Lioness Playbook Series / Managing Your Business Cash Flow

Lioness Playbook Series

Managing Your Business Cash Flow

Your guide to better understanding, managing and improving your business Cash Flow.

Successful South African women entrepreneurs share their strategies for managing cash flow in their businesses to fuel growth.

Introduction

About the

Lioness

Playbook Series

Lioness Playbook Series provides practical business advice and insights delivered directly by leading African women entrepreneurs selected from the Lionesses of Africa community. These experienced women entrepreneurs share their proven hacks, tactics and strategies for getting things done in business. Hard won, tried and tested business knowledge is presented in an easy-to-read format for you to learn from and apply in your own business. Relevant, agenda-free, pragmatic, advice and strategies that are sure to help drive successful change in your business and guide your personal growth journey as a woman entrepreneur.

Cash flow is the oxygen of your business

Every entrepreneur knows that maintaining a strong cash flow is key to business successit’s the oxygen that keeps it alive. However, it can be harder to achieve good cash flow management in practice. There are times when the business will have good cash flows, for example after a positive sales period, or after closing a big deal or project. However, there are other times when cash flow is under pressure, after an unexpected essential large-scale purchase, or during a weak sales period when the local or global economy is challenging. Let’s face it, even profitable, fast-growing companies can experience cash flow challenges at times while waiting for big deals to convert into cash in the bank.

So, it’s time to start getting your cash flow management strategy on track. Use this Playbook as your guide. It will help you to focus on how to manage your cash flow better, no matter what stage of your business-building journey you are on. Our featured Lionesses bring their own experiences to the table, sharing their proven hacks, tactics, and strategies to help you better understand, manage, and improve your business cash flow.

Enjoy our Lioness Playbook.

Melanie Hawken

Founder & CEO

Lionesses of Africa

Efficiently managing cash flow plays a significant role in the sustainability of SMEs

In today’s difficult economic environment and ever-changing business landscape, managing cash flow effectively is more critical than ever. In fact, research underscores the significant role that cash flow plays in the success and sustainability of small and medium enterprises (SMEs).

At Absa, we recognise the contribution these businesses make in driving economic growth, creating jobs and fostering innovation. We also understand the unique challenges that SMEs face, particularly those owned by women. Our ongoing engagements with business owners reveal that managing cash flow can be particularly difficult, especially during the critical first two years of operation.

It is against this background that we collaborated with the Lionesses of Africa to develop this playbook. The learnings from the last few years have underscored that access to appropriate resources, training, mentorship and funding opportunities can enable positive outcomes for women entrepreneurs. This playbook is an effort to supplement the collection of resources already available.

We remain committed to walking the journey with you and we continue to be inspired by your resilience, the strength of your vision, and the potential of your enterprises. We look forward to seeing your businesses flourish.

Ronnie Mbatsane

Managing Executive for SME Business, Absa Relationship Banking

Empowering women entrepreneurs to navigate the complexities of cash flow management

As part of our strategy to be the primary partner for our clients, and broader efforts to transform South Africa’s economic competitiveness, Absa is fully committed to support women entrepreneurs along their journey by building strong relationships with them and creating innovative solutions that meet their unique needs.

Our focused approach to the various client segments we serve, coupled with our strategy of keeping close to our clients, allows us to respond to the specific challenges faced by today’s women-owned businesses.

As the Bank of the Entrepreneur, we are proud to sponsor this Cash Flow Playbook, designed to provide practical insights, tools and strategies to navigate the complexities of cash flow management. This collaboration is a testament to our commitment to supporting small businesses, particularly those owned by women, which contribute to the growth and prosperity of our economy.

The resource is designed to provide actionable insights, practical strategies, and real-world examples to help you navigate the complexities of cash flow management and guide you in making informed financial decisions.

It is our hope that this guide serves as a valuable companion on your entrepreneurial journey and that it helps you achieve your business goals.

Sanah Gumede

Managing Executive for Strategy

and Customer Value Management,

Absa Relationship Banking

Featured Lionesses

ndiswa Silin a,

nnie M r nda,

f und r, GGES

f und r, Rufar Garm nt

le Ma wents ,

Ma latse Mamaila, a ren nders n,

Mamela t li,

Map l ata ,

Mar aret Hirsc ,

Ma ricia C x,

f und r, Asmara C ff

f und r, NO-Bi di s

f und r, KOA A ad m

f und r, ak N t

f und r, dikan

-f und r, Hirs ’s H m st r

f und r, W m

Mic ele Carelse,

Nneile Nk lise,

f und r, F d H a t

f und r,

P mzile K za, zelle brams n,

f und r, at it a-Bi di s

f und r, Fynb s Fin F d

Sas a Kn tt,

-f und r, J b Crysta

Sewela Sets e,

f und r, fata En in rin

T k zile Man wir ,

f und r, Ni tiqa Hair ar

South African women entrepreneurs share their top cash flow management advice

“Keeping a cash reserve is my number one cash flow management recommendation. Creating and keeping that buffer makes sure you can pay your debts even when your business isn't making as much money as projected.”

— Mauricia Cox

“...by getting to know your finances, especially your cash flow projections, women entrepreneurs can make smarter decisions that drive the growth and sustainability of their businesses.”

— Lauren Anderson

“Always make sure that you keep making a profit and that you keep ploughing that profit back.”

— Margaret Hirsch

“I rely heavily on an annual budget as well as monthly budgets to help forecast upcoming expenses and potential shortfalls. This gives me the opportunity and time to 'make a plan'

— Michele Carelse

“Avoid neglecting cash flow projections. Many entrepreneurs focus solely on profit and loss, overlooking cash flow forecasts. This can lead to liquidity issues, even if the business is profitable on paper.”

— Mamela Luthuli

“Keep the project pipeline full. A constant flow of new projects secures consistent income. Avoid project gaps that create cash flow disruptions, making it harder to meet ongoing expenses.”

— Andiswa Silinga

Once you have a clear insight into the cash situation you can find a balance between what needs your focus income or expenses.”

— Sasha Knott

“Be careful of the big, juicy deal. While large orders or clients may be great for revenue, the resulting cash flow strain may put your business at risk.”

— Annie Muronda

“At any given time in your company, always ensure your cash on hand can provide at least a 6 months runway. If not, then make some cuts in your company so that you have cash on hand for 6 months.”

— Nneile Nkholise

“I've learned to sidestep common traps. First, don't neglect budgeting; always track income and expenses. Build cash reserves to weather uncertainties and avoid the hand to mouth cycle.

A Roadmap to Success:

Managing Your Business Cash Flow

A step-by-step guide for

So, where do you start when it comes to cash flow management? Whether you’re a young, first-time entrepreneur or a seasoned professional, our step-bystep guide for mastering your cash flow is designed to help you pay your expenses, grow your business, and minimise the stress associated with it.

Understand your cash flow

"Cash flow" is known to be the lifeblood of any business. For any entrepreneur starting up or scaling a business, it's not just crucial; it's a game-changer. Your business's survival hinges on your grasp of the concept and its impact.

Cash flow in business refers to the total amount of money coming into and going out of the business. A positive cash flow fuels business growth, enabling you to hire more staff, open new locations, and acquire better equipment or assets. Conversely, a negative cash flow indicates that more money flows out of the business than in.

Think of your cash flow like a water tank. You want to keep it full to enable business operations and growth. To achieve this, the amount of money coming in should exceed the amount going out. Positive cash flow means you earn enough money to pay your bills and have extra to reinvest in your business. Additionally, you are able to deposit money into your bank account and withdraw it without the concern of your account becoming overdrawn.

While it may seem simple, there is always more to learn, and this Playbook is designed to guide you through it and provide you with great advice from leading women entrepreneurs.

Think of your cash flow like a water tank. You want to keep it full to enable business operations and growth.

Why is cash flow so important for your business?

Cash flow is crucial for the success and sustainability of any business. It represents the movement of money in and out of a company, and having a positive cash flow is essential for meeting financial obligations such as paying employees, suppliers, and bills on time. Without a healthy cash flow, the business may struggle to operate smoothly and may even face the risk of insolvency.

Additionally, a positive cash flow provides the flexibility and resources needed for future growth and investment. It allows the business to seize opportunities, expand operations, invest in new equipment, or hire additional staff. A strong cash flow also indicates the financial health of a business and its ability to weather unexpected expenses or economic downturns.

Furthermore, understanding and managing cash flow effectively can help women entrepreneurs make informed decisions about pricing, inventory, and expenses. It provides valuable insights into the financial performance of the business, helping to identify and predict potential cash flow gaps or areas for improvement.

In short, cash flow is the lifeblood of a business. It enables day-to-day operations, supports growth and investment, and serves as a key indicator of financial health. Therefore, maintaining a positive and stable cash flow is imperative for the long-term success of a small business.

Cash flow vs. profit

Is profit the same as good cash flow? In short, no.

Business owners often make the mistake of thinking that as long as they are making a profit according to their accounts, there will be enough cash to support ongoing operations.

It's important to remember that even profitable small businesses can experience cash shortages. This may come as a surprise, but a business could be making a significant profit and still experience negative cash flow due to the business owner withdrawing cash to cover personal expenses.

In essence, profit reflects a business's financial performance. It's the amount of money a company earns after deducting all expenses. A business can either have a positive profit, which means it earns more money than it spends, or a negative profit, which means it spends more money than it earns. Cash flow, on the other hand, pertains to the amount of cash entering and exiting a business. It's vital for day-to-day operations – even if a business makes a profit, it will struggle to pay expenses if that cash isn't flowing consistently. Consequently, cash flow is directly linked to the business's success.

“Revenue is vanity, profit is sanity, cash flow is reality.”

Cash flow is the lifeblood of a business. It enables day-to-day operations, supports growth and investment, and serves as a key indicator of financial health.

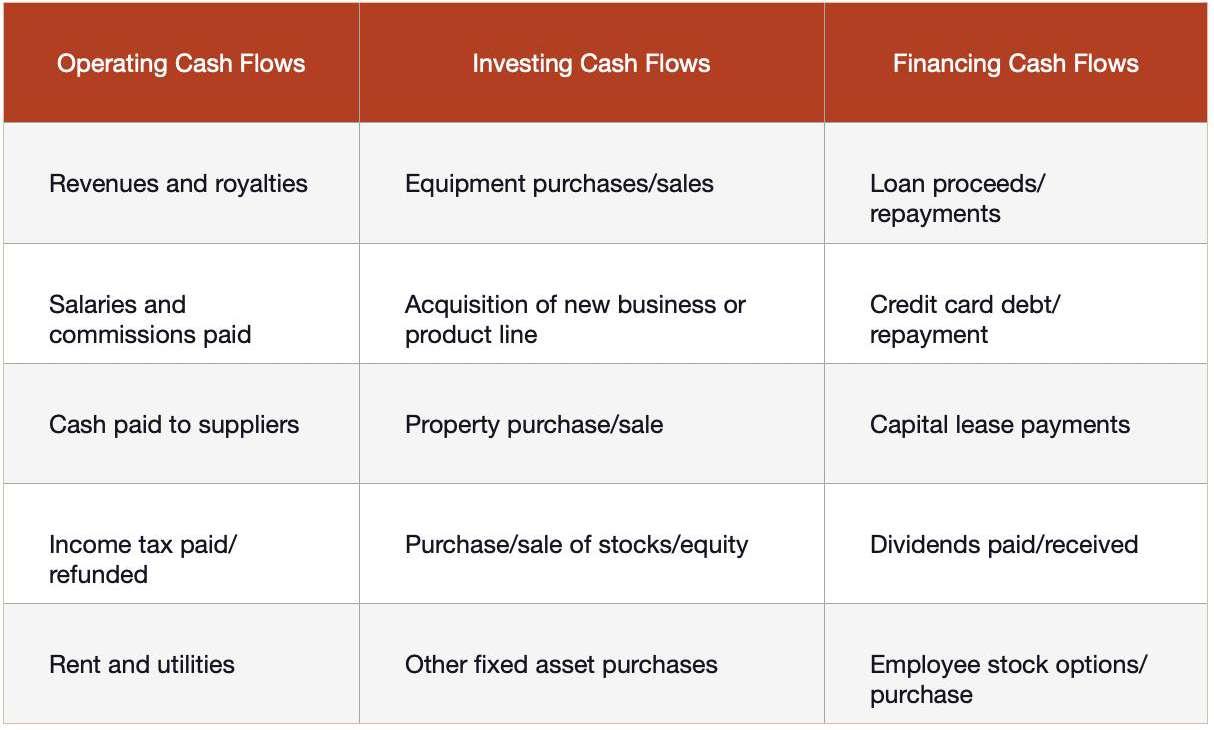

3 Types of cash flows

The management and reporting of cash flow involves categorizing cash flows into three types: operations, investments, and financing. Cash flows from operating activities stem from the day-to-day business operations, such as paying wages, buying inventory or paying for utilities. Investment cash flows are associated with long-term assets, such as equipment purchases or property sales. Financing cash flows result from debt and equity activities, including debt and interest payments to creditors and dividends to shareholders. Below, you'll find examples of different types of cash flows for small businesses.

Manage your cash flow

How can you track how much cash you have in your business at a given time? What about the cash needed to operate and grow your business? What about future cash needs to buy new equipment or assets?

Cash flow management involves monitoring the money coming in and going out of a business over time. Tools and techniques for cash flow management enable business owners to predict and control the amount of available money for the business in the future. Effective cash flow management is crucial for the success of small businesses.

Three techniques help small business owners understand, manage, and enhance business cash flows:

1. Cash flow statement

2. Cash budget

3. Cash flow analysis

We will explain how to prepare a cash flow statement, create a cash budget, and conduct a cash flow analysis.

How to calculate your small business cash flow

Before using any of the three cash flow management techniques, you need to know how cash flow is calculated. The most common method of calculating a SME’s cash flow breaks cash flow balances into the three categories (described in the previous section) and adds them to the cash balance at the beginning of the period. That formula for any time period is:

The statement of cash flows is one of three financial statements that a small business must prepare at the end of each accounting period. The other two financial statements are the income (P&L) statement and the balance sheet. The cash flow statement is the single most valuable tool a small business owner has for managing liquidity and solvency over time. It breaks down cash flows into operating, investing, and financing activities, helping business owners manage liquidity and solvency. It identifies cash flow challenges, gaps between income and expenses, and areas for potential growth and investment.

Effective cash flow management is crucial for the success of a SME business.

Prepare a cash flow statement

Here are 5 steps for preparing a cash flow statement for a small business using the irect metho transactions from the company's operating activities. This inclu es cash receive from customers an cash pai to suppliers, employees, an for operating expenses to the company's investing activities. This involves cash receive from the sale of assets an cash pai for the purchase of assets, such as equipment or investments with the business's financing activities. This inclu es cash receive from borrowing or issuing shares, as well as cash pai for ebt repayment an ivi en s investing, an financing activities. This involves summing up the cash flows from each category to arrive at the net increase or ecrease in cash for the perio cash flow statement (a basic Excel sprea sheet works well, or fin a free template online), presenting the net cash flow from each activity category an reconciling the beginning an en ing cash balances

Start wit cas from operating acti ities

Detail cas flows from in esting acti ities

Identify cas flows from financing acti ities

Summarize t e net cas flow

Present t e cas flow statement

These steps will help in preparing a comprehensive cash flow statement using the irect metho for a SME business.

The cash flow statement is the single most valuable tool a small business owner has for managing liquidity over time

Create a monthly cash budget

One way to improve an manage your business's cash buffer is to create a monthly cash bu get that relates to your cash flow projections an anticipates cash nee s. By un erstan ing projecte cash flows, business owners can set asi e the cash they will nee for expenses an can manage business activities accor ingly. A cash bu get shoul be create 6-1 months in a vance an a justments ma e as nee e base on actuals. Follow these 3 steps

Estimate Cas Inflows

Begin by estimating the cash that your business expects to receive in a given perio . This inclu es sales revenue, accounts receivable collections, an any other sources of incoming cash such as investments or loans. Be realistic in your estimates, taking into account factors like seasonality an economic con itions

Project Cas O tflows

Next, i entify an estimate all the cash payments your business is likely to make uring the same perio . This shoul inclu e expenses such as payroll, rent, utilities, loan repayments, inventory purchases, an any other operating costs. Consi er the timing of these payments to accurately project when the outflows will occur

Prepare t e B dget

With the estimate cash inflows an outflows in han , create a cash bu get that outlines the projecte cash position for specific time perio s, such as weekly or monthly. This bu get will help you un erstan when your business is likely to experience surpluses or shortages of cash, allowing you to plan an manage accor ingly. Regularly review an up ate the bu get as circumstances change to ensure its accuracy an usefulness.

Be realistic in your estimates, taking into account factors like seasonality and economic conditions.

Cash flow analysis

Cash flow analysis is an important tool for managing the cash flow of a SME business

This technique involves examining various aspects of a business that can affect its cash flow, inclu ing accounts receivable, inventory, accounts payable, an cre it facilities The goal of cash flow analysis is to i entify any cash flow issues that may affect the liqui ity of the business, to n ways to improve the cash flow an to i entify cash flow problems ahea of time

Identifying Cash low Patterns:

By analyzing cash flow, a SME can i entify recurring patterns an tren s in its cash inflows an outflows This can help in pinpointing perio s of surplus or shortage, allowing the business to plan an strategize effectivel

can highlight inef ciencies in accounts receivable an accounts payable processes

By optimizing these processes, a business can expe ite incoming cash an manage outgoing cash more effectively, thereby improving overall cash flow

Streamlining Accounts Receiva le and Accounts Paya le orecasting and Planning

Identifying Cost Reduction Opportunities

Utilizing cash flow analysis, a small business can create accurate cash flow forecasts, allowing for proactive planning an resource allocation By forecasting cash inflows an outflows, the business can anticipate potential shortfalls an surpluses, enabling better nancial ecision-making business can i entify areas where costs can be minimize By scrutinizing cash outflows, the business can n opportunities to re uce expenses an improve overall cash flow

By analyzing cash flow, a SME can identify recurring patterns and trends in its cash inflows and outflows

Improve your cash flow 03

Running a small business presents numerous financial challenges, with cash flow management being a primary concern. SMEs can employ various strategies to enhance cash flow and bolster business expansion.

In this section, we will explore 12 ways for you to enhance your business cash flow. It is important to commit time and energy to this task. Women entrepreneurs can effectively track the money coming in and going out, which enables better decision-making and proactive planning. Tracking cash flow helps in understanding when to expect peaks and troughs in cash, identifying potential shortages, and ensuring there's enough liquidity to cover operational expenses, investments, and growth initiatives. Moreover, analyzing cash flow data reveals valuable insights into areas for cost savings, optimizing revenue generation, and identifying potential financial risks. Ultimately, a solid grasp of cash flow allows small business owners to navigate challenges, seize opportunities, and sustain long-term success.

What causes cash flow problems?

Before discussing ow to improve your cas flow, it makes sense to understand w at causes cas flow issues in t e first place. Some of t e most common causes include

Bein too optimistic:

Entrepreneurs by nature are optimists. But w en

it comes to cas flow, t at attribute can be a downfall. For instance, don’t spend too muc oping t at you’ll make it up tomorrow

Hi h fixed costs:

Hig fixed costs suc as rent or salaries can put a strain on cas flow during periods of slow sales

Late customer payments:

W en customers fail to pay t eir invoices on time, it can lead to a cas flow crunc for t e business

High stock levels:

Having excessive stock can tie up funds t at could be used for paying bills or investing in growt

Seasonal fluctuations:

Many businesses experience fluctuations in sales t roug out t e year, w ic can create cas flow problems during slow or off-peak demand periods

Not preparin a cash flow forecast:

Not understanding t e business’s anticipated future cas flow can lead to being unaware of impending cas s ortages.

Overspendin too soon:

One way to avoid spending too muc is by creating a business plan w ere you map out w ic milestones you s ould meet before you make certain investments

Not havin enou h of a cash buffer on hand:

Many small business owners start up wit little to no reserve for rainy day funds.

To avoid t is dilemma, a good best practice is to ave at least two mont s of operating expenses in your business savings account

Don't assume that you can solve a cash crunch by raisin funds:

Even if your business meets t e criteria for receiving credit or is attractive to investors, t e loan application and investment-seeking process can be time-consuming, especially during a crisis. It is better to concentrate on managing t e funds your business currently possesses, w et er t ey were internally generated or borrowed, rat er t an continually searc ing for additional funding.

To maintain a positive cas flow, business owners need to take steps to manage and mitigate t ese problems. In t e section t at follows we outline several strategies you can begin utilizing today to begin to improve your cas flow.

Make strategic decisions on how to improve cash flow to ensure your business remains vibrant and competitive in the long term.

12 ways to improve your cash flow

Improving cash flow is crucial for the health and sustainability of your small business By adopting a comprehensive approach that includes leveraging technology, enhancing customer relationships, optimizing inventory management, and strengthening supplier relationships, you can create a more resilient and flexible financial foundation Remember, effective cash flow management is not just about monitoring the money that flows in and out of your business; it’s about making strategic decisions to ensure your business remains competitive in the long term

Discount stock sittin on s elves

Many small businesses have stock sitting on shelves A healthy cash flow relies on the swift turnover of stock for which the cash outlay has already been made To improve cash flow, it's important to know the average industry norms for stock turnover You can offer discounts or bundle slow-moving stock with other products and services to help sell them and improve your balance sheet

Speed up your accounts receivable

There are several ways to speed up the collection of payments from customers These include leveraging technology to accelerate payment receipt, promoting credit card payments, offering discounts and incentives for early payment, and ensuring that invoices are sent out early, are accurate, and have clear payment due dates

onduct credit checks on customers

Conduct credit checks on customers seeking credit to minimize the risk of late payments and cash flow disruptions When a small business is considering extending credit to customers, it's crucial to conduct thorough credit checks to mitigate the risk of late payments and cash flow disruptions This process typically involves obtaining and reviewing the customer's credit report, assessing their credit history, evaluating their current financial status, and setting clear credit terms to minimize potential risks By implementing these measures, small businesses can make more informed decisions and minimize the impact of late payments on their cash flow

Optimize accounts payable

It's crucial to maintain good relationships with vendors and suppliers when managing accounts payables Paying invoices on time and capitalizing on early payment discounts can help build trust with vendors and lower expenses It's also worth exploring opportunities to negotiate more favorable payment terms, such as by entering into long term contracts in return for discounted prices.

Cu spending

It may seem obvious, but one of the quickest ways to improve cash flow is to reduce spending. Focus on enhancing cash flow by eliminating unnecessary expenses and paying for essential costs at more strategic times. This can aid in curbing overspending and boosting cash flow.

6 Use accoun ing and budge ing sof ware

If hiring a bookkeeper is too expensive, or if you already have one, using software to track receivables and payables, generate invoices, pay bills, and create cash flow statements and other related reports can improve your small business's cash flow management. Technology not only saves time but also saves money by providing the tools to better understand and manage cash flow.

7 Be aware of he shor - erm financing op ions available o you

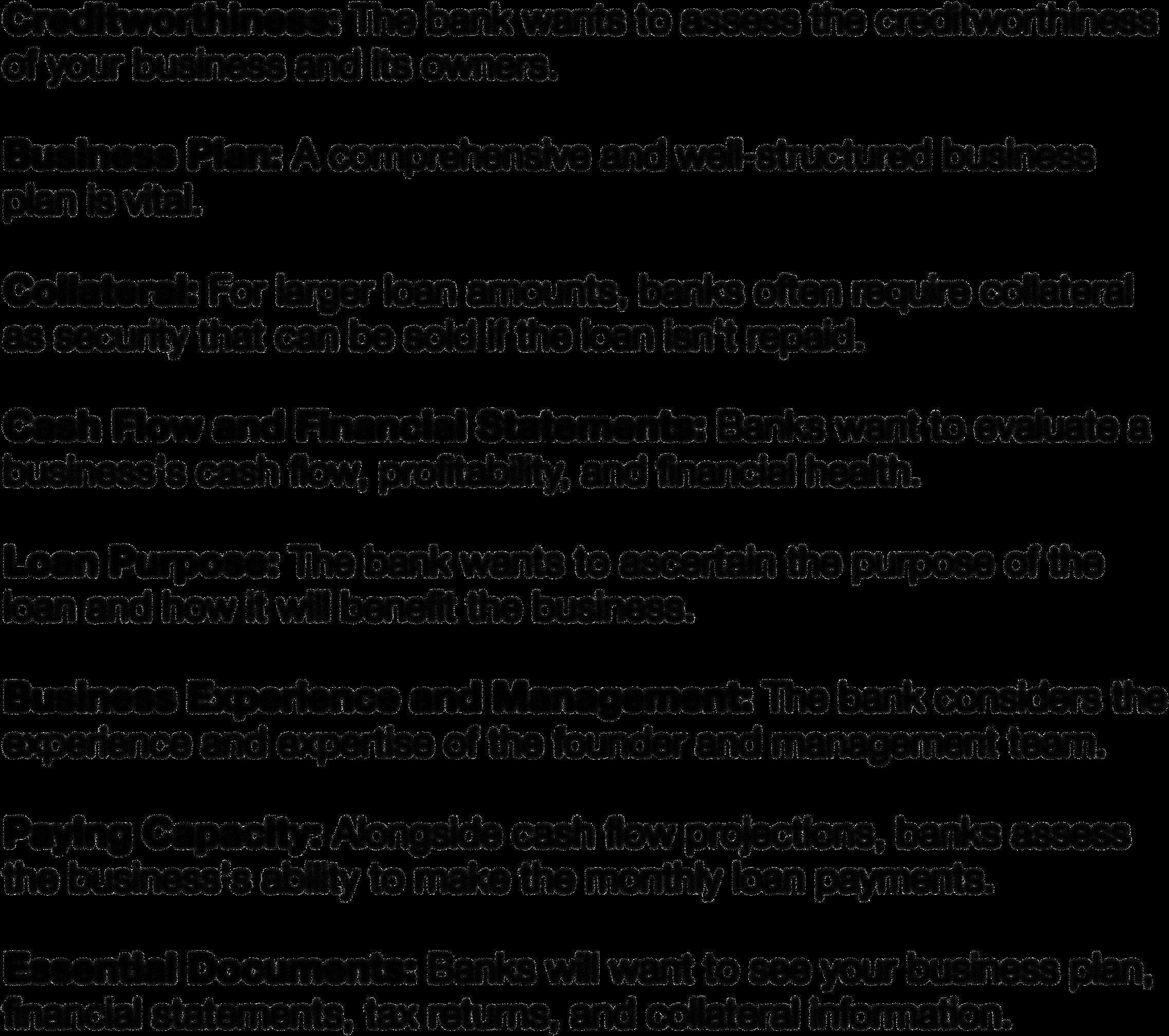

When facing a cash crunch, it's crucial to already know what options are available to you for addressing the cash flow gap. Educate yourself about temporary funding options in advance. Talk to your bank about potential solutions like a revolving line of credit, or a short-term business loan and keep an eye on your credit score so that you'll have access to funding when you need it.

Co sider leasi g vs. purchasi g fixed assets

Consider flexible ways to finance long-term and capital-intensive assets, such as equipment and facilities. Additionally, depending on the market and the stability of your business, you might find it more advantageous to buy real estate and make mortgage payments instead of being tied into a long-term lease. Choosing leasing over purchasing equipment or real estate could help to lower initial costs and improve cash flow.

Increa e price or rates

9. Bootstrap your busi ess as lo g as possible

Maintain a mindset that your business should consistently produce enough operating cash flow to meet its obligations without relying on debt, and base financial decisions on this premise. It can help to imagine that debt is not an option and make cash decisions accordingly.

In the first year of operating a small business, owners may struggle to determine the appropriate pricing for their products or services. Consequently, they often opt to set low prices in order to attract early customers. It is crucial to accurately assess the value of the offerings to customers. It is important to benchmark with competitors and industry standards. It is also essential to test the market and make price adjustments as needed. For instance, a coffee shop could consider increasing the price of one or two high-demand products to gauge the impact on sales.

10. Look for ways to automate processes

Identifying the routines and processes that hinder cash flow in the daily management of a small business can be challenging. Technology often holds the key to boosting productivity. It's important to pinpoint redundant and manual tasks that could be automated or removed, freeing up employees to concentrate on tasks that generate cash flow. or instance, empowering salespeople with data and technology can help them close deals more efficiently and swiftly.

12. U e online payment olutions

Encourage customers to use online payment solutions. Offering multiple payment options can speed up the receipt of funds. Digital payments can be processed and deposited into your account more quickly than traditional methods, improving your cash ow.

SMEs can employ various strategies to enhance cash flow and bolster business expansion.

Managing your Business Cash Flow: Women entrepreneur playbooks

Andiswa Silinga

Founder of Gemini GIS and Environmental Services

www.gges.co.za

Andiswa Silinga is the co-founder of Gemini GIS and Environmental Services in South Africa, established in 2018. She is a leader in the field of geospatial and drone technology. By leveraging these tools, she empowers businesses in mining, construction, and energy sectors to minimize their environmental impact. Her expertise unlocks valuable insights that guide sustainable practices across these industries. A passionate mentor, she actively invests in shaping the next generation of experts in her field.

Andiswa Silinga’s CASH FLOW MANAGEMENT playbook

Insights into how to control cash flow to build a sustainable consulting business. my approach

Consistently attract and retain paying clients to drive cash flow

Find knowledge

The high failure rate of startups, particularly due to cash flow issues, was a concern for us as we launched our consulting practice. Recognizing our lack of business experience, we enrolled in an Enterprise Development (ED) program that equipped us with critical aspects of finance, such as budgeting, cash flow management, financial statements, and data analysis.

Develop your Cash Flow Roadmap

While we explore various pricing models as our business grows, hourly billing currently provides a strong foundation for our cash flow projections. Since income is directly tied to the time spent working on a project, we have a clear picture of the revenue generated throughout the project lifecycle. By factoring in the anticipated costs associated with delivering these projects and business operations, we gain a comprehensive understanding of our projected cash flow. This approach serves as a roadmap for our cash flow, allowing us to anticipate our financial needs and make informed decisions.

Understand how your sales conversion cycle impacts cash flow

We've faced periods of slow client acquisition, which have left a significant dent in our financial health. Initially, we relied heavily on one-off projects. This over-reliance proved detrimental for two reasons. First, the sales conversion cycle can be lengthy, creating long gaps between securing a client and receiving payment. Second, the pressure of completing a large project often diverted our attention from sales and marketing activities.

“The sales conversion cycle can be lengthy, creating long gaps between securing a client and receiving payment.”

Interaction between cash flow, sales, and marketing

Our success depends on the active interaction between cash flow, sales, and marketing. Here's how it works: Consistent sales and marketing efforts attract paying clients, generating a steady stream of cash flow. This cash flow then fuels further investment in marketing, leading to even more client acquisition and, ultimately, even better cash flow. It's a virtuous cycle that ensures the longterm success of our consulting business.

Strategies for taking control of your cash flow

To improve our cash flow, we've adopted a two-pronged approach:

Ideal client profiling using the 70/20/10 model. This framework helps us identify clients who are a good fit for our services, contribute most to our bottom line, and avoid projects unlikely to yield long-term benefits.

As our business grows, we're exploring the potential of value-based pricing. This approach moves us away from hourly billing and allows us to charge based on the specific results and outcomes we achieve for clients.

By combining these strategies, we are taking control of our cash flow and building a sustainable consulting business that thrives on delivering exceptional value to our clients.

“Our success depends on the active interaction between cash flow, sales, and marketing.”

Avoid project gaps that create cash flow disruptions

Invest in accounting software to simplify tracking income and expenses and boost cash flow.

“Keep the project pipeline full. A constant flow of new projects secures consistent income. Avoid project gaps that create cash flow disruptions, making it harder to meet ongoing expenses. Be proactive in finding new opportunities and manage project timelines to keep the momentum going. If you cannot do this yourself, consider hiring a salesperson or marketer to ensure your pipeline stays full.”

Annie Muronda’s Playbook

Key cash flow management hacks for a direct-to-consumer business

Annie

Muronda

Founder of Rufaro Garments

www.rufarogarments.com

Annie Sibindi Muronda is the founder and managing director of Rufaro Garments and has overall executive management responsibility for the company. Under Annie’s leadership, Rufaro Garments has built a vertically integrated end-to-end manufacturing capability supported by the bespoke distribution of uniforms through brick-and-mortar and online outlets. Rufaro Garments has found particular resonance in the burgeoning affordable independent schools market and now provides stylish yet affordable school uniforms to over 40,000 students across South Africa.

my approach

Keep an eye on the future and predict your cash flow needs ahead of time

Beware the hidden risk

Cash flow is a hidden risk for businesses that deliver their products or services before customers can buy them. This risk applies to most direct-to-consumer (D2C) or customerfacing businesses that need to have products on the shelves before customers can buy them. In a perfect world, businesses would receive payment for their products and then use that cash to make and deliver them. However, for most businesses, the pattern is reversed; they have to spend their own money to make the product, pay for distribution of the product, and then hope that a customer will buy and pay for the product.

Compounding this is the uncertainty of when a sale will be made and when payment for that sale will be received. This uncertainty is why cash flow is an essential concept for small businesses. Without available cash, businesses can not afford to deliver their products or services (including paying the staff needed). As a result, they will not have products on the shelf, therefore not generating sales to earn revenue. It can be a vicious cycle.

A key cash flow hack for any business

The first and most important cash flow hack for any business is to choose clients and business models that pay sooner rather than later. Examples include requiring customers to pre-pay for orders or pay a deposit and working with clients who pay as soon as the product is delivered.

“...choose clients and business models that

pay sooner rather than later.”

Price appropriately for delayed payments

Unfortunately, when small businesses service large clients such as corporates or government departments, they often have to accept payment on delayed terms of up to 90 days or more in some cases. These arrangements can be catastrophic to a small business. One way to mitigate this impact is to price appropriately for delayed payments, which includes adding a margin for the cost of working capital needed when payment is delayed.

“...add a margin for the cost of working capital needed when payment is delayed.”

Dealing with late-paying clients

For entrepreneurs dealing with late-paying clients, securing working capital from funders becomes a necessity to bridge the cash flow gap. However, the key to managing this effectively is to be proactive. It's crucial to establish relationships with financiers before the need for working capital arises. By doing so, you can ensure that you're prepared for any cash crunch that may come your way, rather than scrambling for solutions when it's already too late.

“It's crucial to establish relationships with financiers before the need for working capital arises.”

Learn from Annie Muronda’s Playbook

Keep an eye on the future and be proactive

tip one

Negotiate working capital facilities with funders before you need the cash. It will likely be too late when you actually need the money.

tip two

Look forward. Project your cash flow needs into the future and manage them proactively.

Entrepreneur Advice

“Be careful of the big, juicy deal. While large orders or clients may be great for revenue, the resulting cash flow strain may put your business at risk.”

Buhle Magwentshu

Founder of Asmara Coffee

Buhle Magwentshu is the owner of Asmara Coffee in South Africa, which was established in 2018. It is an artisanal micro-roastery with the vision of making quality, artisanal coffee appealing to the palates of coffee connoisseurs and newcomers alike. Buhle completed her Diploma in Food & Nutrition, BTech in Quality Management, and a certificate in Management Development. Before establishing her business, she worked in various entities in both retail and manufacturing (FMCG). In 2023, she opened her first cafe, offering a complete food and beverage experience.

Buhle Magwentshu’S Playbook

Insights on managing cash flow in a business facing currency fluctuations

approach

ake proactive measures by using

forecasting

Developing a clear strategy

We understand how important it is to take proactive measures to minimize the impact of volatile market conditions on our operations. Since we import raw materials, we are susceptible to currency fluctuations. To manage the risks associated with currency fluctuation, we have implemented several key strategies:

1. Negotiating favourable supplier terms

2. Diligent accounts receivable management

3. Strong financial reporting and analysis

4. Strategic production forecasting and lean inventory management

Accurate forecasting is essential for effective cash flow management.

www.asmaracoffee.co.za

Negotiating favourable supplier terms

We have focused on building mutually beneficial relationships with our suppliers and negotiating favourable repayment terms and fixed pricing agreements to reduce the financial impact of fluctuating exchange rates.

Build mutually beneficial relationships with your suppliers and negotiate favourable repayment terms

Diligent accounts receivable management

Our bookkeeper ensures timely invoicing and actively follows up on outstanding payments. We use digital invoicing systems and automated reminders to streamline cash collection processes and optimize cash flow efficiency.

Strong financial reporting and analysis

Our accounting reporting system provides valuable insights into our financial performance, enabling data-informed decision-making and proactive risk management.

Strategic production forecasting and Lean Inventory Management

We use predictive analytics to forecast production needs and maintain minimal stock levels accurately. We follow a "just-in-time" inventory approach to lower carrying costs and minimize inventory obsolescence risks.

Just-in-time inventory management can lower carrying costs and minimize your inventory obsolescence risks.

Learn from Buhle Magwentshu’s

Invoice promptly and manage your receivables

Entrepreneur Advice

tip one

Maintain a robust system for monitoring and optimizing accounts receivable. This involves promptly invoicing customers for goods rendered and diligently following up on overdue payments.

tip two

Use digital invoicing systems and automated reminders to streamline cash collection processes and optimize cash flow efficiency.

“One significant cash flow management pitfall to avoid is underestimating the importance of accurate forecasting. Failure to forecast cash flow effectively can lead to unexpected shortfalls or surpluses, resulting in financial instability and missed opportunities.”

Mahlatse Mamaila

Founder of INO-Biodiesel

www.inobiodiesel.co.za

Mahlatse Mamaila is the founder of INO-Biodiesel and Girl Water and Environmental Science Research, started in South Africa in 2020. As a climate negotiator and International Young Leader, she is passionate about creating change, especially for young girls and boys in rural communities. She works with 20,000 women and youth to promote regenerative agricultural development for food security and a sustainable environment. Mahlatse has received multiple international awards and was nominated for the 2024 EarthShot Prize.

Mahlatse Mamaila’s Playbook

Insights on cash flow management from a green business leader

my approach

Manage and track cash flow continually to stay on track

Understanding our cash flow

In January each year, I develop my annual business action plan, which sets our activities, goals for the year, and the budget for implementing the plan, detailing the estimated expenditure on each product or initiative. Goals to be achieved are set and tracked weekly, monthly, and annually. This action plan helps me to manage and track my cash flow continually. I regularly go back to it to see if we are still on track, or if we may have made a loss, or spent much more than we estimated on a project. If unexpected expenses and losses occur because sometimes things don't go as planned, we need to regularly revisit and update the action plan and cash flow forecast.

“Keep your finances predictable by organising them, using financial tools and reports to monitor your cash flow”

Managing our cash flow

I have an accountant, and it's easy for me to manage my cash flow as I have an accounting background. I use Yoco to manage my payroll, invoices, and cash flow. I continually track the business cash flow using my action plan. I have monthly management account meetings with the accountant to see where we are spending more, and if necessary, we try to cut our costs. This tracking against my action plan helps me to see if I'm running a sustainable business. I need to know if we are making a profit, expanding, or making a loss, or to identify if there's something wrong with what we're doing - we need to figure out what it is and fix it. This approach enables me to ensure that my business is expanding and will continue to be sustainable in the next five to ten years.

“...tracking

against my action plan helps me to see if I'm running a sustainable business.”

Improving our cash flow

We establish good relationships with our customers to ensure good cash flow and on-time payments. Our business model requires a 70% deposit before we proceed with production. This means our customers pay reliably and on time.

We also have a steady customer base and have developed good relationships with them over time, which also ensures reliable payments.

Diversifying our product and service offerings to improve cash flow

We are diversifying our business model to introduce new revenue streams to better manage our cash flow. Previously, we were focused on producing our end-product offerings to customers, but we are now also moving to offer training services, including those for unemployed youth. For example, we will be training 40 unemployed youth in greenfield biofuel manufacturing later this year. We will also be applying the power of digital technology for climate action, and we get carbon credits for every litre of used cooking oil we collect. I check every two weeks to ensure we submit the correct and accurate carbon credits for our cash flow.

A steady customer base with well developed client relationships helps to ensure reliable payments and a predictable cash flow.

Learn from Mahlatse Mamaila’s Playbook

Pay attention to incoming and outgoing money

Entrepreneur Advice

tip one

Keep your finances predictable by organizing them, using financial tools and reports to monitor your cash flow, and helping you to make better financial decisions.

tip two

Always check your accounts to ensure you're on the right track.

“The most critical cash flow management pitfall to avoid is not paying attention to incoming and outgoing money. Failing to create a cash flow forecast, and mismanaging credit are the major causes of cash flow issues.”

Lauren Anderson

Founder of KOA Academy

www.koaacademy.com

Lauren Anderson is the CEO and co-founder of Koa Academy in South Africa, established in 2021. With a diverse background in healthcare and a passion for leadership and effective systems, she has honed her skills in strategic planning, team building, and problem-solving. Her commitment to positively impacting her community has led her to the education sector, where she is leveraging technology and innovative teaching methods to create a dynamic and engaging online school.

Lauren Anderson’s Playbook

Insights

on managing cash flow from an innovator in edu-tech

my approach

Learn to love your business numbers, budgets and cash flow projections

Prior to starting Koa, my background was not in finance, and I had yet to familiarize myself with management reports and the workings of a profit and loss statement. However, my passion for budgets and numbers led me to swiftly assemble a team of individuals with extensive expertise in these areas.

It is crucial for women entrepreneurs to have a proper understanding of their business's financial numbers and to embrace budgeting for several reasons. Importantly, by getting to know your finances, especially your cash flow projections, women entrepreneurs can make smarter decisions that drive the growth and sustainability of their businesses. Understanding the company's financial health empowers them to allocate resources effectively and identify areas for improvement.

“...my background was not in finance, and I had yet to familiarize myself with management reports and the workings of a profit and loss statement.”

Learning 1: Sometimes you need to spend in order to make.

One of my most nerve-wracking cash flow moments was in year one of Koa when our cash runway was very short. We needed to grow our number of students to survive. My natural instinct was to hold tight to our purse, but we had to spend more money on marketing to ensure we got enough enrolments to cover our costs. Knowing when to spend and what to spend it on is crucial. By spending the money early on marketing, I was giving up the cushion that ensured we could cover operational costs for longer. As we took the plunge, I had many sleepless nights, but it paid off! We secured enough enrolments to gain further funding and ultimately reach profitability.

“...by getting to know your finances, especially your cash flow projections, women entrepreneurs can make smarter decisions that drive the growth and sustainability of their businesses.”

Learning 2: Build lean.

We learned how to build our product in a really smart way, never compromising on the things that were important to us, such as high teacher/learner ratio and quality education. However, we designed our initial platform by leveraging existing solutions rather than spending big on custom IT builds. If we had spent exorbitant amounts of money on the tech we use, we would have had a good product but no customers.

“Knowing when to spend and what to spend on is crucial.”

Learning 3: You're only as good as your team.

Having a team of people whose experience I could draw on has been invaluable. Even though I am ultimately responsible, having smart people around me makes me more courageous in my financial decisions.

Learn from Lauren Anderson’s Playbook

Schedule time for managing your cash flow

tip one

Be disciplined: Set time aside in your calendar to review your management report every month, compare your monthly spending to your budget, and ensure you know what is happening with your finances.

tip two

Have excellent accountants: Knowing that your numbers are correct and reliable is essential for making the right decisions.

Entrepreneur Advice

Don't let poor cash flow sneak up on you. Decisions made under financial pressure are often made out of fear. Instead, be proactive and make changes to the company or look for funding before you get to the point where you are desperate.

Cash in the bank puts you in a more powerful position to negotiate.

Mamela Luthuli’s Playbook

Insights on managing cash flow from an innovative IT solutions provider my approach

Make cash flow management a cornerstone of your business success

Mamela Luthuli

Founder of Take Note IT

www.takenoteit.com

Mamela Luthuli is the founder and CEO of Take Note IT in South Africa, providing cyber security and innovative IT solutions since 2007. She has made significant contributions to South Africa’s cyber security and IoT industries, including establishing the Cyber Excellence Academy to train young, highly-skilled cyber security employees. Through her work, she aims to create opportunities for marginalized and disadvantaged women and young leaders of tomorrow.

Managing cash flow effectively has been a cornerstone of Take Note IT's success. As a female CEO and entrepreneur, I have navigated various challenges to ensure that our small business operates efficiently and sustainably. Here are some key strategies and experiences that have shaped our approach to cash flow management.

1. Implementing Financial Controls

During the early stages of Take Note IT, one of our main focuses was establishing strong financial controls. We achieved this by putting in place a thorough accounting system to track every transaction meticulously. Regular financial audits and detailed record-keeping became standard practices. These controls gave us a clear understanding of our financial position, enabling us to make well-informed decisions and promptly rectify any discrepancies.

“I have been intentional about communicating my vision and mission through consistency in how we serve our employees, communities, and clients.”

2. Emphasizing Cost-Effectiveness

To maximize our resources, we adopted a three-quote system for significant purchases. This approach involved soliciting quotes from at least three suppliers before purchasing. It allowed us to negotiate better deals and ensured we were not overpaying for goods and services. This practice not only helped in reducing costs but also fostered a culture of fiscal responsibility within the business.

Implementing a detailed costing process helps to set realistic budgets and avoid unexpected financial shortfalls

3. Leveraging Consultants

Hiring full-time staff for every need was not feasible for a small business like ours. Instead, we strategically utilized external consultants for specialized tasks. This approach proved to be cost-effective and efficient. Consultants brought in the necessary expertise without the long-term financial commitment of permanent hires, allowing us to manage our budget more effectively.

4. Accurate Project Costing

One of our early challenges was accurately estimating project costs. Underestimating expenses led to budget overruns and cash flow issues. To address this, we developed a meticulous project costing system. Each project underwent thorough analysis to identify all potential expenses, from labour to materials. This detailed costing process helped us set realistic budgets and avoid unexpected financial shortfalls.

5. Negotiating Supplier Payment Terms

Maintaining a healthy cash flow requires strategic management of our payables. We negotiated favourable payment terms with our suppliers, extending payment periods where possible. This strategy allowed us to hold onto our cash longer, providing more flexibility in managing our finances. In some cases, we also secured early payment discounts, further enhancing our cash flow.

6. Forming Strategic Partnerships

Collaboration has been critical to our growth strategy. We formed strategic partnerships with other small businesses to share resources and reduce costs. These partnerships provided mutual benefits, such as bulk purchasing discounts and shared marketing expenses, which helped us manage our cash flow more effectively.

7. Focused Financial Planning

Detailed financial planning and budgeting have been integral to our success. We regularly review our financial performance and adjust our budgets as needed. This proactive approach ensures that we are prepared for any financial challenges that may arise. Additionally, we maintain a cash reserve to cover unexpected expenses, which has proven invaluable during times of uncertainty.

”Maintaining a healthy cash flow requires strategic management of our payables. We negotiated favourable payment terms with our suppliers, extending payment periods where possible”

Forecast your cash flow to anticipate shortages

tip one

Regularly review cash flow statements to identify and address potential issues early.

tip two

Maintain a cash reserve to manage unexpected expenses without disrupting operations.

Advice

Avoid neglecting cash flow projections. Many entrepreneurs focus solely on profit and loss, overlooking cash flow forecasts. This can lead to liquidity issues, even if the business is profitable on paper. Always forecast your cash flow to anticipate shortages and plan accordingly.

Entrepreneur

Mapholo

Ratau

Founder of Ledikana Creations (Pty) Ltd

www.ledikana.com

Mapholo Magapatona-Ratau is the founder, managing director and designer of Ledikana, a lifestyle brand established in Johannesburg, South Africa, in 2014. It specialises in the manufacturing and retailing of contemporary readyto-wear African clothing and corporate gifting, including Golf wear and accessories targeted at tourists, locals, business travellers, tenants and corporations in and around OR Tambo International Airport and Melrose Arch, where its retail businesses operate. Before her career as an entrepreneur in the fashion industry, Mapholo worked in the financial sector.

Mapholo Ratau’s Playbook

Insights on managing cash flow from a prominent lifestyle brand builder

my approach

Entrepreneurship and money management have been part of my life for as long as I can remember. From early childhood, I helped my parents with their businesses, and my various side hustles have prepared me to become the owner of a formal, established business.

I took control of my company's cash flow from inception. By checking my bank statements every week, I can create realistic budgets, make projections and identify challenges. This money management approach allowed me to identify opportunities and threats as early as possible, enabling the business to operate proactively rather than being reactive. With the onset and continuation of the challenges presented by COVID-19, my business, like many other businesses, suffered, and I developed a phobia of money and cash flow. .

Develop a money management approach that allows you to identify opportunities and threats as early as possible

This resulted in me avoiding scrutinising the health of my cash flow and bank balances. I had to call myself out, transform my thinking and overcome my financial fears. With the help of my coaches and mentors, I started rechecking the bank statements, tracking my income and expenses, and evaluating these against business practices, sales, and stock. Whether the cash flow was trending positively or negatively, I captured and recorded all the data accurately in Excel.

“...a small

business owner must fully understand all aspects of their business, including statutory accountability, invoicing, declarations, and payroll.”

Doing this consistently allowed me to forecast current, future and expected cash flow against income and expenditure. By disciplining and educating myself in this manner, I managed to overcome my financial fears and learned to understand the monthly operating expenses, and the gross and net income of my business. Small business owners generally and commonly believe that, as entrepreneurs, they should lean on financial professionals to manage their finances. While this is always helpful, a small business owner must fully understand all aspects of their business, including statutory accountability, invoicing, declarations, and payroll.

As such, I invested in training to get myself proficient in our accounting system. This skill set helped me to be better at tracking my cash flow. It was incredibly helpful in making me aware of unnecessary expenses, reviewing insurance policies and cellphone contracts and closing unnecessary bank accounts that attracted unwanted and excessive fees. It also assisted us in invoicing clients quickly and exporting all expenses and income directly onto the balance sheet and general ledger. We implemented a set of debt collection policies regulating how we follow up and collect on overdue payments, and changed our payment terms to benefit clients.

Finally, I realised that, to keep my business financially sound, the business practices needed to be continuously monitored and managed and, if need be, changed.

“I took control of my company's cash flow from inception. By checking my bank statements every week, I can create realistic budgets, make projections and identify challenges.”

Learn from Mapholo Ratau’s Playbook

Stay on top of your finances and become money-savvy

tip one

Be in control and stay on top of your finances.

Schedule a regular time weekly to check your bank statements. Evaluate your cash flow and become money-savvy.

tip two

Learn everything you can and develop yourself to become an effective businesswoman.

Entrepreneur Advice

“Schedule time for forecasting and planning. Neglecting to forecast and plan for irregular fluctuations in revenue and cash flow can lead to high financial strain in the business.”

Margaret Hirsch

Executive Director of Hirsch’s Group

www.hirschs.co.za

Margaret Hirsch is the Executive Director of Hirsch’s Group, the largest independently owned appliance and electronics retail outlet in Southern Africa, now in its 45th year. Margaret oversees the day-to-day operations of all Hirsch’s stores and their concept stores. The Hirsch’s story is one of constant expansion and success. Margaret has been recognised with many international and local awards for her business, social, and charitable work, uplifting communities nationwide.

Margaret Hirsch’s Playbook

Insights on managing cash flow from an award-winning woman entrepreneur

Keep ploughing profits back into the business

It's important to reinvest any profits back into the business immediately. This practice helps in developing budgeting skills and an appreciation for the value of money. After getting your business started and reinvesting profits for at least five years without spending on unnecessary items, such as new vehicles, for instance, you should continue reinvesting the money until you have built a strong financial foundation and a solid cash flow.

Reinvest profits until you have built a strong financial foundation and a solid cash flow for the business.

Think ahead

At Hirsch's, we looked at our expenses and saw that our most significant expense was our rent. What could we do to avoid this? The obvious answer was to buy our own properties, pay them off, and then we wouldn't have the burden of rent. This is precisely what we did. How did we start? We saved R100 a month to buy a small property, which we then improved upon, sold, and bought a better property, and so it went on. Today, we have millions of Rands worth of properties in our portfolio. It's important to start small and only borrow money when you absolutely need it and pay it back as quickly as you possibly can. If there is a need to borrow money for something essential that will improve the business and make it work quicker, smarter, and faster, make sure that you don't over-extend and also make sure that you pay the money back as quickly as you can.

“...make sure that you don't over-extend and also

make sure that you pay the money back as quickly as you can.”

Make sure your product is marketable

Work on solving a customer's problem, and if you have an amazing product or service, be sure that the customers want that product or that problem solved. Many businesses close down so quickly because they have wonderful products, but nobody really wants them. Your product or service has to be something that the consumer is definitely looking for and one that solves a problem in their lives. Product and service sales mean cash flow.

“Start small, and reinvest your profit. This is the way to grow sustainably.”

Develop an online presence

A strong online presence is needed as everyone does their research online. Always remember the best and cheapest way of marketing is word of mouth. Nothing is more powerful than a testimonial from a happy customer. Constantly think of ways to ensure that your customers are happy. At Hirsch's, our mission is to have happy customers who return often. Turn your happy customers into sales, which in turn, means cash flow.

Learn from Margaret Hirsch’s Playbook

Keep ploughing that profit back

tip one

Start where you are today with what you have.

tip two

Keep ploughing that profit back.

Entrepreneur Advice

“Start by yourself and when the workload becomes too much, get one employee, and then as the business builds and you can afford more, take people in one at a time. Teach each one yourself and ensure their values are the same as yours - let them learn your culture. Always make sure that you keep making a profit and that you keep ploughing that profit back.”

Mauricia

Cox

Founder of Wellchemco

www.wellchemco.co.za

Mauricia Cox is the founder of WELLCHEMCO in South Africa, established in 2023. She is an engineer who has dedicated her career to water and wastewater treatment. She founded WELLCHEMCO to develop cosmetics that have minimal impact on our water sources, helping to protect the environment for future generations, and as a platform dedicated to championing holistic wellness by integrating wellness and beauty. WELLCHEMCO empowers women to radiate from the inside out.

Mauricia Cox’s Playbook Insights on managing cash flow from an eco-friendly beauty brand builder

Build a cash reserve to help manage irregular cash flow needs

Managing cash flow effectively is crucial for the stability and growth of any business.

I have implemented the practices below, and I hope businesses can maintain healthy cash flow by undertaking some of the following:

Budgeting

I regularly create cash flow forecasts to anticipate future cash inflows and outflows. This allows me to plan for upcoming expenses and understand when to expect revenue. I consistently document and prioritise all my fixed expenses in my budgeting process. I continuously revisit my budgets and adjust them as needed to reflect any change in my business conditions.

Monitoring

I monitor cash flow by frequently reviewing financial statements, cash flow statements, and bank balances. This helps me identify missed payments early, allowing for timely corrective actions and ensuring an accurate depiction of cash flow at the end of each month.

Efficiency

Ensure your cash flow tracking process is efficient. I initially set up Excel spreadsheet templates to uniformly track and monitor sales, revenue, and fixed expenses. This approach enhanced efficiency and minimised errors.

Expense Management

I manage my expenses by distinguishing between essential and non-essential spending, including fixed monthly expenses and occasional advertising and marketing costs. I regularly review my expenses and cut costs when business conditions require it, ensuring no compromise in product quality.

Maintaining Reserves

I learned this the very hard way! Build and maintain a cash reserve! This is important to cover unexpected expenses or downturns in business. All businesses undergo periods of low sales or downturns, and this will act as a buffer to provide financial stability that will allow you to pay fixed expenses incurred during periods of low sales.

Relationships

Businesses thrive on relationships. By paying your expenses on time, you can negotiate favourable payment terms with suppliers and service providers. Leverage business-to-business rates and maintain open, honest communication with your suppliers and service providers.

Financing Options

I began my journey by self-funding, as my business couldn't handle repayment obligations initially. I encourage new business owners to explore various financing options, such as lines of credit, loans, or investments, to manage cash flow gaps. However, use financing wisely to support growth without over-leveraging, ensuring your business can meet repayment terms. This requires a solid financial plan.

Inventory Management

My business relies on inventory for product sales, so I optimise inventory levels by minimising waste, streamlining processes, and maintaining low stock levels without risking stockouts. Additionally, I built strong supplier relationships to negotiate better terms, such as shorter lead times and bulk purchase discounts.

Cash Flow Statements

Regularly, I prepare and review cash flow statements using Excel to track the movement of cash in and out of the business. This practice offers insights into operational efficiency, revenue, expenses, and sales, highlighting areas or products needing attention. Additionally, it aids in determining the necessary marketing strategies.

Technology and Automation

Many accounting software tools are available to automate cash flow management, increasing accuracy, saving time, and providing real-time financial insights. By linking to your bank account and sales channels, these tools automatically track cash flow, minimising human error.

Learn from Mauricia Cox’s Playbook

Know your industry and your numbers

tip one

Keeping a cash reserve is my number one cash flow management recommendation. Creating and keeping that buffer makes sure you can pay your debts even when your business isn't making as much money as projected. It also helps you deal with unforeseen expenses and downturns.

tip two

Monitoring cash flow allows you to be proactive, to plan for fixed and variable expenses, and identifying potential shortfalls early.

Entrepreneur Advice

“The worst mistake in cash flow management is not taking all costs into account, especially those that happen occasionally. Ignoring these expenses can cause unforeseen deficits and jeopardise your financial security. To guarantee thorough and precise budgeting, always include both fixed and variable expenses in your cash flow planning.”

Michele

Carelse’s Playbook Insights

on managing cash flow from a natural health brand builder

my approach

Maintain a culture of financial discipline in the company

Michele Carelse

Founder of Feelgood Health

www.feelgoodhealth.co.za

Michele Carelse is the founder of Feelgood Health, a South African plantbased, natural health company founded in 2000. We focus on 100% natural medicines, essential oils and 'food as medicine' products for the whole family, including the family pet. Our mission is to make natural health alternatives readily available to everyone and do so sustainably. Our products may be bought online, in health shops, pharmacies, retail stores and vet shops.

Cash flow is at the heart of every business, especially a growing business. In fact, the faster a business grows, the more challenging cash flow becomes! While it may feel great to have orders rolling in, it can become very stressful when the time comes to pay expenses when you have not yet been paid for these orders! As a multi-channel natural health business, cash flow management is a finely tuned balancing act! For a company with both wholesale and retail channels, as well as a presence on 3rd Party platforms like Amazon and Takealot, managing cash flow can be a constant tightrope walk! Here are some insights and strategies that have helped me maintain a healthy financial pulse!

“I rely heavily on an annual budget as well as monthly budgets to help forecast upcoming expenses and potential shortfalls. This gives me the opportunity and time to 'make a plan'”

1. Understand your business’s cash flow cycle

There is an inherent difference in cash flow between wholesale and retail.

While wholesale transactions often involve longer payment terms, retail sales can provide ready cash to bridge the gaps. I have learnt to use this to my advantage by adopting the following strategies:

Negotiate the most favourable payment terms with wholesale customers, as well as suppliers.

Make sure wholesale customers pay within the agreed-upon terms and follow up closely when they don't.

In certain cases, we offer payment incentives for early payment, which can really benefit us and our customers.

2. Stock management

Inventory and order fulfilment management is very important

With more than 500 products, Feelgood Health needs an accurate inventory management system to avoid overstocking or stock outages.

Overstocking ties up cash and means more resources are used (e.g., warehouse space), while stock outages affect sales. We keep a close eye on historical sales and seasonal fluctuations and try to make sure that our inventory is streamlined to accommodate this.

3. The importance of planning and budgeting

I rely heavily on an annual budget as well as monthly budgets to help forecast upcoming expenses and potential shortfalls. This gives me the opportunity and time to 'make a plan', rather than being caught short with unexpected expenses!

4. Investigate your cash flow financing options

Consider establishing a line of credit with a reputable financial institution and use this wisely (credit is expensive!). This can provide a safety net for unexpected cash flow fluctuations and can be a real lifesaver when there is a sudden spike of orders that need to be financed. You should consider approaching your bank for an overdraft or using one of the reputable business financing companies

5. Stay on top of your numbers

Most important is to stay on top of your numbers and to maintain a culture of financial discipline in the company, always minimising unnecessary expenses and exploring cost saving measures. Although it is not always possible, try to keep a cash flow buffer when sales are up and expenses are down – this will serve you well in months when things are the other way around!

“A financial advisor can save you time - instead of the long and tedious research exercise on how to handle certain matters, you can delegate while focusing on other aspects of the business.”

Learn from Michele Carelse’s Playbook

Give

yourself the opportunity and time to be proactive

tip one

Know your numbers! Look at historical sales and expenses and try to be prepared for them.

tip two

Negotiate the most favourable payment terms possible with your suppliers.

Entrepreneur Advice

“'Flying blind' when it comes to cash flow can result in disaster. Always keep on top of cash flow and give yourself the opportunity and time to be proactive when there are problems, rather than exposing yourself to nasty surprises!”

Nneile

Nkholise

Founder of Thola

www.getthola.com

Nneile Nkholise is the co-founder of Thola Inc. in South Africa and the U.S., established in 2021. She studied BSc Physics at the University of Witwatersrand and Mechanical Engineering at the Central University of Technology. Before founding Thola, she founded a FemTech company called iMed Tech and worked as a project engineer in the construction sector. She is passionate about climate change and helping communities become climate resilient. She is equally passionate about football and has devoted her life to supporting amateur football development in rural communities.

Nneile Nkholise’s

playbook

Insights on managing cash flow from

an agri-tech business leader

my approach

Ensure your cash on hand can provide at least a 6 months runway

My primary role as CEO is to ensure our company's financial health. I have achieved financial health by building automated CRM tools that enable me to track every cent that comes in and leaves. Having financial data analytics systems in place that provide snapshots of cash flow and tie our cash flow to projects/activities happening in our company also helps me.

“ ...it's important to fully understand every activity happening in the company and be able to forecast the impact of each activity on the company's bottom line.”

As a CEO working in a tech company, it's important to fully understand every activity happening in the company and be able to forecast the impact of each activity on the company's bottom line. When our team decides to build and launch a product feature, I need to develop a financial forecast framework which accounts for the development cost, the customer acquisition costs (to get customers to use that specific feature), the marketing costs of that feature, and the customer support costs.

“We constantly revisit the budget we have committed to...”

I created a monthly cashflow projection and budget for the business. The budget is incorporated into our financial management system and helps us to check if we are on track or overspending. We constantly revisit the budget we have committed to, ensuring that all key fixed and operating expenses are taken care of before spending on unplanned activities, and I track our cash flow.

Equally, the financial returns we will make from customers using and paying for that feature. The goal is always keeping the profit margins at 50% and above. In our work environment, the reality is that it may take time before a company has a healthy cash flow because software product adoption takes time before a company hits hockey-stick growth. Hence, having a good understanding of the internal functions of my company would be helpful. Also, I have a solid understanding of our market dynamics, such as knowing or forecasting risks in the market that could affect cash flow such as interest rate increases, inflation, political instabilities, etc.

“...I have a solid understanding of our market dynamics, such as knowing or forecasting risks in the market that could affect cash flow such as interest rate increases, inflation, political instabilities, etc.”

Learn from Nneile Nkholise’s

Have cash on hand to provide a 6 months runway

Entrepreneur Advice

tip one

Build good CRM tools that easily help you track your cash flow frequently.

tip two

Keep in touch with local and global macroeconomic dynamics (e.g. recession) that could affect your cash flow.

“At any given time in your company, always ensure your cash on hand can provide at least a 6 months runway. If not, then make some cuts in your company so that you have cash on hand for 6 months.”

Phumzile Khoza’s Playbook

Insights on managing cash flow from the founder of a township-based business

my approach

We stay focused, adaptable, and resilient, positioning us for success in our sustainable, township-based business

Phumzile Khoza

Founder of Lathitha-Biodiesel

www.lathitharecycled.co.za

Phumzile Khoza is the founder of Lathitha Biodiesel in South Africa. The company was established in 2020 during the lockdown but only got formally registered in 2021. Phumzile has a passion for entrepreneurship and, as a result, has no formal employment background. With beauty and lifestyle experience dating back to her early teens, Lathitha Biodiesel proves that you can achieve your dreams despite feeling scared.

Managing cash flow presents unique challenges as a female entrepreneur in the maledominated biodiesel industry. Here's how we've effectively navigated these challenges, particularly given my lack of previous employment background.

Understand Your Cash Flow Cycle

We start by understanding the cash flow cycle of our biodiesel business. This involves identifying when money comes in from sales, investments, etc. and when it goes out for raw materials, salaries, utilities, etc. Understanding this cycle helps us anticipate periods of surplus and shortage.

“...we can effectively manage cash flow as female entrepreneurs in the biodiesel industry, even without previous employment background. We stay focused, adaptable, and resilient”

Create a Detailed Budget

We develop a comprehensive budget outlining all our expenses and revenues, including fixed costs (like rent, salaries, and utilities) and variable costs (like raw materials and transportation). Our budget is realistic and accounts for market fluctuations and seasonal changes in demand.

Monitor Your Expenses Closely