International Adviser INCLUDE: PANEL FOR THIS ISSUE:

AUTUMN 2022 ISSUE 90 FREE SUBSCRIPTION OFFER INSIDE The Leading Magazine For International HR Professionals Worldwide

HR

FEATURES

How Cost Estimates Will Help You Get The Best Out Of Your GM Programme Global Mobility In Times of Crisis Tax Risks Within The Assignment Lie Cycle Global Tax Update • EU Migration Law Updates 2022 Global Immigration Update Global Mobility Update The Evolution Of Remote Work ADVISORY

In This Issue

The 2022 Global HR Conference

How Cost Estimates Will Help You Get The Best Out Of Your GM Georgia Wilson, ECA International

Shaping Your Global Payroll Model To Align With Strategic Objectives Hayley McKelvey & Lee-Ann Kilroy, Deloitte Payroll & Workforce

Global Tax Update Andrew Bailey, BDO LLP

Tax Risks Within The Assignment Life Andrew Bailey, BDO LLP

EU Migration Law Updates Hugo Vijge, Vialto Partners

Global Immigration Raj Mann, Vialto Partners

Global The

2 INTERNATIONAL HR ADVISER AUTUMN CONTENTS 1 3 5 12 31

Invitation

Programme

Management

Cycle

2022

Update

Mobility In Times Of Conflict And Crisis

RES Forum The Evolution Of Remote Work Worldwide ERC The Impact Of Covid-19 On Global Mobility Deborah De Cerf, Employee Mobility Institute Directory While every effort has been made to ensure accuracy of information contained in this issue of “International HR Adviser”, the publishers and Directors of Inkspell Ltd cannot accept responsibility for errors or omissions. Neither the publishers of “International HR Adviser” nor any third parties who provide information for “Expatriate Adviser” magazine, shall have any responsibility for or be liable in respect of the content or the accuracy of the information so provided, or for any errors or omissions therein. “International HR Adviser” does not endorse any products, services or company listings featured in this issue. www.internationalhradviser.com Helen Elliott • Publisher • T: +44 (0) 20 8661 0186 • E: helen@internationalhradviser.com Ben Everson • T: +44 (0) 7921 694823 • E: ben@internationalhradviser.com International HR Adviser, PO Box 921, Sutton, SM1 2WB, UK Cover Design by Chris Duggan In Loving Memory of Assunta Mondello 28 9 19 23 Origination by Debbie Morgan and Printing by Gemini Group The International HR Adviser team work with a British planet positive printer, with a commitment to best practice environmental management including achieving the top score in Europe for the Green Leaf Awards, full FSC Certification, and ISO14001. Well managed sourcing of both virgin pulp and recycled papers, in addition to carbon balancing ensures that you can enjoy International HR Adviser with a clear eco conscience. 15 32

The 2022 Global HR Conference

On Monday 17th October 2022

at The Adelphi Building, 1-11 John Adam Street, London from 12.30pm – 4.45pm

For Senior Global HR Professionals only, this one day event will cover issues and topics specifically aimed at those managing their company or organisation’s global mobility.

Seminar Programme

Aligning GM Policies With Wider Business Objectives Concerning Sustainability And Inclusivity Agendas

ECA International will discuss how GM teams can adapt and modify mobility policies to:

• Broaden the succession talent pool

• Build more sustainable work practices for internationally mobile employees

Tax & Mobility Update

Update from BDO regarding tax changes and topical mobility issues & trends

Immigration Update

Vialto Partners' global advisory team will discuss the latest global immigration updates, trends and predictions pertinent to Senior Global HR Professionals and Global Mobility teams

Buying Mobility Software – Are you Horizontal or Vertical?

Replacing outdated vertical vendor and systems relationships with a horizontally integrated platform will save you time, improve the UX for your employees and improve data security for your company. Building on our latest article in the International HR Advisor, Tracker Software Technologies (TST) will explain how to achieve efficiencies and break down this topic into a manageable project and one that can be implemented in all organisations. Hosted by TST International

Remote Work - A Competitive Advantage In The Fight For Talent

With talent more willing than ever to leave for fresh opportunities, physical and virtual, is it time to take decisive action to attract and retain our global workforce in a human centric, purposeful and sustainable way? And if so, what can we do? Hear how we took a multi-faceted approach to implement remote working to transform our business, and how we hold our own experiences at the core as we continue to partner with our clients to reimagine their global workforce of tomorrow, covering the risks and opportunities of managing a remote working workforce across international borders.

Hosted by Deloitte LLP

To register your free place at this event that is organised by International HR Adviser, please email helen@internationalhradviser.com with the name/s of those who would like to attend, along with your/their job title and company name.

We look forward to seeing you there!

YOU ARE CORDIALLY INVITE TO

How Cost Estimates Will Help You Get The Best Out Of Your GM programme

It is no secret that international assignments and even permanent transfers can be very expensive, but does your organisation know just how much they are costing?

Monitoring and controlling the costs of assignments are both consistently a major concern for global mobility (GM) teams and their organisations –in fact, more than half of companies participating in ECA International’s latest Managing Mobility Survey reported that these are currently significant challenges for them. This is where cost estimates come in; they enable companies to determine how much potential international moves will likely cost before they begin. This insight is indispensable to different stakeholders across the business and is used for a range of purposes:

• Decision makers use cost estimates to assess whether a given assignment or permanent relocation is worth the significant investment, and to reduce the chance of unpleasant surprises further down the line. Companies may therefore choose to incorporate the preparation and sign-off of a cost estimate in their standard assignment process

• For the business unit bearing the expense, knowing the expected cost of an assignment means that it can be incorporated into its budget

• Companies are more likely than ever before to use a greater variety of international move types, and GM teams can use cost estimates to evaluate and compare different scenarios.

Traditional long-term assignments remain popular, but in some cases short-term assignments and permanent relocations are attractive alternatives. Even for longterm assignments, there are different types when it comes to pay – it can be calculated based on a home salary starting point (i.e. the salary for the equivalent job in the home country) or a host salary (i.e. the local market rate in the host

country). Some use the cost estimates to make comparisons between the cost of continued employment in the home location and the cost of an assignment. With many organisations having a stronger focus on the bottom line, looking at the different possible scenarios in advance can be a useful tool when GM is seeking management buy-in

• One of the key purposes of a GM programme is business enablement. Being able to accurately project costs to support the business in their daily operations will help GM managers demonstrate the value of their programme

• Many companies, particularly those in the construction and energy sectors, need to tender for projects that will require international assignments. Estimating labour costs is usually an important part of how companies’ bid teams calculate rates and safeguard margins.

The Building Blocks Of A Cost Estimate

Typically, costs are split into four components: salary, annual benefits, oneoff relocation costs, and tax and social security liabilities:

• For any type of assignment, salary and bonus payments make up a large part of the total costs. Where the assignee is entitled to additional allowances and pay adjustments as part of their assignment salary, these amounts are taken into account. Cost of living adjustments (i.e. COLAs) are usually provided for long-term assignments where the package is homebased, whereas an allowance to cover daily essentials is typical for a short-term assignment. Assignment allowances and location allowances are also often given. When the salary is host-based – and this could be the case for either a longterm assignment or a permanent transfer – then the gross salary to be paid in the host location is usually all that needs to be considered (and any bonus payments)

• On top of salary, other annual costs need to be considered as well. These are made up of ongoing benefits provided during the assignment (or, for permanent transfers, benefits provided during the first year).

Accommodation is usually the largest expense; in some locations, this can even exceed the cost of the salary. Other benefits that may be included are utilities, education for children, a company car, home leave, medical insurance and annual tax return preparation – and the costs incurred will depend on the assignee’s destination and the size of the relocating family. While the benefits provided will vary from one move type to another, this component still increases the package significantly

• Most companies also factor in the one-time costs incurred at the start of a move (and at repatriation in the case of assignments). Some of the more significant costs relate to the physical act of relocating an employee and their family to another location. As with the annual costs, costs for flights, shipment of personal effects, temporary accommodation, and other similar expenditure will vary considerably depending on the circumstances of the assignee and the locations between which they will travel. The relocation costs of repatriating should also be considered for assignments, though these will of course not apply for permanent transfers

• Finally, on top of salary payments, benefits and relocation costs, the thorny issues of tax and social security must be considered. Together these have the potential to make up a substantial proportion of the overall cost of a move. The elements of the package that are taxable and the rates at which they are taxed will vary depending on each host location’s fiscal law. When an assignee’s pay is home-based – for either a long-term or short-term assignment – their package is normally tax equalised. Their salary, benefits and relocation costs are quoted net and the company meets the income tax and social security contributions (employee and employer) incurred on these. When an employee is quoted a gross host salary for a long-term assignment, the employer usually still pays any tax that arises on move-related allowances, benefits, and relocation support. In permanent transfer cases, normally the employee is quoted a

3 GM PROGRAMME www.internationalhradviser.com

gross host salary and is required to pay any tax that arises on the additional benefits and relocation support provided, with the employer required to pay social security contributions due on the package.

The Benefits Of Knowing What Assignments Will Cost

Making cost estimates an integral part of the mobility process improves cost awareness and control. Often the only part of the business with a good idea of the total costs of an assignment is the GM team. Cost estimates allow better communication of these costs to relevant stakeholders in a clear and accessible way. This greater awareness inevitably improves cost control; faced with information on the significant outlay, the business unit bearing the cost will see it needs to be justified by a clear business rationale if the assignment is to go ahead.

Going further than cost control, if cost reduction is a priority, then demonstrating the full costs to the business can encourage the implementation of more stringent approval requirements for assignments. Being able to compare various scenarios will also enable the business to select the most cost-efficient move type. Where a choice of the assignment location is an option, a cost estimate will provide clarity on where to base the assignee.

Unlocking The Full Benefits Of Cost Estimates By Using Software

While cost estimates come with many advantages, creating them manually comes with challenges. It is typically timeconsuming to gather data from HR teams and a vast range of different vendors, not to mention that running the calculations themselves is intricate work and requires a certain amount of in-house GM knowledge. Mobility teams, especially those under significant time and workload pressures, may therefore not be in a position to run cost estimates regularly or consistently.

Software specifically designed for running cost estimate calculations removes such obstacles. ECA’s 2022 Global Mobility Now Survey found that 4 in 10 companies are already using software to automate calculations like cost estimates, whereas 5 in 10 say they are not currently automating these yet believe that doing so would add value for them – and for good reason. Cost estimate calculators already configured with mobility and tax data save considerable time and reduce the risk of human error. Clear and attractive outputs from a specialist system are also quick to share, and are much easier for other parts of the business to review and understand than large and detailed spreadsheet files full of

manual workings. Ultimately, transparency and easy communication is at the heart of why using cost estimates encourages better decisions and helps to hone businesses’ mobility programmes.

Key Account Manager, ECA International Georgia is part of ECA’s Client Services team and is responsible for some of ECA’s key accounts in northern Europe. She advises major multinational companies on current practices in global mobility, and supports the use and development of software solutions. To discuss cost estimates or other mobility-related issues: georgia.wilson@eca-international.com www.eca-international.com

GEORGIA WILSON

GEORGIA WILSON

4 INTERNATIONAL HR ADVISER AUTUMN www.internationalhradviser.com

The 2022 Global HR Conference Monday 17th October 2022 The Adelphi Building, 1-11 John Adam Street, London, from 12pm – 4.30pm ALIGNING GM POLICIES WITH WIDER BUSINESS OBJECTIVES CONCERNING SUSTAINABILITY AND INCLUSIVITY AGENDAS hosted by ECA International ECA International will discuss how GM teams can adapt and modify mobility policies to: • broaden the succession talent pool • build more sustainable work practices for internationally mobile employees Join us for this FREE one-day event aimed at Senior Global HR Professionals only. To register a place for yourself and your colleagues, please email helen@internationalhradviser.com with the names and job titles of those who wish to attend. We look forward to seeing you there!

Shaping Your Global Payroll Model To Align With Strategic Objectives

What is a ‘Global Payroll Model’? It can mean different things to different organisations; and for some, the desired Global Payroll Model is a distant dream. Employees are essential to all organisations, yet payroll, which connects the employee to the company, and which is often a material cost in the P&L has historically been construed as an overhead.

Now, with the ever-increasing role of technology and the growing complexity of global workforces, Global Payroll Models are at the forefront of HR and Payroll professionals’ minds.

A Global Payroll Model is a strategic framework typically developed to realise a desire for a single global payroll process, provider or system. An organisation’s payroll model should reflect its strategy, governance stance and the wider organisational operating model. On average, 80% of payroll processes should be the same regardless of location, with the remainder linked to specific country requirements. However, many organisations lack a consistent payroll model that underpins a global strategy, which, particularly post-pandemic, needs to support agile hybrid working scenarios.

There is no singular correct approach for operational payroll management, but organisations need to be confident that the model they select delivers a high-quality payroll

output across the workforce. Employees expect to be paid on a consistent basis, and delays can create workforce challenges (60% of employees have identified mistakes on their payslips and 21% of UK workers have changed jobs after being paid late(1)). Suboptimal payroll processes can impact both reputation and employee morale, often leading to longer-term consequences(2)

This article considers some of the options available to organisations that are reviewing their own Global Payroll Model or looking to establish one for the first time.

What Is A Global Payroll Model, And What Are The Options?

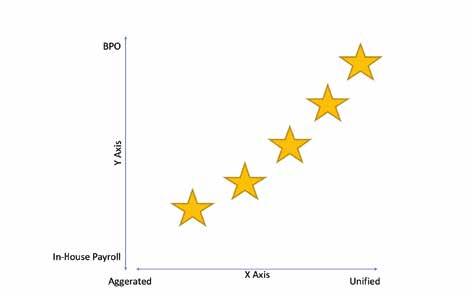

To echo an oft-cited phrase, ‘no one-size fits all’. There are numerous payroll models to accommodate a range of specific requirements. Organisations will be able to plot their operational model on a graph (Figure 1), showing:

• Y Axis – where the global payroll sits on the trajectory of being fully outsourced to a Business Process Owner (BPO) or managed internally (In-House Payroll)

• X Axis - the level of harmonisation of the global payroll itself, for example, are multiple countries’ data operated separately (Aggregated) or is there a unified global payroll model (Unified)?

There is no absolute correct model, but it is important to first understand the status quo and why this is the case.

The pros and cons of in-house versus outsourced have long been debated. For example, it may be argued that an in-house

team preserves flexibility and allows for shorter payroll turnaround times. Conversely, an advocate of outsourcing may say that this gives the organisation access to the latest technologies and removes the perceived key-person risk of an in-house environment.

The pros and cons of an aggregated model versus a unified global model are equally debated. For example, being able to view all data in one system under an aggregated model is powerful, but this does not allow the user to effect change for local payments. On the converse side, a unified system will give access to the local calculation, but this may be in a different report format meaning different gross to nets in different languages.

It’s horses for courses in determining the optimal position on the Operational Model graph. However, what is critical in assessing a change to a global model or, indeed, the inception of a new global model, is knowing the drivers for that change.

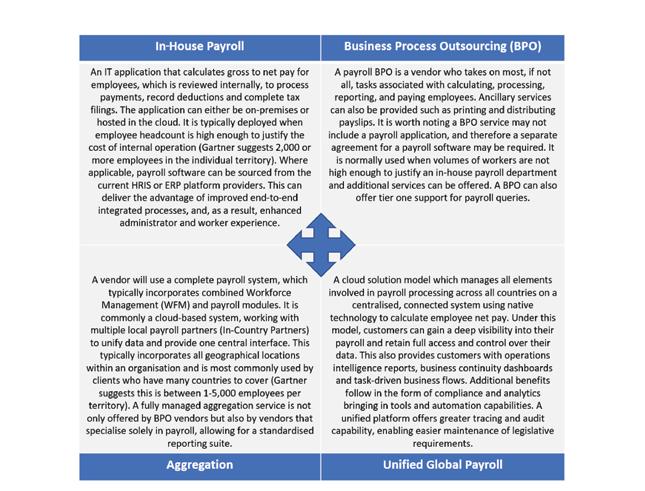

Features of the various model approaches are summarised in Figure 2.

Why Is Change Needed And How Will This Fit In The Organisation?

Driving Change In Your Global Payroll Model

There are three key considerations when deciding on a revamp of your Global Payroll Model:

1. Design and governance

2. Drivers and triggers for change

3. Global payroll maturity.

1. Design And Governance

The design and governance of the payroll model must reflect the organisation’s general corporate vision:

• The payroll strategy should have strong objectives, a purpose statement with clear goals and a team that can support delivery.

It is essential that all employees are guided by common principles to ensure global objectives are met

• GDPR and compliance obligations must be placed at the forefront of all operations.

The payroll governance model must be robust and enable high standards (it is 2.71x more costly to be non-compliant rather than compliant with mandates(3)). There must be a clear understanding of the difference between processes and controls

• Compliance regulations are ever-changing, and companies must adopt different

5 INTERNATIONAL HR STRATEGY www.internationalhradviser.com

Figure 1: Global Payroll Model – operational approaches

methods to prevent data breaches. This can be supported with rigorous controls that are updated and tested regularly to ensure processes are compliant

• The payroll operating model is pivotal to the efficient and accurate delivery of payroll. Companies should use technology, via use of data-driven analytics, to enable efficient and accurate payroll delivery. This will allow organisations to create an integrated payroll operations system which can deliver a high-class payroll process, for both employees and the organisation.

2. Drivers And Triggers

In order to trigger a global payroll change, there are several hurdles to overcome. Addressing clear pain points such as a lack of integration between existing organisational technologies is a good start. Utilising shared services and common tools across teams will allow tasks to be streamlined and enable uniform output.

Three of the biggest triggers for companies are (i) standardisation, (ii) allowing for organic headcount increase, and (iii) expansion into new territories. These drivers can be catalysts to propel an average payroll process into one that can be representative of a truly global payroll model.

In addition, the following four drivers have developed in recent years.

• Organisational Agility - organisations

are often in need of a payroll system that can be readily available to respond to ever-changing requirements. As the world changes, as seen with the COVID pandemic, the payroll department is required to make fast actioned changes to accommodate new legislation such as furlough pay or winter energy support

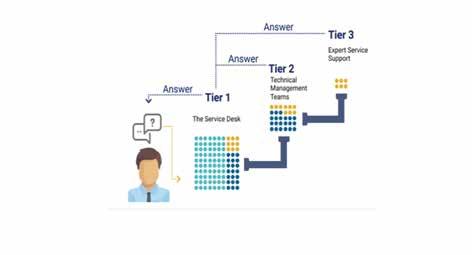

• Query Management - the existence of an effective and integrated query management system is pivotal, especially in a period of change when there is the need for real-time information and innovative solutions to business challenges. As illustrated in Image 1, having a traditional multi-tiered query system simply doesn’t

suffice for many organisations, as this reduces the employee experience by leaving their query between the tiers for days or even weeks

• Technology - if your chosen methodology is an outsourced payroll model, it is imperative that there is an agile technology platform underpinning service. Equally important is the expertise and knowledge of the supporting team, helping drive real change in employee experience and looking towards future technology provision for both employees and the business - such as on-demand pay, app single sign-on or direct communication, when GDPR and other privacy rules allow Global Payroll Model approaches

6 INTERNATIONAL HR ADVISER AUTUMN www.internationalhradviser.com

Figure 2:

Image 1: Tier 1-3 Query Management

• Analytics - the need to have uniform reporting has become increasingly important. As organisations seek to globalise their payroll systems, output must also be consistent and harmonised. Having a global data management and analytical system will allow for more detailed and robust reporting of payroll activity, enabling real-time reporting of not just employee level information but also organisational finance data, providing items such as gender gap information or trends on resignations of the employee base.

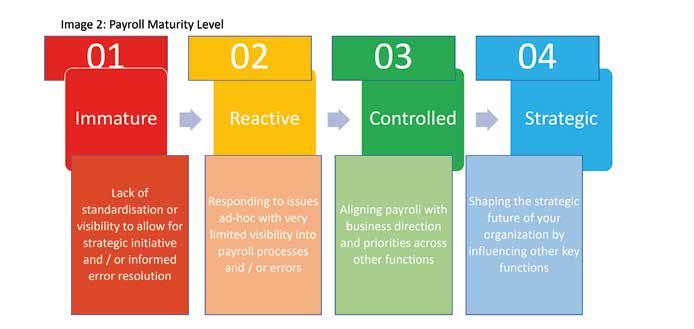

3. Global Payroll Maturity

Many existing payroll models sit between ‘Immature’ and ‘Reactive’ (see Image 2: Payroll Maturity Level). These two typically lack automation (say, between the HR and payroll systems) and therefore the ability to integrate data and effect change is limited. This is a common feature of payroll model failures, as teams often become overwhelmed with the volume of work, and the level of manual intervention leads to an overall higher risk profile. In order to mature, the payroll model must evolve to reflect the strategic vision of the organisation. Subject to that vision, this might be achieved in numerous ways:

• Creating and implementing a robust operating framework, whether in-house or outsourced

• Deploying high-capability technology and integrations through the vendor and technology ecosystem

• Developing highly skilled teams, and

• Enabling smart data reporting back into the organisation.

Driving Value

Payroll is an often undervalued, yet critical function. There are many ways in which to achieve a highly functioning Global Payroll

Model. At the core is the baseline need for payroll to be efficient, accurate and compliant. Those charged with leading the Global Payroll Model must achieve these three objectives at a minimum, and then progress onto defining and finessing a function that delivers in line with organisational strategic objectives, thus driving added value back into the business.

References:

(1) UK employees switch jobs due to poor payroll experience HR review

(2) www.economicjournal.co.uk/2020/ 07/poor-payroll-management-canharm-your-company-in-more-waysthan-one/

(3)www.corporatecomplianceinsights. com/true-cost-compliance

7 INTERNATIONAL HR STRATEGY www.internationalhradviser.com

LEE-ANN KILROY Associate Director, Payroll and Workforce Management Deloitte LLP D: +44 20 8071 0443 E: lkilroy@deloitte.co.uk HAYLEY MCKELVEY Partner, Payroll and Workforce Management Deloitte LLP D: +44 20 7303 3940 E: hmckelvey@deloitte.co.uk DELOITTE PAYROLL AND WORKFORCE MANAGEMENT Our mission is to define the payroll function of the future, for the workforce of the future. We created Deloitte Payroll and Workforce Management to deliver, transform and disrupt. We work with client organisations to solve the most complex challenges driving employee experience, efficiency and value. We deploy Deloitte market knowledge, subject matter expertise and insight to rethink the payroll and workforce management function. We focus on a range of areas, including global payroll delivery, strategy design, operational optimisation, vendor selection, technology implementation, automation and ecosystem design. Find out more here: www.deloitte.com/uk/en/pages/tax/articles/payroll-andworkforcemanagement.html Image 2: Payroll Maturity Level

Global Tax Update

BELGIUM

Cross-border teleworking after COVID-19 (i.e., after 30 June 2022)

Are you an employee who has been teleworking cross-border because of the COVID-19 measures and who will continue to do so after COVID-19, or do you as an employer have employees in that situation? If so, 30 June 2022, was an important date. This is specifically the case for employees who are teleworking in Belgium, the Netherlands, France, Luxembourg, or Germany.

During COVID, Belgium had concluded mutual COVID-19 agreements with its neighbouring countries (the Netherlands, France, Luxembourg, and Germany) implementing a fiction for the homeworking days exercised by the employee. As a result of this, homeworking days were deemed to be executed by the employee in the state where they would have exercised their employment in a regular situation.

These COVID-19 agreements, and with that the fiction, ended on 30 June 2022. This implies that homeworking days exercised outside the state of the employer will be taxable in the home country of the employee. As a result, taxation will shift from the state where the employer is located to the home country of the employee.

30 June 2022, marked the end of the fiction in terms of taxation, and initially marked the end in terms of social security. However, during the European Administrative Commission meeting in mid-June, an agreement was reached to establish a new transitional period up until 21 December 2022, for social security purposes.

The objective of this transitional period is to allow all parties concerned to adapt to the changed working patterns and to allow Member States as well as the Administrative Commission to investigate specific situations to see whether a structural change of the applicable rules is necessary. Consequently, until that date, teleworking days will not be considered when determining the employee’s applicable social security legislation. Cross-border teleworking will only imply a change of your applicable social security legislation, or the legislation of your employees, as from 1 January 2023.

However, a Limosa notification (if applicable) is again mandatory as from 1 July 2022 (this notification was not due during the Covid-neutralisation period).

Working from home or teleworking as part of the ‘new normal’ does not only have consequences in terms of applicable taxation and social security. It may also have an impact on the following:

• Applicable labour legislation and existing labour agreements (annex needed)

• Teleworking policies (that will need to be established or updated)

• Compliance (specific formalities apply such as the request of an A1-declaration or Limosa)

• Current payroll administration (that will need to be adjusted), and possibly the need to process a payroll in the home country of the employee

• The employer’s remuneration policy

• The employee’s additional pension build-up

• Etc.

BDO Comment

Clearly, the above is a major change that requires your attention. If you have questions, or if you need any assistance in this respect, do not hesitate to contact your Belgian adviser. They can discuss with you the implications that teleworking as from 1 July 2022 (or as from 1 January 2023), may have on your situation or that of your employees, and talk you through the steps to be taken to ensure you remain compliant.

CANADA Tax Related Hoiusing Proposals From The 2022 Federal Budget

Real estate prices in Canada have escalated significantly over the past two years, but even before that, Canadian housing prices had been steadily rising at a rate higher than wage increases. While affordable housing is a complex matter with no easy solution, new tax initiatives proposed by the federal government could offer some relief.

In this article we discuss the five income tax proposals related to housing and what they mean for taxpayers.

New Tax-Free First Home Savings Account

The boldest of these initiatives is the introduction of a new registered account, the Tax-Free First Home Savings Account (FHSA). First-time homeowners would be able to contribute a maximum of C$40,000 over their lifetime to this account, at a maximum of C$8,000 per year, starting in 2023.

Similar to a tax-free savings account (TFSA), the funds contributed into an FHSA will be able to earn investment returns taxfree. Unlike the TFSA, the contributions into an FHSA would be tax-deductible. Further, unlike a TFSA, any unused annual contribution cannot be carried forward.

When a withdrawal is made from the FHSA to purchase a qualifying home, the withdrawal will be tax-free. However, if a withdrawal (rather than a transfer) is made for any other purpose, it will be taxable.

The proposals also provide for flexibility for moving funds between an RRSP and an FHSA. For example, if there are funds in an RRSP, they could be transferred to an FHSA over five years to provide C$40,000 tax-free to purchase a home.

However, funds in an RRSP could also be used to buy a first home under the Home Buyers’ Plan (HBP). The HBP has been in existence for many years and allows a homebuyer to take a loan of up to C$35,000 from their RRSP to use for purchasing a home. This loan must be repaid to the RRSP over 15 years or be taxed as a withdrawal over 15 years.

There may be situations where a transfer from an RRSP to an FHSA to buy a home makes sense because the FHSA funds can be withdrawn tax-free with no need to repay the funds. However, while funds from an RRSP to create a Home Buyers’ Plan can be withdrawn all at once, funds can only be transferred from an RRSP to a FHSA at a rate of C$8,000 per year.

Real estate prices in Canada have escalated significantly over the past two years, but even before that, Canadian housing prices had been steadily rising at a rate higher than wage increases

9 GLOBAL TAXATION www.internationalhradviser.com

Each individual will need to assess how the FHSA could benefit them. This new plan also represents an opportunity for a parent to help their adult child save for a first home.

Multigenerational Home Renovation Tax Credit

Many older adults would like to stay in their own home and live as independently as possible. For some families, a home may be renovated to create an area within the home of adult children where an elderly parent can live. This is one type of situation where the proposed Multigenerational Home Renovation Tax Credit (MHRTC) could help.

The proposed MHRTC will be a refundable credit calculated as 15% of eligible expenses to an upper limit of C$50,000. Although the final details are not yet available in legislation, eligible expenses would be defined as those used to create a secondary unit within the main unit. The secondary unit would need to be a self-contained unit with a private entrance, kitchen, bathroom facilities, and sleeping area. The secondary unit could be newly constructed or created from an existing living space that did not already meet the requirements to be a secondary unit.

It is proposed that this credit would apply for the 2023 and subsequent taxation years, for work performed and paid for and/or goods acquired on or after 1 January 2023. If your family is thinking about creating a secondary unit for an eligible person, it might make sense to wait until 2023, as this new credit could provide up to C$7,500 in tax relief.

Home Buyers’ Tax Credit

There is currently a non-refundable tax credit available to first-time home buyers of C$5,000, which provides tax relief at 15% or C$750. The budget proposed to double this credit to C$10,000, which would provide up to C$1,500 in tax relief. This proposal will apply on the purchase of a qualifying home made on or after 1 January 2022.

Home Accessibility Tax Credit

The budget also proposed that another of the current housing tax credits be doubled. The Home Accessibility Tax Credit (HATC) provides a 15% non-refundable tax credit on eligible home renovation expenses up to C$10,000.

Eligible expenses for this credit are incurred when the expenses are for the renovation or alteration of a home to allow an adult age 65 and over to have greater accessibility in the home, or to have a reduced risk of harm within the home. An adult individual who is eligible to claim the disability tax credit, or a supporting person of such an individual, can also claim the credit for these types of renovations.

The budget proposed to double the annual expense limit to C$20,000, which would then provide up to C$3,000 in tax

relief. This enhanced measure would apply when the expenses are incurred in the 2022 or subsequent taxation years.

Residential Property Flipping Rule

The Canadian tax rules distinguish between a capital gain, which is currently only 50% taxable, and income gains, which are fully taxable. The principal residence exemption is a provision in the Canadian tax legislation that provides a tax-free gain on the sale of a residence that meets the definition of a principal residence.

The government is concerned that individuals who purchase real property, including rental property, with the intention of reselling within a short period of time (“property flippers”) are incorrectly reporting their gain on resale as a capital gain, or in some cases as a tax-free gain from the disposition of a principal residence, rather than as fully taxable business income.

To address this, the federal budget proposed to treat the disposition of any real property held for less than 12 months as business income, except in limited circumstances that would be beyond a taxpayer’s control (such as death, marital breakdown, addition of family members, disability, change of place of work, and insolvency).

It is proposed that this measure would take effect in respect of residential properties sold on, or after, 1 January 2023. The government has yet to issue draft legislation with respect to this measure.

BDO Comment

It is positive to know that governments and tax authorities are aware of the everyday concerns of taxpayers and then take steps to proactively help. Do speak with your Canadian tax adviser for regular updates regarding progress with these Budget proposals.

CHINA

Preferential Tax Policy introduced for residents of Hong Kong and Macau working in Nansha, Guangzhou

New rules have recently been introduced for residents of Hong Kong and Macao who are working in Nansha, Guangzhou. These rules effectively limit the Chinese individual income tax burden liability to what the individuals would have paid had they remained tax resident in and working in Hong Kong and Macao respectively.

IRELAND

Updated Revenue Guidance on SARP Requires Preplanning for Assignments/ Transfers to Ireland

In June 2022, the Irish Revenue published updated guidance on the qualifying conditions to avail of the Special Assignee Relief Programme (SARP). The new guidance

includes clarifications on some practical issues encountered by employers in determining employees' eligibility for SARP.

This is helpful in clarifying scenarios where the conditions for SARP would be deemed to be met, or not as the case may be.

However, a new interpretation by the Irish Revenue of a pre-existing requirement, to perform duties in Ireland in each of the 12 consecutive months following the employee’s arrival into Ireland, will be of concern to employers and their relevant employees. It should also require careful planning of periods of leave/vacation and hybrid working arrangements throughout the 12-month period following the employee’s arrival in Ireland, so that this potentially very valuable income tax relief is not inadvertently lost.

The guidance also provides clarity on scenarios in the 6 months prior to the employee’s arrival in Ireland, where another condition for SARP relief outlined below could be deemed not to be met, that will also require advance consideration.

Background

Firstly, as a brief overview, SARP is an Irish income tax relief aimed at encouraging the relocation and assignment of key talent within organisations to Ireland.

Where conditions for SARP are met, it allows for 30% of an individual’s taxable employment income over € 75,000 to be disregarded for Irish income tax purposes. This is subject to a current upper income threshold of € 1 million.

SARP relief is available for individuals arriving in Ireland from 2012 to 2022. It is expected this year’s Finance Act will further extend the relief beyond 2022. Once an individual qualifies for relief under SARP, they can avail of it for up to 5 consecutive tax years, provided the qualifying conditions continue to be met for each year of claim.

For example, an individual arriving in Ireland in 2022, and who qualifies for SARP in that year, could potentially claim SARP for tax years 2022 to 2026 inclusive, where they continue to meet the conditions for SARP in each of those years.

For more information on the qualifying conditions for SARP please speak to your adviser or request a copy of BDO’s SARP bulletin.

What’s New?

One existing condition to qualify for SARP is that for the whole of 6 months immediately before the relevant employee arrives in Ireland, they must be a full-time employee of the non-Irish “relevant employer”. This is defined as a company located in a country with which Ireland has a Double Taxation Agreement or Tax Information Exchange Agreement.

In their recent guidance, the Irish Revenue clarify that the above condition for SARP would NOT be met in the following circumstances:

10 INTERNATIONAL HR ADVISER AUTUMN www.internationalhradviser.com

• Where an individual takes up their employment with an associated company in Ireland before they arrive in Ireland. However, a limited exception is provided by the Revenue where the individual intends to take up employment with the associated company but is prevented from travelling to Ireland to commence their duties due to unforeseen circumstances outside of their control. In such cases, the performance of pre-arrival duties outside Ireland for the Irish company may be permitted if these do not exceed 5 workdays in total in this 6-month period

• Where an individual carries out work duties in Ireland in the 6 months immediately prior to commencing their Irish assignment/employment. A limited exception is also made here to allow for up to a total of 5 workdays in Ireland working for the foreign (relevant) employer during this 6-month period. The Revenue also clarify that brief trips to Ireland on holiday/look-see visits in the 6 months immediately before arrival will not prevent the employee from meeting the above condition for SARP, if all of the other qualifying conditions are met.

As already referenced above, a significant update in the recent guidance is the suggested denial of the availability of SARP

relief where an individual does not perform duties in Ireland in each of the 12 consecutive months following their arrival to Ireland. An example is provided of an employee who arrives in Ireland in January 2022, and spends all of August 2022 on vacation outside of Ireland. In that case, the Revenue's stated view is that the individual, who would otherwise have been entitled to claim the relief, is ineligible for SARP.

BDO Comment

For any pre-arrival Irish tax consultations with employees, who are relocating to Ireland on assignment or to take up an employment with an associated company in Ireland, we strongly recommend those take place at the earliest opportunity and before the employee commences their Irish role or arrives in Ireland to take up those duties. This should allow the adviser to identify and clarify to the employer and employee their requirements so that an opportunity to avail of SARP is not lost, and to ensure that the relevant parties are aware of their responsibilities in this regard.

It should also be noted that where the above criteria for SARP is not met, the impact for the employee is not limited to the loss of the tax relief under SARP for just the first year of claim, but will result in

losing the tax relief for every year in which the employee may otherwise have met the criteria to qualify for SARP (up to a maximum of 5 years).

Prepared by BDO LLP. For further information please contact Andrew Bailey on 0207 893 2946 or at andrew.bailey@bdo.co.uk

ANDREW BAILEY

11 GLOBAL TAXATION www.internationalhradviser.com

Tax Risks Within The Assignment Life Cycle

As we come out of ‘Covid restricted mobility’ and businesses again expand globally, so comes the challenge of moving people. In this article we explore the tax risks arising at various points in the assignment life cycle.

Pre-Assignment

Who Is Going, Where And What Will It Cost? Could You Structure It Differently?

In general, projects start with a potential business opportunity where it is necessary to move people to a different location.

Given that staffing is amongst the biggest expense, it is amazing how few businesses consider the tax cost of any assignment/ project. For example, many businesses express surprise some 18 months after the assignment has ended once the final tax bills come in, saying that if they had known that it would be that expensive then they never would have sent the individual/s on assignment. Some businesses resort solely to basic internet research that often throws up outdated figures and rules and omits practical, on the ground, local experience. A properly considered upfront analysis of the assignment, the applicable rules and projected tax cost, can assist greatly with budgeting and managing cost expectations for all.

Planning can also help reduce the cost of an assignment. In many instances there are tax breaks for short-term assignees, e.g. UK, the Netherlands, Sweden and Denmark all have such reliefs. These reliefs may have conditions attached, for example, to the length of the assignment, the employer’s location or the level of salary and allowances. Such tax breaks can be considerable, for example, the Dutch ‘30% facility’. Additionally, paying certain benefits through the employer or having the employer provide them directly can result in reduced tax and social security liabilities. By considering available tax breaks in conjunction with the aims of the project, assignments can be planned and structured in the most tax efficient manner, potentially significantly reducing the costs of an assignment.

Work Permits/Immigration

Clearly you do need to obtain the right work permits and visas to ensure that an individual can legally work in the country.

The applicable rules may dictate whether an individual can/cannot be employed locally and has to be on an assignment. Do check such rules, as they may restrict the ability of the business regarding employment structuring and tax planning.

Tax Policies

With few assignees, arguably, a tax policy is not needed, as this permits maximum flexibility to reduce tax costs, however, when the numbers accumulate the advantage of a structured approach becomes more apparent. By setting out the approach of a business to international mobility this provides a ready template as to how to deal with assignments and sets out the tax and social security philosophy (e.g. tax equalisation, home social security, assisted

tax returns, host based etc.). A policy can help to reduce tax risks by addressing clearly the approach to be adopted for international assignments and localisations.

Do You Know Who Your Assignees Are And Do You Know Where They Are?

Surprisingly, many businesses are still unable to correctly identify all of their assignees and their locations. Apart from the obvious security and duty of care risks that arise, tax risks abound. The issue of short-term business visitors (and remote workers) is on the rise post-Covid, and will again be a major topic and revenue generator for tax authorities around the world. This will lead to a potential high risk tax exposure for businesses. It is important that businesses can track where their assignees and remote workers are, can identify the potential tax trigger points and proactively manage these. Don’t assume that tax treaty exemption will always apply (or that no action needs to be taken), the conditions for such exemption all need to be met – not just the 183-day test – and remember that tax treaty exemption applies to the individual, and does not necessarily remove the reporting and withholding obligation for the employer. Be aware that authorities are becoming increasingly sophisticated when it comes to tracking and sharing data between different government departments. For example, the Australian tax and immigration authorities proactively share data.

Departure Meetings In Home Country And Arrival Meeting In Host Country

These meetings can be invaluable in assisting both the employee and employer to understand what tax forms and procedures need to be completed and followed, and what records needs to be kept for the duration of the assignment. Failure to hold such meetings can result in assignees missing out on opportunities through ignorance, such as failing to keep relocation receipts, workday and travel records or registering for expatriate concessions (e.g. please read the update Irish SARP rules in our Global Tax Update).

During The Assignment

Withholding Taxes - Is The Company Paying Withholding? Are They Paying The Right Withholding?

Frequently the biggest tax risk that arises with assignees (and remote workers) is the failure by the employer to deduct

With few assignees, arguably, a tax policy is not needed, as this permits maximum flexibility to reduce tax costs, however, when the numbers accumulate the advantage of a structured approach becomes more apparent

12 INTERNATIONAL HR ADVISER AUTUMN www.internationalhradviser.com

withholding taxes. Withholding taxes such as Pay As You Earn (UK), Pay As you Go (Australia) should often be deducted by the employer. Employees can be fickle and with many moves resulting in early cessation of assignments and possible termination of employment on, or shortly after completion, it can be difficult or impossible to recover taxes from former employees. Where there is a failure to deduct withholding, tax authorities will generally look to the employer to rectify the position and may insist on a grossing up of any resulting tax liabilities, thus increasing the tax cost. Always deduct withholding taxes and do this on a timely basis: after all, you can usually get this refunded if excess withholding is paid. Where variations to withholding are appropriate (e.g. UK’s nil tax codes and reduced s690 overseas workday relief withholding directions or tax treaty exemption), do ensure you get the appropriate documentation from the tax authority evidencing their approval.

Are You Picking Up Split Payments And Pre-Assignment Payments?

Assuming withholding taxes are being deducted, do ensure it is being operated on the correct basis. For example, are split payroll amounts being taken into account?

It is very easy to overlook home country/ third country payments that remain in existence. Additionally, payments that relate to the assignment but are paid before the assignment commences, could be liable to withholding in the host country. All may need to be reflected in the payroll calculation, and even if there is no actual payroll or entity in the host location, withholding taxes may need to be operated on a shadow or ghost payroll basis. Payments will of course also need to reported, as appropriate, in the individual’s tax returns.

Is The Company Picking Up All The Benefits – Home And Host Paid Or PreAssignment Paid?

Another issue that is frequently overlooked for business or individual reporting is that of benefits. Again, it is important that both home/ third country benefit provision is considered when assessing host (and home) country tax liabilities. It is very easy to overlook their provision, for example, continuing home country long-term storage or medical insurance costs. Additionally, where benefits such as relocation expenses are paid pre-assignment, these can often be forgotten when it comes to assessing host country liabilities. Host country rules will need to be examined to determine what needs to be reported and taxed.

Is Social Security Being Paid In The Right Location – On Home And Host Payments?

Part of the initial assignment structuring should be to determine where social security

will be paid. This may be in the home country, the host country, both or neither, or in a third country depending on the circumstances. Bear in mind that social security costs can sometimes outweigh the tax costs, with employer contributions in locations such as France and Italy being approximately 40% on an uncapped basis. Contributions in other countries such as Germany, may appear high at face value, but capping limits the costs for high earners and employers. In other countries such as Hong Kong and Singapore, it may not be possible for foreigners to join the local social security system. Planning can help to reduce any social security liability but the impact on future benefits does need to be considered. This is of course extremely difficult with ever changing rules.

Once the right location for payment has been determined and the individual is on assignment, it is important to ensure that social security liabilities are calculated on the correct amount. For example, are all cash payments being recorded? Payments through split payrolls are often overlooked as are benefits provided in home or host countries. Do gather all details on a timely basis so that liabilities for both the employee and employer can be correctly calculated and paid. As with withholding tax, failure to deduct by the employer can result in additional liabilities for them if the employee becomes an ex-employee. Always deduct where you need to, and do ensure you have the right, up-to-date certificates of coverage in place, to demonstrate why liabilities are being or are not being deducted as appropriate.

Are Tax Returns Being Filed By The Individual – On What Basis?

Completion of personal tax returns whilst an individual is on assignment can often be overlooked or dismissed as an easy compliance task. This is particularly risky when one considers there will be added complexities, interactions between differing tax systems and the unfamiliarity of foreign implications and foreign tax regimes to deal with. Failing to provide tax assistance can lead to missing and incorrect tax returns – whether innocent or otherwise. This could affect the corporate reputation of the business entity and possibly even its ability to continue to undertake business in a location. Providing professional assistance with this task can help both the employee and the employer to ensure correct and timely filings, and leave both parties to focus on the success of the assignment.

Have Any Tax Reconciliations Been Undertaken?

Where there are tax equalisation commitments by the employer to meet certain or all elements of an assignee’s

foreign tax liability, it is important to ensure that not only is the correct liability paid, but that relevant steps are taken to recover hypothetical tax underpayments or real home country tax refunds from the employee. Tax leakage may occur for the employer where this does not take place promptly or at all.

Recharges And Bearing The Cost/Transfer Pricing

From a business perspective, cost and benefit typically go together and should be located in the same place. However, this relatively simple business rule can have far reaching consequences. Recharges can jeopardise potential treaty exemption for the individual. The failure to consider people issues and the resulting costs can create problems with tax authorities when transfer pricing rules are overlooked. Changes introduced following the introduction of Base Erosion and Profit Shifting (BEPS) rules need to be considered from an international mobility context. In certain circumstances recharges can also trigger a non-recoverable VAT liability.

Corporate Residence And Permanent Establishments

Although your company is located in, and is a resident of a certain country, sending people to another country may create a local presence to such an extent that the company also will be subject to local corporate taxation. Whether or not this is the case will depend on their purpose of being there, their numbers and seniority, their activities and value creation. Does their presence create a ‘fixed place of business’ or ‘permanent establishment’? This whole area is currently under scrutiny by tax authorities, particularly in a postCovid world of hybrid working and remote workers, so do look out for future changes.

Post-Assignment

Tax Equalisation Reconciliations And Loans

On cessation of the assignment it will be necessary to unwind any tax loans and deal with final tax equalisation reconciliations. Do remember to undertake these tasks, especially as so many individuals leave their employer after an assignment and memories of tax arrangements agreed at the outset of an assignment quickly fade.

Trailing Liabilities – Stock And Bonuses.

Are You Taking These Into Account?

Naturally you have been correctly reporting stock awards and bonuses during the assignment itself, but do you continue to track and map those relating to the assignment once the individuals cease their assignment? How long do you track for? Tax authorities around the world

13 TAXATION www.internationalhradviser.com

are increasingly aware of the potential for tax to be overlooked and not paid in such circumstances. They will pursue such liabilities, so do ensure you withhold and file as appropriate, and remember to collect any contribution towards tax and social security liabilities from the employee.

Use Of Carry Forward Foreign Tax Credits

In certain circumstances, payment of taxes by the employer, whilst an individual is on assignment, may result in excess foreign tax credits, which may be unusable during the course of the assignment but available thereafter. As the taxes giving rise to these credits were paid by the employer, arguably they belong to the employer not the employee. How long does your business track such foreign tax credits to ensure any tax refunds generated go to you?

Tax Clearance Certificates, Tax Payments And Post-Assignment Individual Tax Returns

Relevant departure forms should be submitted to record the individual’s tax departure from the host country and return to their home or next country. Do remember that certain countries, for example Singapore, require tax matters to be settled and liabilities paid before a departure clearance certificate can be

obtained. Don’t forget that final year tax returns may still need to be filed and the existence of post-departure bonuses and stock may necessitate filings beyond the actual year of departure.

Forgotten Bank Accounts And Host Country Investments

In the rush to move to the next location, or return from assignment, it can be relatively easy to forget to shut foreign bank accounts or report their or other host country investments ongoing existence in future tax returns. Don’t forget to do so, otherwise tax authority enquiries will probably ensue. The volume of information reported between tax authorities is seeing a massive surge and this can easily trap the forgetful. Do seek to get it right from the outset.

I have only briefly touched on the tax risks that can arise from international assignments during the assignment life cycle. Careful tax planning, a structured approach to tax, and implementation of a tax process, can help both employers and employees alike to mitigate tax liabilities and minimise tax risks. All department teams (HR, Tax, Finance, etc.) should work together with the assignee and the tax adviser to achieve this goal.

If you would like to discuss any of the issues raised in this article or any other expatriate matters, please do not hesitate to contact Andrew Bailey on +44 (0) 20 7893 2946, email Andrew.bailey@bdo.co.uk

ANDREW BAILEY

Andrew Bailey is Head of Global Employer Services at BDO LLP. He has over 30 years’ experience in the field of expatriate taxation. BDO can provide global assistance for all your international assignments.

ANDREW BAILEY

Andrew Bailey is Head of Global Employer Services at BDO LLP. He has over 30 years’ experience in the field of expatriate taxation. BDO can provide global assistance for all your international assignments.

14 INTERNATIONAL HR ADVISER AUTUMN www.internationalhradviser.com

The 2022 Global HR Conference Monday 17th October 2022 The Adelphi Building, 1-11 John Adam Street, London, from 12pm – 4.30pm TAX & MOBILITY UPDATE hosted by BDO LLP BDO will be hosting an Update regarding Tax Changes and Topical Mobility Issues and Trends. Join us for this FREE one-day event aimed at Senior Global HR Professionals only. To register a place for yourself and your colleagues, please email helen@internationalhradviser.com with the names and job titles of those who wish to attend. We look forward to seeing you there!

EU Migration Law Updates 2022

Immigration law is often viewed as an area where nation-states are free to legislate independently and at their own discretion based purely on national interests. However, as the European Community evolved and became the European Union (EU), and in line with the bloc’s deepening integration, member states gradually agreed on minimum standards and harmonisation on immigration. For example, at the start of the Covid-19 pandemic, member states decided to close their internal borders based on national interests, while subsequent agreement at EU level led to a gradual reopening of internal borders and common entry requirements at least for the Schengen area(1). Another more recent example is the unanimous decision made by EU member states to use the Temporary Protection Directive as a means to create a common legal residence status for Ukrainian refugees fleeing the war in Ukraine.

While the existence and impact of EU asylum legislation on national immigration policy is well known and often subject to public debate, EU legislation on labour migration is generally subject to less scrutiny. However, this does not mean that the impact of EU laws on labour migration is less significant. In particular, over the past two decades, the EU has steadily increased legislative measures in an effort to make the bloc an attractive place of employment for global talent and in turn drive the economies of its constituent member states.

The EU’s executive body, the European Commission, generally proposes legislation that fosters harmonisation in specific areas of labour migration and these are then discussed and negotiated in detail by EU member states. As a result some laws end up being watered down as member states fail to agree on certain contentious issues, such as labour market testing and salary thresholds. However, the European Commission’s efforts will always continue, following a trend of further harmonisation that can be expected to continue in future.

In 2020, the European Commission published its plans in the field of immigration in its New Pact on Asylum and Migration. A key pillar of the plans is the Skills and Talent Package, which is specifically intended to address key labour market issues across the EU. Among other measures, this package contained a commitment by the European Commission to revamp existing legislation on labour migration to tackle the skills shortage in the EU.

under the leadership of the European Commission and, following agreement by member states, the review Directive entered into force on 17 November 2021. Member states have until 17 November 2023 to implement the amended Directive into national legislation.

The aim of the new Directive is to simplify the procedures and qualifying criteria, widen the scope and to strengthen the rights of EU Blue Card holders.

The most important changes are:

• Facilitated possibility for EU Blue Card holders to undertake business activities in other member states

• Minimum duration of an employment contract reduced from 12 months to 6 months

• Currently Blue Card holders are allowed to move to another member state after a continuous stay of 18 months. This will be reduced to 12 months

• Recognition of professional experience in addition to or instead of educational qualifications

• Standard validity of the Blue Card to be increased from 12 months to 24 months, or the length of the contract plus three months

• Reduction of processing time from 90 days to 60 days (or 30 days for employers included in a national trusted employer scheme)

EU Blue Card

In late 2021, a first key step was taken as the amendment of the EU Blue Card Directive was rubber stamped by EU member states. The EU Blue Card was originally introduced in 2009 in order to address talent shortages across the EU as the European equivalent to the US Green Card. The purpose was to make it easier for non-EU/EEA/Swiss nationals to work freely in multiple EU member states within the European Union. However, studies over several years showed that use of the EU Blue Card category was generally low across member states, and therefore a revision was proposed by the European Commission in 2016. However, the negotiations between member states on some key aspects of the revision ended in a deadlock. It is under the Skills and Talent Package that the negotiations were revived

• Greater flexibility in respect of the salary threshold, which can be between 1 and 1.6 times the average gross salary of the member state, instead of 1.5. Employers and non-EU/EEA/Swiss employees will likely welcome this increased flexibility and simplified qualifying criteria. Yet it remains to be seen how EU member states will implement the revised Directive for EU Blue Card holders and their family members. This is despite the fact that the final text was watered down in order to break the deadlock. For example, the scope of activities that EU Blue Card holders can perform in other member states without a work permit for up to 90 days are generally already permitted for all business visitors based on national law regardless of nationality.

On 27 April 2022, another important milestone was reached in the EU’s efforts to attract key talent to its labour market when the European Commission published its proposals to amend two further pieces of EU legislation on labour migration: the Single Permit Directive and the Long-term Residence Directive.

The EU Blue Card was originally introduced in 2009 in order to address talent shortages across the EU as the European equivalent to the US Green Card

15 EUROPEAN IMMIGRATION UPDATE www.internationalhradviser.com

Single Permit Directive

The Single Permit Directive entered into force in 2011, and ensured that individuals and employers applying for residence and work authorisation in a member state would be able to benefit from more simplified and efficient processes. For example, applicants would only need to submit a single application for combined entry, residence and work authorisation and, after approval, a single approval should be issued.

The European Commission has now submitted proposals aimed at making those rules and processes more efficient.

The main proposed changes are:

• The possibility for individuals to apply from their home country outside the EU as well as in-country

• A maximum of 4 months processing time, including labour market testing and issuance of an entry visa (if applicable)

• The possibility for the employee to change employer during the permit's validity

• The possibility for the employee to keep the permit for at least another 3 months in the event of unemployment

• New provisions on penalties against employers in case of violations of working conditions, freedom of association and access to social security benefits and to introduce complaints mechanisms. These would be welcome changes, as shorter processing times, simplified requirements and increased employee flexibility ensure that non-EU nationals can be hired more easily for positions in the EU. Nevertheless, it remains to be seen whether EU member states will agree with these proposals or whether the negotiations will be as complex as for the revised EU Blue Card.

Long-Term Residence Directive

The EU’s Long-term Residence (LTR) Directive entered into force in 2003, and in essence ensured harmonisation of requirements and processes for issuance of long-term residence status for non-EU/EEA/Swiss nationals. For example, the Directive specifies that LTR status must be granted after continuous and legal residence of at least 5 years in the territory of the member state, a maximum processing time of 4 months from date of submission, and common standards for loss of the status as a result of residence outside the member state of issuance or the territory of the EU. In addition, the Directive sets out general conditions for holders of LTR status in one member state to apply for residence in another member state.

However, the Directive is somewhat limited in its effect given that most member states require individuals to pass civic integration and language tests in order to obtain LTR status. In addition, the Directive allows member states to apply labour market tests to those seeking to work and

reside in another member state. As a result, the Directive is not widely used in member states, who are still permitted to issue LTR permits on national grounds, and does not promote intra-EU mobility effectively.

The EU Commission has therefore submitted proposals for an amended LTR Directive.

The main proposed changes are as follows:

• Periods of residence in other member states will be able to be counted towards the cumulative 5 years required to obtain LTR status

• No labour market testing required for persons with an LTR status in one member state who wish to reside and work in another member state

• No labour market testing required for family members of LTR status holders in the member state where the main applicant holds that status

• Facilitated family reunification requirements, and family members of an LTR permit holder that were born in the member state of issuance automatically acquire LTR status

• Reduction of processing time from 4 months to 90 days

• Possibility to apply for LTR status in a member state other than where the status was issued after 3 years residence (instead of 5 years)

• Permitted absence from the EU without losing LTR status increased from 1 year to 2 years.

If these changes are adopted by EU member states, it will provide additional grounds for intra-EU mobility for holders of LTR status. It will also ensure potential applicants will not be limited in their movement within the EU due to a fear of losing accumulated periods of residence in different member states. However, civic integration and language requirements will still generally apply for applicants, which means that it is likely potential applicants will seek to stay within a particular language region, if not a particular member state, for a significant period of time before applying for LTR status.

Interestingly, a new provision has been added, which specifies that periods of residence in a member state on the grounds of investment will not count towards the cumulative period required to obtain LTR status. This is clearly aimed at certain member states’ investor and ‘golden’ visa schemes that have been subject to criticism amid reports of abuse. It is likely that many member states will welcome this change.

As with the proposals on the Single Permit Directive, it also remains to be seen whether member states will adopt the proposals. In this respect there may be some additional challenges as individual member states may seek to protect their existing national immigration policies on long-term residence.

ETIAS And EES

While not specifically related to labour migration, the EU’s plans to implement new systems to regulate entry and exit from the Schengen area by non-EU nationals are well documented. Specifically, in late 2022 and early 2023 the EU will implement the European Travel Information and Authorisation System (ETIAS) and the new Entry and Exit System (EES). These measures are the outcome of initial proposals from 2016 by the European Commission under the Agendas on Security and on Migration.

Travellers who are visa-exempt for short stays (up to 90 days in a rolling 180 day period) may currently simply enter the Schengen area on the basis of their passports and will be stamped upon entry and exit. However, once ETIAS goes live, those nationals will generally be required to complete an online registration form prior to travel. The authorisation will be valid for 3 years and will allow them to enter and exit the Schengen area freely as long as the 90 days’ stay in 180 days is not exceeded.

Travellers will be required to include personal details on the form, including education, occupation, travel history and criminal antecedents (if applicable), and pay a fee of EUR 7 per person.

While there are some exceptions, such as for holders of an EU entry visa or residence permit and for British citizens with a valid residence permit issued under the EU-UK Withdrawal Agreement, ETIAS will generally apply to all visa exempted non-EU nationals travelling to the Schengen area.

In addition to ETIAS, the EU will also implement the new Entry and Exit System (EES), which is an IT system that will digitally register the entry and exit of most EU nationals travelling to the Schengen area, replacing the current manual process of passport stamping. While holders of an EU entry visa or residence permit and some other specific groups will not be subject to the EES, it will otherwise apply to all non-EU nationals travelling to the Schengen area.

The main aim of ETIAS and EES is to more efficiently and diligently manage cross -border movement to and from the EU and prevent cross-border crime and terrorism. While it will practically impact many travellers who are currently permitted to enter the Schengen area simply on the basis of their passports without prior registrations being required, it is not expected that it will restrict travel for any particular group.

Closing Remarks

The EU’s Skills and Talent Package aims to make the EU more attractive for high-, medium- and low-skilled talent across a variety of sectors. In general, the measures that amend the Directives discussed in detail above include increasing harmonisation across

16 INTERNATIONAL HR ADVISER AUTUMN www.internationalhradviser.com

EU member states, simplifying procedures and promoting intra-EU mobility. Given that recent reports have shown that the EU is facing significant challenges in attracting key skills that are needed across different regions and industries, it is likely that such changes will be welcomed by businesses and employers operating across the EU.

Conversely the implementation of ETIAS and EES will likely be viewed as increasing the administrative burden for persons travelling to the EU. However, the argument can be made that this burden is necessary and acceptable in order to control the EU’s borders and tackle crime and terrorism. Whether this will

indeed be successful remains to be seen. In the meantime, employers should ensure their short-term and business travellers are aware of the new requirements so that they can continue to travel without disruption.

Reference:

(1) The Schengen area comprises Austria, Belgium, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden, Switzerland.

The 2022 Global HR Conference

IMMIGRATION UPDATE hosted by Vialto Partners

To register a place for yourself and your colleagues on Monday 17th October, please email helen@internationalhradviser.com with the names and job titles of those who wish to attend.

HUGO VIJGE

Europe Advisory Lead, Vialto Partners. Email: hugo.vijge@vialto.com

HUGO VIJGE

Europe Advisory Lead, Vialto Partners. Email: hugo.vijge@vialto.com

17 EUROPEAN IMMIGRATION UPDATE www.internationalhradviser.com

Global Immigration Update

Introduction

From the new Prime Minister and Home Secretary in the UK; to changes in the EU approach to Russian nationals; and an increased focus on attracting and retaining skilled talent in Asia-Pacific, there have been significant changes to immigration policy and legislation over the last 3 months. Please do read on for further details.

Australia - Outcomes From Australia's Jobs And Skills Summit

The Australian government's Jobs and Skills Summit has lifted the permanent migration cap to 195,000 places effective immediately. $36.1 million in additional funding has been pledged to accelerate visa processing and resolve the current backlog. This includes a surge capacity of 500 staff over the next nine months. Ideas from the Summit will be used to rebuild Australia's migration program in the national interest.

The long-awaited Jobs and Skills Summit was held in Canberra last week bringing together Australian businesses, governments, unions and individuals to address the challenges facing the Australian labour market and economy today.

A key area of focus was Australia’s migration programme. A snapshot of key initiatives agreed to during the Summit include:

• Increasing the permanent Migration Programme ceiling to 195,000 in 2022-23 to help ease widespread, critical workforce shortages. These increased caps are effective immediately

• Providing $36.1 million in additional funding to accelerate visa processing and resolve the visa backlog. This includes a surge capacity of 500 staff over the next nine months

• Increasing the duration of post study work rights by allowing two additional years of stay for recent graduates with select degrees in areas of verified skills shortages to strengthen the pipeline of skilled labour in Australia

• Extending the relaxation of work restrictions for student and training visa holders until 30 June, 2023 to help ease skills and labour shortages.

Within the overall planning level of 195,000 places, allocations have been made to various visa streams as follows:

• 142,400 places allocated to the Skill visa stream

• 52,500 places allocated to the Family visa stream; and

• 100 places allocated to the Special Eligibility stream.

The Summit also laid out priorities for further work, with a focus on reviewing the purpose, structure and objectives of Australia’s migration system to ensure it meets the challenges of the next decade. The following items have been flagged for consideration:

• Assessing the effectiveness of the skilled migration occupation lists

• Expanding pathways to permanent residency for temporary skilled sponsored workers

• Raising the Temporary Skilled Migration Income Threshold (‘TSMIT’). The current TSMIT of $53,900 has not increased since 2013

• Reforming the current labour market testing process following consultation with unions and business

• Examining the potential for industry sponsorship of skilled migrants

• Embedding a role for Jobs and Skills Australia, a newly formed statutory body providing independent advice on workforce, skill and training needs. Jobs and Skills Australia’s analysis of skills shortages will set priorities for the skilled migration programme

• Policies to address critical labour shortages across regional centres and how to improve access to skilled migration by small business.

In the coming weeks, the government will task three eminent Australians to consider how Australia’s migration program can be rebuilt in the national interest. Submissions from the wider community will be sought over the next 12 months to contribute to a national white paper on employment.

What This Means