LOCAL REAL ESTATE GUIDE

2023

Q1

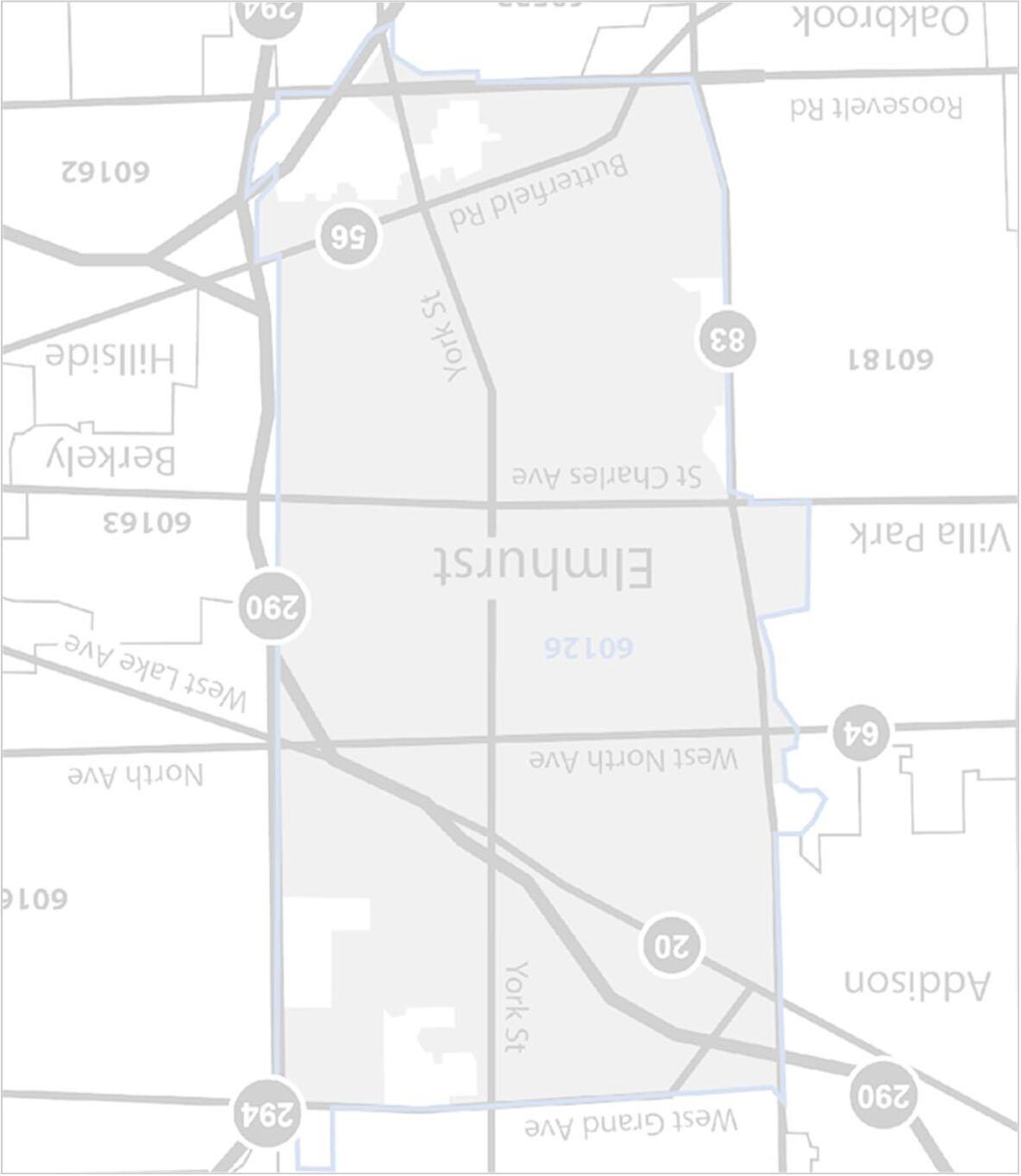

ELMHURST

CLOSED:closed transaction reflecting the final sales price (does not include any seller credits)

CONTRACTED:contingent or pending transaction reflecting the latest asking price

CONTRACT TIME:number of days between the first list date and the contracted date (does not include time from contract to close)

HOME INVENTORY:number of homes currently available for sale

MEDIAN:middle value of a given dataset (all report values are medians, which are less impacted by outliers than averages)

PRICE DISCOUNTS:percentage difference between the initial list and recorded sale price

PRICE PER SQ. FT:ratio of the price to the square footage of a closed transaction as a relative price measure (factors in home size)

NORTHWEST

(North Ave. to Lake St. and Rte. 83 to Hwy. 294)

CENTRAL WEST

(Prairie Path to North Ave. and Rte. 83 to York St.)

NORTHEAST

(Lake St. to Grand Ave. and Hwy. 294 to Rte. 83)

CENTRAL EAST

(Prairie Path to North Ave. and Hwy. 290 to York St.)

SOUTHEAST

(Prairie Path to Butterfield Rd. and Hwy. 290 to York St.)

SOUTHWEST

(Prairie Path to Butterfield Rd. and Rte. 83 to York St.)

“Seller’s Market” Remains this Spring with Parallels to Last Year

More

Many homes selling at a small discount to ask; homes over $700K showing little / no discount

Generally higher relative prices;homes <$400K softened some as did Northeast and Central East

Demo and new construction permits declining; lowest Q1 back to 2009 –2011 timeframe

New listings were down almost 30% across price ranges in Q1

January was particularly soft with new listings down by nearly 40% from last year

Dramatic declines at <$400K over the last 2 years finally slowed some for the quarter

Price Range'23'22%

<$400K 3437-8%

$400K - $699K 5584-35%

$700K - $999K 2641-37%

$1M+ 4561-26%

Q1 and last 12 months showed lower listing activity across all submarkets

Many Elmhurst areas now experiencing 10+ year lows for listing activity over the last 12 months (well below pre-pandemic)

Northeast Elmhurst at historical lows for new listings (even below Great Recession)

Jan. –Mar. (YoY%)

Submarket'23'22%

Northwest 2336-36%

Northeast 813-38%

Central West 3140-23%

Central East 3440-15%

Southwest 3358-43%

Southeast 1323-43%

Contracted homes were down nearly 30% in Q1 across price ranges (<$400K was flat)

Contracts picked up some in March with the last month of the quarter down ~10%

With very limited availability, contract activity is lowest at the $700K –$1M range

Contracted activity was meaningfully lower across all submarkets in Q1

Homes under contract are now at or below pre-pandemic levels across Elmhurst areas over the last 12 months

Central West has held up the best over the last 12 months, but also did not experience the same dramatic increases as other areas

Northwest Northeast Central West Central East Southwest Southeast

Northwest 1927-30%

Northeast 613-54%

Central West 2227-19%

Central East 2630-13%

Southwest 3455-38%

Southeast 1019-47%

Closed homes were down nearly 35% for the quarter; however, homes priced over $1M remain 20%+ higher over the last 12 months

Declines at <$400K have been tremendous over the last 12 months (and 45% lower in Q1); currently at historical lows with rising prices

Closed home sales activity was lower across submarkets in Q1; Central areas experienced the smallest declines

Northeast Elmhurst activity remains very low (for the quarter and last 12 months)

Central East and Southwest remain the most active areas for home closings

Northwest Northeast Central West Central East Southwest Southeast

Submarket'23'22%

Northwest 1322-41%

Northeast 47-43%

Central West 1012-17%

Central East 2024-17%

Southwest 2534-26%

Southeast 814-43%

Available homes declined nearly 30% and remain at 15+ year lows for this time of year

Inventory is particularly limited for homes priced $700K –$1M (1/2 of what it was on a relative basis versus 2019)

Inventory reaching a bottom after declining 75%+ from pre-pandemic levels

Home inventory is extremely low across submarkets; Northeast showed a large percentage increase from a very small base

South Elmhurst home inventory remains particularly low relative to history (less than 10 homes available combining submarkets)

Only Central West has more than a dozen homes available across price points

Northwest Northeast Central West Central East Southwest Southeast

Contract time declined for homes over $700K in Q1; homes priced under $400K saw contract time increase dramatically

Homes went under contract around 3 weeks or less in most cases during the quarter

Expect contract times to remain short with limited available inventory

Contract time in Q1 was still relatively quick, but mixed (North submarkets increased to a month or longer)

Submarkets experienced large percentage changes due to low day counts (i.e., a day or two change is a big relative move)

Homes on the market for 3 weeks or longer are likely overpriced or have other factors impacting time / interest

Jan. –Mar. (YoY%)

Submarket'23'22%

Northwest 412846%

Northeast 3112158%

Central West 1621-24%

Central East 196217%

Southwest 912-25%

Southeast 1026-62%

Sales mostly closed at 97% –99% of original list price for Q1 as sellers often accepted a small discount; homes priced less than $400K had more negotiability

Multiple offers are more situation-specific than the expectation; homes receiving many offers were likely underpriced Price discounts have returned in most cases, but remain relatively tight

Price Range'23'22%

<$400K 94%98%-4%

$400K - $699K 98%98%-1%

$700K - $999K 99%99%0%

$1M+ 99%98%1%

Price discounts have been mostly consistent across submarkets, but some variability developing

Northwest saw discounts widen for the quarter, but homes in this area often sold for full price over the last 12 months

Buyers and sellers mostly met at a small discount to asking price during Q1

Jan. –Mar. (YoY%)

Submarket'23'22%

Northwest 95%98%-3%

Northeast 100%97%3%

Central West 98%98%0%

Central East 98%99%-1%

Southwest 99%99%0%

Southeast 97%98%-1%

Price per sq. ft. trend was higher across price ranges in Q1, except under $400K

All price ranges remain at record levels over the last 12 months other than <$400K (which is slightly below based on the last 2 quarters)

Pricing continues to hold / increase based on very low home inventory

Jan. –Mar. (YoY%)

Price Range'23'22% <$400K $244$252-3% $400K - $699K $282$2656% $700K - $999K $274$2615%

$354$3307%

Submarkets saw mixed prices for Q1 with most areas advancing (Northeast and Central East declined)

Central East remains above $300 per sq. ft. over the last 12 months with Southwest and Central West approaching that level

North Elmhurst submarkets are on the lower end of relative prices, but have grown 10%+ over the last 12 months

Jan. –Mar. (YoY%)

Submarket'23'22%

Northwest $252$23010%

Northeast $226$274-18%

Central West $322$26920%

Central East $279$295-5%

Southwest $282$2733%

Southeast $290$25912%

Sale prices are lower across submarkets, except Northeast (these values are influenced by the mix of homes sold)

Northeast closed sale price increase in Q1 is an outlier (due to mix) with price per sq. ft. significantly lower

While overall sale prices are influenced by many factors, more growth is expected

Jan. –Mar. (YoY%)

Submarket'23'22%

Northwest $340K$435K-22%

Northeast $350K$340K3%

Central West $637K$758K-16%

Central East $513K$567K-10%

Southwest $480K$488K-2%

Southeast $488K$555K-12%

Over 1,235 new home permits since 2010

Permit activity trailed off significantly in Q1; new homes down 50%+ and demos down 30%+

Demo permits converged with new permits and roughly equate over the last 12 months

Rolling Last 12 Months (YoY%)

Permits