KEEPING CUSTOMERS ON BOARD

24.05

Major banks boost tech and broker support HOW BROKERS RATE NON-BANKS

Hands-on approach and flexibility win praise

TOP SOLUTIONS FOR SMES

Non-banks are stepping up

Chris Bates Flint

KEEPING CUSTOMERS ON BOARD

24.05

Major banks boost tech and broker support HOW BROKERS RATE NON-BANKS

Hands-on approach and flexibility win praise

TOP SOLUTIONS FOR SMES

Non-banks are stepping up

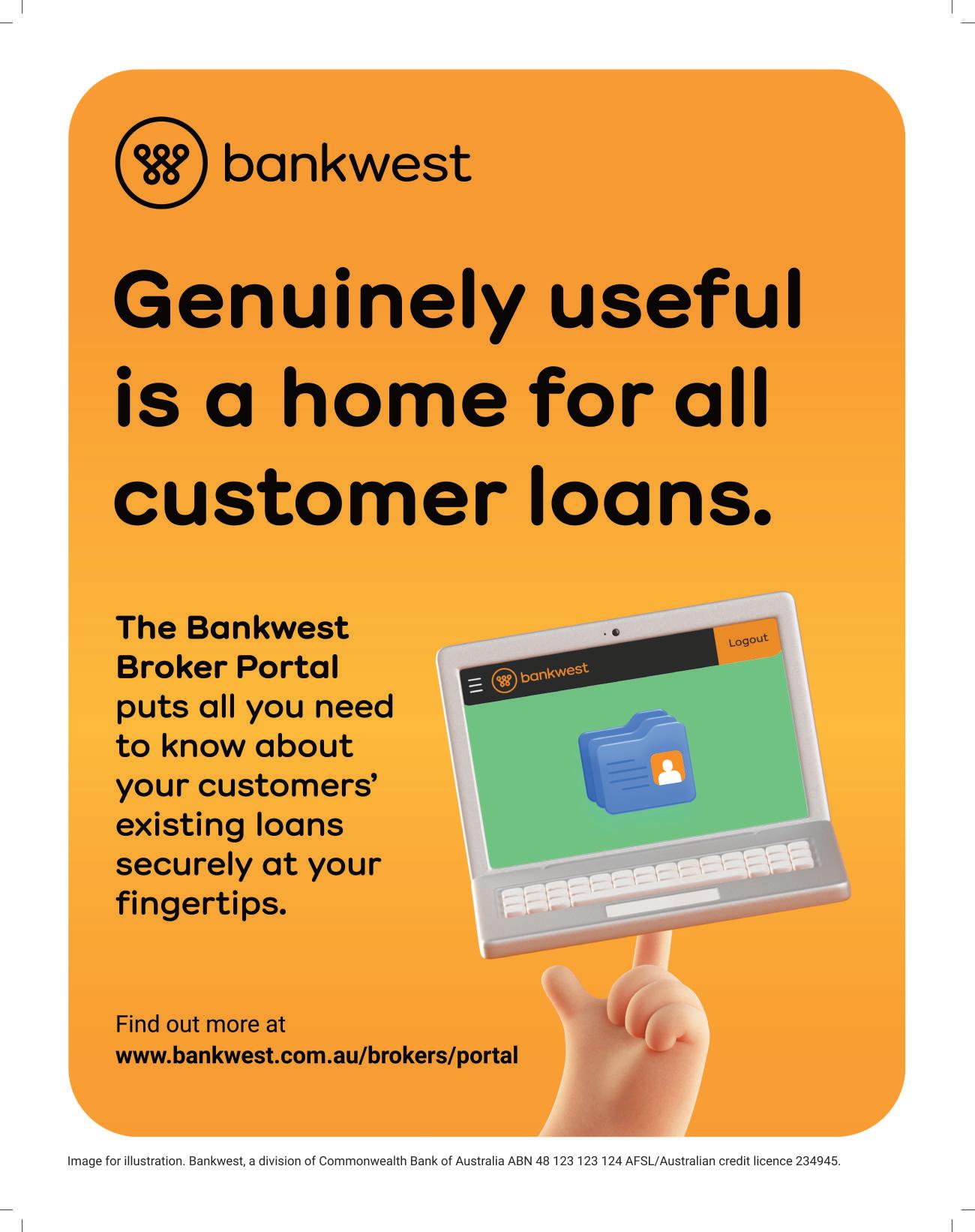

At ANZ, our commitment to the relationship we have with brokers is as strong as ever and will remain that way in the future.

ANZ & BROKERS WORKING BETTER TOGETHER

ANZ Broker

CONNECT WITH US

Got a story or suggestion, or just want to find out some more information?

twitter.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

02 Editorial

Brokers will see the rewards of building strong client relationships

04 Statistics

Home prices heading upwards

06 Opinion

For brokers, change is not only inevitable but necessary, says Blake Buchanan

MPA’s annual survey highlights what brokers value most about working with non-bank lenders – and unveils this year’s top medal winners

Flint’s co-founder talks about the development of a brokerage with a unique business model that puts the broker in the driver’s seat

Prioritising products, relationships and service wins Bluestone top marks from brokers

58 FHBs remain positive

How brokers can help first home buyers achieve their dream

64 e tech revolution

Will the industry make the most of AI’s potential to unlock business e ciencies?

67 Five questions to ask yourself

Tips for priming your mindset to maximise focus and productivity

70 Brokerage insight

Top 100 broker Thaer Burbar is reaping the benefits of a diversified brokerage

72 Other life

Sharing the joy of fishing helps Mohammed Zahr build business relationships

Major banks discuss how they are boosting tech and working to support brokers and their clients 32 FEATURES STEPPING UP

Non-banks and brokers are there for small businesses that need tailored and flexible finance solutions 48 FEATURES

Our daily newsletter. Keep on top of property market trends, business strategy, and what industry leaders have to say.

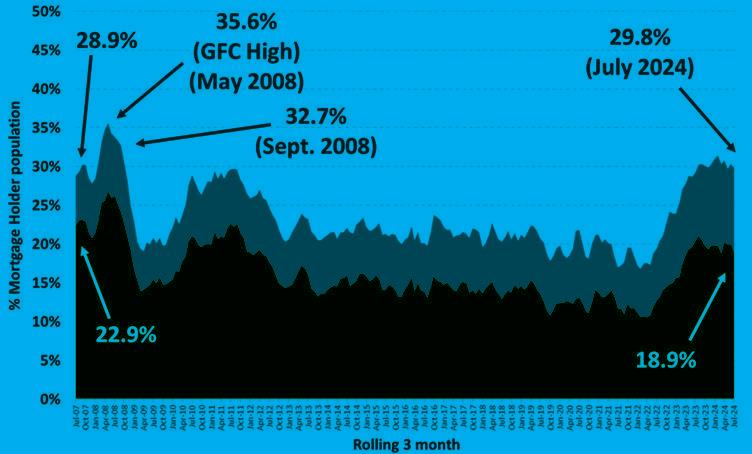

There’s no doubt times remain tough for homeowners, but there are signs of better days on the horizon, and brokers, as always, will have a key role to play in turning things around Australia’s economy continues to lag due to a per capita recession, with GDP per capita falling 0.4% in the June quarter, marking the sixth successive decline. Despite inflation moderating, Aussies are feeling the pinch of the cost of living crisis. And while the official cash rate hasn’t moved since November, mortgage holders are still impacted by higher interest rates due to the Reserve Bank’s 13 cash rate increases since May 2022.

But the MFAA’s August 2024 refinancing and mortgage stress survey, of 372 mortgage brokers, reveals some improvements for borrowers. It shows that while loan serviceability remains the number one challenge for borrowers, only 68% of brokers identified it as the main reason clients had been unable to refinance in the past six months, compared to more than 80% previously.

The number of brokers’ ‘mortgage prisoner’ clients also fell, from 82% in July 2023 to 69% in August 2024. And over half (56%) of brokers found the 1% serviceability buffer for ‘like for like’ refinances had made it easier for their clients to refinance.

Customer

Customer Success Executive Shara Cruzat

4711

antony.field@keymedia.com

SUBSCRIPTION ENQUIRIES tel: +61 2 8311 5831 • fax: +61 2 8437 4753 subscriptions@keymedia.com.au

ADVERTISING ENQUIRIES claire.tan@keymedia.com

However, the cost of living is a growing concern. More than a quarter of brokers surveyed said it was the most likely reason for financial stress. But two stats stood out – 91% of brokers said clients had used them for the first time to refinance, and 98% had helped clients refinance to a new lender in the previous six months.

What this says is that brokers continue to enjoy the trust of borrowers who need brokers’ expertise to help them navigate the complex and competitive world of lending.

While the refinancing boom is over, borrowers are still looking to brokers to help them find a better deal. This will only ramp up when the RBA eventually cuts interest rates and the economy improves. It’s then that the efforts of brokers to build strong relationships with their clients will pay off.

In this issue of MPA, we explore several market segments that bring opportunities for brokers, including SME lending, first home buyers and the development of broking technology. In our annual Major Banks Roundtable we look at how major banks and their broker partners have worked together over the last 12 months.

The results of the 2024 Brokers on Non-Banks are revealed, and the Big Interview cover story focuses on brokerage Flint, which has a unique structure and strategy.

Enjoy reading MPA’s October edition.

AUSTRALIAN BROKER simon.kerslake@keymedia.com T +61 2 8437 4786 NZ ADVISER alex.knowles@keymedia.com

T +64 9 200 1319

CANADIAN MORTGAGE PROFESSIONAL chris.anderson@keymedia.com

T +1 720-441-2255

MORTGAGE PROFESSIONAL AMERICA chris.anderson@keymedia.com

T +1 720-441-2255

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com

T +44 203 868 3406

$10.9trn

Value of Australian residential real estate

National home values rose 0.5% in August, marking the 19th consecutive month of growth, though the pace is slowing, CoreLogic reports. The quarterly increase was 1.3%, less than half the rate of the same period in 2023. Growth varied regionally, with Perth, Adelaide and Brisbane seeing the strongest gains, while Melbourne, Darwin and Hobart experienced declines.

$1.2trn

Value of Australian commercial real estate

PropTrack reported a 0.22% rise in national home prices in August, marking 20 consecutive months of growth. Perth led with a 23.2% annual increase, while Melbourne prices fell

11.2 million

of Australian dwellings

Proportion of household wealth held in housing

in August, declining for the fifth month in a row. Tight supply and strong demand drove growth in markets like Perth, Adelaide and Brisbane, while Melbourne faced weaker momentum and investor challenges.

Household deposits at Australia’s banks reached a record $1.5 trillion in July, with $30.8 billion added that month. Since the start of rate hikes in April 2022, deposits have increased by over $230 billion, according to APRA data.

The

value of new housing loans rose 1.3% in June to $29.2 billion, with investor loans rising 2.7% and owner-occupier loans up by 0.5%. Investor lending rose 30.2% annually, led by strong growth in NSW, Qld and WA, the ABS reports.

VALUE OF NEW BORROWER-ACCEPTED LOAN COMMITMENTS (SEASONALLY ADJUSTED)

The total number of dwellings approved in July rose 10.4% to 14,797, following a 6.4% decrease in June. Despite this increase, approvals remain 5.1% below the five-year average, according to ABS data.

Change is not only inevitable but necessary for brokers to successfully serve their clients long into the future, says SFG’s Blake Buchanan

I HAVE seen a lot of great things happening within the mortgage broking industry over the last two decades and in particular the excellence that we have achieved in serving our clients. As Australians’ preferred choice of finance vehicle when it comes to asset ownership, brokers have loyally and professionally served their clients and now dominate the lending landscape.

For many years I have heard the pundits talk about adaptability, and I have learnt that this is more than a simple cliché; rather, it is the most appropriate noun to describe brokers.

In the scheme of things, we are a relatively young industry, having been around for less than 40 years. When you reflect on our age and the important work we do, alongside the many changes and scrutiny we have faced – whether involving remuneration, regulations or other areas – in hindsight, we see that much of this has made us stronger and highly regarded by the most important stakeholders, such as lenders, clients and the government.

Nonetheless, and regardless of whether we want change or not, it is not only inevitable but required, particularly if we are to continue to serve our clients beyond the mid-term.

why

A common theme of ‘our why’ is that we want to help people. This is the primary response when you ask brokers why they got into this industry, and it is one of the things I am most proud of.

The lending landscape is complex and competitive – this is why borrowers need brokers. Whether borrowers use a broker or

not, they all benefit from brokers. This is because brokers open up competition and drive interest rates and fees down as lenders compete for your business.

Just as people seek out accountants for tax advice and help with returns because they are experts, consumers similarly seek out brokers in the lending field to validate their borrowing choices. The key word here is ‘people’, as people want to have a relation-

Running a business is hard, but it is made harder if you are smaller and need to look after all facets of a business yourself. This requires a high degree of business discipline to achieve success, and many more brokerages are opting to outsource and/or scale up so they have assistance in running their businesses.

There will always be new problems to solve, but for today we can solve many that will have a meaningful impact on our businesses and the service we o er.

By taking the time to review your biggest asset – your client base – you can discover how to be more e cient. It’s crucial to know key market insights, such as client behaviours, run-o , conversion rates and why clients choose us. With a deep understanding of your business, you can identify areas that will improve your service and output.

If you wonder about high-performing brokerages and how they have the time to

We can see the trend of brokerages becoming more sophisticated and structured as single-operator numbers decline in favour of growing or joining a firm

ship with someone who can be trusted, who can guide them and be their expert.

Brokers will always be required, but this does not guarantee that we will be as relevant to future generations without adapting.

‘How we do things’ will change, but ‘what we do’ won’t. This is why we must continually review our model and adapt to ensure that we remain relevant and accessible to borrowers, serving their best interests.

We can see the trend of brokerages becoming more sophisticated and structured as singleoperator numbers decline in favour of growing or joining a firm.

As our industry is continually scrutinised, mortgage brokers should also scrutinise their business models and sustainability in a changing finance world.

do it all, it is because they are always reviewing their own performance and making adjustments.

If you are looking for somewhere to start, begin by building your customer experience process. This is really about penning a process for how your customers experience your service.

Then, engage your systems providers to customise and automate as many of these interactions as possible. That way you will have a consistent approach and be well on your way to maximising output against e ort with better results.

MPA Top 100 broker Chris Bates talks about the development of Flint, a new type of brokerage that provides brokers with the tools and support to drive success while ensuring they retain ownership

mortgage broker Chris Bates has a vision: to develop brokers into niche experts who are equipped with the tools to reach their true potential and can retain control over their own businesses.

Bates, who has featured in MPA’s Top 100 Brokers list in the last four years – 2020, 2021, 2022, 2023 – and this year too, is the managing director of financial services brokerage Flint. He and Flint CEO Christian Stevens launched the business in February 2024 with a focus on providing an extensive range of lending solutions, superior technology, and a unique business model that puts the broker in the driver’s seat.

Bates has been in the mortgage industry for a decade and says his first five years as a broker were very difficult.

“The first five years were incredibly tough; I only settled $130 million,” Bates says. “Even after having seven years as a financial adviser and knowing how to sell advice, the transition to building an excellent mortgage brokerage is much more complicated than anyone believes.

“There are enormous challenges in building a talented team and driving efficiency while maintaining profitability and a trusted engine required to scale up.”

Bates started Blusk, a joint financial advice and mortgage broking business, in 2014, partnering with Ben Sum, who is now an owner of Flint alongside Bates and Stevens. The

pair sold the financial advice division of Blusk in 2020 to focus on mortgage structuring, helping higher-income Australians with complex property strategies.

“We learnt many lessons and settled over $1.4 billion,” says Bates. “More importantly, we built an engine and process required to scale.”

Among the lessons learnt were how to deliver great client experiences by providing quality

boutique brokerage mindset and build something more impactful”.

Flint aims to become a national, advicedriven finance brokerage, says Bates. Its strategy is to have a group of brokerages operating under one process and one team to change the financial future and lives of 10,000 Australian families annually.

Flint has developed a unique business

“The elephant in the room must be addressed: why would you work in a brokerage and not own your trail book or any of the business?”

advice and building a solid reputation in a target market. These strategies came in handy when Bates and Stevens met in 2019 and eventually formed a partnership five years later.

“We openly shared learnings, debated our plans and celebrated each other’s success,” says Bates.

He and Stevens discussed creating something more significant. “We knew the future of broking needed a much bigger team and investment in consumer-leading technology to thrive in the digital revolution of broking.”

Realising that their strengths, as well as those of Sum, were complementary gave the trio the “confidence to step out of a small

model – Flint Director. “This offers to elevate highly aspirational, experienced and talented brokers by building a long-term profitable asset they own in an environment, team and system that helps them settle much more and much faster than they would achieve trying to make a brand themselves,” Bates says.

The director model enables brokers to confidently focus all their energy on frontend business-generating activities, knowing they have an experienced back-end team to deliver exceptional customer experience and strategic advice.

“We focus on developing brokers into niche experts, powering them with sales tools and

Name: Chris Bates

Title: Managing director, mortgage broker

Company: Flint

Years in the industry: 10

Career highlight: “Moving from a sole broker to building a genuine business. I went from struggling to settle $45 million to settling $320 million in just three years and will do $500 million plus this financial year”

Career challenge: “The biggest challenge was building a business, brand, culture and team that people want to be part of in the long term”

technology while leveraging social media to build an online brand presence that enables them to land critical strategic partnerships,” says Bates. Brokers have everything they need to break out of the $50 million to $100 million club and comfortably rise up the MPA Top 100, he adds.

Flint also harnesses brokers’ strengths in di erent sectors of the market. Current Flint Directors specialise in areas such as first home buyers, private banking, advice partnerships, sports and media professionals, over 50s, real estate partnerships, digital partnerships, women and agribusiness.

“Other key areas we are looking at are commercial, development, expats, professional investors and many more.”

Directors receive support to develop their personal brand, niche-relevant collateral, pitch packs, marketing funnels, thought leadership, podcasts, video content and partnership agreements. “We have built a regular mentorship program from two brokers who have built personal brands from the ground up, all within a custom-built, inspiring o ce environment where directors work together on their businesses,” says Bates.

Flint’s philosophy is to work smarter, not harder, and use client-focused technology and automation as much as possible. This includes HubSpot for marketing automation and lead nurturing and Broker Engine for its CRM.

“We’re currently doing a lot of work with AI and will be rolling out several tools to assist our brokers with outbound multichannel conversations at scale so they can supercharge their growth.”

Flint has an Australia-based, highly qualified strategy team, mainly with CPA and financial planning expertise, which heads up the directors’ support team. This team dramatically increases opportunity conversion.

“Brokers have a team with the knowledge, expertise, top-tier bank status and ability to quickly produce a highly personalised strategy to give the director an optimal chance to win the client,” says Bates.

Once the client joins, over 30 team members are available to provide customer experience,

Brokers retain legal ownership of their clients and trail book

Brokers are given the support to become niche experts – Flint provides them with sales tools and technology and leverages social media to build the brokerage’s online brand

Some of the niche areas serviced include rst home buyers, private banking, sports and media professionals, over 50s, real estate partnerships, advice partnerships, digital partnerships, women and agribusiness

Brokers have the support of a highly quali ed strategy team, featuring CPA and nancial planning experts who help increase conversions

The directors’ support team looks after customer experience, credit, loan processing, and settlement and post-settlement services for brokers

was born. Unlike traditional brokerages, Flint’s structure ensures brokers “are in complete control of their future”.

“You’re creating an asset you own and can settle much more than if you are alone, as the team, systems and processes are already built,” says Bates.

“The elephant in the room must be addressed: why would you work in a brokerage and not own your trail book or any of the business?”

Flint created legal ownership for brokers from day one. “If a broker decides to leave, a buy-or-sell event demonstrates how they own their client book long-term.”

In the past, aspirational brokers had only a few choices – they could work as employees or contractors within a business, join a franchise or start a new brand and business. Bates says these options have holes, which is part of why the broking industry is primarily made up of ‘one-broker bands’, with few larger, successful independent brokerages and franchises.

“We believed there had to be a better way to grow a brokerage that top brokers wanted to be a part of and [that] would be mutually beneficial”

credit, loan processing, settlement and postsettlement services.

“Ultimately, Flint’s o er removes the challenges of running your own business and the often-unspoken opportunity cost of distractions to their business growth,” says Bates.

Brokers who become directors are more content because they are part of a team and achieve a better work-life balance.

Bates and Stevens had looked at other successful brokerages for a model that worked.

“We couldn’t find one, and we believed there had to be a better way to grow a brokerage that top brokers wanted to be a part of and would be mutually beneficial,” Bates says.

After months spent on research and getting tax and legal advice, the Flint Director model

Large independent brokerages struggle to grow because of the di culties of developing and keeping a talented broker team who can drive growth. Bates says most top brokers eventually decide to leave and start their own businesses to build assets they can one day sell.

He says the contractor model has faced legal challenges related to sham contracting, franchise law and broker asset ownership, while franchises don’t appeal to top brokers because their brands often don’t align with their target market and can present growth challenges.

“We want brokers to join and stay with us long-term because they own an asset, and just as importantly, Flint is a high-value-adding business partner that truly powers their growth.”

Partner with Prospa to help make business happen for your small business clients.

Fast approvals with funding possible in hours

Business loans up to $500K with 5 year terms for lower weekly repayments

Line of Credit up to $500K to simplfy cash flow

Unlimited extra repayments to help businesses save on interest

Brokers value non-banks’ personalised, hands-on support and flexible credit policies over brand recognition and commissions but signal growing concern over rates and fees

MPA’S Brokers on Non-Banks 2024 survey cements the broker-lender relationship as a cornerstone of the complex mortgage market. Non-bank lenders continue to carve out a bigger chunk of market share by combining high-quality products with competitive pricing and delivering them with speed.

Hundreds of brokers from across Australia scored the performance of non-banks across 10 metrics, propelling the highest achievers into the winners’ circle.

This year’s data indicates that the best non-bank lenders have strengthened their ties with brokers by adapting their strategies in response to shifting third party channel and customer needs.

One broker highlighted a non-bank lender’s exceptional performance on an unconventional refinancing assessment: “Their flexibility in accepting the client’s situation and recognising that the refinance would greatly improve their financial situation was remarkable.”

Non-banks’ expanding lending prowess –rising to 16% of Australian commercial real

estate debt (ACRED) from 10.4% in 2020 –is no small feat. They have capitalised on opportunities the big four may have missed and were quick to cater for underserved consumers.

“The banks have contracted their appetite for anything that doesn’t fit neatly inside a box,” says National Mortgage Brokers (nMB) managing director Gerald Foley.

“Non-banks see less volume and try to understand individual borrower needs and price risk accordingly. We’re seeing more complicated cases, especially with selfemployed borrowers, that banks struggle to accommodate.”

As in years past, brokers ranked turnaround times among their top priorities, suggesting speed remains critical. There’s general satisfaction, as over half of brokers believe non-banks have improved, and a significant portion noted no change:

• “Most non-banks pick up the deals in less than 48 hours”

• “They seem to be working faster to obtain approvals for us”

There was a striking shift in brokers’ expectations of non-bank lenders as BDM support and credit policy shot to the top of their priority list at first and second place, respectively, from seventh and last place in 2023.

This revelation highlights a need for proactive communication and guidance from brokers’ non-bank partners, as well as lending policies that are in tune with evolving consumer needs and market conditions.

David McQueen, Loan Market’s CEO, points out that non-banks are keenly aware of broker needs, and some of the country’s best BDMs and credit assessors work for them. Delivering on these aspects is essential to giving brokers confidence in their proposition.

“As funding has become more expensive and challenging, non-banks have tilted away from competing against the majors to increase their focus on policy and servicing niches,” McQueen says.

“Competitive pricing is important, but certainty is even more so. For example, can

a lender make this loan work, and how quickly? The best non-banks can make it clear if they can do the loan and how quickly. Consistency is key, and this has never really changed.”

Brokers’ continued emphasis on interest rates, which rose in priority to fourth place from eighth last year, underscores their sensitivity to the impact of competitive pricing on their ability to help clients achieve their financing goals.

Better rates are a familiar chant among brokers. Only 6.1% listed competitive rates as a reason to pick a non-bank lender over a mainstream bank:

• “Non-banks are getting better with easier conditions, but interest rates are still a barrier to many clients in this high cost of living environment”

• “It’s down to rates and fees, I’m afraid”

Lending products remain a central focus for brokers this year, who gave enthusiastic thumbs-ups for Alt Doc and Alt Doc Prime as the best non-bank products of the year from these leading lenders:

• Bluestone Alt Doc: “simple verification process and fast turnaround times”

• Pepper Money Alt Doc: “the best that I have seen so far; using BAS and self-declaration of income has been favourable for my clients”

• Resimac Alt Doc Prime: “by far and away the cheapest solution for low-doc applications”

Two significant changes in brokers’ priorities are worthy of note: a sharp drop in brand recognition as a priority suggests brokers desire functional factors and practical support over brand identity; and a shift away from communications, training and development further underscores the need for more direct assistance from non-bank lenders and their representatives.

In this year’s survey, brokers were asked to rank non-bank lenders across 10 categories: BDM support; brand recognition; commission structure; communications, training and development; credit policy; interest rates; online platform and services; product diversification opportunities; product range; and turnaround times. Brokers could rank the non-banks with a score out of five in each category.

Only those institutions that achieved a response rate of at least 10% of brokers for each non-bank were included in the final list.

The survey also recorded broker responses on their preferred non-banks in these areas: specialist lending; first home buyers; property investors; commercial; alt doc; SMSF; and foreign non-residents.

MPA asked the brokers a series of questions relating to their business with non-bank lenders, as well as which non-bank they would like to see added to their aggregator’s panel, but these did not influence the overall score.

Non-banks saw a rebound in the number of broker loans put through, with brokers emphasising the need for flexibility to keep momentum going

MPA’S SURVEY showed a significant recovery this year in the proportion of brokers who put loans through non-banks to 67%, nearly catching up with 2021’s high of 69%. This follows a sustained decline beginning in 2022 and bottoming out at just 50% in 2023.

This improvement shores up the nonbank lenders’ increased market share and attests to their efforts over the past year to boost their offerings, service to brokers and competitive products.

“The non-banks seem to be looking less for cookie-cutter applications and will take the time and dedicate the resources to assess scenarios individually,” nMB’s Gerald Foley explains. “Non-banks often need to be nimble, so having the ability to identify niches and change product parameters quickly to meet these opportunities helps brokers enormously.”

The percentage of brokers putting the lowest proportion of loans (20% or less) through a non-bank declined to 50% this year, versus 60% in 2023.

At the high end of loan volume, 10% of brokers put more than 60% of their loans through non-banks than last year, showing an encouraging increase from 8% in 2023.

Non-banks have picked up market share after a period of decline, which industry experts attribute to consumer confidence during uncertain economic times, and service propositions, among other factors.

Loan Market’s David McQueen emphasises that non-banks are often faster at responding to consumer needs and less restricted by regulatory burdens.

“Non-banks do not have the same buffer and affordability issues that banks have, and this has led to an increase in non-bank

HAVE YOU SENT MORE LOANS TO NON-BANKS IN THE LAST 12 MONTHS THAN IN THE PREVIOUS YEAR?

volume,” he explains. “In addition, they have been better at identifying underserved customers. SMSFs and self-employed customers are excellent examples of [where non-banks] have quickly gone to market and addressed customer needs.”

The expected proportion of loans forecast to go through non-banks in 2025 is significantly lower than last year’s estimates – 36% versus 47% – suggesting that nonbank lenders may need to adapt their product and service offerings further to retain broker support and remain competitive.

While growing overall, the non-bank sector faces upcoming challenges and opportunities, including its inclusion in Australia’s Consumer Data Right open banking scheme, targeted for November 2024. ASIC is also investigating potential new regulations.

The opportunities lie in non-banks strengthening their oversight and transparency on governance and risk management, factors that will improve relationships with brokers and benefit their clients.

Brokers stated that non-bank lenders remain the best choice for diverse customers, particularly the self-employed. They offered the following reasons for this:

• Flexible credit policies: comments highlighted credit policy flexibility and understanding, and willingness to accommodate various client needs

• Specialised loan products: catering to niche markets, such as low doc, alt doc, SMSF, special situations, commercial loans and unique client requirements, allowing brokers to expand their businesses through diversification

In the ranking of reasons for using a non-bank, the significant rise in clients lacking standard documentation indicates that brokers serve more clients who don’t fit the traditional borrower mould, such as freelancers, small business owners and others who struggle with mainstream bank requirements.

On the other hand, the pronounced decline – to third place from top spot last year – in non-banks taking a wider view than credit score suggests that, while this factor is still relevant, non-banks may be the first choice for clients with documentation issues rather than poor credit.

Commenting on a lender’s SMSF product, one broker highlighted “strong servicing and lower level of documentation requirements compared to other lenders”.

Although personalised service placed fifth again this year, brokers ranked it higher than in 2023, highlighting the trend towards a tailored, client-centric approach that the top non-banks are leveraging to position themselves as the friendlier alternative to the mainstream’s more rigid bank experience.

A positive shift in borrower perception towards non-bank lenders signals significant strides the sector has made in reputation and client satisfaction, o setting concerns about brand awareness

BROKERS’ RATINGS of the benefits of using non-banks in 2024 spotlight the growing acceptance year-over-year of nonbank lenders and their products – and illuminates the highly competitive nature of the sector. Although there is a clear runaway winner, a relatively minor point di erence between the gold, silver and bronze medallists highlights the close competition among the top contenders.

The top three non-banks overall won nine golds, five silvers and three bronzes across all categories except for interest rates. That accolade went to the fourth-place winner overall, Resimac.

Bluestone ended Pepper Money’s six-year streak, winning gold for BDM support as part of a strong performance overall. RedZed and Prospa earned a joint silver for turnaround times; RedZed took the bronze medal for communications, training and develop-

From credit decisioning to settlement, brokers can speak directly to the case managers and their dedicated Relationship Manager.

Access to a range of tools and calculators, giving you more control and certainty for your clients before, during and post settlement.

Greater visibility and control of your in-progress applications and post settlement client information.

We consider the circumstances of every individual and have a flexible credit policy and lending options to suit your customer scenarios.

Access the same home loan tools as the assessors

Providing your client with accurate information and a faster decision time.

Always get an answer quickly with our consistent turnaround times of 1-2 days.

ment; and Pepper Money won three golds for product range, product diversity opportunities and brand recognition.

Non-banks in the middle of the rankings with gold wins included ORDE Financial for commission structure.

As in previous years, the golds determined the ultimate champion, and Bluestone was crowned first place overall with a score of 4.07 out of 5. This result, and the other top lenders’ final tallies, outshone last year’s by a significant margin, a testament to the ongoing improvements brokers praised.

RedZed emerged among the top three non-bank lenders brokers wanted to see added to their aggregator panel this year, with ORDE Financial claiming first place and Liberty coming in second.

Interest rates are on one side of a doubleedged sword for brokers doing business with non-banks, with 68% citing high rates and fees as the main barrier to flowing more business their way. This can send brokers and their clients to mainstream banks out of the sheer need for more a ordable rates. Brokers appreciate the competitive edge non-banks bring to the market, but some have concerns:

• “Rates are the only reason I don’t use them more”

• “Most of my clients are seeking to refinance to [mainstream] banks within a year due to lower interest rates”

• “Five years ago, fewer non-bank lenders were available, and their rates were horrendous. With more competition in the market, they have become more viable”

• “I think non-banks have improved their o erings but have a way to go in terms of rates”

• “Service levels are being delivered better than mainstream banking, and the real opportunity will be to get into mainstream lending at competitive LVR-banded rates”

• “Postcodes could also do with a review around the nation, as well coming alongside mainstream banking”

Some brokers took a more nuanced approach to non-banks’ pricing, citing their innovative product o erings and flexibility as standout:

• “With the major banks jacking up their interest rates on SMSF loans that they no longer want on their books, it’s an

opportune time to o er the lower rates”

• “Flexible when the client hasn’t completed tax returns”

• “Takes into account di erent scenarios for self-employed clients that might not have two full years of financials at the same income level that they are currently earning”

• “Ability to consolidate tax debts and get clients out of bad situations at a cost that’s not overly expensive”

• “Enables me to put clients into a better financial situation, and then, with guidance, refinance them to a better interest rate once the situation improves, without me losing my income”

The second barrier to using non-banks was a lack of brand awareness, and while a consistent theme year after year, it ranked last on brokers’ importance scale in 2024. Non-bank brand awareness appears healthy, as just 12% of respondents noted it as a barrier this year, compared to 11% in 2023, 20% in 2022 and 27% in 2021.

The number of brokers whose clients were typically open to considering non-bank products has dramatically reversed, rising to 91% and stemming a three-year decline. Last year, 82% expressed confidence in non-bank products, compared to a high of 90% in 2021.

Bluestone won the gold medal for credit policy as well as BDM support, underscoring its strong product and credit knowledge that brokers perceive as a frontrunner.

“Having easy access to a local credit team to back up the BDMs also helps to workshop scenarios to be confident that the answer in the discussion will match the final answer when the application is submitted,” says nMB’s Gerald Foley.

Loan Market’s David McQueen adds, “The role a BDM plays in non-bank lending is critical. Non-banks often support more complex client needs as they can explain what they can and can’t do and respond quickly and correctly on scenarios.”

The survey’s overall results show that brokers increasingly value personalised service and adaptable policies in the complex lending environment. Direct and practical support in helping them grow their businesses trumps a non-bank lender’s brand image.

Non-banks that prioritise operational efficiency while balancing leading-edge service offerings will maintain broker satisfaction.

A majority of brokers noted continued improvements in turnaround times, and there is a rising call for enhanced communication to process loans e ectively

NON-BANK lenders have heard brokers’ clarion call on turnaround times being crucial to making or breaking a deal. This year, a record-high majority of brokers – 87% – said turnaround times had improved or remained satisfactorily the same. Far fewer brokers than last year, 12% versus 17%, felt speed had worsened.

nMB’s Gerald Foley observes that most non-bank lenders deliver an acceptable turnaround time, making this factor much less of a di erentiator than in previous years.

“Di erences occur when an application needs more time to understand the transaction’s pros rather than simply finding reasons to say no,” he says. “With risk-based pricing, non-banks often have greater flexibility.”

Brokers credited enhanced support from top non-bank lenders’ BDMs in quickly executing deals, giving a general sense that more specialist lenders o er quicker turnaround times on assessments, approvals and settlements.

Non-banks have strengthened their processes, resulting in faster turnaround times, as noted by brokers:

• “Most non-banks take a common-sense approach, so it helps when assessors pick up the phone and call the broker for a quick chat”

• “I had a loan looked at, approved and settled within days, and the service was first-class”

• “My BDMs push my deals to the front of the queue every time”

Brokers among the small group who believed that times had worsened noted the increased complexity of some deals and lenders’ operational ine ciencies as reasons for this:

• “More volume leads to slower turnaround times”

• “Sta ng levels don’t seem appropriate”

• “It takes much longer when it is a little outside of the box”

Bluestone won gold in the turnaround times category with a hefty margin above its nearest competitor. Brokers mentioned the non-bank specifically for “its BDM support”, which consistently helps speed and e ciency. Again this year, La Trobe Financial did not rank well for turnaround times. Still, it picked up four medals, including silver for interest rates and bronze for credit policy. Brokers also named La Trobe Financial as their preferred lender for foreign non-residents

and commercial categories, niches in which it dominates.

Brokers’ suggestions for how non-banks could improve their service remain consistent with last year’s. However, slightly fewer brokers said simpler income verification and better-trained BDMs and credit assessors were problematic, demonstrating the progress non-banks have made in these areas.

This year, there was a moderate rise in the number of brokers seeking better communication as a component of exceptional service. Feedback from survey respondents included:

• “Better written processes and after-care, plus better-written checklist and policy”

• “Better rates with higher borrowing capacity”

• “Assessors who understand valuations better”

The proportion of brokers who believed better technology could boost service levels remained consistent with 2023 at 24%, suggesting that the steady improvements non-banks had made hadn’t shifted brokers’ perceptions one way or the other.

None of this year’s top non-banks cracked four out of five marks from brokers for their online platform and services, underscoring the need to embrace new and emerging technologies to create seamless and broker-centric processes, stay at the cutting edge and increase market share. Turnaround times

91% likely to use a mortgage broker to obtain a loan for their property.

Discover more insights into the behaviours and attitudes of over 3,000 first home and additional property buyers.

Source: Helia Home Buyer Sentiment Report 2024. n=3002 total.

“Not yet. In terms of product flexibility and policy decisions, they’re good, but the pricing is not since the cost of funding from non-banks is still at high levels”

“Non-bank policies tend to be more lenient and understanding of a client’s financial position”

“They offer faster turnarounds and better BDMs, who actually care and want to service you and your clients”

“They’re not competitive on rates. Systems are not up to scratch, and service levels must improve post-settlement. There are lots of disgruntled customers when dealing with overseas call centres”

“Rates are always a factor, but that’s not non-banks’ niche”

“No, because most are too clunky during the process and charge for valuations instead of o ering free valuations like mainstream banks. Non-banks also have limited internet banking compared to other banks”

“Non-banks are the most crucial element to the future of mortgage broking. At all costs, we must use non-bank lenders at every reasonable opportunity. Without them, our industry will die”

“They provide an alternative view on lending and an opportunity for borrowers who would otherwise not have been able to access credit”

“They are providing more solutions and reasonable serviceability options for the current market conditions”

“Somewhat, but there is more to do. What is disappointing is when non-bank lenders decide to take on bank policies”

Bluestone stormed to victory in Brokers on Non-Banks 2024, with medals in eight out of 10 categories and voted as brokers’ preferred specialist lender

“WITH A focus on digitisation, we’re investing in new technology to improve and further streamline our approval processes and speed up decisions,” says Bluestone’s chief commercial o cer, Tony MacRae. “We aim to achieve same-day, and often instant, approval for over half of the applications we receive.” Bluestone’s winning strategy involved supporting brokers with the right people in the right roles. The non-bank grew its BDM team by 33% and introduced a state-based

leadership model with senior people on the ground. An education-first approach gave brokers access to industry-leading experts.

“This was evident in the work we did in the SMSF space, providing market-leading education on the set-up and working of SMSFs and borrowing within such structures,” MacRae says. “We aim to help brokers grow their business, ensuring they can help a broader range of customers.”

Simplifying processes and eliminating

unnecessary documents underscored Bluestone’s top performance, cutting the time to unconditional approval by more than half in the last 12 months.

“Through smart technology, simplified processes, access to credit decision-makers, and BDMs focused on helping brokers grow their business, we can continue to help more brokers and their customers deliver upon their financial and homeownership goals,” MacRae says.

. What strategies or practices set Pepper Money apart in winning gold medals for product range, product diversification opportunities and brand recognition?

Barry Saoud, general manager mortgage and commercial lending: Our strategy focuses on being the first-choice and leading non-bank, enabling our customers and brokers to succeed. We’ve achieved this through invaluable feedback we’ve received from brokers and customers.

Our emphasis on diversification of credit policy, industry-leading technology and e ective BDM support has enabled us to provide brokers with the necessary tools and knowledge to help a greater number of customers succeed.

Pepper Money’s success is firmly rooted in our robust credit policy. We take the time to understand our customers’ evolving needs and circumstances, o ering diverse products and policy options. We are known for our industryleading turnaround times. Our e ciency is a result of our adoption of innovative technology and automation. We’ve also built strong alliances with our brokers, who trust our brand implicitly.

How do you plan to build on this momentum to drive even greater success?

BS: Pepper Money never stands still, and that’s true in our approach to evolving our o ering to move with the market. Continuous innovation and enhancement of our product o erings and policies are at the heart of our operations.

Across the past 12 months, we’ve introduced new loan products and policy enhancements tailored to the needs of evolving market segments or emerging trends. Just as we do with our residential products, we also provide a near prime option for our commercial and SMSF o erings. This ensures we don’t limit our customers to only the prime category. We most recently introduced policy changes designed to empower brokers to meet the unique needs of their clients, particularly the self-employed.

RedZed achieved a tie for silver in turnaround times, a top-ranked broker priority, and a bronze in communications, training and development. What are the factors driving your high performance in these categories?

Calvin Cordle, managing director: A great user experience and fast turnaround times have always been core to RedZed. In FY24, one of our key focuses was further improving operational e ciencies to deliver even better experiences.

We set about measuring key touchpoints, such as assessment turnaround times and the time it takes our teams to answer calls and emails, to track our progress and identify areas for improvement. This has helped take our service levels to new heights.

We also focus on developing educational resources to help brokers learn, grow and liberate the ambitions of their self-employed customers, such as the Self-Employed Broker Academy. We regularly host PD sessions for brokers through our partnerships with the Melbourne Storm, Hobart Hurricanes and the North Melbourne Football Club.

How do you plan to capitalise on your success and reach new heights?

CC: I want the RedZed team to pause and celebrate. This is great recognition of their hard work over the last year, and my congratulations go to all RedZedders. The enhancements we’re making to our product and service o erings resonate with brokers and Australian self-employed small business owners. The best part is that we’re only just getting started.

Resimac earned gold for its competitive interest rates, setting it apart in the market. What key approaches and strategies drive this standout performance?

Chris Paterson, general manager distribution and marketing: Resimac is proud of this result and to be recognised by brokers for our competitive interest rates. We know that competitive interest rates are a key consideration for brokers, forming an important part of the broader o ering we provide. By deeply understanding these customers, we can often provide options that other lenders may be unable to.

How do you plan to leverage your current success and position Resimac for continued industry leadership?

CP: We are grateful to be recognised by brokers with whom we enjoy working every day. Our team is dedicated to the broker channel, and it’s great to hear we’re on the right track. Brokers know Resimac as a flexible specialist lender. We’re often recognised for our tailored solutions for self-employed and credit-impaired borrowers. We continually leverage insights from sources like Brokers on Non-Banks and our research to guide our focus and improve broker and customer experiences. Some exciting work is underway to continually improve process consistency and decision-making speed while maintaining our flexible and agile approach. We’re also enhancing our digital solutions with more self-service options for brokers and customers to improve their experience.

The team at Bluestone Home Loans is celebrating after taking the top spot in

Brokers on Non-Banks for 2024. Chief commercial officer Tony MacRae says the honour is a result of prioritising products, relationships and service

WHEN A non-bank relies entirely on mortgage brokers as a source of its loans, the strength of that lender’s relationship with the third party channel needs to be rock solid.

This is certainly the case with Bluestone Home Loans. Its tireless and focused efforts to grow its team, enhance its product range and online platform, improve credit policies, speed up turnaround times and support and educate brokers have paid off, with Bluestone being named the overall winner of MPA’s 2024 Brokers on Non-Banks survey.

It’s been a rapid rise in the Brokers on Non-Banks’ rankings for Bluestone, which jumped from sixth position in 2022 to third last year and now the No.1 spot.

Bluestone chief commercial officer Tony MacRae says it’s an honour to top the rankings, and it reflects the work the team has put into making relationships, service and products a priority.

“Our products are designed to help brokers grow their business by providing solutions for the customers that other lenders either don’t cater for or, if they do, they make applications complicated,” says MacRae.

“Over the past 12 months we’ve brought in new leadership and expanded our team, lifting our presence in the market. Supporting our BDM-to-broker relationship is also a team of subject matter experts and comms profes-

sionals delivering educational programs that provide real value to the broker.”

MacRae says collaborative efforts across the entire Bluestone business have helped deliver a number of policy improvements. “This has resulted in us becoming easier to deal with, something that we’ll continue to focus on.”

In the Brokers on Non-Banks survey, brokers are asked to rank non-banks across 10 categories – turnaround times; BDM support; commission structure; communications, training and development; interest rates; product range; credit policy; online platform and services; brand recognition; and product diversification.

Bluestone achieved the number one ranking in five of these categories: turnaround times; BDM support; communications, training and development; credit policy; and online platform and services.

The lender also took second place for commission structure and product range and came in at No. 3 for product diversification. This means that out of the 33 medals (gold, silver and bronze) available, Bluestone won nine – an impressive 27% of all rankings.

MacRae says time is everything for the broker and borrower. “We understand that. We eliminated unnecessary documentation and

simplified processes, making it easier to submit applications,” he says. “We have more than halved turnaround times.”

“We ramped up our broker support, introducing state-based leadership with a focus on building relationships and growing the ‘on the ground’ team by 30%,” says MacRae.

Communications, training and development

Collaborating with the marketing and communications team, Bluestone established a regular cadence that ensured “we had simple, clear and regular messages for our broker network”.

“We also ensure that we have open communication between our BDMs and our entire broker network.”

MacRae says market-leading education is important. “We’ve been working with subject matter experts to deliver webinars and workshops such as SMSF and solution-based lending. BDMs also play a critical role in delivering grassroots support and local training and visits for brokers.”

Bluestone introduced over 40 policy changes that have allowed it to provide solutions for more customers, says MacRae.

Name: Tony MacRae

Title: Chief commercial officer

Company: Bluestone Home Loans

Years in the industry: 25+

How important is it for Bluestone to be so highly ranked by brokers? “It will always be important to us. Given that our goal has been to establish the best relationships and service with our brokers and aggregators, to be ranked highly in so many categories is a real honour and a reflection of the dedicated team we’ve built.”

“We launched a new website that made it easier for brokers to navigate and help their customers with solution-based lending,” says MacRae. “Delivering on providing the best service to brokers and their customers has been the team focus in the last 12 months.”

Bluestone’s alt-doc product was named among the three top non-bank products for the last 12 months. Bluestone was voted the preferred non-bank for alt-doc lending.

As a product o ering, alt-doc enables Bluestone to provide brokers with a solution for borrowers who have varied or nonstandard forms of income, MacRae says. “Banks often can’t or won’t lend to these customers … or just make it tough for them with too many hoops to jump through.

“Our mantra has been to simplify. Our alt-doc o ering has benefited particularly with this focus, seeing simplification in verification for accountants’ letters, the number of documents required for income verification, and turnaround times.”

MacRae says every incremental improvement contributes to a better experience for brokers and borrowers, which of course results in really positive feedback.

Brokers also ranked Bluestone as the preferred non-bank for specialist lending.

“We believe that life or financial circumstances shouldn’t necessarily get in the way of a good borrower’s ability to access credit and achieve their property goals,” says MacRae.

“We consider the individual’s circum-

stances, taking a forward-looking approach to provide responsible and accessible solutions for customers that may have had a financial hiccup.”

MacRae says it’s critical that BDM and credit teams work closely with the broker to thoroughly understand each case. “Without specialist lending these customers would be shut out of the borrowing market. With this in mind, it’s critical that our BDM and credit

ourselves [up] as the preferred broker partner.”

Bluestone has been around for quite some time, but you can’t stand still, MacRae says. “We’ve got some exciting plans for the future, including digitising the application process with a goal to deliver an immediate decision on many occasions.”

By leveraging tech and data, the lender is well on its way to implementing new platforms and interfaces to provide a better expe-

“Brokers are why we exist. This relationship is very important. We’ve spent the last 12 months listening to brokers, optimising the experience with us and enhancing the lender-broker relationship”

teams are focused on working with the broker to find the pathway to yes.”

There’s no doubt that Bluestone is operating in a highly competitive market. MFAA data for the June quarter shows mortgage brokers wrote 73.7% of all new home loans.

For Bluestone, the broker channel is vital – 100% of its loans are broker introduced. “Brokers are why we exist, and so this relationship is very important; it needs to be nurtured,” says MacRae. “We’ve spent the last 12 months listening to brokers, optimising the experience with us and enhancing the lender-broker relationship, increasingly setting

rience and service for brokers and their clients. MacRae says people must not forget that purchasing a home is, in most cases, the largest financial transaction any of us will ever make. “Borrowers need and want support through the often-stressful process. Tech can facilitate the speed and ease of a transaction, but we are still a relationship business, and understanding borrowers’ needs and being able to find suitable solutions for them is equally important – this is where we’ll continue to focus.”

Expanding its product range is a key focus for Bluestone in 2025, says MacRae. This will enable the non-bank to provide solutions for more customers, cementing its relationship with brokers as a preferred partner.

In a competitive market in which many borrowers are struggling due to economic pressures, customer retention is crucial. At MPA’s Major Banks Roundtable, third party leaders discussed how they partner with brokers to support customers, as well as the investments they are making in AI and other technology tools

NOW THAT the cashback battles are truly in the rearview mirror, major banks are not so narrowly focused on winning new customers – it’s keeping existing customers that remains vital in the current market.

While the figures fluctuate, it’s clear the refinancing boom is over. The latest data from PEXA’s Refinance Index for the week ending 15 September shows a 17.5% year-on-year drop in mortgage refinancing volumes.

This doesn’t mean mortgage holders aren’t refinancing, just that activity has slowed. ABS lending indicators for July 2024 show the value of external refinancing for total housing (both owner-occupier and investor) rose 4.3% to $16.6 billion but was down 21.4% year-on-year. External refinances are new loans obtained to replace existing loans provided by di erent lenders.

The KPMG major Australian banks half-year 2024 report shows that net interest margins continue to decline, and it’s always more cost-e ective to retain borrowers on the books than to acquire new ones.

Mortgage brokers are a vital piece of the puzzle in any major bank retention strategy. The trust and confidence Australians place in brokers is at an alltime high: brokers wrote 73.7% of all new home loans in the June 2024 quarter, according to the MFAA.

With this in mind, the major banks are working hard to foster strong relationships with brokers and their clients. This includes providing support for customers undergoing financial di culties and assisting brokers when it comes to retention conversations.

But it’s also about upgrading technology, including the use of AI, to streamline and speed up loan processes and decisions, and giving customers a better life-of-loan experience.

To discuss these and other issues, MPA hosted the 2024 Major Banks Roundtable at Café Sydney. Representing the major banks were Adam Brown, executive, broker distribution, NAB; Wendy Brown, head of broker distribution, Macquarie Bank; Razia Khan, general manager third party banking, CommBank; and Sarah Willsallen, state general manager NSW/ACT – mortgage broker distribution, Westpac Group.

Broker participants included Fabio De Castro, director, Simplify Finance, and Melanie Cunliffe, managing director Indigo Finance.

Natalie Smith, general manager third party at ANZ, was unable to attend in person but provided written responses.

The home loan market remains highly competitive. Major banks face declining net interest margins, competition from non-bank lenders, and borrowers who are struggling with higher interest rates and inflation. How are you meeting these challenges and working closely with brokers who now have a market share of 73.7%?

Innovation and exceptional service, superior technology, listening to broker feedback and partnering closely with brokers to support their clients for the life of the loan – these are some of the main factors driving major banks in a competitive sector.

The major banks have adjusted to customers’ changing economic circumstances during a cost of living crisis that’s been hitting people hard.

After 13 increases to the official cash rate since May 2022, some clients’ mortgage buffers were running low or had depleted altogether. This meant both the banks and brokers had a greater focus on clients’ finances and spending habits and on helping them determine the right time to borrow rather than ‘how much can I borrow?’.

Willsallen said it was great to see so many lenders wanting to support customers into homeownership.

“That competition drives innovation, and it drives service excellence, which is good for all of us,” she said. “We do need to ensure

that we manage mortgage returns to build a sustainable business, and we’ll continue to focus on the right balance of risk, margin and volume.”

Willsallen said Westpac was pleased that the investments it had made over last three years to improve broker technology, systems and tools had driven such strong improvements in time to decision and in its Net Promoter Score from brokers in the last 12 months.

Westpac has been listening to broker feedback about what it should focus on to make further improvements. “We’re committed to doing all we can to make it easier, simpler and faster for our brokers and customers,” Willsallen said.

Khan emphasised CommBank’s strong partnership with brokers. “CommBank has been supporting brokers for over 30 years now to help grow their businesses,” he said. “We understand that brokers play a crucial part in a stable economy.”

The bank has invested heavily in broker technology, such as its CommBank broker portal (Your Loans, Your Applications). It focuses on listening to brokers to understand “what they want and need”.

“We want to ensure their experiences with CommBank remain seamless,” Khan said. Looking at how to diversify support for brokers was also important; using data insights and analytics to help brokers understand and grow their businesses.

“We’re also doing a lot of work around diversity and inclusion, such as for women in business, and providing additional support from our sales team.”

Smith said that in a highly competitive home loan market, ANZ was committed to standing out through innovation and exceptional service.

“As broker market share reaches close to 74%, we are dedicated to enhancing our support for this important channel,” she said.

“Our focus remains on delivering differentiated propositions across all channels during these changing economic times. With significant developments like our recent Suncorp Bank acquisition and the expansion of ANZ Plus, we are positioning ourselves to better serve both brokers and their customers.”

Adam Brown said brokers were working in a very different economic environment than they were 12 months ago and 12 months prior to that. Despite the challenging economic conditions, about two thirds of NAB customers were ahead on their home loan payments by an average of three and a half years.

“You hear a lot about people paying ahead and building up buffers, but it actually masks those customers that are a bit more challenged,” Brown said.

Four in 10 Australians had experienced some sort of hardship. In NAB’s past conversations with brokers, customers had been

focused on the maximum amount they could borrow, but this had now switched to ‘how much can I really afford?’, Brown said.

“So the conversation that you then have with brokers is really how do you support these customers through getting a home loan? And when’s the right time to get a home loan? Once they’ve actually got the home loan, how do you best support that customer for the life of the loan?”

Brown said brokers were doing a good job of providing customer support beyond the transaction. NAB is also focused on helping customers for the life of the loan, acknowledging the difficult economy and cost of living challenges.

Wendy Brown from Macquarie Bank said it was clear that the right conversations were taking place between brokers and their customers, particularly around understanding their financial situations. “We’ve noticed that in the quality of that book. Great conversations have happened – what they [customers] need versus what they want and what they can afford.”

More than 90% of Macquarie Bank’s loan flow comes from brokers, Brown said. In terms of technology, the bank focuses on providing platforms and functionality that will help brokers do business whenever and wherever it works for them.

Macquarie Bank works with brokers to

security app, to brokers and their support staff so they can feel confident that they are assisting their customers in the most secure way possible.

“For us it’s about scale and technology but for the best outcomes for the customer and broker,” said Brown. “The more control we

“We are seeing more instances of application fraud. It’s an industry challenge. Automation and checking is critical in identifying that and seeing some of the patterns across our portfolio” Adam Brown, NAB

provide them and their support staff with seamless access to the information they need to help them be more efficient. It has rolled out Macquarie Authenticator, a market-leading multi-factor authentication

can put in a broker and customer’s hands the better.” The information supplied in the broker portal, or that customers could see across mobile and internet banking, “helped to give confidence throughout the home loan process”.

“They can clearly see revert rates – both the broker and the customer. That element of control is really important, especially when you’re coming into a higher interest rate and inflation environment.”

Adam Brown added that the advisory role banks play with brokers and customers was very important. Over time, NAB has built up its premium access proposition, providing a team member who will work with a broker on a loan scenario before it goes to credit assessment and lodgement.

“We know brokers hate that long ‘maybe’ answer versus a really quick no or a quick yes,” he said. “Having that certainty up front, and not wasting time when there’s increased costs and increased regulation, has been really important.”

Wendy Brown agreed that it was important for lenders to provide clear credit guidance for brokers and their customers to ensure a better and more efficient experience in the application stage.

On the topic of spending and financial capacity, De Castro said roundtable participants would be surprised to know how many owner-occupiers did not have a budget or know much they could afford to borrow.

“When you ask that question, you’d be surprised how people just implode,” he said. Some clients’ redraw [facilities] were running low, and some had run out of savings. “I think the real effects of the rate rise we’re starting to see now [are] eating into buffers.”

A recent NAB consumer sentiment survey showed that almost 60% of people had cut back on eating out; 50% had reduced their ‘micro-treats’, such as buying coffee and snacks; and around 50% had scaled back on entertainment, such as streaming services.

“Twenty per cent of people have cut back on what they’re spending on their pets, such as insurance … all this money is going into loan buffers,” said Adam Brown.

Melanie Cunliffe said customers were now very cautious about their spending and the amount they could borrow for a home loan.

“It’s almost like they think the credit environment is going to be so tough that they’re not going to be able to borrow,” she said. “It’s about coaching them through to the other side and reassuring them ‘we’ll be alright, let’s see what we can borrow, let’s work through it together’.

“I think people are very nervous because of interest rates that they’re going to lose that possibility of homeownership.”

What AI-driven tools or data platforms are you using, or planning to introduce, that improve the broker and customer experience? How will AI change the banking industry?

Artificial intelligence is a hot topic at present. News stories and advertising provide constant updates on the latest AI-supported products and platforms that are set to make everyone’s lives easier.

AI is also making huge inroads into the worlds of banking and mortgage broking.

A September 2023 KPMG Global Tech Report found that 60.8% of banking tech-

Mortgage brokers wrote of all new homes in the June 2024 quarter – the second-highest broker market share on record

73.7%

6.5ppt

Brokers’ market share rose in the June quarter from 67.2% one year prior

Value of home loans settled by mortgage brokers exceeded for the first time in the June quarter – jumping $18.64bn from the previous quarter to $100.11bn

$100bn

$11.49bn

Value of home loans settled by mortgage brokers rose by in the June quarter (or 12.96%) year-on-year

“Whether a broker seeks pricing [on a loan] through the Macquarie Bank portal or the customer requested it, the price remains the same for 90 days, providing equality for all”

Wendy Brown, Macquarie Bank

nology leaders believed generative AI, AI and machine learning would be critical to achieving short-term ambitions.

Wendy Brown said it was often underestimated just how long AI had been in use. Macquarie had been investing in AI for several years in a number of different ways, alongside a range of other data science technologies, including machine learning.

“We’ve been using it for some time across different use cases; historically, for example, we would use it on the risk of a street or a postcode, or property or valuation.”

Brown said a key benefit of AI was that it freed up time to enable the bank’s teams to focus on higher-value engagements. Instead of manually reviewing documents, they could focus on engaging with and providing insights to brokers.

Macquarie Bank uses AI in the loan and documentation review processes, which helps to deliver even faster turnaround times for customers and more efficient experiences for brokers engaging with the bank. It also uses AI to detect instances of fraud and scams.

Macquarie Bank takes a copilot approach with AI, “with a human overlay, and we have found that to be very successful”, said Brown.

“We work in a highly regulated environment, so it’s vital that there is the right level of oversight and governance on AI and other data science processes.”

Willsallen said she has a favourite quote when it came to AI: “I don’t want AI to paint the next Picasso for me – I want it to clean my kitchen so I have time to learn how to paint.”

She agreed with Wendy Brown that AI had been part of banking infrastructure for a long time. “We want to see where it adds value to make things faster and simpler,” Willsallen said. This includes use in document identification and verification and ensuring these are aligned with policy.

“Where it can make it faster for humans

because they then don’t need to check something, that’s gold,” said Willsallen. “It makes it faster and easier for our team members, for our brokers, but also means we get outcomes for customers faster.”

Adam Brown said AI is critical to driving efficiency internally at NAB but also to speeding up lending outcomes for brokers and customers. AI also detects trends in large data sets, which is valuable for combating fraud and scams and boosting security.

“We are seeing more instances of application fraud,” Brown said. “It’s an industry challenge. Some of the automation and checking is critical in identifying that and seeing some of the patterns across our portfolio.”

At CommBank, Khan said AI and other technology is being used for fraud detection but also to help customers predict their bills

and know their cash flow, often through the CommBank app.

The bank has also introduced Benefits Finder, which has put $1.2 billion in government benefits and grants back into the pockets of customers.

CommBank also generates data insights that are particularly aimed at growing broker businesses. “It can highlight di erent triggers that your customer may be about to refinance. Have a conversation with them if you haven’t already,” said Khan.

Smith said ANZ’s commitment to leveraging technology is transforming how the bank serves its customers and supports brokers.

“Our recent partnership with Microsoft to establish an AI Immersion Centre signifies a major step forward in accelerating AI adoption across the bank.

“We’re empowering our leaders to drive innovation and enhance services. AI is integral to improving customer experiences, protecting clients and streamlining processes, all while adhering to our core principles of risk, privacy and ethics.”

Smith said that while technology evolved, it would never replace the essential human touch in banking. “Instead, AI will complement and enhance the personal relationships that brokers and lenders provide, creating opportunities for a more seamless and insightful customer experience.”

Broker question from Melanie Cunliffe: What are your plans around investing in and using AI in enhancing the ‘broker channel’ model in comparison to ‘direct to consumer’, and how are they different?

Willsallen said Westpac doesn’t see a difference in the way it approaches AI and technology for brokers and their clients. “We want to make it faster for every customer, regardless of whether it’s through a broker or directly,” she said. “Our lending origination capability that manages this for us manages it agnostically across our channels.”

But there are some specific differences, Willsallen said. For example, when broker applications come through ApplyOnline it involves an assessor rather than a lender. “If the technology makes an assessor’s job faster, it’s also going to make a lender’s job faster and vice versa.”

Westpac focuses on how to make processes work faster for customers, providing quick, correct and valid answers.

Khan said introducing AI policies and processes is occurring faster with brokers than consumers. “Because we’re dealing directly with brokers, we can be faster with the right compliance overlay … with direct to consumer, there’s a few more checks and balances that we need to be confident of.”

The digitisation quality in CommBank’s loan application processes remains the same for both broker and direct-to-consumer channels. “Our goal is to try and digitise a big

part of the back end so brokers and lenders get a faster time to yes,” Khan said.

Adam Brown said NAB continues to work on its new origination platform. “We’ve got one in three of our unconditional approvals going through the new platform. We started with the broker channel because we’ve got 60 to 65% of our [loan] flow coming through the channel,” he said.

Brown said that when it comes to digitisation and AI automation, it makes sense to start where the volume of business is the greatest – the broker channel.

“In the face of increasingly sophisticated

scams, it’s imperative that brokers and banks alike invest in robust processes and cuttingedge technology to enhance our prevention and detection capabilities.”

NAB’s proprietary channel and commercial broker business will also be included in the one origination platform, providing a similar experience for customers no matter the channel. “It’s build once and apply to all, as opposed to the past, where many of us looked at channel-by-channel decisions,” Brown said. “That’s not efficient; it’s costly, and it’s hard to maintain.”

Wendy Brown said that at Macquarie Bank

the approach used to be to trial technology tools in the direct-to-consumer channel first and then “iron out any kinks” before rolling the functionality out to brokers. But the bank has evolved that process to pilot new technology with a group of brokers first before launching more broadly, and this has worked successfully.

“Broker feedback is so important to us, and we know that our perception of what they want and need, and what takes time in a broker business, may be different to their perspective, so this process is important to get a deeper understanding.”

Transparency is key, Brown said, and Macquarie has a consistent approach, reinforcing the broker’s brand in market.

De Castro said everyone seemed to agree that AI was not being used to replace people’s jobs but to boost efficiency.

“I love AI because if it makes you [banks] more efficient, it makes me more efficient, and that leads to retention.” He said it also

“CommBank has been supporting brokers for over 30 years now to help grow their businesses. We understand that brokers play a crucial part in a stable economy” Razia Khan, CommBank

meant that banks could allocate resources to make sure that RMs and BDMs were meeting brokers, uncovering their needs and helping them grow their businesses.

De Castro said he loved the fact that broker market share had almost reached 74%, but he believed some brokers had the attitude that this meant ‘banks need brokers’.

“We need each other,” he said. “We need to remember we’re all on the same path. We’ve got to evolve together as an industry.”

He hoped the “old-school mentality of brokers that played golf and lived on trail” was gone. “It’s a bad image for people like me who are trying to build actual businesses,”

De Castro said. He said he hated rewriting loans because doing that meant his books size wasn’t growing.

“It’s about that partnership [with banks]. What can we do to empower customers to stay where they are?”

Broker question from Fabio De Castro: What tools and processes are being implemented to empower brokers in retaining our mutual customers?

Leading into to his question for the major banks, De Castro said they all did an amazing job, but retention was challenging.

He gave the example of going to a client’s bank, trying to get a better loan deal, and being given an offer that did not meet the customer’s expectations.

He would do all the work to find a better rate at another lender and gain approval for that loan, only for the original bank to say at the last minute that it would match the rate.