The Salt Lake County office market ended 2024 with strong tenant demand for spec suites, enhanced amenities, and plug-and-play sublease spaces. Landlords worked to transform Class B properties to compete for tenants seeking high-quality environments, while new construction lagged thanks to elevated tenant improvement costs More tenants opted to renew longer lease terms in an effort to prioritize stability over uncertainty in a market evolving to meet changing preferences and navigate economic challenges

No new office construction projects broke ground in Salt Lake County at year-end as developers grappled with sticker shock from escalating costs. Construction dropped from 218, 552 square feet at the same time last year to 137,137 square feet currently. Rising tenant improvement costs and persistently high vacancy rates have forced developers to pause on future projects while they wait for more favorable market conditions With no projects on the horizon, landlords are instead focusing on upgrading existing properties to meet tenant demand for high-quality, amenity-rich space.

Top Construction Projects

Avg. Asking Lease Rates

Salt Lake County’s average asking lease rates for office space edged slightly up from $27.52 full-service gross (FSG) last quarter to $27 55 FSG at year-end, a modest increase thanks to steady demand for premium spaces despite broader market challenges Spec suites and Class B upgraded to Class A space drove activity this quarter as tenants prioritized high-quality, move-in-ready options and pushed landlords to modernize older spaces and add amenities Suburban markets with enhanced offerings like upgraded finishes are attracting tenants who are seeking a balance between quality and cost. Expect demand for these premium spaces to hold lease rates steady despite economic uncertainty and rising vacancy rates

Absorption

Absorption in Salt Lake County improved significantly this quarter from negative 1,085,596 square feet at year-end 2023 to negative 424, 351 square feet currently. Several large transactions in key submarkets drove momentum and contributed to this rebound, including Granger Medical’s 20, 618-square-foot lease in Sorenson Research 3, Echelon Biosciences’ 19,865 square feet in CentrePointe A, Franklin Covey’s 26, 358 square feet in Minuteman V and Acima Credit’s 54,834 square feet in Minuteman I. Positive lease signings point to a stronger market outlook and increasing tenant confidence

Vacancy

The overall direct vacancy rate for office space in Salt Lake County increased to 18 37 percent from 16 23 percent at year-end 2023 as tenants assessed their space needs and looked for high-quality properties. Sublease vacancy, however, decreased to 4 58 percent, a notable improvement as subleases expired to direct listings and sublease interest heightened thanks to their cost-effective and plug-and-play appeal The combination of less sublease space and steady leasing activity reduced availability, reversing a long-standing growth trend in the sublease market. As landlords focus on speculative buildouts and upgrades, expect continued pressure from elevated Class B availability

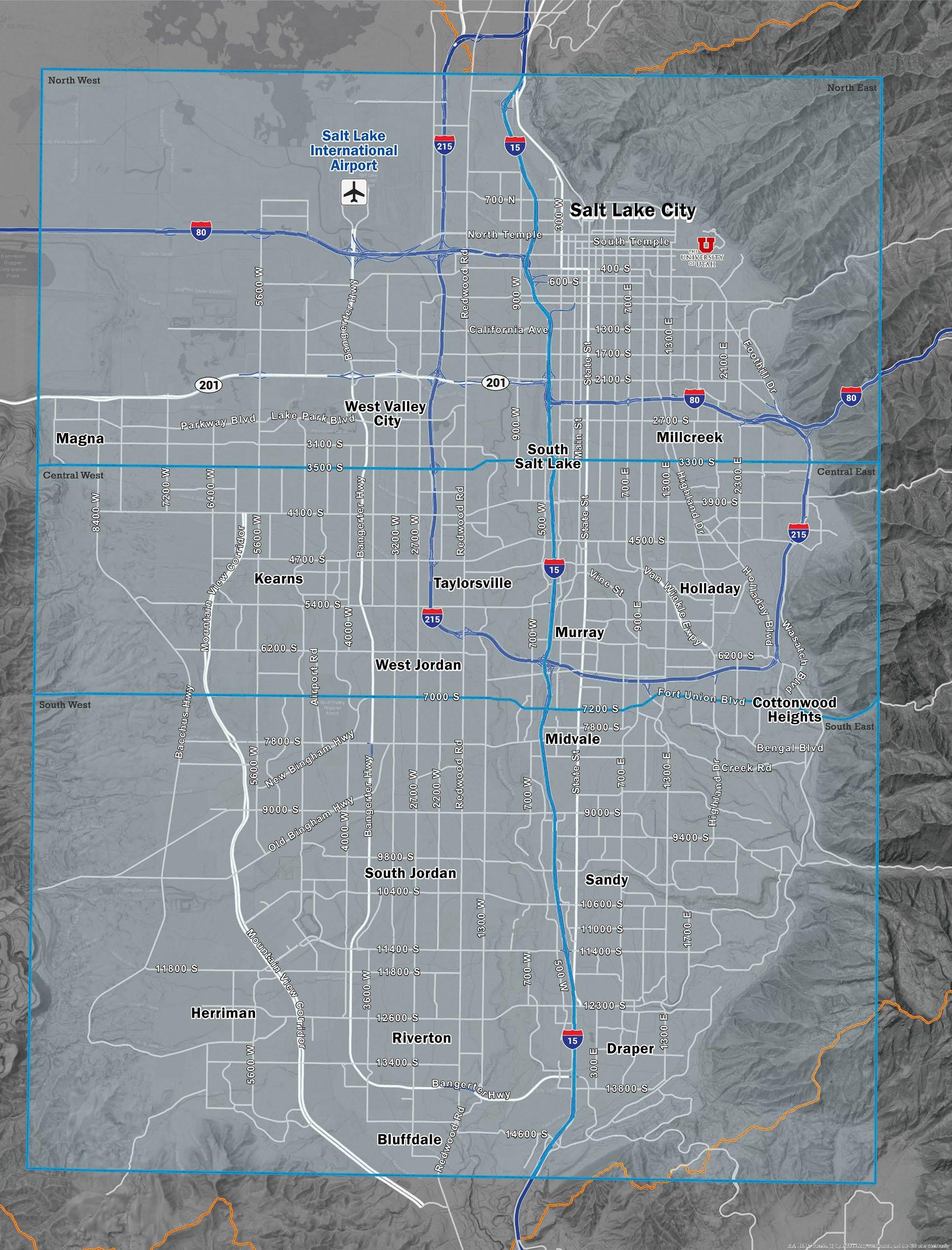

Salt Lake County | 24Q4 | Office | Market Statistics

Foothill

Salt Lake County | 24Q4 | Office | Market Statistics

Salt Lake County | 24Q4 | Office | Market Statistics

Largest Sublease Availabilities

Industrial 24Q4

Headline

In the face of varied economic challenges, the resilient Salt Lake County industrial market ended the year with tenants actively pursuing large-scale spaces and landlords capitalizing on limited availability Consistent tenant demand and a lack of new construction will keep lease rates steady throughout 2025. High interest rates and elevated construction costs have curtailed speculative projects, keeping supply constrained and competition strong.

Current Market Indicators

Historic Comparison Construction

Salt Lake County industrial developers have been hesitant to break ground on speculative projects thanks to elevated interest rates and construction costs. Year-end total current construction reached 3,365,310 square feet compared to 4,896,078 square feet recorded at the same time last year Any new developments in 2025 will likely be build-to-suit, as speculative projects are not financially feasible

Top Construction Projects

Industrial 24Q4

Avg. Asking Lease Rates

Industrial asking lease rates stabilized at $0 84 NNN compared to the previous quarter and the same time last year. With no anticipated substantial new construction and limited available space, landlords are likely to gradually increase rates throughout 2025. The South East submarket reported the highest year-end rate at $1 16 NNN with just one available space Expect the lack of options to intensify competition among tenants.

Absorption

Year-to-date industrial absorption reached a positive 4,169,878 square feet, a marked improvement compared to 3,736,680 square feet at the end of 2023. Western Partitions secured 216,027 square feet on Harold Gatty Drive in Salt Lake City, Cache Valley Electric Company took 48,281 square feet in West Jordan, and Smackin' Snacks leased 48,000 square feet in Salt Lake City, underscoring the market's capacity to attract a diverse range of tenants despite limited overall availability A combination of pent-up demand and strategic tenant positioning helped drive positive momentum in the industrial sector.

Vacancy

The direct vacancy rate for industrial space in Salt Lake County decreased from 5 27 percent to 4 41 percent year-over-year thanks to strong tenant activity and limited new supply While spaces over 100,000 square feet in size dominate vacant inventory, landlords hesitate to divide buildings into smaller configurations As the pace of new construction slows despite steady tenant demand, expect lease rates to rise Landlords who offer more flexible and functional space configurations may see quicker absorption.

4th Quarter Transactions

Lease

5742 Harold Gatty Dr

Western Partitions 216,027

Transaction Date: 11/01/2024

Renewal

615 S Gladiola St ESM

156,750 SF

Transaction Date: 10/22/2024

Lease

835 W 2600 S American Refrigeration Supplies

55,582 SF 10/03/2024

Lease

1736-1746 S 4250 W

Smackin’ Snacks

48,000 SF

Transaction Date: 11/01/2024

Lease 1717 S 4800 W

Peczuh Printing Company 44,105 SF

Transaction Date: 12/19/2024

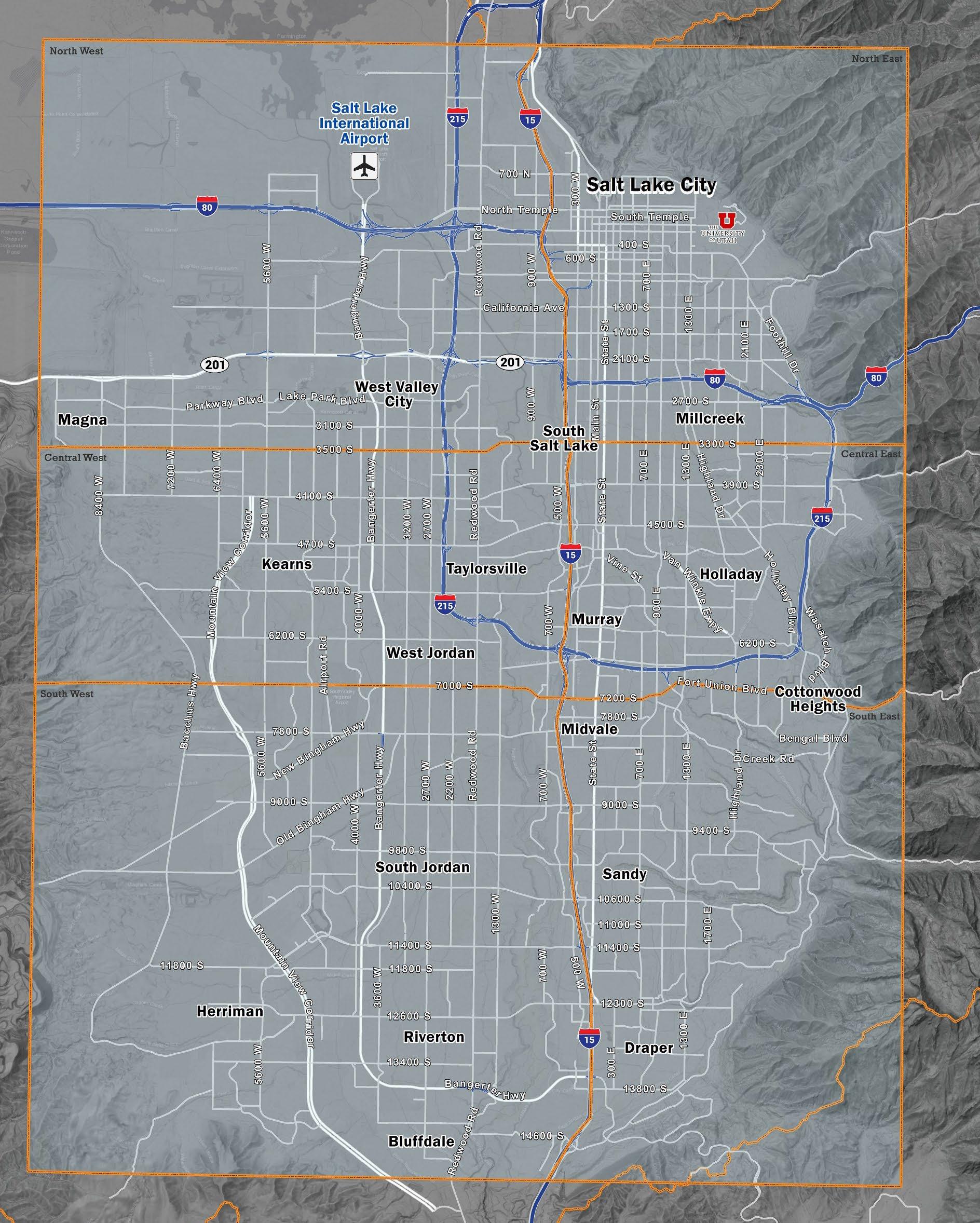

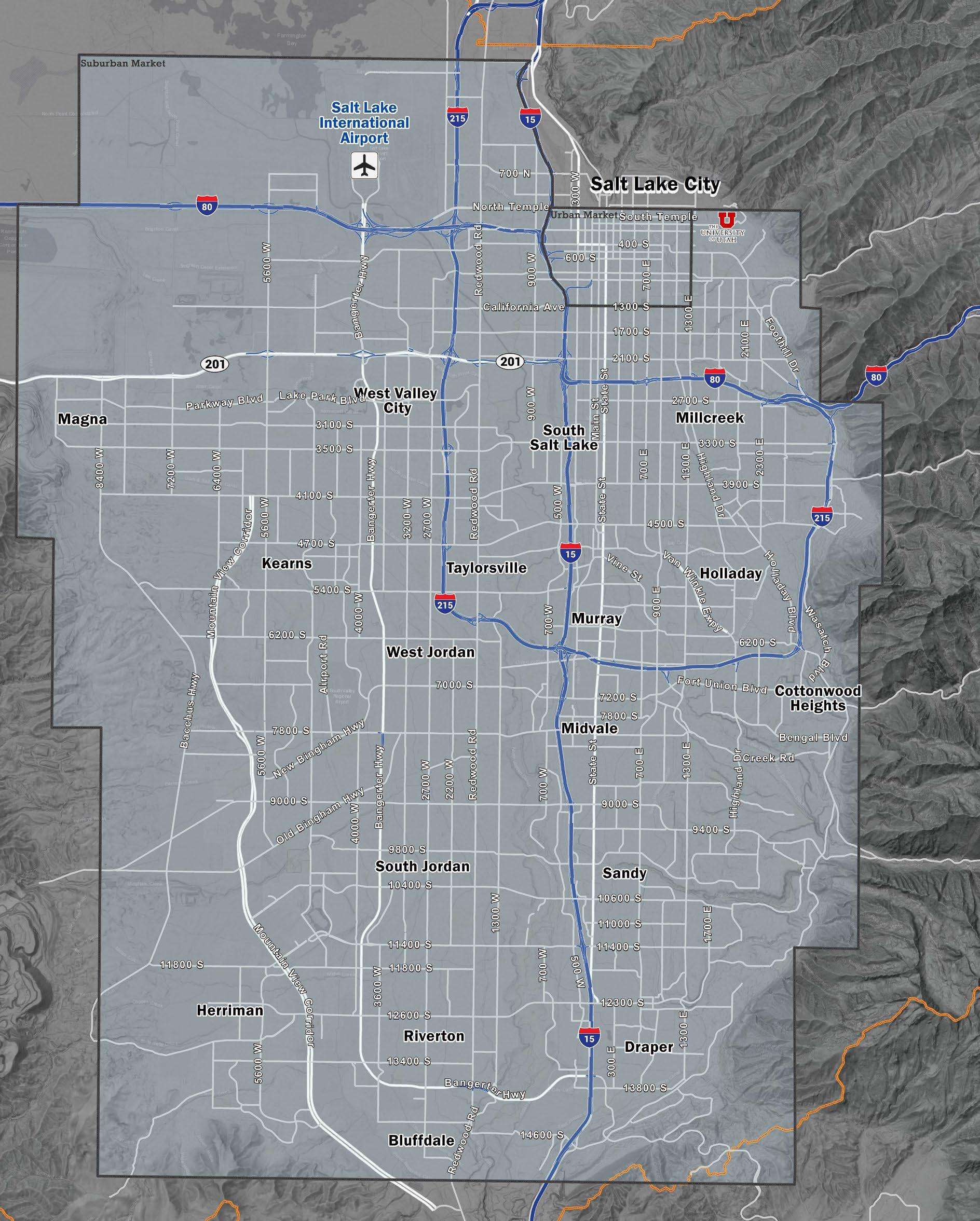

Market Overview

Market Activity

North West

Direct Vacancy Rate: 5.47%

YTD Absorption: 2,798,835 SF

Lease Rate: $0.80 NNN

North East

Direct Vacancy Rate: 1.06%

YTD Absorption: 143,198 SF

Lease Rate: $0.91 NNN

Central West

Direct Vacancy Rate: 1.56%

YTD Absorption: (99,379) SF

Lease Rate: $0.97 NNN

Central East

Direct Vacancy Rate: 1.64%

YTD Absorption: 41,770 SF

Lease Rate: $0.77 NNN

South West

Direct Vacancy Rate: 3.97%

YTD Absorption: 1,265,824 SF

Lease Rate: $1.03 NNN

South East

Direct Vacancy Rate: 0.19%

YTD Absorption: 19,630 SF

Lease Rate: $1.16 NNN

Current Market Indicators

Headline

Salt Lake County’s dynamic retail market ended the year by navigating strong demand and limited supply Retailers have been adapting to a competitive environment and limited availability by considering more flexible and creative solutions, including repurposing underutilized office space and exploring smaller, neighborhood shopping centers as viable alternatives to traditional large-format locations As construction activity increases in key areas, particularly the South West submarket, high-demand zones are putting continued upward pressure on lease rates In the face of fierce competition, retailers who are willing to innovate and adjust to evolving space needs can expect a positive outlook

Historic Comparison Construction

Salt Lake County’s retail construction activity ramped up to a total of 682, 677 square feet in development, a healthy year-over-year increase from 474,575 square feet at the end of 2023. The South West submarket accounted for nearly 86 percent of total construction with large projects like Academy Village and Midas Crossing in Herriman However, persistent supply constraints leave retailers struggling to secure space in a market trying to keep up with growing demand.

Top Construction Projects

Retail 24Q4

Avg. Asking Lease Rates

The average asking lease rate for retail space in Salt Lake County rose to $23.37 per square foot NNN by the close of the fourth quarter, a $0 16 increase quarter-over-quarter and a $2 16 increase year-overyear thanks to limited availability and continued high demand, particularly in high-traffic areas. The North West quadrant reached a high of $30.69 NNN due to limited availability and smaller, higher-priced space significantly influencing the overall rate Lease rates in other areas of the county saw steady rates.

Absorption

Retail absorption in Salt Lake County slowed to positive 63,147 square feet year-to-date compared to 639,374 square feet at the close of 2023

Evergreen Restaurant Group leased 15,205 square feet in Murray and Ulta secured 10,000 square feet at Legacy Plaza @ 54th in Taylorsville, keeping absorption positive In the face of continued historically low vacancy rates, tenants have limited options, leading to slower absorption across the county As more new developments come online, expect absorption to gradually pick up at a tempered pace in tight market conditions

Vacancy

Salt Lake County’s retail vacancy rate increased slightly from 2.28 percent at the same time last year to 2.43 percent currently. Landlords are beginning to explore creative solutions to maximize available space, causing an uptick in adaptive reuse projects. Underutilized office buildings and other nontraditional spaces are being transformed into retail environments, particularly on upper floors, alleviating some market pressure Additionally, brands seeking a more localized presence have looked to neighborhood shopping centers as a viable alternative to traditional mall or lifestyle center locations $0.00 $5.00

Market Overview

Market Overview

Overall Market Totals

Market Activity

North West

Direct Vacancy Rate: 2.50%

YTD Absorption: (24,289) SF

Lease Rate: $30.69 NNN

North East

Direct Vacancy Rate: 3.42%

YTD Absorption: 15,598 SF

Lease Rate: $25.67 NNN

Central West

Direct Vacancy Rate: 1.93%

YTD Absorption: 30,659 SF

Lease Rate: $2.08 NNN

Central East

Direct Vacancy Rate: 1.76%

YTD Absorption: (50,891) SF

Lease Rate: $24.52 NNN

South West

Direct Vacancy Rate: 1.93%

YTD Absorption: 151,223 SF

Lease Rate: $21.74 NNN

South East

Direct Vacancy Rate: 3.50%

YTD Absorption: (59,153) SF

Lease Rate: $21.03 NNN

4th Quarter Transactions

Sale

380 W Data Dr

Onset Financial

127,420 SF

Transaction Date: 10/01/2024

Renewal

10855 S River Front Pkwy Cricut

127,012 SF

Transaction Date: 12/16/2024

Renewal

440 W 200 S Bureau of Land Management

59,596 SF

Transaction Date: 10/31/2024

Sale 950 N 2200 W JustAng Airport Center 87,657 SF

Transaction Date: 10/29/2024

Lease 13997 S Minuteman Dr Acima Credit 54,834 SF

Transaction Date: 11/25/2024

Top Construction Projects

Market Overview

Overall Market Totals

Market Activity

Downtown

• Vacancy: 19.15%

• YTD Abs: (110,069) SF

• Lease Rate (FSG): $28.20

Suburban

• Vacancy: 18.03%

• YTD Abs: (312,282) SF

• Lease Rate (FSG): $25.02

4th Quarter Transactions

Sale

380 W Data Dr

Onset Financial

127,420 SF

Transaction Date: 10/01/2024

Renewal

10855 S River Front Pkwy Cricut

127,012 SF

Transaction Date: 12/16/2024

Sublease

2600 N Ashton Blvd nCino Portfolio Analytics 50,411 SF

Transaction Date: 11/15/2024

Lease 13997 S Minuteman Dr Acima Credit 54,834 SF

Transaction Date: 11/25/2024

Extension 12936 S Frontrunner Blvd

Truhearing 48,053 SF

Transaction Date: 12/06/2024

Top Construction Projects

Overall Market Totals

Market Activity

South Valley

• Vacancy: 16.29%

• YTD Abs: (139,193) SF

• Lease Rate (FSG): $27.18

Utah County North

• Vacancy: 10.36%

• YTD Abs: (19,056) SF

• Lease Rate (FSG): $25.27

Headline

Utah County’s office market had a resilient fourth quarter in the face of shifting tenant preferences and continued economic uncertainty With spec suites leasing faster than shell spaces, landlords decided to finish some suites to allow tenants who are eager for immediate occupancy to visualize their future space and avoid typical tenant improvement delays, offering a faster and more seamless transition Landlords also focused on enhancing Class B buildings with high-end finishes and amenities and positioning them as competitive Class A space. New construction remained stagnant, however, with escalating construction costs deterring any new development The outlook seems cautiously optimistic as the office market navigates current conditions

Historic Comparison Construction

The construction landscape in Utah County remained relatively quiet, with just 27,475 square feet under development at year-end compared to 68,000 square feet at the same time last year. Demand for medical office space continued, but developers are feeling cautious in the face of rising of construction and tenant improvements costs Instead, they have focused on upgrading and repositioning existing properties to appeal to tenants seeking high-quality spaces Until vacancy rates improve, expect the pace of new construction to stay slow

Avg. Asking Lease Rates

The average asking lease rate for office space in Utah County dropped slightly from $24.33 fullservice gross (FSG) last quarter to $24 00 FSG at year-end, reflecting market stability and ongoing tenant demand, particularly for welllocated, upgraded spaces. Strong demand for Class A space drove lease rates highest in the North quadrant Despite a slight decrease in lease rates, the overall market is holding steady as tenants seek flexible, high-quality office space with modern amenities.

Absorption

Year-to-date absorption in Utah County remained negative, increasing from negative 128,825 square feet at the end of 2023 to negative 209,851 square feet one year later. Several significant leasing transactions helped mitigate overall negative absorption, including Cozy Earth’s 30,097 square foot expansion at Thanksgiving Park VI and Trajector Holdings 14,480 square feet at Canyon Park Technology Center While the market faces challenges, demand for space in well-positioned locations remains strong

Vacancy

Direct office vacancy in Utah County increased to 13.90 percent year-end compared to 11.12 percent at the end of 2023 as tenants honed in on their office needs and adjusted to shifting market conditions Fortunately, sublease vacancy decreased to 5.95 percent from 6.44 percent year-over-year thanks to more than 20 sublease deals totaling more than 350,000 square feet leasing throughout the year. Fewer subleases are now coming online as tenants have met their space needs and are feeling more comfortable in their current offices, pointing to a more stable market moving forward.

$30.00

$20.00 $25.00

$15.00

$10.00

$5.00

200,000 400,000 600,000 800,000 1,000,000

(200,000)

(400,000)

Top Construction Projects

Market Activity

Utah County North Direct Vacancy Rate: 10.36% YTD Absorption: (19,056) SF Lease Rate: $25.27 FS

Utah County West

Direct Vacancy Rate: 0.00%

YTD Absorption: 0 SF

Lease Rate: $0.00 FS

Utah County Central

Absorption: (194,079) SF

Rate: $23.08 FS

Utah County South Direct Vacancy Rate: 18.40% YTD Absorption: 3,284 SF Lease Rate: $21.50 FS

Industrial 24Q4

Headline

Utah County’s industrial market ended a steady year with robust tenant activity and ongoing development. Developers continued to target opportunities in the southern quadrant, feeling confident about the market’s potential. Vacancy rates declined in the fourth quarter due to strong leasing momentum, while absorption demonstrated continued demand for large-scale space. Expect the market to maintain stability over the next three years with a leasing pace more aligned with 2019 pre-pandemic levels, and power supply considerations as a key discussion topic for new developments in 2025.

Current Market Indicators

Historic Comparison Construction

The drive to build industrial space in Utah County is gaining momentum, particularly in the southern quadrant Total construction reached a strong 2,933,934 square feet, with nearly all industrial projects completed in 2023 fully leased or approaching full occupancy thanks to strong demand for highquality space. Developers who secured land in prior years are finally moving forward with new projects, feeling confident in the market’s long-term potential and laying the groundwork for measured but steady growth in the coming years

Avg. Asking Lease Rates

The average asking lease rate reached $0.95 NNN at year-end compared to $0 96 NNN last quarter Businesses seeking space in the 20,000–50,000square-foot range are driving demand and showing no signs of slowing in the near future. Consistent lease rates reflect a balanced market that accommodates both tenant needs and developer expectations Expect lease rates across Utah County’s industrial market to remain steady or increase modestly, further solidifying the area’s reputation as a desirable location for industrial tenants

Absorption

Year-to-date absorption reached positive 1,485,707 square feet at the end of 2024 compared to positive 1,718,544 square feet at year-end 2023 Alice Lane secured 71, 043 square feet at Lakeshore in Springville, Top Health Manufacturing occupied 68, 871 square feet in Payson Tech Center, and Total Facility Solutions took 49,461 square feet in Northshore Commerce Building 1 in Saratoga Springs Utah County’s resilient industrial market is underscored by sustained demand for expansive, strategically located facilities

Vacancy

Vacancy rates in Utah County decreased significantly from 4 63 percent last quarter to 3 88 percent at yearend, highlighting robust leasing activity across all quadrants. Once current construction reaches completion, vacancy rates will likely rise for a quarter or two, but new spaces will fill quickly as demand continues to outpace supply Limited available space underscores the market’s strength and consistent demand for industrial facilities

(100,000) 400,000 900,000 1,400,000 1,900,000

Utah County

Industrial 24Q4

4th Quarter Transactions

Lease

2111 W Center St Alice Lane

71,043 SF

Transaction Date: 11/30/2024

Lease

68 W 1130 N Top Health

Manufacturing

68,871 SF

Transaction Date: 10/09/2024

Sale

560 & 572 E 1700 S M-Con Real Estate

Holdings 43,614 SF

Transaction Date: 12/09/2024

Lease 593-659 N Saratoga Rd

Total Facility Solutions 49,461 SF

Transaction Date: 10/31/2024

Lease 593-659 N Saratoga Rd Picklr

36,957 SF

Transaction Date: 10/31/2024

Top Construction Projects

Overall Market Totals

Market Activity

Utah County North

Direct Vacancy Rate: 1.71%

YTD Absorption: 719,199 SF

Lease Rate: $1.13 NNN

Utah County West

Direct Vacancy Rate: 8.18%

YTD Absorption: 194,069 SF

Lease Rate: $0.99 NNN

Utah County Central

Direct Vacancy Rate: 4.09%

YTD Absorption: (132,243) SF

Lease Rate: $0.97 NNN

Utah County South

Direct Vacancy Rate: 5.48%

YTD Absorption: 704,682 SF

Lease Rate: $0.89 NNN

Headline

Utah County’s resilient retail market saw strong demand drive continued competition for space through the end of the year Vacancy rates hovered at a tight 2 48 percent, while lease rates continued to rise as retailers competed for available locations. Construction activity increased year-over-year, and areas like Saratoga Springs and Eagle Mountain saw rapid development and premium prices. Retailers started exploring non-traditional spaces and flexible formats to adapt to and navigate a competitive market With more favorable interest rates on the horizon, the market is well-positioned for continued growth and its accompanying challenges and opportunities for retailers and developers.

Current Market Indicators

Historic Comparison Construction

Retail construction in Utah County showed steady growth in the fourth quarter, reaching 473,589 square feet compared to 196,086 square feet at the same time last year. However, as developers faced ongoing financial challenges in bringing new space to the market, only build-to-suit retail projects were completed in 2024 With vacancy rates remaining well below 3 percent and no new speculative retail space on the horizon, tenants are facing increased difficulty in securing space amid tight market conditions.

4th Quarter Transactions

Sale

898 S 2550 E

Bluefin Property Investments 24,394 SF

Transaction Date: 12/17/2024

Sale

248-260 N Main St Altura Packaging 20,140 SF

Transaction Date: 10/09/2024

Lease 153 W Crossroads Blvd MB Pizza 2,576 SF

Transaction Date: 10/15/2024

Lease 6 W Main St

The GoForth Foundation 2,342 SF

Transaction Date: 12/20/2024

Lease

2235-2293 N University Pkwy Liberty Horizon 1,872 SF

Transaction Date: 11/27/2024

Avg. Asking Lease Rates

The average asking lease rate for retail space in Utah County rose to $26.88 per square foot NNN by the close of the fourth quarter of 2024, a significant increase compared to $24 67 NNN at the same time last year In the face of high demand and limited availability, newer developments in high-growth areas like Saratoga Springs and Eagle Mountain are commanding premium prices. As vacancy rates remain low and competition for space intensifies, expect lease rates to continue to climb, making the market increasingly favorable for landlords and those able to secure space in these sought-after locations

Absorption

Retail absorption in Utah County showed positive movement in the fourth quarter, with year-to-date absorption reaching 57,738 square feet, down from 173,488 square feet at the end of 2023. Given low availability and limited leasing activity, expect incremental increases in absorption as tenants compete for limited options. Absorption may see further increases as new developments come online, especially in high-demand areas.

Vacancy

Utah County’s retail vacancy remains exceptionally tight at 2 47 percent As demand outpaces supply, landlords are getting more creative with the scarce available space. Zoning policies are expected to adapt to market conditions, potentially allowing developers to repurpose underutilized properties, converting office buildings into second- or third-floor retail spaces As apparel, food and beverage, and experiential pursuit retailers continue to expand, the retail landscape will likely make room for new formats that meet current needs and capitalize on existing space, addressing ongoing vacancy constraints and providing additional opportunities in high-demand areas well into 2025

Top Construction Projects

Market Activity

Utah County North Vacancy Rate: 1.10% YTD Absorption: 24,099 SF Lease Rate: $31.02 NNN

Utah County Central Vacancy Rate: 3.07% YTD Absorption: 119,059 SF Lease Rate: $21.78 NNN