6 minute read

8.11 CARBON OFFSETS

Description

This Strategy advocates for a net zero emissions reduction target for Council’s operations by 2040. It is feasible that by this time most emissions from energy will have been eliminated, however some emissions may remain, for example in heavy fleet such as trucks and large road plant, as well as waste. Future revisions to this Strategy may consider Council’s supply chain emissions, such as emissions in goods and services that Council purchases. These are referred to as scope 3 supply chain emissions, and Australia’s Climate Active standard sets out methodologies for estimation of these that are aligned with global standards.

Given the potential for Council to have residual emissions by 2040, it is prudent to be aware of carbon offset options that are available that could help Council to achieve its targets. This section outlines the national standard for carbon neutrality and what this may look like for MidCoast Council given the experience of other local councils.

What is Climate Active?

Currently, the ’gold standard’ for carbon neutrality in Australia is Climate Active certification (formerly the ‘National Carbon Offset Standard’, or NCOS). NCOS was launched by the Australian Government in 2010 to provide a credible framework for achieving carbon neutrality. Initially, the Standard was designed for organisations, products and services and was expanded to events, buildings and precincts in 2017.

The Climate Active Carbon Neutral Standard for Organisations (Organisation Standard) is a voluntary standard to manage greenhouse gas emissions and achieve carbon neutrality. It provides best-practice guidance on how to measure, reduce, offset, validate and report emissions that occur as a result of the operations of an organisation (encompassing scopes 1, 2 and 3 emissions as explained earlier). Further information is available at www.climateactive.org.au.

What additional emissions might MidCoast Council need to consider?

As well as residual scope 1 and 2 emissions (such as from transport fuel), Council may need to consider its supply chain scope 3 emissions under Climate Active, including:

1. Purchased goods and services

2. Capital goods

3. Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

4. Upstream transportation and distribution

5. Waste generated in operations

6. Business travel

7. Employee commuting

8. Upstream leased assets

9. Downstream transportation and distribution

10. Processing of sold products

11. Use of sold products

12. End-of-life treatment of sold products

13. Downstream leased assets

14. Franchises

15. Investments

An assessment of each data category will highlight those sources that must, should and do not need to be included in a Climate Active-compliant carbon inventory, based on an assessment of how relevant these sources are to MidCoast Council.

What might MidCoast Council’s emissions be under Climate Active?

For regional local governments it is typical for works associated with road and pavement construction and maintenance to be significant sources of supply chain emissions, including from concrete / cement, reinforcing or pipe steel and bitumen / asphalt. Other building construction is also significant, but tends to be an irregular source of emissions. Other relevant emissions sources usually include the procurement of business services, business travel, information technology services, communications, postal services, paper consumption, water consumption, etc. Employee commute emissions may also be relevant and are commonly included.

A typical scope 3 supply chain carbon footprint can add substantially to existing reported energy and waste emissions from Council’s operations, with 20-40% increase seen in relevant examples.

Options to reduce Council’s supply chain and residual scope 1, 2 emissions

If Council has residual emissions in 2040, and was to determine that its greenhouse gas emissions reduction target should extend to Council’s scope 3 supply chain emissions, then three primary options will be available to achieve reductions in these:

• Extend sustainable procurement to encompass the emissions embodied within goods / capital works materials that Council purchases, and to encourage, incentivise or require suppliers to reduce their carbon footprint

• Implement local sequestration projects, including through Council’s Greening

Strategy and through continued restoration of local wetlands. These sequestration / blue carbon initiatives are likely to be difficult to measure in terms of carbon sequestration

• Purchase carbon offsets to reduce residual emissions, including consideration of abatement as well as sequestration / removal offsets.

What other Councils have been certified under Climate Active?

The following is a list of Councils that have undergone Climate Active certification42 .

• Bayside City Council • Brisbane City Council • City of Adelaide • City of Melbourne • City of Sydney • City of Yarra Council • City of Moonee Valley • Maroondah City Council • Moreland City Council • Randwick City Council • Woollahra Municipal Council

Instead of full Climate Active certification, Councils can decide to self-certify their carbon neutral status. The recommended way to undertake self-certification is to use the Climate Active Standard for guidance, from determining the boundary of the carbon footprint and preparation of the carbon account to the purchase of carbon offsets. The following Councils have undergone self-certification:

• Maribyrnong City Council • City of Fremantle43

Scope for abatement

Carbon offsets will enable Council to achieve a net zero emissions target by 2040, with the amount of offsets required dependent on the boundary of Council’s carbon footprint and the success of abatement and sustainable procurement measures in reducing this footprint.

Key decisions that Council would need to take include the role of abatement offsets (e.g. from renewable energy projects elsewhere) and sequestration offsets (e.g. from regional / national tree planting schemes).

Risks and mitigation

Two of the principal risks associated with purchasing carbon offsets and achieving Climate Active certification are:

• Purchasing reputable carbon offsets and balancing cost and offset sources (see the main types of offsets below),

42 https://www.climateactive.org.au/buy-climate-active/certified-brands#category1 43 https://www.fremantle.wa.gov.au/towards-zero-carbon

• Data collection systems integrity including records management, data analysis frameworks and methods to receive and handle data from multiple sources on a recurrent basis

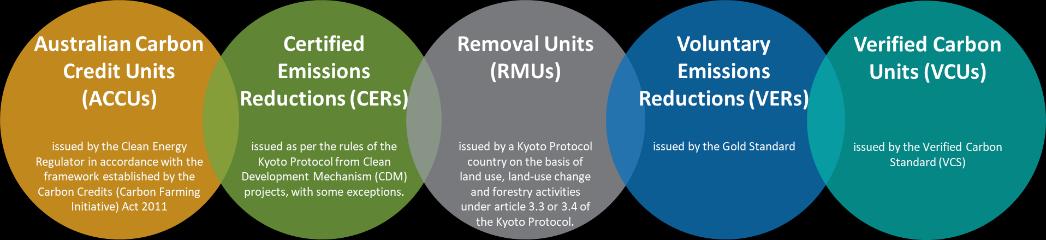

ACCEPTED OFFSETS FOR CLIMATE ACTIVE CARBON NEUTRAL CERTIFICATION

• Australian Carbon Credit Units (ACCUs) issued by the Clean Energy Regulator in accordance with the framework established by the Carbon Credits (Carbon

Farming Initiative) Act 2011 which has now been amended to establish the

Emissions Reduction Fund (ERF).

• Certified Emissions Reductions (CERs) issued as per the rules of the Kyoto

Protocol from Clean Development Mechanism (CDM) projects, with some exceptions.

• Removal Units (RMUs) issued by a Kyoto Protocol country on the basis of land use, land-use change and forestry activities under article 3.3 or 3.4 of the

Kyoto Protocol.

• Voluntary Emissions Reductions (VERs) issued by the Gold Standard.

• Verified Carbon Units (VCUs) issued by the Verified Carbon Standard (VCS).

When deciding what offsets to purchase, the location, type, volume, price and accreditation standard would ordinarily be taken into account. In particular organisations will typically evaluate the balance between price (e.g. for high volume international offsets) and location (e.g. Australian removal offsets) or sustainability credentials.

Costs and benefits

The cost to offset an organisation’s emissions is a function of the actual offset projects selected, their location, the volume of offsets purchased, the accreditation standard under which offsets have been created, and market demand and supply. In the current market offsets can be purchased for as little as ~$1.50/offset and up to $18/offset.

Costs for licensing and verification would also be considered so that the full cost of offsets can be estimated and used to inform future decisions by Council.