Q1 2023

GLEN ELLYN

LOCAL REAL ESTATE GUIDE

METHODOLOGY

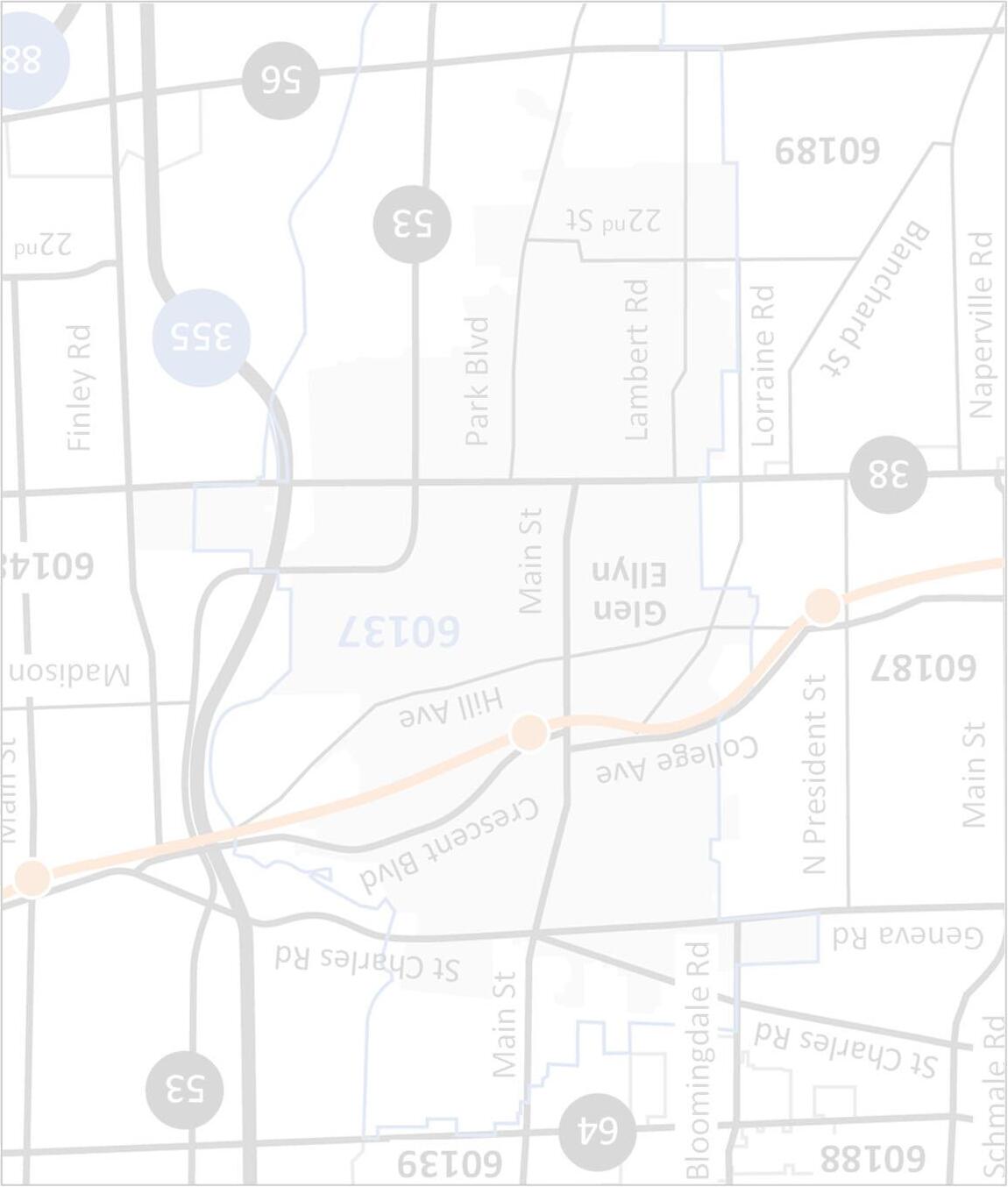

Overview of Terms and Glen Ellyn Submarkets

CLOSED:closed transaction reflecting the final sales price (does not include any seller credits)

CONTRACTED:contingent or pending transaction reflecting the latest asking price

CONTRACT TIME:number of days between the first list date and the contracted date (does not include time from contract to close)

HOME INVENTORY:number of homes currently available for sale

MEDIAN:middle value of a given dataset (all report values are medians, which are less impacted by outliers than averages)

PRICE DISCOUNTS:percentage difference between the initial list and recorded sale price

PRICE PER SQ. FT:ratio of the median price to the median sq. footage of a closed transaction as a relative price measure

NORTHWEST (West of Main St. / North of Pennsylvania Ave. to St. Charles Rd.)

NORTHEAST

(East of Main St. / North of Crescent Blvd. to St. Charles Rd. )

CENTRAL WEST (West of Park Blvd. / South of Pennsylvania Ave. to Roosevelt Rd.)

CENTRAL EAST (East of Park Blvd. / South of Crescent Blvd. to Roosevelt Rd.

SOUTH (South of Roosevelt Rd.)

Note: All figures represent detached single-family homes unless otherwise specified. Price range data based on the village of Glen Ellyn. Submarket figures based on the approximate areas identified on map above and do not include every home within village limits.

2

MARKET SUMMARY

“Seller’s Market” Remains this Spring with Parallels to Last Year

Flattening Relative Sale Prices Sale Price / Price

Overall flat relative prices, but “split market” with higher end increasing / lower end decreasing

Short Market Times List to Contract Days (Q1)

2

lessacross

submarkets

Narrow Price Discounts Sale Price Discounts (Q1)

of homes across price points and submarkets selling at a small discount to

Mostly

weeks or

price points, but certain

longer this quarter

Majority

ask

Per Sq. Ft. (Q1) Home Inventory (Mar) 3% “Seller’s market” with

year low

homesthis time of year Fewer Available Homes Mixed Activity New Home Listings (Q1) Contracted Homes (Q1) 9% 10% Closed Homes (Q1) 4% 3

15+

of available

NEW LISTINGS

New listings were up 10% in Q1 with increases across price ranges, except $800K+

Overall listing activity back to 2015 levels or lower; homes prices below $400K are down dramatically with rising values

Listings appear to be bottoming with activity finally starting to pick up

Rolling Last 12 Months (YoY%)

Jan. –Mar. (YoY%) 4

145 223 114 102 0 100 200 300 400 500 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 <$400K $400K –$599K $600K –$799K $800K+ (-20%) (-32%) (-20%) (-23%) Price Range'23'22% <$400K 211817% $400K - $599K 484020% $600K - $799K 252025% $800K+ 2530-17%

By Price Range

Submarket

Q1 experienced mixed new listing activity across submarkets

Northwest experienced a large increase for the quarter and is the only area with more listings in the last 12 months

New listings in the Central submarkets have fallen dramatically over the last 2 years (Central West increased in Q1)

Jan. –Mar. (YoY%)

5

Months

117 30 104 97 71 0 50 100 150 200 250 300 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 Northwest Northeast Central West Central East South (-44%) (+23%) (-22%) (-28%) (-33%) Submarket'23'22% Northwest 261753% Northeast 67-14% Central West 22215% Central East 2022-9% South 715-53%

By

Rolling Last 12

(YoY%)

CONTRACTED HOMES

By Price Range

By Price Range

Contracted homes declined 9% for the quarter; market is split with higher end decreasing and lower end increasing

Month of March was particularly soft (down almost 30%) after a slightly higher January and February to start the year

Contracts likely to remain mixed based on more new listings but low inventory

Jan. –Mar. (YoY%) 6

Last

Months (YoY%) 107 149 66 66 0 50 100 150 200 250 300 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 <$400K $400K –$599K $600K –$799K $800K+ (-18%) (-36%) (-40%) (-27%)

<$400K 272317% $400K - $599K 453915% $600K - $799K 1522-32% $800K+ 1023-57%

Rolling

12

Price Range'23'22%

All submarkets were lower for Q1 with two areas having less than 10 contracts

Significant increases following the pandemic have returned to historical contract levels (below in some cases)

Northeast submarket generally has the lowest level of contract activity (also the smallest map area analyzed)

Submarket'23'22%

Northwest 1114-21%

Northeast 39-67%

Central West 1520-25%

Central East 2223-4%

South 812-33%

7

Jan. –Mar. (YoY%) (-39%) 60 19 69 71 47 0 50 100 150 200 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23

Central East South (-41%) (-17%) (-26%) (-31%)

By Submarket Rolling Last 12 Months (YoY%)

Northwest Northeast Central West

CLOSED HOMES

By Price Range

Closed homes declined less than 5% in Q1 with larger percentage declines at higher end of market (on a small base of volume)

March closings increased 15%+ following more listings and slightly higher contracts in January and February

Closing activity following overall declines in contracts with low home availability Jan.

Price Range'23'22%

22220%

- $599K 353113%

- $799K 1216-25%

1114-21%

8

Last 12 Months (YoY%) 107 149 62 85 0 50 100 150 200 250 300 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 <$400K $400K –$599K $600K –$799K $800K+

–Mar. (YoY%)

Rolling

(-28%) (-42%) (-45%) (-8%)

<$400K

$400K

$600K

$800K+

By Submarket

Glen Ellyn submarkets mostly lower for Q1, except Northwest (up) and South (flat)

Central areas remain the most active for closings despite some of the largest declines over the last 12 months

Closed activity now back to pre-pandemic levels over the last 12 months (some areas trending below)

9

Jan. –Mar. (YoY%) 65 22 70 75 51 0 50 100 150 200 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23

Northeast Central West Central East South (-37%) (-14%) (-32%) (-26%) (-42%) Submarket'23'22% Northwest 12850% Northeast 18-88% Central West 1415-7% Central East 1620-20% South 11110%

Rolling Last 12 Months (YoY%)

Northwest

HOME INVENTORY

By Price Range

Available homes have declined significantly across price ranges, but inventory is flattening at low levels

Overall inventory is down over 85% from March of 2020 (staggering statistic)

Scarce inventory expected to continue driving “seller’s market” conditions

Mar. Trends (Relative%)

Mar. Quarter End (YoY%)

30% 25% 22% 9% 6% 23% 23% 16% 30% 38% 22% 22% 21% 12% 19% 25% 30% 40% 48% 38% 0% 25% 50% 75% 100% '19'20'21'22'23 <$400K $400K –$599K $600K –$799K $800K+

10

2 12 6 12 0 25 50 75 100 125 150 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 <$400K $400K –$599K $600K –$799K $800K+ (+20%) (-33%) (+50%) (-25%)

By Submarket

Home inventory is down meaningfully across submarkets, despite North areas being up year-over-year

Extremely limited home availability in all areas (only Northwest with over 5 homes)

Mix of home inventory is atypical (nothing available in Central East as an example)

Mar. Trends (Relative%)

Mar. Quarter End (YoY%)

Northwest Northeast Central West Central East South

22% 23% 18% 26% 50% 9% 11% 19% 20% 23% 20% 26% 30% 25% 31% 36% 27% 22% 15% 10% 10% 22% 5% 0% 25% 50% 75% 100% '19'20'21'22'23 Northwest Northeast Central West Central East South

11

10 4 5 0 1 0 15 30 45 60 75 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23

(N/M) (+67%) (-29%) (-80%) (N/M)

CONTRACT TIME

Days between listing date and contract signing have been low (mostly less than two weeks) for a few quarters

During Q1 only homes priced under $400K saw contract times increase (also the case for the last 12 months)

Expect contract times to remain short with very limited home availability

Jan. –Mar. (YoY%) 12

Last

11 5 5 5 0 25 50 75 100 125 150 175 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 <$400K $400K –$599K $600K –$799K $800K+ (-29%) (+10%) (-29%) (-62%) Price Range'23'22% <$400K 16157% $400K - $599K 810-20% $600K - $799K 813-38% $800K+ 820-60%

By Price Range Rolling

12 Months (YoY%)

By Submarket

Contract times were mixed during the quarter with a low number of closings

Days to contract trend is mostly lower; only Central West and South higher in Q1 from a low comparison last year

Homes on the market for more than two weeks could be overpriced or have other factors impacting time / interest

Rolling Last 12 Months (YoY%)

Northwest Northeast Central West

Central East South

13

Jan. –Mar. (YoY%) 7 5 8 5 7 0 25 50 75 100 125 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23

(-58%) (-30%) (-27%) (+40%) (-29%)

Central East 613-54% South 508525%

Submarket'23'22% Northwest 1215-20% Northeast 724-71% Central West 3911255%

PRICE DISCOUNTS

By Price Range

Price discounts across price ranges widened slightly for the quarter

Over the last 12 months most Glen Ellyn homes sold for around full price, except those under $400K

Price discounts expected to remain narrow given limited home inventory Jan.

- $599K 98%99%-1%

- $799K 99%100%-1%

99%99%-1%

14

–Mar. (YoY%)

98% 100% 100% 100% 80% 85% 90% 95% 100% '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 <$400K $400K –$599K $600K –$799K $800K+ (+1%) (-1%) (0%) (+2%)

$400K

$600K

$800K+

Rolling Last 12 Months (YoY%)

Price Range'23'22% <$400K 97%98%0%

By Submarket

Mixed price discounts across submarkets with most areas widening; Central East was flat, and Northeast tightened in Q1

Only one sale in the Northeast closed during the quarter (and at full asking price)

There is slightly more negotiability for buyers so far this year compared to last year (and the last 12 months)

Rolling Last 12 Months (YoY%)

Submarket'23'22%

Northwest 97%100%-3%

Northeast 100%98%2%

Central West 96%99%-3%

Central East 98%98%0%

South 98%100%-2%

15

Jan. –Mar. (YoY%) 100% 100% 100% 100% 99% 80% 85% 90% 95% 100% '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 Northwest

(+2%) (+1%) (+1%) (0%) (+1%)

Northeast Central West Central East South

PRICE PER SQ. FT.

Price per sq. ft. was roughly flat in Q1, but “split market” conditions showed higher end homes increasing and lower end decreasing

Relative prices set new records above $800K for the last 12 months after another strong quarter

Price growth is mixed, but higher end homes experiencing continued appreciation

16

Last 12 Months (YoY%) Jan. –Mar. (YoY%) $205 $250 $262 $314 $75 $125 $175 $225 $275 $325 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 <$400K $400K –$599K $600K –$799K $800K+ (+8%) (-6%) (+5%) (+17%) Price

<$400K

$400K

$599K

$600K

$799K

$800K+

By Price Range Rolling

Range'23'22%

$192$212-9%

-

$225$251-10%

-

$261$23412%

$306$26316%

By Submarket

Most submarkets were up for the quarter, except Central West

Strong increase for Northeast in Q1 despite much lower overall closed sale prices (driven by home size mix); also represents only one closed transaction

Central West declined in Q1 although overall sale prices increased the most of any area (again driven by home size mix)

Rolling Last 12 Months (YoY%)

17

Jan. –Mar. (YoY%) $278 $305 $290 $297 $223 $100 $125 $150 $175 $200 $225 $250 $275 $300 $325 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23

(+16%) (+6%) (+15%) (+9%) (+12%) Submarket'23'22% Northwest

Northeast

Central West

Central East $286$2629% South $223$20210%

Northwest Northeast Central West Central East South

$259$2494%

$334$26028%

$252$265-5%

CLOSED SALE PRICES

By Submarket Rolling Last 12 Months (YoY%)

Overall sale prices were mostly higher for Q1, except the Northeast (one transaction)

Significant increase in Central West pushed overall prices back above Northwest for the last 12 months

South remains on the lower end of prices

Limited home inventory and more updated homes driving increases

Jan. –Mar. (YoY%)

Submarket'23'22%

Northwest $533K$523K2%

Northeast $597K$970K-38%

Central West $593K$470K26%

Central East $615K$568K8%

South $513K$490K5%

$572 $908 $578 $665 $436 $250 $350 $450 $550 $650 $750 $850 $950 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 Northwest Northeast Central West Central East South K (+40%) K (+10%) K (+7%) K (-3%)

K K K K 18

K K K (+9%) K K

NEW CONSTRUCTION

Permit Activity

Nearly 100 new home permits since 2018; activity has mostly declined recently

Nitti Development permits primarily related to homes completed along Fairway Court (issued mostly in 2018 and 2019)

New construction is a relatively small proportion of Glen Ellyn sales

Builder Name# Permits% Permits

New Home Permits Issued

29 22 17 19 11 0 10 20 30 40 '18'19'20'21'22

Yearly Permits (2018 –2022)

19

Nitti

McMaster

Ray

Builders77% Fine Home Builders66% McKeown

Homes55% Oakley Home Builders55% Harding

Homes44% M House Development44% Patrick

Builders44% Ladesic

Scott33% All

C&C Shenuk Construction22% Concorde Builders22% Evermore Homes22% Muellner Construction22% RPV Construction22% All Others2526% Total98100%

Builder Summary (2018 –2022)

Development1616%

/ Faganel Custom Homes77%

Whalen

Classic

Custom

J Murphy

&

Service Concepts22%

COMPARING HOME TYPES Analyzing Glen Ellyn Home Types for Q1 2023 New Listings119920 Contracted Homes97815 Home Inventory3237 Contract Time16 days19 days7 days Price Discounts98.3%97.8%100.5% Price per Sq. Ft. $237$198$183 Closed Sale Price$475K$381K$203K Home TypeSingle FamilyTown HousesCondos 20 Closed Homes80616

COMPARING SUBURBS

21 Analyzing Western Suburb Markets SuburbMedian PriceQ1 YoY%Price / Sq. Ft.Q1 YoY%Contract DaysQ1 YoY% Clarendon Hills$1.3M76%$238-15%37311% Downers Grove$438K-2%$2351%25178% Elmhurst$483K-3%$2786%1838% Glen Ellyn$475K-6%$237-1%1633% Hinsdale$900K-15%$2975%225% Lisle$400K-5%$190-2%814% Lombard$325K-6%$212-2%1721% Western Springs$675K13%$294-6%10-57% Westmont$361K-5%$2110%70% Wheaton$428K1%$2180%12-20%

Compass is a licensed real estate broker and abides by federa l, state and local equal housing opportunity laws. All materialpr esented herein is intended for informational purposes only, is compiled from sources deemed reliable but is subject to errors, omissions, and changes with out notice. Sources include Midwest Real Estate Data LLC and Gl en Ellyn Community Development department. Th is is not intended to solicit property already listed. Glen Ellyn Office 479 N Main St, Suite 230 Glen Ellyn, IL 60137 www.kellystetlerrealestate.com Kelly Stetler 630.750.9551 kelly.stetler@compass.com Teresa Parry 810.569.0078 teresa.parry@compass.com Christina Corso 815.922.0459 christinacorso@compass.com