Investing responsibly is essential for those looking to align their values with their financial goals. We take a look at the growth of this class.

Pg 12-15

With new legislation in the pipeline, it’s essential that FAs stay up to date with the latest happenings in the funeral insurance industry.

Pg 16-18

EDUCATIONAL POLICIES

The rising cost of education means that saving for a child’s future should be a part of everyone’s financial portfolio. We look at an innovative product that offers this and more.

Pg 20-21

OFFSHORE INVESTING

From loop and Shariah investing to trusts and foreign pensions, the latest trends in offshore investing are worth investigating.

Pg 22-25

Investing takeaways from 2024

It’s been a challenging, surprising, unpredictable year. Are there things investors could have done differently? MoneyMarketing asked three industry experts about their experiences in 2024.

Mike Adsetts, Global Chief Investment Officer at Momentum Multi-Managers

The biggest takeaway from 2024 is reflecting on the significant challenges the year brought. Many of these risks were somewhat anticipated as early as the beginning of the year, but while they were identified, no-one knew how they would transpire. The discussion initially focused on whether a recession was looming for the US economy. However, as the months passed, the narrative began to shift toward the possibility of achieving a ‘soft landing’. This led to debates and differing viewpoints, with the central question being whether there were sufficient economic indicators pointing to a feasible soft landing.

Inflation was another critical issue, continuing to run at elevated levels, causing concern across markets. The initial outlook for 2024 included the expectation that interest rates in developed markets might ease. However, the pace and timing of such rate cuts were still uncertain, with central banks being cautious.

The anticipation and response to these evolving conditions highlighted the delicate balancing act central banks faced throughout 2024.

The two elections – South African and US – were always going to be key economic indicators. We were hesitant about the impact of local elections on the markets. It created a difficult situation because South African assets were undervalued but if the results of the election were unfavourable, the risk was that yields would spike up, the rand would weaken, and local equity markets would continue to be under pressure. We positioned our portfolios to be a bit underweighted in South African assets because we were concerned about the outcome of the local election, but it was a little bit moderated. Where we did have an underweight, it wasn't a big underweight. We were cautious. After the elections, the markets rallied quite strongly as the outcome was better than any of us had anticipated. The US election also brought some surprises. While the presidential race was always too close to call, no one predicted the total red wave that emerged. Trump is known as being an unpredictable president, and will probably be a very unpredictable president this time around, looking at the appointments he's made to date. There's also a view by some in the US that Trump will be more interventionist in the Federal Reserve, but that remains to be seen.

We don't foresee the dollar losing its status as the global reserve currency. There's no real potential replacement for the US dollar as a reserve currency in the near, medium and even a couple of decades into the future. We will, however, probably start seeing deglobalisation to a point that it’s replaced by regionalisation. As America becomes more protectionist, other contenders see an opportunity for themselves to stake a place in the world.

UP-TO-DATE INDUSTRY NEWS

Stay ahead of the curve with the latest industry news & insights, or have it delivered to your inbox to read later.

Read digital issues from all our B2B titles on your PC, smart phone or tablet. PDF downloads also available.

Remove geographical barriers and expand on your expertise with knowledge-sharing webinars across a variety of topics.

Continued from previous page

Another thing that surprised us in 2024 was the strong performance of listed property locally. It had a strong run up until the end of last year, so our view was that it was starting to get overvalued. However, it continued to rally over the year, being the best-performing sector by far.

The biggest challenge this year was dealing with a constantly changing macro environment. It’s not just a 2024 issue; it's been ongoing since Covid. This makes predicting market behaviour extremely tough. It reinforced for us that investment strategies based purely on predictions can lead to high anxiety and random outcomes. So, we focus more on maintaining a long-term perspective rather than reacting to short-term changes.

History shows us that unpredictable events happen. This reinforces the importance of a long-term mindset. Trying to chase trends or react to immediate concerns can lead to poor decisions. We avoid being reactive to the uncertainty, staying anchored to our investment philosophy, which focuses on long-term outcomes rather than trying to predict random events.

There have been positive impacts from the recent political changes in South Africa, which is a relief. However, we remain cautious because the GNU is still new and not very robust. We need to factor in that this political arrangement might not be stable long-term, so we keep this in mind while constructing portfolios.

We were more cautious this year because of global uncertainties. There's always pressure on asset managers to outperform, but taking big, speculative bets can be risky in such unpredictable times. It’s important to have a clear, long-term strategy and not rely solely on predicting uncertain outcomes.

The market reaction to the US election has been positive, especially for US stocks, and we have a healthy exposure to them.

“Trying to chase trends or react to immediate concerns can lead to poor decisions”

“Building strong client relationships and maintaining open lines of communication were vital”

However, small-cap stocks have seen the most significant gains, and we haven't heavily invested in that sector. It's still early, and predicting the full impact of this election on the market is difficult. We prefer to remain cautious and focus on the long-term view.

Geopolitical issues are hard to predict. Our approach is to focus on building resilient, globally diversified portfolios that can withstand different scenarios. It’s about ensuring our investments are robust enough to handle unexpected shocks.

The market has become more reactive, especially with the rise of AI and algorithmic trading. The average holding period for US stocks is now less than six months, indicating a shift towards short-termism. We invest in highquality, resilient companies and hold them long-term to avoid short-term volatility.

In 2025, with ongoing geopolitical tensions and economic uncertainties, our strategy remains focused on tuning out the noise, maintaining a long-term view, and constructing robust portfolios.

Hildegard Wilson, Head of Investment Solutions at Glacier by Sanlam

One of the most significant challenges in 2024 was the rapid shift in product mix, moving from protected or guaranteed products to marketlinked options, along with a strong trend towards offshore allocations. This transformation necessitated a keen eye on tracking trends to remain competitive and relevant. In addition, the myriad of global elections posed a unique challenge in managing client expectations. Building strong client relationships and maintaining open lines of communication were vital in addressing the uncertainties of the year.

A key strategy that proved successful was offering a diverse range of products tailored to meet the varied needs of clients. This approach enhanced client satisfaction by aligning investment products with specific client objectives.

One of our focuses was on ensuring clients fully understand portfolio and investment strategies, and the importance of clear communication and education when introducing new investment concepts was evident.

Global economic and geopolitical events significantly influenced investment decisions and portfolio management in 2024. To address the potential outcomes of these events, having a diversified portfolio became crucial. This strategy ensured that portfolios could withstand various economic and political scenarios, providing resilience and adaptability in an unpredictable world.

As we wrap up an unpredictable year, MoneyMarketing spoke with three investment experts about their experiences in 2025. From our unexpected local election results leading to the formation of a GNU, to a pivotal US election and ongoing conflicts in the Middle East and Ukraine, it’s been a challenging time for investors. ‘Long-term’ and ‘diversify’ remain the guiding principles. While we hope for stability in 2025, the outlook suggests more uncertainty ahead.

As I write this, COP29 is off to a rocky start, with host Azerbaijan’s fossil-fuelbased economy causing controversy and Trump’s re-election threatening another US exit from the Paris Agreement. But how are we doing on ESG commitments closer to home? In South Africa, there’s a noticeable uptick as companies are increasingly focused on ESG, and investors are recognising its benefits. If ESG isn’t on your radar yet, now might be the time to start paying attention.

We’re also looking at education policies in this issue, and why a new way of thinking about them is in order. There’s also some insight into the latest updates on regulations around funeral policies, and how this could affect FAs.

It’s been a busy, eventful 2024, and we hope you can all take a break and have a peaceful and happy holiday season. May we all emerge in 2025 ready for whatever rollercoaster rides the markets have in store for us. Stay financially savvy,

Sandy Welch Editor, MoneyMarketing

Mohamed Mayet CEO, Sentio Capital Management

How did you get involved in financial services?

Fortunately, I found myself in financial services quite early in my career. It wasn’t exactly the result of some grand masterplan; rather, it was a mix of luck and serendipity. From my teenage years, I knew I wanted to be in finance, though I wasn’t entirely sure what that entailed. I was captivated by numbers and business dynamics, and finance seemed the perfect path to combine both passions.

As a student, I would eagerly dive into case studies on institutions like Goldman Sachs and Berkshire Hathaway, dreaming of one day doing similar work. It felt like a far-off aspiration for a young man from inner Johannesburg, with the odds seemingly stacked against me. Still, I was determined. My goal was to work in an investment bank, and eventually, I secured a position in a division of RMB Bank and was part of the early journey of OUTsurance. I contributed to several successful financial start-ups along the way, but my true passion was always in the markets.

This passion led me to work as a sell-side investment analyst, covering the consumer and industrial sectors for a European investment house.

Later, I became Head of Research at Merrill Lynch, focusing on the consumer and global luxury goods sectors. Seventeen years ago, I co-founded Sentio with my business partner and co-principal, Rayhaan Joosub. Reflecting on the journey, it’s clear that financial services have always been my calling – something that has evolved in different forms over time, and I’m grateful for the path it’s taken me on.

What was your first investment –and do you still have it?

My first listed investment took place during the tech bubble of the early 2000s, and, unfortunately, I lost my entire capital. I had put money into a selection of financial and

tech stocks, guided by a rather naïve approach, which quickly taught me some valuable lessons. To make matters worse, I had also convinced my newly inherited father-in-law to co-invest with me. It was a humbling experience that underscored the importance of thorough analysis and research. I certainly don’t hold onto those investments anymore, but I carry the lessons –and a few scars – from that experience.

What have been your best – and worst –financial moments?

That’s a tough question. Plenty of challenging moments come to mind, something inevitable when you’ve been in the industry for a while. Among the best, I recall my early days as an analyst covering the retail sector. I issued a welltimed sell recommendation on Edgars, followed by a buy at the right moment. It felt like a high

significant blind spots. The market has a way of humbling everyone – not ‘if’ but ‘when’. Embracing humility helps you recognise your limitations and opens up an abundance of opportunities.

The second lesson, closely related to humility, is that you’re only as good as your last result. No matter how clever you believe your ideas are, the scoreboard is the ultimate judge. At Sentio, humility is embedded in our culture, guiding our processes and approach to investing. It’s worth noting that true humility can’t be faked; it has to be authentic and part of your ‘investment soul’.

What makes a good investment in today’s economic environment?

In a world dominated by high-frequency data – often just noise – and resulting market volatility, the notion of a ‘good investment’ can easily be mistaken for speculation or chasing high-risk, high-reward ideas. The danger here is becoming a slave to sentiment, which can be a slippery slope.

“It’s clear that financial services have always been my calling – something that has evolved in different forms over time”

point in my career; I thought I was at the top of my game. More recently, my proudest moments have been with the Sentio team, where we successfully navigated around stock ‘bombs’ like Steinhoff, African Bank, EOH and Lonmin. It was a powerful reminder of how a few poor stock choices can quickly undo years of gains.

As for the low points, they’ve often been tied to investing in small caps, especially when liquidity dried up in 2016, and being too early in certain resource stocks that seemed undervalued a couple of years ago.

What are some of the biggest lessons you have learnt in and about the finance industry?

My most valuable lesson is that humility is a competitive advantage in this industry. It’s easy to feel like a superstar investor, but that mindset can lead to

In this environment, successful investing requires a focus on process rather than outcome. A process-driven approach is probability-adjusted, while an outcomefocused one tends to be backward-looking and difficult to replicate. At Sentio, our philosophy is clear: we rely on scientific analysis, not forecasts, to identify the best ways to compound long-term returns. This means seeking out stocks and thematic sectors with resilience against market sentiment, aiming for higher probability returns over time rather than simply chasing what’s currently trending.

What finance/investment trends and macroeconomic realities are currently on your watchlist?

Globally, three significant trends demand our focus:

• An evolving multi-polar and confrontational world is altering geopolitical dynamics and affecting global markets.

Data is emerging as the new oil, generating economic value and transforming various industries.

• A rising disillusionment among young individuals in developed markets reveals their economic disadvantages relative to past generations.

By Prelisha Singh Partner,

The NHI Act: A flawed execution of a laudable idea

Robust contestation on how to best fulfil the fundamental rights of South Africans complements and strengthens our constitutional democracy. Recent debate has centred on the effective realisation of the right to access healthcare, which the state is required progressively to realise for all South Africans, irrespective of their background and income.

Accessing healthcare and the NHI Act

The right to access healthcare came into sharp focus on 15 May 2024, when President Cyril Ramaphosa signed the National Health Insurance (NHI) Act into law, prompting the initiation of constitutional challenges by concerned stakeholders. The most recent of these was filed on 1 October 2024 in the North Gauteng High Court, Pretoria, by the South African Private Practitioners Forum (SAPPF), represented by Webber Wentzel. According to the government, the NHI Act is intended to generate efficiency, affordability and quality for the benefit of South Africa’s healthcare sector.

An assessment of South Africa’s current healthcare landscape shows a stark difference between private and public healthcare. The country has a high-quality, effective private healthcare offering. However, it is currently inaccessible to the many South Africans who cannot afford private care or medical aid payments. Public healthcare, on the other hand, is understaffed, poorly managed, and plagued by maladministration and limited facilities.

A vehicle for universal healthcare?

The NHI Act has been positioned as the vehicle to address this disparity and to realise a desire to take steps towards achieving universal healthcare in South Africa. But a closer reading of the Act highlights numerous problems with its content and implementation design. The absence of clarity, detail or guidance contained in the Act makes it impossible to assess how the Act will actually be implemented (or, by extension, what the effects of this implementation will be).

This is particularly concerning given that years have passed since the economic assessments, on which the Act was based, were undertaken. Also problematic is the apparent lack of consideration given by the government to submissions made by affected stakeholders during multiple rounds of constitutionally required public participation. SAPPF underscores these deficits in seeking both to have the President’s decision to assent to the Act reviewed and set aside, and the Act itself declared unconstitutional.

Presidential obligations and Constitutional requirements

President Ramaphosa was obliged, in terms of sections 79 and 84(2)(a) to (c) of the Constitution, not to assent to the Act in its current form. Section 79 requires the President to refer to Parliament any bill that he or she believes may lack constitutionality. In this case, it is difficult to conceive how the President, or any reasonable person in the President’s position, could not have had doubts regarding the constitutionality of the NHI Bill. The decision by the President to sign unconstitutional legislation into law, instead of referring it back to Parliament for correction, is also irrational.

The President’s duty properly to have referred the NHI Bill back to Parliament is affirmed by the fact that the President is enjoined, by section 7(2) of the Constitution, to respect, protect, promote and fulfil the rights contained in the Bill of Rights.

SAPPF’s application demonstrates that the NHI Act, in its current form, infringes upon the rights to access healthcare services, to practice a trade, and to own property. Patients, including those using private healthcare, will be forced to use a public healthcare system that currently fails to meet its key constituents’ needs. Practitioners’ rights to freedom of trade and profession will be infringed upon, and the property rights of medical schemes, practitioners, and financial providers will be unjustifiably limited.

On its current text, the Act could make South Africa the only open and democratic jurisdiction worldwide to impose a national health system that excludes by legislation private healthcare cover for those services offered by the state –notwithstanding the level or quality of case.

Potential exclusion of private healthcare

Concerns regarding the rights infringements in the NHI Act are exacerbated by its lack of clarity and the fact that crucial aspects of its implementation are relegated to regulations, with no clear guidance provided in the Act itself.

For example, section 49 provides that the NHI will be funded by money appropriated by Parliament, from the general tax revenue,

payroll tax, and surcharge to personal tax. However, this stance does not reconcile with section 2, which provides that the NHI will be funded through ‘mandatory prepayment’, a compulsory payment for health services in accordance with income level. Crucially, the extent of the benefits covered by the NHI’s funding mechanism and its rate of reimbursement, which impact affordability and the provision of quality healthcare, remain unknown.

The Act is, at best, a skeleton framework, seemingly assented to in haste. It is conceptually vague to the extent that the rights it seeks to promote will, in fact, be infringed if implemented. This renders the Act irrational, in addition to its other constitutional defects.

The need for meaningful public participation

The NHI Act represents a radical shift of unprecedented magnitude in the South African healthcare landscape. This should be – and is required to be – underpinned by meaningful public participation, up-to-date socio-economic impact assessments and affordability analyses, and final provisions that provide a clear and workable framework for implementation.

It is not sufficient for these vital issues to be addressed after the fact. Further engagements with stakeholders and the solicitation of proposals by the government cannot be used to splint broken laws. Collaborative engagement, including the solicitation of inputs for meaningful consideration, should take place during the lawmaking process, not after its conclusion.

A shift of the magnitude proposed by the Act – absent compliance with the structures of the law-making process and adherence by the state to constitutional standards, including rights protections – would be detrimental to the entire healthcare sector, public and private, and not in the best interests of patients and practitioners.

Notwithstanding the legal contestation surrounding the Act, it and the laudable goals underlying it can also be a watershed. The achievement of universal health coverage is an opportunity for the different stakeholders in South Africa’s healthcare system to meaningfully collaborate and inform well-supported, factually informed, rational and genuinely progressive legislative steps by the state.

Given the questions surrounding the Act and the evident needs it seeks to address, the space exists for healthcare stakeholders to align around shared goals and values. They can leverage their available resources to design a healthcare system that serves all of South Africa’s people fairly and equitably, using the significant existing resources invested in the country’s healthcare sector.

Martin Versfeld Partner, and

Alexandra Rees

Senior Associate, Webber Wentzel

Angela Ngcemu, CFA Business Development Associate, Laurium Capital

It’s never too late to hedge your investments

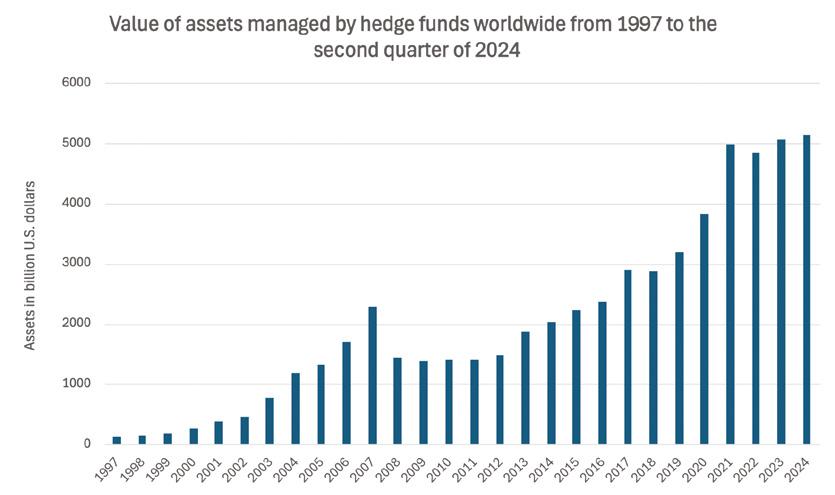

The hedge fund industry has grown rapidly globally, with more than $5tn invested in hedge funds (see Figure 1 below), while in South Africa, the hedge fund industry’s assets have lagged, with assets under management (AUM) standing at R138bn in 2023. Retail funds comprise 32% of this figure, while the rest comprises institutional investors. According to Markov Processes International, the top 10 Ivy League endowments had an average of 22% allocation to hedge funds in 2023, indicating the strategic value these institutions place on hedge funds. With this knowledge, one would wonder why local investors have lagged in allocating to hedge in diversified portfolios.

Source: Statista 2024

In South Africa, hedge funds began to gain traction in 1995. By 2003, the industry had grown to R2,3bn and to R26bn in 2007. Historically, hedge funds were primarily available to high-net-worth individuals and institutional investors until the introduction of new regulations in 2015. These regulations brought hedge funds under the Collective

Investment Schemes Control Act (CISCA), finally allowing retail investors to access these funds. In South Africa, hedge funds are overseen by the Financial Sector Conduct Authority (FSCA), who believe their role is to regulate and supervise hedge fund managers with the following aims –

(a) to provide for the protection of investors in hedge funds;

(b) to assist in the monitoring and management of systemic risk;

(c) to promote the integrity of the hedge fund industry;

(d) to enhance transparency in the hedge fund industry and

(e) to promote financial market development.

South African hedge funds are some of the most highly regulated funds in the world. Retail Hedge Funds (RIHFs) are limited to a maximum gross exposure (leverage) of 200%. In contrast, hedge funds in the United States are regulated under the Dodd-Frank Act, which focuses more on transparency and reporting rather than on limiting strategies or exposure. The hedge fund industry dates back to 1949 when Alfred Winslow Jones pioneered the concept by using short selling and leverage to protect his portfolio in declining markets. Over time, hedge funds became perceived as complicated and are often misunderstood. The intense regulatory nature of local hedge funds has also acted as a double-edged sword, bringing relief but also inducing anxiety in investors, with these stringent regulations being seen as a signal of danger. It is time to demystify this misconception.

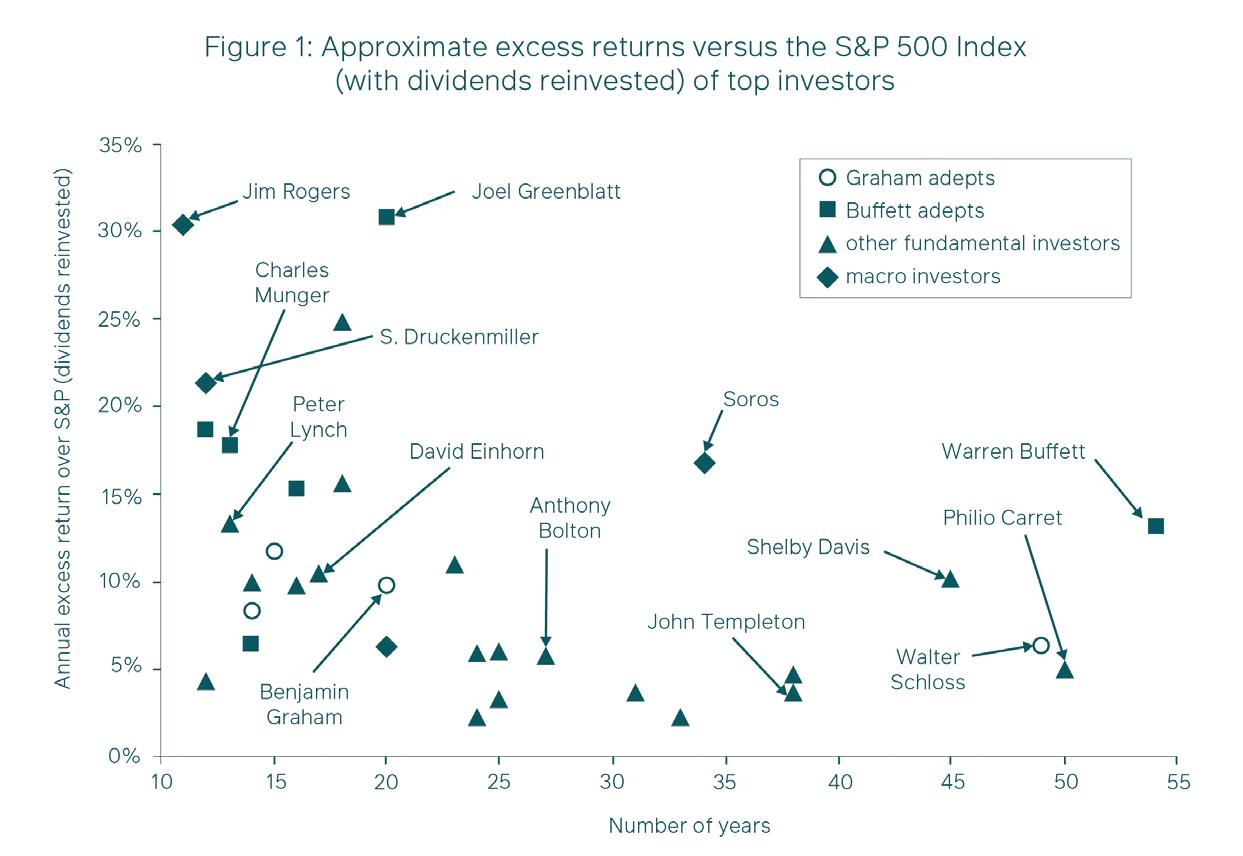

Following is a risk-return scatter plot that shows that hedge funds’ superior returns do not necessarily come at the expense of additional risk to the investor. Since hedge funds have a broader toolset, they can tailor their return and risk profiles to suit their investors’ needs.

EARN YOUR CPD POINTS

The FPI recognises the quality of the content of MoneyMarketing’s December 2024 issue and would like to reward its professional members with 2 verifiable CPD points/hours for reading the publication and gaining knowledge on relevant topics. For more information, visit our website at www.moneymarketing.co.za

For both institutional and retail South African investors, hedge funds present a compelling value proposition to diversify portfolios, preserve capital, and achieve superior risk-adjusted returns in a highly regulated environment that protects investors. The outdated perceptions that hedge funds are risky or opaque do not reflect the reality of their benefits in South Africa. As the industry continues to grow, understanding the role of hedge funds can lead to more informed, confident investment decisions.

Local investors have an opportunity to piggyback on the risk-reward research already conducted by global investors and prestigious institutions that focus strongly on sustainable growth and capital preservation and see hedge funds as an essential asset class in their portfolios.

To find out more about Laurium’s hedge fund offering, please visit our website and contact our team: www.lauriumcapital.com

Figure 1: Global Hedge Fund Assets in Billion US Dollars

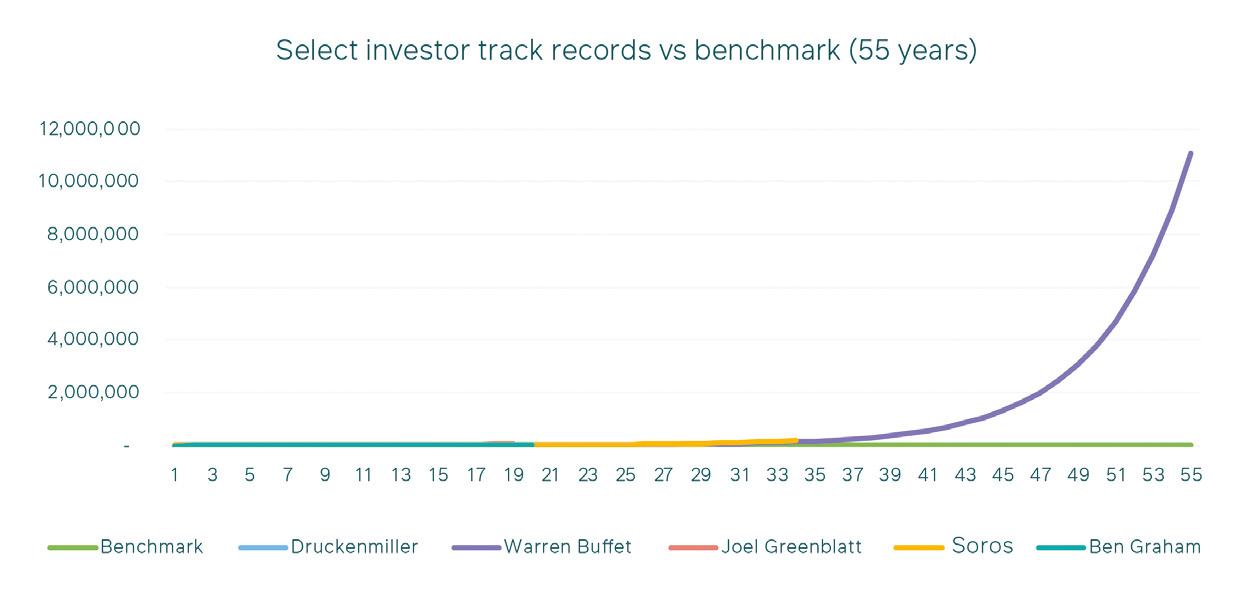

Figure 2: Laurium Hedge Fund Net Returns in Perspective vs. Market Indices – 1 January 2013 to 31 October 2024

Source: Morningstar Direct (31 October 2024)

CIS tax up for discussion

Adiscussion document has been released by National Treasury in terms of Collective Investment Schemes (CIS). It’s been welcomed by the Association for Savings and Investment South Africa (ASISA). Dr Stephen Smith, consulting senior policy adviser at ASISA, explains the document invites responses from the public, advisory firms and the CIS industry primarily on how a simplification rule might be designed to distinguish between income

versus capital gains when portfolio assets are bought and sold.

The discussion document stems from a commitment by National Treasury in 2020 to review the income tax treatment of amounts received by portfolios of collective investment schemes.

The changes up for discussion primarily address whether income tax or capital gains tax should apply when selling investments in these funds. To explain it simply, income tax (at an investor’s marginal tax rate) applies to shares bought and sold for a profit. However, if the investor can prove that the shares were held as a long-term asset, capital gains tax, which is typically lower, is applied instead.

Currently, interest income exceeding R23 800 (for those under 65) from unit trusts is taxed at the investor’s marginal rate. Additionally, a 20% dividend withholding tax is imposed on dividends paid out from a unit trust (although unit trusts within tax-free savings accounts are exempt from these taxes).

“The document offers several proposals for discussion aimed at implementing a new

New appointments

Sanlam’s new Group Executive

Sanlam has appointed Shadi Chauke as Group Executive: Market Development and Sustainability (MDS). Chauke’s role will support Sanlam’s ongoing commitment to driving sustainable growth, social impact and transformation.

Chauke, a Chartered Accountant, brings over 20 years of finance, creative and social impact experience. Her background includes serving as an Audit Partner at Deloitte & Touche South Africa, as well as holding NonExecutive Director roles on boards across the financial services, insurance, healthcare, retail and microfinance sectors. She is also the founder of Vahluri Advisory Services, a social impact advisory firm. Chauke was also a freelance actress, television and film producer. Chauke will lead Sanlam’s efforts across stakeholder relations, market development, communications, brand and reputation management, corporate social responsibility, sustainability and transformation.

Amplify Investment Partners appoints Head

Wade Witbooi has been appointed as Head of Amplify Investment Partners, effective 1 January 2025. Witbooi will take responsibility for setting and executing the strategy for the business, driving growth and ensuring alignment with overall business objectives. He was previously a Senior Portfolio Manager at Sanlam Investments Multi-Manager.

Witbooi has close to 15 years of industry experience and was previously an investment analyst within the research team at Glacier by Sanlam from 2012 to 2014. He joined Sanlam Investments in 2014 as an investment

analyst within the Retail Strategy and Client Solutions team. Two years later he joined the multi-manager team as a portfolio manager, and during this time he also managed portfolios for the Glacier Invest Discretionary Fund Manager (DFM) business.

New Chief Executive Officer for M&G Investments Southern Africa

Over recent months, M&G Investments Southern Africa has been working purposefully on reinvigorating its strategy. In line with this, the company has appointed Ann Leepile as Chief Executive Officer, with effect from 3 February 2025. Leepile has over 22 years of experience in the investment industry, most recently serving as CEO of AlexForbes Investments. Prior to this, she spent six years as CEO of Absa Asset Management. With a strong track record in portfolio management, global manager research, and responsible investing, Leepile is well positioned to guide M&G Investments Southern Africa into its next phase of growth.

Osmotic Engineering Group strengthens management team

tax regime for CIS portfolios and achieving tax certainty. This does not mean there will be a new tax liability for the millions of South Africans who save through CIS portfolios.”

“This does not mean there will be a new tax liability for the millions of South Africans who save through CIS portfolios”

Smith explains that the CIS industry is strictly regulated, and the investment powers of portfolio managers are stipulated in regulation.

“It is therefore somewhat anomalous that explicit tax certainty should not be afforded these portfolios in law. The National Treasury discussion document offers several optional proxies to achieve this end. ASISA is appreciative of the fact that the document acknowledges that there may be more than one way of improving income definition.”

resilience in Africa, ensuring access to clean, safe water.

Rajnandan highlights the importance of sustainable infrastructure investment:

Sustainable water, energy, telecom, built environment and asset management company

Osmotic Engineering Group (OEG) has announced significant management changes and business expansion. The leadership team has been bolstered by the addition of Lynesha Pillai, a water resource engineer, and Nichal Rajnandan, a specialist in asset management.

Pillai focuses on addressing infrastructure planning and water security related to climate change and

“My role involves ensuring that our infrastructure projects, such as water, energy and telecom systems, etc. are designed and managed for long-term sustainability,” he says. “For our investors, asset management ensures long-term value creation, capital allocation, minimised risk, and diversification, while ensuring Environmental, Social and Governance (ESG) goals are integrated. It ultimately reduces risk and increases return on investment.”

Wade Witbooi

Nichal Rajnandan

Shadi Chauke

Anne Leepile

Lynesha Pillai

By Mike Adsetts Global Chief Investment Officer at Momentum Multi-Managers

A surprise to the upside!

This year was always going to be interesting, with the war in Ukraine grinding on and with the continuous escalation of the conflict in the Middle East –the risk of regional contagion was an everpresent danger. It was not just geopolitics that was spicing up the landscape. More than half of humanity was going to the polls during the year, with the bigticket item being the United States (US) election in November 2024. Add to that sticky inflation and the debate about whether there would be a hard or soft landing in the US: Would the US fall into recession, or not?

What was clear at the start of the year was that as investors we are no strangers to volatility, and this year has certainly delivered the ups and downs with numerous surprises.

In South Africa (SA), we were also facing our national election in May 2024. SA asset classes looked reasonably priced, but a good price does not always mean there is a stream of willing buyers, especially when factoring in uncertainty and political risk.

At the start of the year, we were relatively pro-growth and cautious about what would happen in the SA elections. But what transpired during the year?

The geopolitical conflicts seem to have largely been restrained as localised events, although there continues to be a gradual escalation in the Middle East. This hot spot of conflict has not, so far, materially impacted oil and energy prices, although the risk of escalation and more direct conflict between Israel and Iran remains a real geopolitical risk.

By Tobie van Heerden CEO 10X Investments

The US seems to have been able to engineer a soft landing and avoid a recession. At the same time, inflation slowly continued its downward trajectory, followed by interest rate cuts in major developed economies. These two factors in concert supported the markets. US markets rose to historic highs, albeit dominated by technology heavyweights. Although markets performed well, it still was difficult for active managers to outperform equity market indices.

At home, the ANC performed much worse than expected at the national ballot and we were all on tenterhooks about how this would play out.

The formation of the Government of National Unity was the best possible outcome for the country, significantly improving sentiment in and towards SA. This culminated in a strong rally after May, with SA asset classes outperforming many international asset classes. After many years in the doldrums, the outstanding performer for the year was listed property, despite headwinds in the sector. A strong valuation underpin, a reducing interest rate trajectory, and positive sentiment resulted in the sector being the standout performer locally.

Local was lekker again, which was a great outcome for all of us and we are slowly starting to see the benefits. There continues to be upside potential for SA, with ratings sentiment improving slowly and the possibility that we will be off the grey list towards the end of next year.

All things considered, 2024 has surprised to the upside, notwithstanding the substantial risks that were present at the start of the year and are still present.

As always, when you face an uncertain environment, the best course of action is to focus on the long term, make sure that your portfolio is wellmatched to your objectives, and harness the benefits of diversification. That is what we do at Momentum Investments, and I think this is sound advice on how to best prepare your investments to navigate an uncertain and dynamic world.

Exchange traded funds on the up in SA

According to data from the Association for Savings and Investment South Africa (ASISA), 10X Investments earned 27% of the overall net flows in the index-linked fund market in the last year, giving the company significant traction among specifically retail investors (either direct or via intermediaries).

Exchange Traded Funds (ETFs) are fast becoming a fundamental component of a diversified share portfolio amid 16-year high interest rates in the US and evolving market conditions. Globally, index funds and ETFs account for over a quarter of inflows, and in the US, more than half of inflows are from these products.

“Investors are increasingly turning to costeffective, transparent investment options that expose them to a range of assets,” says 10X Investments CEO Tobie van Heerden. He adds, “Just three years ago, index-driven funds made up 6% of market inflows in South Africa and now we’re at 10%, and we predict that we could reach 20% within the next five years.” According to the JSE, the market capitalisation of listed ETFs has

increased from R68bn in 2019 to R167bn in 2024, a staggering growth of 147%.

10X Investments’ total growth has garnered substantial market attention, thanks to consistently growing assets under management (AUM) and its user-friendly platform. ASISA data from the second quarter of 2024 revealed that more than 55% of the net flows into the country’s market-tracking funds had been allocated to 10X Investments and its competitor Satrix.

Long-term investment growth

10X Investment’s flows have shown consistency for every quarter since Q3 2023 – ranging between R1,5bn to R1,9bn net positive – showing a consistent growth trend. Being the incumbent index-driven ETF provider, Satrix received 28% of these flows, ranging from -R58m to R3,6bn over the same period. It is noted that all other firms lost market share, with Sygnia notably among those, only attracting just over 1% of the total market-linked flows according to ASISA figures.

10X Investments’ success highlights a shift towards digital and cost-efficient investing in South Africa, as investors increasingly prioritise convenience, transparency, and low fees. The ETF product’s design – which allows for lower management fees and broad market exposure – has positioned the company as a prominent player in South Africa’s evolving investment landscape.

“The market condition suggests that South Africa is beginning to follow global investing trends. The country is on a path towards having 20% to 25% of industry AUM held within systematic ETFs and Mutual Funds,” says van Heerden.

Global trends also indicate that the index-driven investment market is one where the leaders make the market. Having achieved consistent growth in recent quarters, 10X Investments aims to further expand its offerings, providing more options that reflect investor demand for highperforming, low-cost products – helping its clients grow their wealth through innovative investment services.

“Investors are increasingly turning to cost-effective, transparent investment options that expose them to a range of assets”

Momentum Investments is part of Momentum Metropolitan Life Limited, an authorised financial services and registered credit provider (FSP 6406).

Simple ways to use AI and data analytics to transform your business

By Warren Bonheim Managing Director of Zinia

If you’ve heard a lot of buzz about artificial intelligence (AI) and data analytics but felt like it’s only for tech experts, think again! The truth is these tools are no longer reserved for large companies or IT wizards. AI and data analytics are becoming easier to use, offering powerful ways to improve your business without requiring advanced technical skills. You don’t need to be a tech genius. From automating everyday tasks to making smarter decisions based on real-time data, AI and data analytics can have a huge impact on your company’s success.

Make better decisions

Every business gathers data, whether it’s sales numbers, customer preferences or website traffic. The challenge? Turning that raw data into something meaningful. That’s where data analytics comes in, helping you make smarter decisions based on facts, not just gut feelings.

Imagine being able to predict what your customers want before they even tell you. Data analytics tools can analyse patterns in your sales and customer behaviour, giving you insights that let your business stay ahead of trends.

"AI and data analytics are becoming easier to use, offering powerful ways to improve your business”

Tools like Google Analytics or Power BI make this process super easy, offering visual reports and dashboards that help you see what’s working – and what isn’t. You don’t need any special training; the tools do the heavy lifting for you.

Automate routine tasks with AI

One of the best things about AI is its ability to automate repetitive tasks, freeing up time for you and your team to focus on more important things. Take customer service, for example. AI chatbots can handle common questions, such as order tracking or appointment scheduling, instantly. This means your team can focus on resolving more complex issues. These chatbots are smart enough to learn from each interaction, so they get better over time, providing even better service to your customers.

Another big benefit of AI is how it can streamline your operations. From automating data entry to handling inventory management, AI tools can take care of the day-to-day tasks that often slow you down. With platforms like Zapier or Automate.io, you can easily set up these automations without needing to write a single line of code.

Personalise your customer experience

We all know how important it is to deliver a personalised experience to customers. AI makes this not only possible but easy. By analysing customer data, AI can help you tailor marketing messages, product recommendations, and promotions to fit each person’s preferences.

For example, tools like HubSpot can track customer interactions and deliver personalised content at the right time, improving engagement and sales. Whether you’re running a small business or a larger operation, this level of personalisation can help you build stronger relationships with your customers, keeping them loyal to your brand.

Save time and money

One of the greatest advantages of AI and data analytics is how much time and money they can save your business. With AI automating tasks and data analytics providing insights that help you make better decisions, you’ll reduce inefficiencies and cut unnecessary costs.

Data analytics can also show you where you can optimise costs, whether that’s reducing energy consumption or cutting down on waste. It’s like having a personal business consultant that works around the clock, analysing every aspect of your operations.

Scale as you grow

Another great thing about AI and data analytics is how they can grow with your business. Whether you’re expanding your team, opening new locations or entering new markets, these tools can easily scale up to meet your needs.

AI-powered tools are often cloud-based, meaning you can adjust them as your business changes. For example, if you’re suddenly handling more customer queries than usual, you can easily scale up your AI chatbot service to handle the influx, ensuring smooth operations without overwhelming your team.

Getting started is

easier than you think If all of this sounds great but you’re still unsure where to begin, don’t worry. Getting started with AI and data analytics is easier than ever. Most platforms come with easyto-use interfaces, and many offer free trials or demos, so you can explore them before fully committing.

Start by identifying one or two areas in your business where you could use some extra help. Maybe you want to improve your customer service, or maybe you’re looking to make more informed decisions based on data. Once you’ve identified the areas to focus on, explore platforms that align with your needs. Tools like Google Analytics, Power BI, and HubSpot are popular choices that don’t require a technical background.

AI and data analytics aren’t just for techsavvy people. These tools have become user-friendly and accessible to businesses of all sizes, providing practical ways to improve efficiency, make smarter decisions, and deliver a better customer experience.

By Francois du Toit CFP® PROpulsion

WBuilding trust, enhancing experiences and growing communities

e’re constantly juggling a range of challenges in today’s environment – from adapting to virtual meetings to balancing marketing and prospecting. Let’s look at some practical solutions to common issues that can raise the bar for your practice, improve client experiences and create lasting value.

Your virtual meeting setup

Virtual meetings are here to stay, but unfortunately, many professionals still rely on the basic built-in cameras and microphones of their laptops. For large businesses, this is a missed opportunity to represent their brand with professionalism and polish. As independent advisers, investing in a quality setup doesn’t have to break the bank – excellent webcams, microphones and lighting solutions can all be achieved within a budget of around R5 000 to R 10 000. Consider the client’s perspective: clear video, crisp audio and a well-organised background immediately improve their experience. In a world where people expect quality in everything they see and hear online, a good virtual setup can set you apart, showing clients that you take every interaction seriously.

“It’s essential to go beyond credentials and educate clients on what our role entails and how we can help them”

The power of titles: clarifying your role The financial planning profession has a fascinating mix of titles – financial adviser, financial planner, wealth manager, broker and more. But do clients actually understand the differences between them? Titles matter because they shape client perception and trust.

As an industry, we may know what differentiates a financial planner from a broker, yet clients often do not. And while designations like CERTIFIED FINANCIAL PLANNER® / CFP® are valuable, it’s essential to go beyond credentials and educate clients on what our role entails and how we can help them. This clarity not only strengthens trust but also empowers clients to choose the professional who best fits their needs.

Marketing vs prospecting

Marketing and prospecting are two distinct approaches, each essential to building a sustainable practice. Marketing is a long-term game; it’s about building brand awareness and credibility. This includes producing content, hosting webinars or even speaking at events – all designed to keep your name top of mind with your target audience. On the other hand, prospecting is a more immediate, hands-on approach. It involves identifying specific clients, reaching out, and creating opportunities for engagement. Where marketing might attract potential clients over time, prospecting is what keeps your revenue flowing in the short term.

Supporting the next generation of advisers

Bringing fresh talent into financial advice and planning isn’t just about hiring; it’s about nurturing, mentoring and sharing our hard-earned knowledge. It’s disheartening to see new advisers and planners drop out early in their careers. Many complete all their qualifications only to find the practical reality daunting, often due to a lack of support and mentorship.

If you’re considering hiring for succession or expanding your team, consider providing clients to newer advisers or involving them in client interactions gradually. Support them with regular feedback and training, helping them build confidence. Taking an active role in their development can lead to a more motivated, loyal team and ultimately ensure the longterm success of your practice.

Turning clients into community

A ground-breaking way to think about client relationships is to see them as part of a community rather than a collection of individuals. Community brings people together, creating connections among clients who share common values and goals. By building a sense of community within your practice, you can offer clients more than just advice – you provide a platform for them to connect, share insights and even collaborate.

One approach is to host client events, workshops, or webinars that allow clients to interact. This strengthens client loyalty and enriches their overall experience. In the long run, clients who feel part of a community are more likely to remain with you, trust your advice, and recommend your services to others.

Small changes make a big difference

As financial advisers and planners, we are in a unique position to shape not just financial outcomes but also our clients’ experiences and perceptions. Small changes, like upgrading your virtual setup or clarifying your role, can significantly impact client satisfaction and trust. Meanwhile, balancing marketing and prospecting, supporting new talent, and fostering community can all contribute to building a practice that’s resilient, engaging, and ready for the future.

Embrace these practical steps, and you’ll be well on your way to creating a practice that clients value, where team members thrive, and where the power of community strengthens every interaction.

Stay curious and raise the bar!

Francois Du Toit created PROpulsion, a dynamic community for financial planners and advisers promoting growth and success. He presents the weekly PROpulsion LIVE show on YouTube, with over 275 episodes delivered, leveraging his 25 years of expertise while hosting guests both domestic and international to educate and motivate. Dedicated to learning and applying new tech, he aims to make a large-scale impact. For further details, go to www.propulsion.co.za.

Why ESG investing makes sense

By Sandy Welch Editor, MoneyMarketing

Incorporating ESG (Environmental, Social and Governance) factors into investment strategies helps manage risks, improve long-term outcomes, and uncover opportunities, making it an essential element of contemporary investment approaches.

It’s important to note that ESG is not just about the climate and environment, it’s also about ethical business practices, ethnicity and diversity. Roger Eskinazi, Managing Partner at Tickmill, explains: “Environmental focuses on reducing carbon emissions, waste, and adopting renewables. Social examines fair labour practices, diversity and community impact. Governance assesses ethical leadership, transparency and shareholder treatment.”

Eskinazi goes on to say that for traders, having a firm handle on each of these ESG factors is crucial for identifying quality sustainable investments. “ESG not only helps to minimise risk, but also supports companies that are having a positive impact on the world. Sustainable investments are becoming increasingly mainstream, and we expect this trend to continue as awareness and interest in the asset class grows.”

The rise of sustainable investing Sustainable investing has grown exponentially in recent years as both institutional and retail investors realise that they can align their financial goals with their values. According to a recent Morgan Stanley report, more than half (54%) of individual investors planned to boost their allocations to sustainable investments in 2024, while more than 70% believe strong ESG practices can lead to higher returns. The importance of ESG considerations in investment management has been a topic

of growing debate, with some global asset managers questioning their effectiveness, says Conway Williams, Head of Credit at Prescient Investment Management (PIM). “Critics argue ESG integration may be overstated, but evidence shows it enhances risk management and drives long-term financial performance. At Prescient, we view ESG as essential for addressing risks and creating client value,” he says. “It has evolved into a crucial component of modern risk management.”

In its recently released Responsible Investing Report for 2024, PIM reiterated its call for a sustainable approach to investment management. Highlighting its three-pillar approach – integrating ESG into investment, product development, and corporate culture – PIM underscores its mission to foster both financial stability and impact.

“ESG is not an add-on but a critical part of modern investment strategy, enabling us to navigate a rapidly-evolving world with confidence and resilience,” explains Michelle Green, Credit Analyst and Chair of the ESG Committee at Prescient Investment Management.

Mike Adsetts, Global Chief Investment Officer at Momentum, says responsible investment practices are embedded into Momentum’s investment thinking and management. “Integrating environmental, social and governance (ESG) issues into investment decision-making and applying stewardship practices are two key parts of our role as a responsible investor, also known as Responsible Investing (RI),” he explains. Momentum prioritises industry participation to foster a responsive environment for societal sustainability. A key achievement is Momentum Global Investment Management’s approval as a UK Stewardship Code signatory, showcasing rigorous commitment to sustainability and responsible investing practices. “As a sustainability-focused business, we believe that integration of ESG

practices is the most appropriate way to ensure that our portfolios authentically address the challenges and opportunities of ESG.”

Know your facts

In South Africa, the regulatory environment supports ESG integration. Regulation 28 of the Pension Funds Act mandates that fiduciary investors consider both financial and nonfinancial risks, including ESG factors, in their decision-making processes. This ensures that asset managers are required to account for environmental, social, and governance risks when managing retirement funds, further underscoring the importance of ESG in South Africa’s investment landscape.

Closely connected to ESG, the green taxonomy is another critical tool for identifying sustainable investments. It provides clear guidelines to assess whether an investment is truly environmentally sustainable, helping to differentiate between genuinely sustainable assets and those engaged in ‘greenwashing’ – a practice where companies falsely present their products or activities as environmentally friendly.

For traders looking to invest sustainably, thorough research is essential, as is considering ESG factors and utilising tools like the green taxonomy. “Investing sustainably will allow traders to not only seek financial returns, but also to make a meaningful contribution to the planet’s future. It’s a way to invest in both profit and purpose,” says Eskinazi.

Are the returns there?

Multiple studies have highlighted ESG’s role in delivering superior investment returns. Morningstar research revealed that over a 10-year period, 58.8% of sustainable funds outperformed their traditional counterparts. Similarly, the NYU Stern Centre for Sustainable Business analysed 1 000 studies conducted between 2015 and 2020 and found that ESG and financial performance were positively linked in 58% of the corporate research papers. Critics sometimes accuse asset managers of ESG scepticism or ‘greenwashing’, but this doesn’t define the industry. Williams emphasises that at PIM, ESG is integral to the investment process. Through rigorous, datadriven methods, PIM ensures ESG practices are authentic, creating and preserving value for clients rather than being superficial. ESG’s role goes beyond simply promoting ethical practices – it provides an analytical framework that helps investors identify risks that could materially impact financial performance.

The global picture

Globally, we find ourselves at the threshold of irreversible climate change. Global warming has been an immediate and growing threat for some time. It is largely being driven by greenhouse gas emissions from energy consumption and industrial activities. At the recently held Conference of the Parties to the Convention (COP29), which refers to the United Nations Framework Convention on Climate Change (UNFCCC), a key goal was to increase the amount currently paid by developed countries to the developing world to combat climate change impact, as per the 2015 Paris Agreement. With the US probably going to pull out of the agreement under a Trump presidency, this mission became even more difficult. Without US payments to the UNFCCC or to the Green Climate Fund, it will be impossible for Europe to

make up the shortfall. The impact of this could be seriously damaging to developed countries. Mark Lacey, Head of Thematic Equities at Schroders, acknowledges US election challenges for the energy transition sector but emphasises that the long-term need to shift away from fossil fuels remains. Despite potential US climate policy reversals, global renewable energy demand is accelerating, driven by AI-related data centres, heating/ cooling needs, and corporate goals for fossilfree operations. Renewable power is a critical solution for global energy security, with rapid deployment in economies like India and the Middle East offsetting potential US weakness.

In contrast to the US, China, once one of the worst air polluters, reported its clean energy capacity reached 1 206 gigawatts (GW) in August 2024, according to the National Energy Administration. In 2020, China set a target to reach 1 200GW of renewables power by 2030, which was more than double the renewables capacity of the country at the time. The early achievement of this goal highlights the energy sector transformation of the world’s largest emitter of greenhouse gasses.

What’s happening in Africa?

Andries Rossouw, PwC Africa Energy Utilities and Resources Leader, predicts clean power in Africa will reach 25% by 2025, driven by solar, wind, and hydro growth. While capacity rose, actual power generation in 2023 grew less than 1% due to ageing coal plants and lowerefficiency, weather-dependent renewables. Southern Africa has positioned itself as a leader in renewable energy development, particularly in solar and wind, with South Africa dominating the region’s investments. Namibia is focusing on renewable buildout to support green hydrogen production, capitalising on its abundant solar and wind resources, with its oil and gas finds likely to make it a new regional energy hub.

Evaluating biodiversity

Ninety One’s Sovereign Biodiversity Index is a tool that enables investors to assess biodiversity and nature-related risks at the national level. Over half of global GDP relies on ecosystem services, making this vital for sovereign debt investors. Peter Eerdmans, Co-Portfolio Manager, EM Sustainable Blended Debt, highlights the importance of evaluating governments’ impacts on biodiversity, particularly in emerging markets, where economies heavily depend on natural resources like agriculture.

The Index helps sovereign investors allocate capital to issuers safeguarding biodiversity and preserving natural capital. It is the third tool in Ninety One’s ESG assessment framework, complementing the Climate and Nature Sovereign Index (2020) and Net Zero Sovereign Index (2021).

Continued on next page...

Left to right: Conway Williams, Head of Credit and Michelle Green, Credit Analyst and Chair of the ESG Committee both from Prescient Investment Management; Mark Lacey, Head of Thematic Equities, Schroders; Andre Nepgen, Head of Discovery Green; MIke Adsetts, Global Chief Investment Officer at Momentum.

Continued from previous page...

South Africa’s new Climate Change Act was signed into law by President Ramaphosa in July 2024. It aims to create a low-carbon economy and society that is resilient to climate change, and ensure the transition to green economy doesn’t increase existing inequalities. This Act is important – we saw an increase in our carbon intensity by just under 3% and an increase in our fuel factor by just under 4% from 2022 to 2023. “This indicates that our efforts to reduce emissions still have some way to go,” Lullu Krugel, PwC Africa Sustainability Platform Leader, says. “While this is contrary to expectations, given the levels of loadshedding and record numbers of solar PV installed in 2023, it is important to recognise that beyond electricity generation, the fuel factor figures we looked at include the energy used to drive our cars and trucks, diesel to keep generators on during loadshedding, as well as wood, coal and paraffin for heating and cooking in homes.”

“We are a resilient nation, but we are not yet climate resilient,” says Matt Muller, PwC South Africa Climate and Nature Specialist. “The effects of climate change are increasing the cost of living, threatening food and water security, and affecting livelihoods. The flooding event in KwaZulu-Natal in 2022 exemplifies the severe impact that a changing climate can have on our society and its most vulnerable members.”

The cost of non-compliance

It is important, however, that the situation changes. By 2034, some South African businesses could be paying an additional 60% of their electricity generation costs in carbon taxes.

This is according to research by Discovery Green, in partnership with EY’s Africa Sustainability Tax division, which highlights the significant financial risk local businesses face. South African carbon taxes alone are projected to increase by 143% by 2030. Tax allowances, which offer up to 85% relief, depending on the industry, may be phased out within the decade.

The core of the problem is South Africa’s heavy reliance on coal for electricity generation, emitting roughly 1 tonne of CO2e for every megawatt-hour of electricity consumed. This makes our electricity twice as carbon intensive as the global median. “The only way to mitigate the financial risk of carbon taxes is to consider high coverage renewable energy strategies that limit the reliance on coal-generated electricity to zero,” says Andre Nepgen, Head of Discovery Green.

Bridging the green funding gap

Hloolo is an innovative platform that connects green SMEs to the necessary opportunities, knowledge, finance and resources. It’s the third phase of the Circular Economy Accelerator (CEA), an ambitious multi-year initiative designed and implemented by Fetola in partnership with Nedbank, JP Morgan Chase and the Embassy of Finland. CEA was launched in 2021 to create a thriving circular economy ecosystem in South Africa. Phase three (Hloolo) is dedicated to closing the gap between green businesses and the world of finance and market opportunities.

“By 2034, some South African businesses could be paying an additional 60% of their electricity generation costs in carbon taxes”

The impact of EU taxes on South African exporters

From 2026, South African exporters to the EU could face higher costs under the Carbon Border Adjustment Mechanism (CBAM), paying the carbon tax difference between regions. Discovery Green estimates CBAM could raise electricity generation costs for energy-intensive industries like aluminium, iron, and steel by 70% by 2034. As CBAM’s scope expands, more industries may be affected, Nepgen warns.

The role of private capital

At COP29, British International Investment (BII) announced investments and partnerships to mobilise private capital into climate finance. Highlights included investments in India’s renewable sector, a major Asia initiative, and a blended finance facility in West Africa for renewable projects. BII also launched de-risking tools like concessionary capital facilities and green bonds to attract private investors to climate-vulnerable nations.

Private investors, which collectively manage trillions of dollars in assets, have been reluctant to commit capital to climate finance in emerging economies because of the perceived level of risk that such investments entail.

Macro factors such as local currency volatility, political instability and regulatory restraints are often cited as embedded reasons for not investing in countries that are most vulnerable to the impacts of the climate emergency.

But these fears might be obscuring the opportunities that exist. The International Finance Corporation (IFC) and the European Investment Bank (EIB) recently unveiled new credit risk data from the IFC’s Global Emerging Markets Risk Database spanning more than 30 years and 15 000 private-sector loans worth more than $500bn to companies in developing economies. It showed that default rates in emerging markets are much lower than commonly perceived.

Globally and locally, there’s a long way to go to achieve all the ESG goals but at least there are promising green shoots. South Africa’s pathway to true ESG compliance may require a more gradual adoption of renewables, prioritising first the economic and social pillars of ESG by stabilising the economy and reducing unemployment, says Energy Partners’ Johan Durand. This would lay the foundation for a successful transition to renewable energy, meeting environmental goals in a way that supports the country’s long-term growth and development.

By Oyena Mtuzula Head of Credit and ESG Analyst, Terebinth Capital

Skills gap hindering the implementation of ESG commitments

ESG integration in investment decision making is no longer a niche practice. It keeps gaining prominence on the back of tighter regulatory intervention, increased demand for ESG products, and supply of sustainability-related instruments. In a Harvard Law School Forum on Governance article titled the ‘The Seven Sins of ESG Management’,* which discusses the most common misconceptions and problematic practices among companies when dealing with ESG matters, lack of board and management oversight features strongly. The issue of not having enough ESG expertise on company boards has become a vital recurring one.

Why it matters

An effective ESG strategy needs to be driven by the highest level of authority (management and board of directors), bringing it to full alignment with the broader business strategy. ESG should be a core part of the values and vision of a company. We need board members with relevant credentials to ensure ESG is incorporated at a strategic level and that firm-wide commitment is achieved. ESG strategies are sometimes outsourced to other smaller departments. For example, if is handed to

the marketing and business development divisions, it could arguably be for demonstrative purposes and not necessarily a core part of operations. Closing the gap between commitments and operational realities matters.

Do boards have enough ESG knowledge to make proper decisions?

As financial institutions, one of our key fiduciary duties is that of stewardship, which involves ensuring active ownership and company engagements. Our responsibility is to promote the best governance practices that will yield long-term industry-beating and sustainable returns within our investee companies. One of the ways companies can show long-term public commitment is through ESG training and education. It is also important as a catalyst for countries to hasten the transition to a low carbon economy.

It has become evident that there are not enough ESG skills/expertise among senior decision makers and company boards. Further to this, some companies do not disclose or have insufficient disclosures when it comes to relevant education/experience related to ESG. The Responsible Investing momentum has been accompanied by a surge in demand for skills. According to the UNPRI, the demand for ESG skills is outpacing supply, creating a sustainability skills shortage. Positively,

there has been an increase in corporate boards ESG skills in the past five years, meaning they are better prepared for tackling financially material sustainability issues than in 2018, but major weaknesses persist.

Asset managers’ involvement

With ESG gaining traction, asset managers need to do a thorough analysis of sustainability reports and board credentials. Director elections can be used to leverage dissatisfaction. After voting against a resolution, post-filing actions are important in that there are steps in holding companies accountable. That is why at Terebinth Capital sustainability forms a key part of our investment process, as investing responsibly remains a primary responsibility to all our clients. We hold boards accountable and exercise our fiduciary duty to vote with care. We take the time to understand board composition and effectiveness, which means understanding the extent the individuals who serve as board members are appropriately independent, capable, and experienced. ESG fluency of corporates needs to be observed at various levels and functions to ensure ESG commitments are met.

*Papadopoulos, K and Araujo, R, 2020, ‘The Seven Sins of ESG Management’, Harvard Law School Forum on Corporate Governance, https://corpgov.law.harvard. edu/2020/09/23/the-seven-sins-of-esg-management/

By Siobhan Cassidy MoneyMarketing contributor

AHigh-level review aims to reduce tears over funeral policies

review of regulation governing the distribution of funeral policies in South Africa, announced in early November, promises to bring much-needed clarity to the industry and relief for millions of consumers who value these products for both financial and cultural reasons. In a joint statement issued on 6 November, the Financial Sector Conduct Authority (FSCA) and the Prudential Authority (PA) announced a review that aims to go beyond improving the sector’s regulatory framework to supporting small and emerging businesses and empowering consumers through a financial literacy programme.

The review is a response to concerns raised by the funeral parlour industry “around potential issues in the current regulatory framework that may be hampering the ability of the market to achieve meaningful long-term growth and effectively serve its historically under-served customer base”. The joint statement also pointed to concerns about “the existence of an unlicensed funeral insurance market and prevailing poor practices in relation to the distribution of funeral insurance, even within the licensed market”.

The ASISA release adds layers of importance and complexity, and some intrigue, to this review of a sector, where the lack of regularity and transparency seem to be at odds with its relevance and value to consumers.

Cultural importance

News of the review will be welcomed by consumers because of the practical and cultural importance of funeral insurance. It’s often a ‘must-have’ in a country where a large proportion of drivers are uninsured and only a small minority of people are prepared financially for retirement. Funeral cover is the most held insurance product in South Africa, according to the FSCA Financial Sector Outlook Study 2022, and “inflates the number of South Africans who are insured”. The study said that 42% of adults claim to have an insurance product, but when funeral cover is excluded, the share of South Africans with an insurance product drops to 19%.

According to ASISA figures, at the end of June 2024, of the 35.2 million risk policies held by life insurers for policyholders paying monthly premiums, 15 million were funeral policies against 13 million life, disability, severe illness and income protection policies, and 7 million credit life policies. Noting that funeral insurance

“holds a unique and prominent place in South Africa, driven by a mix of cultural, economic and social factors”, Mfanafuthi Mlungwana, Head of Mass Market Distribution at Discovery, pointed to a 2020 study by UK insurer SunLife that ranked South Africa as the fourth most expensive country in the world to die in. South Africans spend approximately 13% of their average salary on funerals.

When people don’t have a policy or savings, they will often take out a loan rather than skimp on a funeral. The burden of having to repay the loan is set off against enormous cultural pressure to give the deceased a dignified ‘sendoff’. According to Xolani Buthelezi, Managing Director of Scarlet Capital, the cultural importance of a dignified funeral cannot be overstated: “Funerals are viewed not only as a personal or family matter but as a community event where one’s respect for the deceased is on display.”

The costs often extend beyond the basic funeral, and may include livestock for traditional ceremonies, food for guests and transportation, adds Buthelezi, who traces his own interest in insurance to when, as a young man, he borrowed money to pay funeral expenses for an uncle who had been a father figure to him.

The popularity of funeral insurance in South Africa is also a function of accessibility. Unlike life insurance, funeral policies are simple and don’t require medical examinations or proof of income. This can also lead to ill-informed consumers treating funeral cover as a savings product or life cover. Theo Bohlale Head: Actuarial Group Benefits, Sanlam Retail Mass, says he has seen cases where clients hold “multiple funeral policies to cover needs better suited to life policies”. He adds that he encourages clients to discuss their needs with advisers.

Family connection

Funeral policies can include anyone with a family connection, subject to the insurer’s limits, says Anna Rosenberg, Senior Policy Adviser at ASISA. “Funeral policies are designed to cater for one’s immediate family, as well as extended families where one person is likely to be expected to pay for the funerals of several family members.”

Buthelezi says the ease of obtaining funeral policies and the straightforward claims process can lead to misuse, including cases of ‘murder

for money’. “Because it’s so easy to insure multiple family members and the payouts are quick, some see this as a means to a financial windfall,” he says.

Nceba Sihlali, Manager Adjudication: Life Insurance Division at National Financial Ombud Scheme, confirms consumers can buy as many policies from different financial service providers as they like. The overall limit is R100 000 per individual per funeral policy, although policies may have their own limits. “It often happens that one family member is covered in more than one policy with the same insurer. For instance, a person may be covered by both his brother and his son under different policies. Such policies may have a limitation on the total cover payable in respect of any one life assured.”

He says duplication is sometimes only discovered at claims stage when, for example, names don’t correspond. “The practice by insurers in those cases is to pay out in full to the first claimant proving a claim, and refund the other claimants whatever premiums may have been paid in respect of the other policy. This often causes dissatisfaction among policyholders.” Saying insurers had adjusted policies and practices to avoid such issues, Sihlali noted the ombud rarely received complaints about over-insurance now. Still, he says, “it would be good to have regulatory certainty”.

Bohlale, of Sanlam Retail Mass, says working with an adviser helps to ensure there are no surprises at the payout stage. He adds that an adviser would “typically do a needs analysis that considers the client’s financial needs, life stage, suitable products, existing product holding and affordability, which helps to identify any risk of over-insurance”. Buying

“Funeral insurance holds a unique and prominent place in South Africa, driven by a mix of cultural, economic and social factors”

multiple policies was also the consequence of a historical mistrust of insurance companies due to past experiences where claims were frequently denied, and recourse options were limited. “While ombudsman bodies and consumer protection laws have evolved, the lingering perception of unreliability means people often ‘double up’ on policies across different providers to hedge against the possibility of a claim being declined.”

Many South Africans view funeral insurance as a form of family savings. It’s accessible, readily available and relatively inexpensive. For lower-income households, funeral insurance may serve as the only financial instrument providing a semblance of financial security, even if it is an inefficient one. Bohlale notes financial literacy is a major issue. “People may purchase multiple small policies, some even unknowingly, through retail accounts, banks, or other channels. Without clear guidance, individuals assume that more policies equal more security, leading to duplication and excess expenditure on premiums.”

Promising to cover regulation, consumer education, as well as supporting small businesses in this complex, crucial and culturally important sector, the FSCA and PA review has its work cut out for it. Workshops will be set up for stakeholders input in the first half of 2025.

A 46% surge in insurance fraud and dishonesty

One challenge that faces the funeral and life insurance industry is fraud, and it’s growing. According to the comprehensive fraud statistics for the industry, released by the Forensic Standing Committee of the Association for Savings and Investment South Africa (ASISA) in November, the increase in fraud is concerning. But it’s not all bad news.