ANASTASIA DONDE Senior Editor, Middle Market Growth adonde@acg.org

If you’ve been following M&A trends for a long time, you’ve likely noticed that investment in certain sectors is cyclical by nature. Consumer and pockets of industrials or energy often follow economic cycles or consumer confidence. At the same time, private equity tends to create its own cycles—where many firms move in herds and follow the same trends.

In an On the Horizon piece on p. 34, executives from GF Data and Private Equity Info say that “many private equity firms tend to have similar industry focuses over time; some industries are in vogue for private equity at certain times, while other industries cycle out of favor.” In the article, they study data from both platforms to explore whether private equity piling into certain sectors impacts valuations. Cycles aren’t just about sector trends or economic peaks and troughs. Certain investment ideas or strategies can move in cycles, too. This issue’s Deal Roundup on p. 8 explores a trend among take-private deals, which was also a topic of a feature story in Middle Market Executive in the summer of 2022. At the time, deal volume and stock performance was just starting to go south and some investors had surmised macro headwinds could lead to more take-private opportunities.

Now, we’re almost two years into an M&A slump and delisting middle-market companies can be one avenue to explore amid a dearth of deals in the market. In some cases, smaller public companies are going unnoticed by analysts and don’t see a lot of trades. Others might be undervalued for unclear reasons, and the frequent performance reporting and public scrutiny that come with being publicly traded might weigh on executives and their growth plans.

The topic of the cover story (p. 50) in this issue is ESG and DEI, an area we also explored in depth in a fall 2022 issue, but it seems sentiment has changed since then. Investment firms increasingly say they’re following in their LPs’ footsteps when it comes to ESG priorities and LPs are split, with some championing ESG and DEI initiatives and others dropping them. A speaker at ACG’s DealMAX event this year described it as “swinging pendulum” where sentiment will continue to sway back and forth but should eventually reach an equilibrium.

Wherever our readers find themselves in some of these cycles, it’s often helpful to see the patterns, and either jump into the lucrative trends or break apart from the herd. //

42 DEVELOPING CORPORATE GOVERNANCE FOR AI

Artificial intelligence is all the rage, even as organizations struggle to develop rules of engagement. AI governance has been hampered by patchwork regulations, a lack of understanding about the technology, and little clarity around who within a company should be responsible for oversight.

50 THE SWINGING PENDULUM OF ESG PRIORITIES

Political backlash over environmental, social and governance considerations in investing has forced private equity firms to reconsider if and how to include ESG as part of their strategies, and how to strike the right balance between values and value creation.

CEO Brent Baxter bbaxter@acg.org

VICE PRESIDENT, ACG MEDIA

Kathryn Maloney kmaloney@acg.org

SENIOR EDITOR

Anastasia Donde adonde@acg.org

DIGITAL EDITOR

Carolyn Vallejo cvallejo@acg.org

ASSOCIATE EDITOR

Hilary Collins hcollins@acg.org

SENIOR ART DIRECTOR

Michelle Bruno mbruno@acg.org

GRAPHIC DESIGNER

Mary Parrish mparrish@acg.org

VICE PRESIDENT, SALES Kaitlyn Gregorio kgregorio@acg.org

ADVERTISING SALES ASSOCIATE

Kelly Matava kmatava@acg.org

Association for Corporate Growth membership@acg.org www.acg.org

Copyright 2024 Middle Market Growth® and Association for Corporate Growth, Inc.® All rights reserved.

Printed in the United States of America.

ISSN 2475-921X (print) ISSN 2475-9228 (online)

There are a lot of moving parts to any M&A deal — but when you buy a company, it’s the people who drive the numbers. That’s where we come in. From navigating delicate transitions to streamlining talent management with a host of HR tools and resources, Insperity can help your portco reach its full potential. We’re your partner for harnessing the human factor — that vital area where business objectives and employee engagement align.

Develop a strong human capital strategy with Insperity, ACG’s preferred HR solution for middle market companies.

FULL-SERVICE HR EMPLOYEE BENEFITS HR TECHNOLOGY

insperity.com/acg | capital.growth@insperity.com

There comes a time when you’re ready to move boldly—to invest in yourself and your business by using what you have to fund where you want to go. At Cadence, we help power those dreams with simple, affordable business financing that leverages your assets.

In a scarce deal environment, PE investors are increasingly eyeing public companies to take private.

Comvest Partners’ Alex Ray and Maneesh Chawla explore the stark divide between bank-led auctions with high demand and those with little to no interest.

Lincoln International’s Max Golembo analyzes current M&A trends, along with market challenges and opportunities ahead.

Once exclusively reserved for institutional capital, private equity is making inroads with retail investors.

Recent hires and promotions among middle-market investors and advisors.

In a limited M&A environment, investors are scouting for middlemarket take-private opportunities

Amid a slowdown in M&A activity over the last few years, private equity investors are looking in every corner for investment opportunities, leading some to turn to public companies that they can take private.

A November 2023 survey by law firm Dechert found that 94% of respondents are likely to pursue take-private deals—a major increase from 2022, when only 13% of GPs expressed intentions of pursuing such transactions. Those firms are now scouring the public markets to find potential companies to acquire, Dechert found.

The emergence of interest in take-private deals reflects larger forces at play in M&A, says Justin W. Steil, partner and head of the transactions team at MiddleGround Capital, a Lexington, Kentucky-based private equity firm. In June, MiddleGround invested in L.S. Starrett Company, a Massachusetts-based publicly listed tool manufacturer that was founded in 1880 and incorporated in 1929.

BY ANNEMARIE MANNION

“You are seeing the slowdown in M&A translate to fewer private equity exits,” Steil says. “In the absence of private equity firms bringing their

portfolio companies to market, firms like ours are working to be more creative in finding new investment targets, such as publicly traded businesses, to maintain deployment.”

Every buyer needs a seller, and other factors, including limited access to capital and the slump in the share price of special purpose acquisition companies (SPACs), are also prompting some public companies to mull going private. In early 2022-2023, SPACs saw a 93.2% drop in funding from a peak of $250 billion in deals reported in 2020-2021, according to the Michigan Journal of Economics

“A lot of businesses don’t necessarily have the cash or the capital structure to execute their business plans,” Steil says. “They were depending on continued access to public markets.”

High interest rates are another force motivating take-private deals.

All companies are struggling with high interest rates, and the public ones are doing it in the limelight.

MARKUS

Co-Head

BOLSINGER

of Private Equity, Dechert

“All companies are struggling with high interest rates, and the public ones are doing it in the limelight,” says Markus Bolsinger, co-head of the private equity practice for Dechert.

“If you have an investor that’s coming in to take your company private and right-side your balance sheet, I think that’s attractive to the management team.”

The bureaucratic stresses of being a public company are yet another driver of take-private deals.

Companies are asking themselves, “Why should I live quarter to quarter, when I could be private and really focus on running the business the way I think it should be run?” says Christina Bresani, managing director

and head of corporate advisory for investment bank William Blair.

She says the take-private momentum has been going on for the last 12 to 18 months.

“Public companies, management teams and boards are frustrated with being public,” she says. “They’ve seen their share prices dip and not recover as they’d like them to, despite improved operating performance.”

Rising costs associated with being a public company are another concern. “Being public is not cheap,” says Bolsinger. “There are a lot of costs that go along with it with respect to compliance and disclosure obligations and so forth. Not every company is meant to be in the public market.”

Doug Starrett, CEO of L.S. Starrett Company, says the stock price was one reason why the company decided to go private.

“[We] were undervalued by the public markets for many years, which was not reflective of our performance,” Starrett says. “This was harmful to all of our stakeholders.”

Red tape was another reason.

“Exploding government regulations and SEC reporting made it onerous for small public companies like Starrett to survive,” the CEO adds.

In a transaction that closed in June, MiddleGround acquired Starrett, which makes more than 5,000 variations of precision tools, gages, measuring instruments and saw blades for industrial, professional and consumer markets worldwide. The all-cash transaction was struck at $16.19 per share, which MiddleGround noted was a 63% premium to the closing stock price on March 8, the last trading day prior to the announcement. On March 13, Starrett was trading at $15.77 and had a market capitalization of $109.7 million.

Other take-private deals in 2024 include private equity firm CORE Industrial Partners’ acquisition in June of Fathom Digital Manufacturing

Corp., a provider of on-demand digital manufacturing services. In March, Mdf Commerce Inc., a SaaS company that implements digital commerce technologies, agreed to be acquired by KKR. In the all-cash transaction, Mdf shareholders were entitled to $5.80 in Canadian dollars per share, equating to about $255 million in total equity value, and a 58% premium on Mdf’s Toronto Stock Exchange closing price of $3.68 on March 8.

While interest in take-privates is rising, Bolsinger says the deals don’t happen overnight, and many don’t cross the finish line.

“You may work on 10 deals and, if you are lucky, you may close one,” he says.

There are many reasons why a take-private deal doesn’t close. They could include valuation disagreements, concentrated stockholders who are not interested in selling, a target that’s in the middle of implementing a strategic plan or findings in the nonpublic material that are not attractive to the potential buyer.

News that a take-private deal is being considered is another risk to closing a deal.

“You look at a company and there is a leak that someone is looking at taking that company private, and the stock price shoots up, and all of a sudden the premium you planned to offer is gone,” Bolsinger says.

Laying the groundwork for a takeprivate deal can be a slow process. MiddleGround’s Steil says his firm had sought over years to build a relationship with Starrett, long before the transaction became a reality.

“Starrett is a company we’ve been tracking for some time,” he says. “We have a public markets tracker where we watch the universe of companies and see how they are trading and look to identify attractive opportunities.”

MiddleGround sent a letter to Starrett in 2020 pointing out the benefits of going private.

“We did not get a response then, but in 2023 they came to the same conclusions we had about the benefits of being a private company,” Steil says. “When we visited, they actually held up our letter in the air.”

According to Steil, the letter was the first step in building a rapport with CEO Starrett, who eventually saw that MiddleGround was credible and had a lasting interest in the company.

Starrett says his company used a variety of advisors to help navigate becoming a private company. Lincoln International served as financial advisor, and Ropes & Gray served as legal counsel to Starrett. William Blair advised MiddleGround in connection with the acquisition and debt financing of Starrett, and Dechert served as legal counsel to MiddleGround.

For other public companies considering going private, CEO Starrett’s advice is to “clearly understand why you want to pursue the option and carefully weigh the risks and rewards.”

Starrett says his company chose MiddleGround for its “operational expertise, understanding of the value of the brand and returning fair value to all our stakeholders.”

Looking to the future, Steil says MiddleGround wants to ensure that Starrett, which has been around for more than 140 years, will thrive.

“We feel we can work with the management team to accelerate revenue growth through product extensions and that we can leverage our deep operational expertise to help them improve the efficiencies of their existing facilities,” he says. //

ANNEMARIE MANNION is a former reporter for the Chicago Tribune and a freelance writer.

BY ALEX RAY, DIRECTOR, AND MANEESH CHAWLA, MANAGING PARTNER, COMVEST PARTNERS

Middle-market deal flow from investment banks has become highly bifurcated in terms of competition within formal auctions.

On the one hand, we are seeing competitive bank-led sale processes garner significant interest, with 30 to upward of 80 indications of interest. Yet simultaneously, we are also observing processes generating minimal interest.

Of course, we should always expect variance in the level of interest a bank-led process will attract. (Some businesses will always turn more heads than others.)

Notably, though, the current range of interest resembles less of a normal distribution and more of a barbell. The stark separation between the two sides warrants a closer look.

Several notable factors are contributing to the divergence in buyer interest. They include: Sector attractiveness. In a market where leverage inevitably has to come down due to elevated interest rates, PE groups have become more selective about where they invest. Assets with strong end markets, solid growth potential and good margins that are not capital-intensive traditionally garner a lot of private equity new platform interest—even more so in the current environment. This is evident in sectors such as consumer services,

maintenance repair and overhaul, industrial services, marketing services, IT services and facility services, where closed deal volume for companies with $50 million to $500 million in enterprise value (EV) has collectively grown, even since the peak of 2021, according to data from SPS by Bain & Co.

Conversely, asset-intensive businesses in areas such as consumer products, building products, aerospace and defense, and general heavy manufacturing are garnering very little sponsor interest. Closed deal volume in those categories is down anywhere from 40% to 70% over that same time frame.

The result has been a huge shift in the closed deal category mix along with a smaller universe of attractive sectors—and, thus, a diminished population of deals attractive to the sponsor community.

Valuation expectations in out-of-favor sectors. There are contrarians in every market who pursue out-of-favor asset categories in hopes of investing at the bottom and ultimately making a return on the buy. Additionally, plenty of investors employ a value and/or relative value investment strategy, looking to buy “B” and “C” assets with the goal of turning an “OK” business into a great company.

But the reality for value-oriented investors is that many founders continue to anchor their valuation expectations based on prior years, creating a large bid-ask spread that inhibits deal activity with no pressure to transact.

Additionally, many sponsors invested in businesses at much higher multiples over the last five years compared to where trades are warranted in today’s environment. Consequently, they are very cautious and thoughtful about exit timing.

Lack of product at the upper end of the market. Deal volume lethargy at the upper end of the market (transaction value of $500 million or more) over the last 18 to 24 months has caused many larger funds to move down market as the pressure to deploy capital persists.

Toward that end, many groups had developed theses in certain sectors and have been motivated to invest regardless of an asset’s size, especially in consolidation strategies where they can put more capital to work quickly.

As an illustration, closed deal volume at the upper end of the market is down 55% compared to its peak in 2021 and fell 25% year over year in 2023 to the lowest levels since 2016. The first quarter of 2024 marked the slowest annual start since 2016, according to data from SPS by Bain & Co. The emergence of single-asset continuation vehicles has also taken a growing number of larger high-quality assets out of the market and provided general partners the opportunity to hold onto their winners for longer if they see continued opportunity for value creation while also relieving pressure to return capital to LPs.

Unsurprisingly, the bifurcated market results in far too much capital chasing too few deals at the lower end of the market. The increased competition has naturally resulted in higher valuations for in-favor assets. One example is the broader business services category, where valuation multiples jumped approximately 1.5x in 2023 compared to 2021 for deals in the $100 million-to-$250 million EV range, according to a GF Data 2023 M&A report.

Given today’s environment, PE firms should focus on sectors in which they have a competitive edge and differentiated angle. Those participating in frothy categories will need to pick their spots and double down on organic growth strategies and operational efficiencies to drive value creation. The ability to underwrite meaningful multiple expansion at exit is becoming more challenging in some sectors, as is the ability to blend down entry multiples significantly through add-on M&A, albeit to a lesser extent.

Additionally, some firms may consider starting smaller, pursuing assets further down market, and maintaining an open mind to doing more business-building to keep up with capital deployment.

While timing is anyone’s guess, there is a logical path to entering a more “normal” buyer demand environment. We are already seeing some positive signs of logjam relief. For one, lending is beginning to open up at the upper end of the market, typically a harbinger of future deal volume growth.

The U.S. economy continues to hang in there, which should further bolster overall investor sentiment. Each month, we get further away from the COVID-19, supply chain and inflation disruptors of certain pockets of the market, which should result in more normalized business performance and instill investor comfort in reengaging in disrupted sectors.

Finally, while seemingly fleeting of late, rate cuts later this year or next should also bring relief and serve as another catalyst to entering a more normal deal environment. //

ALEX RAY is a director of business development at Comvest Partners, where he is responsible for managing relationships with intermediaries, as well as originating new investment opportunities for the firm’s private equity strategy. He was named one of Middle Market Growth’s Business Development Pros to Watch earlier this year.

MANEESH CHAWLA is a managing partner at Comvest Partners and head of the Private Equity strategy, where he is responsible for all key aspects of the investment process including sourcing, transaction execution and portfolio company oversight.

BY MAX GOLEMBO, VICE PRESIDENT, LINCOLN INTERNATIONAL

As the first half of 2024 drew to a close, the market landscape revealed several dynamics, with deal volumes showing an upward trajectory even as the search for quality assets becomes more challenging. Below we provide a comprehensive analysis of M&A trends, unveiling the challenges and opportunities that lie ahead.

Deal volume in the first half of this year is up, but quality varies. There are fewer soughtafter assets compared to 2023, and transactions with redeeming qualities result in over-subscription from an interest perspective.

Post indication of interest, private equity is digging deep into diligence. By and large, funds are bidding on a smaller percentage of deals, relative to the marketing materials they receive. They are wary of making an acquisition in a market with an uncertain macro outlook.

PE is beginning to see cracks in company performance across the board. When examining their portfolios, they are identifying negative trends from both a demand perspective and input cost, which leads them to be even more skeptical when reviewing new opportunities. This trend overall is preventing deals from coming to market.

While deal volume is up, there is a prevailing sentiment that a smaller percentage of deals are closing due to the overall macroeconomic uncertainty.

Despite these challenges, there remains a cautious optimism, with anticipation building for a resurgence in deal activity as we move into the latter half of 2024 and look toward 2025.

Enterprise values increased during Q1 2024 from Q4 2023 in business services, consumer, healthcare, industrials, and technology, media and telecom at varying levels, according to the Lincoln Private Market Index. Each sector is experiencing varied trends.

• BUSINESS SERVICES: Enterprise values in business services increased by 0.9% during Q1 2024, compared to Q4 2023. The utility and infrastructure services subsector, in particular, is set for sustained expansion, propelled by factors transforming the industry. Aging infrastructure and priorities on sustainability and decarbonization, along with tighter regulations, have led to significant demand for infrastructure upkeep, renewal and upgrade. Additionally, utilities in various markets have progressively shifted nonessential functions to external service providers over recent years. In professional services, companies are leveraging AI to optimize tasks and scale operations, freeing up time for employees to focus on high-level strategy and projects that require the human touch.

• CONSUMER: After a booming 2021, M&A activity has declined, mainly because of waning consumer confidence and spending impacted by high inflation, interest rates and global geopolitical events. Sectors like food and beverage, personal care and pet products are performing well, while durables and discretionary goods face challenges. EVs, however, did increase by 0.2% in Q1 2024 (relative to Q4 2023). Despite lower container shipping costs indicating decreased demand for overseas consumer goods, there’s optimism for an M&A revival amid valuation gaps and deal postponements.

• HEALTHCARE: Healthcare EVs increased by 2.1% in Q1 2024 from Q4 2023, despite heightened regulatory scrutiny and potential election concerns. Although the performance of healthcare companies has been consistent, it’s uncertain whether valuation multiples will start to decrease due to recent scrutiny, potentially leading to a future reduction in EVs. Given the uncertainty in the market, advisors have had to get creative around process strategy, like offering select buyers access to management early on in the

preparatory phase of a sale process to get them excited about the company’s story. This helps ensure adequate market receptivity.

• INDUSTRIALS: Despite a 1.8% rise in industrial EVs in Q1 2024 versus Q4 2023, this sector saw a decline in revenue and EBITDA growth compared with a year ago. Additionally, covenant default rates for industrial companies nearly doubled, indicating a growing gap between high-quality assets and the rest of the sector, with some subsectors possibly under increased strain. Rising input costs are an ongoing challenge due to inflation, and there is a constant chase to match customer pricing with them. Many companies have successfully passed these price increases on to clients, but there has often been a lag. Amid uncertainty, Lincoln observes businesses consistently enhancing operational efficiency, driving sustainable growth and harnessing technological advancements—a positive sign in the current environment.

• TECHNOLOGY, MEDIA AND TELECOM: The technology, media and telecom (TMT) industry saw a 0.8% increase in EVs during Q1 2024 from Q4 2023. Additionally, TMT M&A activity is showing signs of a slow recovery, with valuations of private tech companies bolstered by the rise in public tech stock values. However, IPO exits remain elusive for all but the largest firms, making smaller TMT companies appealing for PE take-private moves. Despite nearly record levels of PE dry powder, Q1 M&A volume remained steady from Q4 2023, indicating a cautious approach from buyers focusing on growth and profitability, with particular interest in companies exhibiting the “Rule of 40+.” Liquidity for LPs is crucial, with distributions to paid-in capital (DPI) being a key focus, alongside adept portfolio management and leveraging debt markets for recaps as alternatives to full sales.

While challenges persist, the strategic nuances across sectors and burgeoning overall deal volumes hint at a richly complex yet promising horizon for M&A during the second half of 2024 and into 2025.

This evolving narrative not only captivates the interest of investors but illuminates a path paved with cautious optimism, strategic ingenuity and a steadfast commitment to realizing the market’s vast potential. //

MAX GOLEMBO is a vice president in financial sponsor coverage at investment bank Lincoln International in Chicago. He was named one of Middle Market Growth’s Business Development Pros to Watch earlier this year.

Wealth advisors and institutional consultants are increasingly offering private equity options to retail investors, but they come with a variety of hurdles and risks

BY ANASTASIA DONDE

Institutional private equity fundraising continued its slide this year, and many LPs are already oversaturated on private equity. In the first quarter, 150 private equity funds closed with $166.8 billion in capital commitments, representing a 38% decline from the same quarter last year by volume and a 6% decline by dollar value, according to Preqin.

Moreover, most U.S. institutional investors already have private equity programs in place, with some reporting that they’re overallocated to private equity because of the liquidity mechanisms and stock performance in recent years. This is leading to the pursuit of other avenues for growth. For some firms, that means increasingly tapping international investors. For others, it’s turning to retail investors.

So far, most of the activity has been among private wealth banks and registered investment advisors (RIAs) that offer private equity as an option in retail investors’ portfolios or as part of a mutual fund offering. “Private banks and wealth advisors have been raising money from individuals for private markets for a number of years,” says Jessica Mead, regional executive for North America at fund administrator Alter Domus. “These are usually smaller, semi-liquid fund

structures, with redemptions capped as a percentage of NAV.”

Some of the largest private equity firms, including Blackstone, Apollo Global Management and KKR, have also launched dedicated funds for retail investors. Most recently, Borgman Capital, a lower middlemarket investment firm in Wisconsin, launched its Pass the Hat platform, which gives accredited investors access to Borgman’s portfolio. Still, experts cite a variety of hurdles when it comes to getting retail investors—who are used to daily liquidity—into long-dated private equity funds. More frequent performance reporting, transparency and other nuances are in play.

A variety of private banks, RIAs and other wealth advisors have started to offer private equity as an investment option to their retail clients. Some come in the shape of “interval funds” that have limited liquidity options; others are private equity investments offered to end-clients in a menu of options.

Thrivent, a Minneapolis-based financial services firm, announced in April that it is now offering private equity as an asset class in its Asset Allocation Funds/Portfolios. Retail investors can gain exposure to private

equity funds for as little as $50 per month. The firm’s four asset allocation funds will eventually build to a 4%-6% allocation to private equity spread across a highly diversified portfolio of PE funds, says David Royal, chief financial and investment officer at Thrivent. “We wanted to include private equity as a diversified asset class,” he says. The allocation is starting at six secondary funds-of-funds to get broad exposure to private equity across primarily domestic middlemarket buyout funds. The mutual funds offer daily liquidity—a stark contrast to the long lockups typical of private equity.

Royal says Thrivent ran a variety of models and scenarios based on past redemption rates through market cycles. He doesn’t think sudden significant withdrawals from clients would necessitate pulling money from the private equity funds. “Our redemption rates have been low historically, even in the worst-case scenarios,” Royal says. “We don’t have any significant shareholder concentration.”

Thrivent also manages $75 billion in insurance assets and has a dozen people who manage private equity, primarily focused in the middle-market buyout space for the organization’s general account. The same team searched for the secondary funds-offunds for the retail channel, Royal says. “From a risk/return perspective, the middle-market looked more attractive [than large-cap],” he adds.

Meketa Investment Group, an investment consulting firm that advises pension funds and other institutional investors, also used its experience to give retail clients access to private equity. The firm launched its Meketa Capital and Meketa Infrastructure Fund subsidiaries in February. The Primark Meketa Private Equity Investments Fund offers retail investors exposure to private equity co-investments via an “interval fund,”

Wealth management firms are exploring this as a new frontier. They are not familiar with the space; they need someone to guide them through this effort.

MICHAEL BELL CEO, Meketa Capital

which is a mutual fund with quarterly liquidity and a 5% cap on money that investors can withdraw at one time. Other products in this space include “tender funds” that also have quarterly liquidity, but a board has the right to suspend withdrawals.

Meketa Capital CEO Michael Bell says the firm partners with 60-80 preferred private equity managers that Meketa Investment Group, the fund’s subadvisor, has worked with via its institutional arm and invests directly in portfolio companies through co-investments. Most of the exposure is in North American funds that are diversified by vintage year and sector, he says. The firm has made 20 investments to date since January. “We’ve been sourcing co-investment work with these firms for decades. The diligence is based on long-standing relationships,” Bell says.

Many private wealth banks and RIAs are putting 5%-10% of retail investors’ asset allocations into private markets or other alternatives, Bell says. He thinks over time that exposure could grow to 20%. Typically, capital is cut from small and mid-cap public stocks and diverted to private markets.

Wealth advisors that are new to the world of private equity can benefit from the knowledge of more experienced participants that understand the return differential between top

and bottom quartile managers, for example, and the liquidity expectations of private equity investments.

“Wealth management firms are exploring this as a new frontier. They are not familiar with the space; they need someone to guide them through this effort,” Bell says.

Some of the largest private equity firms have launched mutual funds that offer retail investors access to their private markets platforms. Blackstone raised $1.3 billion in January for its BXPE retail fund, according to The Financial Times. The offering invests in traditional buyouts, biotechnology and preferred equity. KKR launched its K-Series of private markets funds for retail investors last year, with the first strategy named K-Prime. The firm said it raised $500 million per month for the strategy from affluent investors. Apollo executives, meanwhile, have said they plan to offer private credit opportunities to retail investors and exchangetraded funds, according to comments made at a conference in May.

Fees on these retail funds are usually lower than institutional funds (2% management fees and 20% performance fees). The retail funds typically charge a 1%-1.25% management fee and a 12%-15% performance fee, with a 5% hurdle rate.

In May, Borgman Capital launched its Pass the Hat online platform for retail clients as a way to test the market. The strategy offers accredited investors access to Borgman’s portfolio companies at a $50,000 investment minimum. Prior to launching Pass the Hat, the firm had completed 18 investments with commitments from high-net-worth individuals and family offices. With Pass the Hat, the goal is to make it easier for additional accredited investors to access private equity. The platform has lockup periods of five to six years, similar to other private equity investments, according to CEO Sequoya Borgman. He notes that private equity is the only alternative investment not broadly available to retail clients yet.

Executives at SS&C GlobeOp, the fintech company’s fund administration division, say that retail investors are becoming more aware and educated about private equity. “Private equity is buying so many corporations, the average investor wants that exposure,” says Bhagesh Malde, global head of SS&C GlobeOp. Where retail investors would normally get access through public stocks, there aren’t as many of them available. According to The Atlantic, the number of public companies has shrunk by half (from 8,000 to about 4,000) between 1996 and now. The share of total companies under private equity ownership, meanwhile, has grown from 4% to 20%. Given the latest developments in take-private deals and limited IPOs, the trend is expected to continue.

Malde says there is interest “in the ability to democratize these investments” and predicts that private markets or alternatives exposure could grow to 10% of retail clients’ portfolios in the coming years (from 5% or less now). “I think it’s a global trend,” he adds. “Consumers in India are also clamoring for exposure to private equity and real estate.”

Even as firms look to capitalize on the growing interest in private equity, setting up a retail strategy involves a lot of back-office work, anti-money laundering mechanisms and figuring out the right liquidity mix. For its part, SS&C GlobeOp helps clients with automating and digitizing the onboarding process and preparing the paperwork for accredited investors.

Tapping into the retail channel for private equity also involves courting investors over time. “You won’t be able to set this up tomorrow; you have to build relationships through banks and advisors,” Alter Domus’ Mead says. Private markets firms must also turn data around quickly and respond to greater transparency needs and likely monthly (as opposed to quarterly) reporting.

When it comes to vetting private equity investments, “I think retail investors place a lot of trust in who it is,” says Neal Chansky, head of the Registered Funds Business for SS&C GlobeOp. “Whether it’s an independent financial advisor or a large private bank, investors rely on the advisor to do the underlying homework and due diligence on the product.” //

ANASTASIA DONDE is Middle Market Growth’s senior editor.

• MARCH 2023: KKR registers its K-Prime retail private equity fund, according to Bloomberg. The strategy raised $500 million per month through the end of last year, according to a quarterly earnings call.

• JANUARY 2024: Blackstone Group raises $1.3 billion for a private equity fund tailored to wealthy individual clients, according to The Financial Times The Blackstone Private Equity Strategies Fund (BXPE) is continuing to fundraise.

• FEBRUARY 2024: Institutional consulting firm Meketa Investment Group launches its Meketa Capital and Meketa Infrastructure Fund subsidiaries for individual investors. These offerings include managing and distributing interval funds, managing customized private market fund vehicles and providing consulting services.

• APRIL 2024: Financial services firm Thrivent starts offering private equity as an asset class within its Asset Allocation Funds/Portfolios. It’s one of a few major financial services firms to offer private equity exposure in a daily valued mutual fund.

• MAY 2024: Lower middle-market firm Borgman Capital launches Pass the Hat, an online platform that provides accredited U.S. investors with access to private market investment opportunities sponsored by the firm.

• JULY 2024: Asset management firm T. Rowe Price files its T. Rowe Price OHA Flexible Credit Income Fund with the SEC. The interval fund will invest in senior and junior loans originated by T. Rowe’s private debt subsidiary, Oak Hill Advisors.

Renovus Capital Partners

Gary Tang has joined Philadelphia-area investment firm Renovus Capital Partners as principal. Tang will focus on expanding Renovus’ healthcare services investment vertical. Prior to his new role, Tang was most recently a vice president at Chicago Pacific Founders, and he previously worked for Norwest Venture Partners. Before Norwest, Tang worked for Baird as an associate, and he began his career at PwC.

Michael Gebhardt has joined private investment firm VSS Capital Partners as a principal. He will focus on new investment opportunities, due diligence, transaction execution and portfolio company value creation. Prior to joining VSS, Gebhardt was a principal at Sagewind Capital. Previously, he was a vice president at Tailwind Capital and an associate at Riverside Partners.

Shelby Cowley has joined MidCap Advisors, a New York City-based middle-market advisory firm, as managing director. She comes to MidCap Advisors after serving as both a director and vice president of M&A at insurance and business solutions provider Acrisure, where she led more than 150 acquisitions. Prior to her senior executive roles at Acrisure, Cowley served as a private equity analyst at 50 South Capital and as an associate at Ernst & Young.

Global investment bank Lincoln International has hired Ryan Mitchell as a managing director to lead the firm’s distribution efforts within the Business Services Group. Mitchell will be based in Richmond, Virginia, where Lincoln recently opened an office and expanded its U.S. footprint to the Mid-Atlantic region. Prior to joining Lincoln, Mitchell was a managing director in the services and industrials group at Piper Sandler. Previously, he was head of the Commercial and Industrial Investment Banking Group at BB&T Capital Markets.

Houlihan Lokey

Erik Kistler has joined investment bank Houlihan Lokey’s Healthcare Group as a managing director. Based in New York, Kistler will cover select areas within healthcare retail multisite, physician practices and pharma services. Before joining Houlihan, he most recently served as an executive director at Moelis & Co., where he covered multisite healthcare and pharma services. Prior to Moelis, Kistler spent six years at Edgemont Partners, a healthcare-dedicated investment bank.

Harris Williams

Harris Williams, a global investment bank specializing in M&A and private capital advisory services, announced that Sam Hendler is rejoining the firm as a managing director focusing on healthcare IT, based in the Boston office. Hendler was previously with Harris Williams from 2005 to 2022 and was promoted through the ranks to managing director. He most recently was managing director of business development in the healthcare vertical at Thomas H. Lee Partners.

OceanFirst Bank

Chad Dally has joined OceanFirst Bank, a regional bank headquartered in New Jersey, as market president of greater Washington, D.C., and head of aerospace, defense and government services. Dally was most recently managing director and regional head of government contracting, mid-corporate and middle-market banking at TD Bank in Vienna, Virginia. Earlier in his career, Dally held roles at Capital One, Wachovia and Harbourside Community Bank in South Carolina.

Pritzker Private Capital

Pritzker Private Capital, a family-backed direct investing firm, has added Anna Edgcomb (pictured, left) and Alyson Brown (right) as vice presidents. Both will help source and execute investments.

Edgcomb rejoined PPC as vice president of manufactured products after receiving her MBA from University of Chicago’s Booth School of Business. She was previously an associate at PPC and began her career in investment banking at Bank of America Merrill Lynch.

Brown has joined PPC as vice president of services, having served most recently as senior associate at Wind Point Partners. Prior to that role, she worked at McKinsey & Co.

Configure Partners

Configure Partners, an investment banking platform specializing in debt placement and credit resolution services, announced the hiring of Connor Barth as a director and the promotion of Fitz Marren to associate.

Barth was previously a vice president within the Debt Capital Markets practice at Piper Sandler, and he began his career within the Capital Advisory Group at Lincoln International.

Marren joined Configure in 2022 as an analyst, having previously worked as an associate at Ankura Consulting Group.

Insperity, a provider of human resources and business performance solutions and an ACG Official Sponsor of Growth, announced that four professionals within its Private Capital Markets (PCM) team have been promoted to the role of private capital advisor from their previous positions as business performance advisors.

Amanda Cooper Benbow, CBPA, (pictured) joined Insperity in 2017. She has a track record of collaborating with private equity firms, investment firms and family offices to orchestrate seamless mergers and acquisitions.

Brad Burke serves the Northeast region and partners with PE and venture capital firms and family offices to help their portfolios move beyond growth plateaus, optimize operations and drive additional value creation.

Monica Alfisi helps firms expand market reach and increase sales revenue. Prior to joining Insperity, Alfisi consulted with dental and medical practices, helping them increase revenue, streamline operations and implement comprehensive training programs.

Ryan Brown joined Insperity in 2009. Before Insperity, he held several sales leadership roles in the staffing and recruiting industries before embarking on a 10-year journey as an entrepreneur and business owner.

Houlihan Capital

Houlihan Capital, a valuation, financial advisory and investment banking firm, named Rodger Howell as its CEO. Howell’s tenure follows that of Houlihan Capital Co-founder William Butrym, who has transitioned to board member and senior advisor. Howell’s career has included successful leadership positions at PwC and PRTM Management Consultants. Houlihan Capital also announced that it is transitioning to an employee stock ownership plan structure.

Edison Partners

Growth equity investment firm Edison Partners announced the promotion of Michael Dirla to vice president. In his new position, Dirla will work more closely with Edison Partners’ portfolio companies while expanding his role in identifying and evaluating potential investments in financial technology and enterprise solutions.

Dirla joined Edison in 2021. He had previously served as an associate at private equity firm Lightyear Capital and began his career as an investment banking analyst at Credit Suisse.

Women’s sports are having a moment with fans and sponsors, thanks in part to the Caitlin Clark effect. Can the recent momentum draw private capital investors?

Ortoli | Rosenstadt Partner Paul Pincus explains indemnification, and what exactly a seller is responsible for when selling a business.

Private Equity Info and GF Data investigate the extent to which buyer demand affects pricing in the middle market.

CORE Industrial Partners’ founder discusses the add-on strategy for its metal components business PrecisionX.

Women’s sports are having a moment in the spotlight with fans and sponsors. Experts say PE investors could soon get in the game, too.

BY CAROLYN VALLEJO

The Caitlin Clark effect on the economics of women’s sports is undeniable. In May 2023, just weeks after Clark’s record-setting run with the University of Iowa Hawkeyes in the NCAA basketball tournament—she scored the most points in a single NCAA tournament, male or female—PwC conducted research into the accelerating momentum (and revenue) of women’s sports.

Its survey concluded women’s sports fans tend to be more engaged than their male counterparts, resulting in higher game attendance and merchandise purchases, a greater likelihood of betting on games and increased viewership of game broadcasts.

Since then, Clark has been drafted into the Women’s National Basketball Association, and her star only continues to rise. “Caitlin Clark is definitely a catalyst right now,” Lori Bistis, a deals partner at PwC and leader of its sports practice, told Axios in May.

Sports fans continue to watch how far and wide female athletes’ impact can reach across other corners of the sports universe.

Now, investors are watching closely, too. As private equity acquirers begin to embrace M&A opportunities in sports teams and leagues, experts say women’s sports are gradually attracting dealmakers’ interest.

“It’s not necessarily because they’re looking at getting in to do the right thing,” says Shane Winn, managing director, strategy and sports marketing, at Allison Worldwide, a marketing and communications consultancy. “It’s because they realize

there is economic value in getting involved, and that no one else was doing it.”

Allison recently partnered with market research and consulting firm The Harris Poll to launch their inaugural Sports Momentum Index, a monthly consumer poll providing data behind shifting trends in sports fan engagement.

The first edition of the index finds sports are entering a new era with fans as women’s athletics take center stage. Unsurprisingly, the index shows surging momentum within the WNBA as fans reported increased personal relevancy and engagement with the league between February and late May.

“We really captured the WNBA perfectly when it was pre-March Madness,” says The Harris Poll Managing Director Jennifer Musil. “Caitlin Clark was out there (in February), but not in the way she was about to become in March.” All seven

inputs accounted for in the index increased for the WNBA between February and May, a phenomenon Musil attributes to Clark’s star power.

Shifting trends in sports span beyond women’s basketball. The Professional Women’s Hockey League scored second place on the index’s list of sports and leagues experiencing the most momentum to date, surpassing even the National Football League, which placed sixth.

Winn notes that Allison’s index can be applied to several use cases, including brands looking to sponsor teams and leagues, as well as investors and acquirers seeking data to guide their business development and deal sourcing initiatives. There’s a gap in the market for such insight, he says. “There’s not a lot of data out there that would give an investor or brand real visibility into the value of investing in emerging or women’s sports,” he adds. “For the investor community, (the index) can be looked at as an input in decision making. It’s another lens to put on investment considerations.”

Look at how awesome we’re doing (with limited outside investment). ... Now imagine what it could be like if we got just part of what people are putting into men’s football.

LACY MILE

President and Wide Receiver, Utah Falconz

PE investment in professional sports kicked off in 2019 when Major League Baseball first allowed minority investments in teams; the National Basketball Association, National Hockey League and MLS followed suit, while the NFL is now in discussions to do the same.

PitchBook data shows PE sports investment has been dominated by men’s athletics. In women’s sports, investment has occurred on a smaller scale, often through individual backers and venture capital support.

Michele Kang, who owns the Washington Spirit women’s soccer team, announced last December that she acquired the London City Lionesses Football Club. In May, professional women’s basketball league Unrivaled announced receiving seed funding from a slew of individuals, including actor Ashton Kutcher, former Warner Brothers chairwoman and CEO Ann Sarnoff and University of Connecticut women’s basketball head

coach Geno Auriemma, among others. Private investment firm Range Group led the round.

An inquiry within middle-market search engine Grata reveals 4,766 companies operating in the women’s sports team and league space (including team-adjacent businesses like sports broadcasting companies and equipment retailers).

Of them, merely 16 are private equity-backed.

One prominent PE investor in women’s sports is Sixth Street. Last September the firm acquired a majority stake in the National Women’s Soccer League (NWSL) for $125 million. More recently, in March, PE giant Carlyle Group, along with the Seattle Sounders Football Club, acquired the Seattle Reign FC, an NWSL team, for $58 million.

While some deals are getting inked, industry players in women’s sports say opportunity remains for potential investors as awareness, viewership and fan engagement increase. Yet a lack of funding continues to hold back growth for many teams and leagues.

One team eager to show investors its growth potential is the Utah Falconz, a women’s semi-pro tackle football team within the Women’s National Football Conference (WNFC). Founded eight years ago, and part of the WNFC for about five, the Falconz are a rapidly expanding entity. President and wide receiver Lacy Mile says the team continues to embrace its broader goals in the community as it focuses on growth.

“Our mission is really around being involved in the community, setting people up for the future, leadership, financial success, education—all of those things that are skills outside of just playing football,” she tells Middle Market DealMaker. “I think we’re also

BY THE NUMBERS

4,766 companies operate in the women’s sports team and league space

4,672 are private 4,396 are bootstrapped

16 are private equity-backed

growing a lot on understanding how to run as a business and grow.”

The Falconz roster has consistently expanded over the years. The team can have anywhere from 40 to 60 players, a coaching staff of between eight and 10, and a 10-member board, plus administrative staff, Mile says.

External investment for both the team and the league at large—mostly through sponsorship—is an increasing priority, particularly as Falconz team members must still pay to participate. Mile says the league’s support in bringing in sponsors is crucial to easing financial burdens on the bootstrapped business. WNFC sponsors include brands like Adidas and Rydell, whose support helps the team pay for essentials like uniforms and travel expenses.

But expanding outside investment will be key to turning the Falconz from a pay-to-play model to one where players are compensated.

That’s not a far-fetched goal. Mile says the Falconz are setting new attendance records with stadium games. Meanwhile, in 2022 the WNFC announced that viewership of games streamed on the Vyre

Network increased 475%, marking the league’s most-viewed playoff season in its history.

Earlier this year, the WNFC secured a five-year broadcasting deal with streaming platform DAZN Group for both tackle and flag football games, yet another reflection of the sport’s growing revenue-generating potential. “With women’s sport ratings reaching new heights, DAZN is expanding its coverage beyond its existing portfolio of premium women’s soccer rights,” stated Esmeralda Negron, co-CEO of Women’s Sport for DAZN, in a press release in April. “The WNFC is a perfect addition given the popularity of tackle football and the emergence of women’s flag football as an Olympic sport in 2028.”

Mile notes that, despite sponsorship support and increased viewership, external funding remains limited, forcing the team to “be more efficient with our money.” Still, she’s optimistic that the tides could be turning.

As to whether the Caitlin Clark effect will translate to other women’s sports and spur greater investment activity, Mile expects the movement to take time. “I’m seeing more of an openness to it, though it’s going to be a bit slower as it makes its way to women’s football,” she says.

Investors should consider the impressive growth that teams like the Falconz have managed without much financial support, Mile adds. “The biggest thing to be said is, look at how awesome we’re doing (with limited outside investment). Look at how good the competition is when we all still have full-time jobs. Now imagine what it could be like if we got just part of what people are putting into men’s football,” she says. “We’re definitely looking for people to come in and invest so we can make our product even better.” //

CAROLYN VALLEJO is Middle Market Growth’s digital editor.

PAUL PINCUS, ESQ. Partner, Ortoli | Rosenstadt LLP

Although every seller would like to sell its business “as is” and walk away from any liabilities, few deals get done that way. Instead, subject to negotiated limitations, most buyers expect the seller to be responsible, and make the buyer whole, for certain liabilities relating to the seller’s previous ownership—a concept M&A professionals refer to as indemnification. Indemnification provisions are essential to allocating risk between the parties and require careful drafting. The increasing use in recent years of representations and warranties insurance (RWI), either as a supplement or replacement for a seller indemnity, has heightened the importance of detailed attention to indemnification provisions and to a strong understanding of the changing market.

A seller is generally liable for any breaches of its representations, warranties and covenants contained in the purchase agreement. Representations and warranties are written statements the seller makes about itself and the business, which may include ownership of equity interests and assets, authority to transact, corporate organization, financial statements and liabilities, and customers and contracts, among other things. Covenants are promises by the seller to take (or not take) specific actions, which may include agreements not to compete with the business after closing (typically for three to five years) within a defined geographic area and not to disclose confidential business information. In a typical deal structure, if the seller’s

representations and warranties aren’t accurate, or the seller breaches its covenants, it must indemnify the buyer for any resulting losses.

Asset deals sometimes follow a so-called “our watch / your watch” approach. Under this approach, a seller may be required to indemnify the buyer for all liabilities arising prior to closing of the transaction, whether or not the liabilities would be a breach of any representation or warranty (and, in exchange, the buyer is required to indemnify the seller for all liabilities arising after closing).

A seller’s liability is typically limited by negotiated survival periods for claims, caps, baskets and other limitations on recovery.

SURVIVAL PERIODS: The term “survival periods” refers to the time that a party entitled to indemnification can bring a claim against the other party. Typically, the seller’s indemnification obligations for breaches of most “standard” representations and warranties last 18-24 months after closing. However, potential liabilities discovered during the buyer’s due diligence may be subject to separately negotiated and more extended survival periods. Representations and warranties relating to “fundamental” matters (such as the seller’s ownership of the equity interests or assets being sold, and its authority to enter into the transaction), and other matters such as taxes, ERISA and broker’s fees, typically last longer.

A seller’s indemnification obligations in deals without RWI are usually limited to an agreed-upon percentage of the purchase price (cap), which varies with the deal value and the matter for which indemnification is sought. In smaller transactions, liability for breaches of “standard” representations and warranties is often limited to 15%-20% of the purchase price. In larger transactions, liability for breaches of “standard” representations and warranties usually will not exceed 10% of the purchase price. Indemnification for potential liabilities discovered during the buyer’s due diligence that are subject to separately negotiated survival periods may be subject to separately negotiated liability caps. Indemnification for “fundamental” matters (and other matters for which similarly extended survival periods apply) is typically capped at the purchase price (or sometimes uncapped).

To discourage litigation over matters involving small amounts of money, buyers and sellers typically negotiate thresholds (baskets) to the seller’s indemnity obligations, below which the seller will not be liable (typically, 0.5%-1% of the purchase price, depending on the deal’s value). These thresholds can be in the form of deductibles or what M&A

professionals call “first-dollar” or “tipping baskets,” where the buyer can seek indemnification from dollar one for all losses once the threshold has been reached. Indemnification for known liabilities (such as pending or threatened litigation), “fundamental matters” and other matters for which extended survival periods apply will typically be excluded from such baskets.

However, in asset deals following the “our watch / your watch” approach, claims related to pre-closing liabilities and post-closing liabilities may not be subject to the limitations that are imposed on claims related to breaches of representations and warranties.

CAPS AND BASKETS – DEALS WITH RWI: A seller’s indemnification obligations in deals with RWI are usually limited to half of the RWI deductible, and subject to agreedupon caps, certain matters that are excluded from RWI coverage and losses in excess of the RWI coverage amount. In a “no seller indemnity” structure, a seller can have no exposure for breaches of its representations and warranties. Whether or not there is RWI, the parties usually will state expressly that no limitations of liability for indemnification will apply if the seller has committed fraud, and buyers often will seek no limitations of liability for breaches of covenants.

Buyers frequently seek to fund potential indemnity claims by placing a portion of the purchase price into escrow at closing (frequently, 10% in deals not using RWI) or by deferring payment of a portion of the purchase price and insisting on a right of offset against the deferred payment(s). A buyer may also seek to fund potential indemnity claims by purchasing RWI. However, RWI currently is not available on deals under about $20 million in value, will be subject to an overall coverage limit (usually 10% of the transaction price), is subject to a deductible (historically, about 1% of the transaction value), and will not cover known liabilities or breaches of covenants.

Understanding market standard terms for a seller’s indemnity obligations is essential to both buyers and sellers. Since indemnification is one of the most heavily negotiated provisions of a purchase agreement, either party’s failure to understand market standard terms creates the risk of that party insisting on indemnification terms that can kill a deal. //

PAUL PINCUS, ESQ. is a partner at the international law firm Ortoli | Rosenstadt LLP and head of the firm’s Mergers & Acquisitions practice. He can be reached at (212) 8298931 or php@orllp.legal.

BOB DUNN Managing Director, GF Data

ANDY JONES Managing Director, PrivateEquityInfo. com

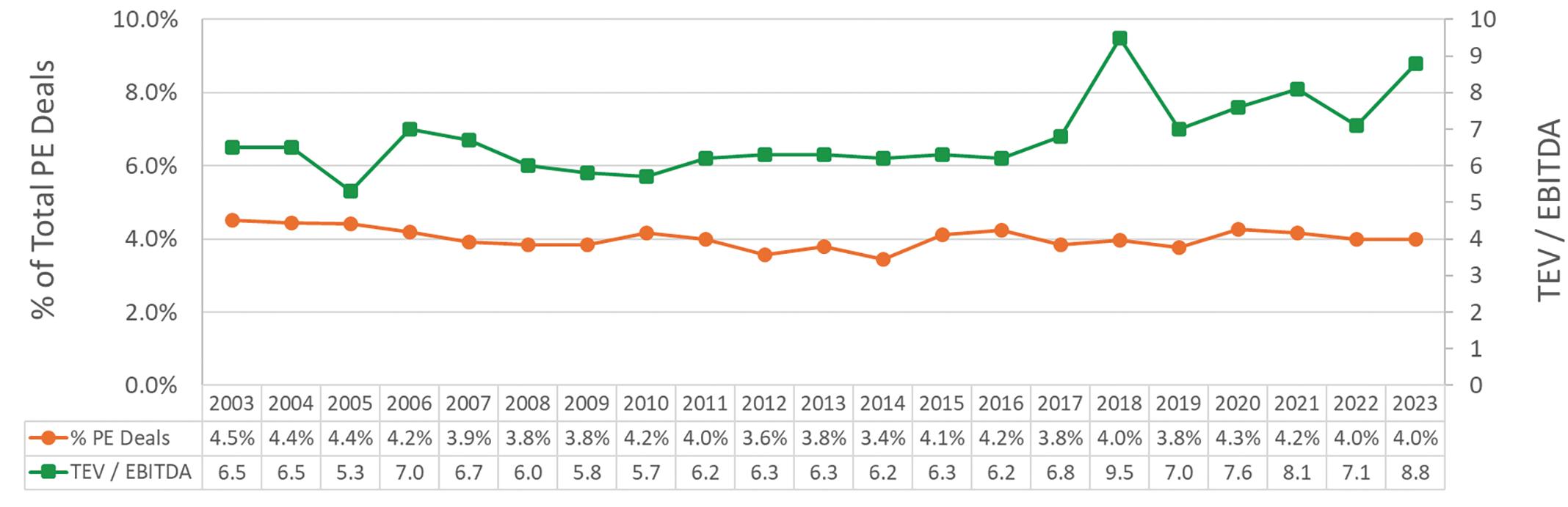

How much impact does buyer demand have on pricing in the middle market? Private Equity Info and GF Data teamed up to investigate.

We overlaid the top four three-digit NAICS codes based on their share of deal volume over the past two decades using data from Private Equity Info—a research database used by M&A professionals—with valuation data from GF Data, an ACG company. We then tested whether increased demand by private equity groups translates into higher multiples over time.

The results were mixed.

In some industries with a high share of private equity deals, we see evidence that private equity acquisitions might create sufficient buy-side demand to increase valuations of companies in these sectors. Other industries show lower or no correlations between private equity acquisitions and valuation metrics.

Many private equity firms tend to have similar industry focuses over time; some industries are in vogue for private equity at certain times, while other industries cycle out of favor. Consequently, financial buyers, as a collective, can become heavily concentrated in select industries, and these concentrations are generally cyclical.

We selected four NAICS industry codes that have experienced the largest market share for platform acquisitions by private equity over the last 24 years. These include:

541 – Professional, Scientific and Technical Services, which grew in share of PE acquisitions by 56% over the 24-year period and represented 10.3% of total private equity platform acquisitions.

511 – Publishing Industries (except Internet), which grew by 71% and represented 7.5% of the deal total.

334 – Computer and Electronic Product

Manufacturing, which saw 36% growth and a 6.8% share.

325 – Chemical Manufacturing, which fell by 13% over the 24-year period and represented 4% of completed deals. (Find market share ratings for other industries at privateequityinfo.com/trends.)

There was a high level of correlation (0.76) between deal activity and valuation for NAICS 541, which also represented the largest percentage of activity of the four industries. Heavy concentration of private equity acquisitions, coupled with substantial growth of private equity investments within a given industry, has the strongest positive impact on pricing.

The next two, NAICS codes 511 and 334 (with 7.5% and 6.8% share of total PE deal volume, respectively), proved more moderately correlated. Deal activity tracked by PEI for NAICS 511 had a 0.65 correlation with valuations from GF Data, while NAICS 334 had a correlation of 0.55.

Finally, we get to NAICS 325 (Chemical Manufacturing), which was the only NAICS code we analyzed that experienced a decline in deal volume based on PEI data. In this case, we found no correlation between deal volume and valuation, allowing us to draw the conclusion that a decrease in deal activity does not necessarily impact pricing, especially for cyclical industries.

The takeaway? For industries with increasing market share and a relatively high percentage of completed deal activity, it does appear that deal volume correlates to deal value. For those with decreasing market share and a smaller percentage of deal activity, volume has less impact on value. //

PROFESSIONAL, SCIENTIFIC, AND TECHNICAL SERVICES

COMPUTER AND ELECTRONIC PRODUCT MANUFACTURING

CHEMICAL MANUFACTURING

Private Equity firms prioritize cybersecurity to secure investments and enhance long-term value. Beyond regulations, it’s a strategic imperative that impacts deal certainty and investment risk. In today’s cyber landscape, resource-limited portfolio companies face heightened vulnerability, emphasizing the need for PE leaders to prioritize cybersecurity in transactions.

CORE’s founder and managing director shares the macro factors that keep him optimistic about the manufacturing sector

BY HILARY COLLINS

Private equity firm CORE Industrial Partners has concentrated on manufacturing, industrial technology and industrial services since its founding in 2016, leveraging the deep expertise of its partners, who have previously served as CEOs or presidents of industrial businesses. And that focus has clearly paid off: In May, CORE’s portfolio company PrecisionX Group acquired National Manufacturing Co., in a move calculated to expand the company’s deep draw and die stamping capabilities, as well as grow its footprint in the medical and aerospace and defense (A&D) markets. John May, founder and managing director of CORE, sat down with Middle Market DealMaker to share the rationale behind the acquisition, what’s next for PrecisionX Group and more.

Middle Market DealMaker: When sourcing this deal, what were you looking for in an investment target, and how did National Manufacturing Co. fill those requirements?

JOHN MAY: Given the significant total addressable market and the highly fragmented nature of the market, CORE has been researching the deep draw and progressive die stamping space as a thematic vertical since 2018. The unique and technically complex capabilities of the industry drive substantial stickiness (the tenure of the customer base is roughly 20 years), as well as a superior margin profile. The limited maintenance capex is attributable to the nature of both the equipment and process. National Manufacturing not only met each of these criteria but also provided further exposure to highly attractive A&D and medical applications, as well as a new facility with significant excess capacity and quality certifications (ISO9001, ISO13485 and AS9100) that can support continued growth with minimal additional investment.

MMD: PrecisionX Group comprises three companies CORE has acquired since February 2023—GEM Manufacturing, Coining and now National Manufacturing. What kinds of growth are you prioritizing now?

MAY: CORE continues to prioritize organic growth from cross-selling capabilities across the broader platform customer base while also opportunistically evaluating add-ons that will augment the capability set, drive improved scale and geographic diversification, and expand the universe of current customers. Many businesses we acquire prioritize maintaining existing customer relationships over cultivating new ones, and their outbound sales functions are limited as a result. At PrecisionX Group, we identified this challenge early, invested substantial resources into the hire of a commercially inclined CEO and CCO and charged them with two key objectives:

• Accelerate growth with existing customers by leveraging the broader platform capability set

• Identify and onboard new customers serving critical medical, A&D, space and electric vehicle applications

To support those initiatives, we’re opportunistically evaluating add-ons that will augment the platform capability set across other forms of specialty stamping and expand the universe of current customers. Interestingly, we’ve seen a concentration of these businesses in the Northeast, and our business development team has done a great job cultivating relationships with their owners through direct outreach, culminating in several transactions.

MMD: How are you planning to incorporate National’s team into PrecisionX Group? What does your

integration playbook for these add-ons look like?

MAY: Although each transaction is nuanced, CORE takes the same care in each one to ensure the right people are retained and knowledge is appropriately disseminated as former owners transition toward retirement, and National will be no different. The integration playbook consists of a mix of tactical and strategic workstreams. We prioritize integrating the back-office functions (i.e., finance, HR, IT, etc.) into the broader platform to facilitate management of the business and enable growth. As those workstreams are completed, we shift focus to the development of a threeyear strategic growth plan that will inform platform strategy over our investment horizon.

MMD: Why did CORE decide to specialize in the industrials sector, and how does this deal fit into your broader investment strategy?

MAY: We believe there is a significant opportunity within manufacturing and industrial technology, attributable to a handful of compelling macro dynamics. These include small manufacturing companies with less than 500 employees comprising more than 90% of all manufacturing companies in the United States; the large baby boomer generation that owns these businesses facing challenges with succession; and U.S. manufacturing continuing to grow in an industrial resurgence underpinned by near-shoring/reshoring.

MMD: What are some headwinds you’re watching in the space, and how do you plan to drive growth despite those?

MAY: While we anticipate broader market softness due to elevated interest rates, geopolitical tensions and supply chain interruptions, historically CORE has strategically targeted manufacturers with highly differentiated value propositions and end markets that are inherently resistant to market cycles. Additionally, CORE’s leadership team, with a combined 100-plus years of operating experience, has navigated prior cycles as the CEOs of comparable businesses, allowing us to better anticipate and mitigate challenges.

MMD: At the start of 2024, experts predicted a strong year for industrials M&A—how has the dealmaking environment been shaping up thus far this year?

MAY: The dealmaking environment has been softer than anticipated through the first half of the year. However, despite the challenging environment, CORE continues to pursue select opportunities in strategic and thematic verticals with substantial capital to deploy from the recently closed Flagship Fund III and Services Fund I. //

HILARY COLLINS is ACG’s associate editor.

Uncover proprietary transactional information provided by an established pool of private equity groups on a blind and confidential basis. Obtain accurate and up-to-date information to value and assess middle-market businesses.

When it comes to valuing M&A transactions in the middle market, no other source provides the level of quality and granularity as GF Data.

GF Data provides the most reliable data on private-equity sponsored M&A transactions with enterprise values of $10 million – $500 million.

To learn more about subscribing or contributing, scan the code or contact bdunn@acg.org. GFData.com

GF Data is proud to be part of the ACG family.

Artificial intelligence is all the rage, even as organizations struggle to develop rules of engagement. AI governance has been hampered by patchwork regulations, a lack of understanding about the technology and little clarity around who within a company should be responsible for oversight.

Political backlash over environmental, social and governance considerations in investing has forced private equity firms to reconsider if and how to include ESG as part of their strategies, and how to strike the right balance between values and value creation.

Experts weigh in on some of the pitfalls of using artificial intelligence and how regulation and corporate governance around these tools could start to take shape

BY BRITT ERICA TUNICK

While there is little doubt among private equity firms that artificial intelligence will play an important role in driving up valuations for future deals, there is less certainty about how to handle AI-specific corporate governance. Although regulators are actively working to establish rules for the use of AI, most private equity firms have done little in the way of creating policies for this new technology—both at the firm level and portfolio companies.

“Right now, it still feels a little like the Wild West, and companies are all over the place. They’re figuring out where to test the waters and how to do it in a way that is risk-appropriate until they can get more comfortable with the technology and have the appropriate processes and policies in place,” says Glynna Christian, head of law firm Holland & Knight’s Global Technology Transactions practice.

“This is all still super new, and lawyers are just catching up with this in the last six to 12 months,” she adds, noting that the number of attorneys focusing on the issue seems to have doubled over the past year. As lawyers get up to speed, Christian says conversations about corporate governance and risk are beginning to be elevated to the board level.

Lawsuits in the U.S. and Europe against AI platforms are also spurring PE executives to pay attention to the issue, amid allegations of copyright infringement and outright data theft. In the case of Stability AI, Getty Images filed suit alleging that the platform copied millions of its copyrighted images and that the algorithm can be used to replicate the style of its artists. A similar copyright suit was filed against OpenAI by two authors who allege that the AI platform has copied more than 300,000 books to train its algorithms. Meanwhile, PE firms’ own fears about having their data and proprietary information compromised by AI technology loom large and have contributed to the slow pace of adoption within the industry.

While comprehensive AI legislation has yet to emerge in the U.S., there are already multiple regulations in place. Federal agencies have issued guidance, including the Department of Justice, the Securities and Exchange Commission and the Consumer Financial Protection Bureau, among

Right now, it still feels a little like the Wild West, and companies are all over the place. They’re figuring out where to test the waters and how to do it in a way that is riskappropriate until they can get more comfortable with the technology and have the appropriate processes and policies in place.

GLYNNA CHRISTIAN Head of Global Technology Transactions, Holland & Knight

others. The White House Office of Science and Technology Policy has issued its own guidance, and multiple bills have been proposed in Congress. There are also a wide range of state-level consumer protection laws. Although nearly all share common themes, such as data and privacy protection, bias prevention and mitigation of false information, the laws differ significantly across states.

Such inconsistencies and a lack of comprehensive AI regulations are making it difficult for PE firms to identify best practices. “There are a lot of AI regulations coming, especially at the state level in the U.S.,” says Avi Gesser, a partner and co-chair of the data strategy and security group at law firm Debevoise & Plimpton. “This is going to lead to a patchwork of inconsistent, sometimes vague, overlapping regulations on a technology that is changing quickly and can be used in all aspects of business, ranging from simple, low-risk uses like brainstorming, to complex, high-risk use cases like deciding who should be hired or which customers

should get large amounts of credit.”

The European Union’s Artificial Intelligence Act (the AI Act) might offer clues for how U.S. regulations will progress. A 108-page document that outlines EU regulators’ plans to monitor how AI systems work and how they are being used by businesses, the AI Act applies to any organization that uses AI and does business within the EU.

The law focuses on multiple aspects of AI, from how algorithms or apps use and protect people’s personal information and conform to existing data and privacy laws, to the prohibition of “unacceptable risks,” such as deceptive tactics to influence people’s decision-making. Other aspects include documentation requirements and the ability to demonstrate compliance upon request.

Though the law was passed by the European Parliament in early March and approved by the EU Council in late May, industry experts say the regulation wasn’t well thought out and there is little clarity about which divisions of government will ultimately be responsible for executing it. “Just because something is a regulation doesn’t mean it’s going to stick. … They put a hard year into the AI Act and were dedicated to getting it out the door, but when regulations get passed in a way that leaves so many people asking so many questions, it makes it harder for the next round of laws to get attention,” notes one industry expert.

Regardless, the increase of regulatory focus has the PE industry’s attention. “It’s still early days, but there is no question AI governance is becoming a more frequent topic on due diligence questionnaires,” says Ken Bisconti, co-head of financial software company SS&C Intralinks. “There is a wide variation in the market in terms of comfort around AI and how an acquisition target approaches its governance.” Intralinks itself uses AI tools in its products, which host data rooms for companies going through M&A processes.

Though there are significant differences in the regulations that have emerged, a central concern of regulators is data privacy and security. While regulators are largely focused on third-party risks regarding consumer data, as well as potential biases within AI platforms that could negatively

impact individuals, a major concern for PE firms is the possibility that AI tools—particularly generative AI—could result in leaked proprietary data and confidential information. “Firms want to ensure AI systems don’t inadvertently leak sensitive data such as personal information, trade secrets or intellectual property. They are focused on implementing robust cybersecurity measures to protect AI models and training data from unauthorized access and manipulation,” says Bob Petrocchi, co-head of SS&C Intralinks.