6 minute read

COVID-19 booster

Boosted by COVID-19, the structure of Asia-North America container trade is changing with increased use of US Gulf and East Coast gateways a fast emerging trend. Andrew Penfold summarises

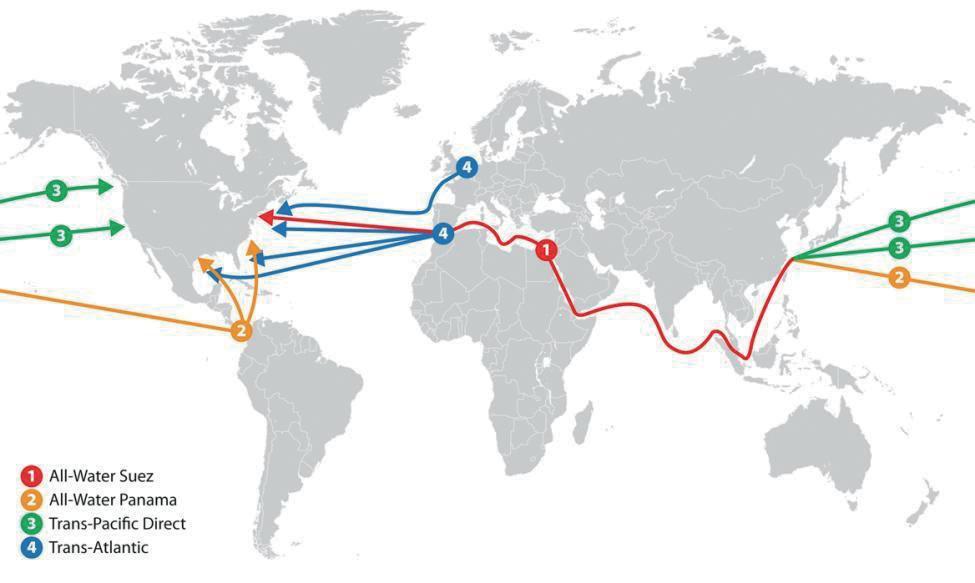

8 The main arterial

trade routes serving North America. Congestion on the West Coast is seeing increased interest in alternate port gateways to access the main US markets

The supply chain disruptions noted since mid-2020 have had far-reaching implications for the Asia to North America container trades. Shipping lines have sought (and found) alternatives to the major West Coast terminals with underlying comparative costs favouring long under-utilised alternatives. Were these trends already underway before Covid and has the pandemic just accelerated latent trends?

The dominant China to San Pedro (Los Angeles/Long Beach) route has been the major driver of overall demand since it began to explode in the mid-1990s and double stack intermodalism became the primary feature of the business. However, several trends have been modifying the position since the mid-2010s, these include: 9 Increased competition from Canadian ports with strong intermodal links to the Midwest. Both Vancouver and

Prince Rupert have seen volumes increase, with this supported by strong investment in capacity and extended intermodal reach. The shorter ocean hauls from China have also been a major factor here. 9 The development of the Panama Canal was a major catalyst. With much larger units – of up to 15,000TEU – transiting the Canal, the all-water route was already seeing increased demand prior to current congestion problems.

The improvement of US East Coast ports has further catalysed these developments. 9 At the macro- level, major importers have sought alternatives to reliance on China. As Chinese production costs have increased there has been a shift to cheaper suppliers in south-east Asia. This trend was already inplace before Covid but is accelerating now for both economic and political reasons. The focus on this region makes the transport costs via Suez competitive on some

North American East Coast trades.

Looking ahead, what does this mean for port development?

WHAT HAS HAPPENED?

The congestion in San Pedro has seen very long berthing delays throughout 2021 and this is continuing. With upwards of 100 vessels awaiting handling, this has effectively reduced the supply side of the container shipping equation and seen freight rates climb to unprecedented levels. The genesis of this situation is complex and results from labour difficulties, supply chain uncertainties and other short-term disruptions. Although the lines have been delighted by the impact of this on their profits the long-term impact is problematic. For some containerised goods the freight rate is now making economic production in China uncompetitive – this was seen as highly unlikely pre-Covid. More onshoring will be the result but (more importantly) new alternatives are being sought.

Sea-Intelligence data shows that at the global level before the pandemic around two per cent of container capacity was accounted for by port delays – the current position is 11 per cent, with no sign of improvement.

In addition to higher freight costs the delivery time for goods has increased dramatically (thus undermining one of the selling points of the San Pedro argument). New data from San Francisco-based forwarder Flexport’s Ocean Timelines Indicator covering export to final delivery indicates average eastbound delivery times have increased from around 50 days pre-pandemic to a high of 110 days in January 2022.

These issues are compounding already established trends.

Total North American port demand since 2010 is summarised in Figure 1. The overall scale of demand is clear, with preliminary data for 2021 indicating a total of over 68mTEU. This is the result of continuing reliance on manufactured imports and the bounce back in demand from Covid (although the sustainability of this with reduced QE from the Federal Government must be questionable). Total North American CAGR was around 6.2 per cent since 2015 – an acceleration over the longer-term trend.

Demand has increased on the West Coast, but this masks some important trends. The market share of each seaboard is summarised in Figure 2. The Pacific Northwest has stagnated in terms of market share, but the poor performance of Seattle/Tacoma obscures the growing importance of the Canadian terminals. More importantly, the market share of Pacific South (San Pedro plus Oakland) has contracted across the period from a peak of over 37 per cent in 2010 to an estimated 33.5 per cent in 2021.

REORGANISATION UNDERWAY

Transport costs from China to the Midwest (the focus of continental demand) were already swinging in favour of the All-Water option ahead of the pandemic, with East Coast ports recording cheaper built-up transport cost (ocean + port + inland) of around US$350-400 per forty-foot container. The congestion related charges have grown this dramatically and this has been directly reflected in increased deployments via Panama to the East Coast ports. Surging demand at established ports (NY/NJ and Virginia) has been joined by other terminals, such as Savannah.

The move by Georgia Ports Authority (GPA) to accelerate capacity additions of around 1.6m TEU per annum at the Garden City Terminal and elsewhere in the port is typical of moves to accommodate increased demand and is representative of developments being noted in other ports. This capacity should be onstream by June – an increase of around 25 per cent in six months. The port has not been immune from congestion, but the speed of response is remarkable and underlines the pace of structural shifts underway. The GPA is also extending its effective reach by adding container yards near major demand locations thus reducing dwell times at the marine terminals.

The speed of reaction at these terminals (together with significantly lower costs) is in sharp contrast to the response of West Coast terminals to market conditions over 2021.

East Coast ports have geared up to accept not just new Panamax vessels but also anticipate Megamax vessel calls from Asia on the Singapore trades. As the centre of gravity moves away from China to ASEAN and Indian suppliers the Suez option will become increasingly realistic.

This does not mean that San Pedro will see volume declines but, rather, that recent shifts in market share will continue. Given current high stevedoring cost structures and intermodal restrictions from California it is difficult to see what steps can realistically be taken to reverse this trend.

The level of interest in new developments in the US Gulf, especially the proposed Plaquemines Parish terminal downriver from New Orleans, further confirms the level of pressure to find alternative routes to/from the Midwest. Utilising the Mississippi system will allow a new route of access and, when combined with strong demand from booming Texan markets and the availability of export opportunities (elsewhere scarce), will further revise the structure of the trades.

PORT DEVELOPMENT IMPLICATIONS

The impact of all of this is complex, but the following seems certain: 9 San Pedro needs to up its game in terms of productivity and intermodal capacity. The drift away from China will accelerate pressures as alternative routes come into play.

Other options are eating away at market share. 9 The Pacific Northwest has been successful, but this has been entirely focused on Vancouver and Prince Rupert.

Capacity is under strain here and some acceleration of capacity is required if hard-fought gains are to be maximised. 9 The East Coast has the opportunity to further build on current gains, with hitherto secondary ports set to further capitalise on lower costs and strong inland links. It is anticipated that strong and sustained investment will be required. 9 New options such as US Gulf/Mississippi terminals offer real potential and there is scope to significantly revise trades from Asia via Panama onto this route.

These trends were well underway in the period following the Panama Canal expansion. Covid has underlined the need for new options and the result will be some fundamental restructuring of the Asia-North American trades in the next few years.