4 minute read

NORTH AMERICA OUTLOOK

by Dr. Chris Kuehl

United States Outlook

The economic forecast has resembled one of those slasher movies where there is a threat around every corner, and clueless teens are dropping right and left. Each week seems to bring a new challenge, and the media continues to feed a never-ending desire for drama. The bank crisis was depicted as the end of modern civilization and the trigger for a return of the Great Depression. On closer examination, the issue was one of a few badly run banks paying for their sins. For those that want to trust in the data and avoid the hysterical commentary, it has been frustrating as there have been as many positive developments as there have been negative ones.

A report from the Brookings/Financial Times tracker asserts that economic conditions around the world are far better than they were expected to be. Growth is expected in the U.S.,

U.K., Eurozone, Japan, and China.

The consumer has been affected by inflation, to be sure, but they are still active – especially those in the upper 30% of income earners. The estimates for GDP growth have been bouncing around over the last few weeks. A month ago, the GDP Now estimates from the Atlanta Fed were 2.6% growth and then 3.2% but in the last week that number was ratcheted down to 1.7% and most recently to 1.5%. The decline has been attributed to a slower pace of consumer spending, and that has been blamed on some adjustments in the labor market. After nearly a year of hiking interest rates in an attempt to slow the economy, the Fed is starting to see some reaction in the labor market.

signs of upward movement. The other factors that affected growth include the bank fiasco, as investors froze for over a week and millions of dollars sloshed from bank to bank as depositors tried to figure out where they could locate a safe haven.

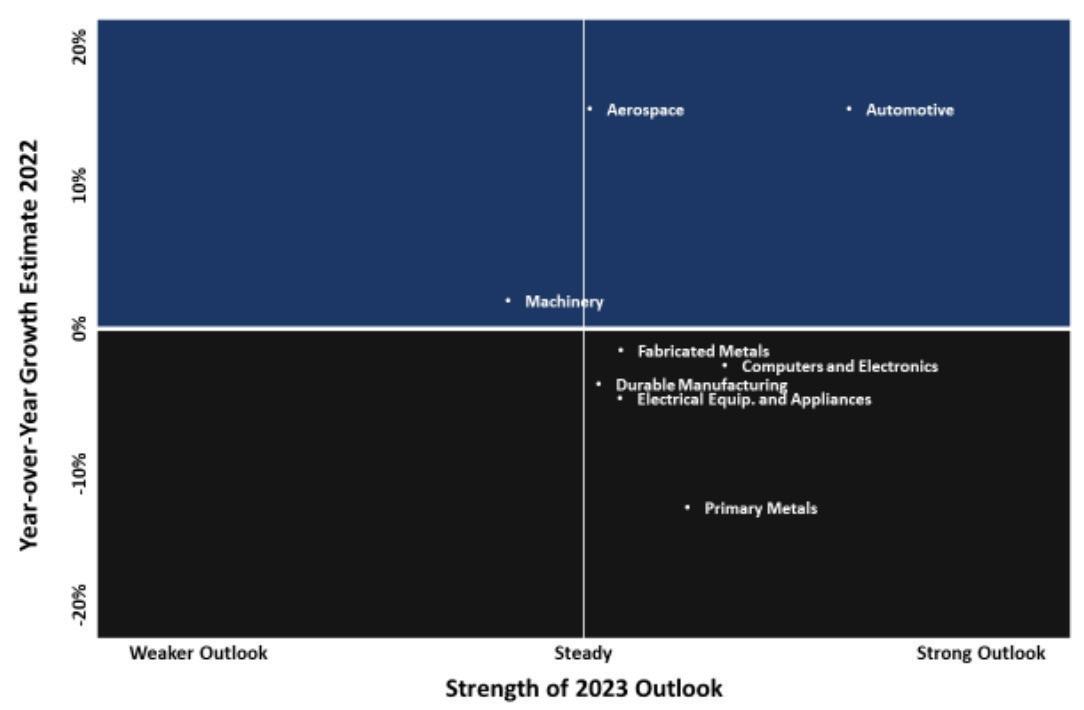

The longer-term estimates are more encouraging – especially for manufacturing. The ongoing disenchantment with China has continued to fuel reshoring efforts. The fastest growing segment of commercial construction has been manufacturing, as new facilities are needed to accommodate the shift from China and the growth in the use of robotics and technology. The inhibitions regarding reshoring remain as they have been – worker shortage and the need to find adequate transportation for both inbound and outbound activity. In the latest ASIS matrix, there are several industrial sectors that still show solid growth

There are fewer jobs on offer, although the number of open positions remains high. There are 9.9 million openings, but that is down from 10.9 million a month ago. The rate of joblessness remains very low but has shown some continued

– automotive and aerospace still lead the pack. Many of the other sectors still have a reasonable outlook for the coming year but see slower growth numbers than were evident in 2022.

The Armada Strategic Intelligence System is an examination of the industrial sector as defined by the Federal Reserve’s industrial production measure. We strip out the data on utilities and mining to isolate just the manufacturing sector. Most of the sectors are going through a similar period of adjustment. There was significant inventory build in the last year as companies tried to cope with a broken supply chain. This has saddled around 70% of businesses with excess inventory levels. Until that supply is gone, there will be little reordering. That cycle usually manifests this time of year, and now it is estimated that reorders will not resume until late summer or early fall.

For the U.S., the message is still confusing. There are as many reasons to be somewhat optimistic as there are reasons to retreat. Even the big analytical organizations are providing contradictory reports. The head of the World Bank has been preaching gloom and doom at the same time that her own organization has been proclaiming better progress than expected for the world economy.

Canadian Outlook

The outlook for the Canadian economy is as mixed as it has been for the U.S. The Bank of Canada has asserted that it is sticking to the 4.5% level with the interest rate, but there have been developments in the labor market that are testing that resolve. The rate of unemployment has remained very low at 5.0%, and there has been job growth for the last four months despite the hikes. More importantly, there has been continued wage growth and that undermines the efforts of the BoC. The drivers of the Canadian economy are still intact. Commodity demand has been solid and the manufacturing sector has mirrored what has been taking place in the U.S. The strongest sector for U.S. manufacturing has been automotive, and that is also the sector in Canada that is most closely linked to the U.S.

The analysis from the Royal Bank of Canada still holds that there will be a mild recession in the middle of the year. The rate hikes tend to have a lagging impact, and most of the response will be seen in second and third quarter. It has been noted that consumer sectors are already starting to lag – the housing sector is moribund (at least for single family) and the global manufacturing numbers have been down. That affects demand for Canadian commodities as well as the manufactured goods that go into other assemblies.

Mexican Outlook

A few months ago, the Finance Ministry in Mexico asserted that 3.0% growth was likely in 2023. Most dismissed this claim as wishful thinking but now it looks far more accurate than those more pessimistic forecasts. The economy is on pace to grow at least that fast in the first quarter and is expected to pick up speed as the year progresses. In the fourth quarter of last year, the pace fell to 0.5%, and in Q3 it was at 0.9%. The 3.1% expansion in Q1 has been attributed to recovery in all four major economic sectors for the country. Manufacturing is the number one driver and has been boosted by record levels of foreign direct investment. The FDI pace is unprecedented, and 45% of it is brand new. This is mostly attributed to the shift in supply chain options from China. Companies that still need a low labor cost environment are finding opportunities in Mexico. Tourism is making a comeback as the pandemic threat starts to ease. Remittances from the Mexican workers in the U.S. continues to be a major source of national income, and the fourth pillar is oil production. The recent hike in the per barrel price will benefit Mexico.

Author profile: Dr. Christopher Kuehl (Ph.D.) is a Managing Director of Armada Corporate Intelligence and one of the co-founders of the company in 1999. He has been Armada’s economic analyst and has worked with a wide variety of private clients and professional associations in the last ten years. He is the Chief Economist for the National Association for Credit Management and is on the Board of Advisors for their global division –Finance, Credit and International Business. n