Real Estate Pros Rally in Recovery Efforts After Helene's 'Catastrophic Devastation' Melissa Dittmann Tracey

Magazine is Self-Supporting

Salt Lake Realtor® Magazine is self-supporting. The advertisers in this magazine pay for all production and distribution costs. Help support this magazine by advertising. For advertising rates, please contact Mills Publishing at 801.467.9419. The paper used in Salt Lake Realtor® Magazine comes from trees in managed timberlands. These trees are planted and grown specifically to make paper and do not come from parks or wilderness areas. In addition, a portion of this magazine is printed from recycled paper.

The Secret to Better Feedback

President Dawn Stevens Real Broker

First Vice President

Claire Larson Woodside Homes of Utah LLC

Second Vice President

Jodie Osofsky Summit Sotheby's

Treasurer

Amy Gibbons KW South Valley Keller Williams

Past President

Rob Ockey Berkshire Hathaway

CEO Curtis Bullock

DIRECTORS

Janice Smith

CB Realty (Union Heights)

Laura Fidler

Summit Sotheby's (Draper)

Jenni Barber Berkshire Hathaway

J. Scott Colemere Colemere Realty Assoc.

Chris Anderson Windermere Real Estate - Utah

Morelza Boratzuk RealtyPath (South Valley)

Michael Rowe CB Realty (SL-Sugarhouse)

Eric Santistevan Engel & Volkers (Holladay)

Hannah Cutler CB Realty (Union Heights)

Michael (Mo) Aller Equity RE (Advantage)

Linda Mascher Realtypath LLC (Advisors)

Advertising information may be obtained by calling (801) 467-9419 or by visiting www.millspub.com

Managing Editor Dave Anderton

Publisher Mills Publishing, Inc. www.millspub.com

President Dan Miller

Art Director Jackie Medina

Graphic Design

Ken Magleby

Patrick Witmer

Office Administrator

Cynthia Bell Snow

Sales Staff Paula Bell Dan Miller

Salt Lake Board: (801) 542-8840 e-mail: dave@saltlakeboard.com Web Site: www.slrealtors.com

and

of

Permission will be granted in most cases, upon written request, to reprint or reproduce articles and photographs in this issue, provided proper credit is given to The Salt Lake REALTOR as well as to any writers and photographers whose names appear with the articles and photographs. While unsolicited original manuscripts and photographs related to the real estate profession are welcome, no payment is made for their use in the publication.

Views and opinions expressed in the editorial and advertising content of the The Salt Lake REALTOR are not necessarily endorsed by the Salt Lake Board of REALTORS . However, advertisers do make publication of this magazine possible, so consideration of products and services listed is greatly appreciated.

Ever noticed the mysterious vanishing act of feedback and good customer service in real estate? You show a house, and then… crickets. No notes, no feedback—nothing. You’ve sent multiple emails, a text, and even a voicemail, yet still, silence. Sound familiar?

Providing timely and constructive feedback after a property showing is one of the most crucial aspects of real estate communication. When buyer agents share insights with seller agents, it helps sellers understand how their property is perceived: Is the pricing right? Does the home need adjustments? Is it appealing to buyers?

Despite the critical value feedback offers, it’s often overlooked— sometimes due to time constraints, other times simply because the process is inefficient. But there’s a solution: platforms like Aligned Showings, available through the Multiple Listing Service (MLS), make providing feedback much simpler and streamlined. Timely feedback enhances professional relationships, contributes to smoother transactions, and demonstrates collaboration and transparency—key qualities in a successful agent.

Aligned Showings is more than just a showing management tool; it’s a game-changer for feedback communication between buyer and seller agents. Here’s how to use it effectively:

1. Add Aligned Showings to Your Listing

Once you secure a listing, you can easily integrate Aligned Showings through the “Manage Listings” section on UtahRealEstate.com. This ensures that all feedback for each showing is well-organized and easily accessible.

2. Access the Platform

On your UtahRealEstate.com dashboard, simply click the Aligned button—conveniently located on the left side of the page. This will take you directly to the interface where you can manage showings and feedback effortlessly.

3. Set Up a Feedback Survey

Navigate to step #5 under Listings Set Up: the Feedback Survey. Customize a feedback form that touches on key points—buyer interest in the property, pricing opinions, or feedback on the home’s features. Once completed, the form can be sent automatically to your seller for immediate review.

If we can’t take 30 seconds to fill out a feedback form, how can the public perceive us as professionals? To truly shine in this industry, we need to step up our customer service game, and it starts with something as simple as completing a five-question form. Trust me, your sellers will thank you, your reputation will sparkle, and hey, you might even start a trend!

Dawn Stevens President

The Salt Lake Board of REALTORS

Happenings

Five Realtors® to Join Board of Directors

The Salt Lake Board of Realtors® congratulates Kim Farber, Kristel Gough, Lori Khodadad, Russell Orchard, and Donna Pozzouli on their election to the Board of Directors. These candidates received the highest number of votes from the general membership and will each serve a four-year term starting Jan. 1. The 16-member Board of Directors® guides the association’s mission to lead in providing support to professional Realtors® through advocacy, education, communication, and service.

In the News

Increased Housing Demand Pushes Prices Higher

The dramatic increase in immigration in recent years has implications for housing costs, according to a report released in September by the Center for Immigration Studies, an independent, non-partisan, non-profit research organization.

Immigration is significantly increasing demand for housing, particularly rental properties. Of households headed by immigrants who arrived between January 2022 and August 2024, 89.5 percent reported being renters.

The Census Bureau noted that the rise in rents during 2023 was by far the largest in the past decade. This is consistent with the possibility that immigration, including illegal immigration, has significantly driven up housing prices in areas with heavy immigrant settlement.

“The city of New York reports that it has spent or expects to spend $12 billion over the next three years on housing, food, health care, and other services for recently arrived illegal

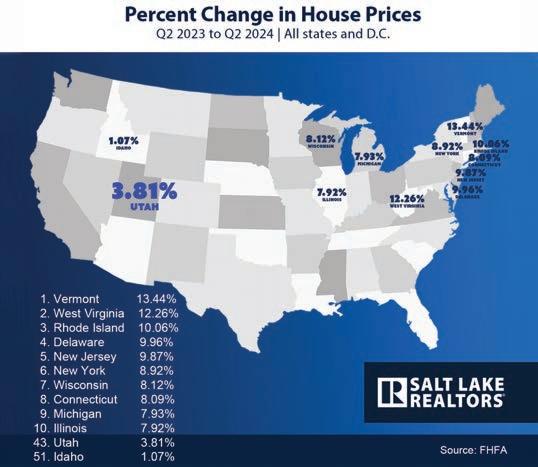

Utah House Prices Increased in the Second Quarter

U.S. house prices rose by 5.7% between the second quarter of 2023 and the second quarter of 2024, according to the Federal Housing Finance Agency (FHFA). In Utah, home prices increased by 3.81% over the past year, ranking among the bottom 10 states in slowest appreciation. However, Utah home prices have risen by 65.33% over the past five years. “U.S. house prices experienced their third consecutive slowdown in quarterly growth,” said Dr. Anju Vajja, Deputy Director of FHFA’s Division of Research and Statistics. “The slower pace of appreciation as of the end of June was likely due to higher home inventory and elevated mortgage rates.”

immigrants,” according to the report. “To cover these new expenses, the city plans to cut its budget by 5 percent across various services, including sanitation, public education, and the police department.”

Immigration likely affects the housing market in complex ways. While it drives up demand for housing, it can also lower construction costs by reducing wages in the construction industry, the report noted. Conversely, it may indirectly impact affordability by lowering wages, making housing relatively more expensive.

The Keys to Aging at Home? Frank Conversations and Financial Planning

What to do now to stay in your own home as you grow older.

By Clare Ansberry

Staying in your own home as you get older can strain finances and family members. Preparing can lessen the burden of aging in place.

About 77% of older adults want to age in their current home. Doing so requires an objective assessment of the home, honest discussions with family, and a realistic financial plan. Delaying preparation—or not preparing at all—makes the difficult task of aging at home even harder.

Almost nine out of 10 Americans 65 and older lived in their own home in 2021, according to Harvard

University’s Joint Center for Housing Studies. Often those homes have stairs and narrow doorways, and need modifications. As people age, they may need help from adult kids or require paid in-home care, which can be more expensive than people think and generally isn’t covered by Medicare.

“You have to consider the variables when you grow older,” including a home’s size and safety, said Ken Dychtwald, 74 years old, co-founder and chief executive of Age Wave, a California-based consulting firm specializing in aging-related issues. “We think about child-proofing a home. How do you age-proof a home?”

Only about half of adults 65 and older say they have had serious conversations with loved ones about future needs—who will help take care of them and how they will pay for it—according to a recent survey by KFF, a health-research nonprofit.

“Frank discussions with kids can be unnerving,” said Dychtwald. “We talk about vacations and hopes and dreams for their lives. We need to have the same discussion about what to do when we get older.” If parents aren’t forthcoming, adult kids need to be upfront about what they can and can’t do.

Ronna Lichtenberg, 73, told her adult stepchildren that she and her husband were financially stable but handling their own expenses meant less wealth to pass on.

“That money will go to take care of us. If you want an inheritance, speak up now,” she recalled saying. None did. “I just forced the conversations once I realized how hard they are,” said Lichtenberg, owner of the socialmedia platform Granny Ronna.

A certified financial planner, Danielle Miura, 29, raised the subject while visiting her parents and discovered they have different visions. Her mom, she said, likes socializing and the idea of a 55-plus community, and her dad likes his privacy.

“I’m an only child. I want to start asking these questions,” said Miura, of Ripon, Calif.

Home is where the steps are

Less than half of adults ages 65 to 79 lived in singlefloor homes with a no-step entry, according to a 2023 Harvard University study. Steps can be a hazard. Onefourth of Americans 65 and older fall each year. Home elevators are an option but can cost between $20,000 and $100,000.

Smart-home technology, including security doorbells and fall-detection sensors, can help people live at home longer and provide peace of mind to adult kids who live far away, said Andy Miller, who started AARP’s AgeTech Collaborative, a group of businesses developing agingrelated technology. His parents, who live in Florida, can control lights and other devices with their voice.

“They have voice-enabled everything,” said Miller, 54. He lives in Boston and is building a new home that will have ambient monitoring throughout, wood floors without thresholds and safety knobs on the stove.

Patricia Wahlgren, an Omaha, Neb.-based gerontologist and certified aging-in-place specialist, visits homes for $250 and makes recommendations to add lighting, replace doorknobs and enlarge bathrooms; she’ll also review transportation options and nutrition. Wahlgren,

Introducing our exclusive monthto-month rental 55+ Independent Living cottages, the first of their kind in Utah! These twin homes range from 1,500 to 2,300 sf and feature 2 bedrooms, 2 baths, an office/den, fireplace, double car garage, and front/back yards—entirely maintained by us. Enjoy spacious, zero-transition homes with the convenience of senior living amenities, including 24/7 emergency services, Chefprepared meals, housekeeping, Art of Living Well® programming, beautiful gardens, outdoor spaces, and a clubhouse - offering seniors complete maintenance-free living!

51, said she and her husband are modifying their home incrementally and added grab bars, single-lever faucets and a higher toilet during a recent bathroom update.

Money matters

The ability to age at home often depends on your resources. Financial experts say you should know what you have in savings and home equity to remodel if needed, understand what is—and isn’t—covered by insurance, and anticipate living expenses.

The median national cost for round-the-clock in-home care is about $24,000 a month, according to Genworth, a long-term-care insurance company, with higher costs in states like California, where monthly median costs are close to $27,000.

“Financial planning is crucial,” said David Brillant, a lawyer in Walnut Creek, Calif., who specializes in estate planning and taxation. Many families will need longterm-care insurance, home equity or both.

Equity in the home—refinancing or a home-equity credit line—can help pay for remodeling and in-home care, but interest rates affect that decision. In 2022, median home equity for 65 and older homeowners was

$250,000, according to the Harvard study. About 60% of homeowners ages 65 to 79 are mortgage-free on their primary homes, the study found.

Insurance can help but has limits. Private long-termcare insurance, which can be costly, will pay for in-home care but generally doesn’t cover the first 90 days of care and has payment caps. Short-term care insurance, which also covers home-care costs, is less expensive and typically offers a year of benefits.

Durr Sexton, 67, president of a national insurance brokerage firm in Houston, said people need to carefully review their policies and ask professionals for clarification. He recalls a fellow broker—who had a long-term-care policy and was caring for his wife who had Alzheimer’s— not fully using it because the broker misread the policy and thought the benefits were more limited.

“People need to understand the benefits,” said Sexton. “They need to understand the limitations.”

Write to Clare Ansberry at clare.ansberry@wsj.com.

Interest rates on home loans are built up using an index based on the current market, such as the bond market, and a markup that represents the lender’s profit.

By The Lighter Side of Real Estate

If you’re like many home buyers, sellers, or even real estate agents, you might have gotten excited when you heard that the Federal Reserve recently cut its benchmark interest rate

After watching them hike the rate 11 times since 2022 and reaching its 23-year high, it sounds like great news, right? After all, shouldn’t lower rates from the Fed mean cheaper mortgages, more buying power, and a potential boost in home sales? Whether you’re a buyer hoping to secure a lower monthly payment or a seller eager for more buyer activity, it seems logical to expect that the Fed’s decision will immediately affect the mortgage market.

However, while it’s understandable why so many people believe that a Fed rate cut leads directly to lower mortgage rates, this is a common misconception.

You’re not wrong to think that the two might be related. After all, the Federal Reserve is the central bank of the United States, and its policies influence many aspects of the financial system. When you hear the news about a rate cut, it’s easy to assume that this would directly

impact mortgage rates since they both involve lending and borrowing. In fact, many real estate professionals and media outlets fuel this assumption, highlighting potential benefits to home buyers and sellers when the Fed announces a change.

And to some extent, there is a ripple effect that can occur over time. However, it’s crucial to understand that the Fed doesn’t directly set mortgage rates. Mortgage rates are influenced by a different set of factors altogether.

If Rates Aren’t Tied to the Fed’s Moves, What Actually Drives Them?

While the Fed’s rate cuts don’t set mortgage rates, the economic conditions they influence — like inflation, consumer confidence, and lending activity — can have an indirect effect over time.

The Federal Reserve controls short-term interest rates through its decisions about the federal funds rate. But the 30-year fixed mortgage rate, for example, follows longer-term rates, and are primarily influenced by the

bond market — specifically the yield on the 10-year U.S. Treasury bond.

When the Fed cuts rates, they’re typically trying to spur the economy by making borrowing cheaper in the short term. However, mortgage rates, which are based on longer-term economic outlooks, don’t always move in lockstep. In fact, mortgage rates could potentially increase after a Fed rate cut, if the bond market senses inflation or economic instability on the horizon. Although, according to Yahoo Finance, the average rate did happen to dip 0.11 percentage point after the Fed announcement, bringing it to the lowest level since early February 2023.

When investors buy Treasury bonds, they typically seek safety — meaning they might flock to these bonds during times of economic uncertainty. As demand for bonds increases, yields (or interest rates) decrease.

Since mortgage lenders tend to set their rates based on what’s happening with these longer-term bond yields, this is the key area to watch when trying to predict mortgage rate movements.

But honestly, even knowing that it’s the 10-year U.S. Treasury bond you should be watching doesn’t really do you any good. There are so many factors involved when it comes to the current average mortgage rates, and it would be nearly impossible for even a mortgage expert

or economist to base their real estate sale or purchase on what and when they predict the market will do in the future.

Rates Matter, but Your Needs Matter More

Of course, interest rates matter to some degree when you’re deciding to buy or sell a house. They will impact how much you pay per month, which can dictate what you can and can’t afford, and whether it’s a viable decision for you to move.

But if you can afford the monthly payments, you should buy or sell a house when it makes sense for you personally, not based upon the current mortgage rates.

For example, if you need to buy or sell a house because you’re bursting at the seams and need a bigger place, or because you’re relocating to a different area, or getting married or divorced, waiting for rates to possibly come down a smidge like they did last week probably isn’t going to be worth the wait.

Many buyers, sellers, and even agents get overly optimistic when they hear about a rate cut, assuming that mortgage rates will automatically follow. Unfortunately, this can lead to disappointment, and end up impacting their decision-making process.

Imagine delaying a home purchase in anticipation of lower rates, only to watch mortgage rates inch even higher due to factors unrelated to the Fed’s actions. Or waiting to sell your house until rates are lower because you think it will mean more buyers will be in the market,

only to find that when rates finally do come down, it’s switched to a buyers’ market in your area because of bigger issues in the economy.

So, what does all of this mean for you as a home buyer or seller? It’s essential to understand that mortgage rates are influenced by a complex web of factors, not just the Federal Reserve. While the Fed’s actions can have an indirect impact on mortgage rates over time, basing your decisions solely on Fed announcements is risky.

As a buyer, your best move is to stay informed about broader economic conditions and keep an eye on Treasury yields. Remember, mortgage rates tend to follow the bond market, so when yields drop, mortgage rates likely will too. Don’t wait around for a Fed decision to dictate your next steps—talk to your lender, lock in a rate when it’s favorable, and focus on your long-term financial picture.

As a seller, it’s easy to get caught up in the excitement of potential rate cuts and assume that they’ll drive a flood of buyers to your home. While lower mortgage rates can certainly increase buyer activity, remember that real estate is hyper-local, and the broader market sentiment (like economic confidence) plays a larger role. Instead of waiting for an uncertain rate change, focus on pricing your home competitively, staging it well, and working with your agent to market it effectively.

Source: The Lighter Side of Real Estate. Check out their content marketing services at lightersideofrealestate.com.

Image licensed by Ingram Image

Why We Need the 30-Year Fixed-Rate Mortgage

The New York Times has questioned the cultural and economic reliance on homeownership in the U.S.

By The Salt Lake Board of Realtors®

The 30-year fixed-rate mortgage has long been the bedrock of the American dream, offering millions of families an affordable and stable path to homeownership. However, this pillar of financial security is now under threat, as discussions about eliminating it grow louder in some policy circles. Doing away with the 30-year mortgage could mean skyrocketing monthly payments, putting homeownership out of reach for many middle-class Americans.

Fortunately, the Realtors® Political Action Committee (RPAC) is on the front lines, fiercely advocating to protect this vital mortgage option. By lobbying on Capitol Hill, RPAC is fighting to ensure that the 30-year mortgage remains accessible, keeping the dream of homeownership alive for future generations. Without their efforts, millions could face a housing market dominated by unaffordable,

shorter-term loans, destabilizing families and communities across the country.

The 30-year fixed-rate mortgage, first introduced during the Great Depression, revolutionized the housing market by allowing homebuyers to lock in stable, long-term interest rates. Before its creation, mortgages were typically short-term, with high down payments and balloon payments due at the end. This made homeownership difficult for many Americans and contributed to the widespread foreclosures of the 1930s. Today, the 30-year mortgage remains a popular option because it offers predictability, allowing homeowners to budget long-term without fear of rising interest rates. However, this stability is not without its critics.

In a Nov. 19, 2023, article titled “A 30-Year Trap: The Problem With America’s Weird Mortgages,” The New York Times argued that the 30-year mortgage poses

significant risks for lenders and questioned the cultural and economic reliance on homeownership in the U.S. Ultimately, the piece challenged the long-standing belief that homeownership, supported by 30-year fixedrate mortgages, is universally beneficial.

Last month, The Times explored how younger generations in the U.S. are beginning to reshape the traditional idea of the American Dream, which has historically centered around homeownership. The article, “The American Dream Without a House? Believe It,” examined how the concepts of prosperity and personal fulfillment are evolving as the housing market becomes increasingly inaccessible to young adults. With soaring housing costs, rising inflation, and student loan debt, many millennials and members of Gen Z are finding homeownership more and more out of reach.

Forbes magazine has called for the 30-year mortgage to disappear. “The 30-year fixed rate mortgage should be retired — for good,” the article said. “Despite continued proof that it fails to build up wealth for the most disadvantaged Americans, and that mortgage debt should not be a burden as homeowners approach their 50s and 60s, misguided advocates maintain that the 30-year fixed rate mortgage should

be at the core of the U.S. housing finance system.”

In addition, some members of the banking and financial sectors argue that the 30-year mortgage, with its long-term fixed interest rates, can be less profitable and more difficult to manage than shorter-term or adjustable-rate mortgages (ARMs). ARMs allow banks to adjust interest rates based on market conditions, transferring the risk to borrowers. However, if the 30-year fixed-rate mortgage were eliminated and replaced with shorter-term mortgages (such as 15- or 20-year loans), monthly payments would typically be higher. This is because the loan principal would need to be paid off over a shorter period, increasing the amount borrowers must pay each month.

RPAC consistently opposes legislative or regulatory changes that could threaten the availability of the 30year mortgage. For example, the committee has fought against proposals to reduce the role of governmentsponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. These GSEs help maintain liquidity in the housing market, ensuring that banks can offer affordable 30-year mortgages to homebuyers. Without this government backing, access to long-term fixed-rate loans could become more limited, potentially increasing borrowing costs for millions of Americans.

Through its tireless efforts, RPAC continues to champion the 30-year fixed-rate mortgage, ensuring that it remains a stable and affordable option for homebuyers across the country.

Digestible, one-page resources provide clear guidance on key topics for home buyers and sellers working with agents who are Realtors®.

By The National Association of Realtors®

The National Association of Realtors® announced a new series of consumer resources designed to help agents who are Realtors® empower home buyers and sellers following recent practice changes. To date, NAR has published six installments in the series and will continue to release new resources in the weeks ahead.

You can find the installments at facts.realtor.

“At the heart of what we do as Realtors® – who abide by a strict code of ethics – is protect and promote the interests of our clients,” said Kevin Sears, President of the National Association of Realtors®. “We are committed to making the process of buying or selling a home as transparent and seamless as possible for clients, and

this new series of guides provides an exceptionally clear roadmap for the process of working with an agent who is a Realtor®.”

The following guides are currently available – in English and Spanish – on NAR’s website:

1. Why am I being asked to sign a written buyer agreement: covers recent practice changes when it comes to working with a real estate professional as a home buyer.

2. Open houses and written agreements: covers what buyers need to know about touring homes, attending open houses and when a written buyer agreement is needed.

3. Realtors’® duty to put client interests above their own: covers NAR’s strict Code of Ethics that all agents who are Realtors® must follow and their ethical duties to act in their client’s best interests.

4. What veterans need to know about buying a home: covers what NAR is doing to promote access to financing for veterans and highlights the options available to veteran buyers in their homebuying process.

5. Offers of compensation: covers the process and options available for offering compensation to a buyer’s agent and the reasons why this may be a compelling option for sellers to consider when marketing their property.

About the National Association of Realtors®

6. Negotiating written buyer agreements: covers what home buyers should expect when negotiating a written buyer agreement with an agent who is a Realtor®.

The National Association of Realtors® is America’s largest trade association, representing 1.5 million members involved in all aspects of the residential and commercial real estate industries. The term Realtor® is a registered collective membership mark that identifies a real estate professional who is a member of the National Association of Realtors® and subscribes to its strict Code of Ethics.

Housing Competition Remains Fierce

Sixty percent of home sellers nationwide sold their home in less than a month.

By Melissa Dittmann Tracey

Despite a sluggish summer for home sales, potential buyers are still facing pockets of steep competition in some parts of the housing market.

Sixty percent of home sellers nationwide sold their home in less than a month, a sign of strong buyer demand, according to the latest Realtors® Confidence Index, a survey of 1,600 NAR members. But the market has eased somewhat, with the average home listed in August receiving 2.4 offers, down from 3.2 a year earlier. Twenty percent of homes sold above list price in August, down from 31% a year ago.

In areas where competition remains high, some home buyers are still waiving contingencies to make their offers stronger. For example, 18% of buyers waived the inspection contingency and 20% waived the appraisal contingency in August, according to NAR’s data. Whether the fall market fares better than summer likely will depend on where you live. “In areas with persistent housing shortages, principally in the Northeast region, the recent falling interest rates could reignite more buyer interest—but without necessarily increasing supply,” said NAR Chief Economist Lawrence Yun. “Therefore, multiple offers could intensify.”

On the other hand, Yun noted that in areas with a measurable increase in inventory, like in the South,

the number of buyers could match or even outpace housing supply.

Home buyers also are increasingly facing off against cash buyers. Twenty-six percent of buyers in August paid in cash, much higher than the historical average of 15%, according to NAR research. “Those in the ‘haves’— compared to the ‘have-nots’—are doing well,” Yun said. “Record high stock market wealth, along with record high housing wealth, allows for more cash purchases.”

NAR membership remained high at the end of August, about 1.53 million, showing that real estate remains a viable career, Yun said. “It could be due to more listings coming onto the market,” he noted. Since 2020, inventory levels have been at all-time lows but are gradually starting to climb. “Inventory levels are 20% above one year ago,” Yun said. “That requires more activity and movement of Realtors®.”

Yun also noted that falling mortgage rates tend to lead to greater buyer activity, so real estate pros may perceive more business opportunities are coming.

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine and editor of the Styled, Staged & Sold blog.

NAR Recognizes 2024 Good Neighbor Award Winners

Each of the five winners will be awarded a $10,000 grant for their charity and be featured in the fall 2024 edition of Realtor® Magazine.

By The National Association of Realtors®

The National Association of Realtors® proudly unveiled the five winners of the 2024 Good Neighbor Awards. Celebrating its 25th year, these distinguished awards spotlight Realtors® who are not only experts in their field but also champions of volunteerism.

The 2024 Good Neighbor Award winners are as follows:

Ed Gardner, Gardner Real Estate Group (Portland, Maine)

Stacy Horst, Keller Williams Atlantic Partners (Fernandina Beach, Florida)

Christopher Johnson, Imagine Associates LLC Realty (Ellenwood, Georgia)

Danette Johnson, Moab Realty (Moab, Utah)

Charlie Wills, Charlie Wills Team–Real Estate Partners (Madison, Wisconsin)

“Good Neighbor Award winners exemplify the spirit of caring and the heartfelt commitment that defines the best of our profession,” said NAR President Kevin Sears, broker-associate of Sears Real Estate/Lamacchia Realty in Springfield, Massachusetts. “Their dedication extends beyond traditional real estate boundaries, forging significant, positive changes in their neighborhoods and underscoring the vital role that agents who are Realtors® play in building stronger, more resilient communities.”

Each of the five winners – selected by a multistage, criteria-based judging process – will be awarded a $10,000 grant for their charity and be featured in the fall 2024 edition of REALTOR® Magazine. NAR will formally present each with their official award on November 9 during NAR NXT, the association’s annual conference, hosted this year in Boston.

More About Each Winner:

Ed Gardner, Gardner Real Estate Group (Portland, Maine)

Gardner founded the Equality Community Center, which houses 18 LGBTQ-focused nonprofits under one roof with below-market rent. This arrangement fosters collaboration and increases operational efficiency among the organizations, reducing duplicated efforts. Additionally, he is spearheading the nonprofit’s latest project, the development of a 54-unit affordable housing complex for seniors.

Stacy Horst, Keller Williams Atlantic Partners (Fernandina Beach, Florida)

Horst co-founded Erin’s Hope for Friends following the tragic loss of her 17-year-old daughter, Erin, who struggled with social connections and ultimately took her own life. In her memory, Horst and her husband established e’s Club, a supportive space for teens and young adults on the autism spectrum. The club fosters lasting relationships through joyful interactions and has positively impacted the lives of more than 1,500 individuals.

Christopher Johnson, Imagine Associates LLC Realty (Ellenwood, Georgia)

Johnson, a board member of 100 Black Men of DeKalb and holder of a doctorate in education, leverages his background as a teacher and principal to enhance educational and economic opportunities for African American youth. As a mentor, he teaches financial literacy and leadership skills, and organizes trips to broaden children’s horizons. He has contributed significantly to the growth of the organization at the local and national levels and has helped introduce financial literacy programs for teens to his local real estate board.

Danette Johnson, Moab Realty (Moab, Utah)

Johnson was a founding member of the Moab Free Health Clinic, which was established in 2008 to serve uninsured and underinsured individuals in this rural and remote area. The clinic handles approximately 3,000 appointments annually, offering primary care, mental health services, vision screening and dental care. Using her real estate expertise, she helped the clinic secure larger facilities due to growing demand for its services.

Charlie Wills, Charlie Wills Team–Real Estate Partners (Madison, Wisconsin)

Wills, co-founder of 100 Men of Dane County, initiated a program where 100 community members make a significant impact by committing to donate $4,000 annually. Each quarter, they accept proposals from local nonprofit causes supporting children and select one to receive a $100,000 grant. To date, they have donated more than $2.3 million in grants, primarily benefiting small nonprofits.

In addition to the winners, the following Realtors® have been recognized as Good Neighbor Awards honorable mentions and will each receive $2,500 grants for their charity:

• Daniel Davies, Davies-Davies & Associates Real Estate (Queensbury, New York)

• Howard Friedman, Compass Commercial Real Estate (Bend, Oregon)

• Beth Gilbreath, Century 21 Signature (Dubuque, Iowa)

• Tisha Janigian, She Is Hope Realty (Canoga Park, California)

• Alicia Stukes, LPT Realty Inc. (Bowie, Maryland)

NAR’s Good Neighbor Awards program is sponsored by Realtor.com®. In September, the public was invited to vote for their favorite of the 10 finalists. The top three vote-getters all received additional donations for their charities. The following Realtors® have been crowned as this year’s Web Choice Favorites:

• Beth Gilbreath, who will receive an additional $2,500 bonus donation for The Red Basket Project Inc.

• Tisha Janigian, who will receive an additional $1,250 bonus donation for She is Hope LA.

• Stacy Horst, who will receive an additional $1,250 bonus donation for Erin’s Hope for Friends.

“The Good Neighbor Awards showcase the exceptional commitment of real estate agents who go above and beyond their professional duties to enrich the lives of so many in their communities,” said Realtor.com® CMO Mickey Neuberger. “We extend our congratulations to this year’s winners, finalists and Web Choice Favorites, and commend every agent dedicated to making the world a better place – it all begins with being a good neighbor.”

About the National Association of Realtors®

The National Association of Realtors® is America’s largest trade association, representing 1.5 million members involved in all aspects of the residential and commercial real estate industries. The term Realtor® is a registered collective membership mark that identifies a real estate professional who is a member of the National Association of Realtors® and subscribes to its strict Code of Ethics.

About Realtor.com®

Realtor.com® is an open real estate marketplace built for everyone. Realtor.com® pioneered the world of digital real estate more than 25 years ago. Today, through its website and mobile apps, Realtor.com® is a trusted guide for consumers, empowering more people to find their way home by breaking down barriers, helping them make the right connections, and creating confidence through expert insights and guidance. For professionals, Realtor. com® is a trusted partner for business growth, offering consumer connections and branding solutions that help them succeed in today’s on-demand world. Realtor.com® is operated by News Corp [Nasdaq: NWS, NWSA] [ASX: NWS, NWSLV] subsidiary Move, Inc. For more information, visit Realtor.com®.

of Ownership, Management and Circulation

1. Location of known Office of Publication: 772 E. 3300 S., Suite 200, Salt Lake City, Utah 84106

2. Location of known Headquarters of General Business offices of the Publisher: 772 E. 3300 S., Suite 200, Salt Lake City, Utah 84106

3. Publisher: Mills Publishing, Inc., 772 E. 3300 S., Suite 200, Salt Lake City, Utah 84106

4. Editor: Dave Anderton, Salt Lake Board of Realtors, 230 W. Towne Ridge Parkway, Suite 200, Sandy, Utah 84070

5. Owner: Salt Lake Board of Realtors, 230 W. Towne Ridge Parkway, Suite 200, Sandy, Utah 84070

6. Known bondholders, mortgages, and other security holders owning or holding 1 percent or more of total amount of bonds, mortgages or other securities: None.

7. Extent and nature of circulation:

Miller, President of Mills Publishing, Inc. 9/30/2024

Image licensed by Ingram Image

Real

Estate Pros Rally in Recovery Efforts After Helene’s ‘Catastrophic Devastation’

You can help provide housing-related assistance to households affected by the deadly hurricane and flooding.

By Melissa Dittmann Tracey

Real estate professionals have acted quickly to bring relief to victims of September’s killer storms.

Hurricane Helene unleashed a 500-mile path of destruction that stretched across six states this weekend, bringing the force of a record-breaking storm surge and strong winds that wiped away or flooded homes and businesses, leaving at least 116 people dead and many still unaccounted for. In response, real estate professionals are stepping up to help affected

communities, and the Realtors® Relief Foundation is actively raising funds for housing-related assistance to help disaster victims.

“The destruction and disruption to daily life is unimaginable,” Tony Harrington, North Carolina Realtors® 2024 president, posted in a video to members.

Buncombe County, N.C., was among the hardest hit places by the storm’s catastrophic flooding and mudslides, which killed at least 30 people in that

"Real estate professionals can play a crucial role in providing community support and helping in recovery efforts."

– Gia Arvin, Florida Realtors® President

county alone. North Carolina Gov. Roy Cooper said the hurricane caused “catastrophic devastation of historic proportions” in the state.

Helene made landfall in Florida as a Category 4 hurricane on Sept. 26, then barreled in as a tropical storm that plowed through Florida, Georgia, Tennessee and the Carolinas. “Families have lost homes, businesses or even loved ones,” Harrington said in the association’s video. “We’re committed to providing all the support and assistance possible in recovery and rebuilding. … Every contribution—no matter how small—will make a difference for those in need during this time of rebuilding.”

Keller Williams quickly initiated its KW Cares team to coordinate aid for any of its agents affected in the region. KW Cares, the brokerage’s philanthropic arm, distributed nearly 500 generators to the Greenville, S.C., area and parts of Florida; millions lost power from the storm. KW has also distributed 32 emergency grants so far to help its associates who needed to evacuate or replace lost items from the storm.

“Hurricane Helene caused significant devastation, particularly in Asheville, N.C., the surrounding towns and parts of Florida’s coastline,” said Alexia Rodriguez, CEO of KW Cares. “The road to recovery will be long.”

The property damage caused by the storm nationwide is estimated at $15 billion to $26 billion, and an additional $5 billion to $8 billion in lost economic output, according to Moody’s Analytics.

How REALTORS® Can Help

Real estate professionals can play a crucial role in providing community support and helping in recovery efforts, Gia Arvin, Florida Realtors® president, said in a statement. “Rebuilding after a storm like Hurricane Helene really comes down to recovery and resilience,” Arvin said. “It’s not just about getting back to how things were; it’s about coming together as a community to ensure everyone’s safety and create a positive path forward.”

The Realtors® Relief Foundation is raising funds to provide housing-related assistance to Hurricane Helene disaster victims. Here are three ways real estate professionals can donate to RRF:

Text “HeleneRelief24” to 71777.

Visit RRF.realtor and click “Donate.”

Mail a check payable to REALTORS® Relief Foundation, 430 N. Michigan Avenue, Chicago, IL 60611 (Include “RRF Contribution” in the memo).

Since its inception in 2001, the RRF has distributed more than $48 million in disaster relief to more than 24,000 families. That includes a record $8.3 million in 2023 alone. The National Association of Realtors® collaborates with state and local Realtor® associations to cover all of RRF’s administrative costs so that 100% of donations collected go directly to supporting families impacted by disasters.

Hurricane Helene

Real Estate Agent Flies on Rescue Missions to Help Helene Victims

By Melissa Dittmann Tracey

Cristina Grossu Biffle received more than 1,500 panicked messages on her personal email and social media shortly after Hurricane Helene struck her home state of North Carolina. Grossu Biffle, GRI, SRS, a real estate professional with Realty ONE Group Select in Mooresville, N.C., and her brokerage were located about two hours outside of the storm’s impact zone, but the frantic messages coming in pleaded for help to check on loved ones or vacationers who rented Airbnb properties in remote mountain areas.

One from a frantic client read: “We haven’t heard from Brad! Can you check on Brad and make sure he’s OK?”

Floodwater from Helene had washed away roads, homes and businesses, knocking out power and electricity for hundreds of thousands of residents. So, after responding to several calls for help, Grossu Biffle and her husband, Greg, a NASCAR driver and pilot, hopped into the helicopter they own.

They joined others who own private helicopters to begin flying rescue missions into remote communities, often risking their own lives as they landed on steep, forested terrain and flooded-out areas that larger planes couldn’t reach. The group began flights to deliver supplies to those stranded, including food and water.

Grossu Biffle says she’s still in shock from what she saw, flying beside her husband on 10 flights. “It’s just overwhelming,” she says. Some people are walking down the road, waving at you from below, trying to get your attention. And you can see that one mile up

the road where they’re walking—there’s no road. It’s washed away. It’s a road to nowhere.”

Grossu Biffle says the devastation became too intense for her after several flights. She and her husband would land on the side of a mountain and 10 to 20 people would rush up to them, wanting to get into the helicopter. But they only had two extra seats. The Biffles would take anyone they could while checking on the well-being of others and helping to deliver supplies.

“The hardest part for me is knowing that we can’t help everybody,” Grossu Biffle says. “I’m still receiving a ton of messages. All of these people have reached out, and we can’t respond back to everyone.”

The Biffles were able to help successfully coordinate the delivery of 500 Starlink satellite internet devices, which SpaceX and Polaris delivered on pallets to their home within eight hours of making a request. The Biffles began delivering those devices last Thursday to mountainside towns. The Starlink kits allow areas with no power or electricity to use their devices to get in touch with families or friends.

Meanwhile, Grossu Biffle fears many more deaths will emerge from the devastation. Of the 227 deaths reported as of Sunday across the six states that Helene struck, more than half have been in North Carolina. Hundreds are still missing.

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine and editor of the Styled, Staged & Sold blog.

AUGUST 2024

Sales Dip as Prices Hold Steady

Home sales across Salt Lake County declined in August, while home prices remained stable. There were 1,084 total home sales in August, a 6.87% decrease from 1,164 sales in August 2023. Single-family home sales fell to 722, a 9.52% drop from 798 sales a year earlier. Multi-family home sales also decreased slightly to 336, down from 346 a year ago.

The median sales price of all homes in Salt Lake County rose to $530,000, an increase of 1.92% from $520,000 in August 2023. The median price of single-family homes edged up to $600,000, a modest 0.08% increase from $599,500 a year ago. However, multi-family home prices declined slightly to $422,700, compared to $424,000 in August 2023.

The typical Salt Lake home stayed on the market for 31 days in August, up from 21 days a year earlier. The number of homes under contract in August rose to 1,324 listings, a 1.07% increase compared to the same month last year.

Nationally, existing-home sales declined in August, according to the National Association of Realtors® (NAR). Sales fell in three of the four major U.S. regions, with the Midwest remaining unchanged. Year-over-year, sales decreased in three regions but stayed steady in the Northeast.

Total existing-home sales, which include single-family homes, townhomes, condominiums, and co-ops, dropped 2.5% from July to a seasonally adjusted annual rate of 3.86 million in August. Year-over-year, sales declined 4.2% from 4.03 million in August 2023.

“Home sales were disappointing again in August, but the recent development of lower mortgage rates coupled with increasing inventory is a powerful combination that will support sales growth in the coming months,” said NAR Chief Economist Lawrence Yun. “The home-buying process, from the initial search to closing, typically takes several months.”

Total housing inventory at the end of August stood at 1.35 million units, up 0.7% from July and 22.7% from one year ago (1.1 million). Unsold inventory is at a 4.2-month supply at the current sales pace, up from 4.1 months in July and 3.3 months in August 2023.

“The rise in inventory – and the corresponding increase in months’ supply – suggests that home buyers are in a better position to find suitable properties at more favorable prices,” Yun added. “However, in areas where supply remains limited, such as many markets in the Northeast, sellers still appear to hold the advantage.”

The median existing-home price for all housing types in August was $416,700, up 3.1% from one year ago ($404,200). All four U.S. regions posted price increases.

“The recent development of lower mortgage rates coupled with increasing inventory is a powerful combination that will provide the environment for sales to move higher in future months.”

Lawrence Yun

Chief Economist National Association of Realtors®

Salt Lake County

Pamela Abbott

Barton Allan

Judy Allen

Suzanne Allred

George Anastasopoulos

Brent Anderson

Clay Anderson

Diane Anderson

Kay Ashton

Sue Avalos

Margaret Averett

Laurence Bailess

Les Bailey

Brent Barnum

Veda Barrie-Weatherbee

Edward Belka

Ken Bell

Raymond Bennett

Richard C. Bennion

Steven Benton

Michael Black

Gregg Bohling

Russell Booth

Virginia Bostrum

Robert Bowles

Mary Ann Brady

Janet Brennan

Steve Brown

Stephen Bryant

Barbara Burt

Hedy Calabrese

Gregory Call

Tracey Cannon

Julie Carli

Carol Cetraro

Scott Chapman

Garn Christensen

Brian De Haan

Babs De Lay

Lynn Despain

Jerard Dinkelman

Darlene Dipo

Sally Domichel

Rebecca Duberow

James Dunn

Randy Eagar

Carol Edgmon

Douglas Edmunds

Michael Evertsen

Bijan Fakjrieh

Alan Ferguson

Jack Fisher

Gale Frandsen

David Frederickson

Howard Freiss

Brent Gardner

Heidi Gardner

Paul Gardner

Linda Geer

Sheila Gelman

J. Carolyn Gezon

Larry Gray

Richard Grow

D. Brent Gudgell

Klaire Gunn

James Haines

John Hamilton

Mark Handy

Grant Harrison

Stephen Haslam

Michael Hatch

Thomas Haycock

Bill Heiner

Jeffrey Helotes

Blake Ingram

Kent Ingram

Esther Israelson

Jackson Jensen

Kevin Jensen

Ron Jenson

Jeffrey Jonas

Steve Judd

David Kenney

Kay Kenyon

Henry Kesler

Douglas Knight

Peggy Knight

Wayne Knudsen

Karl Koenig

Randall Krantz

Leah Krueger

Kathryn Kunkel

Gary Larson

Teresa Larson

Vann Larson

Michael Lawrence

Clark Layton

Shauna Leake

Kaye LeCheminant

Daniel Lindberg

Michael Lindsay

Martin Lingwall

Mildred Llewelyn

Don Louie

Ted Makris

Margaret Malherbe

Al Mansell

David Mansell

Dennis Marchant

Susan Mark-Lunde

Paul Markosian

Margene Wrigley

Henry Youngstrom

Elizabeth Memmott

Uwe Michel

Gordon Milar

Kyle Miller

Preston Miller

David Moench

Richard Moffat

Gary Monk

H.Craig Moody

Randal Moore

Thomas Morgan

Thomas Mulock

Charles Mulford

Melanie Mumford

Jacqueline Nicholl

John Nielson

Michael Nielson

Robyn Nielson

Van Nielson

Victor Oishi

Joseph Olschewski

Brent Parsons

Joan Pate

Yvonne Pauls

Derk Pehrson

Douglas Pell

Robert Plumb

Noel Quinton

Helen Rappaport

David Read

Jerry Reed

George Richards

W. Kalmar Robbins

Stan Rock

Emilie Rogan

Elizabeth Smith

Kenneth Smith

Rick Smith

Skip Smith

Jeffrey Snelling

Lorenzo Spencer

Kenneth Sperling

Anna Grace Sperry

Robert Spicer

Trudi Stark

Lee Stern

Sandra Straley

Gary Strang

John Strasser

Kevin Strong

Thomas Swallow

Sonny Tangaro

Joan Taylor

Rosanne Terry

Martin Vander Veur

Craig Vierig

Peter Vietti

Hilea Walker

H. Blaine Walker

Richar dWalter

Dana Walton

Sally Ware

Jerry Webber

William Wegener

David Weissman

Jeffrey Wells

Wayne Whetman

Jeff White

Darlene Whitney-Morgan

Clayton Wilkinson

Thomas Wilkinson

Kimball Willey

Byron Christiansen

David Clark

Deborah Clark

Terry Cononelos

Jeffery Cook

Philip Craig

Dan Davis

Robert Davis

Marvin Hendrickson

Terry Hill-Black

Lynda Hobson

Ted Holmberg

Sheryl Holmes

Rhys Horman

Carol Howell

Gary Huntsman

Ronnald Marshall

Susie Martindale

Christopher McCandless

Curtis McDougal

Miriam McFadden

John McGee

Russell McKague

Andrew McNeil

John Romney

Marie Rosol

Christopher Ross

David Sampson

Mark Schneggenburger

Gary Shiner

Jeff Sidwell

Debra Sjoblom

Douglass Winder

Robert Wiskirchen

James Witherspoon

Linda Wolcott

Cynthia Wood

Sherrill Wood

NATIONAL BUILDER - LOCAL

THE LUKE’S

Kestyn Design Coordinator

HOMETOWN:

Herriman, Utah

WHAT DO YOU LOVE MOST ABOUT D.R. HORTON?

(Shantell) “The commitment the employees here at D.R. Horton have made to each other and to our communities, makes a real difference. This commitment includes a hard-working yet fun work environment. We have amazing home designs, top-notch overall community designs, and our construction team is fully dedicated to building quality homes. It brings me great satisfaction to design homes, see them being built, and then see our homeowners moving in and enjoying their new homes in an awesome, newly-built community.”

(Kestyn) “The diverse housing options here at D.R. Horton help everyone to find a place to call home. We want everyone to enjoy our homes and communities. Here, we work hard supporting and learning from each other. We take pride in each homeowner’s experience and satisfaction with their D.R. Horton home.”

Shantell (pictured right) is the Architectural/CAD Manager at D.R. Horton, Utah Division, and is excited and proud to have a family member (Kestyn, pictured left) working alongside her at a company where family is first

D.R. Horton, America’s largest homebuilder, is celebrating a milestone! 45 years in business, and an astonishing 1,000,000+ homes built! D.R. Horton is also Utah's premier builder of amenity-driven communities and spacious floor plans designed for living!