SFDR IMPACT ANALYSIS

A Comprehensive Review of ESG Integration in Europe

IRELAND EDITION

maples.com/esg

3 5 6

8

Introduction

SFDR – At a Glance

Our ESG Advisory Group

ESG Integration in Ireland

Analysis of Article 8 Funds

Analysis of Article 9 Funds

Are Managers Considering Principal Adverse Impacts?

SFDR Website Disclosures

SFDR Implications for Third Party Managers

SFDR - Impact on EEA Fund Distribution

Key Trends for Sustainable Investing

2 | Maples Group

About the Authors 10 12 14 15 16 18 20 22

CONTENTS

INTRODUCTION

SFDR has been in place since March 2021, however it only became fully effective on 1 January 2023. As such it is an opportune time to assess how it has affected the European asset management landscape.

SFDR has had a significant impact on the European funds space. Assets in European sustainablefocused funds currently stand at over €4.6 trillion¹. The aim of this SFDR Impact Analysis is to provide asset managers with a practically focused assessment on the current state of ESG integration in Europe, as well as valuable insights as to how it is likely to evolve in the future. This SFDR Impact Analysis is also designed to assist asset managers considering establishing a European domiciled fund or marketing a fund in Europe, by identifying how SFDR is impacting such fund launches and providing a guide on navigating the SFDR requirements as well as peer analysis on approaches taken to date.

The impact of SFDR is most pronounced in the retail / UCITS space, principally driven by a combination of investor sentiment, regulatory requirements and traditional distribution channels, all of which we examine in this analysis. While the number of sustainably-focused alternative investment funds is significantly lower, that number is growing, particularly since the Investment Limited Partnership regime has been enhanced, which we examine in this analysis.

About this SFDR Impact Analysis

For the purposes of this first edition of our SFDR Impact Analysis, we have specifically focused on ESG integration in Ireland. In particular, on the 6,443 Irish domiciled active funds identified in the Monterey Insight Ireland Fund Report 2022 (“Monterey Ireland Report”). These 6,443 Irish domiciled active funds form the market sample for our statistical analysis. In addition to the Monterey Ireland Report, we have also used publically available SFDR disclosures, and sought to rely on relevant third party ESG data. We intend to expand our review to cover Luxembourg domiciled funds in the second edition of our SFDR Impact Analysis, which will be published in Q4 2023.

¹ Source: Morningstar Q4 2022 in Review.

This significant sample size (6,443 active funds), coupled with available data has enabled us to clearly understand the current state of play of ESG integration, as well as identify noticeable trends developing in the European sustainable space.

Market Leader

The Maples Group is a leading international service provider offering clients a comprehensive range of legal services on the laws of Ireland, Jersey, Luxembourg, the British Virgin Islands and the Cayman Islands, and is an independent provider of fiduciary, fund services, regulatory and compliance, and entity formation and management services.

SFDR Impact Analysis | 3

The aim of this SFDR Impact Analysis is to provide asset managers with a practically focused assessment on the current state of ESG integration in Europe.

In Ireland, the Maples Group is the market-leading legal adviser to Irish-serviced funds having advised on 1,470 funds in 2022², and maintained this position for 10 consecutive years. As we have acted on the greatest volume of Irish funds for such a sustained period, our teams have a more rounded exposure to what is happening at the cutting edge of the Irish asset management market which enables us to track all relevant information and statistics on new product trends and innovative fund structuring.

In an ESG and sustainable finance context, this provides us with an unparalleled overview of how managers have responded to the introduction of SFDR and the greater demand for investments with strong ESG credentials.

Ireland - Sustainable Finance Fund Domicile

Ireland is the second largest funds domicile in the EU. Net assets in Irish domiciled funds reached €3.7 trillion in 2022, with €90 billion in net sales³ . 17 of the top 20 global asset managers have Irish domiciled funds. Ireland is a major hub for distribution, with Irish funds being sold / distributed in over 90 countries globally. Ireland is also the leading domicile for exchange traded funds (“ETFs”), representing over 67% of the total European ETF market. Ireland recently established its International Sustainable Finance Centre of Excellence, the aim of which is to become an international hub from which the finance industry in Ireland will develop its response to sustainability demands and deliver on Ireland’s net zero transition.

About Monterey

Monterey Insight is a leading independent fund industry research company that provides the only comprehensive report of service providers for all investment funds serviced in UK, Luxembourg, Ireland, Jersey and Guernsey. The Monterey Ireland Report includes only active funds, i.e. it excludes from consideration funds which are in termination, as well as unlaunched / unseeded funds.

4 | Maples Group

² Source: Monterey Insight Ireland Fund Report 2022. ³ Source: Central Bank of Ireland data, as of 31 December 2022.

Ireland is the second largest funds domicile in the EU and has over 1,400 sustainability focused funds.

SFDR - AT A GLANCE

WHAT IS IT?

SFDR seeks to establish a harmonised approach on sustainability-related disclosures provided to investors domiciled within the EU. Broadly speaking, SFDR imposes sustainability related disclosure and transparency obligations on both the asset manager (i.e. at the entity level) and on the fund which it manages (i.e. at the product level).

WHO IS IN SCOPE?

SFDR applies to asset managers (and investment advisers) domiciled or operating in the EU, who are managing or distributing funds to European investors.

DOES IT APPLY TO NON-EU ASSET MANAGERS?

Yes, if those non-EU asset managers are managing EU funds or marketing non-EU funds via national private placement regimes in the EEA they will be required to comply with SFDR.

WHAT DOES IT REQUIRE?

SFDR requires asset managers to provide more transparency on how they integrate sustainability risks into their investment decisions and the consideration of how principal adverse sustainability impacts into the investment process.

DOES SFDR HAVE CATEGORIES OF SUSTAINABLE PRODUCTS?

Yes, SFDR identifies three types of funds and distinguishes between them depending on the extent of environmental, social and governance ("ESG") integration. The three types being colloquially known as an Article 6 fund, an Article 8 fund and an Article 9 fund

WHAT IS AN ARTICLE 6 FUND?

A fund that either does or does not integrate the consideration of sustainability risks into its investment decision making process.

WHAT IS AN ARTICLE 8 FUND?

A fund that promotes environmental or social characteristics, investing in companies which follow good governance practices.

WHAT IS AN ARTICLE 9 FUND?

A fund that has a sustainable investment objective.

WHAT IS A SUSTAINABLE INVESTMENT UNDER SFDR?

It is an investment that contributes towards an environmental or social objective chosen for, or characteristics promoted by, your fund, provided that (i) the activities of that investment do no significant harm ("DNSH") to such environmental or social objectives / characteristics; and (ii) that investment follows good governance practices.

Determining what is deemed a sustainable investment is subjective; asset managers are afforded absolute discretion in designing their own framework to assess if an investment qualifies as sustainable.

WHAT ARE THE MIFID SUSTAINABILITY PREFERENCES?

EU based distributors must assess an investment's suitability for retail investors. Within that assessment is a requirement to establish that investor's sustainability preferences. Distributors can only make investment recommendations based on alignment with that investor's sustainability preferences.

WHAT DOES TAXONOMY-ALIGNED MEAN?

The Taxonomy Regulation establishes a framework to classify environmentally sustainable economic activities (otherwise known as Taxonomy-aligned) by setting harmonised criteria for determining whether an economic activity qualifies as environmentally sustainable.

WHAT ARE PRINCIPAL ADVERSE IMPACTS?

Principal adverse impacts ("PAIs") and sustainability risks are interrelated though different concepts. The concept of PAI intends to capture the impact of investment decisions that results in negative effects on sustainability factors.

WHERE DO I MAKE THE SUSTAINABILITY RELATED DISCLOSURES?

Asset managers managing or distributing Article 8 or Article 9 funds must make sustainability related disclosures in its (i) fund prospectus; (ii) website; and (iii) periodic reports.

SFDR Impact Analysis | 5

OUR ESG ADVISORY GROUP

Our ESG Advisory Group is a dedicated, multi-disciplinary team of ESG and sustainable finance experts drawn from our Funds & Investment Management, Finance, Banking, Corporate, Real Estate and Dispute Resolution teams. Our global footprint ensures that we have exposure to ESG trends and sustainable finance developments. It also enables us to draw on the experiences and expertise of the entire Maples Group, to develop a uniform and consistent approach to ESG initiatives for our global clients.

Our ESG Advisory Group continually engages with governments, regulators and industry associations, in many of the jurisdictions in which we operate, to help shape the financial services industry’s response to developments in ESG and sustainable finance regulation.

ESG Integration in Europe

A number of years ago we recognised the importance that ESG and sustainable finance would have for asset managers operating within the EU. Our European ESG team is highly focused on the impact of the EU’s Sustainable Finance Action Plan for the European asset management sector, in particular, the impact of SFDR and the Taxonomy Regulation.

We can quickly evaluate how an EU regulatory requirement is being treated under both Irish and Luxembourg law, as well as compare and contrast positions taken by the CSSF and the Central Bank of Ireland on a specific ESG or sustainable finance issue.

Our ESG Advisory Group proactively collaborates with external stakeholders operating in the European sustainability space and has co-authored with the Frankfurt School of Finance and Management and the Environmental Liability Solutions Europe Ltd a Do No Significant Harm Handbook , to assist asset managers to identify good practices and provide guidance on the evaluation and reporting of the ‘Do No Significant Harm’ principle under SFDR.

How We Can Help

We have collaborated with leading global asset managers and institutional investors operating in the EU to develop end-to-end SFDR compliance solutions at both the operational level within the asset manager and at the underlying fund / financial product level.

Our ESG specialists can audit policies and procedures to identify those affected by SFDR, and best advise how those policies can be enhanced to integrate the consideration of sustainability risks into the investment decision-making process and overall risk framework.

At the underlying fund / financial product level, we can assist with SFDR financial product analysis, including undertaking a full review of all offering documents and marketing collateral to assist with the determination of SFDR product categorisations, as well as helping prepare Article 8 and Article 9 pre-contractual disclosures, website and periodic disclosures.

The Maples Group also offers a range of other ESG solutions to support our clients including ESG data and reporting, fund and manager ESG certification and the Maples ESG Platform is designed to support the operational and compliance requirements of SFDRcompliant Article 8 or 9 funds. For further details see below in the section entitled Maples ESG Platform

6 | Maples Group

The Maples Group is fully committed to the goals and initiatives of sustainability. We are highly focused on the impact that ESG and responsible investment will have on the financial services sector.

LEARN MORE - maples.com/esg

Our ESG Advisory Group is a dedicated, multi-disciplinary team of sustainable finance experts. Our global footprint ensures that we have exposure to ESG trends and sustainable finance developments.

SFDR Impact Analysis | 7

ESG INTEGRATION IN IRELAND

Ireland is committed to the European Green Deal, a framework to facilitate the public and private funding needed for a transition to a climate-neutral, green, competitive and inclusive European economy. Ireland is recognised as an international hub at the forefront of addressing sustainability demands and delivering on net zero transition.

Overview of the Irish Market

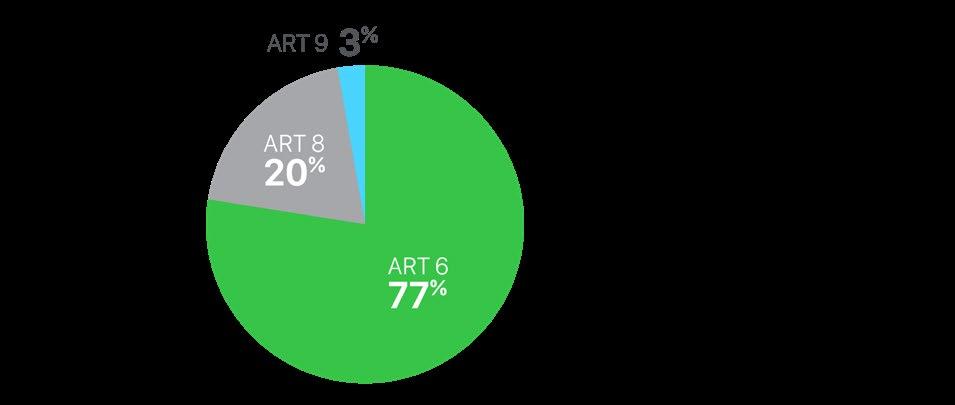

Of the 6,443 Irish domiciled funds forming our market sample, the vast majority are categorised as Article 6 funds (77%), with sustainability focused funds (e.g. those funds categorised as either an Article 8 fund or an Article 9 fund) accounting for the remaining 23%.

This dominance of Article 6 funds does not mean that the level of overall ESG integration is low. Managers of Article 6 funds are considering ESG and sustainability factors in their investment process. EU regulated managers are now legally required to consider ESG factors alongside other traditional factors as part of the overall investment decision making process.

So while consideration of ESG factors may not be determinative now in the investment selection process, with the growing acceptance that ESG integration has an impact in driving positive investment returns for investors, we expect this to change over time.

Retail Dominance

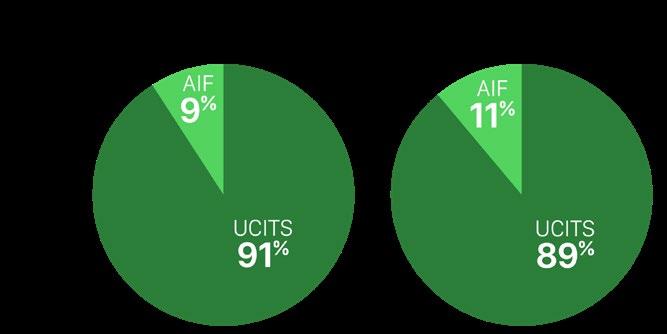

The preference for establishing sustainability focused funds as UCITS is pronounced. In both the case of Article 8 funds and Article 9 funds, approximately 90% of those funds are structured as UCITS.

ARTICLE 8

ARTICLE 9

The dominant position of Article 6 funds is not surprising. The Article 6 categorisation is effectively the default position, and given SFDR only became fully effective in January 2023 (with the final text only agreed immediately prior thereto), large numbers of asset managers took a wait and see approach (before considering categorising their funds as either Article 8 or Article 9 funds).

8 | Maples Group

SFDR FUND CATEGORISATION BY NUMBER OF IRISH FUNDS

This has been driven by both genuine investor preference for sustainability focused products as well as the traditional UCITS distribution channels demanding them. Before being able to sell a fund to an investor, EU based distributors must assess that investment's suitability for that retail investor, and included within that assessment is a requirement to establish that investor's sustainability preferences. Distributors will then have to make investment recommendations based on these sustainability preferences. As a direct result of these requirements, distributors are now seeking more sustainability focused funds from product manufacturers. We explore the impact of these sustainability preferences on the product design in the Analysis of Article 8 Funds and Analysis of Article 9 Funds sections below.

There is no general requirement to establish a professional investor's sustainability preferences, hence the demand for sustainability focused products in that space is lessened.

Article 8 Funds – Upwardly Mobile

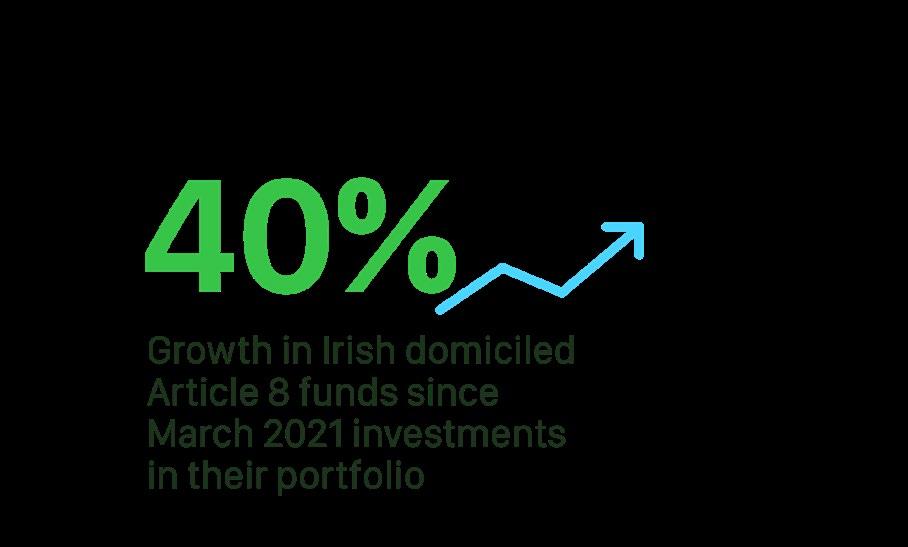

While the number of Article 6 funds is substantial, the number of sustainability focused funds is growing, particularly in the case of Article 8 funds. Since SFDR was introduced in March 2021, the number of Irish domiciled Article 8 funds has grown by more than 40%. The growth of the Article 8 fund in Ireland is consistent with the wider European position, where approximately 44% of all new fund launches in Q4 2022 were categorised as Article 8 funds⁴.

consistent with the European position. The criteria for qualifying as an Article 9 fund is significant, where all or substantially all of the fund's assets must consist of sustainable investments. This has proved challenging for asset managers and explains in part the low number of Article 9 funds, which we discuss in greater detail in the Analysis of Article 9 Funds section below.

4Source: Morningstar Q4 2022 in Review.

SFDR Impact Analysis | 9

This is clearly indicative of both a greater familiarity of SFDR by asset managers, as well as growing investor

GROWTH IN IRISH DOMICILED ARTICLE 8 FUNDS SINCE MARCH 2021

ANALYSIS OF ARTICLE 8 FUNDS

While representing approximately 20% of all Irish domiciled funds today, we would expect this figure to grow exponentially in the coming years – growth in Article 8 funds has risen by 40% since the introduction of SFDR.

Article 8 Deep Dive

The growing popularity of Article 8 funds can be attributed to a clearer understanding by asset managers of the Article 8 categorisation, coupled with the greater flexibility that an Article 8 fund offers in terms of product design and portfolio construction (as compared to an Article 9 fund). The share of overall Irish domiciled assets held by Article 8 funds is growing. These funds currently account for over 27% of all assets held in Irish domiciled funds.

What are Article 8 Funds investing in?

The underlying investments of an Article 8 fund must contribute towards the promotion of the environmental or social characteristics designated by that Article 8 fund.

The flexibility of the Article 8 fund is demonstrated by the asset allocation it supports. Equity focused strategies dominate, representing nearly 44% of all Article 8 funds, followed next by ETF focused and debt focused Article 8 funds. All of which is not surprising given these are the predominant strategies within the UCITS space. The Other segment is broadly made up of liquid alternatives, index tracking and cash strategies.

ARTICLE 8 - ASSET ALLOCATION

MiFID Sustainability Preferences Impacting Product Design

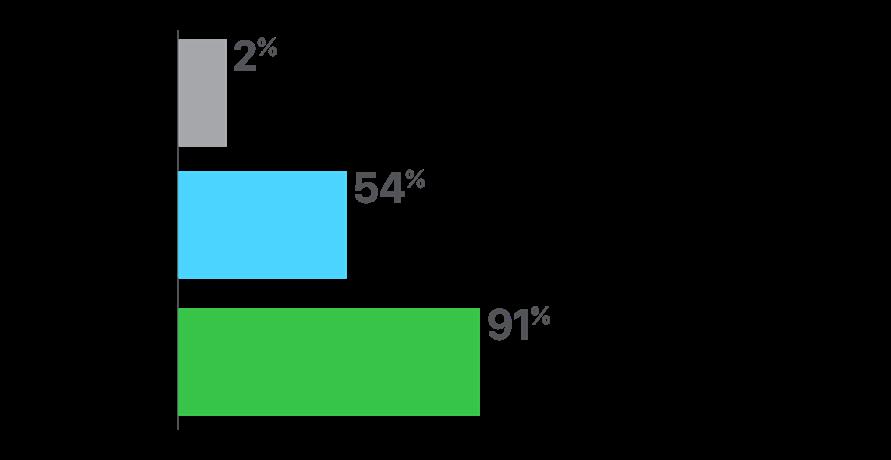

Unlike an Article 9 fund, there is no requirement for an Article 8 fund to commit to holding sustainable investments. However, over half of all Article 8 funds have voluntarily elected to do so. This is in part designed to satisfy the MiFID sustainability preferences. In order to satisfy these requirements (i.e. meet an investor’s sustainability preferences), Article 8 funds must do at least one of the following: (i) commit to a minimum holding of sustainable investments; (ii) commit to a minimum holding of Taxonomy-aligned investments; or (iii) consider PAI of their investment decisions on sustainability factors, at the product / fund level.

Ascertaining whether an investment is Taxonomyaligned is currently quite challenging for asset managers, largely due to the lack of available, reliable and / or verifiable data. This has prompted asset managers to be cautious in asserting that a fund’s underlying investments qualify as being Taxonomyaligned. As a result, only 2% of the Article 8 funds forming part of our sample have committed to holding Taxonomy-aligned investments. The EU reporting framework is being enhanced in 2025, whereby companies will be required to report on the impact their activities have on environmental and social matters, so these data challenges will diminish in due course and Taxonomy-alignment will likely increase as a result.

Most pronounced, is the number of Article 8 funds which are considering PAIs at the product level. A staggering 91% of the Article 8 Funds sampled do so, which is in stark contrast to the levels of asset managers considering PAI at the entity level, which we discuss further below in the section below entitled Are Managers Considering PAIs?

ARTICLE 8 FUNDS & MIFID SUITABILITY PREFERENCES

While significant, this level of adoption is understandable, as it ensures that one of the three categories is met and an Article 8 fund may be eligible for recommendation to clients that have expressed sustainability preferences.

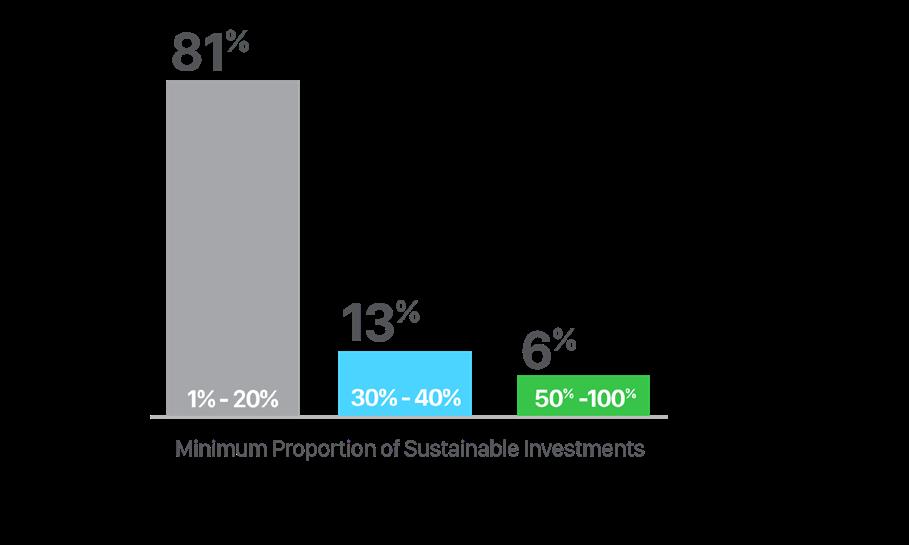

What’s in a Name?

Article 8 funds committing to holding sustainable investments may well take on additional importance if the recent ESMA consultation on guidelines on fund names using ESG or sustainability terms is to take effect. This consultation advocates that funds using "ESG", "Sustainability" or similar terms should have a minimum commitment of 80% of its portfolio towards investments promoting environmental and social characteristics and / or the social objective of the fund, out of which 50% should consist of sustainable investments. This consultation does not impact Article 9 funds, given the expectation that all or substantially all of investments of an Article 9 fund must be sustainable investments.

ARTICLE 8 FUNDS THAT COMMIT TO SUSTAINABLE INVESTMENTS

which we discuss in greater detail in the section Key Trends for Sustainable Investing, however if these were to become binding, based on our analysis only 6% of existing Article 8 funds would be eligible to use sustainability related terms in their naming conventions. Others will need to either rename their Article 8 funds or entirely reconstruct their portfolio allocations, neither of which is ideal from an investor relations perspective.

In the interim, asset managers should have regard to these proposals when contemplating naming their Article 8 funds.

SFDR Impact Analysis | 11

to any minimum proportion of taxonomy alignment Committing to any minimum proportion of sustainable investments

PAIs

Committing

Considering

ANALYSIS OF ARTICLE 9 FUNDS

Only 3% of Irish domiciled funds have categorised themselves as Article 9 funds. This is broadly in line with the European position and reflects an initial uncertainty surrounding the criteria for the categorisation.

Article 9 Deep Dive

The low level of funds categorising themselves as Article 9 funds can be principally traced back to July 2021, when the European Commission confirmed its expectation that the portfolio of an Article 9 funds should consist almost exclusively, of sustainable investments. This high bar has put asset managers off the Article 9 fund categorisation, with some managers preferring to classify their sustainability focused products (with significant exposures to sustainable investments), as Article 8 funds. It also led to a significant number of fund re-categorisations (from Article 9 to Article 8), which we explore in more detail below.

Commitment to holding Sustainable Investments

In practice, few Article 9 funds solely consist of sustainable investments. It has proved a difficult threshold to reach, as even the most sustainability

OF ARTICLE 9 FUNDS COMMIT TO HOLDING AT LEAST 80% SUSTAINABLE INVESTMENTS

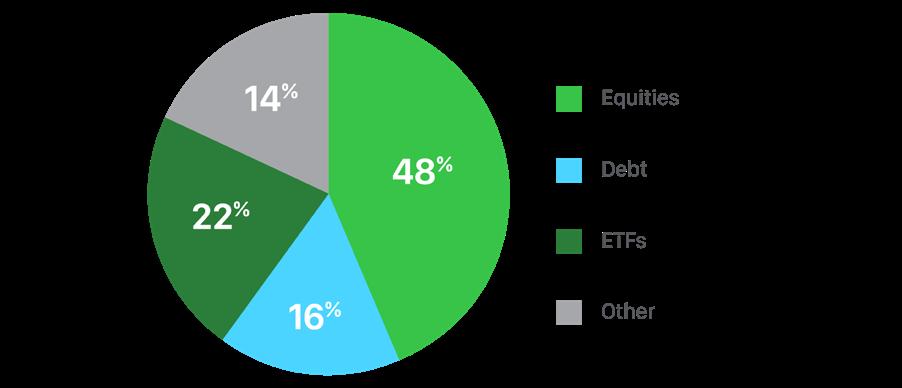

While the portfolio of Article 9 funds should consist of all, or substantially all, of sustainable investments, and therefore they do not enjoy as much flexibility as Article 8 funds, it is notable that asset allocation in Article 9 funds is broadly similar to their Article 8 counterparts.

12 | Maples Group

As with Article 8 funds, equity strategies dominate, representing nearly half of all Article 9 funds, followed next by ETFs and debt focused Article 8 funds. The Other segment is broadly made up of alternatives, private equity and real estate strategies.

Taxonomy Alignment - Article 9

As would be expected owing to their sustainable investment objective, a significantly higher proportion of Article 9 funds (15%), commit to holding a minimum proportion of Taxonomy-aligned investments. Of note however, is that the actual minimum committed proportion of those Article 9 funds is, in nearly all instances, below 10% of their assets. Again, the lack of available, reliable and verifiable data is presenting challenges to Article 9 fund managers committing to

Article 9 Reclassifications

As has been widely publicised, a significant number of Article 9 funds reclassified as an Article 8 funds in the lead up to the full implementation of SFDR on 1 January 2023. In an Irish context approximately 25% of all Article 9 funds reclassified as Article 8 funds.

While these downgrades may have been genuinely prompted by changes to a particular fund's sustainability objectives, it is more likely due to the European Commission confirming its expectation that Article 9 consist entirely of sustainable investments.

Impacted most by this were Article 9 ETFs. As passively managed funds (reliant on the composition of their underlying indices), ETFs are not in a position to adjust their portfolios towards sustainable investments (as would be the case for actively managed funds). As a result, over 35% of all reclassifications from Article 9 to 8 occurring in Q4 2022 were ETFs, primarily those tracking Paris Aligned Benchmarks ("PABs") and / or Climate Transition Benchmarks ("CABs"), prompted by a fear that these would not be deemed sustainable investments.

In April 2023, the European Commission confirmed that funds passively tracking either PABs or CABs would be deemed to be holding sustainable investments, so it is quite possible some of these reclassifications may be reversed later this year.

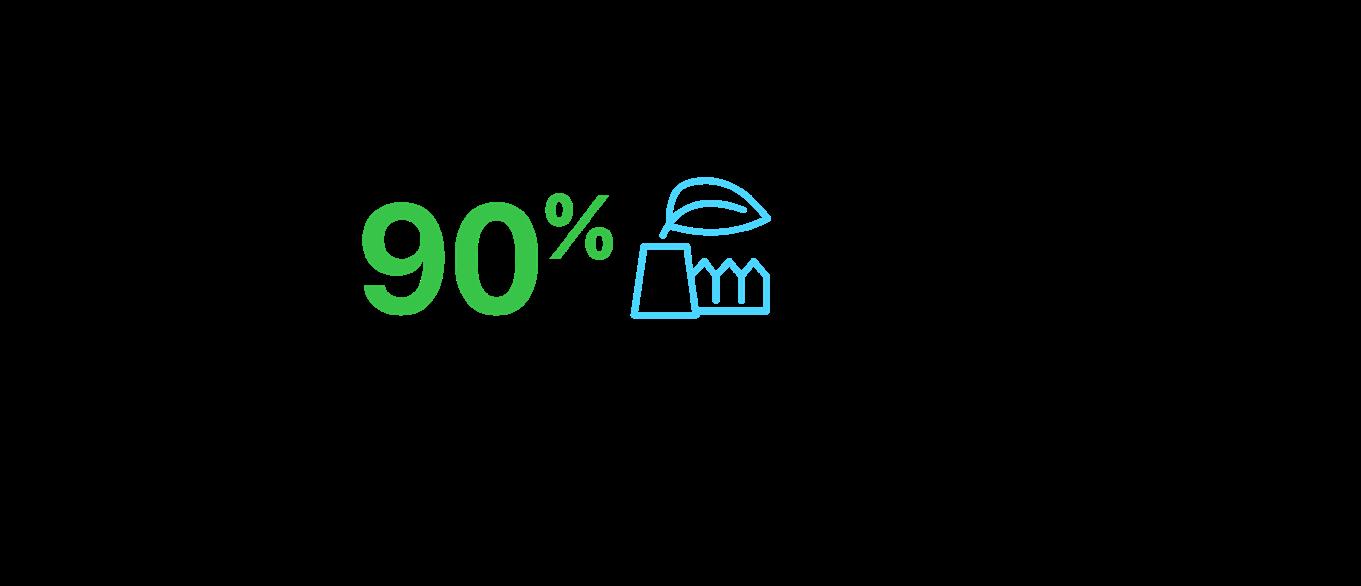

ILPs – A Growth Area for Article 9s?

The Investment Limited Partnership (“ILP”) is Ireland’s flagship regulated partnership vehicle. Owing to the flexibility on investment restrictions, borrowing and related features as well as the speed-to-market, the ILP is proving to be one of the more popular regulatory categories for ESG funds. Since the revamp of the ILP regime in 2021, over 11% of the ILPs established since are categorised as Article 9 funds, nearly four times higher than the industry average.

More aligned with what we have seen for Article 8 funds, nearly all Article 9 funds are considering PAIs at the product level (95%). This largely flows from the obligation that Article 9 funds must hold sustainable investments. Generally speaking, asset managers are utilising PAIs as part of their assessment of whether or not an investment is deemed a sustainable investment (in particular, as part of the DNSH test).

Asset managers have recognised the flexibility provided by the ILP to invest in sustainable asset classes as varied as land-based salmon farms, forestry, as well as sustainable infrastructure (wind and solar power plants). Given Ireland’s position as a centre of excellence for sustainable finance, and the growing international recognition of the ILP, we would expect the number of Article 9 ILPs to continue apace.

SFDR Impact Analysis | 13

ARTICLE 9 - ASSET ALLOCATION

OF ARTICLE 9 FUNDS COMMIT TO HOLDING TAXONOMY-ALIGNED INVESTMENTS

ARE MANAGERS CONSIDERING PAIS?

SFDR requires that managers disclose whether they consider PAIs of their investment decisions and whether they negatively impact on sustainability factors.

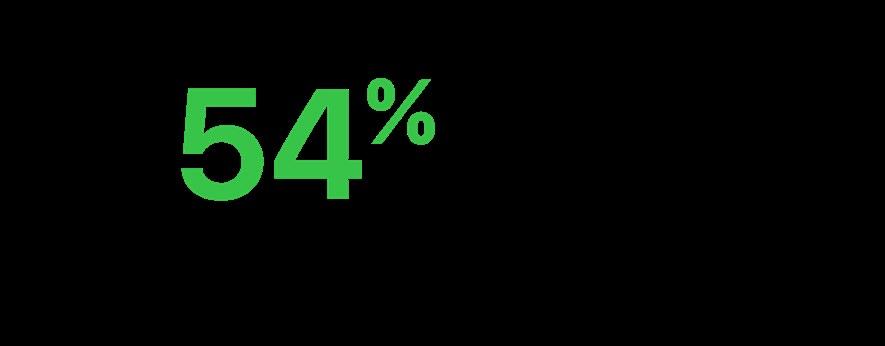

Consideration of PAI at Entity Level

Consideration of PAIs at entity level is on a “comply or explain” basis, save for those asset managers who have in excess of 500 employees who are obligated to consider PAI.

This obligation is distinct from considering PAI at the fund level. If an asset manager opts into considering PAI at entity level, it must do so in respect of every fund under its management. Asset managers opting in must undertake PAI reporting as at 30 June each year (using a prescribed reporting template), with respect to the previous reference period (ending at the preceding 31 December).

Asset managers who opt out of PAI consideration need to disclose on their website the rationale for doing so.

Are Managers opting into PAI?

Unsurprisingly, no they are not. We analysed the top 30 asset managers of Irish domiciled fund based on the Monterey Ireland Fund Report and found that a little over funds (91%) and Article 9 funds (95%) but nonetheless can be easily explained.

Consideration of PAI at the fund level may be undertaken on a fund by fund basis, enabling managers to cherry pick which Article 8 funds and / or Article 9 funds to report on. It has proved a more efficient and attractive approach (to PAI reporting) as opposed to the asset manager opting into PAI consideration at entity level, thereby obliging it to report on all funds under its management, irrespective of their SFDR categorisation or whether or not they are even offered to EEA domiciled investors.

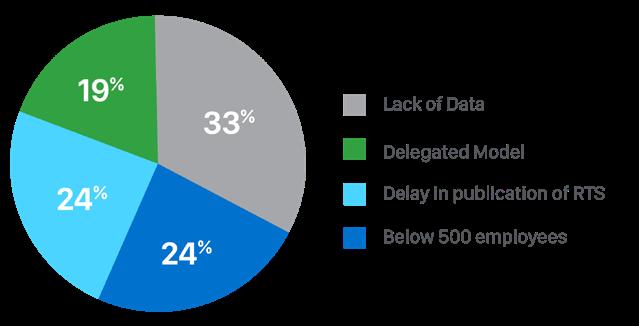

If not, why not?

The rationales cited by asset managers opting out of PAI consideration unsurprisingly have focused on the wellpublicised issues with SFDR compliance – namely the delay in the finalisation of the legislation, as well as the lack of available, reliable and verifiable data.

RATIONALES FOR NOT CONSIDERING PAIs

14 | Maples Group

AT ENTITY LEVEL

OF MANAGERS CONSIDERING PAIs OF THEIR INVESTMENT DECISIONS

SFDR WEBSITE DISCLOSURES

SFDR establishes three principal areas where sustainability related disclosures must be made – fund prospectus, fund periodic reports and website disclosures.

Don't forget about the Website

SFDR website obligations require both entity level and product level disclosures. It is important that asset managers have controls in place from both a compliance and operational perspective to ensure that all website disclosures adhere to both the SFDR content and location rules.

Again as part of our Analysis, we examined the SFDR website disclosures of the top 30 asset managers operating in Ireland. These managers who collectively manage over half of all Irish domiciled Article 8 or Article 9 funds, enabling us to discern the broader market approach. While there is a high degree of compliance with both the entity level and product level disclosure obligations, there remains room for improvement.

Website Content and Location Rules

SFDR requires that the website sustainability disclosures be "...clear, succinct and understandable to investors published in a prominent easily accessible area of the website". SFDR further mandates that Article 8 and Article 9 fund specific disclosures be housed in a separate section of the website entitled "Sustainabilityrelated Disclosures" which should be located in the same part of the website where other fund specific information is housed.

Encouragingly, the vast majority of the asset managers sampled included the prescribed SFDR sustainability disclosures on their websites, however only half of the asset managers sampled complied with the SFDR website location rules, i.e. labelling the dedicated section "Sustainability-related Disclosures". That said, user experience varied significantly. It was not always

the case that the SFDR sustainability disclosures were located in prominent or easy to find / accessible area of the website.

Navigating from the asset manager's homepage to ultimately locating the SFDR sustainability related disclosures was often challenging. Some assets managers, while having prominent ESG sections on their website, these sections did not always include (or intuitively link to) the specific SFDR disclosures.

To avoid regulatory scrutiny, asset managers should be minded to review their SFDR website disclosures in terms of both accessibility and location.

Refresh this Page

Another important aspect of SFDR website disclosures is the requirement that it be kept up to date. SFDR implicitly recognises the interplay between the Article 8 and Article 9 pre-contractual disclosures (which may become dated over time) and the website disclosure, which should remain contemporary. This interplay is established within the Article 8 and Article 9 fund precontractual templates by the requirement to include a hyperlink (to where more specific product information may be found). Asset managers must not ignore or fail to keep their SFDR website disclosures up to date, otherwise they are likely to be subject to regulatory scrutiny, and possible sanction.

SFDR Impact Analysis | 15

SFDR IMPLICATIONS FOR THIRD PARTY MANAGERS

SFDR compliance lies with the UCITS management company, the AIFM or MiFID firm of the relevant fund. The prevalence of third party AIFMs and UCITS management companies in the European fund space has created an interesting SFDR compliance dynamic.

The Rise of the Third Party ManCo

The number of Irish domiciled funds with a third party UCITS management company or AIFM ("Third Party ManCo") has doubled since 2020. This was largely driven by the increased substance requirements imposed by the Central Bank of Ireland and the phasing out of the

SFDR obligations. While this approach is understandable given the inherent link between SFDR requirements and the day-to-day management of a fund, given the increased regulatory focus on outsourcing and delegation in general, it is crucial for Third Party ManCos that the SFDR compliance model applied is appropriately contracted.

What about the Contracts?

sustainability focused funds. For the purposes of this Analysis, we analysed the SFDR website disclosures of the top ten Third Party ManCos operating in Ireland as per the Monterey Ireland Report, who in aggregate manage approximately 25% of all Irish domiciled Article 8 and Article 9 funds.

SFDR and the Delegated Model

Third Party ManCos typically operate under a delegated model, whereby the day-to-day investment management of the specific fund is delegated to an underlying investment manager. SFDR does not contemplate for, or expressly address the delegated model. Neither does SFDR expressly require that all management entities within the same fund structure, individually and separately, assume responsibility for compliance. Rather in the case of a multi-manager scenario, it falls on the two entities to agree on whom will assume the responsibility and the corresponding SFDR disclosure obligations.

Our Analysis suggests that Third Party ManCos have placed a significant reliance on delegate investment managers for compliance with some or all of the various

As with any regulatory obligation, identifying the responsible party for carrying out that obligation must be clearly documented. In a delegated management model, this responsibility should be documented in the investment management agreement between the Third Party ManCo and the delegate investment manager. In an SFDR context, if there is no expressed contractual arrangement put in place between the parties, the responsibility for SFDR compliance will default to the Third Party ManCo.

SFDR implementation prompted significant industry focus on pre-contractual, periodic report and website disclosure, however we have not seen a corresponding level of attention placed on the repapering of existing investment management agreements. This suggests that the contractual delegation of SFDR obligations, in terms of clearly delineating the responsibility for carrying out and complying with those obligations, as well as reflecting how the Third Party ManCo oversees the performance of same, is lacking.

Third Party ManCos would be well advised to undertake an analysis of its delegate arrangements to ensure that they have appropriately dealt with SFDR compliance obligations. Failure to have done so potentially creates a regulatory compliance risk, not only in an SFDR context, but also from an outsourcing / oversight perspective, exposing the Third Party ManCo to potential regulatory sanction.

16 | Maples Group

OF ALL IRISH DOMICILED FUNDS HAVE A THIRD PARTY MANCO

Sorry page not found

In the context of how Third Party ManCos are approaching SFDR website disclosure obligations, a heavy reliance has been placed on the inclusion of hyperlinks (to the delegate investment manager's website). This approach is in of itself permissible under SFDR, however we found that these hyperlinks failed to meet the SFDR website requirements (in terms of both location, as well as content).

A common issue encountered was that the hyperlinks directed the user to the delegate investment manager's home page, as opposed to the dedicated area of the website where SFDR disclosures are required to be housed. In some cases, the specific Article 8 or Article 9 fund disclosures were difficult to locate (e.g. not in a prominent easily accessible area of the website). In other cases, the delegate investment manager's website did not include the specific Article 8 or Article 9 fund disclosures or more egregiously the hyperlinks to the delegate investment manager's website were inoperative.

Where a Third Party ManCo is relying on a delegate investment manager to meet the SFDR website requirements, it is incumbent on that Third Party ManCo to continually monitor those links. Dormant or inoperative hyperlinks clearly indicate a lack of ongoing oversight by the Third Party ManCo on the delegate investment manager, something which is easily identifiable by regulators, such as the Central Bank of Ireland, as part of a thematic review or inspection. Failure to appropriately maintain the SFDR website disclosures would likely be deemed a material non-compliance issue, and attract regulatory sanction.

SFDR Impact Analysis | 17

Failure to appropriately contract for SFDR not only creates a potential regulatory compliance risk, but may also expose a Third Party ManCo to regulatory sanction from an outsourcing / oversight perspective.

SFDR - IMPACT ON EEA FUND DISTRIBUTION

Non-EU investment managers looking for new sources of capital or diversification of their investor base are increasingly turning to Europe. To successfully fund raise in Europe, non-EU managers need to be familiar with the nuances of European fund distribution and how it has been impacted by SFDR.

SFDR Applies to Non-EU Managers

SFDR applies to asset managers (and investment advisers) domiciled or operating in the EU, who are managing or distributing funds to European investors. Non-EEA managers either managing EU funds or actively marketing their products via national private placement regimes in the EU will be subject to SFDR.

Additionally, EEA-domiciled funds managed by non-EU managers are also in scope of SFDR, even if those funds are not marketed through national private placement regimes in or towards EEA domiciled investors. For example, a US domiciled investment adviser marketing a Cayman Islands fund into Europe is in scope of SFDR, at both the entity level and the fund level. Adherence to the entity level obligations might potentially prompt changes (from an operational and procedural perspective) for such non-EU managers.

Successfully Navigating European Distribution

Our Global Registration Services team (“GRS”) supports and assists managers navigate the complexity of requirements associated with distributing their fund products in a multi-jurisdictional environment. We provide support throughout the distribution chain to include market intelligence, market entry of sustainability focused funds within Europe, as well as the maintenance of ongoing reporting and filing obligations for those funds which have successfully registered in Europe.

For further details of our GRS offering please see our Guides to Marketing Funds in Europe

Gateway to Europe –Maples Group ESG Platform

In addition to our dedicated GRS team, the Maples Group has established the Maples ESG Platform, specifically structured to host ESG and sustainability-focused funds (the "ESG Platform"). This offers a turnkey solution for clients looking to launch a segregated SFDR-compliant Article 8 or Article 9 sub-fund, allowing them to take advantage of the high demand for ESG focused funds in Europe. EU and non-EU clients looking for a flexible solution for SFDR compliance and European distribution can take advantage of an established fund platform with regulatory approval and legal agreements already in place.

The ESG Platform affords clients access to industry leading ESG practices and service providers for ESG advisory, fund management, fund distribution, operational and reporting solutions. This includes exclusive access to a first-of-its-kind solution for independent certification of a fund's and manager's ESG strategies.

For further details please see our ESG Platform

18 | Maples Group

SFDR Impact Analysis | 19

KEY TRENDS FOR SUSTAINABLE INVESTING

Given our position in the sustainability space, we have gained valuable insights into how managers are structuring ESG funds. Recent developments would also suggest that SFDR is transforming from a disclosure regime and becoming a product regime.

Disclosure Regime or Labelling Regime?

SFDR was implemented as a disclosure regime, its original objectives were clear, to provide a harmonised approach in respect of sustainability-related disclosures to European investors, to enable those investors to objectively assess the sustainability credentials applied by each fund product. However, over the course of its implementation and its ongoing evolution, SFDR has become a labelling regime and arguably, its likely future state is potentially a product regulation.

This transformation can be directly traced back to the various guidance and / or proposals emanating from ESMA and the European Commission.

The best example of this can be seen with the recent consultation on ESMA consultation on guidelines on fund names using ESG or sustainability terms. As we discussed previously, this advocated that funds using "ESG", "Sustainability" or similarly ESG themed terms should have a minimum commitment of 80% of its portfolio towards investments promoting environmental and social characteristics and / or the social objective of the fund, out of which 50% should consist of sustainable investments, effectively ascribing minimum sustainability criteria for Article 8 funds. These quantitative thresholds have been broadly criticised given the lack of calibration of the SFDR definitions (e.g. sustainable investment). Similarly, such thresholds (and the definitions underpinning them) are routed in the here and now and therefore exclude transition investments. So it remains to be seen if they will be introduced in the short term, but nonetheless remain indicative of how the legislators are currently viewing SFDR.

Enhanced Role of the Depositary

Another example of the SFDR metamorphosis and one of the most interesting areas of development within SFDR is the role of the depositary. It is fair to say that depositaries took somewhat of a back seat during the development and implementation of SFDR – deeming it to be a disclosure regulation with compliance a matter for the asset manager (to ensure it provided its investors with adequate sustainability related disclosures). However, recent publications from both the CSSF and the Central Bank of Ireland have confirmed that depositaries should monitor any binding commitments in the SFDR related disclosures (e.g. proportion of the fund exposed to environmental and social characteristics and / or sustainable investments), as part of its depositary oversight function and, in particular, treat such commitments as akin to investment restrictions. The depositary community has quite understandably been blindsided by these developments. SFDR makes no reference whatsoever to the depositary, let alone the role the depositary should play. Similarly the pre-contractual templates themselves do not frame the commitments as investment restrictions, rather it focuses on disclosures around minimum proportions and / or planned allocations.

Such an interpretation poses numerous practical challenges, not least how a depositary can create an oversight framework to monitor the various bespoke methodologies for assessing what is a sustainable investment (noting the subjectivity within that definition and the extensive discretion afforded to asset managers to determine same). Treating these allocations or commitments as investment restrictions is effectively transforming SFDR from a pure disclosure regulation into a quasi-product regulation.

20 | Maples Group

SFDR 2.0 – An ESG Product Regime?

Against this backdrop, the French financial regulator, the AMF, has recently advocated that for the introduction of minimum sustainability criteria for both Article 8 and Article 9 funds, it would fall on EU national competent authorities to supervise and ensure compliance with those minimum criteria. It also advocated for increased Taxonomyalignment by Article 9 funds, as well as standardising the definition of sustainable investments. The AMF believe that the introduction of such minimum sustainability criteria would reduce the potential for greenwashing.

The European Commission has already indicated that it will review SFDR later in 2023, but all of these developments suggest that the direction of travel for SFDR 2.0 could move away from a disclosure regulation and a potential transformation into a product regime.

SFDR Impact Analysis | 21

ABOUT THE AUTHORS

IAN CONLON

Ian is a partner of Maples and Calder's Funds & Investment Management team in the Maples Group's Dublin office. Ian is recognised as a leading lawyer in the ESG and sustainable finance space and is a member of the Maples ESG Advisory Group. He regularly advises clients on the establishment of sustainability focused investment funds, as well as global asset managers looking to integrate ESG as part of their organisational and operational frameworks. Ian is a regular contributor and speaker at industry conferences and events on ESG and sustainable finance, as well as the broader Irish and European regulatory space. Ian is recommended by Chambers Global, ILFR and Legal 500. Clients describe Ian as "exceptional, he has incredible knowledge of the ESG and sustainable investment space ".

NIAMH O'SHEA

Niamh is a partner of Maples and Calder's Funds & Investment Management team in the Maples Group's Dublin office. Niamh has particular expertise in the ESG and sustainable investment space. She regularly advises asset managers on the implementation and compliance with the EU’s Sustainable Finance Disclosure Regulations and the Taxonomy Regulation. Niamh is a frequent speaker at industry events on ESG and recently co-authored a Level 2 Guide to the EU Sustainable Finance Disclosure Regulation.

RICHARD O'DONOGHUE

Richard is a senior associate of Maples and Calder's Funds & Investment Management team in the Maples Group's Dublin office. He advises in respect of the establishment, authorisation and on-going operation of Irish regulated investment funds including UCITS, AIFs and other fund products. He also advises fund service providers including management companies, administrators, depositaries and investment managers. Richard has extensive experience on the implementation of and ongoing compliance with the EU’s Sustainable Finance Disclosure Regulations at both product and entity level. He has a particular focus on SFDR pre-contractual and periodic reporting requirements.

22 | Maples Group

ACKNOWLEDGEMENTS

We would like to thank and acknowledge the various contributors for their time and valued input in producing this SFDR Impact Analysis. In particular, Gerard Grogan, Rebecca Prati, Grace Phelan and Aoife Convey of the Maples Group.

maples.com/esg