US and European CLO Market Reviews

Listings Update Bringing You CLOser

Standard & Poor's Director Europe CLOs

Global Minimum Tax / Pillar Two

OECD Issues Guidance on CLOs Cayman Islands BOTA

Listings Update Bringing You CLOser

Standard & Poor's Director Europe CLOs

Global Minimum Tax / Pillar Two

OECD Issues Guidance on CLOs Cayman Islands BOTA

The Maples Group is delighted to present our December 2024 edition of The CLOser.

In addition to our regular US and European market reviews and listings updates:

• Our Bringing You CLOser external article comes courtsey of Sandeep Chana, Director, Structured Credit at S&P Global Ratings

• We present an article on the impact of the OECD Minimum Tax, known as Pillar Two and a discussion on the new Cayman Islands beneficial ownership regime.

• Our second 'Bringing Us CLOser' feature shining a spotlight on diversity, equity and inclusion highlights our collaborative efforts with the Irish Disability Bill

• And finally, we feature members from our global CLO team.

James Reeve

+1 345 814 4467

james.reeve@maples.com

In this US CLO market review, we provide our observations and analysis in respect of activity in the period from 1 January 2024 through to 31 October 2024, with a focus on transactions in which the Maples Group was engaged. In terms of the key developments during this period, we highlight the following:

• the large number of deals exiting their non-call periods coinciding with favourable market conditions leading to significantly heightened CLO refinancing and reset activity as compared to 2023;

• the removal of the Cayman Islands from the EU's AML List, on 7 February 2024, and materialisation of the anticipated shift back to the Cayman Islands as traditional 'home' and generally preferred jurisdiction for US CLO SPVs;

• approaches towards compliance with the US Corporate Transparency Act (the "US CTA"), with initial divergence in approaches shifting towards compliance for US CLO entities (for more on this see page 28); and

• the enactment of the Cayman Islands Beneficial Ownership Transparency Act (the "BOTA"), replacing the prior beneficial ownership regime, aligning the regulatory framework with equivalent regimes in other jurisdictions and bringing Cayman Islands CLO entities into scope for compliance to maintain a beneficial ownership register.

However, the major headline is the intense level of activity that has largely persisted from around early to mid-Q1, which may result in 2024 being a record-breaking year that, by time of writing, has led to new issuance volume YTD coming within approximately US$10 billion of 2021's record of US$187 billion.

While the US market overall been exceptionally busy, turning our attention specifically to data for the deals on which the Maples Group has been engaged one can see from Figures 1 to 6 below that, consistent with the big picture, we have had an incredibly strong year. The general trend from new issuance CLO closings to new warehouses and refinancings and resets has been upwards. This is perhaps most clearly illustrated when the different types of activity are combined in Figures 4 and 5, depicting cumulative transaction 'closings' on a month-by-month basis. Figure 5 breaks down the information by activity type: warehouse, new issuance and refi / reset. Analysing the data cumulatively for the review period on this basis one can see the stark increase as compared to 2023, with new issuance related activity (incorporations, warehouses, new issuance) averaging around 50% up on prior year. Of itself, that is extremely notable, but by no means the end of the story with the dramatic uptick in refinancing and resets transactions paling such increases into relative insignificance.

In the June 2024 edition of The CLOser, we provided information regarding the total number of 'open' warehouses on which we were engaged, which at that time stood at around 108. Figure 7 below illustrates the variability of the cumulative total of 'open' warehouses on our books monthly and an interesting feature of this data is the net growth by around 15-20%. This provides a good pipeline as we head through to the rest of the year and into 2025 - and underscores the market confidence in that short to mediumterm period.

Additional observations with respect of CLO warehouses and new issuance:

Warehouse Duration

Please see Figure 8. The warehouse durations recorded on 'closed' CLOs were mostly in the range of 2 to 8 months. As is always the case, there is a large degree of 'scatter' in the data but roughly 75% of deals were in this range and broadly the trend has been downwards, i.e. towards shorter / more efficient warehouse periods. Eliminating anomalous outliers, the average duration seems to land between 7-7.4 months.

Please see Figures 10 and 11. Unfortunately, we do not have a complete dataset for price-to-close periods but the information available and presented in these charts provides a good indication as to the typical price-to-close periods for CLO new issuance and refi / resets. With regards to the latter, we have tended see some very short periods much less than the average of around 15 days. In terms of the former, i.e. new issuance, we have witnessed a little more consistency / less erratic behaviour, with around 30-38 days being the norm. In both cases, however, there does appear a possible trend towards longer durations between pricing and close, but this is very much an approximation. The period between pricing and close can be particularly challenging where the issuer SPV is to be redomiciled / migrated between jurisdictions, so this is something we are always keen to watch and advise upon.

Please see Figure 9. Deal size has broadly trended upwards, although overall average is much the same as what which we reported upon in June, i.e. ~US$500 million.

Please see Figure 12. As in prior editions, we provide a separate global listings update, which can be found on page 16, analysing the latest trends and developments in detail. By way of brief overview, however, we note in this general US market review that around 80% or so of new issuance CLOs this year have not listed on any securities exchange. This denotes a possible slight (~5%) shift, further, towards no listing. Where there is a listing, the preferred exchanges remain Euronext Dublin and the Cayman Islands Stock Exchange.

Please see Figure 13. The Maples Group has worked on deals with over 57 different CLO managers so far YTD. Around 65% of deals so far have been with about 18 of the most active managers using Maples. On a CLO manager basis, we are therefore in the privileged leading position among offshore service providers having secured engagement with around 50% of all active managers YTD in the US CLO space.

Please see Figure 14. As has traditionally been the case, warehouse financing arrangements can take the form of debt and / or equity elements and where there is equity investment this commonly involves issuance of preference (or sometimes termed, preferred) shares. With introduction of the BOTA, preference share financing arrangements become highly relevant as investors will potentially be required to provide information for compliance purposes and will need to be included on the entity's beneficial ownership register, which would not be the case if such investment is held via sub notes or other debt instruments. The Maples Group has issued a number of legal updates, including a CLO focussed one regarding implications of the BOTA, which John Dykstra and Joe Jackson discuss in our Q&A in this edition, located on page 32.

As can be seen from Figure 14, a little over half of warehouse transactions this year have included preference shares.

Proceeding to CLO Close

Please see Figure 15. Thus far, we have seen cumulatively around 143 new warehouses 'opened' in the review period and, of those new warehouse, around 45% have proceeded to a successful CLO closing. As at the time of writing, the total number of 'open' warehouses on our books stands at around 115-120.

We have covered this topic extensively in prior editions – please see, in particular, our June 2024 edition, October 2023 and year in review piece summarising observations during the first full year of listing on the EU's AML List for further information and background.

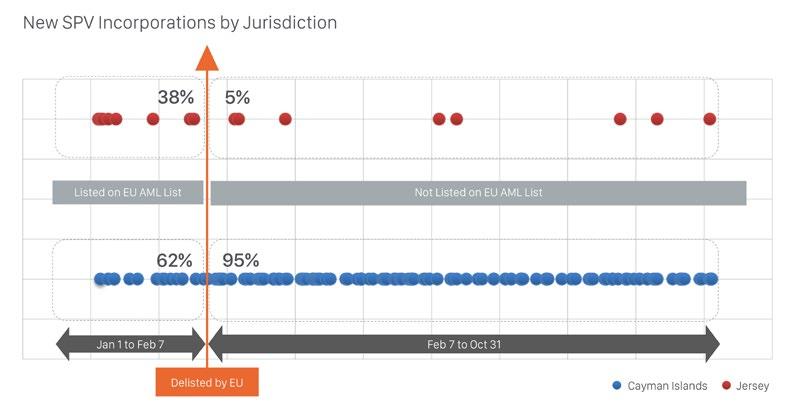

The relatively immediate trend back towards utilisation of Cayman Islands SPVs by the US CLO market, post-delisting of the Cayman Islands on 7 February, is evident from the data presented in Figures 16 and 17 below. One can see that the anticipated switch happened first with regards to new SPV incorporations, with 95% or greater of new SPV instructions received being in respect of Cayman Islands SPVs. YTD, however, in terms of closed CLOs, around 62% or so of our deals have employed Cayman Islands SPVs with the remainder being done out of Jersey. There are, of course, many existing warehouse entities and CLOs that have issued with non-Cayman Islands SPVs, predominantly Jersey SPVs and, in that respect, what we have seen, as deals exit their non-call periods and become viable for a refinancing / reset, is an occasional concurrent migration of the issuer over to the Cayman Islands. There has certainly not been a wholesale shift of non-Cayman Islands entities back 'home' – and nor is there any legal imperative for such a change – but many CLO market participants are preferring to see issuers move back and perhaps this is more pronounced of a preference where managers have a long legacy of deals done with Cayman Islands SPVs. Despite this there are exceptions, with occasional new US CLO SPVs being incorporated in Jersey and / or migrations to the jurisdiction. The Cayman Islands office CLO team members very much look forward to continued opportunities to work collaboratively with our Jersey CLO team members on these and many other finance transactions.

Earlier this year, at the DealCatalyst / LSTA Annual CLO Industry Conference at the end of April, Moody's reported on the very substantial proportion (70%+) of their rated deals that were exiting their non-call periods and hence would be eligible to be refinanced or reset. This trend has continued of course, and the Maples Group has seen an exceptional wave of instructions coming through, persistently since around February with upticks at various times but overall a strong and steady upwards flow. We are now not far off 300 instructions YTD, which is an incredible number, and of those deals towards 80% have closed already or have 'priced' as at time of writing. As can be seen from Figures 18 and 19, CLO vintages between 2018 and 2022 have accounted for most of the activity, with a large number being from the 2020-2022 range.

Although the year had a relatively modest start in the first few weeks or so, activity rapidly picked-up pace and certainly a major defining feature of the year, as many had forecasted, is the wave of refinancings and resets. New issuance volume at the time of writing stands at around US$178 billion involving around 115 or so managers, outstripping 2023 by far and bringing the record-breaking levels of 2021 clearly within sight. As regards refinancings and resets, at the time of writing those stand at over US$256 billion across over 550 transactions. Despite looking as though 2024 will be a new record-breaker, most predictions for 2025 are bullish, principally due to the expectation around tight spreads and demand from banks, insurance companies and CLO ETFs. Deutsche Bank and Morgan Stanley are both touting figures in the range of US$200 billion in new issuance, with BoA nudging higher – and it will be interesting to see whether expectations around the new US presidency and policies result in even more favourable conditions. Possible headwinds include global geopolitical developments / events and inflationary pressures, but overall, it seems that we are all going to be extremely busy for the rest of 2024 and beyond!

Most predictions for 2025 are bullish, principally due to the expectation around tight spreads and demand from banks, insurance companies and CLO ETFs

Stephen McLoughlin

+353 1 619 2736

stephen.mcloughlin@maples.com

Callaghan Kennedy

+353 1 619 2716

callaghan.kennedy@maples.com

2024 was a signature year for the European CLO market with total issuance to date already surpassing the record €40 billion of issuance seen in 2021. This was despite several macro headwinds in the form of geopolitical and economic uncertainty and is demonstrative of the continued strength of the European CLO offering.

This year's issuance mix included a record number of CLO managers coming to the European market, including new / debut managers. We generally see this as a very positive development for the market as it broadens the pool of offerings for investors in terms of choice and selection around management strategies. As well as a steady stream of new issuer activity, the second half of this year has largely been dominated by CLO refinancings and resets. This shouldn't come as surprise, as much of the refinancing activity so far relates to 2022 and 2023 vintage CLOs that are ending their non-call periods. For more information on the continued wave of expected refinancing and reset activity, please refer to our article with Sandeep Chana (Director, European CLO at S&P) on page 18.

There has also been a noticeable increase in participation from thirdparty equity investors, particularly

in the mezzanine and equity tranches of CLOs. These investors are increasingly investing directly into warehouses, providing earlystage funding and enhancing the overall liquidity of the market. Furthermore, investment banks continue to provide Class A loans into CLO structures (both for new CLO issuances and refinances / resets) in significant number.

Based on our discussions with market participants, sentiment is expected to remain very positive, with analysts projecting record-breaking growth for the remainder of 2024 and into the first half 2025. In the months ahead, continued demand for European CLOs is expected to be being driven by historically low default rates and attractive yields compared to other fixed-income assets.

In a positive development for the European CLO market,the first mid

market CLO landed in recent weeks and it is expected that 2025 will see further issuances of mid-market CLOs. In contrast to the US, where mid-market CLOs have long been a source of funding for mediumsized corporates, the development of this market in Europe has been stymied for several reasons. In the past it has been difficult to source a diverse pool of loans from a broad pool of industries to sufficiently dilute credit risk. In addition, the presence of GBP denominated loans has created difficulties in understanding how foreign exchange risk will be addressed, other than increasing CLO subordination.

Several established asset managers have been working to overcome these difficulties (hence the increased optimism) and given the successful first landing of this product offering we understand that they are accelerating their prelaunch workstreams.

The European Commission has launched a targeted consultation to gather feedback on the functioning of the EU securitisation framework. This consultation aims, among other things, to assess the effectiveness of the current framework and the current due diligence requirements, as well as to identify areas for potential improvement. The consultation is part of the Commission's broader efforts to ensure that the securitisation market in the EU remains robust, transparent and resilient.

In particular, the consultation paper asks market participants whether the securitisation framework needs to be amended in respect of the jurisdictional scope of the legislation and whether the definition of 'securitisation' is too broad or too narrow.

On 1 November 2024, the new UK regulations on securitisation came into effect. The pre-existing rules, which tracked the EU Securitisation Regulation framework, were replaced by a new framework.

One noticeable aspect of the new UK regulations is that the rule-making power is granted to the financial regulators, being the Prudential Regulatory Authority of the Bank of England ("PRA") and the Financial Conduct Authority ("FCA").

As mentioned, for the most part, the new UK regulations follow the EU Securitisation Regulation framework. However, the new UK framework is noticeably different in respect of the requirements applying to UK institutional investors. There is more flexibility for UK institutional investors with respect to their obligations to verify compliance with transparency requirements.

UK institutional investors will no longer be required to verify that the originator, sponsor and SSPE are producing Article 7 reporting on the required templates. The new rules will change the diligence requirement to a principles-based approach. Investors will need to ensure that the originator, sponsor or SSPE (wherever they are established) has made and has agreed to make certain information available at the specified frequencies but will no longer require the information reporting to be on specific templates.

The Corporate Sustainability Reporting Directive ("CSRD") is a regulatory framework introduced by the European Union to enhance and standardise sustainability reporting by companies. It aims to ensure that companies provide more consistent, comparable and reliable information on their environmental, social and governance performance. This directive is part of the EU's broader strategy to promote sustainable finance and achieve the goals of the European Green Deal.

The CSRD applies to a broader range of companies compared to its predecessor, the Non-Financial Reporting Directive ("NFRD"). Commencing on 1 January 2025, CSRD will apply to large undertakings (not subject to NFRD).

Such large undertakings are undertakings that, on their balance sheet date, exceed at least two of the following three criteria:

i. balance sheet total: €25 million;

ii. net turnover: €50 million; or

iii. average number of 250 employees during the financial year.

It is expected that CSRD will have little impact on the European CLO marketplace due to:

a. mechanisms to allow for the EU to recognise other reporting standards as equivalent to those under CSRD; and

b. the turnover threshold (€50 million) coupled with the expected declining rate environment in the months and years ahead.

A review of the CLO listings on the Cayman Islands Stock Exchange ("CSX") in 2024 highlights several main themes in the CLO market this year: (i) a record breaking year for new issuance,(ii) the revival of the refinancing / reset transaction; and, (iii) the return to the Cayman Islands as the jurisdiction of choice for the incorporation of US CLO issuers.

As of the end of October 2024, a whopping 108 CLOs have listed on the CSX, compared to 20 CLOs listed for the same period last year, and 32 CLOs listed in the entirety of 2024. In 2021, often cited as a benchmark for the current year for new issuance and refinancing, 131 were CLOs listed on the CSX. For 2024, the number of CLOs listed on the CSX is expected to surpass the 2021 tally, as both the new issuance and refinancing pipeline remains strong through this last quarter. To date, of the 108 CLOs listed on the CSX t, the Maples Group has listed over 40% of the CSX-listed CLOs.

Thus far in 2024, the balance between new issuance listings and refinancing listings has been evenly split. To date, of the 108 CLO listings on the CSX, 51 (47%) have been new issuance deals and 57 (53%) have been refinancing or reset deals. In 2023, this split was weighted more towards new issuance listing, with 81% of the listings being new issuance deals, and 19% being refinanced deals. Again, the 2021 data is similar to the current year, but with the weighting slightly favouring new issuance deals (57% new issuance listings and 43% refinancing listings).

In 2021, 95% of the CSX-listed CLO issuers were incorporated in the Cayman Islands; with the other 5% of CLO issuers being Delaware incorporated. In 2023, after nearly two years of the Cayman Islands being on the EU AML List, 50% of the CLO listings on the CSX were by Cayman Islands issuers; 38% were by Jersey issuers, 6% were by Bermudian issuers, and 6% were by Delaware issuers. On 7 February 2024, the European Commission removed the Cayman Islands from its list of 'high-risk third countries' identified as having strategic deficiencies in their anti-money laundering / counterterrorist financing regimes ("EU AML List") and since then, we have seen a strong preference in the market to return to the Cayman Islands as the jurisdiction of choice for the incorporation of US CLO issuers. As noted and discussed further in our US Market Review, as of October 2024, 81 or 75% of the CLO listings on the CSX were by a Cayman Islands issuer with a Delaware co-issuer; 18 or 17% were by a Jersey issuer with a Delaware co-issuer; 7 or 6% were by a Bermudian issuer with a Delaware co-issuer; and 2 or 2% were by a Delaware issuer.

March and October 2024 were the most active months for CLO listings on the CSX, with 19 and 14 listings, respectively. In addition, the trend away from listing the full stack and towards listing only a single tranche of notes, or a couple of senior secured tranches, has continued: 48% listed only a single class of CLO notes, and a further 36% listed only two or three classes of notes.

The Maples Group listed 42% of all the CSX-listed CLOs during this period, including 36% of the Cayman Islands issuers, 78% of the Jersey issuers and 100% of the Delaware middle market issuers listed on the CSX.

Based on the Group's recorded data as of the end of October 2024, approximately 15% of new issuance CLOs sought a CSX listing for one or more tranches of notes, and approximately 10% of refinancing or reset transaction sough a CSX listing for one or more tranches or notes.

The Maples Group’s Fiduciary team in Ireland has strengthened its position as the leading Corporate Services Provider to SPVs, in what is shaping up to be a banner year for European CLOs.

According to industry intelligence group Atlantic Star’s latest Irish CSP Report, the Maples Group was the leading CSP for total active Irish SPVs in September with 824 SPVs, representing an 18.8% market share, some 4.9% ahead of the next placed firm.

For Company Secretary (CoSec) services to active Irish SPVs, the Group held an equally strong position, as CoSec on 888 vehicles, covering 20% of the market, 6.3% ahead of the nearest competitor.

With 4384 SPVs currently active as of September 2024, which is 6.2% ahead of the same month last year, the international financial services sector in Ireland is in buoyant shape, underpinned by the dynamic CLO sector.

There were 1589 active securitisation SPVs in Ireland at the end of September, which was up 11.9% on the previous 12 months, reflecting the surge in CLO issuance. Securitisations represented 36.2% of active Irish SPVs in September, with CLOs accounting for 18.4% of active SPVs.

Although SPV numbers consolidated at elevated levels in September, with total active SPVs edging 0.1% lower from the previous month, the positive trend of the past six months, which has seen record highs both in terms of assets and vehicle numbers, remains intact.

“Bothintermsofnewdealsandmorebroadlyinthe structuredfinancesector,2024hasbeenanextremely strongyear,withmanagersandarrangerstakingadvantage ofthelowerinterestrateenvironmentin2024tostructure transactionsatattractivepricing,”saidJulianDunphy,Head ofStructuredFinance,Fiduciary–Ireland.

“Weareseeingthishealthyactivityacrossthespectrum, includingincreasinginterestinassetclassessuchas significantrisktransferdealsandasset-backedfinancings. wellasaresurgenceofrefinancingsandresets,whichwill notalwaysbeevidencedbynewIssuerlevels,”addedJarlath Canning,SeniorVicePresident.“Despitecautiondueto potentialinterestraterisksandborrowerdefaults,2024is shapingupasarecordyearforCLOactivities,withissuance levelspoisedtorivalthehighsof2021.”

Julian Dunphy

+353 1 697 3231

julian.dunphy@maples.com

Jarlath Canning

+353 1 679 3294

jarlath.canning@maples.com

Our eighth ‘Bringing You CLOser’ inside view from recognised CLO industry participants and experts features Sandeep Chana, Director, Structured Credit, S&P Global Ratings. In this Q&A with Amanda Lazier and Joe O’Neill, Sandeep shares his thoughts on certain developments in the European CLO market year to date and takes a deep dive into what trends and innovations have emerged in CLO documentation.

The European CLO market is now in record-breaking territory, surpassing the near €40billion of issuance we saw in 2021. How has increased issuance impacted Euro CLO pricing?

From my perspective it’s been an extremely busy year and based on my conversations with market participants, 2025 will be no different.

From a cost of funding perspective, AAA CLO liabilities have generally shown a downward trend throughout the year, averaging 129 basis points (bps) in the third quarter, from an average of 149bps at the beginning of the year. This overall reduction in funding costs has improved CLO arbitrage and incentivised investors, such as CLO equity, to re-enter the market. While

this year has seen a steady stream of new issue activity, it has also been dominated by CLO refinancings and resets. If we include refi and reset activity in the US market, then YTD reset volume globally is at an all-time record. See our European CLO Market Review 2024 and Outlook on page 14.

European CLO resets have seen a significant comeback in 2024. What are the key drivers behind this trend and what might this mean for next year?

The second half of the year has seen a significant comeback in European CLO resets, particularly for 2022 and 2023 vintage CLOs. Interestingly, some vintages outside these cohorts have also come forward for a reset, largely driven by the

fact that they have ended or are close to ending their reinvestment periods. Approximately 26% of S&Prated CLOs are now outside their reinvestment periods, potentially a record amount at any single point in time, making them viable candidates for refinancing.

A closely watched metric is the proportion of "CCC" rated assets held by CLOs. This metric may draw more scrutiny for CLOs that have ended or are close to ending their reinvestment periods, accelerating the need to reset. CLOs at this point have less flexibility to trade out of their CCCs, concentration risk grows through note deleveraging, and the cost of funding the CLO increases once the AAA notes start amortizing. This may incentivize CLO equity investors to consider a reset.

Looking forward to 2025 and beyond, this trend may continue as nearly €30 billion of CLO paper (approximately 66 CLOs) will be exiting their reinvestment period in 2025 making them potential candidates for a refinancing.

What trends or innovations have emerged in CLO documentation, particularly around key provisions such as reinvestment flexibility and overall management of key CLO tests?

Several trends and innovations have emerged in CLO documentation, particularly around key provisions such as reinvestment flexibility and the overall management of key CLO tests. Two recent themes observed are the expansion of reinvesting capabilities over the life of the CLO and the utilization of cash positions to satisfy reinvestment provisions.

In recent years, CLOs have found ways to better manage their portfolios once the reinvestment period has ended, especially during stressed economic periods. A common feature we're seeing included in documentation is what we refer to as the "Unsatisfied Portfolio Profile Mechanism". This mechanism allows CLOs to continue reinvesting even if certain portfolio profile tests are failing, provided the failing test is made no worse following the proposed reinvestment. For example, if a CLO is failing its fixed rate asset limit, it may still trade its portfolio as long as the reinvestment does not include the purchase of more fixed rate assets. In our view this mechanism helps aid scenarios where the requisite trade is likely to erode CLO par, for instance through a credit impaired reinvestment or where the CLO will lose overall par but remain above their target balance.

CLOs are also seeking ways to "make cash work" more effectively, implementing changes in their documentation to reflect this. This includes the "synthetic" distribution of principal cash to improve the calculation of par value tests (also known as overcollateralization ratios) and applying discount rates to cashtrapping mechanisms to fast-forward CLO equity returns.

Focussing on the calculation of par value tests – which in our view is a feature imported from the US CLO market – these are primarily designed to protect CLO investors from par erosion and losses in the underlying portfolio by ensuring that interest and/or principal proceeds cure predefined par value tests on each payment date. At the same time, a CLO's reinvestment conditions require compliance of the same par value tests to ensure that the underlying portfolio's par value is generally maintained or improved every time the CLO manager is trading the portfolio. In both cases, recent CLOs have been calculating their par value tests by pre-determining the repayment of the CLO notes by an amount equal to the amount of principal cash the CLO currently holds, and in the case of par value test calculations to continue reinvestment, ahead of when the payment is actually made to CLO investors. Utilising the calculation of cash (1) in the CLO waterfall and (2) for reinvestment conditions in this manner allows CLOs to maximize equity returns and continue reinvesting for longer.

Taking a longer term view, what trend patterns have you noticed in how CLO documentation has evolved over time and how has this impacted investor risk appetite?

What’s interesting from our viewpoint is how certain areas of CLO documentation has evolved over time. It essentially tells us a story where CLO investors are focussing their attention when it comes to credit concerns, and also where documentation has become more or less flexible over time.

Now, we appreciate that it’s not always easy to identify trends and changes over time – reviewing CLO documents can be complex and involves a meandering of several overlapping terms and concepts. To that effect,

S&P’s Document Review Score (SPDRS) provides some colour on how certain sections in documentation has evolved. The SPDRS helps assess the relative strength of documentation across European CLO transactions, focussing on 15 CLO document parameters that, in our view, may affect CLO performance.

A summary of five of these parameters are given in the heat map below, which solely focuses on Duration Risk. Duration Risk considers key factors that may extend the maturity of the underlying assets in the portfolio.

What’s noteworthy from our analysis is how CLO documentation has evolved over the years with respect to maturity amendment provisions (the first parameter in the heatmap above). This section in CLO documents describes the circumstances in which CLO managers may vote in favour of or against an amendment to the maturity of a loan, i.e. an extension to the loan maturity. During the first half of 2023, CLO investors (and market participations generally) expressed concern around how existing language in amendment provisions was being interpreted – where a socalled “snooze drag” may be enacted, permitting borrowers to disregard CLO lenders who fail to respond to a consent request or otherwise abstain from voting. In response, nearly all CLOs issued in the remainder of 2023 reflected much tighter maturity amendment language: for example, if the CLO manager cannot vote for a maturity amendment then they must vote against it. This has resulted in a ‘cooling’ of the maturity amendment provisions during the Q3 and Q4 of 2023, as shown in the above heatmap.

When it comes to a CLO’s weighted average life test (WAL) (the second parameter in the heatmap above), the way this can be modified has become more flexible. Traditionally, a

WAL test could only be extended via investor consent. More recently, an extension mechanism (typically know as a WAL Step Up) is now embedded within the actual test, making it easier for CLOs to extend the life of the underlying portfolio. The inclusion of this feature has dominated 2023 and 2024 vintage CLOs, and hence is why the heatmap shown above is darker during this period relative to previous years.

There’s been a lot of discussion about launching European middlemarket CLOs. What are you hearing in this regard and where do you see the market heading in terms of issuance and investor appetite?

This topic is becoming increasingly popular with market participants. We’re seeing more reverse enquires coming in regarding the possibility of issuing a European middle market/ direct lending CLO and wouldn’t

be surprised if we see something materialize this year or early next. And now that the first deal is out, we think there will be a lot more interest in doing middle market CLOs in Europe, effectively adding a third stream to the CLO product offering in 2025, i.e middle market CLOs in addition to new issue BSL and refinancings/resets.

In our view the likely starting candidates for issuers of middle market CLOs in Europe will be those managers who already have an established BSL CLO platform and a direct lending arm that they want to securitise and overlay with CLO technology.

To demonstrate proof of concept, we think that the first few European middle market CLOs will likely start with plain vanilla portfolios, for instance, comprising only of eurodenominated loans, limited PIK

features and possibly a small BSL sleeve to complement portfolio diversity. From thereon we may start to see more add-ons coming through, such as sterling- and euro-denominated loans to increase portfolio diversity and PIK-only features on some loans. However, we expect this will come through much farther down the road as the middle market sector continues to expand into Europe.

Members of the Maples Group's CLO team and wider group provide legal support to proposed new Irish disability rights legislation.

The Disability (Personal Budgets) Bill 2024 (the "Bill") was introduced in the Irish Parliament in October 2024 by leading Irish Senator, Tom Clonan, with wide crossparty support.

The Bill’s publication is a significant milestone, especially for the Maples Group, as several partners, associates and trainees worked with Senator Clonan on drafting this Bill and the supporting white paper, in a pro bono capacity. If the Bill is enacted, it will represent an important step forward in the advancement of the implementation of the rights of persons with disabilities in Ireland.

The Bill amends and builds on the existing framework of the Irish Disability Act 2005 and provides for a right for persons with disabilities to receive a personal budget and to select and purchase personal social services. With a personal budget, the individual can tailor the services they purchase to their needs, which in turn enhances independence and self-determination, allowing the individual to shape their own life.

The Bill also coincides with the Disability (Miscellaneous Provisions) Bill 2023 which, if passed, will oblige the Irish State to provide financially for the health needs of persons with disabilities that are identified in an assessment of needs.

Addressing the Irish Parliament, Senator Clonan said, "This Bill will revolutionise the situation for disabled citizens acrosstheIrishStatewhocannotgettheservices,supports, therapies,andsurgeriesthattheyneed.Itwouldtakecontrol awayfromtheIrishHealthBoardandputitintothehandsof disabledcitizensthemselvesandcarers.Thisislegislation thatwillbringusintothetwenty-firstcentury".

Reflecting on the collaborative effort, Andrew Quinn, Tax partner in the Dublin office and member of the Maples Group's CLO team, said, "Thishasbeenahugelyrewarding journeyfortheMaplesGroup,workingwithSenatorConan andhisteam,fromdevelopingtheinitialconcept,through theresearchanddrafting,toafinalBillnowpublished and entered into the records of the Irish Parliament and supportedbyallpoliticalparties".

Claire Morrissey, Data, Commercial & Technology partner and disAbility committee lead in the Dublin office, also praised the Bill’s introduction, "WearedelightedthisBill hasnowbeenintroducedandSenatorClonanwillcontinue tohaveourfullsupportastheBillprogressesthroughthe parliamentaryprocess".

Aligned with the Maples Group's Diversity, Inclusion & Equity strategy, the Group's disAbility committee is proud to be working closely with Disability Legal Network (DLN) and other firms to enhance visibility and promote awareness and understanding of disability within the legal sector.

Those involved in this important project from the Maples Group include Andrew Quinn, Claire Morrissey, Alma O'Sullivan, Ciara O'Rourke, Ciara Ní Longaigh, Gillian Burke, Mairéad Lordan, Mary Gill, Sarah Lydon, Liam Needham, Mary O'Neill and Lynn Cramer.

At the time of publication, the Bill is currently at Second Stage before the Irish Senate.

Andrew Quinn

+353 1 619 2038

andrew.quinn@maples.com

The new OECD Global Minimum Tax, also known as Pillar Two, is an international tax initiative aimed at ensuring large multinationals pay an effective tax rate of at least 15% in every jurisdiction in which they operate by way of imposing new Pillar Two 'top-up taxes' on relevant entities.

An entity can be within scope of the rules and subject to the new top-up taxes if it is consolidated on a line-by-line basis for accounting purposes into a group that has more than €750 million of annual revenue.

CLO issuers, wherever they are established, are typically designed and intended to pay zero or minimal corporation tax at the entity level, since they are a collective pooling or pass-through investment vehicle, and tax is meant to be borne by investors on their respective interests.

The imposition of a Pillar Two top-up tax on a CLO issuer would affect the creditworthiness of the entity, the bondholders' position and the ratings accorded by rating agencies, so it is key that such entities are not subject to substantive tax.

Against this background, the OECD released guidance during the summer that allows jurisdictions to partially exempt a 'securitisation entity' (which includes most CLO issuers) from the rules and the new top-up taxes. This new guidance will be particularly relevant to transactions where the collateral manager or retention holder consolidates the issuer for accounting purposes.

More than 140 countries have committed to the global minimum tax reforms by agreeing to the 2021 "Statement on a Two-Pillar Solution to Address the Tax Challenges Arising from the Digitalisation of the Economy". Approximately 50 of those countries have now published draft or final implementing legislation. The rules are in force in the EU (as a result of an EU Directive), the UK and a number of offshore financial centres. There are some major economies where implementation has stalled – including the US – but the rules have now attained a critical mass and become established in the international tax landscape.

The reforms operate through two mandatory interlocking top-up taxes enacted locally, based on a set of model rules. The income inclusion rule (the "IIR") taxes a parent entity on the profits of its low-tax subsidiaries in other jurisdictions. The undertaxed profits rule (the "UTPR") is a back-stop provision to fill in any gaps where a low-tax entity in the group (regardless of jurisdiction) is not caught by the IIR. The UTPR top-up tax is shared between implementing jurisdictions based on their proportion of the group's employees and tangible assets.

The qualified domestic minimum top-up tax (the "QDMTT", known in the EU as the "QDTT") is an optional third topup tax that allows a jurisdiction to bring the effective tax rate of its own entities up to 15% before other jurisdictions can tax them under the IIR or UTPR. Where a QDMTT in a jurisdiction is deemed to meet certain standards following an international peer review process, a group can elect for no IIR or UTPR top-up tax to arise in respect of the entities in that jurisdiction. This is known as the QDMTT safe harbour.

What does the OECD Guidance say about securitisation entities?

The OECD has continually issued commentary and administrative guidance since the model rules were first published. These materials provide instruction to local tax authorities tasked with translating the model rules into legislation and can serve as aides to interpretation.

The administrative guidance released in June 2024 addresses the application of the rules to securitisation entities. It first clarifies that an orphan securitisation entity is considered part of a Pillar Two group where the consolidating entity has 'control' of the securitisation entity under the relevant accounting standard, even where the consolidating entity does not hold any of the securitisation entity’s ownership interests.

The guidance notes that the QDMTT is the main top-up tax that tends to concern securitisation entities. This is because entities directly holding CLOs are not typically parent entities (so the IIR does not apply) and jurisdictions can choose to allocate UTPR top-up tax away from securitisation entities (and in practice, CLOs rarely have employees or tangible assets).

The guidance sets out three options that a jurisdiction can take in respect of securitisation entities and the QDMTT. The first option is to impose the QDMTT on securitisation entities as normal, i.e. do nothing. The second option is to exempt securitisation entities from the QDMTT. However, a group must then 'switch off' the QDMTT safe harbour in respect of that jurisdiction. The third option is to exempt securitisation entities from the QDMTT, only where the QDMTT liability can be reallocated to a non-securitisation entity.

None of the exemption options is automatic. They require positive action from jurisdictions to implement them. We expect that many jurisdictions will prefer the third option as they will be careful to protect their eligibility for the QDMTT safe harbour. The third option is more limited as it only shifts the liability to another entity and requires there to be at least one non-securitisation entity in the same jurisdiction. Even so, it will be useful to the relevant securitisation entities and interested parties, such as rating agencies, to limit the

securitisation entities' tax risk through this option, where it is available.

It is worth noting that the model rules have broad exemptions for investment funds and certain of their subsidiaries. In our experience, most CLO issuers would not satisfy all the 'investment fund' definition criteria. For example, they may not be subject to an appropriate regulatory regime. In the limited circumstances where a CLO issuer is both an investment fund and a securitisation entity, the existing exemptions for investment funds take precedence, and the securitisation guidance does not apply.

The Maples Group has been very involved in this issue in the main CLO jurisdictions in which we work. The following is a summary of how the OECD guidance is being implemented in those jurisdictions.

Ireland first enacted legislation giving effect to the Pillar Two rules in the Finance (No.2) Act 2023 in December 2023. Ireland elected to impose a QDTT along with the IIR and the UTPR mandated by Council Directive (EU) 2022/2523.

The Finance Act 2024 was passed into law in November 2024 and includes Ireland’s implementation of the OECD guidance. Ireland has chosen the third option set out in the OECD guidance.

In Luxembourg, the Law of 22 December 2023 on Minimum Taxation first implemented the Pillar Two rules in accordance with Council Directive (EU) 2022/2523.

Like Ireland, Luxembourg imposed the IIR, the UTPR and a QDTT. On 31 October 2024, a draft amendment to adopt the third option set out in the OECD guidance was published. The amendment is expected to be voted on before yearend and will apply with retroactive effect as of the initial implementation of the Pillar Two regime in Luxembourg.

Jersey's States Assembly unanimously adopted legislation to implement an IIR and a 15% multinational corporate income tax ("MCIT") in October 2024. The MCIT is modelled on the QDMTT but due to some important differences it is not intended to be recognised as a QDMTT by other jurisdictions or to qualify for the QDMTT safe harbour. Accordingly, the MCIT contains a full exemption for "securitisation entities" (which definition follows the OECD guidance).

The Cayman Islands Government has not announced any plans to introduce the global minimum tax. However, it has agreed to the "Statement on a Two-Pillar Solution" and has said that it will support the reforms through tax transparency and information-sharing measures.

The last decade has seen an explosion in the growth of ETFs across the globe, with global AUM of $2.7 trillion in 2004 growing to over $13.3 trillion in 2024. Assets in European ETFs have grown in line with this trend, now standing at over $2.1 trillion, with assets forecasted to rise 15% annually until 2030, reaching $4.5 trillion in AUM by that date.

While initial ETFs had traditionally been established as passive index tracking products, the past number of years has seen an increase in the breadth of asset classes to which ETFs are gaining exposure and an increase in number of active products being approved on both sides of the Atlantic. There are numerous reasons as to why an asset manager may consider entering the ETF space – in addition to responding to investor demand, asset managers have seen the operational benefits of ETFs and as such, have sought to put their existing strategies into the ETF wrapper. From an investor perspective, the ability to avail of the advantages of an ETF is a significant factor - being able to access a diversified product which offers them greater transparency than would typically be the case with a normal mutual fund is beneficial.

On the European side, Ireland is the domicile of choice with more than 70% of European ETFs domiciled there. Luxembourg is Europe's next largest market (standing at 21%), so the vast majority of European ETFs are domiciled between those two jurisdictions.

Matching the growth of the CLO market itself, a broad range of investors are interested in accessing exposure to CLOs through different mechanisms and one such strategy that has developed in the US and is currently rising in Europe is the ability to gain exposure through mutual funds (UCITS and AIFs), as well as ETFs.

There was heightened interest in the recent launch of an ETF share class by Fair Oaks in its existing UCITS product - Fair Oaks AAA CLO Fund, and we are in conversation with several CLO managers now actively exploring how to replicate similar strategies to broaden their CLO product range.

From both an Irish and Luxembourg regulatory perspective, a CLO is considered a transferable security and, as such, it is possible to gain exposure to CLOs through UCITS and AIFs, as well as ETFs. In a UCITS and ETF context, such products are required to be targeted at non-retail investors only, with related safeguards required to be built into the structure in respect of the target market identification.

Further, at least 80% of the total CLO investment must be restricted to the AAA investment grade tranche, with the remainder being invested in the rest of the investment grade stack. In this, Ireland has effectively moved to match the Luxembourg position, which is a welcome development given the traditional strength of the ETF market in Ireland, as well as the fact the European CLO issuer market is located in Ireland.

One additional consideration is EU Securitisation Regulation compliance. As the ETF is a UCITS as a matter of law, it is subject to this regulation as an institutional investor, meaning it can only hold EU-compliant securitisation positions. For EU-only ETFs, this is not an issue. However, if the ETF is seeking global exposure, it will presently be more restricted in its ability to buy EU-compliant US CLO positions mirroring the general regulatory friction between the US and EU CLOs markets. It is hoped that the reform of the EU Securitisation Regulation currently being consulted upon in Europe will reduce this friction, albeit primarily on the question of transparency reporting rather than risk retention compliance, per se.

If an asset manager is looking to enter the ETF space, the most common routes available to establish an ETF include establishing a new standalone ETF umbrella platform; converting an existing mutual fund into an ETF; adding an ETF share class to an existing UCITS sub-fund (which was the means chosen by Fair Oaks); and adding a new ETF subfund onto an existing platform.

The Maples Group maintains a unique position in the Irish and Luxembourg markets in providing legal advice, registrations and listing services for ETFs across both markets. This, combined with our global CLO practice, means we are best positioned to advise on these structures.

The Maples Group has earned industry-wide recognition for providing bespoke, innovative, client focussed solutions for the establishment and market entry of ETFs on a multijurisdictional basis. Combining expert local knowledge and full project management functionality, the Maples Group delivers a comprehensive suite of solutions to ETF issuers and managers. For example, for asset managers who might be new to ETFs there are fresh operational considerations that are not present in a mutual fund context, like the selection and appointment of authorised participants and market makers, the fragmented European market infrastructure and the variety of dealing and settlement models.

Regardless of the option taken by asset managers, there are a number of points which are required to be considered in the context of the establishment of an ETF. Advance conversations with the fund regulators are encouraged (the Central Bank of Ireland or the CSSF in Luxembourg) and demonstrable familiarity with both the CLO and ETF products are helpful, albeit not determinative (e.g. from a collateral management or market liquidity perspective).

Deirdre McIlvenna

+353 1 619 2064

deirdre.mcilvenna@maples.com

Niamh O’Shea

+353 1 619 2722

niamh.o'shea@maples.com

Colm O’Donoghue

+353 1 619 2116

colm.o’donoghue@maples.com

Wendy Ebanks

+1 345 814 5820

wendy.ebanks@maples.com

Daniel Grugan

+1 302 340 9968

daniel.grugan@maples.com

As many readers will be aware, there has been a significant legal development that may impact the US CLO market and filing obligations under the US Corporate Transparency Act (the “CTA”). On December 3, 2024, the United States District Court for the Eastern District of Texas issued a nationwide injunction on the CTA in connection with the case Texas Top Cop Shop, Inc., et al, vs Merrick Garland, Attorney General of the United States.

Based on the Maples Group's understanding at time of publication, this ruling effectively suspends the enforcement of the CTA and its associated requirements pending further order of the court. The Memorandum Opinion and Order can be accessed here and we encourage consultation with US legal counsel to understand the potential implications and to determine whether any action is required in light of these developments

On December 5, 2024, the Department of Justice, on behalf of the Department of the Treasury, filed a Notice of Appeal and issued a statement saying, “In light of a recent federal court order, reporting companies are not currently required to file beneficial ownership information with FinCEN and are not subject to liability if they fail to do so while the order remains in force. However, reporting companies may continue to voluntarily submit beneficial ownership information reports”. The full statement can be found here

The situation at time of publication is dynamic and may evolve as this case progresses through the courts. The Maples Group will continue to monitor the situation and issue further updates in due course if significant developments occur.

ForfurtherguidanceonCTAcomplianceforCLOmanagersfrom theMaplesFiduciaryteaminDelawareandmoreinformationonour rangeofCTAservices,readour 'CTAChecklistforCLOManagers.' Ourend-to-endCTAservicesincludearrangingEINs,reportingto theFinCENportal,USentityformationandfacilitatingBOIfilings. Wealsoprovideindependentmanagerstoco-issuerentities, effectivelysubstitutingthosekeyindividualsatCLOmanagerswho otherwisewouldbein-scopeandrequiredpersonallytocomply withtheCTA.

There has been a significant legal development that may impact the US CLO market and filing obligations under the US Corporate Transparency Act

Jersey has made productive changes aimed at supporting issuers of debt securities, including CLO issuers, through its most recent regulatory update, which is expected to promote administrative efficiency and a reduction of regulatory costs, further enhancing Jersey's reputation as an attractive jurisdiction for the structuring of debt securities vehicles.

Following recognition by the Committee of Experts on the Evaluation of Anti-Money Laundering Measures and the Financing of Terrorism of the Council of Europe (officially referred to as MONEYVAL) of Jersey's strong performance in the implementation and effectiveness of its anti-money laundering (“AML”) measures, the Jersey Financial Services Commission (the “JFSC”) has moved, in one of various regulatory changes made in recognition of the low risk of AML non-compliance in certain industries, to provide revised guidance in relation to existing AML legislation (the "AML Legislation").

The revised Guidelines on interpretation of Article 36 of the Proceeds of Crime (Jersey) Law 1999 (the "Guidelines") issued by the JFSC in October of this year, brings certain issuers of debt securities outside of the requirement to register with the JFSC under existing AML legislation. The application of the revised guidance to an issuer of debt securities is contingent upon them satisfying the following criteria:

1. that they have obtained a regulatory consent from the JFSC authorising the issue of debt securities. This form of consent is obtained as a matter of practice for all CLO issuers advised by the Maples Group; and

2. the issuer must be able to evidence that the holders of such debt securities are institutional investors. This can be achieved through various means, including an issuer setting sufficiently high minimum consideration thresholds for their securities issue programmes.

Prior to the guidance update, a Jersey body corporate (or other legal person registered in Jersey) participating in the issue of 'securities' – such definition being interpreted in a broad manner by the JFSC, and which included the issue of profit participating notes or similar debt instruments - was under an obligation to register with the JFSC (incurring an upfront and annual registration fee) and adopt certain procedures and practices to comply with the AML Legislation. The AML Legislation did permit issuers to rely upon professional service providers to implement these procedures and practices on their behalf and clients of the Maples Group will be familiar with arrangements put in place to ensure compliance.

With the revised Guidelines, issuers meeting the relevant criteria will no longer be considered to be participating in the issue of 'securities' for the purposes of the AML legislation and, consequently, will be exempt from both the requirement to register with the JFSC and implement the specific procedures and practices required to evidence compliance. Existing issuers of debt securities complying with the previous guidance in relation to Jersey's AML Legislation can also benefit from the revised Guidelines by de-registering their AML regulatory filings and reviewing their procedures and practices for efficiency gains.

With the reduction of administrative obligations and regulatory costs, the Guidelines represent a positive development to Jersey's appeal as a favourable jurisdiction for structuring debt securities issuances and will be welcomed by both prospective and existing CLO issuers, looking to utilise this streamlined and cost-effective framework, while at the same time continuing to comply with the highest international AML standards.

John Dykstra

Partner | Finance | Cayman Islands

+1 345 814 5530 | john.dykstra@maples.com

Joe Jackson

Associate | Finance | Cayman Islands

+1 345 814 5287 | joe.jackson@maples.com

Monette de Luna

Vice President | Structured Finance | Cayman Islands +1 345 814 5846 | monette.deluna@maples.com

What did you do before working at the Maples Group?

Having worked in the Philippines as an external auditor with one of the Big Four accounting firms for six years, the growth in servicing hedge fund audits from my home country around 10 years ago led to an opportunity for me to relocate to the Cayman Islands with EY. I was working in the Wealth & Asset Management group there and after two years I joined the Maples Group in Client Accounting, before transferring to the Structured Finance team. Training in the Philippines coming straight from doing an accounting degree at university could be very intense and demanding at times. In the Cayman Islands I have found the style of working to be quite different. It has

been particularly nice to experience working with people from so many different backgrounds and the social events really help you to get to know everyone.

One of the sayings I like to try and live by is "There are no failures, just learning". What I mean by this is that it’s important not to be too hard on yourself and don’t be afraid of making a mistake. These aren’t mistakes but instead are opportunities to learn and grow from. Rather than stopping us pursuing goals and looking back on failures, I prefer to have a more positive outlook towards life and try to do better next time.

What do you like to do in your spare time?

I live an active lifestyle and work life balance is very important to me, so I am often going to the gym and playing tennis or pickleball. Outside of work, I love cooking for friends. Cooking is like a therapy for me and one of my favourite dishes to make is a Filipino style mung bean soup where I use pork spareribs, with bitter melons, fruits and leaves.

If you could add a word to the dictionary, what would you add and what would it mean?

I think if I could add one word to the English dictionary, it would be a Filipino word, 'Gora'.

Filipino culture has a vibrant spirit and a zest for new adventures, to embrace life with an open heart. Whether it's travelling to a new place, trying exotic foods, or meeting new people, Filipinos are known for their willingness to dive headfirst into experiences. Gora captures that courage, faith, enthusiasm, and optimism in saying yes to a new adventure or experience. So, the next time someone ask you to take on a new adventure and conquer the world, without hesitation respond with "Gora!"

Jonathan Brown

Associate| Finance | Cayman Islands

+1 345 814 5620 | jonathan.brown@maples.com

What did you do before working at the Maples Group?

I was born and raised here in beautiful Grand Cayman.

I attended, Cayman Prep & High School, from kindergarten straight through to the end of high school. After that, I went off to the University of Miami, and studied finance. I have a Bachelor of Science in that, (Go Canes) after that, I headed off to the UK, and studied the GDL and LPC at the College of Law in London. And after that I came back to Maples, and I've been working here ever since.

What is your life's motto?

What is my life's motto? I don't really have one, if I'm going to be honest with you. There is an old idiom that I do quite like, which I got from Pat Riley of the Miami Heat, back in 2006: "Burn the boats".

Basically, when your back is against the wall, don't give yourself the option to give up. You burn the boat, stay on the beach, fight till the end. I quite like that. It's not really a motto, but it's a saying I do quite like.

What do you like to do in your spare time?

In my spare time, I like to fish, spend some time outside, you know, living in the Caribbean, it kind of opens up the all the water sports options, which I'm very much into, though these days, I spend most of it, chasing my 17-month-old son around.

If you weren’t a lawyer, what job would you have done?

100%. I would be a pilot. My dad was a pilot. My mom was a flight attendant. I grew up around airplanes. In my off days back at school, I used to sit in the jump seat and fly with my dad all over the Caribbean.

So, yeah, it would 100% be something to do with aircraft and most likely a pilot.

Our CLO team comprises 33 specialist CLO lawyers and 63 specialist CLO fiduciary professionals across our global network. Since the inception of the CLO market over 20 years ago, we have provided our clients with the benefit of our unparalleled depth of knowledge, experience and insight into what we see across the whole structured finance market, from the latest warehousing structures, to the latest regulatory developments and how they impact CLOs, to ongoing post-closing CLO issues.

For further information, please speak with your usual Maples Group contact or the primary CLO contacts below.

Cayman Islands

James Reeve +1 345 814 5129 james.reeve@maples.com

John Dykstra +1 345 814 5530 john.dykstra@maples.com

Tina Meigh +1 345 814 5242 tina.meigh@maples.com

Jonathon Meloy +1 345 814 5412 jonathon.meloy@maples.com

Anthony Philp +1 345 814 5547 anthony.philp@maples.com

Amanda Lazier +1 345 814 5570 amanda.lazier@maples.com

Dublin

Stephen McLoughlin +353 1 619 2736 stephen.mcloughlin@maples.com

Callaghan Kennedy +353 1 619 2716 callaghan.kennedy@maples.com

Andrew Quinn

+353 1 619 2038 andrew.quinn@maples.com

William Fogarty +353 1 619 2730 william.fogarty@maples.com

Lynn Cramer +353 1 619 2066 lynn.cramer@maples.com

Joe O'Neill +353 1 619 2169 joe.o'neill@maples.com

Michael Gagie +65 6922 8402 michael.gagie@maples.com

Jersey

Paul Burton +44 1534 671 312 paul.burton@maples.com

London

Jonathan Caulton +44 20 7466 1612 jonathan.caulton@maples.com

Luxembourg

Arnaud Arrecgros +352 22 55 12 41 arnaud.arrecgros@maples.com

Yann Hilpert +352 28 55 12 58 yann.hilpert@maples.com

Cayman Islands

Guy Major +1 345 814 5818 guy.major@maples.com

Peter Lundin +1 345 814 5757 peter.lundin@maples.com

Cleveland Stewart +1 345 814 6624 cleveland.stewart@maples.com

Delaware

James Lawler +1 302 340 9985 james.lawler@maples.com

Dublin

Stephen O’Donnell +353 1 697 3244 stephen.odonnell@maples.com

Jersey

Marc Randall +44 7829 933 113 marc.randall@maples.com

London

Sam Ellis +44 20 7466 1645 sam.ellis@maples.com

Netherlands

Allard Elema +31 203 998 233 allard.elema@maples.com