TOP 100 BROKERS REVEALED

How the year’s best are raising the bar AMA’S BIG WINNERS 2024 awardees in the spotlight NON-BANKS FORGE AHEAD Serving the underserved

TOP 100 BROKERS REVEALED

How the year’s best are raising the bar AMA’S BIG WINNERS 2024 awardees in the spotlight NON-BANKS FORGE AHEAD Serving the underserved

How

CONNECT WITH US

Got a story or suggestion, or just want to find out some more information?

twitter.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

02 Editorial

It’s a vital new tool, but AI can’t replace human connections

04 Statistics

How brokers can boost their value proposition through diversification 12

Australia’s regional suburbs where property prices are surging

06 Opinion

Brokers need more than one string to their bow, says ANZ’s Ivan Mioc

14 Creating a personal brand

Tools and strategies to help brokers stand out in a crowded market

Find out who topped the list of the best Australian brokers in 2024, raising the bar on loan volume and client service

Flint has set up an elite team of private brokers servicing high-net-worth clients. Huetos and two of his colleagues share insights about their careers and explain the benefits of Flint’s Private Broker model

20 A model for growth

Two brokers rise to the top with the game-changing support of Aussie’s Platform Plus

24

Leading non-banks discuss how they’re strengthening their niche in the lending market

78 Brokerage insight

Loan Market Geraldton takes a holistic approach to serving the community

80 Other life

A love of cricket has taught broker Roshan Bhattarai lessons in teamwork

58

FEATURES UNVEILING THE WINNERS

Highlights from the 2024 Australian Mortgage Awards’ celebration of excellence in the industry

Our daily newsletter. Keep on top of property market trends, business strategy, and what industry leaders have to say.

If you were trying to determine what topic dominated the mortgage broking landscape this year, it would be hard to go past artificial intelligence.

While AI has been around for some time, in 2024 it was a subject that brokers, and the general public as a whole, couldn’t avoid. AI systems are now front and centre in the mainstream media, advertising and social media, relentlessly promoted as a must-have technology that will make our lives better and easier.

In the mortgage and finance industry, there’s no doubt that the use of AI is rising exponentially, with brokers using it to streamline time-consuming administrative and processing tasks, assist with customer communications and the production of marketing material, and for other tech applications.

Used in the right way, AI can boost the efficiency and productivity of brokerages, helping them act faster, provide better data and gain a competitive advantage over other businesses that don’t use the machine learning technology. But it’s important to remember that AI has its limitations – it makes mistakes and can’t replicate the warmth and familiarity of simple human connections.

The MFAA recently released a discussion paper on the safe and ethical use of AI in the mortgage broking industry. Created as a result of extensive discussion with MFAA

members, the paper explores how mortgage and finance brokers are considering the use of AI and provides practical guidance for those looking to integrate AI into their businesses, including a checklist.

AI is a fantastic tool that brokers can’t afford to be without – but it is just that, a tool to assist business growth. It’s not a substitute for the creativity, understanding, empathy and unique personalities of human beings.

As someone once said, “I don’t want AI to paint the next Picasso for me – I want it to clean my kitchen so I have time to learn how to paint.”

In the December edition of MPA, we look at the best ways for brokers to market themselves and their businesses, and explore the opportunities provided by business diversification. The rise in popularity of non-bank lenders, and how they are partnering with brokers, is also in the spotlight in this issue’s Non-Banks Roundtable.

And to close the year on a high note, MPA reveals the winners of the hugely popular 2024 Australian Mortgage Awards and announces Australia’s Top 100 brokers.

Wishing all our readers and stakeholders a Merry Christmas and a Happy New Year.

Antony Field, editor, MPA

ADVERTISING ENQUIRIES claire.tan@keymedia.com

MortgageProfessionalAustralia is part of an international family of B2B publications and websites for the mortgage industry

AUSTRALIAN BROKER simon.kerslake@keymedia.com

T +61 2 8437 4786

NZ ADVISER alex.knowles@keymedia.com

T +64 9 200 1319

CANADIAN MORTGAGE PROFESSIONAL chris.anderson@keymedia.com

T +1 720-441-2255

MORTGAGE PROFESSIONAL AMERICA chris.anderson@keymedia.com

T +1 720-441-2255

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com

T +44 203 868 3406

Combined value of Australian residential real estate 1%

Increase in national home values in Sept 2024 quarter – the softest rise since Mar 2023 quarter

522,317

Property sales recorded in 12 months to Sept 2024

Average days properties spent on market in Sept quarter

Source: CoreLogic, September 2024

Soaring capital city prices are pushing buyers to regional areas, where home prices are booming. In NSW, Lochinvar saw a 67% rise, while in Queensland, Townsville’s Hyde Park grew 59% as the state’s regional areas continue to draw thousands of interstate arrivals seeking affordability and a lifestyle change.

Australia’s million-dollar markets hit a record high in August, with 29.3% of suburbs now having median values above $1 million, up from 21.7% in January 2023, CoreLogic reports. Sydney and Brisbane led growth, each adding 46 million-dollar markets.

NET CHANGE

VALUE OF NEW BORROWER-ACCEPTED LOAN COMMITMENTS (SEASONALLY ADJUSTED)

Interstate property enquiries have surged in 2024, with 22% of buyers seeking homes outside their home states, up from 17% last year, PropTrack reports.

The NT, Tasmania and the ACT are attracting the most interstate interest, driven by affordability, investment potential and job opportunities.

SHARE OF ENQUIRIES COMING FROM PROPERTY SEEKERS BASED IN A DIFFERENT STATE, 12 MONTHS TO AUGUST 2024

Brokers who can o er both commercial and residential lending solutions can broaden their client base and boost retention, says ANZ’s Ivan Mioc

WE think about diversification, we often think about an investment strategy, but the truth is diversification can be used as a strategy for running our businesses.

For brokers, diversification into commercial lending is a great way to broaden your client base. We know the needs and requirements of our clients change all the time, and when it comes time to move beyond a home loan, fulfilling the holistic needs of your clients gives you another way to add value, retain relationships, build trust and grow your book.

If you’re a broker who’s thinking about taking the plunge into commercial lending, bear in mind that it is covered by simpler regulations than home lending, and borrowing requirements are generally bespoke in nature to suit the business, its cash flow requirements and capital position.

Brokers who can move seamlessly between the complexities of commercial and residential lending are uniquely positioned to understand the entirety of their clients’ needs, which is key to being able to provide the best service and, ultimately, the right financial solution.

We know customers value the service brokers provide, which is why the greatest asset brokers have is their existing customer base. I encourage mortgage brokers to analyse their books, look at where they’re growing and consider building on those strengths. Firstly, if the customer has an ABN, they are likely to have some form of business lending requirement. Be curious about what the customer is telling you as there may be an underlying business that you can support. For example, when you look at your customer

base, do you have a natural a nity with a specific industry or profession? Is this something you can build on and leverage to further grow your business?

Some industries are more specialised than others, such as health, franchising and agribusiness. ANZ recognises this, and we have specialist bankers that have industry expertise and are available to partner with brokers and assist their customers.

whose goal is to provide holistic financial solutions to their customers, regardless of whether they meet their business or personal needs. It’s important that we help support brokers and their customers – and o ering a ‘full service’ is an excellent client retention tool.

Investing in your professional development to build your commercial knowledge and skill set is crucial. Partnering with an ANZ Broker Account Manager and working with our bankers to learn more about commercial lending will help build your confidence and knowledge.

However, a broker’s professional development shouldn’t be limited to policy, product and process updates from aggregators or lenders. Brokers should also explore opportunities to learn about growing their own businesses. To support brokers with this, ANZ recently held a business growth seminar for brokers.

The seminar leveraged ANZ’s long-standing relationship with the University of South

Customers are increasingly savvy, and the competition for their business is fierce, so it’s important that brokers have a number of strings to their bow

On the other end of the spectrum, there are thousands of small businesses out there who require a more generalist approach.

Customers are increasingly savvy, and the competition for their business is fierce, so it’s important that brokers have a number of strings to their bow.

We know that diversifying can be a challenging transition, which is why education is so important, as is the support o ered by ANZ’s Broker Account Managers and bankers.

ANZ’s data shows that approximately 35% of retail applications it receives are for selfemployed customers. This represents genuine opportunities for brokers. If a broker isn’t talking to their customers about their commercial lending needs, another broker will.

We want to support accredited brokers

Australia’s Australian Centre for Business Growth to deliver modules about strategy, sales, marketing and scaling for growth, all of which are all critical considerations for business owners looking to sustain and grow their businesses over the long term.

Diversification is a strategy that will help brokers grow professionally, create more opportunities and manage risk. By diversifying, you will find yourself integral to the end-to-end customer experience, which ultimately adds value to your customer base.

Ivan Mioc is ANZ’s general manager commercial broker and origination. He has been at ANZ for 20 years and is a strong advocate for the broker industry. Mioc has held several leadership roles across the bank, focusing on commercial and small business lending.

Flint is leading the way in servicing high-net-worth clients, setting up Flint Private. The expert team includes former private bankers Salvador Huetos and Matthew Mohl, supported by head of settlements Sabrina Jhugroo

THE MOST successful people in life and business aren’t happy with the status quo. They want to get out of their comfort zone, challenge themselves and strive for new goals.

This is especially true for Salvador Huetos, Matthew Mohl and Sabrina Jhugroo, who have made the leap from working at major banks to joining financial services brokerage Flint.

Former senior private bankers Huetos (St.George) and Mohl (CommBank), and Jhugroo, a former NAB credit assessor and head of settlements at a large brokerage, are now using their impressive skills and banking knowledge as members of Flint’s Private Broker team focusing on high-net-worth clients.

Private broking is a niche sector of the mortgage and finance industry, with a limited number of brokers who have the experience to offer high-income clients flexible and individualised solutions to their financial needs.

MPA asked the Flint Private Broker team about their career transitions, the benefits of the Flint ownership model, and the extensive support structure in place to assist both brokers and their clients.

Huetos says leaving the familiarity of a traditional banking environment was a professional and personal challenge. “The most significant part of this was stepping out of the comfort of a stable salary and entering an environment where income can be mostly inconsistent,

particularly in the building phase,” Huetos says. “But creating something from the ground up was key, not only for myself but for my family.

“Rebuilding my network, client base and competing in a market with a vast number of brokers was a steep learning curve, but ultimately it taught me resilience and the importance of strong client relationships.”

Huetos says what drove his decision was the

but also most rewarding leaps”, Mohl says. Unlike in banking, where excellent performance can only get you so far, and incomes are capped, Mohl says “going stronger and harder for our clients” as a Flint Private Broker reaps rewards. “Every minute that you put in is what you get back out in this industry. Every opportunity that comes your way is another chance to further your network and increase

“At Flint, private brokers don’t just earn an income – they own their trail book, clients and partners and, by extension, their future” Salvador Huetos, Flint

desire for greater autonomy and control over his future. “Flint’s robust support system was instrumental during this transition, allowing me to focus on the relationships and values that matter most.”

Mohl says moving from banking to broking was a scary but logical leap. The bank provided a certain level of comfort, resources and fast turnaround times, but there were also the limitations of offering one product.

Making the transition from a stable PAYG role to the unpredictability of self-employment as a broker was “one of the biggest challenges

your income. That sense of ownership – the idea that my success was now directly in my hands – became motivation.”

Flint Private Brokers have access to a wide range of lenders and loan options, unlocking better outcomes for clients. Huetos says this gives them the flexibility to offer tailored solutions that fit each client’s unique circumstances.

“Now that we have access to the best policies, [and] our clients have more options, that increases their chances of approval, and it ensures we get the best deal possible to suit their needs and objectives. Flexibility and

Broker model: Flint Private

Broker team:

Salvador Huetos (pictured) – 16+ years’ experience; formerly at Westpac Group’s St.George Private Division

Matthew Mohl – 17+ years’ experience; formerly at CBA Private

Sabrina Jhugroo – 12+ years’ experience; formerly at NAB as a credit assessor, then ran settlements at one of Australia’s largest brokerages

Strategy/credit team: Five chartered accountants (CPAs)

Client base: High-net-worth clients, including medical professionals, tech professionals, legal and accounting professionals, self-employed clients and business founders, and family offices TEAM PROFILE

choice are game changers for both clients and brokers,” Huetos says.

The aim is to build trust and help private clients, whether business owners, investors or individuals, achieve their financial goals.

Mohl says having access to multiple lenders on Flint’s panel has been incredible. He has been able to assist customers who had run out of options with their banks and provide outof-the-box solutions.

While broking is a highly competitive market, Flint Private aims to carve out its own space by focusing solely on high-net-worth clients whose incomes are at least $600,000, for minimum total lending of $5 million.

Huetos says it’s all about providing a tailored, client-centric and strategy-led approach to mortgage advice that goes beyond a mortgage, looks at a client’s full financial picture and delivers solutions aligned with their goals.

Brokers can build, control and own their trail books, staying in charge of their own futures

The focus is on high-net-worth clients – providing a tailored, holistic approach to addressing complex nancial needs

Brokers are supported with a strategy team of CPAs, plus skilled back-o ce sta and a network of nancial planners, buyers’ agents, accountants and wholesale investment managers

High-touch support allows brokers to spend more time building trust and long-term relationships with clients

“We are attuned to the needs of private bank clients. We replicate the private banking experience in the broking space with a CPA-led strategy team” Matthew Mohl, Flint

“Our emphasis is on high-quality customer experiences for our target market. We believe we have the best-in-market capabilities for assisting the complex needs of high-net-worth clients. It’s about being a trusted partner, not just quick wins.”

Flint Private has built a team of highly experienced professionals. Its strategy team is made up of certified accountants (CPAs) who have a deep understanding of tax strategies, cash flows and complex financial structures.

The brokerage also employs skilled admin sta and uses a network of financial planners, buyers’ agents, accountants and wholesale investment managers to ensure a holistic approach to servicing HNW customers.

Jhugroo leads Flint’s settlements team, which proactively manages settlements, ensuring transparency and seamless communication. “This builds trust with clients and refer-

rers, strengthening relationships and encouraging repeat business,” she says.

“Our back-o ce team manages communications with lenders, lawyers and stakeholders, freeing brokers from administrative tasks. This allows brokers to focus on nurturing client relationships and expanding their business.”

Jhugroo ensures that all transactions are executed flawlessly, resolving potential issues before they arise and ensuring stress-free settlement experiences. She says Flint Private’s settlement expertise gives its brokers a point of di erence by o ering a seamless, high-quality experience tailored to discerning clients. “This fosters trust and strengthens client and referrer relationships.”

Huetos says Flint’s private brokers “don’t just earn an income – they own their trail book, clients and partners and, by extension, their future”, creating long-term assets that provide

security for their families. “This approach ensures brokers stay invested in the success of their business while having the flexibility to build their brand. Flint provides the support, but ultimately the success and growth belong to the brokers,” Huetos says. “By managing loan processing, client onboarding and other administrative tasks, Flint allows brokers to concentrate on growing their business.”

Mohl says he and Huetos bring more than 30 years of experience as private bankers at major banks. “We are attuned to the complex and high-touch needs of a private bank client. We replicate the private banking experience in the broking space with a CPA-led strategy team.”

Flint Private Brokers specialise in complex structuring and lending, ranging from residential to commercial and development finance. HNW clients benefit from tailored policies and solutions that are usually not available to the retail channels. These can range from higher LVRs to HNW loan policies that align with clients’ exit strategies. Niches also allow asset lending, professional investor IO servicing, as well as the use of alternative sources of investment income due to complex income structures, flexibility around cash flow, or asset- and liquidity-based lending.

Huetos says the private broker model is similar to most private banks, with an extensive team of credit specialists to assist in structuring deals. “The di erence is that we have deep contacts with all the lenders, especially all of the private banks and internal senior credit teams.

“We o er a high-level, personalised service that high-net-worth clients expect. We can confidently o er comprehensive financial strategies, allowing us to build trust and longlasting relationships.”

This service model considers the busy lives of clients. It includes a concierge-style service featuring after-hours meetings, virtual consultations and a dedicated senior onshore team to manage the entire process from start to finish.

Mohl says a high-touch experience is essential to the successful retention of private bank clients. Flint’s directors/bankers are available seven days a week, while also working closely with the clients’ private bankers.

or visit orde.com.au/team Loans up to $2.5 million Up to 80% LVR

Stretching beyond home loans into other areas of finance and even complementary services can help mortgage brokers future-proof their businesses by strengthening client relationships and attracting new customers

THE ABILITY to diversify is an important skill that every broker should have if they want to remain competitive, retain customers and ultimately grow their business.

As the market for home loan customers becomes more crowded, some brokers are looking to offer other types of lending and services to avoid relying solely on residential mortgages for their income.

A growing number of brokers are diversifying into commercial lending. The MFAA Industry Intelligence Service 17th Edition report revealed that the total book value of commercial lending handled by mortgage brokers continues to grow. Between 1 April 2023 and 30 September 2023, it reached a record high of $78.12 billion. It also increased 6.85% to $5.01 billion period-on-period.

But diversification is not just about commercial property lending; it also covers SME finance, such as for asset and equipment purchases, lines of credit and cash flow funding; SMSF lending, personal loans and more. Some brokerages diversify by offering non-lending services.

Roberto Sanz, general manager sales and partnerships at small business lender Prospa, and Amol Khuntale, an award-winning broker and director of ASK Financials, gave MPA their insights on different ways to diversify and how it can benefit broker businesses.

Adding value to broker offering Sanz says Prospa sees diversification as a means of increasing the value proposition

brokers offer clients when they address a range of funding needs.

“Right now, small business lending presents a huge opportunity because of the unique support that SMEs require,” Sanz says. “Small businesses are often time-poor, and cash flow remains as the top funding need. Brokers who can solve for these needs will strengthen their proposition in the SME market.”

By understanding the unique pressures and opportunities of SMEs, brokers can offer tailored solutions that meet a wide range of needs, from cash flow and growth capital to strategic financial advice, says Sanz.

“It’s about becoming that go-to partner clients can rely on as their needs change. Take, for example, a broker in Sydney who worked

with a client for over 10 years, helping them grow their business from $200,000 to $6 million annually. You can imagine how their needs evolved over time, and how valuable that relationship became for both the client and the broker.”

A YouGov study from October 2024 shows that 30% of SMEs are planning to seek external funding over the next 12 months. Sanz says now is the time for brokers to work with their SME clients on what’s next in 2025.

Khuntale, who was named the 2024 FBAA New Finance Broker of the Year, says he sees diversification as a way of creating value across interconnected fields to support clients holistically. His Melbourne brokerage, ASK Financials, has expanded into business

and commercial loans to meet its clients’ broader financial needs.

“Transitioning into business finance involved focused upskilling, including specialised training in loan structures, cash flow analysis and attending commercial training sessions conducted by our aggregator,” says Khuntale.

“While challenging at first, this shift has been rewarding, allowing us to provide comprehensive solutions and strengthen client relationships.”

ASK Financials also offers SMSF lending, providing clients with tailored solutions for their self-managed super funds.

“Looking ahead, asset finance is our next area of focus,” Khuntale says. “Expanding into asset finance will allow us to further meet our clients’ diverse financial needs, strengthening our role as their all-in-one financial partner.”

For Khuntale, diversification extends beyond lending. He has recently set up three separate businesses to complement ASK Finance: investor platform Investar.io to provide a wealth of data to investor clients; Skill Pal, which provides back-office support to brokers; and Digistratics, a marketing service for brokers.

“Together, they form a comprehensive ecosystem, enabling us to empower brokers, buyers and investors on every step of their journey. It’s strengthened client trust, increased referrals and positioned us as a comprehensive resource in the industry.”

Diversifying is about future-proofing your business, says Sanz. “With open banking and AI simplifying home loan comparisons and processing, the role of residential brokers will evolve. Moving forward, value-driven relationships will outperform purely transactional ones, so it’s in mortgage brokers’ interests to offer more than just one solution.”

Sanz says by expanding into areas such as SME and commercial finance, brokers can build stickier relationships that support clients across every stage of their journey, creating lifetime value.

“Diversifying revenue streams also adds stability, helping brokers weather housing market fluctuations. At Prospa, we’ve seen an 11% increase in mortgage brokers referring business over the past year, which shows how trusted relationships can unlock real opportunities.”

To successfully diversify their businesses, brokers can’t do it alone – they need training and support. Sanz says Prospa provides a full suite of tools and resources to help brokers confidently branch out into new business lending areas. This includes ongoing access to free educational resources, such as webi-

Khuntale says new brokers wanting to diversify can start by understanding their clients’ needs and identifying complementary services that add real value.

“Invest in quality training and upskilling to build expertise in each area. Diversification should enhance your clients’ journey – so grow thoughtfully, focusing on services that strengthen relationships and set you apart in a competitive market.”

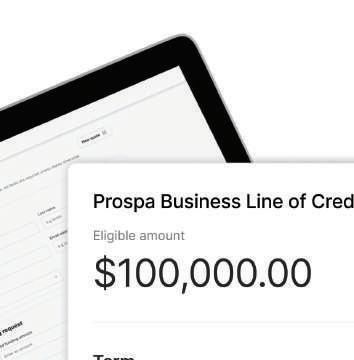

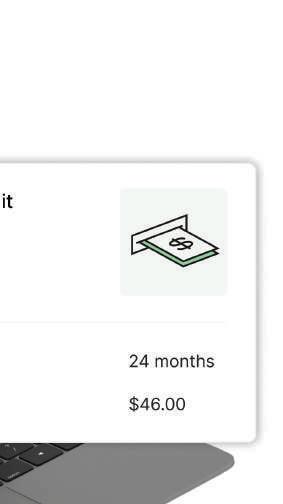

Sanz says the new Prospa IQ tool is designed to give broker partners confidence in its accuracy and outcomes. It enables partners to generate on-the-spot quotes, backed by

“Moving forward, value-driven relationships will outperform purely transactional ones, so it’s in brokers’ interests to offer more than just one solution” Roberto Sanz, Prospa

nars and marketing materials, which brokers can use to manage client conversations and grow their businesses.

New technology is making it even easier for brokers to diversify, says Sanz. “Prospa Intelligent Quoting, our newest quoting innovation, allows more brokers to confidently assess their clients’ creditworthiness in real time, improving their customer experience.”

Prospa BDMs are there to help brokers every step of the way. Sanz says a broker recently expanded into SME lending, relying on Prospa’s support to help a self-employed client open a new cafe in Perth after they had been turned away by a major bank.

“With Prospa, the broker secured $500k in funding. The client was thrilled with the fast turnaround and level of service and soon returned to the same broker for help with refinancing their residential loans.

“Prospa’s BDM supported the broker throughout the entire process.”

Prospa’s credit decision engine. “The tool automatically analyses bank statements, credit profile and serviceability in real time with no credit checks,” Sanz says. “It determines the client’s borrowing capacity, price and term.

“On top of that, partners can now choose the service approach that best fits their business model,” he adds. “They can manage their own clients’ applications end to end through our Partner Led service, or they can spot and refer the opportunity for us to run the application.”

Prospa has also sharpened its rates for good-quality businesses, ensuring brokers can access competitive rates for their clients.

“We’ve also enhanced our loan products, including five-year terms on business loans, as well as increasing our line of credit limit up to $500,000. Together, these changes will help reduce repayments while serving a larger and more diverse group of businesses,” says Sanz.

In a residential mortgage sector where brokers dominate market share, customers have never had so many brokers to choose from. That’s why brokers need the right plan and tools to market themselves effectively to clients

IT’S NO LONGER enough for mortgage brokers to just explain to customers what services they provide and then expect valuable leads to flow. Potential clients want to know much more about the brokers themselves – their values, their goals, their personalities – before they choose a broker.

In an industry in which almost 74% of all new residential home loans are written by brokers, a smart and well-executed marketing strategy can help brokers cut through a crowded market. It’s all about creating a personal brand and tailoring your

marketing plan to your client base.

Social media is also vital and requires a regular, high-touch approach that engages your audience and prompts further action.

To understand how an effective marketing plan can help brokers succeed, MPA sought the views of Blake Buchanan, general manager of Specialist Finance Group (SFG); Sally Chadwick, executive manager, corporate communications, events and franchise marketing at Mortgage Choice; and Emily Lonsdale, general manager – growth at Lendi Group.

Support with marketing strategies

“If you fail to plan, you are planning to fail” is a well-worn phrase, but apt when it comes to brokers promoting their businesses.

Chadwick says brokers should set up marketing strategies aligned with their aspirations. “An effective marketing strategy will enable you to stand out from the competition, connect with new and existing customers and grow your business,” she says.

“At Mortgage Choice, our brokers’ priority is supporting their customers. We don’t expect them to be marketing experts, which is why we provide our brokers with personalised support to create effective marketing strategies.”

Mortgage Choice franchisees are encouraged to complete an annual Marketing Planner to structure their local marketing activity. Chadwick says being more strategic enables brokers to benefit “from the significant investment we make into the Mortgage Choice brand, and our connection with the realestate.com.au brand”.

“We help brokers leverage that national brand presence by providing a huge range of marketing tools, resources, campaign assets, technology and expert advice that they can use locally to build their brand, generate leads and nurture customer relationships.”

Buchanan says brokers have marketing opportunities through many channels, including existing clients, referrers and especially the open market. “Our role is to provide

information, strategic advice and, importantly, access to systems such as SFGconnect that can digitise much of the marketing you do in your business,” he says.

“Whilst there are finite channels that you can market within, brokers should take a holistic approach to marketing and imbed these in your business activities.”

Buchanan says if brokers don’t have particular strengths in certain areas, they should look to outsource these systems and seek out experts who can help them with their marketing journey.

Lonsdale says Lendi Group invests heavily in digital advertising campaigns across multiple platforms, including Google and Meta, to increase brand awareness and drive customer appointments to Aussie retail stores and broker businesses. “Earlier this year, we launched our Aussie mobile app, which has put our brokers’ businesses in the palms of their customers, facilitating brokercustomer connection more easily than ever before. The app is equipped with a range of features, including referral tools, that support lead generation.”

Digital marketing is not just about top-offunnel lead generation, says Lonsdale. Lendi

Oct 22–Mar 23

tions, allowing brokers to leverage promotions year-round to drive customer growth and incentivise appointments.”

Chadwick says growth looks different for everyone, so creating a tailored strategy is an opportunity to set clear goals, define success and then adapt activity to suit. “For example, if your main goal is brand awareness or lead generation, the marketing activities you

“Our role is to provide information, strategic advice and, importantly, access to systems such as SFGconnect that can digitise much of the marketing you do in your business”

Blake Buchanan, SFG

Group uses a sophisticated CRM strategy to nurture low-intent leads into high-intent customers and to re-engage past customers, bringing them back into the funnel.

“Our journeys program places customers into bespoke nurture journeys where they receive tailored communications relevant to their situation,” says Lonsdale. “We’ve adopted an ‘always on’ approach to competi-

choose to invest in will likely be different than those for connecting with existing customers or building business referral relationships.”

Mortgage Choice’s CRM platform delivers targeted communications using advanced email segmentation and content personalisation. The aggregator also works closely with brokers to refine their SEO strategies and improve search rankings.

23–Sep 23

Social media: an essential tool

Buchanan says social media is a costeffective way for brokers to get their message out and is preferred by those who know how to capitalise on it. “Two important things to remember – have an impactful message and a hook to increase enquiries but also to ensure you have an audience.”

Brokers can build their own audience on social media by requesting that people like and follow their page. “Alternatively, why not get your message out to an already-built audience,” says Buchanan. “For this, community or interest groups are a great way to advertise and participate in conversations about finance needs. With social media it takes consistency, and it will deliver results over time if your message is great.”

More than 95% of Australians own a smartphone, says Lonsdale, so social media is a vital avenue for connecting brokers and customers and meeting customers where they hang out – online.

“For many people, their property search journey starts on social media,” she says. “Property buyers are looking for experts to answer their questions, and brokers have a key role in educating them.

“Mortgage broking is a people-centric industry; social media is an effective tool for brokers to showcase their human side, build

a personal brand and create an online community,” Lonsdale says.

Lendi Group provides training and resources to help brokers grow their social presence, including social media masterclasses and a comprehensive suite of collateral they can customise for their business. “We’re constantly capturing video and visual content and encourage our brokers to get involved – our brokers are the stars of the show,” she says.

audience wants. Consistency is key – stay true to your brand and be consistent with your visual style, your tone of voice and the type of content you produce.”

Lendi Group encourages brokers to embrace networking with existing customer bases, local businesses, online and out in the community, says Lonsdale.

“Don’t be shy to ask for referrals. Word of mouth can be a huge driver of business, and

“Having a view on relevant topics and informing and educating your target audience about the issues that matter to them can create more powerful connections and build trust”

Sally Chadwick, Mortgage Choice

Chadwick says TikTok, Instagram, Facebook and LinkedIn are invaluable for building an online presence, connecting with new audiences and staying top of mind for existing customers. “We encourage brokers to include social media as a core part of their marketing strategy.”

Buying a home is the biggest financial decision many people will make, so trust is hugely important. “Building an authentic identity through social media can help to build and reinforce that trust,” she says.

To help drive engagement, each month Mortgage Choice brokers are provided with timely and relevant content, including seasonal competitions, to post on social media via a social media scheduling tool.

Lonsdale says brokers need to be visible and present, online and in their community. “Building and sustaining a personal brand requires a consistent cadence of activity for cut-through; it’s not something you can stop and start.

“To resonate with your target customers, you need to know who you are and what your

great businesses are built on referrals. Look for avenues to add credibility to your personal brand, including industry awards and thought leadership opportunities in media.”

Aussie brokers are assisted in building their personal brand through community activations; support with establishing and maintaining an online and social media presence; media opportunities to showcase their expertise; support with industry award

343,524

submissions; and dollar-for-dollar matching incentives to encourage local area marketing initiatives.

Chadwick says a unique and authentic personal brand sets brokers apart from their competitors and creates meaningful connections with target markets.

When building a personal brand, she says it’s important for brokers to reflect on both their own and their business’s strengths and values. “Understand your target audience and define your unique selling proposition. This is where you define what makes you di erent and how this will benefit your target audience.”

Thought leadership is also important, says Chadwick. “Having a view on relevant topics and informing and educating your target audience about the issues that matter to them can create more powerful connections and build trust.”

She suggests making short social media videos, for example highlighting government incentives for first home buyers, and notes that customer testimonials and positive Google reviews are also powerful tools.

Buchanan says brokers need to have a customer journey process attached to their service. This will not only ensure consistency of service but also bring the wow factor to clients.

“If you do this, you can grow your audience by asking for reviews and promoting

360,316

4.89% Oct 22–Mar 23 Apr 23–Sep 23

these through your marketing. Don’t forget to also o er to assist any of your clients or referrer networks as these are the lowhanging fruit when you do an excellent job.”

Brokers need to also target specific audiences such as first home buyers, property investors and SMSFs. Buchanan says a cheap and easy way to do this is to join groups focused on these interests or niche markets. “If there isn’t one out there, you can build your own community and o er insights to your desired market. There are also plenty of seminars and networking groups that you can join, but again, these take time and consistency to be able to create a known profile for yourself which will gain trust and grow enquiries.”

Chadwick says, “You need to meet your audience where they are. That means understanding their needs and what matters to them and being active on the channels they use. It’s also important to deliver content in a language and tone that will resonate with your target audience.” For example, younger first home buyers are more active on TikTok than other platforms.

Tailoring and personalisation is crucial in email marketing, Chadwick says. She advises brokers to personalise content and use a segmented database, so audiences are not being sent irrelevant content.

On social media, she says paid activity – such as ‘boosting’ social media content or running campaigns – can help brokers target social media users with specific interests or from specific demographics. Local area marketing activity, such as sponsoring community events during the Hindu holiday of Diwali, is a good way to reach specific clients.

So, once your strategy is place and your marketing activities are in full swing, how do you gauge success? This is where data analytics come in.

Lonsdale says it’s vital for brokers to be across cost-per-lead, cost-per-acquisition and conversion metrics. “This will help you develop an understanding of what strategies have

“Brokers need to be visible and present. Building and sustaining a personal brand requires a consistent cadence of activity for cut-through; it’s not something you can stop and start”

Emily Lonsdale, Lendi Group

been successful and which haven’t, so you can direct your time, energy and marketing spend toward activity that converts e ciently and successfully.”

Buchanan says brokers need to understand how their client base performs by looking at their data, and design marketing strategies accordingly. “An example might be the average life of a loan that you introduce. If you know that on average your clients are refinancing every four to five years, what are you telling them in the lead-up to this period?”

Brokers could have a digitised marketing strategy that informs clients that they’re doing this and the reasons why, Buchanan says. That would position this review period as normal or something that they should be doing.

“Whether it be repricing or refinancing, this strategy has seen reduced attrition rates across many businesses. This in turn can reduce the

need to fill the funnel at the front as you are having fewer leave your service at the back.”

Chadwick says understanding and leveraging data analytics enables brokers to optimise marketing strategies and spend, make more informed decisions, refine targeting and create more e ective campaigns – ultimately leading to improved conversion.

It’s important to understand key metrics –tracking where leads are coming from, looking at engagement metrics such as email open and click-through rates, and measuring the percentage of leads that convert to clients.

Mortgage Choice provides brokers with reporting on their top social media posts each month. “We also take an enterprise view of engagement, which informs our marketing team’s decisions when planning social media and other marketing content for the months ahead,” says Chadwick.

We’ve

Don’t

Aussie’s Platform Plus system is helping brokers such as Samer Demerdash and Clay Bremer achieve career milestones, scale their businesses and thrive in the competitive mortgage industry

DRIVING A business as a mortgage broker is hard, particularly in today’s tough market. Finding a support system that empowers you to build the business you want while delivering top-notch results is invaluable for today’s broker.

Aussie’s Platform Plus support model is designed to do just that, o ering brokers the tools, technology and tailored assistance to not just survive but thrive. It’s a model that doesn’t just streamline processes; it helps brokers create a business that works for them, no matter where they are in their career journey.

For brokers such as Samer Demerdash and Clay Bremer, this innovative system has been

a game changer. Demerdash and Bremer have each harnessed the power of Platform Plus to transform their businesses. From scaling their operations to transitioning into new roles, their stories are proof that, with the right support, there’s no limit to what a broker can achieve.

The journey to becoming a No. 1 broker Demerdash’s rise to the top of the Aussie network is a testament to hard work and strategic adaptation. Joining Aussie in 2017 after a career at Commonwealth Bank, Demerdash was drawn by the freedom and flexibility of the mobile broking model.

“Aussie’s mobile broker o ering gave me

the opportunity to leverage my skills and experience to build a business of my own,” Demerdash tells MPA.

In FY24, Demerdash became Aussie’s No. 1 broker, achieving 30% year-on-year business growth and settling over $127 million. Demerdash’s breakout year also sees him ranked among MPA’s Top 100 Brokers for the first time.

He attributes this growth largely to the Platform Plus model, which, in his words, “allowed me to work much more e ciently and ultimately write more business”. The pre-qualified appointments and operational support provided by Aussie’s Associates and Client Solutions team have been pivotal.

“One of the main advantages of the Platform Plus model is that brokers are provided with high-quality appointments rather than cold, indiscriminate leads,” Demerdash explains. With administrative tasks taken care of, he can focus on providing exceptional client service and building his network.

Demerdash also emphasises the importance of creating a solid foundation in the early stages of broking.

“In the beginning, I focused on building relationships in the community by connecting with like-minded business owners and leveraging my personal network,” he recalls. This focus on connection-building laid the groundwork for his future success, as referrals have now become his largest source of leads.

His advice for other brokers? “Tap into the technology and tools available. Time saved is time that can be invested into building relationships and growing your business.”

For Clay Bremer, becoming a mortgage broker marked a significant career shift after 13 years as an aircraft engineer in the Air

“Fully embrace the technology and tools available. Time saved is time that can be invested into building relationships and growing your business” Samer Demerdash, Aussie

Looking ahead, Demerdash has no plans to slow down. “The only way is up! My goal for 2025 is to exceed the $127 million of FY24,” he says. “I plan to continue leaning into the Platform Plus support model, leveraging the services available to me and delivering exceptional outcomes for my customers. By doing so, I’ll keep growing my business and generating more referrals.”

Force. When he joined Aussie in 2021, he was new to the industry but determined to succeed. “I enjoy working with numbers and people, so broking seemed like a natural choice,” he explains.

Bremer quickly rose to become Queensland’s No. 1 mobile broker in FY24. His secret? Hard work and making the most of Aussie’s support model.

25+

lenders

3,000

home loan options

30+

Multichannel years in the industry

distribution model with various broker pathways

“Platform Plus has allowed me the freedom to focus directly on growth activities like generating appointments, meeting new clients and expanding my presence in the community,” Bremer says.

The support system gave him the confidence to take the leap from mobile broking to franchise ownership.

In October 2024, Bremer purchased Aussie Tewantin on Queensland’s Sunshine Coast, marking a new chapter in his journey as a business owner.

“I’ve been able to leverage the model to build a successful mobile broking business, and now I’m excited to see the productivity I believe will be unlocked by having a team of brokers under one roof all harnessing the same scalable systems,” he says.

Bremer is already working on fostering a high-performing team and building a positive culture. “Aussie provides the tools for success, from AI to client solutions to admin support. I’m giving my brokers the best chance to succeed by ensuring they can focus on what matters – customer care,” he explains.

Looking ahead, Bremer’s ambitions extend beyond Tewantin. “My ultimate goal is to scale to multi-site ownership while maintaining a strong team culture. I want to create a business that thrives on collaboration and shared success.”

Empowering brokers at every stage

Demerdash and Bremer’s stories highlight the versatility of Aussie’s Platform Plus model.

“The more people there are, the more knowledge is shared and the stronger the business. Power and knowledge lie in the collective,” Bremer says.

As both brokers look to the future, their stories demonstrate that Aussie’s Platform Plus model isn’t just about immediate success – it’s a pathway to long-term growth. Whether it’s scaling a business to new heights or making the leap to franchise ownership, the right support can make all the di erence.

Demerdash and Bremer have ambitious goals for the coming years.

For Demerdash, it’s about building on his success and continuing to refine his approach

“Build a high-performance team and leverage the recognised brand and support systems. It’s a game changer” Clay Bremer, Aussie

Whether breaking into the industry, thriving as a solo operator or growing a team, brokers can harness the support system to achieve their goals. From pre-qualified leads to streamlined loan processing, Platform Plus empowers brokers to focus on what they do best: connecting with clients and growing their businesses.

For Demerdash, leveraging the model has allowed him to focus on providing exceptional service to his clients and expanding his referral network. “Technology, AI and automation are here to stay. Fully embrace them to deliver better outcomes for your customers and make your work more seamless and e cient,” he says.

Meanwhile, Bremer is laying the groundwork for his long-term success. By investing in his team and integrating into his local community through partnerships with complementary businesses, he is creating a strong foundation for sustainable growth.

to client service. “I want to consistently deliver better outcomes for my customers, exceed my targets and grow my business even further,” he says.

Bremer is equally driven, with plans to expand his business and deepen his ties to the local community. “I’m excited to grow the team, support my brokers and eventually expand my store footprint,” he says. “But above all, I want to create a positive, thriving workplace where everyone feels supported.”

Their journeys are a testament to what’s possible with the right tools, a clear vision and a commitment to growth. For brokers looking to take the next step in their careers, Aussie’s Platform Plus model o ers a roadmap to success.

To find out more about Aussie’s Platform Plus model and how it can help supercharge your business, go to www.aussie.com.au/ join-us/broker-opportunities/.

Quali ed customer appointments booked for brokers

Loan processing support provided

Sophisticated customer journeys CRM program

Proprietary platform with Approval Con dence technology

Set business funding expectations upfront with clients

Quoting for Line of Credit and Small Business Loans up to $250K

Quote with no impact to client’s credit scores

Automated bank statement analysis

Learn more about Prospa IQ

Third party heads from leading non-bank lenders joined MPA’s annual industry roundtable to discuss the growth of the sector, broker partnerships, competition, technology and cybersecurity

DESPITE THE challenges of a constrained economy, the value proposition of non-banks hasn’t changed. Non-bank lenders continue to o er flexible finance solutions that banks don’t provide, focusing on clients such as the self-employed and small business owners, who often don’t fit the narrow credit criteria that banks apply.

In a cost of living crisis, and with mortgage holders feeling the e ects of higher interest

rates, you could argue that this is where nonbanks come into their own.

Brokers working with non-bank lenders understand their value proposition and how they can assist brokers in servicing a wider range of customers beyond the vanilla. This benefits broker businesses, enabling them to provide more lending options and strengthen client relationships.

Non-banks rely heavily on their broker

partners to funnel customers their way, and as the sector grows, it appears more brokers are realising the value of these lenders, boosting growth in this market.

It’s clear that non-banks compete with banks on solution rather than price, and brokers understand this. But in a competitive lending environment, which can be complex and challenging, non-banks can’t stand still. They need to constantly review their products, policies and

processes to ensure they adapt and keep pace with the needs of brokers and their clients.

Turnaround times, technology and cybersecurity are all important areas that non-banks are working on. They will also need to be prepared to pivot when the RBA moves to cut the o cial cash rate some time in 2025.

To discuss these and other crucial matters for the sector, MPA recently held the 2024 Non-Banks Roundtable at Nobu in Sydney,

bringing together third party leaders from many of Australia’s non-bank lenders, as well as Top 100 Brokers 2024 winner Stephen Michaels, managing director of Catalyst Advisers.

Participants included Jason Arnold, group executive – origination, Pallas Capital; Cory Bannister, senior vice president and chief lending o cer, La Trobe Financial; Royden D’Vaz, general manager distribution and partnerships, Assetline Capital; Tim Lemon,

national sales manager, MA Money; Tony MacRae, chief commercial o cer, Bluestone Home Loans; Chris Paterson, general manager distribution, Resimac; Lee Prior, director of distribution, ORDE Financial; Barry Saoud, general manager mortgage and commercial lending, Pepper Money; David Smith, chief distribution o cer, Liberty; and Belinda Wright, head of partnerships and distribution, Thinktank.

How has the non-bank sector adapted to changing economic conditions over the past 12 months? What have been the key challenges and opportunities for brokers and their clients, and how have you worked with them?

MacRae said it has been an interesting period in the non-bank sector because as the economy has changed, more customers are now falling outside the traditional bank space, providing more opportunities for non-banks.

“At Bluestone, we’ve seen it as a wonderful 12 months of opportunity where we’ve been able to work really closely with brokers, not product flogging but educating in the non-standard space, including near prime, specialist and SMSF lending, to help brokers actually grow their business,” MacRae said.

Bluestone looks at the economic circumstances as an opportunity to push itself forward. “We think the market that falls into the space that we specifically cater for is

“International investment into our nonbank sector is stronger than ever. It’s a signal that there’s increasing interest and attention on Australia globally. Other players are waking up to the potential for growth here” Jason Arnold, Pallas Capital

growing, and being able to provide solutions has seen us significantly increase our volumes over that 12-month period.”

Prior said the changing economy and trends in customer engagement have highlighted an opportunity to further support brokers with more proactive, rather than reactive, strategies.

He said previously brokers were understandably focused on responding to customer needs, such as requests for more competitive rates and cashbacks. However,

after that initial focus, economic changes slowed that growth.

“We’ve got a segment of brokers that have had a reduced need to rely on proactive strategies,” said Prior.

“While the changing economy does have its challenges, there’s also a lot of opportunities for brokers who can successfully navigate this period. ORDE is focused on providing brokers with the support and education they need to better service their clients and grow their business. That means support not just

Open the door to your next move. And theirs.

At Aussie, the doors keep opening – with pathways from broker, to franchisee, to CEO of your own business, and proven support systems to help you get there.

There’s never been a better time to make your move and help Aussies achieve their property dreams. Ready to open the door to opportunity?

Talk to us today.

with products and customer engagement but with referrers and internal processes as well.”

D’Vaz said he believes the current challenge for brokers is not high interest rates or the housing market but more informed customers with higher expectations, which some would say are unrealistic.

However, “for them [customers], those expectations are not unrealistic,” he said. “For a broker, just sticking to one product is not enough any more. Diversifying and broadening your expertise and exploring a full range of opportunities is what’s needed to stay competitive.”

D’Vaz said all non-bank lenders around the table were trying to enhance their offerings and improve policies, given that brokers have access to so many lending options.

“If you look at our business [Assetline Capital], we’ve been one of the leaders in that short-term development and construction space, but we realise that we have to keep moving and be dynamic and agile and offer

more solutions for the brokers.” He encouraged brokers to diversify.

Picking up on D’Vaz’s comment about customer expectations, Michaels said what he wants to do is keep striving forward. He gave the example of a customer who had banked with a major bank for 10 years but had not received the credit answer they wanted from the bank, despite being in a good, creditworthy financial position.

“If you don’t have that option in your toolbelt where you can tell them, ‘now we’re going to our mid-tiers and our non-bank lenders’, then you’re just going to be left behind,” said Michaels.

Previously, Catalyst Advisers brokers would catch up with referral partners for lunch, and “you would just shake the tree and deals would fall out”, but now there had to be a specific reason behind the conversation. “And that reason might be, I spoke to you six months ago, and I couldn’t help that client out. Now we’ve got a different non-bank that

can provide that solution that wasn’t there six months ago.” Michaels said.

“Non-banks give us a reason to, a, keep servicing our clients, but also, b, a reason to keep servicing our referral partners too.”

Diversifying is key for brokers in the construction space, Arnold said. Cost increases have made it a particularly tough market for development finance.

“Valuations have come off in certain segments, cap rates have softened, builders have fallen over, so we’ve never worked more closely with our broker partners,” he said. This includes working through issues such as when feasibility don’t stack up on building projects.

Arnold said that for those brokers looking to diversify away from the banks, needing extra leverage, such as senior and mezzanine finance as well as lower presales, the non-bank sector offers that diversity. “That’s something that will help brokers offer more options to their clients.”

Bannister argued that not a lot had changed in the last 12 months. “In my view, if you’ve only just adapted to current market conditions recently in the last 12 months, you’ve missed a significant opportunity,” he said.

“The market dislocation started off three or four years ago around COVID time, and it’s been the perfect market for a non-bank for a whole host of reasons.”

Bannister said the opportunities for nonbanks had started when banks “pulled in” when it came to finance. “That’s our traditional market. In the last three years, our addressable market has increased significantly on the back of that.”

For non-banks and brokers, it was not about adapting in the last 12 months but continuing to show their value propositions.

Bannister agreed that there were more brokers attempting to use non-banks for the first time, but 80% of La Trobe Financial’s business came from brokers who had discovered the benefits of using its services a lot longer than 12 months ago.

Saoud said, “The non-bank sector plays a vital role in the Australian financial system,

fostering financial inclusion in a market where the real-life needs of borrowers are not always met by mainstream banks.” He said he had seen a continuous improvement in the market for non-bank lending since COVID.

“There’s been a strong continuation of the

wants to maintain an agile nature as a competitive advantage – developing products, working with brokers, understanding the gaps and providing holistic solutions.

Prior said experienced brokers had seen their businesses continue to grow in the

“La Trobe Financial, like many other non-banks, doesn’t try to compete head to head with the banks. We instead target those overlooked or underserved niches” Cory Bannister, La Trobe Financial

changing demographics of your traditional borrower,” Saoud said. “For us, it’s all about a purpose-led solution. How do we continue to fill the gap where the banks aren’t? How do we continue to innovate in the space –whether it’s through our product, through policy, service or experience?”

Pepper Money, like other non-banks,

post-COVID period, but the last 12 months were an opportunity to stop and reflect on their business and make some changes.

“That’s an area where we have supported brokers. We [ORDE Financial] are working with a couple of big groups on how we could help them speak to their referrer networks about valuable new opportunities

or solutions that have become available since the last time they were in contact,” he said.

Smith said Liberty had seen a significant number of new brokers sending business its way.

“The focus for us in recent times has been education – responding to that first-time broker user,” he said. “It means that the sales conversation out in the market is a longer but a deeper conversation, rather than, as Stephen says, shake the tree and the deals will come; now it’s an education conversation.”

D’Vaz said the onus is also on the broker to find out more. “We’re providing the platforms for them to come and learn, and trying to get them to do that can be difficult. We can enhance our products, policies and pricing, but they’ve got to be proactive.

“They need to say, ‘I want to diversify my proposition; I want to learn more. What are you guys offering?’ They’ve got so many options and so much choice now.”

Smith said that because non-bank deals are often less frequent for brokers, the challenge is to maintain visibility and recall. “We have to

“For a broker, just one product isn’t going to be enough any more. Diversifying and broadening your expertise and exploring a full range of opportunities is what’s needed to stay competitive” Royden D’Vaz, Assetline Capital

work harder to stay front of mind like a major might for a straightforward deal.”

MacRae said Bluestone has seen a rising appetite for brokers wanting to learn and diversify. “We’ve seen what we call active brokers double in the last 12 months.”

Since Bluestone launched SMSF lending about 18 months ago, more than half of the brokers that had written SMSF loans with the non-bank had not written deals with Bluestone previously. “All of those, on average, have

brought us another non-SMSF deal, so they are expanding and using it as entry points,” said MacRae.

Wright said diversification had been around for a long time, but there had been no change to “how we talk about commercial and SMSF”. She said she was aware of this, having worked in the residential space for 22 years and then moved into commercial and SMSF at Thinktank.

“At first, commercial may seem complex,

but it’s simply a self-employed loan with a di erent type of security, while SMSF has become a straightforward, repeatable loan product to access. Once we break it all down and explain it, brokers quickly grasp it,” Wright said.

“That’s why we’re focused on broker education, changing the way we communicate with brokers, demystifying SMSF and commercial and really helping them along that journey.”

Lemon said five years ago when talking to a broker, most of them would say, “I don’t write non-bank”.

“Today, it would be very hard to find a broker that would say, ‘I haven’t written a non-bank deal in the last 12 months’,” he said. ‘That’s probably the best part for all of us.”

The MFAA Industry Intelligence Service’s latest report shows that non-bank market share was up 0.5%, rising to 3.5% for the quarter, but the value of non-bank loans fell by 19.6%. From your own data and observations, how are non-banks faring when it comes to competing with banks for broker share of loans, and how are you differentiating your offering in terms of products, pricing and service to brokers and clients?

Paterson said it’s important for non-banks to have diverse options, such as product niches, policies and serviceability criteria, that can help secure finance to meet customers’ needs.

“There are more customers falling outside the square [of banks], and as a broker, if you can educate and provide a solution, there’s more competition in the non-bank space than there ever has been,” he said.

“There’s a lot of di erent options for brokers and customers to consider, and I think that’s where non-bank growth will continue to come – writing those products and policies that the banks don’t.”

Prior said it was di cult to quantify and compare ORDE Financial’s data compared to the MFAA’s findings, as the company has seen positive growth since its launch four years ago. Since 2020, ORDE Financial

has settled around $6 billion and is still in a growth phase, with broker use and volumes increasing.

As a new entrant to the market, Pallas Capital’s growth over the last few years has been significant, Arnold said. The non-bank has enjoyed good brand awareness among brokers and has also ensured its products and pricing are flexible enough to attract brokers.

Bannister said the first point to make about La Trobe Financial was that, like other non-banks, it doesn’t try to compete with the banks. “We know where we sit in the market – we target those overlooked or underserved niches,” he said.

The total addressable market for nonbanks has increased significantly, and there are a few reasons for that, Bannister said. These include regulations on banks, and banks choosing to go after automatable mortgages.

While non-bank lending volumes at the top-line level might have fallen, this is market-driven, he said.

“It’s been a pretty quiet period in terms of sales and purchases in the market over the last 12 months,” Bannister said. “We’re at the peak

of the rate cycle; people’s hands are in their pockets, but I think generally, as a proportion, non-banks are certainly doing well.”

D’Vaz said the MFAA figures don’t quite match what is happening. “Looking at the non-bank sector, I think we do a pretty good job. We’ve got a very high-touch strategy –the BDMs do a great job of getting brokers engaged and hold their hands and walk them

table were a diversified group, competing across a wide range of asset classes.

“If you look at that fuller picture, I’d say the share of voice that the non-bank sector has claimed over the last 12 to 24 months would have increased much more significantly than half a per cent,” Smith said.

Bannister said non-banks also increase the size of the pie available for mortgages written

“Five years ago most brokers would say, ‘I don’t write non-bank’. Today, it would be very hard to find a broker that hasn’t written a non-bank deal in the last 12 months” Tim Lemon, MA Money

through the process and workshop a deal.

“We don’t ever compete with the banks; we don’t want to. What we do, we do it very well.”

Smith said the MFAA provides a lens into the sector, but perhaps not the widest of lenses. The non-banks represented at the

in Australia. “Without the non-banks writing what they write, the pie just shrinks.”

La Trobe Financial is not interested in shifting the pie by heading to a broker’s office and asking what other non-bank lenders are doing and trying to claim a slice of that. Instead, Bannister said it is laser-focused on

areas of the market that aren’t being serviced by other non-banks.

“You’ll find that over time that if you can close enough of those gaps, the whole market grows with you,” Bannister said.

While non-banks are shifting some market share from banks on the edges when it comes to serviceability and policy, Bannister said non-banks are focused on catering for areas of the market in which the banks have no appetite.

D’Vaz said he believed that much of the residential broker market share of almost 74% had been driven by non-banks because their distribution strategies are predominantly through brokers.

MacRae said he also doubted the MFAA’s numbers because Bluestone is in a growth phase, bringing new brokers in, providing better education and delivering solutions.

“I don’t know how many conversations I’ve had with brokers in the last 12 months, where they’ve said, ‘I’ve been letting business walk by my door’, and now all of a sudden they’re going, ‘I’ve got an opportunity to do things differently [with a non-bank].”

Michaels said brokers are now used to dealing with all the non-banks represented at the roundtable. “Someone writes an SMSF deal [with a non-bank], and three months later they’re also writing another deal, such as a light-doc or a low-doc type deal.”

Consumers are also more familiar with the non-banks now, compared to three or four ago when brokers had to educate clients and explain what non-banks did.

Non-bank growth is happening right now, Michaels said, and he expects that to continue into the future, even when the banks are back in the market, interest rates have fallen and APRA has loosened the buffer.

“There’ll be consumers that will say, ‘take me back to that prime lender’, but then there’ll be others that will say, ‘well, they weren’t there for me when I needed them, so let’s keep going because it’s easier, it’s more flexible [with a non-bank]’, ” said Michaels. “Yes, I’m paying a premium, but I’m paying

a premium because it adds value.”

Wright said at Thinktank one reason for market share being lost is customer run-off, and this can be due to BID requirements.

“Mortgage brokers are dedicated to ensuring the best interests of their clients, as they should be. What we are observing is that most banks are actively in market with very strong, easy refinance offerings for the most standard deals, so it’s very hard for us to compete in that space,” said Wright.

The broker has to do the right thing by the customer, which may mean moving them to a bank if they can get a better deal for the client and that meets BID.

Saoud said non-banks had struggled a few years ago when the RBA provided a term funding facility (TFF) to the banks, giving them a competitive advantage. “As part of that, they [banks] had the cashbacks, where they did grow share against the non-banks.”

However, now that the TFF has ended and cashbacks have fallen away, there is a more even playing field for non-banks when it comes to the cost of funds, he said. “This makes us much more attractive to our brokers

and borrowers now when the biggest differentiator isn’t necessarily price, but rather the experience and solutions we offer.”

Non-banks’ solution-led offerings appeal to brokers and consumers for several reasons, Saoud said. “We create trust, transparency, accessibility, and provided we continue to do that as an industry, we’ll see the non-bank sector carry on growing and thriving.”

Broker question from Stephen Michaels: What are the key considerations that non-banks make or think about with their product offerings when knowing they are competing against the big four banks? How do you continuously work on setting yourself apart?

The key, said Arnold, is to not get involved in a pricing war with the banks, because nonbanks can’t win.

“It’s a combination of efficiency and turnaround times and adjusting your policy and combining that with pricing against other non-banks. Combine those three elements –turnaround times, credit policy and pricing;

that’s where your competitive advantage lies,” Arnold said.

At Thinktank, it’s all about understanding the customers it serves, 95% of whom are selfemployed, Wright said.

“It’s about listening to brokers to innovate with products and enhance our policy. When you’re working with self-employed people, it’s about understanding that they all have unique circumstances and needs, and being able to offer that broad range of solutions, whether it be commercial lending, SMSF, residential or our latest private lending offering … and delivering service for the broker as well.”

Lemon said MA Money also focuses on technology – to make sure brokers provide an answer to the customer as quickly as possible. And it’s important to look at postsettlement services, such as internet banking and free features that can be offered to ensure customer retention.

“The longer that customer stays with you, the happier the broker,” he said.

Prior said non-banks should also focus on talking to brokers about products or services that are missing and what gaps they can fill.

“Education has been spoken about, but it comes back to experience,” he said. That means non-banks having the “right people taking the right phone calls and sending the right emails” to ensure that brokers are aware of the difference between non-banks and the banks.

Michaels highlighted some of the ways non-banks do things differently from banks, especially as one in 25 deals is a non-bank deal. He said the service brokers receive from non-banks is completely different to that of the banks. “It’s because non-banks appreciate that you are having to deliver a service before you then deliver a loan product.”

Non-banks market their products in a more personable way than the big banks, Michaels said. “As a broker, you feel like you’re actually dealing with a human being.”

With banks, relationship managers change often, creating a lack of consistency. “As soon as you submit your deal to the bank, you lose

“We’ll always look at the individual deal and assess it. It’s fundamental to how we really differentiate ourselves. Banks will have their 10-minute mortgage, but we’ll find the solution for that complex customer” Tony MacRae, Bluestone Home Loans

all control,” Michaels said. “It’s the scariest thing in the world when you hit submit.”

Conversely, with a non-bank such as MA Money, he said he had known Lemon and written deals with him for 12 years and knew what to expect, compared with a bank BDM he had never met.

Paterson said the strength of non-banks’ BDM teams helps brokers. “Resimac’s view is to help a broker grow their business. We spend time with them getting an understanding of their business and customers. Our BDMs support and educate when it comes to writing that next loan, streamlining the application and credit experience, helping brokers to spot applications likely to get approved or not.

“But also, if they’re faced with a hurdle, the BDM often goes in to bat for their broker.”

Smith said, in answer to Michaels’ question, it was important to note that what the market saw as non-traditional lending a few years ago, and sees now, could become mainstream tomorrow and vice versa. The employment economy is shifting so rapidly that non-banks need to adapt.

He said Michaels will be seeing different customers now to the ones he saw five years ago. “There used to be a quarter of a per cent of the economy represented by those customers, and now there’s 10 times that, and in a couple of years’ time it’ll be five times that again.”

Michaels said he always tells his Catalyst team that, due to the changing nature of rates, policies and property markets, if they are using the same sales pitch and approach to a

client that they had used three months ago, it will be stale.

Customers are also changing how and when they communicate, with Michaels’ clients preferring WhatsApp to emails. “I’m taking phone calls at 8.45 p.m. at night because our clients are really busy professionals. You’ve got to just shift with your customers.”

type of data is most important … so that when we do roll out [in the] AI world, we’re better equipped,” Lemon said.

D’Vaz, who has been in the non-bank sector for a number of years, said he had a di erent view when it came to technology.

“If you don’t continue to evolve your tech, you’re going to get left behind quickly. [It’s about] a continuous review to improve e ciencies, speed to yes, that admin that frustrates brokers and customers” Chris Paterson, Resimac

Brokers need to be dynamic, shifting with the changing market and serving customers’ needs accordingly, Michaels said.

He pointed out that, as a Catalyst broker, he has more in common with non-banks than banks. “Non-banks are thinking, ‘I want to be customer-focused, I want to be agile, and I want a service where no other lender can service’ – that’s a broker; you might as well be a broker.”

Prior said this was the second time he had heard a broker compare their own business to a non-bank’s.

How are you investing in technology and AI to improve credit decisioning, loan processing and turnaround times? What role does broker feedback play in improving tech and your overall offering?

Lemon said that, in response to broker feedback, MA Money had invested heavily in technology to make sure turnaround times were as quick as possible. Its use of AI is in its early stages, but this will ramp up in 2025, with MA Money focusing on data collection and storage.