How brokers are steering mutuals forward INDUSTRY’S RISING STARS Meet Australia’s top young brokers

BANKS IN 2025 Macquarie Bank’s winning streak

Paul Wells and Ryan Harkness

ORDE Financial

CONNECT WITH US

Got a story or suggestion, or just want to find out some more information?

twitter.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

UPFRONT

02 Editorial

Democracy at work in the finance space

04 Statistics

Signs of a slowdown in the rental market

06 Opinion

Broker-tailored loyalty programs can be a great motivator

FEATURES

FEATURES MUTUAL BANKS AT THE TABLE

26 Brokers’ bank of choice

Customer-owned banks discuss the vital role they play in the sector, with the strong backing of brokers

Macquarie Bank on the secrets to its success as fourth-time winner of Brokers on Banks

SPECIAL REPORT

BROKERS ON BANKS 2025

Brokers’ ratings show this year’s best banks prioritise clarity, responsiveness and relationship-driven support

BIG INTERVIEW WILLIAM LOCKETT

For Specialist Finance

Group’s managing director, success is all about maintaining strong relationships and loving the job

54 Making dreams happen

Specialist lenders are coming to the rescue when borrowers face rejection

68 Tips for securing the best talent

An insider’s guide to gaining a competitive edge in recruitment

PEOPLE BUILT FOR BROKERS

ORDE Financial celebrates five years of rapid growth driven by an unwavering focus on brokers 30 SPECIAL REPORT RISING STARS IN BROKING

PEOPLE

70 Brokerage insight

It’s all about the community for Mortgage Choice franchise owner Belinda Sugars

72 Other life

Wisr head of broker Nicole Evans aligns her passion for fitness with her professional life

Australia’s top young brokers in 2025 are shaping a brighter future for borrowers

Our daily newsletter. Keep on top of property market trends, business strategy, and what industry leaders have to say.

Democracy is the best form of flattery

Whoever wins, we lose. So went the tagline of mediocre 2004 monster mashup Alien vs. Predator

While Australia’s impending federal election might not be quite as dire a binary decision, there is certainly a sense that priorities are lacking as our candidates make their pitches to the electorate.

LNP hopeful Peter Dutton has been trying his hardest to steer the political discourse deeper into US-flavoured culture wars territory with his chest-beating about Australia Day celebrations and the prevalence of the Aboriginal flag on Sydney’s iconic infrastructure.

Incumbent Labor leader Anthony Albanese, for his part, is out of step with the Australian electorate. Cowardly apolitical that I am, this is not necessarily my opinion but the sentiment expressed in voter polls on the matter.

Ultimately, Australian democracy will prevail as we head to the booths this year. Thankfully, as the lucky country, whoever wins, we’ll... probably be fine.

What, you ask, does any of this have to do with MPA? A clunky analogy it may be, but it brings us to the theme of our first edition of the year.

Like our esteemed political class, customer-owned banks must balance their fundamental business needs with the demands of their members

Customer-owned banks are the democratic institutions of the finance space. They are duty-bound to the priorities of their many thousands of customers, all of whom have skin in the game. Like our esteemed political class, customer-owned banks must balance their fundamental business needs with the demands of their members. Often, these dual mandates overlap, but not always.

Customer-owned banks must also fight for a competitive edge in the Aussie mortgage market, even at a time when long-overdue interest rate cuts are expected to drive up dealmaking activity as 2025 kicks up a notch.

This month’s MPA roundtable brought together Australia’s leading customer-owned banks to discuss these issues and the critical role brokers play.

Democracy also manifested itself in our latest Brokers on Banks survey, which steered one banking giant to its fourth gold medal in as many years. MPA caught up with Macquarie Bank’s head of broker sales, Wendy Brown, to hear the bank’s secret recipe for broker success.

True, democracy is the worst form of government, except for all the others, as Churchill famously said. Nonetheless, these awards are voted on by the brokers, for the brokers. It’s a laudable accomplishment.

William Farrington, editor, MPA

8437 4786 NZ ADVISER alex.knowles@keymedia.com T +64 9 200 1319

CANADIAN MORTGAGE PROFESSIONAL chris.anderson@keymedia.com

T +1 720-441-2255

MORTGAGE PROFESSIONAL AMERICA chris.anderson@keymedia.com

T +1 720-441-2255

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com T +44 203 868 3406

STATISTICS

RENTAL MARKET GROWTH SLOWS

$11.1trn

Combined value of residential real estate in December 2024

In the fourth quarter of 2024, national rents rose by 0.4%, capping o a year in which rents increased 4.8% – the smallest annual rise since early 2021, CoreLogic reports. This slowdown indicates that the peak of the recent rental boom has passed, as evidenced by the modest quarterly lift. A significant 26.3% surge in investor lending over the year also contributed to higher vacancy rates.

0.1%

33

Median days on the market over the three months to December

26,423

Number of new properties listed nationally over the 28 days to 22 December

Percentage decline in national home values over the December quarter Source: CoreLogic Monthly Housing

HOUSING TARGET SHORTFALL EMERGES

Australia is falling short of its housing targets, with a deficit of over 15,000 homes just three months into the 1.2 million home target set for 2029, ABS data shows. Only 44,884 homes were built in the September quarter against a quarterly need of 60,000. The NT shows the largest shortfall, achieving 78.6% fewer homes than its target.

AUSTRALIA'S HOUSING TARGETS VS COMPLETIONS

KEY STATS AS OF DECEMBER 2024

HOME APPROVAL TRENDS BY

STATE

In November 2024, dwelling approvals in WA and Qld rose by 18.1% and 7.3% respectively, while Vic, NSW, Tas and SA saw drops of 12.9%, 9.9%, 4.2% and 1.6%. Private house approvals fell in most states, except for a 4.3% rise in Qld, ABS data shows.

TOP SUBURBS DEFY MARKET TRENDS

In the past year, 10 Australian suburbs saw home prices surge by at least 40%, with Ardross in Perth leading at a 49.3% increase. This growth, according to Domain, defies the broader market slowdown and is concentrated in Qld and WA.

HIGHEST PROPERTY LISTINGS SINCE 2021

In 2024, new listings rose 7.9% year-on-year, marking the highest number since 2021 and, before that, since 2017, PropTrack reports. December saw a typical 50.6% seasonal drop in listings. Despite a month-on-month decrease of 11.9% in December, listings were up 5.7% overall.

The pivotal role of loyalty programs

Loyalty programs drive motivation and make customers and brokers feel appreciated, says

CommBank’s Baber Zaka

IN THE dynamic landscape of 2025, loyalty programs have evolved to become indispensable tools for businesses aiming to foster customer retention and satisfaction.

As the loyalty program market grows increasingly competitive, the importance of these programs cannot be overlooked. They help foster stronger relationships between companies and their customers, o ering loyal customers tangible rewards.

The evolution of loyalty programs has been rapid – from simple punch cards o ering a free co ee after your 10th purchase to sophisticated, data-driven systems that provide personalised rewards. Today’s programs leverage advanced technologies, including artificial intelligence and data analytics, to understand customer preferences and behaviours better. Businesses can tailor their o erings, ensuring the rewards are both relevant and appealing.

One of the most significant benefits of loyalty programs is their ability to enhance customer retention. Loyalty programs create a sense of commitment, encouraging customers to remain with a brand in exchange for rewards. This loyalty is not just about repeat purchases; it extends to brand advocacy, where satisfied customers become ambassadors, spreading positive word of mouth and attracting new clientele.

Loyalty programs also provide valuable insights into customer behaviour. By analysing data from these programs, businesses can identify trends, preferences and pain points. This information is crucial for refining marketing strategies, improving products and services and creating more e ective customer-engagement methods. In 2025, the integration of digital wallets

and mobile apps into loyalty programs has become standard. Customers can now access their rewards, track their points and receive personalised o ers directly on their smartphones. This enhances the customer experience, making it easier for them to interact with the brand and redeem their rewards.

Additionally, the gamification of loyalty programs has gained popularity, adding an element of fun and competition that encourages continuous engagement.

These incentives not only acknowledge brokers’ contributions but also encourage them to continue their e orts to secure new clients and maintain high service standards.

Loyalty programs for mortgage brokers can be integrated with advanced data analytics to tailor rewards based on individual broker quality and performance metrics. For example, brokers who consistently meet or exceed their quality targets could receive tiered rewards that grow progressively more valuable. This personalised approach ensures the most loyal and e ective brokers feel appreciated and motivated to maintain their high performance.

On the customer front, loyalty programs are immensely beneficial as they provide personalised rewards that cater to individual preferences and behaviours, enhancing the overall shopping experience. For example, CommBank customers who make more than five eligible transactions a month can gain access to the CommBank Yello program, which includes discounts, cashback and o ers. This program is designed to recognise active customers and

Banks can e ectively leverage tailored loyalty programs to foster stronger relationships and drive high performance among brokers

Looking specifically at the financial sector, loyalty programs have become a crucial component of customer-engagement strategies. At Commonwealth Bank, we’ve introduced our own recognition program that seeks to benefit our customers, as well as a new tiering system to support our brokers.

And we’re certainly not the only ones operating in this space. Banks can e ectively leverage broker-tailored loyalty programs to foster stronger relationships and drive high performance. By designing specialised reward systems that recognise and incentivise highquality brokers, banks can continue to work collaboratively with these professionals to help them achieve even greater success and deliver excellent customer outcomes. Rewards can include premium support; access to exclusive training programs; and enhanced support services such as credit o cers and coaches.

help them save on everyday purchases with personalised benefits.

The importance of loyalty programs for customers in 2025 is undeniable. These programs o er personalised rewards, enhance customer retention, provide valuable data insights, integrate seamlessly with digital platforms, promote sustainability, and significantly impact customer engagement, particularly in the financial sector.

As businesses continue to innovate and refine their loyalty strategies, these will undoubtedly play a pivotal role in shaping the future of customer relationships.

WILLIAM LOCKETT: BECOMING BIGGER, BETTER, STRONGER

Specialist Finance Group continues to be a dominant force in mortgage aggregation. For managing director William Lockett, it’s all about maintaining strong relationships, understanding members’ interests and loving the job

IT’S NEARLY impossible to interview William Lockett, managing director at mortgage aggregator Specialist Finance Group, without commenting on his insatiable travel bug. This time, it’s no different.

Lockett spent the better part of January diligently updating his thousands of LinkedIn followers on his various Melbourne adventures, from early-morning jogs along the Yarra to taking in the Australian Open buzz. If you don’t follow Lockett on the socials, do yourself a favour!

But there was more than tennis and flat whites on Lockett’s agenda at the Open – he was there to meet as many SFG team members, broker members and business partners as he could cram into a few short weeks.

This speaks to his hands-on leadership style: he’s always on the move, actively engaging with the industry rather than staying behind a desk.

In Lockett’s words, his leadership style is, “Be present, engaged and constantly driving growth and innovation”.

Lockett is a people person who believes strong relationships are the foundation of building a successful business. It’s no surprise that he secured his fourth appearance on MPA’s Mortgage Global 100 list in 2024.

Love what you do

The key to recognition, says Lockett, is loving what you do. “And I’ve been loving what I do for over 34 years. Over that period of time, I’d like to think that I and our business model have gained business credibility and trust.”

It certainly helps that Lockett and SFG are heavily involved in advocacy matters in the

Payroll Tax Act 2007 underway, there is a glimmer of hope on the horizon.

A matter of pride

“I have a saying that ‘good compliance is good business’,” says Lockett. “The reality is, we operate in the financial services sector, so the more compliant we can be, the better off we are.”

“I’ve been loving what I do for over 34 years. Over that period of time, I’d like to think that I and our business model have gained business credibility and trust”

mortgage industry, which has naturally led to high visibility and respect among their peers.

Lockett came out swinging against the hugely controversial payroll tax matter that has emerged from Revenue NSW in recent years. The issue, which relates to state levies applied to commissions paid by aggregators to brokers, “is very concerning for our industry”, he says, “given the fact that we’ve been operating for 34 years, and it’s now just become an issue”.

It’s been “probably the most challenging thing in the last 12 months”, says Lockett, although with a parliamentary review of the

He maintains that the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was “a big wake-up moment for our industry”, and while it may have resulted in a degree of regulatory overreach, in some respects “it probably needed to”.

“Since the royal commission, our industry has got bigger, better, stronger, and it’s more professional today than it’s ever been. Our industry should be proud of how we’ve dealt with it and all the compliances that have come post the royal commission.”

PROFILE

Name: William Lockett

Title: Managing director

Company: Specialist Finance Group (SFG)

Years in the industry: 34

Highlights of 2024:

• Industry-leading SFG National Conference and Awards in Victoria

• Opening of SFG Queensland office

• Record settlement volumes

BIG INTERVIEW

Lockett highlights that complaints against mortgage brokers have hit record lows since the royal commission. “It should be something that we are very, very proud of. The compliance is certainly working, and we’re heading in the right direction, and we should all be very proud.”

He emphasises that true success in challenging times is impossible to achieve in isolation. “You need to listen, and you need to collaborate with people, because it’s a team thing … Having that maturity in dealing with people teaches you to deal with things better.

“You’re always evolving. One of the great things that we do is we maintain very, very clear and precise communications with people. You treat people with good respect and dignity, and you create empathy. So I suppose

from them about what they need to grow their business model.

“Everyone’s di erent. Some people just want to be a one- or two-man band. Some people want to be five or six. Some don’t want to grow any more, whereas some people want to open the gates, and they want to grow from an expeditious point of view.”

No two business models for SFG members are the same, Lockett adds, “and we accommodate our service model with that”.

“We think the engagement side keeps us on track not only with our growth but also, more importantly, our members’ growth.”

While every relationship, business or personal, has its highs and lows, Lockett believes it’s the tough moments that truly test the strength of the bonds we build.

“Our goal is to be a better aggregator today than we were yesterday. It is also to look forward and plan, invest and innovate so that we are also a better aggregator in the future”

if you combine all of those things, it doesn’t always work, but it gives you a great opportunity to be able to lead in the best way possible.”

Through thick and thin

Lockett’s people-first approach to business has been an invaluable tool in the aggregation space, where fostering relationships with finance brokers on one side and lenders on the other is critical.

“We don’t try to be too big. We have very much a relationship-based approach with all our SFG members, and we have great engagement,” he says.

Lockett explains that engagement with SFG’s members can be both micro and macro in nature, from large-scale, national conferences to more intimate, one-on-one business strategy sessions.

“Because our engagement with our members is a high-touch model, we get a lot of feedback

“Not every day is a sunny day – there are often cloudy days, and there are often stormy days. Keeping your true north on those cloudy days and stormy days is vital. If anything, that is the glue that sticks relationships together.”

Keep mortgage aggregation great

Discussing what comes next, Lockett says: “You can always run o a list. I have been there before and done that, but our goal is to be a better aggregator today than we were yesterday. It is also to look forward and plan, invest and innovate so that we are also a better aggregator in the future.

“We’re always looking for rooms to improve, but we’re looking for ways to improve that we know that we’re capable of doing, and we’re not trying to be something we are not or going outside our realistic zone. It’s knowing where our strengths are and knowing where we can

SFG ACHIEVEMENTS, KEY PLANS FOR 2025

Scaling up SFG’s national footprint and broker resources

Financially supporting SFG members’ growth

go by underpromising and overdelivering.

“So it’s quite simple – we just want to be the best aggregator possible. We strive for that on a daily basis.”

The twists and turns that the industry takes you on are all part of the journey, says Lockett. And for the industry as a whole? “If we all stick together, and if we all make our industry great – which it is – then we should all be proud of what we do.”

Home loans that tick all the right boxes for essential workers

We serve education, emergency services and health workers nationally in all Australian states and territories.

We’re one of a small number of banks participating in the Home Guarantee Scheme to help essential workers’ own their home sooner.

First home buyers annual fees are waived for the life of the loan with the Your Way Plus Home loan package.

Home loan fee waiver, making it easier to do business. Establishment fee waived until 30 June 2025. Saving your clients $600!*

Unlock benefits to thousands of essential workers in niche industry sectors. Become an accredited Teachers Mutual Bank Limited broker today to access four customer-owned industry banking divisions.

To find out more or to become accredited contact broker@tmbl.com.au or 1300 86 22 65

ON BANKS BROKERS ON BANKS 2025

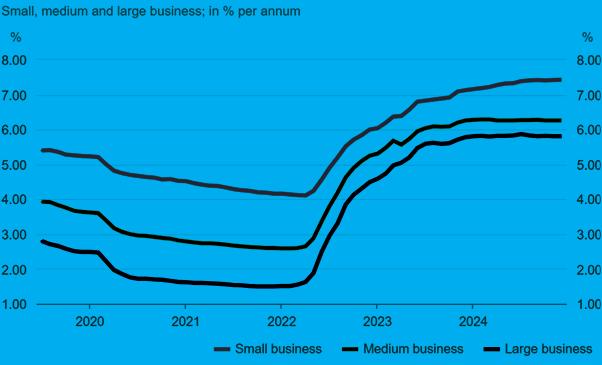

As broker-driven lending reaches new heights, the best banks are delivering what matters most: better credit policy, faster approvals and stronger BDM support

THE RECORD-HIGH market share of Australia’s brokers reinforces their meaningful role in home lending, while also raising expectations for banks to enhance their services and o erings.

To sustain broker partnerships and tap into the burgeoning broker-driven market – which hit 74.6%, according to the MFAA’s September 2024 quarter data, reflecting a 3.1% increase from the same period in 2023 – leading lenders have prioritised operational and service excellence as well as digital innovation.

In MPA’s Brokers on Banks 2025 survey, brokers rated lenders they’ve worked with over the past year across 10 tried-and-true benchmarks. Over 250 respondents also shared their top product picks, tech improvements and the practices that set award-winning banks apart.

More importantly, the top-ranked mainstream lenders are listening and adapting to brokers’ evolving priorities.

This year’s data indicates a clear shift:

• Credit policy ranked first in 2025 with a 4.705 out of 5 rating, up from fifth last year, reflecting the need for clear, flexible, broker-friendly policies

• BDM support rose to second place (from fourth) as brokers sought more accessible, proactive support

• Turnaround times climbed to third place (previously sixth), pointing to demand for faster approvals

• Interest rates dropped to fourth place (from first), though competitiveness remains key (4.554 rating vs 4.214 in 2024)

• Online platform & services moved up to fifth place (from seventh), pointing to brokers’ need for seamless digital tools

For brokers, consistency and credit coach support now outweigh interest rates alone, particularly as lending

conditions tighten. The ability to have real-time access to credit decision-makers is invaluable.

“This is where banks with credit coaches stand out,” explains Indigo Finance managing director Melanie Cunli e. “Even a 15-minute conversation can help brokers structure an application e ectively. Sometimes, if a lender has a slightly higher interest rate, we’ll still prefer them if we know they’ll o er a smooth, reliable approval process rather than a submit-it-and-see approach.”

Specialist Finance Group general manager Blake Buchanan adds that lenders who deliver a high level of consistent service over time are the ones that earn brokers’ loyalty.

This year’s findings confirm that brokers value banks that prioritise clarity, responsiveness and relationship-driven support, key factors that ultimately influence where they choose to place business.

TYPICAL RESPONDENT

Writes $10m–$20m worth of mortgages each year

Aged between 46 and 55 Is most likely to live in NSW Has been in the industry for > 15 years

Years as a broker What do brokers want from banks?

BROKERS ON BANKS PRODUCTS AND PRICING

As interest rates fluctuate and lending bu ers tighten, bank credit policies have surged to become brokers’ top priority, with flexibility outranking product range

BROKERS ELEVATED credit policy to their top priority, and lenders that o er flexible, broker-friendly policies have gained a competitive advantage.

Bankwest continued its winning streak for credit policy. It nabbed first place for diversification opportunities and third for product range. Brokers also praised the bank’s ability to support a variety of clients with di erent needs: “They have an excellent credit policy for self-employed people, and credit sta want to do deals,” said one respondent.

Brokers rewarded Macquarie Bank’s

continuous policy improvements with a second-place finish, up from third last year.

As the only big four bank to lay claim to five categories, CommBank placed third for credit policy; communications, training and development; as well as online platform and services. It took second place for product range and diversification opportunities.

For aggregator SFG’s Blake Buchanan, the top-performing lenders take di erent paths regarding policy. “They might have a policy that they apply exceptionally well and want to be known for, such as SMSF,” he explains.

“These lenders understand that they cannot be all things to all people.”

Interest rates dropped o the top spot to fourth on the priorities list, yet they remained no less important than in 2024 (jumping from 4.214 out of 5 to 4.554) as rates remain high and lending bu ers tighten. Even as optimism abounds around anticipated rate cuts in early 2025, brokers have devoted time to clients’ stress levels. One said: “We are busier than ever as people turn their attention to making sure they are on the most suitable product/lender to conserve money”.

2025 HIGHLIGHTS: PRODUCTS AND PRICING

HAVE PRODUCT RANGES AND PRICING

ING emerged as the top performer for interest rates, earning broker praise for its proactive approach to pricing, and competitive products, while Macquarie Bank came in a close second. Bendigo and Adelaide Bank took third, with brokers citing its competitive fixed rates and white label o ering as valuable.

While MPA’s data suggests brokers generally see an improvement or stabilisation in product range over last year, the higher percentage of respondents reporting ‘no di erence’ to their sixth-place priority may indicate they are sensing less change in lenders’ o erings.

Buchanan notes that having a broad product range is essential. Still, he has observed that, ironically, lenders that take a wide-net approach to capture more market share often fall short of their goals.

“As an industry, most, if not all, categories are covered by various lenders, and most lenders are playing to their strengths,” he remarks. “I think brokers are right to place less importance on product range, primarily because they understand that lenders often fail in service, product quality or other aspects when they try to be all things to all people.”

For the fourth consecutive year, Macquarie Bank came out swinging, earning first place overall in 2025, picking up a 0.08% edge in broker satisfaction over the previous year.

The lender clinched the top spot in turnaround times again this year and saw first-place gains in product range, online platform and services, and brand trust. It also won a topthree spot for outstanding performance in

WHICH IS YOUR PREFERRED BANK?

every survey category, including second for BDM support; commission structure; communications, training and development; credit policy; and interest rates. It tied with Westpac for third place in diversification opportunities.

Brokers’ praise for Macquarie Bank included:

• “Service and rates are great; BDM is fantastic”

• “Interest rates, credit policy, and a process that’s easy for clients and brokers” .

BROKERS ON BANKS

BROKER SUPPORT

Communication and consistency take the lead over brand trust as lenders win broker loyalty with expert guidance

UNSURPRISINGLY, brokers’ preferences and priorities shift from year to year as they adapt to forces that put pressure on the economy and market environment.

In 2025, brand trust dropped dramatically, moving from a solid second place last year, trumped only by interest rates, to the seventh spot, with a corresponding decline in importance among brokers. This swing suggests that brokers are now placing less emphasis on lenders’ market positions and more on practical factors that positively impact their

clients, such as flexible credit policies and competitive rates.

This evolving priority points to a more client-focused approach in a rapidly changing market, as noted by one broker: “Generally, a lender recommendation comes down to who is o ering the lowest rate or su cient borrowing capacity to achieve the objective”.

Macquarie Bank rose to first place from third last year for brand trust, knocking Bankwest o its former top spot to third place. ING held second place for two years running.

Brokers appreciate a bank’s flexibility, strong support, e cient processes and good service, as evidenced by these comments on how the lending leaders in the broker support category are standing out:

• “Macquarie has brand awareness, and its speed to a decision is impressive”

• “ING o ers more competitive pricing, quick approvals and loan doc issuance”

• “Bankwest is easy to deal with”

• “CBA delivers consistency and support”

2025 HIGHLIGHTS: BACKING BROKERS

HAVE YOU GIVEN MORE BUSINESS TO A PARTICULAR BANK IN THE LAST 12 MONTHS, AND IF SO, WHY?

“ANZ because my clients have been mainly self-employed, and their one-year financial policy has been the standout”

“Macquarie, due to their process and customer experience. Their turnaround times are best in market, and clients often want a quick decision, over and above rate (most times)”

“Suncorp due to the package fee being waived and decent pricing discounts”

“NAB because of fast turnaround time and you can talk to assessors directly, which is important so we can o er fast solutions to customers”

“Westpac due to competitive pricing, Bankwest as they help with large investment portfolios, and Ubank because our BDM goes the extra mile every time”

“Macquarie due to their competitive pricing; clients are choosing them over other lenders. Their package fee is also cheaper than most lenders’, which, coupled with their competitive rates, means they are capturing more of the market”

For the fourth consecutive year, Bankwest held its first-place position for commission structure, while Macquarie Bank climbed to second place from third last year, and ANZ claimed third place, up from second position in 2024.

Bankwest climbed to the top spot for communications, training and development, after taking second place over the past two years. After claiming the top position last year, Macquarie Bank clocked a close second place, and CommBank hung on to third.

Brokers noted that they gave more business to Bankwest, Macquarie and CommBank for their flexible credit policies, competitive

YES NO

“No, I try to spread the love, but sometimes you have a run on lenders”

“70% of my business would be policy driven. ANZ has an FHB rebate, so they have some business from me there. Macquarie are a favourite”

“Generally, I’m looking for the path of least resistance, then rates and fees”

“It depends on the type of lending being done as it changes from month to month”

“Not intentionally. If I have stopped using a bank it’s due to their inability to compete with other lenders”

“First home buyer demand has increased, especially due to the unpredictability of rate variations and the shortage of supply, which has led to house prices becoming increasingly una ordable, complicating the process regardless of the bank’s o erings”

rates, quick turnaround times and strong BDM support.

Macquarie Bank is especially noted for its fast decision-making and ease of process, while brokers praised Bankwest for its selfemployed client support and flexibility. CommBank stood out for its policy flexibility and serviceability.

“Consistency is key here,” SFG’s Blake Buchanan explains. “Historical data shows that lenders with a high degree of consistent service over time trump all else. Specials, pricing and periodically improved SLAs tend to have a modest impact on market share results.”

Beyond consistency, communication is a recognised strength of top-performing lenders.

“It doesn’t always need to be great news either; lenders who communicate e ectively, good, bad or indi erent, don’t leave brokers wondering, and this is important, as brokers want to provide clear communication to their clients,” Buchanan adds.

When brokers perceive their experiences with lenders as negative, they pull no punches: “I haven’t stopped using any lenders completely,” one said. “However, I have reduced my business due to channel conflict and horrible application/assessment processes.”

BROKERS ON BANKS

TECHNOLOGY, TURNAROUND TIMES AND SERVICE

Speedy service and digital tools drive broker satisfaction and create deeper lender-broker connections

AN EVOLUTION towards a more relationship-driven broker-lender dynamic is underway, evidenced by the steady four-year climb in the importance of BDMs on brokers’ priority list.

This year, BDM support moved to second place – with a rating of 4.7 out of 5 – from fourth in 2024 and sixth the year prior. This significant rise indicates that brokers are placing more value on personalised support and relationships with banks’ BDMs.

Brokers noted that they are facing an increasingly complex and competitive environment, and BDMs who o er guidance and

problem-solving skills almost guarantee a smooth deal process.

SFG’s Blake Buchanan asserts that top lenders are more than just great communicators – they are empowering their BDM teams to work more closely with internal stakeholders to enhance client service.

“Great lenders understand that this is very much a relationship-based industry that requires BDMs who are present and responsive but also able to assist their brokers as representatives of the lender,” he adds.

For the third year, Bankwest clinched first place for BDM support, Macquarie Bank

retained its second spot, and ING emerged as the third-place winner.

Turnaround times shifted position on brokers’ priority list again in 2025, jumping to third place from sixth last year. This improvement suggests that speed is becoming an even more critical factor for brokers as they focus on providing clients with fast and e cient service, with speed to decision a di erentiator among the top lenders.

Brokers’ experience of turnaround times remains primarily positive, with this year showing an improvement in the overall perception of lenders’ performance in this

area. Fewer brokers reported worsening times, and those reporting ‘no di erence’ saw a noticeable jump to 33% from 20% last year.

The biggest factor pushing lenders into the winners’ circle is transparency, notes Indigo Finance’s Melanie Cunli e. Uncertainty makes it di cult to manage client expectations and adds work for broker teams on constant follow-ups. “If a lender has a five-day turnaround, that’s fine, as long as we know up front,” she says. “The challenge is when an SLA is listed as three or four days, but after submission it blows out unpredictably.”

Buchanan mentions that turnaround times have dominated lender discussions as they seek ways to improve submission and assessment e ciencies while enhancing the customer experience. “It’s no secret that in recent years a few standout lenders have delivered consistently impressive turnaround times for brokers,” he says. “These lenders have gained meaningful market share, and other lenders are looking to replicate or even improve on this to gain more share and the confidence of brokers when submitting loans on behalf of their clients.”

Macquarie Bank led the pack in this category, followed by ING, which climbed to second place from a tie for third last year, and Bankwest slipped to third from second.

Online platforms also moved to fifth on brokers’ priority list from seventh in 2024, with brokers consistently citing the value of digital tools and platform e ciency to

streamline workflows and better serve clients.

Cunli e notes that some lenders’ live chat support has been a major improvement and time-saver. “Another innovation is in postsettlement support,” she explains. “Some top banks have built portals that allow brokers to easily access client information post-settle-

ment. This helps immensely when conducting loan reviews, making the bank feel like a long-term partner rather than just a lender.”

Macquarie Bank knocked digital bank ING out of first place for its online platform and services, Bankwest cracked the second spot, and CommBank nailed a close third.

IS THERE A PARTICULAR TECHNOLOGICAL IMPROVEMENT THAT HAS IMPROVED TURNAROUND TIMES?

“Electronic/online identity verification and electronic signing of applications and loan documents (including mortgages) has made a huge di erence”

“Quickli has improved my personal turnaround times in assisting my clients, and I’m using SalesTrekker to lodge my applications seamlessly with AOL NextGen”

“It seems like lenders have updated their systems to improve the e ciency for credit assessment. I think the move away from needing to provide everyday banking accounts in a loan application has probably sped up the assessment process as much, if not more, than technological improvements”

YES NO

“I believe less volume of applications has helped with time frames”

“We are doing more, and the banks are o ering zero training. If we have an issue, we need to solve it ourselves”

“I have a deal in the system right now which they should have looked at on Monday, but I do not have an AIP as yet, and it is Wednesday today”

HAVE TURNAROUND TIMES IMPROVED OR WORSENED OVER THE LAST YEAR?

BROKERS ON BANKS

WHAT YOU’RE SAYING

2025 proved brokers’ ability to bounce back from a relentless and demanding lending market. Here’s what brokers had to say

THE DECLINE in inflation to 3.2% in December, along with the expected cut to the cash rate in early 2025, helped ease concerns among brokers about the impact on their businesses and clients’ financial wellbeing. But as more brokers face challenges with deals that fall outside the norm, lenders that instil confidence and show reliability capture a bigger share of the expanding third party channel.

Brokers are optimistic about the opportunities ahead:

• “Rates will eventually start to come down, which will relieve some pressure on

PRIZE QUESTION

mortgage owners and may increase capacity moving forward for new clients”

• “We’ve weathered the worst of the storm, and I’m still helping first-time buyers get into the property market, refinancing and bringing aboard new clients”

Channel conflict is still a major issue, but brokers’ views have shifted over the past year. Slightly more brokers now see it as a major problem, rising from 34% to 35%. Meanwhile, fewer brokers now see it as a minor issue (39% vs 45% in 2024), and 5% more brokers this year believe it’s not a problem at all,

highlighting a growing divide in perspectives. One broker, showing frustration at feeling their value was undermined, said, “I had to deal with a BDM when I stopped getting trail for one of my clients. It turned out they went into a branch for a small increase, and instead of referring them back to me, the branch processed the increase.”

Brokers are increasingly seeking strong, transparent relationships with lenders that can o er consistent support, clear communication and the flexibility to meet their clients’ unique needs. Lenders who can deliver this will build the trust needed for them both to thrive.

Whisky Wednesday:

“I am positive about the future expectation on interest rates and on business for the next two to three years. This is on the back of expecting the interest rates will be lower at least by mid-2025 that would usher in an era of more demand for homes, both owner-occupier and investor”

5 x VISA gift cards:

• “Not overly concerned. It seems like a matter of when, not if, the RBA starts cutting rates. I think 2025 o ers great opportunity for brokers. Rate cuts will further stimulate competition in the refinance space and bring more buyers into the market. I am confident my loan volumes will increase in 2025 compared to 2024”

•“The main impact that we anticipate to our business is lender price wars and cash rebates (refi rebate), which has significant clawback potential and is not ideal for the broker channel”

• “I am not worried. I’ve been in the finance industry for over 40 years; people adapt to their environment, and interest rates play only a small part in that environment”

• “Rates go up and rates go down. I am happy navigating any landscape we come across with my clients”

• “I’m happier now that fixed rates are beginning to reduce and that we have some stability in the market. If they come down, even better”

How worried are you about the present rate environment, and what impact do you expect it to have on your business?

HOW HAVE YOU FOUND BANKS’ ASSESSMENT OF LIVING EXPENSES OVER THE PAST 12 MONTHS?

“Assessment of expenses is fair, and the process of verifying has improved over the past 12 months”

“Living expenses are reasonable, as per each lender’s benchmark. Generally, the client is happy to use their actual living expenses”

“They have seemed to streamline a lot of the expenses into general living expenses instead of on top of HEM”

“No issues. Lenders are accepting declared living expenses if they are above HEM”

“Some lenders now categorise things like childcare, private health and strata fees under basic living expenses, which has been a good thing”

“HEM has increased disproportionate to actual spending. This is a bigger punishment for first-time buyers than interest rate increases”

“A nightmare. HEM, in principle, is sound, but in some instances, it’s nonsensical when a client’s salary increases into the ‘next band’”

“Overreaching and, in many cases, unrealistic”

“Increased, and more parameters put in place, making it harder to make exceptions”

“Somewhat harsher, as some banks have a benchmark for certain living expenses. And if that benchmark is not met, they will query an expense”

“The intense focus on living expenses has eased for the majority of lenders, making the process more manageable”

“Lenders have increased their benchmark, but this hasn’t really a ected how I operate, as I ensure I review clients’ living expenses to ensure we aren’t underquoting them”

HOW COULD LENDERS IMPROVE SUSTAINABLE/GREEN LOAN OPTIONS?

“Provide cashback incentives. Make it a simpler process. Every bank should have the green options available for brokers to write”

“Clients are not interested. There’s not a huge demand, and I’m not sure if they need a specific product”

“Make simple eligibility criteria. Currently, there are too many eligibility requirements imposed by lenders o ering such products that the majority of clients we deal with are not able to meet”

“I think they have come a long way and are in a great place as is”

“The green loans business is a farce. Improve on providing competitive interest rates and actually working with brokers and broker-initiated customers for a healthy long-term relationship, rather than encouraging churn”

DO YOU BELIEVE CHANNEL CONFLICT EXISTS?

HAVE YOU STOPPED USING A BANK IN THE LAST 12 MONTHS AND, IF SO, WHY?

“Lack of common-sense assessors”

“Not stop, but only use them as last resort”

“Yes, because of lack of BDM support, di culty in dealing with credit assessment, such as lack of credit assessors reading my detailed notes, raising unnecessary MIR requests. Some like to raise MIRs rather than approve files”

“Major banks because of higher interest rates as compared to second-tier lenders”

“There are several banks that I resist using as they are not supportive of brokers, in my opinion”

“Ubank because its technology only makes the process harder, and AMP Bank due to uncompetitive pricing currently”

“Heritage Bank’s assessment is just too hard. My clients pull the pin due to the onerous and continuous list of questions”

BROKERS ON BANKS

FINAL RESULTS

MPA presents the overall winners of the 2025 Brokers on Banks survey, spotlighting the areas in which these banks outperformed and why brokers preferred them over their competitors

MACQUARIE BANK

Position in 2024: 1st Position in 2023: 1st

For Macquarie Bank, four times is the charm as brokers thrust the significant player in the country’s investment banking and financial services industry into the top spot.

With an overall broker satisfaction rating of 3.93 out of 5, the leading lender is highly regarded for its innovation, unfailing service and support, and product range.

Across 10 categories evaluated by brokers, Macquarie Bank earned an impressive medal haul of four golds, five silvers and one bronze, significantly outperforming last year’s results.

The lender dominated in turnaround times for the fifth year. It also made a comeback and secured the crown for product range, online platform and services, and brand trust, making notable gains in each area. Brokers lauded the bank’s broker platform as “amazing” and noted it significantly contributed to streamlining the application process through to settlement. “They are by far the leaders here,” a broker commented.

The bank also picked up silvers for interest rates, credit policy, BDM support, commissions, and communication, training and development. It tied for bronze in the diversification category.

Macquarie Bank’s O set Home Loan Package was brokers’ top product pick for the second consecutive year. The bank was also brokers’ overwhelming favourite for property investors. Its strong standing among brokers is reinforced by its consistent performance, ranking in the top three across every key metric and outshining challengers with its commitment to the broker channel.

Macquarie Bank shines for its innovation, top-tier service and speed to decision, earning multiple golds and silvers while maintaining a dominant presence in the broker community

To generate the overall survey results, MPA took an average of the results across each category. Each category had an equal weighting in the final result.

Choose a better banking experience for your clients

Partnering with WA brokers to give Aussies greater choice when it comes to finding the right home loan.

Why partner with P&N Bank?

We listen. Efficient, smoother loan processing - thanks to your feedback.

Competitive rates for the life of your client’s loan.

Direct access to Broker Assessors from start to settlement.

BROKERS ON BANKS

Position in 2024: 2nd

Position in 2023: 2nd

Bankwest fought hard, nearly closing the gap to the top spot with just a slim margin of 0.193 points and securing a solid second-place finish.

The leading retail bank rivalled the first-place winner’s gold medal haul, taking top nods for credit policy, BDM support, communications, training and development, diversification opportunities, and commissions, for which it has been the undisputed champ for six years running.

Its triumph in policy and BDM support, categories defining the broker-lender relationship in a challenging and competitive environment, cements its commitment to building strong partnerships with brokers and delivering exceptional service.

Bankwest also claimed silver for its online platforms and services and bronze for turnaround times, product range and brand trust.

The Perth bank retained its second-place status as brokers’ preferred bank for property investors, while placing third for foreign non-residents. It slipped to sixth place from third last year as the favourite for first home buyers.

4th

BANKWEST ING

Position in 2024: 5th

Position in 2023: 6th

Digital bank ING has been on an upward trajectory in Brokers on Banks, advancing from sixth place into the top three leading banks within the past three years alone. A slim margin of 0.092 separated the formidable contender from second place, which, given its strong performance this year across four influential categories, could see its star continue to rise.

ING soared to the top spot for interest rates, earned silver for turnaround times and bronze for BDM support, while retaining silver for brand trust. The lender cracked brokers’ top product pick for its Orange Advantage product, lauded for its competitive interest rate, o set account, and fast turnaround times.

Brokers praised the breakout performer for its proactive approach to o ering competitive rates, products and loan deals amid a rising rate environment. Its e cient, client-focused application process enabled it to stand out from competitors, setting the stage for a new wave of competition among Australia’s legacy banks and emerging players.

COMMBANK WESTPAC

Position in 2024: 4th

Position

in 2023: 3rd

CommBank held steady at fourth place overall again this year, while bulking up its medal haul to win places in half of the 10 survey categories. The big four bank placed in three of four client niches as brokers’ preferred lender for first home buyers, foreign non-residents (second place) and property investors (third). It earned silver and bronze, respectively, for diversification opportunities and credit policy, and broke into the product range category, taking home a silver.

CommBank received an accolade as brokers’ top product pick for its MAV Package, which was cited as a solid product that makes loans simple, with quick turnaround times and excellent BDM support. And for its online platform and services, the bank’s bronze medal win is a testament to its enhancements despite underperforming in past years. Just 0.01% separated it from its silver-medal-winning sibling.

5th

Position in 2024: 11th

Position in 2023: 11th

As one of Australia’s oldest major banks, Westpac has made significant gains, ranking fifth overall in Brokers on Banks 2025. It placed 11th last year and has impressed brokers by elevating its performance across all evaluated metrics.

Westpac tied for bronze with top lender Macquarie Bank for diversification opportunities. Brokers also named it their preferred bank across three client types, with a first-place nod for foreign non-residents and third for commercial and first home buyers.

Many brokers said Westpac was a leader in providing the best loan deals, o ering “great rates, which are a win for clients”. Brokers have also given the bank more business in the past year for various reasons, including bridging loans to new clients, low variable rates and branch access, and the 1% servicing bu er for refinances.

BROKERS’ PICKS

As well as ranking the banks in 10 categories, brokers were asked to name their favourite mortgage products of the last 12 months. Here are the top three

MACQUARIE BANK

Offset Home Loan Package

Macquarie Bank and its ever-popular O set Home Loan Package retained the top spot in 2025 after seesawing in brokers’ top three since 2022.

Brokers emphasised the product’s flexibility, competitive pricing (though not necessarily the cheapest) and e cient service.

Its key strengths include multiple o shore accounts, quick turnaround times, simplicity, ease of use and low annual fees.

Other respondents appreciated “strong technology support” and “excellent BDM assistance”. Brokers highlighted the product’s comprehensive coverage, making it a solid choice for most client needs.

COMMBANK ING

MAV Package

CommBank’s MAV Package emerged in second place this year, garnering the coveted broker pick for the product’s simplicity, quick turnaround times and excellent BDM support.

Brokers praised the product’s flexibility in pricing and policy, including options for the home guarantee scheme and modular homes.

The MAV Package is known for its solid valuation process and strong policy, especially in areas such as negative gearing. It is considered particularly suitable for individual borrowers and company/trust ownership, with a smoother process than other lenders.

Orange Advantage

ING’s Orange Advantage product burst onto brokers’ list of top product picks this year in third place. The product stands out for being a well-rounded o ering for borrowers looking for competitive pricing, flexibility and simplicity.

Brokers praised it for its low rates, lower annual fees and the ability to reprice the home loan for retention.

An excellent interest rate with the added benefit of an o set account makes it competitive relative to other such products on the market.

“It meets clients’ requirements with good rates for principal and interest owner-occupied loans,” a broker commented. Another said, “It’s flexible, with fee-free credit card options, further enhancing its appeal.”

FOUR YEARS AND COUNTING AS BROKER BANK OF CHOICE

Macquarie Bank’s winning streak continues after clinching yet another No. 1 spot in the 2025 Brokers on Banks survey. MPA chats to head of broker sales

Wendy Brown to find out why

GOOD THINGS might come in threes, but when it comes to industry recognition, surely four is better. At least that’s how Wendy Brown, head of broker sales at Macquarie Bank, must be feeling.

Macquarie Bank clinched the number one spot in MPA’s Brokers on Banks survey for the fourth time running in 2025, an achievement that Brown calls “a great testament to the work our teams are doing ... this win is a vote of confidence for our whole team and especially resonates as it’s voted for by brokers”.

As she discusses the win with MPA, it becomes clear that the relationship Brown and Macquarie Bank have with brokers is particularly strong. Though, to be honest, the data speaks for itself – while 70% of home loans originate via the third party channel sector-wide, that number is closer to 90% for Macquarie Bank.

But not content to rest on their laurels, Brown and the Macquarie Bank team have spent the last 12 months refining their ‘always on’ approach to feedback to get to the heart of what brokers need. The manifold ways the team has achieved this include upfront valuations, digital ID verification and integrated liabilities matching, all of which serve to streamline the application process and speed up approvals.

This strong emphasis on understanding

what brokers truly want resulted in Macquarie Bank not only taking home the Brokers on Banks gold but also coming out on top across four survey categories, namely brand trust, online platform and services, product range and turnaround times.

Brown says: “We’re pleased to hear that the enhancements we’ve made to the broker and customer experience, including a range of new technology and features for brokers and their support staff, are being well received.

nent of the mortgage finance supply chain.

“We truly believe that the broker industry delivers positive outcomes for customers because of the depth of knowledge that a broker brings to the home loan journey,” she says. “There’s no doubt that a strong, vibrant broker industry benefits the home loan market – from increased competition to greater accessibility for homeowners.

“For customers, this means that regardless of where or how they live, brokers can provide

“There’s no doubt that a strong, vibrant broker industry benefits the home loan market – from increased competition to greater accessibility for homeowners”

“All of these categories tie back to our partnership approach with the broker market – any updates we make are made with brokers front of mind, and we look forward to working with our broker partners in the year ahead.”

Going for brokers

Brown clearly holds the broker channel in high esteem and sees it as a critical compo-

consumers with access to a broad range of products and services that best suit their specific needs. From a Macquarie perspective, by listening to broker feedback and acting on it, we continuously improve our offerings, which ultimately provides a better experience.”

When it comes to advocating for the value of brokers, the bank likes to make its voice heard. This, notes Brown, is particularly

PROFILE

Name: Wendy Brown

Title: Head of broker sales

Company: Macquarie Bank

Years in the industry: 25

What’s the best part about winning Brokers on Banks 2025? “This win is a vote of confidence for our whole team and especially resonates as it’s voted for by brokers”

EXPERT SPOTLIGHT

prevalent in Macquarie Bank’s ‘Speak to your broker’ advertising campaigns.

The simple things, too, like staying open for business over busy holiday seasons and making continual improvements to the broker portal, go a long way in fortifying the brokerlender relationship.

Brown says, “We have a strong feedback mechanism with brokers, and this has been instrumental to how we do business at Macquarie and our ability to innovate.

“We also use a range of data insights to gain a deeper understanding of our clients and brokers, delving into their needs and

into the market exciting new functionality that allows brokers and their support sta to securely upload additional documents directly to our assessment teams.

“This now means that brokers and their teams can keep track and manage applications through to settlement with total transparency all in the one location – the Macquarie Broker Portal.”

Eye on the prize

At the centre of everything Macquarie Bank does – whether leading the pack in broker technology, listening to and acting on broker

“As we look ahead to 2025, we’ll continue to strategically identify opportunities where we see that technology can drive the biggest impact and e ciency gains for brokers and their support sta ”

wants, so that we continue to be a true partner to the channel.”

Peace of mind

Technology is great, but instilling confidence in brokers that they are sharing sensitive information in a secure environment is a critical component of maintaining trust and credibility. Brown says this has been a key area of focus in developing Macquarie Bank’s broker portal. For instance, in the past year the bank introduced a real-time live chat platform with its assessment teams, as well as secure access to the broker portal for support sta so they can safely collaborate with brokers.

But the application that Brown is most proud of is Macquarie Authenticator, a sophisticated verification mobile application designed with the safety of brokers and customers in mind.

Brown teases more innovations in the pipeline. “We’re dedicated to continuing to innovate in this space and will be launching

feedback, or delivering market-leading turnaround times – is its commitment to making the bank the best of the best in the broker channel.

Clearly, this has not gone unrecognised, given the lender’s remarkable Brokers on Banks winning streak. Is win number five on the agenda?

In Brown’s view, Macquarie Bank will simply keep doing what it does best.

“As we look ahead to 2025, we’ll continue to strategically identify opportunities where we see that technology can drive the biggest impact and e ciency gains for brokers and their support sta .

“Our North Star this year is to continue driving e ciencies for brokers and their businesses by investing in cutting-edge technology to streamline the application process and speed up approvals with one-touch files.

“I’d like to thank all of our broker partners out there for their ongoing support and the time that they provide in sharing their valuable insights with our teams.”

MACQUARIE BANK FOCUS AREAS

Leaders in technology

• New technologies and experiences are coming to Macquarie Bank’s platforms to enhance the lender’s online platform and services for brokers, their support sta and ultimately their customers

Even faster approvals

• This year will see further investment in cutting-edge technology to streamline the application process and speed up approvals with one-touch les

Listening to feedback

• Macquarie Bank communicates with brokers regularly, listening to broker feedback and acting on it to continuously improve the bank’s o ering and provide a better experience

EXPERT SPOTLIGHT

BUILT FOR BROKERS, BACKED BY BROKERS

Non-bank lender ORDE Financial had a crystal-clear vision from the outset, built on substantial industry knowledge and experience. MPA caught up with founders

Paul

Wells and Ryan

Harkness

to look back on five years of hard graft

ORDE FINANCIAL is celebrating five years in the business. It’s hard to believe that in such a short space of time the non-bank lender has emerged as the powerhouse that it is.

Since launching in late 2020, ORDE has settled more than $6 billion in mortgages across Australia, helped over 10,000 Australian borrowers and grown to 150 team members across the country.

Managing directors Paul Wells and Ryan Harkness, chief executive and chief lending officer respectively, lead the business together and had a clear vision from the outset. They wanted to build a new major non-bank lender with a complete broker experience in mind, and to service all deal types, particularly those that other non-bank lenders often neglect.

Wells and Harkness shared some candid views with MPA when discussing ORDE’s first five years.

Sum of the parts

“When ORDE came to market, many brokers were fed up and wanted a better lending experience. Lenders weren’t responding, favouring their own interests and success – success built on the support of the very brokers they were taking for granted,” Wells told MPA Harkness added, “We focus on reliable approvals of complex deals that other lenders can’t or won’t support, delivered with really high service standards.” This ethos spans the full set of products ORDE has to offer. Looking back, Wells and Harkness said that

“our potential was clear to brokers from day one, when we launched the business with a highly flexible product range across residential, commercial and SMSF”.

No new lender, in their view, “has launched with that breadth already in hand. Since then, we’ve added construction, Prestige and are about to expand our interest-only range”.

It’s an undeniably bullish attitude, but they point to the solid growth in broker support, settlement volumes and team footprint to justify it.

“Our growth is really just the sum of lots of good individual experiences and successes leading to satisfied brokers,” Wells said, adding: “Our success is evidence that ORDE is delivering for brokers and the result of our ability to consistently provide an experience that secures their ongoing support.”

It’s not like the founders are lacking on the CV front. Harkness worked for nearly a decade at La Trobe Financial, one of Australia’s largest non-bank lenders. Before going on to create

ORDE KEY FACTS

ORDE, he was the firm’s chief operating officer.

Wells’ stint at La Trobe Financial lasted for closer to 12 years, during which time he acted variously as chief investment officer, head of funding and strategy, and chief financial officer.

This enviable range of experience gave them invaluable insights into how a leading nonbank works and can be improved, setting the stage for the genesis of ORDE in early 2020.

“We knew the ‘best of all’ combination required across product, service standards and culture,” said Wells. “The ORDE launch team had already delivered every product in our range throughout our many years of non-bank management experience.

“But we also believe that only by building a new business, ground up, with reset culture and operations, can a lender comprehensively maintain exceptional service standards at the higher volumes now received by large lenders.”

More than numbers

For ORDE’s managing directors, success is not

Proudly broker-only since day one Over 4,000 accredited brokers Zero to $6bn settlements in four years Full, flexible product range including resi-construction

‘One Lending Team’ of 100+ simplifying complex approvals

“When ORDE came to market, many brokers were fed up and wanted a better lending experience”

just measured in volume numbers. While the loan book has undeniably grown at a decent clip, there’s more that motivates them.

Wells said, “The key growth hasn’t so much been in asset levels, which have met our expectations, as in putting together and growing the very specific culture and skill sets across a large team – both when bringing in great talent and experience, as well as developing it internally.”

Harkness added, “Our growth has always been aligned to our determination to give brokers the experience they deserve, singularly focused on delivering the solutions and exceptional service that ORDE has now become known for at an ever-expanding scale.”

The centrepiece of ORDE’s business strategy, they said, is “to grow a culture centred on broker needs”.

“A real highlight has been seeing brokers, small and big, who are willing to try what we

offer, and often enough provide their generous recognition of our team. We get emails and responses all the time from brokers whose daily life is changing for the better.”

Overcoming challenges

While there is much to be proud of, no one can be fooled into believing that building a new business from the ground up is easy. At ORDE, “scaling and delivering a high-skills culture and team is hard to do, and it’s definitely the primary challenge we focus on”, said Wells. “And it would be impossible without a team wanting the same outcome.”

ORDE uses several cultural and operational frameworks to achieve this, including the ‘One Lending Team’ and ‘ORDE Broker Experience’.

ORDE’s One Lending Team is a highly integrated and aligned team spanning distribution, credit and settlements functions, who work to

benefit brokers and their customers. This unified vision of team culture, without silos, allows for the ORDE Broker Experience – the consistent delivery of end-to-end services and solutions aligned to broker-oriented outcomes.

Watch your attitude

“More fundamentally, you need to decide what your value proposition is,” said Wells. “From the beginning, ORDE based its relevance on what we could bring to, add to, or improve on brokers’ businesses, and perhaps add to the whole broking sector if we forced common improvements to standards.”

To adhere to this philosophy, ORDE doesn’t accept direct applications from borrowers at all – everything originates via the broker channel. To do otherwise would be “a conflict with our core business partners: brokers”.

ORDE’s broker-only approach, and standing start, has allowed the lender to build its offering with a razor-sharp focus. “Our attitude was: listen to what brokers want, understand what brokers want, and then build ORDE out to give them what they want,” said Wells.

“Distractions are plentiful with success; that road is well trodden. To us, it’s about management discipline.

“If we deliver on this fundamental orientation and focus for years, it may just give us the opportunity to be the best non-bank lender for brokers and their customers in Australia.”

ORDE currently partners with Australian mortgage brokers through top-tier aggregators and their subsidiaries, including Finsure, LMG, outsource Financial, SFG, YBR Aggregation, MoneyQuest and Nectar Mortgages, as well as dealing directly with credit licensees.

“Our distribution partners support our broker-first orientation and differentiated product position,” said Harkness. “We are focused on presenting ORDE to brokers across these partners. We also work with credit licensees outside of existing aggregators, and naturally, in time, we want to broaden that where it’s clear that brokers would like to deal with us.”

If ORDE truly is built for brokers, backed by brokers, it should be an easy sell.

IN A lush Cafe Sydney dining room overlooking the iconic Darling Harbour on a sunny February afternoon, MPA brought together six of Australia’s leading customerowned banks (COBs) and two brokerages for a deep dive into this unique part of the banking sector.

Joining MPA were leaders from some of Australia’s premier COBs, namely Gateway

Bank, Beyond Bank, Teachers Mutual Bank, P&N Bank, People First Bank and Bank Australia. Brokers from Waves Mortgage Brokers and Nectar Mortgages also took part to field questions and provide their insights into the state of the mortgage market.

The discussion ranged from attendees’ thoughts on impending interest rate cuts to how COBs manage to compete with the

CLOSE BROKER BONDS ESSENTIAL IN TIMES OF CHANGE

majors, what their members care about most in 2025, and how COBs are balancing these needs with the importance of turning a profit.

The roundtable came following a year of mixed performance in the mutual banking sector. While industry-wide operating profit was e ectively flat in 2024, lending growth outpaced the previous year, as did total

Customer-owned banks continue to fly the flag of dedication to their members amid large-scale consolidation, tough competition from the majors and a complex regulatory environment. Striking the balance is not always easy, but with technology and tight broker relationships, they look to the future with optimism and energy

deposits. Net interest margins (NIMs) also saw a notable improvement as higher interest rates took hold, although cost-to-income ratios trended in the wrong direction.

Two recently merged entities – People First Bank and Newcastle Greater Mutual Group – took the top position and second place respectively as the two largest COBs by total assets. This result provided the perfect

illustration of a sector in the throes of widespread consolidation, which provided further fuel for roundtable discussion.

Front and centre of every topic, though, was the critical role brokers play in driving the success of customer-owned banks. MPA heard how brokers are the driving force behind customer satisfaction, deal flow and even technological progress.

This was never more evident than when the roundtable participants were asked:

What role is the broker channel playing in securing market share growth in 2025?

Gemma Piscioneri, head of retail distribution at P&N Bank, kicked the discussion o : “Brokers are a crucial part of our

THE PANELLISTS

BROKERS

key driver for reaching underserved or niche customer segments, particularly first home buyers and refinancers.”

Darren McLeod, head of third party at Beyond Bank, explained that the lender has only been in the broker space for eight years, but within that time it has grown to more than 50% of Beyond’s business. “It’s a core part of our growth strategy,” he said.

“We’re prepared for the next flow of volume that will come with an interest rate reduction. We’ve been positioning ourselves for growth in 2025 to take advantage of a stronger market as confidence returns.

“The broker market has also helped Beyond expand into regions where we traditionally didn’t have a branch presence. We have branches across Australia, but in NSW and Victoria, where we had little presence, brokers have helped us penetrate those markets. They are now our strongest growth states, and we’re also seeing strong momentum in Queensland.”

Beyond Bank is also participating in the government’s First Home Guarantee scheme and is watching what happens with interest

multichannel approach, working seamlessly alongside our branches, mobile bankers, contact centres, virtual lending teams and digital platforms. This integration ensures we can meet our customers wherever they want, providing the flexibility and convenience they need to choose how they engage with us,” Piscioneri said.

“We operate in one of the most competitive channels in banking, and we know we must listen to our customers to remain relevant. Since the launch of our broker strategy some three years ago, P&N Group has delivered a range of improvements based on broker and customer feedback.”

Mark Middleton, head of third party distribution at Teachers Mutual Bank (TMBL), continued: “The broker channel remains crucial in driving growth, as brokers connect with a wide range of borrowers and play a key advisory role in the loan process.

“There will be underserved segments that brokers traditionally haven’t focused on. From

“Credit unions and customer-owned banks were formed by like-minded people who weren’t being served by the bank industry at the time. That ethos still holds true today” Darren McLeod, Beyond Bank

our perspective, we have many segments –whether that be the health sector or education – that we’ve catered to in the past, but I’m seeing more offerings being introduced by my competitors and the broader market. By strengthening relationships with brokers and providing transparent, consistent and competitive offerings, customer-owned banks such as TMBL will be looking to leverage the broker channel to attract customers who might otherwise go to larger banks.

“In 2025, TMBL is envisioning that our broker partnerships are expected to be a

rates. McLeod said, “The election will also have a big impact on how these products are positioned going forward.

“We’re keen to see how government policies evolve and how they enhance or change these products. So, hopefully they’ll do the right thing and we can take advantage of helping more people with a first home.”

Michael Sancilio, head of connected channels and partnerships at recently unified mutual People First Bank, added, “What we are starting to see in areas where we haven’t had a strong brand presence before is strong

Zeb Drummond Chief operating officer, Gateway Bank

John Leveque Regional manager, Bank Australia

Darren McLeod Head of third party, Beyond Bank

Mark Middleton Head of third party distribution, Teachers Mutual Bank

Gemma Piscioneri Head of retail distribution, P&N Bank

Michael Sancilio Head of connected channels and partnerships, People First Bank

Andrew Diamond Waves Mortgage Brokers

Justine McDonald Nectar Mortgages

YEAR IN REVIEW: 2024 HIGHLIGHTS

interest from brokers for an alternative product to really challenge the majors.”

Bank Australia’s John Leveque, regional manager for Victoria, SA, WA and Tasmania, said brokers “are an extremely important part of our business”. He highlighted that, per the latest statistics, nearly 75% of borrowers are seeking out brokers to help them with their loans; some estimates have

clock in at closer to 80% by the end of 2025.

“Over time, we’ve seen this trend increase, and it’s clear that that’s the customer’s choice. We embrace that,” Drummond said. “Brokers are our partners in delivering the best outcomes for customers, which will in turn be our members.

“What we do from a niche perspective [is] to help them tap into markets that perhaps

“Brokers are a crucial part of our multichannel approach, working seamlessly alongside our branches, mobile bankers, contact centres, virtual lending teams and digital platforms” Gemma Piscioneri, P&N Bank

this figure rising to 80% by the end of 2025.

“That said, at Bank Australia there are two ways to get a home loan – through a broker or online,” said Leveque. “You can’t apply through a branch. We find that a lot of customers that apply online tend to need help, and that’s where brokers can be a great help guiding our customers in the right direction.

“The role for our team then is to make sure that the brokers are provided all the support to ensure the right products and prices are put forward to our customers.

“As I said, customers who embark online may get through it halfway, then they want to speak to someone and they can’t, so this is why the broker channel is starting to expand and why it’s becoming more important to us.”

Gateway Bank’s chief operating officer, Zeb Drummond, said, “The broker channel is absolutely critical for us.” He explained that the bank’s third party channel far exceeds the market average, with 90% of all loans originating through brokers.

The latest MFAA statistics show that 74% is the current market average, although some industry experts expect that number to

previously haven’t been tapped where you know where perhaps the majors can’t play. For example, we cater to environmentally conscious customers who don’t want to feel as though there’s a third-party stakeholder in their loan being a shareholder of a big bank. That’s a key di erentiator for us.

“Listening to brokers is at the heart of our approach,” continued Drummond. “Our internal measure of broker satisfaction is ‘right first time’. Did we get it right the first time? Yes or no? Ninety-eight per cent of the time, the answer is yes.

“And that’s the stu we need to focus on: getting it right the first time and avoiding changes or moving the goalposts halfway through the transaction. Truly listening to brokers and responding to their needs is what will drive future growth. With brokers representing customers 74% of the time, that share is only going to grow.”

A running theme throughout the afternoon’s conversation was what impact the effects of monetary easing will have on the mortgage industry. At the time of the roundtable, odds were on the Reserve Bank of Australia opting to cut the cash rate by

25 LARGEST CUSTOMER-OWNED BANKS BY TOTAL ASSETS

25 basis points at the impending February call – a forecast that proved accurate.

The RBA had undoubtedly lagged behind its global Western counterparts prior to this long-awaited rate cut. Attention has since turned to where the RBA is heading next.

With that in mind, MPA asked the roundtable attendees:

A light at the end of the tunnel is emerging for interest rates and borrowing capacity. How is the customer-owned banking sector priming itself for an uptick in dealmaking volumes?

“I believe 2025 is undoubtedly going to be different to 2024, and there is a ray of hope for most borrowers and brokers,” said Middleton. “The rationale is that interest rates are most likely reducing in the first quarter of this year, which will create opportunities for brokers and, most importantly, their clients. Individuals will commence reassessing their

future financial needs before we start experiencing new opportunities.

Middleton said the 3% serviceability buffer has made it difficult for some borrowers to