10 minute read

SHAKE-UP SCENARIO?

Does 2022 performance among North-West Europe containerports evidence the seeds of structural change? Johan-Paul Verschuure, Director, Rebel Group, details the trends and analyses this key issue

8 Are the seeds of structural change visible in NorthWest Europe container terminal performance? Will Le Havre emerge as the real winner of the events of 2022?

What started as a promising year for container demand in North-West Europe, ended with a sharp reversal of fortune in 2022. For the third year in a row, container markets were highly volatile and performances varied widely per port, traffic type and quarter. In this article, we analyse the container throughput of Northwest Europe (Le HavreGdansk range) in 2022. A multitude of drivers, disruptions and differences make the trends diverge widely across the region. The question is whether these are structural shifts, a shake-up or will there be some reversals over 2023?

Volumes Down

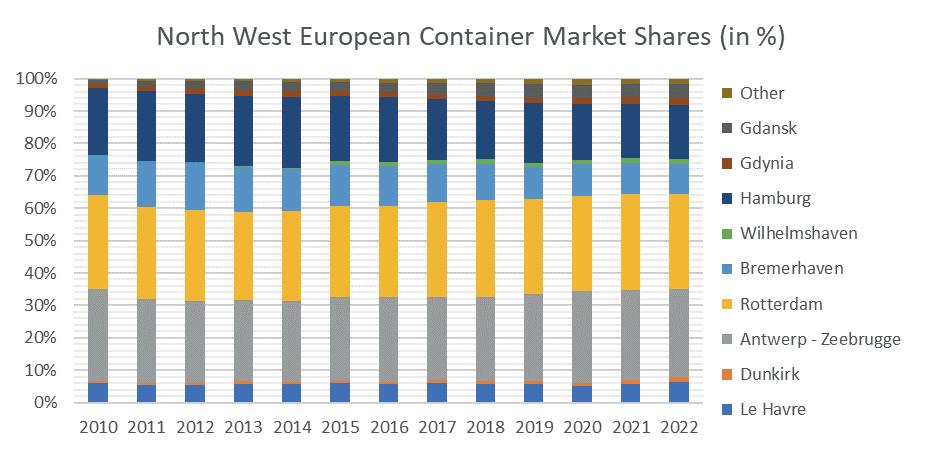

Container handling dropped by 4.3 per cent in 2022 in comparison to 2021 (-2.2 m TEU) over the entire range. This brings the total volume back below 2019 levels but higher than in 2018 and 2020. Le Havre, Dunkirk, Zeebrugge, Wilhelmshaven and Gdansk escaped the declining trend witnessed in the major hubs. The French ports, Zeebrugge and Wilhelmshaven proved good alternatives to their congested counterparts in other parts of the range.

Gdansk saw demand in its domestic hinterland increase, driven by macro-economic demand expansion. On top of this, Polish ports were handling additional rerouted Ukrainian port volumes. The relatively good performance of the eastern ports represents an extension of recent trends. Overall, French and Polish ports gained market share at the expense of (in particular) German ports and to a lesser extent from Dutch and Belgian ports.

However, there is more to the figures than just these headlines. What is most striking is that the total reported decline in tonnage terms is even larger than in TEU. The decrease in the major hub ports in tonnage was almost double that of the decline in TEU. In particular, laden export volumes took a beating. A large number of empties has partially compensated for the even faster decline in laden containers in major hubs. As a consequence of slowing demand, an increasing flow of empties are reported as being idle, with this putting increasing pressure on storage areas, but for different reasons than during the COVID-19 pandemic.

Performance Divergence

There is a wide divergence noted over 2022 performance. The ports of Antwerp and Bremerhaven reported some improvement in the second half of the year after sharp declines in the first half, where performance was shaped by the Ukrainian conflict and congestion. The partial recovery was mostly reported in Q3. Also, Le Havre recorded its growth in 2022 in the second half of the year. In contrast, Hamburg suffered from long strikes last summer and as a result recorded its entire decline solely in the second half of the year. This after the port reported an increase of almost one per cent even in the first half of 2022. Rotterdam also saw a worse second half of the year in comparison to the first half, following slowing macro-economic growth and renewed COVID-19 lockdowns in China.

The decline at the major hubs was to a large extent resulting from lower transshipment volumes. In the first half of the year liners pushed out transshipment activity from congested ports. In addition, transshipment and shortsea activity to/from Russia resulted in lower throughput volumes in the range. With St Petersburg having handled just over 2m TEU in 2021 before the conflict, the sanctions on this trade were felt throughout the range. In this context, it must also be noted that the port of Klaipeda (outside the considered range in accompanying graphics) reported an increase of 57 per cent in container throughput in 2023, up from 0.67m TEU to 1.05 m TEU. Also, Tallinn reported an increase of 18 per cent in 2022. These increases were partially due to cargo diversion from Russia.

Small Ports Outperform Major Hubs

Smaller ports (<2.5m TEU throughput) outperformed their bigger counterparts again. These ports expanded their market shares, both as a result of congestion in major container hubs in the first half of 2022 and the dropping away of Russian container volumes at transshipment ports. This was an extension of the trend since 2016 and brings the market share of the smaller ports to around 19 per cent in the considered range – a sharp increase from the level of 12 per cent noted in 2015.

In line with smaller ports performing well the share of intra-European trade increased again. Since the beginning of the pandemic in 2020, shortsea container volumes have seen their share of total container throughput increase. Dedicated shortsea terminals have been performing well. The Ro-Ro sector actually achieved even higher growth rates as shortsea demand accelerated.

Uk Ports Stable

UK ports saw a decline in volume in 2022, but the UK’s market share has stabilised vis-à-vis the Northwest European range. Since 2016, UK container volumes lost ground relative to their European counterparts. Lower exposure to Russian cargoes has recently benefitted their relative performance. UK volumes in 2016 were 23.2 per cent of Northwest European container volumes to further decline to 20.1per cent in 2021 and rose to 20.3 per cent in 2022. The strikes in Felixstowe however did have a severe impact on container throughput. London Gateway was the key beneficiary of the strike at Felixstowe with Southampton keeping its volume relatively stable.

WHAT NEXT?

2022 was the third year with significant shifts in the container market traffic volumes and routings. The question remains –as in the demand increase during the COVID-19 pandemic –will these changes be structural?

Demand seems set to remain slow following weak macroeconomic growth with this extending the trend of Q4 2022. With persistent pressure on energy and commodity prices, it seems the era of ultra-loose monetary policy will be shelved for the foreseeable future.

Container demand will, however, enjoy a bit of a tailwind from the renewed containerisation of breakbulk. Driven by high freight rates in 2021, breakbulk was taken out of the containers and shipped by multipurpose vessels once again. With the sharp decline in freight rates, containerisable breakbulk will find its way back into the container terminals.

With congestion disappearing as rapidly as it emerged in 2020, it can be expected that the mainline calls will prefer to emphasise their hub-focused networks. The network benefits from these hubs, combining gateway and transshipment, will be even more important given low the fleet utilisation level now. With the large number of newbuilds coming onto the market in the coming two years, the pressure to consolidate volumes will be even higher. Accordingly, the good fortune of the smaller overflow ports is likely to be reversed in the short term.

The smaller ports can continue to benefit from increased shortsea volumes, greater feedering from the major hubs as lines focus on large vessel utilisation rates and the popularity of other niche trades. This has supported the market share expansion of the smaller ports in the last few years and is likely to persist, driven by an increased focus on shortseabased supply chains.

Russian volumes are unlikely to return any time soon and this will leave a gap at the major hubs. However, shortsea terminals are also feeling the impact. This will, however, be partly offset by growth in other Baltic and East European ports. Good feeder networks to the Baltics will be essential for hub port volume growth.

The more structural winner seems to be Le Havre driven by its long-term commitment and investments announced by MSC. It provides MSC with another option to route its cargo over one of their many container terminals in the range. The strikes this time were focused on Germany while French terminals kept operating without strikes. If this continues to be the case, Le Havre may be the real winner of the events of last year and finally realise its long-constrained potential.

8 North-West Europe container volumes and market share 2010 – 2022 inclusive

Hosted by:

Growing Sustainable Supply Chains: Short Sea Shipping & Intermodal Networks Conference Programme

Royal Liver Building, Liverpool, UK

Sponsor: Supporters:

A neutral pan-European network dedicated to the promotion of short sea and feeder shipping and the intermodal transport networks that support the sector.

Chairman: Nick Lambert, Co-Founder & Director, NLA International Ltd visit: coastlink.co.uk contact: +44 1329 825335 email: info@coastlink.co.uk

#Coastlink

Media partners: GREENPORT

DAY ONE – Wednesday 3th May 2023

08:30 Coffee & Registration

09:00 Chairman’s Welcome

Nick Lambert, Co-Founder and Director, NLA International Ltd

SESSION 1: MARKET SECTOR OVERVIEW - THE NEW NORMAL IN AN ADAPTING MARKET

Considering Trends, Market Forces, and emerging Opportunities for Short Sea Feeder Services and Logistics

09:10 Port’s Welcome Address

Claudio Veritiero, CEO, Peel Ports Group

09:25 Gold Sponsor’s Address

09:35 Keynote Presentation

Robert Clegg, Short Sea Director United Kingdom, Containerships CMA CGM GmbH

09:50 Network Development & Appraisal in the Short Sea Sector

Mike Garratt, Chairman, MDS Transmodal

10:05 Building a case for a greener transport alternative for smaller cargo volumes –

Short Sea Shipping and intermodal cargo flow

Michael Rosenkilde Lind, Senior Commercial Manager, Port of Aalborg

A presentation from the Port of Aalborg with the research and findings of the process of trying to establish a new Ro/Ro route with only smaller local stakeholders along with major cargo flows on rail in transit.

10:20 Q&A

10:40 Coffee & Networking

11:15 PANEL DISCUSSION: Post-Brexit & Post-Pandemic: Are we where we need to be?

Panel Moderator: Richard Ballantyne OBE, Chief Executive, British Ports Association

Panellists include:

Doug Bannister, CEO, Port of Dover

Howard, Knott, IEA Logistics Consultant, Irish Exporters Association

Andima Ormaetxe Bengoa, Director - Operations, Commercial, Logistics and Strategy, Port of Bilbao Authority

Sean Potter, Commercial Director, DFDS A/S

12:30 - Lunch & Networking

14:00

SESSION 2: HOW TO PROMOTE GROWTH AND DELIVER RESILIENT END TO END SUPPLY CHAINS

A look at the changing landscape in end-to-end intermodal networks & the just in time supply chain.

14:00 Opening Address

Michelle Gardner, Deputy Director – Policy, Logistics UK

Logistics UK will highlight the opportunities in the supply chain for innovation and modal shift to benefit the environment and consumers as well as operators throughout the supply chain.

14:15

What mode of transport uses Ports?

Stephen Carr, Group Commercial Director, Peel Ports Group

We explore why the true answer to that question defines why both industry and consumers need to think differently about the role and the functions of modern ports.

14:30

Practical examples of building resilience into a supply chain using intermodal services

Geoff Lippitt, Chief Commercial Officer, PD Ports

How intermodal, short sea shipping, RoRo, LoLo and last mile delivery road haulage can interlink to provide resilience and enhance capacity for ports and operators

14:45 Port of Antwerp-Bruges – providing total intermodal connectivity solutions

Justin Atkin, UK & Ireland Representative, Port of Antwerp-Bruges

With excellent connections to the hinterland by estuary and inland barge, rail, road, and pipeline, discover how the Port of Antwerp-Bruges provides totally integrated transportation solutions, helping shippers

15:00 Q&A

15:20 Coffee & Networking

15:50 PANEL DISCUSSION: Freeports: Driving change for coastal shipping and the supply chain?

A discussion on the impacts and benefits of Freeports. How will supply chains adjust? Xx

Panel Moderator: Richard Ballantyne OBE, Chief Executive, British Ports Association

Panellists include:

Giles Jones, Project Manager, Liverpool City Region Freeport

Nolan Gray, Freeport Director, Tees Valley Combined Authority

Arne Mielken, Managing Director, Customs Manager Ltd

17:15 Conference Day 1 Wrap-Up – Conference Chairman

17:30 Conference Close

17:30 Evening Drinks Reception at the Royal Liver Building

18:45 Conference Dinner at the Royal Liver Building

DAY TWO – Thursday 4th May 2023

08:45 Arrival: Coffee

SESSION 3: SUSTAINABILITY & THE ENERGY TRANSITION – A ROUTE TO SHIPPING FREIGHT SUSTAINABLY

The journey and challenges for ports, shipping & logistics in achieving net zero

09:10 Chairman’s Opening & Summary of Day 1

09:15 Keynote Presentation

David Browne, General Manager, MAERSK

09:30 A Green Port’s Journey to Net Zero

Tanya Ferry, Green Port Consultant, Royal Haskoning DHV

Learn how Royal HaskoningDHV is helping the world’s ports embrace digital innovation, decarbonisation, and new-found resilience. And discover the challenges, savings, and operational benefits to be found on the journey to Net Zero.

09:45 Port of Amsterdam – At the forefront of the transition

Mark Hoolwerf, Deputy Director, Port of Amsterdam International

The port of Amsterdam is a global energy hub, meaning that it stands for a significant decarbonisation challenge. This presentation will focus on how the Port of Amsterdam approaches the energy transition, with a focus on its overall strategy and recent initiatives and developments. This will include subjects such as the role of hydrogen, clean shipping, and the collaboration with different parts of the value chain.

10:00 Lessons learned with shore power

Jacob Bjarkam, Business Development Manager, PowerCon

Shore power is expected to be scaled tremendously. PowerCon will provide key insights and lessons learned on how to best to implement this technology successfully, by sharing hands-on experience from past projects plus the latest news and innovation.

10:15 Q&A

10:40 Coffee & Networking

11:20 PANEL DISCUSSION – Driving Efficiency through Data & Port Collaboration

Improving supply chain efficiency through data, collaboration, and digitalisation

Panel Moderator: Tim Morris, Head of Corporate Communications, Associated British Ports

Panellists include:

Richard Willis, Technical Director - Port Operations & Technology, Royal HaskoningDHV

Eleni Bougioukou, Innovation Manager for Energy & Sustainability, Port of Tyne

Grant Hunter, Director - Standards, Innovation and Research, BIMCO

12:35 Conference Wrap up by Conference Chairman

12:45 Lunch & Networking

14:15 - 16:45 Technical Visit & Working Group

Delegates can enjoy a tour of the Port of Liverpool encompassing Liverpool 2, which will be hosted by Peel Ports Group. Delegates also have the opportunity to collaborate in the afternoon working group.

*invited

Conference Fee

Premium Package

£625GBP/ €750euro

Cost per delegate

Standard Package

£590GBP/ €710euro

Cost per delegate

Fee Includes

• Conference attendance including lunch & refreshments

• Electronic documentation

• Technical Visit 4 May 2023

• Conference Dinner 3 May 2023 (Premium Package)

• Presentation download (Premium Package)

Booking Online coastlink.co.uk/buy or complete and fax the booking form below to +44 1329 550192. On receipt of your registration, you will be sent confirmation of your delegate place

Contact Us

For further information on exhibiting, sponsoring, or attending the conference, contact the Events team on: +44 1329 825335 or info@coastlink.co.uk

Venue Royal Liver Building, Pier Head, Liverpool L3 1HU, UK Visit coastlink.co.uk