4 minute read

Global oil & gas investments to hit USD 628 billion in 2022

This year, offshore investments are set to increase 7%, from USD145 billion to USD155 billion.

Global oil & gas investments to hit USD628 billion in 2022

Photo courtesy of Petrobras.

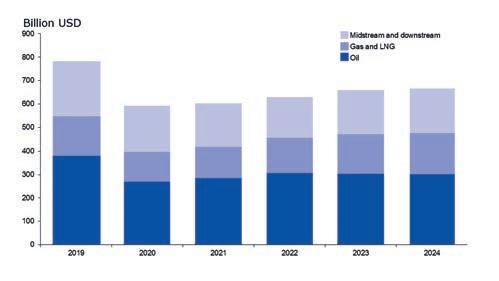

Global oil & gas investments will expand by USD26 billion this year as the industry continues its protracted recovery from the worst of the pandemic and the hurdles imposed by the Omicron variant. An analysis by Rystad Energy projects overall oil & gas investments will rise 4% to USD628 billion this year from USD602 billion in 2021.

Asignifcant factor behind the increase is a 14% increase in upstream gas and LNG investments. These segments will be the fastest growing this year, with a jump in investments from USD131 billion in 2021 to around USD149 billion in 2022. Although this falls short of pre-pandemic totals, investments in the sector are expected to surpass 2019 levels of USD168 billion in just two years, reaching USD171 billion in 2024.

Promising outlook

Upstream oil investments are projected to rise from USD287 billion in 2021 to USD307 billion this year, a 7% increase, while midstream and downstream investments will fall by 6.7% to USD172 billion this year. “The pervasive spread of the Omicron variant will inevitably lead to restrictions on movement in the frst quarter of 2022, capping energy demand and recovery in the major crude- >>

Latin America and Europe will be responsible for around 24% each of the total offshore sanctioning values this year, with deepwater expansions expected in Guyana, Brazil, and Norway. Photo shows Equinor employee at the Johan Sverdrup feld in the North Sea.

consuming sectors of road transport and aviation. But despite the ongoing disruptions caused by COVID-19, the outlook for the global oil and gas market is promising”, says Audun Martinsen, Head of Energy Service Research at Rystad Energy. Drilling further into the numbers, global shale investments are forecasted to surge 18% in 2022, reaching USD102 billion in 2022 compared with USD86 billion in 2021. Ofshore investments are set to increase 7%, from USD145 billion to USD155 billion, while conventional onshore will jump 8%, from USD261 billion to USD290 billion. Regionally, Australia and the Middle East stand out, with Australia likely to see a jump in investments of 33%, thanks to greenfeld gas developments. In the Middle East, investments will rise by an anticipated 22% this year as Saudi Arabia boosts its oil export capacity and Qatar expands production and export capacity of LNG.

Greenfeld projects

This year’s investment growth is very much pre-programmed by the USD150 billion worth of greenfeld projects sanctioned in 2021, up from USD80 billion in 2020. Sanctioning activity in 2022 is likely to closely match 2021 levels, with a similar amount of project spending to be unleashed over the short to medium term. Sanctioning activity is set to rebound in North America, with over USD40 billion worth of projects due for sanctioning in 2022. Six LNG projects are expected to receive the green light, fve in the US and one in Canada. Ofshore projects will also provide ample opportunities for contractors as TotalEnergies’ North Platte project enters the fnal stage of its tender process and LLOG Exploration’s Leon and Chevron’s Ballymore developments in the US Gulf of Mexico look to proceed to the development phase in 2022. For Africa, however, 2022 is expected to be another quiet year with expected sanctioned projects worth a comparatively small USD5 billion.

Source: Rystad Energy Service Cube, Rystad Energy research and analysis.

Global oil & gas investments by market (billion USD).

Regionally, Australia and the Middle East stand out. Photo shows the Thylacine platform at the Otway Basin, offshore Victoria, Australia.

Photo courtesy of Equinor/Ole Jørgen Bratland.

Year-over-year

When it comes to ofshore feld sanctioning, there are around 80 projects worth a total of USD85 billion in the global approvals pipeline for 2022. Of these, ten are FPSOs, 45 involve subsea tiebacks, and 35 are grounded platforms. Latin America and Europe will be responsible for around 24% each of the total ofshore sanctioning values next year, with deepwater expansions expected in Guyana, Brazil, and Norway following recent tax changes. The number of sanctioned ofshore projects is expected to rise year-over-year, but will remain little changed when measured by capital commitments. An outstanding concern for 2022 is execution challenges related to the pandemic and increased infationary costs for steel and other input factors. These are likely to make operators mildly cautious regarding signifcant capital commitments. In addition, major ofshore operators are being challenged on their portfolio strategy as the energy transition unfolds, with many exploration and production companies already directing investment budgets to lowcarbon energy sources.

Photo courtesy of Beach Energy.

Ofshore wind

For ofshore contractors, the energy transition could be advantageous for wind power developments. Spending in the ofshore wind sector reached almost USD50 billion last year, double the 2019 levels. By 2025, Rystad expects ofshore wind investments will rise to USD70 billion as demand for clean energy surges. By contrast, the ofshore oil and gas sector is set to face a challenging energy transition period with oil demand likely to peak in the next fve years, capping ofshore investment at about USD180 billion in 2025.