestionsthanwedid tobeginwith–whichIsuspectwill leadtoournextirresistiblesetof adventures!Whatifwecould transformlearningmanagement systemsintolearningecosystems? Whatifanycommunityoflearners couldconnectwithanycommunityof teachers? Andwhatifabetter understandingofoutcomesfrom learningcouldhelpbothindividuals, organisationsandsocietytothrive?

Iforonebelievethereareexciting timesahead.

$ $ 20 October 2018|

Alain Falys:

A Passionate Leader Empowering Banking Technic

Alain Falys Co-founder & Chairman Yoyo Wallet

Todaytechnologyenthusiastsareemphasizing,withtheirknowledgeanddedicatedmindset,thetechnological revolutionapproachingthedigitalworld.AlainFalysisonesuchEuropeanentrepreneurwiththesecohesive personalitytraits.HeistheCo-founderandChairmanatYoyoWallet.Heisageekatheart,atechnologist,a businessexecutive,andaninvestorwithadeepunderstandingoffinancialservicesande-commerce.

AlainisalsoaPartnerat andafoundingLPatblockchainfundFabric.vc.HeisamemberofRBS’ Firestart.co Technology AdvisoryBoardandaDirectoratFintechcompaniesPelican.aiandOneLinq.nl.

Hepreviouslyco-foundedtheOB10globale-invoicingnetwork,whichfloatedinLondonasTungstenCorporationPlc.He wasSeniorVicePresidentatVisaInternationalandco-foundedOmnisMundi,ane-commerceincubatorwithoperationsin Frankfurt,BerlinandZurich,withsuccessfulstartupssuchasBuyVipsoldtoAmazonin2010.

AlainholdstheDiplômed’EtudesSupérieuresEuropéennesdeManagementfromtheNEOMABusinessSchoolandaBA HonoursdegreeinEuropeanBusinessAdministrationfromtheMiddlesexUniversity,London.

DeliveringSeamlessPaymentExperience

YoyoWalletprovidesacombinedandseamlesspaymentsandretailerloyaltyexperience,deliveringpersonalisedbenefitsto consumersatthepoint-of-sale.Initiallydeliveringpayment,aswellasretailer-specificloyaltycollectionandvoucher redemptiontoitsusersthroughabrandedappexperience,recentpartnershipswithStarlingBankandVisahasnowseenthe companyembeddingthesefunctionalitiesintoindividualbankingappstocreatethelevelsofengagementthatthoseinthe financialservicesindustryhavebeenstrivingfor.

$ $ 22 October 2018|

DigitalizingBankingTechnics

Inthecurrentdigitalworld,bankersneedtoreconnectwith whattheircustomersnowwant,requiringthemto constantlyremainup-to-datewiththeongoingtechnical revolution.Thevastmajorityofconsumersarenow ‘digitallynative’,andnotonlywantapersonalisedinstant bankingexperience,butalsotheabilitytoaccessthe benefitsthattouchtheirdailyconsumerjourney.Atthe sametime,bankersarenowhavingtoconsiderwhatthe expectationsofthenextgenerationofcustomerswillbetheabilitytoadaptaplatformquicklyisonlygoingto becomemoreandmoreimportant.

RenovatingJourneythroughKnowledge

Duringtheearlydaysoftheinternet,Alaincreatedoneof thefirstSaaSplatformsthatcompletelydigitizedsupplier invoicesbycapturingtherightdatatooptimizeaccounting functionalityforcorporatebusinesses.Dealingwiththe sheervolumeandrichnessofthedatathatcameoutofsuch aplatformre-enforcedhisviewtowardsitspower.

Extractingdataandbeingabletoquicklyidentifywhatis essentialiskeytomaximizingthecustomerexperience. ThiswassomethingAlainhadalreadyidentifiedintheearly daysofhiscareerwhenheranthecommercialcarddivision atVisaEurope.Histimetherehelpedshapehis understandingaboutthepowerofpaymentdataandthe paymentrailsbehindthatpaymentdata.

ContinuouslyEvolvingBanker’sRole

Bankersandbankshavebeguntorecognisethatinthisday andage,evenwiththebestin-housetechteams,theywill notbeabletowinnewconsumerswithhigherdemandson theirown.There’snowanobviousneedforpartnerships betweenestablishedbankingandfintechinnovation.Hence whybanksarebeginningtoincorporateexternal functionalityfromthelikesofYoyoWallet,eitherthrough thenewOpenBankingframeworkorindividualbanking initiatives.Thecompanybelievesitspartnershipwith StarlingBankwillbeseenasapioneeringmomentforretail banking.

EmployingEmergingBankingEnthusiastsforBetter Future

Everybankisnowsettinggoalstokeepupwiththis growingmarket.YoyoWallethasalreadypartneredwith StarlingBankandVisa,andthecompanyaimstointegrate

itsfunctionalityintomoretraditionalbankingappsfocusingattentiononthepersonalisationofthepayments experiencetocreateretailerloyalty,regardlessofpayment method.

There are very few moments in any industry sector where visible transformations take place. In banking, these moments usually come about when you see a combination of tech evolution, enhanced consumer expectations, and regulatory change. And it’s a moment when creativity can blossom. The banking sector is now going through one of these rare moments.

"And it’s not about replacing "traditional" with "emerging" - it’s about transforming what’s already there to create a banking experience that adds real value for the customer in a digital age," addsAlain.

‘‘ ‘‘ $ October 2018|

Fastest growing payment gateway with emerging banking technics. $ $ 23

Chris Skinner:

Demystifying the Financial World for You

Skinner Author & Commentator

Itwasaround2000B.C.whenthefirst‘banks’came

intoexistence,makingloanstofarmersandmerchants whocarriedgoodsbetweencities.Overthecourseof fourmillennia,mankindhascomeaverylongwayinterms ofwhatitexpectsfromthefinanceindustry.

Today,financialtechnologyallowsustoeasilyandsecurely sendandreceivemoneyandcommoditiestoandfromany partoftheworldwhilesittingatourdesks.Withthis conveniencealsocomescomplexityandtheaverageperson hardlyunderstandsthemechanismsbehindevensimple, everydaytransactions.

Onepersonwithanintimateunderstandingofthefinancial arenahasbeensharinghisknowledgeandinsightwiththe worldthroughhisbooksandblogs.

HisnameisChrisSkinner.

VariedExperiencesMakeGoodWriters

Anindependentcommentatoronthefinancialmarketsand onFintech,ChrisholdsadegreeinManagementScience andapost-graddegreeinInsurance,alongwithadiploma inIndustrialStudies. StartinghiscareerasaSalesManager,hehasheldseveral positionsinseveralprestigiouscompanies.Chrishasbeen

What will banking look like ten years from now, how will it work and who will make it happen?

‘‘

$ $ 24 October 2018|

Chris

writingblogsforoveradecadeandstillwriteseverysingle day.Hehasalsowrittenseveralbooksontopicsranging fromEuropeanbankingregulationstothecreditcrisisand evenonthefutureofbanking.

Chrisstartedwritingwhenherealizedthathehadthe abilitytotakeverycomplexideasandarticulatethemina conversationalway.Peoplelikehisbooksbecausethey tacklecomplicatedsubjectslikeblockchain, cryptocurrenciesandmachinelearningwhichare increasinglyrelevanttotheFintechindustryandexplain theminawaythatpeopleofallagescanunderstand.

Hislastthreebookshavebeenparticularlypopular. Digital Bank, whichcameoutin2014describesthechallengesof creatingatrulydigitalbankandthemethodstoovercome them.Hissecondbook, ValueWeb showedhowFintech firmsarebuildingtheinternetofvalueforIoTusingthe latesttechnologiesofapps,APIsandanalytics.

Chris’slatestbook, Digital Human showshowtechnology canbecomethebasisofinclusionforeveryoneonthe planet.Thisbookisexceptionalbecauseitalsosummarizes hisexperiencesoftravellingtheworldoverthelastthirty yearsandsomeoftheuniquediscoveriesintotheoriginsof humankindthatChrishasmade.

LessonsthatShapedhisJourney

ManyofChrisSkinner’sbookswerenotplannedbut insteadtriggeredbyparticularinteractionsandincidents. Digital Bank,thefirstbookthathewroteseriously,was conceiveduponarequestfromaclient.Atthatpoint,he hadbeenbloggingforadecadeanddecidedtotakehis postsandeditthemintochapters.

SincethenChrishaslaunchedafutureslabinNCR,the ATMCompanyinthe1990s,anetworkcalledtheGlobal FutureForuminUnisysinthe2000s,andalargenetwork calledShapingTomorrowwhenhebecameindependentin the2000s.

Hespendsaconsiderablepartofhistimelookingatthe futureoffinancebecausehesaysthatitis‘theonlything nobodyknows,buteverybodyisgoingthere’.This forward-lookingapproachbeganmanyyearsagoafterhe gaveapresentationataconferenceandoneofthefeedback formssaid,“Tell me something I don’t know.”

Chris’scurrentfocusonthefuturealsocentersonteaching othershowtomakemoneyfromit.

WitnessingtheChange

Chrisacknowledgesthattheroleofabankerhaschanged overtheyears,especiallyintherecentpast.Tenyearsago,

allbankerstalkedaboutwereregulationsandrisks;now, theytalkabouttechnologyandspeed.

Fastcyclechangecombinedwithcompletelytrustworthy riskmanagementisaverydifferentroletojustdoingrisk managementandthat’sthebigchange.

SageAdvice

Chrisadvisesaspiringfinancialexpertstonotaccept‘no’ forananswerandtochallengeeverything.Hebelievesthat ‘there are no dumb questions, just stupid answers.’

Heemphasizesthattomakeitbiginthefinanceindustry, bankersmustlearnhowtocodeascoding,orgainan understandingofitbecauseithasbecomeasimportant todayasbeingabletospeakEnglish.Thiswillhelpthem focusoncustomerexperiencethroughdigitalrelationships.

Enthusiastsshouldhaveapassionforthethingsfinance represents–economicsuccess,wealth,power–andhow technologyisdemocratizing,decentralizing,and redistributingassets.MoneyandTechnologyareatodds witheachother,andtoday’sbankerneedstounderstand thatdivideandbridgeit.

LookingtotheFuture

Fromapersonalperspective,Chrisrecentlybecamea fatherforthefirsttimeandhismaingoalhasshiftedto givinghissonsthebestchildhoodanyonecanhave.

Fromabusinessperspective,hesaysthathisaimistoleave alastingmarkonthefinancialservicesindustryinitsroad todigitalization,somethingthatcanbearguedhehas alreadydone.

$ $ $ 25 October 2018|

Thewaypeoplemakepaymentsarechangingfasterduetotheimprovedintegrationofdigitaltechnology.Thishas

benefitedtheindustrywithincreasedcompetitionandconsumerdemands.

ThechangescanbewitnessedinTravel,E-commerce,HouseholdBillpaymentsetc.Therecentintegrationoftechnologyin paymentsolutionsmakestransactionsfastandseamlessandcanbedoneatthecomfortofyourhomes.

Althoughwearewitnessingaconsiderablechangeinthepaymentsolutionindustry,thereisstillaconsistentuseofthecash andcards,whichsolelydependsonthegeographicalsetting.Insomeplaces,peopleprefercashandcards,whileinother places,theyencouragethemoreuseofdigitalsolutions;forexample:TheUnitedStatesandCanada.Analysishasshownthat

$ $ 26 October 2018|

intheseareas,theyarelikelytoswitchcompletelyto technologyenabledpaymentsolutions.

Thepaymentsolutionprocesseswillbecomemore innovativebecauseofthefollowingdisruptivetrends;

· DigitalBankingandRemotePaymentApproval

Astheyoungeragedmassesareturninguptotechnology morethanthetraditionalmediums,thereisanotionthat mostpaymentsolutionswillbedonethroughdigitalenabledmediumsratherthancashorcheque.Thiswill resultinmoreengagementofmobilephonesanddigital softwareapplications.

Variousbusinessoutletsareacceptingmoreofmobile paymentwhichishelpingthemtoimprovecustomer experience.Theadditionofinstantalerts,appreciation notificationsandinstantpaymentdeliveryismakingthis innovationmoreinteresting.

· Customer-FocusedStrategyasaPriority One retained customer is one attained success. ~ Chidiebere Moses Ogbodo Customerexperiencepostbusinessencounteriswhat makesadifferenceintheindustry.Digitalbankingsolutions areimprovingthewaycustomersfeelaftermakingtheir payments.Inthepastyears,oneneedtostandinaqueuein thebankbeforetheycanmakeeventhesmallest transaction,buttheintegrationoftechnologyinnovationhas reducedthestresstothelowestlevel.Wecanwitness improvedservicesandinstantexpensemanagementwhich ishelpingeveryonethatisusingthismediumtostayabove thecrowd

· ImprovedCustomerSatisfactionthroughRewards

Acustomertendstocheckbackonthesales-personwho gavethematipordiscountafterpurchase.Thisisalso applicableinpaymentsolution.Afterpeoplemakesa purchaseonlineorevenviacardsandtheselleroffersthem acertainpercentageofdiscount,theywillalwayswantto comeback.Thegoodnewsisthatmostbusinessenterprises aresupportingthisideaincollaborationwiththefinance institutions.

· FinTechCollaborationandExpansionofNetworks

Theinnovationinpaymentsolutionisincorporating feasibilityofresourcemanagementbetweenthefinancial andnon-financialorganizations.Throughthisdevelopment,

theresultwillleadtoeasymergingofboththetraditional mediumofresourcemanagementconceptswiththerecent anddigitalizedconcepts.Variousfinancialorganizations thatmaynotbeabletohandletheprocessofmigrating fromthetraditionalformattothedigitalizedplatformfinds easeindoingsobypartneringwithtechnologycompanies.

Organizationalgrowthismeasuredbothinmarketvalue, infrastructureandtheextentoftheirnetworks.The integrationofdigitaltechnologyadvancesinpayment provisionshelpsespeciallythefinance-oriented establishmentstoeasilyexpandtheirreach,eventothe mosthiddenplacesintheworld.Thishelpstotouchthe livesofpeoplenomattertheclassandstatusanditrepays withtremendouscustomergrowth.

· ImprovedSecurityandPaymentbyCodes

Securityishugeconcernwhenmoneyisinvolved.People aresoconsciousandveryinquisitiveabouthowtheir moneywilltravelfromthesendertothereceiver.Inso manycases,theywilleventhinkthatsuchplatformsas digitalizedmediumsarenottrustworthyasasinglewrong numbercandirecttheirmoneytounknowndestination. Thetransactionasoftheoldwastruecheques.Buttoday, therewillbealimitedneedforthosemethods,rather, paymentwillsimplybedonebyinputtingacertain usernameandpasswordandyourdashboardwillbeopened. Throughthispage,youcaneasilymakeeverypayment.The ageofdigitalizationisturningthewholeprocessintocodebasedandthisraisesthequestionofhowtostaysafe.Itis alsobelievedthatforsecuritypurposes,theinstant notificationoftransaction,linkingofsecuredemailand encryptiontoindividualdataanddisaster-recovery provisionswillleadtheinnovationtobetterdirection.This concernhasabigdealwithblockchain,augmentedreality, IoTandbiometrics.

Youmaybeaskinghowthefuturewilllooklikewithtechenabledpaymentsolutions.Astheworldisgrowingand globalizationisgainingagoodground,peopleblendsinto whattheyseethatisworkingwell.So,asdigitalpayment solutionismakingeventhelifeofthelaymanonstreet easy,morepeopleinthenearfuturewillcompletelyadopt thisinnovation.Itwillnotharmthefinancialinstitutions, butitwillbegreatiftheycanmigrateorbetterintegrate someformoftechnologystrategiesintheirfinancial solutions.Thischangemaybeslow,butitwillbeconsistent asthetechnologychangesarenotgivingroomfor procrastination.

$ $ 27 October 2018| Digi-Payments

Joe Seunghyun Cho:

An Innovator in Banking Industry

JoeSeunghyunChoistheCo-founderandFounding

CEOofLATTICE80andCo-founderand ChairmanofMarvelstoneGroupwhichowns 100%ofLATTICE80.Joeisanentrepreneurandhedge fundmanagerwhohasbuiltacoupleofassetmanagement companiesandworkedonfinancialinstitutionM&Adeals directly.

Joe’sroleinLATTICE80istoopenoperationsinmore citiesandbuildaglobalnetwork.

Joediversifieshisbankingsolutionsintwoanglesamong whichfirstoneishiscloseworkwithFintechsvia LATTICE80platform.Byworkingwithcreative entrepreneurs,Joeandhiscompanyalwayshaveaccessto newideasandinnovations.Secondangleistheirfocuson socialangles.Joeandhisteamarespecializedandfocused inemergingmarketsolutionsandserviceswithsocial impact.

JourneytowardsInnovativeFuture

Asanentrepreneur,Joe’sjourneyhasalwaysbeenbasedon hiswayofcontributiontosocialimpact.Asastudent,he dreamedofworkingwiththeUnitedNations.Hehasbeen volunteeredinNepalasapartofhisKoreannational serviceforover2years.Inearly20s,hefoundhimself drawntowardsthefinancialworldandwonderedhowhe candirecthisskillstobringpositivechanges.

Joe’sfirstexperienceinbuildinganassetmanagement companyandquanthedgefundfromscratchgavehim manyvaluablelessons,andheconsidereditasan achievementtoanextent.Itwasbothenjoyableand challengingforhimtobeabletocreateanewbusinessas anentrepreneurandaninvestor.

Joe’ssecondventureofdevelopingafinancialgroupwith partnerstoacquirea$2Bdollarassetmanagementcompany wasanothersteppingstone.Theexperienceexposedhimto

newideasofhowinnovationcanbeincorporatedto optimizeresourcesintraditionalbusinessesovertime,and theimportanceofhavingateamwithasimilarlongterm visiontomakeitcometrue.

Thisledhimtohisthirdexperimentofbuildinganext generationfinancialgroup,MarvelstoneGroup.With LATTICE80,Joe,beingthegroup’sinnovationarm,brings theexistingecosystemsandstakeholderstogetheruptoa newlevelwhichbringsnewwavesofnewsolutionsand extendsthecompany’sfinancialreachtomoremarketsand untappedsegments.Itisimportanttocollaborateandgrow togethersothatJoeandhisteamcanmakeadifference.

th

Joerecentlyfinishedhis60 travelspending2weeksin Europeand2weeksinAsiawhichhasbeenquite challenging.ButJoewillcontinuehisjourneyasitiswith meetingFintechStartupsandotherstakeholderswhoare buildingthefutureofbankingandmakingtheworlda betterplace,ashefindsitbetterfortheinnovativefutureof bankingsector.

ChallengesthatEveryEntrepreneurExperience

AsperJoe’spointofview,itisexpectedthatevery entrepreneurfaceschallengeseverydaywhereexpected workchallengescanbemanaged,butfewusualthingsthat arenotdirectlyworkrelatedcanbemorechallenging. Peoplemanagementordevelopingaprogressivework cultureiscrucialforanygrowingstartup.Whileonecan countonhis/hertrustworthypeopletobethesupporters,it canbeobservedthattheremaybedistractorsandevenhave todealwithnewchallengeslikefakenewsandInternet trollingthesedays.ButJoeisfortunatetohavebothhis partnersashisstrongpillarsofsupport.

EvolvementofBankers

AccordingtoJoe,withascendinthenumberofpivotaland ground-breakingfinancialtechnology,theroleofbankeris

$ $ 30

October 2018|

continuallyevolvingandhastobechangedasperthe requirements.Asanewgenerationofcustomers(millenials) gearingupandchangingthedemands,bankerswillneedto evolvetofitintoanewcultureofcreatingtheright customerexperience,alongsideagreaterunderstandingon applicationoftechnologiestosupportthat.Joestatesthat, “I am lucky to be in the position to meet many Fintech companies all over the world. While Core banking is very much still the same, we see that technology is making banking more efficient and smarter.”Withthis,Joe mentionedChallengerBanksasanexamplefortherelative concern.

FutureAspire

Itisstillayoungprojectfocusingoninnovationand experimentation.Joe’sjobinthesecondyearistoenter morecitiesandbuildpartnershipsglobally.Hisnearfuture goalistoopenin10citiesandinitiatemoreproductsto bringmoreservicestostartups,investorsandcorporates alike,andasaFintechstartupandplatform,thecompany’s futuregoalistogetlistedeventually.

FormidableAdvice

Joedescribestheattributesthateverybankershouldpossess thewillingnesstolearnnewthingsandshouldbeadaptable tochange.Hefurtherexplainsthatbanksfacecontinuous pressurefromanever-changingglobalenvironmenteven thoughnobodyhasseensignificantdevelopmentsyet.Just bybeingopentochangeandnewsolutions,bankerswillbe abletostandoutamongtheirpeers.

Joe’sadviceistolistentothecustomersandtakeadvantage overtheexistingbankswithlegacysystemsforthe emergingbankingenthusiasts.

“Build the world’s largest network and grow via partnerships rather than competing.”

$ $ 31 October 2018|

Matthias Kröner CEO Fidor

Matthias Kröner:

A Trendsetter Connecting Customers with Humanity and Transparency

Individualswithentrepreneurial

mindsetsareoftendrawnto opportunities,innovation,andnew valuecreation.Entrepreneurial characteristicsincludetheabilityto takecalculatedrisksandacceptthe realitiesofchangeanduncertainty. Onepersonalitywithsuchamarvelous mindsetisMatthiasKröner,aleader indigitalbanking.

Startinghiscareerinthehotelindustry, Matthiasgainedadeepknowledgeof customerservice.Withhis entrepreneurialmindset,hefounded Germany’sdirectbankDABinhis thirties.Hethenventuredoutwhenthe companywassold,ultimatelycofoundingFidorBankin2009.Fidor fulfilledtheneedforanopenbankthat valuedtransparencyandgavevoiceto customers.Fidorwasstartedwitha uniquecommunityconceptthat enabledcustomerstoincreasetheir financialknowledge,sharetheirskills, askquestions,reviewproducts,and makesuggestions.Today,itisproudto countover750,000activecommunity members,andhasexpandedits activitiestocreatebankstogetherwith partners.

AsCEOofbothFidorBankandFidor Solutions,Matthiasdrivesallstrategic decisionstowardsscalingand expandingthegroupinternationally. Underhisleadership,Fidoris continuingtoflourishandhasdoubled itssizeyear-on-year.

$ $ 32 October 2018|

FocusedAimwithPlannedJourney

Matthias’sjourneyhasalwaysbeen centeredaroundlearning:whathecan learnfromhiscustomers,whathecan learnfromhismistakes,andwhathe candotokeephisgoalsfrontofmind. Consequently,Fidorhasadoptedan agileculturewherebyit’salways innovating.

Whenheestablishedthebank,it neededtoreachcustomerswithoutthe helpofhugefundsormarketing budgets.Therefore,thebankbuilta socialmediaanddigitalmarketing strategyarounditscommunitytobuild itsownbrandandreachcustomersin themosteffectiveway.

WithFidorSolutions,theneedwasto developinawaythatpromoted innovation.ThebankselecteditsB2B partnerscarefullytofocusonsuccess. Itnowworkswithbignames-whether theyarecorporationslookingfor solutionsorpartnerscomplementing Fidor’soffering,fromfintechstolargesystemintegrators.

ForthrightBusinessApproach

Thebankgivescustomersthefreedom tocreate. Withthisattitude,Matthias wantscustomerstomanagetheir moneythroughbeingabletodomore, notless.Hewantstogivefreedomand controlbacktotheconsumer,tocreate theirownfuture,whateverthatlooks liketothem.

Thisapproachgoesforbusinessestoo. B2Bcustomersshouldbeabletocreate theirownbanksandnotfeelheld hostagebytheirITcapabilities.

AccordingtoMatthias,techhasgrown somuchoverthepastfewyearsandis notshowinganysignsofslowing, hence,bankersmustbeabletobetter servicetheircustomersandfocuson beinganequalpartner,ratherthan dictatingterms.

ConnectingCustomersonaPersonal Level

Matthiasstronglybelievesinhavinga connectionwithcustomers.Forthat reason,Fidoraimstodesignsolutions

andofferingsthataredirectlyrelevant toitscommunity.Thebanklooksafter suchanapproachandalways welcomesfeedback.

Talkingaboutthevitalattributesthat everybankermustpossess,Matthias says, “A technologically-based mindset is essential. The reality is that, today, people don’t go to banks. They turn to their phones or tablets to bank online. So the question, and the challenge, is then how do we make this process frictionless and add value?” Hefurther adds,“Whilst banking managers have been focused on numbers over the years, there is now a need to change.

Leadership must now focus on creating the right culture to succeed. An agile structure that adapts to customers’ changing behaviors is a must”.

CustomizedServicesforthe Customers

Fidorcreatestechnologythataddresses theneedsofitscustomersthroughits threerobustpillars:

- Bank / customer co-creation:The bankworkstogetherwiththe customers,usingitscommunityasa platform.Customersshareinvaluable informationandrecommendationsthat drivethebank’sroadmapanddesign solutionsthatmakeanimpact.Fidoris currentlyworkingonnewfeatures together,withitscustomers,in responsetoPSD2.

- Co-entrepreneurial spirit:Thebank collaborateswithotherorganizationsto createnewbankingconcepts,andwith fintechstodriveinnovation.Thiscoentrepreneurialspiritfasttracksthe deliveryofinnovativesolutionsto customers.

- Cross-industry approach:Fidor doesn’tjustworkwithbanks,butalso withretailersandtelecom organizationstocreatebusinessmodels focusedonusecasesandcustomer valueforrespectiveverticals.Its knowledgeaboutthecustomersand theirlifestylesisbroad,andthe convergencebetweenbankingand

otherindustriesmeansthatconsumers canmoreeasilybankwithpurpose.

SolutionsfortheFuture

BelongingtoEuropeasahome market,Fidorisgrowingandbringing solutionstoitsbankandnon-bank partners,leveragingitsEUbanking licence.OutsideoftheEU,thebank focusespurelyontechnologyand adaptingitselftotherespectiveneeds ofdifferentmarkets.Forexample,the bank’sdigitalbankingplatform, fidorOS,isshariacompliantinthe MiddleEast,whereitisamandatory requirementforoneofitspartners, AbuDhabiIslamicBank.

Consumerdemandsareevolving rapidly.AsFidor’sbusinessmodel continuestoevolvetomeetthese needs,thebankisfocusedonmaking consumers’experiencesbetterthrough itsmarketplace.Thismarketplacestore givesconsumerstheopportunityto discoverfintechandbankingofferings theycantrust,andhelpthembuild theirwealthwhileenablingbanksto innovateanddiversifytheirofferings.

$ $ 33 October 2018|

The reality is that people turn to their smart device everyday - why should banking be different?

An Insight on the Opportunities BIG DATA INDUSTRY

Inthiseraofchangingtechnologies,theBigData domainhasevolvedinaveryshortperiodoftime.It playsthemostpivotalroleacrossallindustries.The abilityofBigDatatominecriticaldatahasradicallyaltered thedynamicsofthewaybusinessesfunction,drivesales, andattractcustomers.Ithasbecomeanessential componentofbusinessstrategynowadays.Abusinesstastes successbyuncoveringinsightslockedinsidedata.The overlayingtrendswillexaminetheevolvingways enterprisescanrealizebetterbusinessvaluewithBigData andhowimprovingbusinessintelligencecanhelp transformorganizationalprocessesandthecustomer experience.Thereisademandforbetterdatamanagement frommostofthebusinessexecutivesforcomplianceand increasedconfidencetosteerthebusiness.Itwillhelpthem inmorerapidadoptionofBigDataandinnovativeand transformativedataanalytictechnologies.

Insight-drivenOrganizations

Inthispresentyear,businesseswillmovebeyondjustdata handlingtoleveragingtheinsightsthatBigDatauncovers. Asunderstanding,managing,andmanipulatingBigData hasnowbecomefairlyubiquitous,mostofthecompanies havetheabilitytodealwithit.Miningdatawillbethe centerofattractionanditwillhelpeffectivelytomeet organizationalrequirementsandforprecisetargetingof productsandservices.Aninsight-drivenapproachwill facilitateanevolvedcustomerexperience,competitiveness, advancedsecurityandoperationalefficiency.

CybersecurityApplications

Today,everyoneisdependentonthedigitaltechnologyand ourdependencehasreachedanunprecedentedlevel.Cyberattackshavealsobecomemuchmoreprevalent.An increasedoccurrenceofransomwarehasbeenregistered acrosstheglobeandcybercriminalsarenowtargeting personaldataanddevices.Concerningtheprimeindustry, cybersecuritycanonlybepossiblethroughbigdata

analyticswhichwillbecomeamajorareaofinvestmentand willgrowswiftly.Itisnecessaryfortheenterprisesandthe governmentagenciestoupgradetheirsecuritysystemsto next-generationsoftwarewhichcanaddressultra-modern securitythreats.

Analyticsacrosstheenterprise

Itcanbesaidthattheanalyticswillnotremainisolatedtoa fewdepartmentslikemarketingandriskmanagement.On theotherhanditwillinfusetheentireenterprise.To understandthedynamicsofbusinessoperations,data analyticswillbeutilizedandwillalsorevealwaysand meanstoincreaseefficiency.Hencetoderiveoverall businessstrategy,insightsfrommultipledepartmentswill beintegratedandredundantprocesseswillbeeliminated.It willalsohelpthedepartmentstoincreaseefficiency, growth,andproductivity.

Bridgingthetalentgap

Ifthedemandexpandsfurther,thetalentgapindata analyticswillsoar.Itisexpectedthatorganizationsand academicinstitutionswillcollaboratecloselytogenerate skillsandtalenttomeetthedemandfordataengineers.The functionsofallcorporateemployeeswillbeexpectedto understand,appreciateandworkwithanalyticssinceit emergesasoneofthekeyinstrumentsinevery organization.Theacademicinstitutionsarealsolooking forwardtoputtogetherdegreeprogramsindatascience.

IoTandPeople

TherewillbeatransitionfromInternetofThings(IoT)to InternetofPeople(IoP).Interactions,predictiveanalytics aroundhumanbehavior,andothersubjectiveareaswill growandstarttofilterallindustryverticals.Forexample, hospitalswillincreasinglydeploymachinelearning techniquestopredictthelikelihoodoftherelapseofa disease.Thiswillenablethemtoworkoutapatient’s readmissionpreciselyatthetimeoftheinitialdischarge.

$ $ 34 October 2018|

Business-sciencecollaboration

Businesseswillhavetolearnanddeploytraditional,scientifictechniquesofpattern-matchingandartificialintelligencefor analyticsusecases.Forexample,techniquestoanalyzegenesequencesinDNAarebeingusedintext-matchingalgorithmsto processbulkemails.Itisexpectedtoseeveryclosecollaborationbetweendatascientistsandthescientificcommunity. For example,imageprocessingiswidelyusedin‘tagging’insocialmedia,whilevoicerecognitionisusedinapps.

Technology

Therewillbebriskmovingintheorganizationsfromon-premiseplatformstocloudandhybridenvironments.Around44 percentofapplicationsusedbyFortune500organizationsarealreadyonthecloud,andmorethan50percentofIT applicationswillmovetothecloudbytheendoftheyear.Therewillbeariseindemandforanalyticstoolsthataresimple, flexible,andcapableofhandlingavarietyofdatasources.Hadoopenablestostoreanextremelylargevolumeofdataata significantlylowerpricepointandhenceitwillcontinuetobecomeincreasinglypopular.Theshareofunstructureddatain thedatawarehousewillcontinuetoincrease,whichwillfurthercauseforHadoop.Hadoop,now,ispastthebusiness relevanceandscalabilityassessmentphaseanditsadoptionisexpectedtoacceleratestrongly.

Weareadvancingtowardsacompletelynewerainthedomainofanalytics.Bigdataisdisruptiveandithaspavedtheway forpioneeringideasandinnovativetechniquesacrossindustryverticals.Itisnowdrivingthestreamofdisruptionand expandingthescopeofopportunitiesforpreviouslyuntouchedmarketsegments.OrganizationsneedtoleverageBigData analyticstoitsfullcapacitysoastothriveinthiscompetitiveworld.

Industry Insight $ $ 35 October 2018|

Message Solution

Message Solution Technologies Inc. Technologies Inc.

Compliance Transformation

MessageSolutionTechnologiesInc.has

historicallybeenrecognizedasatechnology innovator,creatingvaluefromunstructureddata. Assuch,MessageSolutionhasbecomeoneofthemost influentialvoicesinITindustryaswellasthebanking sector.

BasedintheSiliconValley,MessageSolutionfocuseson world-classcompliancearchiving,eDiscovery,backupand datasecuritysolutions.MessageSolutionmanagementteam iscomprisedofdedicatedprofessionalsfromIBMveterans toStanfordgraduates,thatprovideenterprisesoftware solutionsinvariousindustriesaroundtheglobe.

MessageSolutiondesignstheproductsandservicestobe scalable,robust,andcompatiblewithallmajoremailand filesystemstomeetclients’compliance,eDiscoveryand datasecurityneeds.MessageSolutioncatersitsplatforms andservicestobankingandfinancialpartnersfor companiesassmallas25employeesuptoglobal enterprisesaslargeas130,000users.Ultimately,the companystrivestoprovidesolutionsthatmitigaterisk, reducecostsandincreaseROIforitspartnersandglobal enterprisecustomers.MessageSolutionoperatesglobally withproductsdeployedin50countriesofproviding exceptionalservicesthatgarnercontinualgrowth worldwide.

BestofBreedComplianceandGovernanceSolution

MessageSolutionhasundertakenthetaskofbuilding unifiedarchivingandeDiscoverysolutions.Microsoft Office,ExchangeOn-premise,IBMDomino,andall enterprisefileenvironmentssuchasSharePointandOffice 365OneDriveareallsupportedbyMessageSolution platforms.

The2010Dodd-FrankWallStreetReformandConsumer ProtectionActaddedalayerofaccountabilityandmore costsofdoingbusinessinbankingsector,whichalso spurredmergeracquisitionactivity.MessageSolution addressesthenewdevelopmentandtheneedswiththe softwaresolutionsthatenablecompliance,reducelitigation

costs,andprovidesinstantaccountabilityofdigitalassets forlargeandsmallbusinesses.

Furthermore,MessageSolutionimplementedenterpriseclassfunctionsandfeaturesforglobalbankingentitiesfor communitybankstolargefinancialinstitutionstomeet globalcompliancerequirementsincludingFRCP,Frank Dodd,FINRAfortheU.S.financialorganizations,and GDPRforEuropeanmarketsandassociatedNorth Americanmarkets.

DeliveringHybridServicestoSME’s&Global Enterprise

Clients

MessageSolution’suniquePIIProtectionFramework (PersonalIdentifiableInformation)andinnovative architectureinenterpriseinformationarchivingand eDiscoveryaredesignedtosupportalargevolumeof unstructureddataforretentionmanagementanddatasearch inalllanguages.Scalabilityandvirtualcapabilityarethe company’sbiggeststrength.

MessageSolutionAdvancedeDiscoveryPlatformmakesit easytotrackandmaplegacyPIIfromemailandfileservers whileasecuredemailgatewayblocksandredactsOutlook emailssubjecttoPIIpolicies.TheMessageSolution PlatformalsoenablescomplianceofficerstoprotectPIIand privacyandprovidespermissionsforauditexportand searchanalytics.

ItisfieldproventheMessageSolutionPlatformcan concurrentlysupportover25,000activeusersper VM/server,whichwouldnormallyrequire5to6serversto dothejobbythe’leadingvendors’inthecompliance archivingeDiscoverymarket.Inaclusteredenvironment, MessageSolutionsavesenterprisesandISPs(Internet ServiceProviders)dozensofhardwareserver configurationsinadatacenteroperationoracloud environment.

Also,independentofathird-partydatabase,the MessageSolutionPlatformisavirtualappliancethatis installedovertheInternet.MessageSolutionisthefirstin themarketthathasdeliveredglobalsysteminstallationand configurationwithacompleteonlinedeploymentprocess, includingthemulti-geographicinstallationsacrossthe world.

AsaMicrosoftISVandcloudarchivingeDiscoveryvendor, MessageSolutionprovidesunifiedpoliciesforretentionand sharedaccesstoemail,fileservers,andSharePoint.This ensuresthatenterprisesandorganizationshavetheagilityto searchandaccountforallemailcommunicationandrelated filesondemand.

RedefiningBenchmarks

Initially,globalconglomeratesonlycollaboratedwith

$ $ 38

October 2018|

Josh Liang

knownproviderssuchasIBMorMicrosoft.Inorderto attractglobalprojectsandimplementation, MessageSolutiondesigneditsproductstobebold, advanced,andcapableofsupportingultralargeenterprise environments.Theproductdevelopmentteaminnovated moreadministrator-friendlyfunctionsandfeature-rich solutionstopenetratetheglobalenterprisemarkets.This processrequiredadditionaldevelopmentresourcesand commitmenttothemarketplace.Thankstoaninitial architecturaldesignthatfocusesonsupportinglarge environments,MessageSolution’sleading-edge technologieshavebeenimplementedbylargeenterprises, internationalbanks,andthe financialinstitutionsaroundtheworldtoday.

BeingClientCentricandaTrustedPartner

Recognizedbytheindustrysurveyforexcellenttechnical supportandservices,MessageSolutionhasbeenthefirst choiceoftheglobalcompaniesofallsizes.Evenaftersome enterpriseclientsmademultiplechangesinemailandfile environments(forexamplefromIBMDominoor GroupWisetoMicrosoftExchange,thentoExchange OnlineandOneDriveinMicrosoftOffice365),they continuedusingtheMessageSolutionPlatformbecauseof itscommitmentinprovidingadvancedtechnologiesin compliancearchivingandeDiscoverysolutions.

MessageSolutioneffectivelyhelpsenterprisecustomersstay incompliancebyprovidingthemostcost-effectivesolution inthemarketplace.Thecompanydemonstratesits commitmenttocustomers,andvaluesitslong-term relationshipwithglobalclients.

EnvisioningExcellence

MessageSolutionemphasizesonbuildingtrustand aintainingstrongrelationshipwithitsglobalpartnersand clients.Itsgoalistoexpandinthebankingindustryand embarkonmorechannelpartnerships,managedservice

providers,andsystemintegratorsinallmarketsectors.To achievethem,MessageSolutionwillcontinuetoimprove, build,andenhancetheirproductsandservicestoprovide excellenceinwhatitdoesbest.

What’sNext?

MessageSolutionhasbeenworkingwithbanksand financialinstitutionstoensureprivacyprotectionfortheir clients.AsofMayof2018,GDPRbecameeffective.Thus, MessageSolutionprovideditsEuropeanpartnersandNorth AmericanbusinessesthathavecustomersfromEuropewith compliancearchivingeDiscoveryservicestoprotectand stayingcompliantatthesametime.InJune2018,the CaliforniaConsumerPrivacyAct(AB375)waspassed, whichgivesconsumerstherighttoown,control,andensure thattheirpersonaldataisprotectedandsecuredinfinancial companies’storagedatabase.Tobesure,MessageSolution ispreparingtheirpartnersandclientswiththeadventof AB375.

CustomerSatisfactionandTestimonials

“MessageSolutionhasoneofthebestarchivingsolutionsI haveseenandIwouldliketocontinueonallbrowsers,it’s competitiveandeasytouse.”-PhilipAustin,Shiroki NorthAmerica,Inc

“ThedesignofMessageSolutionEnterpriseEmailArchive, particularlyitsremotesupportcapabilitythatreduces installationrequirementsandeliminatescostsassociated withon-siteinstallation,canreduceIT-relatedsupport costs.”-MichaelOsterman,OstermanResearch

“MessageSolution’sarchivingproductsareeasytouseand customersupportisexcellent.Customersupporthashigh satisfaction.”-GartnerMagicQuadrant2014

$ $ 39

‘‘

MessageSolution is the global technology leader in enterprise compliance archiving, eDiscovery, and data security—delivering in cloud, on premise, and service provider hosted platforms.

‘‘

October 2018|

Nektarios Liolios

AdvocatingaGlobalFintechRevolution

Takingintoconsiderationthedrivetotransformthe fintechecosystem,devisingcontemporary accelerationstrategies,democraticentrepreneurship qualities,andaknackforinnovation,NektariosLiolioshas beenrecognizedasaninfluentialvoiceinbanking. NektariosistheCo-founderandCEOof StartupbootcampFinTech,theorganizationbehindthe globalindustry-focusedinnovationprograms.

Workingtoaddresstherelationshipbetweencorporatesand startups,Nektariosworkscloselywithindustrypartnersand investorsaroundtheworldinkeyFinTechhubsincluding London,NewYork,MexicoCity,MumbaiandSingapore. Drivenbyentrepreneurship,collaborationandthedesireto changetheindustry,Nektariosisaglobalnomad,travel geek,andsneakerfreaker.

“SinceIsteppedintotheworldofFinTechinnovation almostadecadeago,onthesurfaceitappearsthatwehave comealongway,inreality,despiteallthenoiseand #fintecheverywhere,Iseesolittleofrealchange,”states Nektarios.Hehopesthatthiswillchangeoverthenext10 yearsascorporatesunderstandstartupsbetterandrealize thattheseproblemscanbetackled.

Nektariosalsocomprehendsthatbylisteningtoadvicefrom outsidetheorganization,basedonexperienceanddata, corporatescanstarttounderstandtheimportanceoftheir roleandhowbesttoapproachinnovation.

Addressingthemisinterpretedqualitythatstartupsdeliver, Nektariosexpresses,“Weregularlyhearbankscomplaining abouthowFinTechstartupsaren’tofferingtheright solutionsthattheycanplugdirectlyintotheirbusinesses. Manybigfinancialservicescompaniesjoinan accelerator/incubator/labaspartoftheirquesttofindthese mythicalproblem-solvingstartups,butwhenonestarts

Liolios Co-founder and CEO

Liolios Co-founder and CEO

Nektarios

Nektarios

$ $ 40 October 2018|

Startupbootcamp FinTech

diggingalittledeeperitbecomesveryclear,veryquickly thatthereislittleunderstandingofthevaluethatstartups canactuallyprovide.”

“Corporatesneedtounderstandthatstartupswillnotsolve alloftheirproblems.Itisveryraretofindanyonewhohas putinserioustimeandeffortintryingtobestrategicabout innovationbeforegettingstarted,”headds.

AccordingtoNektarios,whathe’smissingmostisthe recognitionthatthelargeorganizationsneedtoworkon themselvestobestartup-ready,inthesamewaytheyexpect thestartupstobeenterprise-ready.Heexpressesthatwhen askedhoworganizationsmeasurethesuccessoftheir initiativesorwhatsuccesslookslike,theresponsesare generallyalotofcorporatewaffle.

Healsoassertsthatmostoftheseorganizationsdon’t incentivizeinnovationacrosstheranks.“Sayingthat,we shouldgivesomecredittothosebanksthathavecreateda meaningfulinnovationstrategyandareembracing innovationbetterthanothers,butnoonehasreallycracked ityet,”headds.

Corporatesneedtodefinewhattheywanttochange internallyandacknowledgethatthiswon’thappenwithout investinginchangingthecompanycultureiswhat Nektariossuggests.EmbracinganR&Dmentalitywhich meanstryingmultiplethingsatthesametime,lookingat failingasanimportantpartoftheprocess,andtofindthe onethingthatwillactuallyworkisthekeytobringabouta change,accordingtohim.Moreover,buildingaportfolioof differentinnovationinitiatives,lookingatthedifferent innovationhorizons,butalso,beingpatientdoestherestof thework,hesays.

Nektariosassertsthatmoststartupsarenotaddressingthe issuesthatarecentraltoabank’sP&L.Banksshouldfocus onwhatthey’regoodat–beclearinwhattheircoreassets areandletotherssolvetheproblemstheycan’tfocuson.

“Stoptryingtodoeverything.Itgoesbacktosettinga clearerpath-figureoutwhattheendgoalisandcreatea roadmapthatwillhelpgetyouthere.Ifbankshadabetter ideaastowhattheywereactuallytryingtoachieve,they mightbemorepatientandbepreparedtoexperiment,”he advises.

Outsideoffinancialservices,someindustrieshavestarted togettheirheadsaroundthis.“Shouldwebelooking outsideofourownindustrytolearnhowtoaddresssomeof ourpainpoints?”asksNektarios.“Successandthereal evolutionoffinancialserviceswillcomefromrecognizing thatstartupscan’tsolveeveryproblem.Someexisting challengescanonlybeaddressedbytheincumbents.They haveto‘buildit’themselvesbutithastohappen,’startup-

‘‘

‘‘

style’,whilstcontinuingtoengagewithstartupsforallthe otherthings,”heasserts.

“Forthistohappen,aseriouschangeinternallywithin banksisrequired,anduntilthen,wewillcontinuetobe frustratedthatwe’renotevolvingasanindustryand keepingupwiththeneedsofthecustomer,”addsNektarios.

ARadicallyDisruptiveOrganization

Startupbootcampiscontinuouslygrowingandexpandingits globalfootprint.InFinTechalone,ithasplanstocontinue toexpandintonewmarketswherethepotentialtobepartof aFinTechhubisinforesight.Thecompanyisalso continuallylookingatnewwaystoengagewithcustomers bylisteningtothechallengesandpainpointsandbuilding newinnovationprogrammodelstohelpaddresstheirkey concerns.

Startupbootcampfocusesonfindingsynergiesbetween emergingandestablishedcompanies.Itfinetuneseach innovationprogramtoenablecorporate/startup collaboration.Thisallowsitspartnerstofindnewlinesof revenue,providesolutionsfortheircustomers,gain innovationinsights,improveinternalprocesses,and leapfrogcompetitionbyinnovatingfaster.

Eachprogramtheorganizationconductsissupportedby corporatepartnerswhoareofferedtheopportunitytogain accesstoaglobalpoolofearlyandlatestagetechnology startups.Thecompanytakestheguesswork,outofwhich startupwouldbethebestfitforeachbusiness.Partnersalso benefitdirectlyfromitsprogramsthroughinnovation initiativesaimedatassistingwiththeirowninnovation painpoints.

With Startupbootcamp, you gain access to the most relevant connections in your industry.

$ $ 41

October 2018|

Multiplying, Managing and Securing your Money

Abankisafinancialinstitutionlicensedtoreceivedepositsandmakeloans.Banks mayalsoprovidefinancialservices,suchaswealthmanagement,currency exchange,andsafedeposits.Therearetwotypesofbanks:commercial/retail banksandinvestmentbanks.Inmostcountries,banksareregulatedbythenational governmentorcentralbank.Banksactaspaymentagentsbyconductingcheckingor currentaccountsforcustomers,payingchequesdrawnbycustomersinthebank,and collectingchequesdepositedtocustomers'currentaccounts.Banksalsoenable customerpaymentsviaotherpaymentmethodssuchasAutomatedClearingHouse (ACH),Wiretransfersortelegraphictransfer,EFTPOS,andautomatedteller machines(ATMs).

Breakingdownthedifferentkindof'Banks’

Commercialbanksaretypicallyconcernedwithmanagingwithdrawalsandreceiving depositsaswellassupplyingshort-termloanstoindividualsandsmallbusinesses. Consumersprimarilyusethesebanksforbasiccheckingandsavingaccounts, certificatesofdeposits(CDs)andhomemortgages.Examplesofcommercialbanks includeJPMorganChase&Co.andBankofAmericaCorp.

Investmentbanksfocusonprovidingcorporateclientswithservicessuchasunderwritingandassistingwithmerger andacquisition(M&A)activity.MorganStanleyandGoldmanSachsGroupInc.areexamplesofU.S.investment banks.

Centralbanksarechieflyresponsibleforcurrencystability,controllinginflationandmonetarypolicyandoverseeing moneysupply.Someoftheworld'smajorcentralbanksincludetheU.S.FederalReserveBank,theEuropeanCentral Bank,theBankofEngland,theBankofJapan,theSwissNationalBankandthePeople'sBankofChina.

Whilemanybankshavebothabrick-and-mortarandonlinepresence,somebankshaveonlyanonlinepresence. Online-onlybanksoftenofferconsumershigherinterestratesandlowerfees.Convenience,interestratesandfeesare thedrivingfactorsinconsumers'decisionsofwhichbanktodobusinesswith.Asanalternativetobanks,consumers canopttouseacreditunion

RevenueGeneration

Abankcangeneraterevenueinavarietyofdifferentwaysincludinginterest,transactionfees,andfinancialadvice. Traditionally,themostsignificantmethodisviacharginginterestonthecapitalitlendsouttocustomers.Thebankprofits fromthelevelofinterestitpaysfordepositsandothersourcesoffunds,andthelevelofinterestitchargesinitslending

$ $ 42 October 2018|

$ $ 43 October 2018|

Unboxing banking

activities.Thisdifferenceisreferredtoasthespread betweenthecostoffundsandtheloaninterestrate. Historically,profitabilityfromlendingactivitieshasbeen cyclicalanddependentontheneedsandstrengthsofloan customersandthestageoftheeconomiccycle.Feesand financialadviceconstituteamorestablerevenuestreamand bankshavethereforeplacedmoreemphasisonthese revenuelinestosmooththeirfinancialperformance.Inthe past20years,Americanbankshavetakenmanymeasures toensurethattheyremainprofitablewhilerespondingto increasinglychangingmarketconditions.

LiquidityCreationandFinancialFragility:ATheoryof Banking

Loansareilliquidwhenalenderneedsrelationship - specific skillstocollectthem.Consequently,iftherelationship lenderneedsfundsbeforetheloanmatures,anindividual maydemandtoliquidateearlyorrequireareturnpremium. Borrowersalsorisklosingfunding.Thecostsofilliquidity areavoidediftherelationshiplenderisabankwithafragile capitalstructure,subjecttoruns.Fragilitycommitsbanksto createliquidity,enablingdepositorstowithdrawwhen needed,whilebufferingborrowersfromdepositors' liquidityneeds.Stabilizationpolicies,suchascapital requirements,narrowbanking,andsuspensionof convertibility,mayreduceliquiditycreation.

BattalionofSecurity

Ifyoulivepaychecktopaycheck,themostyou'reeverat riskoflosingorhavingstolenistheamountofyourlast paycheck–asumyouclearlycan'taffordtoloseifmoney istight.Keepingyourmoneysecureisparamount.And onceyouhavemorethanafewhundreddollarstoyour name,you'llwanttoprotectyoursavings.

Themostsecureplacetoputyourmoneyisabankaccount. AslongasyouchoosealegitimatebankthathasFederal DepositInsuranceCorporation(FDIC)insurance(ora creditunionthathasNationalCreditUnionAssociation insurance),anymoneyyouputinthebank(uptoFDIC insurancelimits)isprotected.Todate,theguarantee providedbytheFDIChasprovedtobecompletelyreliable, evenduringtimesoffinancialcrisislikethe2008recession orthesavings-and-loancrisisoftheearly1990s.

EraofInvestments

Onceyouareearningmoremoneythanyouneedtogetby eachmonth,you'llwanttogobeyondacheckingaccount andstartsavingandinvestingyourmoneytogiveyourself morefinancialsecurity.Withmoneyinsavings,youcan handleirregularexpenseslikecarrepairseveniftheydon't fitintoyourmonthlybudget.Alargeenoughemergency fundcantideyouoverduringaperiodofunemployment.

Andonceyouhaveseveralmonths'worthofemergency savings,you'llwanttotransferyourextrasavingsintoa retirementaccount.Yousimplycan'ttakeadvantageofthe opportunitytoearnmoneyinthestockmarketorearn interestondepositsifyou'reonlywillingtokeepyour moneyunderyourmattressoronaprepaiddebitcard.

RiskManagement

Asageneralpolicy,banksholdontocustomerdepositsto protectthemselvesfromfraud.Whenyoulookupyour bankaccountbalanceattheATMoronlineaftermakinga deposit,youmayseeadifferencebetweenyouraccount balanceandyouravailablebalance.Thisletsyouknowthat adeposityou'vemadehasn'tclearedyet.It'sextremely importanttobeawareofhowyourbank'sdepositholds policyworkssothatyouaren'tpenalizedfortryingtomake apaymentwithmoneyyoudon'tyethaveaccessto.The bank'sholdpolicywillalwaysapplytobusinessdays,not calendardays.Abusinessdayisanydaythatisnota Saturday,Sundayorfederalholiday.

AutomaticSavingPlans

Manybanksofferautomaticsavingsplans,andthesecanbe agreatwaytodeveloparegularhabitofsavingmoney.At somebanks,establishingsuchaplanisalsoawaytoobtain lowerbankingfees.Anautomaticsavingsplanissomething youneedtosetup.Itsimplyinvolveschoosingaspecific sumofanamountthatyou'rewillingtohaveautomatically transferredfromyourcheckingaccounttoyoursavings account,usuallyonceamonthandonthesamedayevery month(exceptwhenthatdayfallsonaweekendor holiday).Althoughsomepeoplearenervousabouttheidea ofcommittingtosaveacertainamountautomaticallyeach month,mostoftheinvestmentleaderssaythatpaying yourselffirstisakeycomponentofbuildingwealth.The othermajorbenefitofestablishinganautomaticsavings planisthatyoudon'thavetoremembertosetasidemoney forsavingseachmonth–yourbankwilldoitforyou.

TheBottomLine

Banksprovidesecurityandconvenienceformanagingyour moneyandsometimesallowyoutomakemoneybyearning interest.Convenienceandfeesaretwoofthemost importantthingstoconsiderwhenchoosingabank, whetheryouareopeningachecking,savingsormoney marketaccountorputtingfundsintoacertificateofdeposit. Besuretodevelopmethodstostayontopofyouraccount balancesinordertoavoidfees,declinedtransactionsand bouncedpayments.Toprotectyourmoneyfromelectronic theft,identitytheftandotherformsoffraud,it'simportant toimplementbasicprecautionssuchashaving complexpasswords,safeguardingyourPINandonly conductingonlineandmobilebankingthroughsecure internetconnections.

$ $ 44 October 2018|

Sankalp Shangari:

A Global Advisor for the Digitally Decentralized Financial Ecosystem

Sankalp Shangari CEO and Founder

Sankalp Shangari CEO and Founder

Backintheday,bankingwasindisputableandwasauniform business,whereclientelewasreliantonwhatthebanks offered;whereasinthepresentscenario,digitalizationhasled toacompletemodernizationinthebankingstructure.Disruptingthe traditionalbankingsystemisadigitalbankernamedSankalp Shangari,theCEOandFounderofLALAWorld,playing reformativerolesinthisdigitalera.Sankalpavidlyconfrontsnew competition,regulations,technology,customerexpectations, challenges,andopportunitiesinordertomeetthecustomer’s requirementsandexpectations.

AbouttheDigitalBanker

Atanearlystage,Sankalprecognizedtheworldofmodern bankingthroughhisformaleducationandhisprofessional experiences.Duringhiscareer,hepursuedMaster’sDegree inFinancefromtheCASSBusinessSchoolwhich polishedhisentrepreneurshipskillandcontinuedto understandabouttheinternationalfinances.Priorto LALAWorld,hegainedhisleadershipexperienceat MacquarieDeutscheBankandwithJPMorgan ChaseinLondonandSingapore. Thisexperienceaidedhimtoimbibethe characteristicsofrecognizingtalentsand employingthemtoachievethebestresults. Sankalpincorporatedthiswithhispassionfor Blockchaintechnologywhichledtothe establishmentofLALAWorldthatseekstouse technologytomakeasocialdifference.AstheCEOof LALAWorld,hisroleistoseekoutnewwaysinwhichtechnology canbeutilizedforalleviatingpovertyandalsotodevelopnew modelsforsocialbusinessthatcanhelpthesocietyatalarge scale.

ThePowerofCompassionandEmpathy

Duringhisinitialdays,eachofhisfamilymembershad residedindifferentcountriesandhadwitnessedthe problemsfacedbydis-advantagedandunbankedpeoplein

$ $ 46

October 2018|

thosecountries.Sankalp’smotherwasespecially empathetictowardstheseproblemsfacedbymigrant workers,whichcompassedhimtomoveherthoughtsand ideastowardsaworldofpossibilitieswhereallthesecould besolved.Hepushedhimselftoworktowardsrealizingher dreamwhicheventuallybecamehisowndream.

Intheyear2013,SankalpgotacquaintedwithBlockchain Technologyasatoolanddevelopedanewsetofideas whichbecamehislife-changingmoment.Finally,he comprehendedtheroadmapofbringinghismissiontolife whichwasnon-existentbefore.

ADecentralizedFinancialEcosystem

CurrentlyLALAWorldproductscanbeusedbyanyone whowantstoattainfinancialfreedom,sinceitsprimefocus hasalwaysbeentheunbanked.Thecompanyrealizesthat thebiggestchallengefacedbytheseunbankedpeopleis thatofanabsenceofcredibletransactionhistoryagainst whichtheycanavailloans.

So,allofthecompany’sbankingsolutionsarebasedonthe creationofauniqueidentifiercalledLALAID.Thiscanbe usedbyanybodyintheworldjustbyprovidingthemobile numberandemailidtoavailbasicservicesintheLALA APP.Further,byaddingmoreinformationanduploading documentsintheapp,theLALAIDcanbebuilttoactasa globalidentificationdocument.Thiscanalsobeutilizedby itspartnerserviceproviderstoavaildifferentservices. Apartfromthis,anotherfeaturethatsetsthecompanyina uniquespacefromotherbankingsolutionsistheLALA Score.Thus,bybuildingonLALAScore,anyunbanked canavailloansviaitslendingarmLALALends.LALA Scorerateseachindividualbasedonvariousparameters, andbasedonthisratings/score,theycanavailloans.

AchievingtheDream

Duringtheinitialphaseofestablishingthecompany, Sankalphadtofacespecificissuesrelatedtofindingthe rightpeopleforhisteamwhosharethesamevisionand whowouldworkwithhimpassionately.Secondly,finding someonefortheroleofanexemplaryleaderandmanager whokepthispeopletogether,recognizedtheirtalentand providedanexemplarygrowthpathtotheircareers.

Buildingateamofhard-workingpersonnelandsharingan equallevelofmotivationtoachievethegoalwasthe biggesthurdlethatheovercameinhisjourney.Today,the ‘LALAfamily’membersarestandingstrongbesideshim

andclockinginseveralhoursoftheirwakinglifetorealize theshareddreamofalleviatingpoverty.

DuetothecollectiveeffortsofLALAfamilyforovertwo years,hehasmanagedtoexpandthecompanyatan exponentialrate.Healsotakesprideinlaunchingthefirst ICO(InitialCoinOffering)thathasdelivereditsworking productswithin6months.

BequeathingtheKeysofSuccess

Nowadays,exhibitionofaspecificsetofcharacteristicsis expectedfromallbankers.Therearesomeskillsthatcould bedevelopedwithresilienceandpractice.Recognizingthis Sankalpsuggeststheemergingbankerstoespeciallypolish theircomprehensionoftechnology.Inaddition,he mentions, “If a banker is acquainted with new technologies and can incorporate those to enhance security, decrease costs and streamline banking processes, then that person can go a long way.”

EnvisioningtheFuture

Theultimategoalofthecompanyistosupporttheinclusion ofthe2.5billionunbankedpeople.Thisisahumongous taskfortheorganisationandhenceSankalphasdividedthe journeyintosub-goals.Theyintendtoachieveacustomer baseofonemillionby2019,provideloansofaroundUSD Tenmillionbytheendoffinancialyear2019andtheyare workingtowardsachievingthe100millionmarkin customerengagementbytheendof2021.

$ $ 47 October 2018|

Utilizing emerging technologies as a tool to successfully develop and run multiple social businesses for alleviating poverty.

Being confident about your future when your organization is designed for control

About theAuthor

Tames Rietdijk (1966) started his career in 1987 at KPMG as accountant (division financial institutions) and has been working mostly for software companies since 1994 in different positions from Product Manager to CTO. Since 2005 Tames has been certified as Anti Money Laundering Specialist by the Association of Certified Anti-Money Laundering Specialists (ACAMS) and he is a tutor at the Radboud Management Academy.

Tames is Chief Operations Officer at BusinessForensics and for the clients in the financial industry (banks and insurance companies) he is a trusted advisor for CFO's, CRO's and Fraud Departments because of his Risk management background combined with a thorough knowledge of software and technology.

In his vision on Risk management Tames calls for Risk based supervision instead of traditional Rule based supervision. Risk based supervision requires trend analyses with a total view instead of a snapshot of a specific event. For Risk management to be effective, more is needed than just detection of risks and that is the reason why the BusinessForensics platform offers a total solution in data mining, big data processing up until case management and sanctioning.

Duetoseveralincidentswithinthefinancialsector relatedtotheirintegrity,peopleandsocietyin generalhavelosttheirtrustinbanksandinsurance firms.Mostofthebanksandinsurancefirmsknowthis betterthananybodyelse.Regulatorsandsupervisorsare almostfuriouslytryingtorestorethistrustbyimposing strictrulesuponthemthatfocusonpreventingtheprevious incidentsfromhappeningagain.Eventhoughthismight winthemsomebattles,Iwilldefinitelynotwinthemthe war,astheissuestheyarestrugglingwitharefarmore complex:

Ÿ

Tryingtomanagetheirdata:volume,privacy, complexity,security,availabilityetc.Especiallyina contextoffinanceandrisk,additionalrequirements

Ÿ

applytotheconfidentiality,originationandaudittrailof data;

ReducingtheirITexpenses:keepingoldagedsystems up-and-runningisdifficultandexpensive,resources understandingthesesystemsaregrowingscarce,and suchasituationisdefinitelystallingITinnovations, wheretheyseemtoberequiredtoadoptnew technology;

Ÿ

Respondingtofindingsfromregulatorsand supervisors,whichneedtoberesolvedimminentlyat theriskoflargefines,negativecareerimplicationsor evenlicenseconsequences;

Ÿ

Replacingcurrentsolutionsbeing‘end-of-lifecycle’

$ $ 48 October 2018|