From listed property to buyto-let investing, property is still offering handsome returns. We look at the trends driving the industry right now.

Pg 10-15

HEDGE FUNDS

The South African hedge fund industry is currently experiencing record-breaking asset growth and double-digit net inflows for the first time. MoneyMarketing speaks to Peregrine Capital about its success in this field.

Pg 16-17

OFFSHORE INVESTING

Are there still opportunities in the offshore investing space beyond the usual suspects? Absolutely, if you know where to look.

Pg 18-23

FIDUCIARY DUTY

The relationship between financial planner and client calls for fiduciary duty. If you’re unsure as to exactly what this entails, read what the experts have to say.

Pg 24-25

Opportunity abounds in an uncertain world

Donald Trump’s return to the White House has ratcheted up tensions around the world, including among South African investors, who have been jealously eyeing impressive market performance in the US for so long. The experts are feeling the weight of uncertainty too, yet it is hard to find one who suggests that investors dramatically change their view on holding a portion of their portfolio offshore. Significant international conflicts in Ukraine and the Middle East, aggressive policy shifts, threats of tariff wars, and generally unpredictable decisionmaking during Trump’s first weeks in power added to investors’ anxieties about the markets, already under pressure from geopolitical tensions.

but also on a market level. Trying to make forecasts based on politics, geopolitical tension and ‘unknowns’ is a losing investment strategy. We prefer to keep our eyes on the fundamentals and valuations, and ensure portfolios are constructed so that no single event in markets can provide a ‘knockout punch’.”

The key to successful offshore investing, much like domestic investing, lies in careful planning, discipline and patience. While core investment principles remain the same, offshore investing comes with additional considerations, including currency fluctuations, varying market regulations, and political and economic risks unique to each region.

There is a lot to be nervous about. But there is always something to be nervous about, even if it is inflated gains, bubbles that threaten to burst, or overexuberance among investors. Investing comes with risk. Those who invest only in ‘risk-free’ assets face the risk of earning returns that are insufficient to offset inflation and meet their future liabilities.

Same old, same old challenges

Reacting emotionally to market fluctuations, even when they are driven by game-changing global events, usually leads to costly mistakes. Panic selling locks in losses, and investment decisions driven by fear (or greed) often lead to regret. In good times and in bad, a well-structured investment strategy should focus on the evergreen fundamental principles, including basing your strategy on well-defined goals, maintaining a diversified portfolio, and leveraging compound growth.

Keep those emotions in check

In the words of Rone Swanepoel, Head of Sales at Morningstar Investment Management South Africa, “No different than any other year, we face many uncertainties and challenges ahead. There is (as always) a multitude of factors at play on a macro level,

Often, an adviser’s toughest job is to help clients resist the urge to react emotionally to events. As Linda Eedes, Investment Professional at Foord Asset Management, puts it, “Many advisers will tell you this is the most important part of their jobs. Often the best thing to do is nothing.” Describing financial advisers as professional hand-holders, Eedes says, “They hold their client’s hands through difficult times and make sure they don’t make emotionally driven mistakes.”

Image: Getty Images/Anna Moneymaker

Continued from previous page

Despite the uncertainties surrounding Trump 2.0, analysts maintain a measured perspective. Patrick Mathabeni, Senior Research and Investment Analyst at Glacier by Sanlam, says the broad outlook is that the Trump presidency will bring about volatility in markets in 2025, but “the US economy is still set to be strong in 2025 (US economic indicators remain positive) and earnings remain fairly robust”.

Victor Mupunga, Head of Research at Private Clients by OM Wealth, points out that distinguishing between Trump’s rhetoric and actual policy remains a challenge. “There is also uncertainty around the sequencing of his policies, as some have conflicting economic effects. For example, his immigration stance could be inflationary, while his energy policies might lower prices. The net impact will depend on which policies take precedence and how they unfold.”

“Trying to make forecasts based on politics, geopolitical tension and ‘unknowns’ is a losing investment strategy”

Political events are notoriously difficult to predict, and their market impact is often counterintuitive. Rory Kutisker-Jacobson, Portfolio Manager at Allan Gray, warns against trying to time the market, noting that reacting to headlines rarely yields positive results.

The risks are real but so are opportunities South African investors should “get used to uncertainty”, says Bernard Drotschie, Chief Investment Officer at Melville Douglas, the boutique investment management company for the Standard Bank Group. He adds, “The advantages of investing offshore, such as diversification from South African-specific risks and access to a broader range of investment

ED'S LETTER

Aopportunities across sectors and asset classes, remain unchanged.” Drotschie adds that the prospects for emerging economies like South Africa “will largely depend on their own reform efforts, as financial aid and preferential tariffs can no longer be taken for granted”.

South Africa, despite its challenges, remains an attractive investment destination. Mathabeni says South African bonds are still offering handsome real yields as inflation is well under control, and equity valuations are still attractive with decent upside potential.

Vuyo Mashiqa, Head: Equity and Equity Derivatives at the JSE, is also measuredyet-bullish, saying, “In a volatile global environment, investors tend to prioritise markets that offer depth, liquidity and strong regulatory oversight – qualities that remain core strengths of the JSE.”

He adds, “While uncertainty can drive short-term market movements, it also creates opportunities for capital to be reallocated into well-structured, resilient markets. South Africa continues to offer a sophisticated investment ecosystem, underpinned by a strong financial sector, globally connected corporates, and a dynamic capital market. As geopolitical and economic conditions evolve, the JSE remains a key platform for investors seeking both stability and growth potential in a changing world.”

Navigating economic insights correctly

As always, a broader perspective is key and, as Mupunga from OM Wealth reminds us, history provides valuable lessons. Noting that markets have generally performed well under both Democratic and Republican administrations, he says economic fundamentals tend to outweigh short-term political fluctuations in the long term.

Glacier’s Mathabeni adds, “While Trump is a volatile character, he is, in the final analysis, pro-markets and pro-business, albeit in an unorthodox or unconventional manner. He is clear about the desire to grow the US

Trump Whitehouse has brought increasing uncertainty to the markets, and it’s not just the traditional investments that are under pressure – as I started writing this ed’s letter, Bitcoin has dropped below $80k for the first time since November last year. Before I had finished writing, it had risen again, on the back of Trump’s announcement of a crypto reserve. And before I could send it for subbing, it had dropped again, as some of the industry showed significant resistance. That’s just the nature of things right now.

It’s one of the reasons offshore investing is more crucial than ever in today’s interconnected global economy. With the increasing unpredictability of financial markets, offshore investing serves as a tool to achieve long-term financial stability and growth, ensuring a well-balanced investment portfolio. It offers your clients the

economy, contain inflation and possibly cut corporate taxes… all of which would be positive for global equities, notwithstanding the rollercoaster ride he introduces in the geopolitical realm, especially pertaining to tariffs (and their inflationary effect).”

The South African economy, while resilient, represents only a small fraction of global economic activity. The offshore opportunity set is enormous. There are currently 279 companies and 2 483 bonds listed on the JSE, against a global selection of tens of thousands of equities and hundreds of thousands of bonds.

South African investors cannot ignore global markets, especially with the shrinking JSE and higher Regulation 28 offshore limits. In February 2022, offshore investment limits for South African institutional investors, including pension funds, increased from 30% to 45%.

Glacier’s Mathabeni notes that South Africans have been allocating more to offshore assets: “While geopolitics have impacted offshore investing, the main driver has been negative domestic factors and strong offshore returns, particularly in the US, despite the rand deterring some investors.”

Offshore investing remains vital for diversification, protecting against local risks, and accessing global growth. While Trump 2.0 adds uncertainty, offshore diversification remains key. A well-structured portfolio helps navigate volatility and seize opportunities. The world is uncertain but for those willing to embrace it, opportunity abounds.

By Siobhan Cassidy MoneyMarketing contributor

potential to diversify risk, access growth markets and shield against currency volatility. By investing across different regions, investors can mitigate the impact of local economic downturns and political instability.

One sector of the market that has performed surprisingly well over the past few years is listed property. Is this a trend that’s likely to continue? We take a closer look to uncover the trends.

Are you fully on top of things when it comes to fiduciary duty? In this issue, Louis van Vuren, CEO of the Fiduciary Institute of Southern Africa (FISA), explains in detail what is expected of financial advisers and how it’s all about enacting your duty to act in the best interests of your clients. It’s about building trust and ensuring transparency.

Stay financially savvy.

Sandy Welch Editor, MoneyMarketing

Read more about Offshore Investing on page 18

Carl Lategan Head of IFA Distribution at Allan Gray

How did you get involved in financial services – was it something you always wanted to do?

I was very fortunate growing up to have a dad who worked in the financial services industry, and he encouraged and taught me to follow certain moneywise principles from a young age, such as budgeting, the benefits of starting to invest early, and the value of time in investing. His influence piqued my interest in the sector. At the time (the late 1980s), the industry was dominated by life assurance companies, and I started my career at Momentum. My very first job was to send the regional offices faxes for outstanding medical requirements for clients being underwritten by the underwriters. I studied, learnt new skills on the job and fulfilled various roles in the business before moving into the world of investments when I joined Momentum Wealth. After 11 years, I left Momentum to join Allan Gray in 2001.

What was your first investment and do you still have it?

My first investment was a retirement annuity that I started when I was 20 years old, and I still have it to this day.

What have been your best – and worst –financial moments?

Some of the best moments I have experienced over the course of my career have been seeing clients invest early enough, stay the course to see the benefit of their investment over time, and build long-term wealth. It’s great to see that what we do as a business delivers for our clients and that we get to play a role in providing insights that

are crucial to making good financial decisions – that’s rewarding to me.

On the flip side of that, the worst moments stem from people making poor investment decisions – be it chronic switching, chasing the next big investment or investing in ‘get-richquick’ schemes – that ultimately erode their wealth.

What are some of the biggest lessons you have learnt in and about the finance industry?

I have learnt many lessons but a few that stand out are the following: We work in a close-knit industry that is centred around people and building trust and relationships. If one doesn’t have a passion for people, one might find the industry challenging.

I’ve also learnt the importance of conducting yourself professionally, with competence, and putting clients first, always. Building a reputation in the financial services industry can take years but it can be destroyed in a moment, so it is prudent to protect your reputation. Lastly, the financial services industry provides those who work in it with a wonderful opportunity to build a career that adds significant value to clients.

What makes a good investment in today’s economic environment?

For me, a good investment is investing in great financial advice. I have seen, and experienced firsthand, the impact of good independent advice. This is not about making a call on what the best investment instrument, share or market will be, but rather to establish the financial goals you want to accomplish, to put a strategy together to accomplish it over time, and to stick to your strategy. Having an independent financial adviser to act as your financial coach and a thinking and accountability partner is invaluable.

“It’s great to see that what we do delivers for our clients and that we play a role in providing insights that are crucial”

What finance/investment trends and macroeconomic realities are currently on your watchlist?

Although we are bottom-up investors at Allan Gray, it is nevertheless important that we stay abreast of local current affairs and global macroeconomic views. This is especially true now, coming off the back of a year where half of the world’s population voted, as the outcome of these events and the knock-on impact affects where we invest and how our portfolios are constructed to achieve long-term returns.

For me, it is also vital to stay on top of regulatory changes and how these impact the independent advice industry, so we can respond and guide advisers appropriately.

What are some of the best books on finance/investing you’ve ever read?

Outliers by Malcolm Gladwell, The Psychology of Money by Morgan Housel, Good to Great by James C. Collins, The E Myth Revisited by Michael E. Gerber, and Same as Ever by Morgan Housel.

The Psychology of Money is one of the most meaningful and insightful books I have read about money, whether it is about making it, growing it or keeping it. It talks to the behaviour and discipline you need to display to become successful in growing your wealth over time. It also explains our relationship with money, our beliefs, and that creating wealth over time is not only about making good investment decisions, but also about your behaviour once you have.

Alternative investments: The potential of up-and-coming artists

Art has become an increasingly attractive alternative investment as part of a diversified portfolio. One of its biggest advantages is that, at the very least, it tends to hold its value and, over time, can increase in value. In the meantime, buyers get to enjoy their acquisitions.

The global art market was valued at $552bn in 2024, and is projected to grow to $585.98bn in 2025 and $944.59bn by 2033, primarily driven by increased sales of artworks, particularly among high-net-worth individuals. As the number of high-net-worth individuals rises globally, there is growing demand for art as a viable asset class to include in their investment portfolios alongside traditional assets like stocks, bonds and real estate.

The acquisition of artworks, however, is not only restricted to high-net-worth individuals, and aspiring art collectors can acquire more affordable pieces from emerging and upand-coming artists. When a purchase is made based on sound advice, an art investment can reap handsome returns.

The most common mistakes new art collectors make are not knowing the important components that influence the value of an artwork, its provenance and getting expert advice. The most important factor is the status of the artist and their biography, as well as the significance of the work within the artist’s repertoire and the social milieu in which it was created. Before acquiring an artwork, it’s essential to research the artist, their background, their creative output, what their work stands for and how it has been received –by the public, the art world and the position of the art market in general.

Look to the experts

This is where expert advice from specialists who understand the art market and current trends can make the difference. For example, in 2012, I sold a still life titled I Love You All the Time by artist Georgina Gratrix for R45 000. The work was from her first solo exhibition in the Cape, a career-defining moment for the young and emerging artist. By 2018, Gratrix’s career had flourished. She had participated in notable museum exhibitions, prestigious residencies and shows across Europe. I encouraged the owner to put the piece up for an Aspire Art auction, where it sold for R591 000, providing a 1211% return on investment to the seller and setting a new auction record for the artist.

Gratrix is far from the only local artist whose work has seen a significant appreciation in value in recent years. In 2018, an artwork by Lisa Brice (now living in London) sold for R39 000 at auction. In 2023, that same piece sold for R1,2m at an Aspire Art auction. Another Lisa Brice piece, Adult Show, was sold for R30 000 in 2019 but went on to fetch R364 000 at auction just one year later.

Cinga Samson, a self-taught artist who started painting after joining a shared artist studio, Isibane Creative Arts in Khayelitsha, Cape Town, is another rising star whose work has appreciated significantly. His breakthrough year was in 2021, with a solo show at the prestigious Perrotin Gallery in New York, being signed by leading contemporary gallery, White Cube, and an exhibition at the FLAG Art Foundation in New York, cementing his international reputation. His works now reach £321 300 at auction. A very early, formative work titled Figure was originally purchased at an exhibition in 2010 for R1 700 before selling at one of our auctions for R240 000 in 2023.

Curation is critical

Specialising in 20th-century, modern and contemporary art, Aspire Art curates live and online auctions and an exhibition and private sales programme, as well as offering art valuation and advisory services. Each piece that we put up for auction is carefully selected. We conduct detailed research into each artist and the artwork we are putting up for auction, putting effort into highlighting each piece’s historical and cultural significance. Critically, we will never put an artwork up for auction that we’re not prepared to sell again later.

Online art auctions are an effective way to embark on an art-collecting journey, offering a good introduction to the art world for new collectors. To make art collecting more accessible to more buyers, Aspire Art recently introduced a buy-now-pay-later model, which allows buyers to pay off artworks over a threemonth period interest free.

Prepare to be patient

During my nearly two decades of handling both primary and secondary art markets, I have learned that the key to assisting a client build an art collection is understanding their long-term ambitions. Acquiring an Irma Stern painting is a reliable way to preserve value and hedge your investment. However, high-end purchases like this may take a long time to appreciate significantly in value. Currently the most valuable South African artist, Stern’s paintings sell for an average of around R5m, with the most expensive selling for £3 044 000 in London in 2011.

Acquiring an artwork from emerging talents will be significantly more affordable, but does come with a degree of uncertainty in terms of how much their work will appreciate in value over time. When it comes to art collecting, it takes experience and insight to recognise emerging talent – and a healthy dose of luck – which is why expert advice is always a good idea. Art collecting is essentially about patience: an art collection is not built up overnight and it does not always appreciate quickly. Instead, regard it as a passion project that has the potential to be a lucrative investment if you have bought carefully. It’s a buyer’s market right now, which means there has never been a better time to start collecting art.

New appointments

Ninety One appoints Leong Kae Xiang

Ninety One has appointed Leong Kae Xiang as Director. He will be responsible for originating, structuring, and executing infrastructure debt transactions across South and South-East Asia, as well as managing relationships with key stakeholders. Kae Xiang is based in Singapore. Ninety One is the manager for the Emerging Africa & Asia Infrastructure Fund (EAAIF), a Private Infrastructure Development Group (PIDG) company. EAAIF provides long-term commercial debt to deliver inclusive and impactful infrastructure projects in Africa and Asia.

STANLIB’s new Head of Money Market

STANLIB Asset Management has appointed Eulali Gouws to take over from Ansie van Rensburg as Head of Money Market on 1 March 2025. Gouws’s promotion reflects a considered succession plan that has been under way for several years. Gouws, who holds a BCom (Hons) in Accounting from the University of Johannesburg, is a qualified chartered accountant and registered CFA Charterholder.

Webber Wentzel announces strategic appointments

Webber Wentzel has appointed new partners to its team, who will join the firm in phases between January and June 2025.

Kathryn Gawith has rejoined as a consultant in the Dispute Resolution Business Unit. Gawith first joined the firm in 2016 as a partner and is highly regarded for her expertise in professional liability, insurance advisory, privacy and data protection laws (including the POPI Act), administrative law, and regulatory compliance.

Lerato Nkanza joined the firm in January 2025 as a partner in the Banking, Projects & Regulatory Business Unit. A highly skilled Debt Capital Markets and Treasury practitioner, Nkanza brings extensive

experience in debt securities transactions, regulatory advisory, and deal execution across Southern, East, and West Africa, as well as North America.

Alfred Sambaza will join the Forensic Services team as a partner in March 2025. With over two decades of experience in forensic and fraud advisory services, strategic governance, and expert accounting, Sambaza’s appointment will enhance the firm’s capacity to manage complex forensic investigations, delivering comprehensive multidisciplinary solutions.

Returning to the firm in March 2025, Samantha Farren will join as a partner in the Commercial Business Unit. With over 25 years of experience in commercial property law, Farren specialises in property finance, renewable energy, and largescale property developments.

Joining the firm in May 2025, Livia Dyer will take on the role of partner in the Commercial Business Unit. With a strong background in South Africa’s regulated sectors – particularly telecommunications, media, and technology –Dyer’s expertise in broad-based black economic empowerment, licensing, and regulatory compliance will help clients navigate an increasingly complex regulatory environment.

New appointments at Bonitas Medical Fund

Vurhonga Rikhotso has been appointed the new Chief Financial Officer (CFO), effective 1 February. She takes over from CFO Luke Woodhouse, whose contract has ended. Rikhotso has 16 years’ experience in both the public and private sectors. Her expertise spans financial reporting, risk management and strategic leadership. She has a proven track record in governance and financial oversight, having held leadership roles in organisations such as Transnet and the Auditor General of South Africa. She also served on the Board of Bonitas, where she was instrumental

in providing strategic oversight and promoting financial stewardship.

Shane Perumal, currently head of operations, has been promoted to Chief Operating Officer (COO), also effective 1 February. With over 25 years of experience in the healthcare industry and a Master of Business Administration (MBA) specialising in Healthcare Management, Perumal has driven operational effectiveness and optimised business processes within the Scheme.

OM Bank CEO gets Reserve Bank backing

OM Bank has received approval from the South African Reserve Bank’s Prudential Authority to appoint Clarence Nethengwe as Chief Executive Officer (CEO) of the country’s newest bank, effective immediately. OM Bank will launch with a select group of clients in early 2025, ahead of a broader public rollout later in the year. The bank will offer a comprehensive range of personal banking solutions, including transactional accounts, savings, and credit products.

Nethengwe has significant work ahead of him. Since 2009, he has built one of Old Mutual’s largest and most successful businesses, the Mass and Foundation Cluster (MFC). His leadership has been instrumental in driving customer-focused solutions that deliver genuine, meaningful value.

Paycorp appoints new board member

International payments provider Paycorp has appointed John Chaplin as a Non-Executive Director to its Board. Chaplin brings over 30 years of global retail payments and fintech expertise. Chaplin has played a pivotal role in the evolution of the payments industry, with extensive experience across card payments, mobile transactions, and B2B financial solutions. His career spans executive and board-level positions at some of the world’s leading payments and fintech organisations.

Leong Kae Xiang

Livia Dyer

Eulali Gouws

Vurhonga Rikhotso

Kathryn Gawith

Shane Perumal

Lerato Nkanza

John Chaplin

Alfred Sambaza

Samantha Farren

Professional fund analysis made easy

FE fundinfo, in conjunction with ProfileData, is a leading provider of investment data to the financial services industry, supplying data to advisers, fund groups and financial trade publications.

ProfileData’s solution helps you save time by not having to trawl across multiple data sources. Being truly independent means ProfileData is free from bias and can help you comply with the FSCA’s calls for objective due diligence. Fund Analytics gives you the ability to adopt a whole of market approach with access to over 300 000 financial instruments, including Unit Trusts & OEICs, Investment Trusts, Pension Funds and ETFs.

Fund Analytics is an industry-leading research solution for comprehensive fund research, portfolio analysis and reporting. It combines decades of investment datacollection expertise with cutting-edge software to help financial advisers and their teams create a robust investment proposition. It has been powering investment decisions for over a decade, and focuses on providing advisers with an efficient solution to build successful centralised propositions and improve profitability, while remaining compliant and keeping costs down.

Supporting your investment process

Whether you build your proposition through the more traditional fund selection route or prefer to outsource, Fund Analytics provides you with the right tools to improve efficiency in each stage of your investment planning process. The wide variety of research, modelling and reporting tools available on Fund Analytics can help you optimise your investment selection, conduct objective due diligence, and demonstrate the

value of your service in a streamlined, fully compliant and profitable manner.

Investment research

• The powerful fund filter tool allows you to easily browse through 300 000 financial instruments to shortlist funds, sectors or managers according to your selection criteria

Conduct meaningful analysis on your shortlist by reviewing extended performance data, ratios, volatility, manager information, fees, asset breakdown, regional breakdown, peer group comparisons, and more

Access the FE Crown Fund Rating, FE Alpha Manager Rating, FE Risk Scores, RSM, Morningstar ratings and more at no additional cost.

Portfolio analysis

Build client portfolios from scratch using the Fund Analytics Dynamic Portfolio Builder tool

• The historic capabilities of the tool allows you to mark fund switching and to assign full portfolio weightings

Conduct comprehensive portfolio comparisons to highlight the value of your recommendation against a client’s current portfolio, benchmarks, funds, and more

• Review and conduct objective analysis on your Discretionary Fund Manager and Model Portfolio data.

“Fund Analytics provides you with the right tools to improve efficiency in each stage of your investment planning process”

Communicate your investment research to clients

• Use a wide variety of presentation tools, including dynamic charts, tables and graphs, to present information to clients in an easyto-understand format

Create bespoke portfolio reports using the Custom Portfolio Report Builder to suit your specific requirements

Export ‘short, medium or long’ portfolio scans with a comprehensive range of details on your portfolio, including individual factsheets, asset breakdown, performance, and more

• The bespoke portfolio reports and scans can be white labelled to suit your brand and maintain professional standards

All portfolios saved on our systems reflect current prices – allowing you to easily automate client reviews.

To find out more about Fund Analytics, contact Tracey Wise on 079 522 8953 or tracey@profile.co.za

Calling Financial Advisors

How Franc is making investing simple and accessible

Franc is a digital wealth platform focused on simplify investing in South Africa. It uses cutting-edge technology and innovative products to bridge the gap between saving and investing, with the aim of providing financial freedom to users.

Helping South Africans grow their money

In South Africa, the latest reported Household Saving Rate is -0.9%, which means that South Africans are spending more than they save. This is coupled with the fact that only 6% of the population are on track to retire comfortably, according to the 2023 10X Retirement Reality Report

There are two big problems that have led to this state of affairs: only 42% of South Africans are considered financially literate (and this proportion is declining), and the world of saving and investing is confusing and inaccessible, often shrouded in convoluted terms and conditions.

Franc was founded by Thomas Brennan and Sebastian Patel to address these two problems. With Thomas’s engineering background and Sebastian’s expertise in actuarial science and investment, the duo has built Franc to be intuitive, accessible, and tailored for every user, cutting through the confusion to help users get started.

A user-friendly investment app Franc’s impact is most evident in its commitment to inclusivity. The userfriendly platform guides individuals in setting up goal-based investment pots through a robo-adviser – the first registered in South Africa. The goal-based approach makes it easier for them to align their savings with their big dreams, whether for personal growth, family support, or starting a business. Each investment pot is underpinned by a combination of handpicked funds – from a money market fund to an offshore exchange-traded fund – selected for being among the top-performing and lowest-cost in their category.

With the goal of helping people build generational wealth, Franc also caters to invested parents who are seeking to secure their children’s future through a dedicated Child Account that is simpler and quicker to set up than many other products on the market. Their Shared Goal feature allows for collaborative saving and investing between couples, families, friends or stokvels.

The savings account, one of Franc’s top-performing products, encourages users to keep their savings separate from day-to-day banking, ensuring users can more effectively set money aside without being tempted to use those funds on a transactional level. The innovative and exciting live interest tracker allows users to see their money grow second by second.

Franc has big growth ambitions

Backed by venture builder Aions Creative Technology (headed by serial entrepreneur Mitchan Adams), Franc is proudly South African, and as a Level 2 BBBEE contributor and 52% Black-owned business, Franc is reshaping the financial landscape while contributing to economic transformation. With a compound annual asset under management growth rate of 70% since its inception, the platform’s scalability and user engagement reflect its success in addressing real market needs.

“We believe that every South African deserves to see their money grow and work for them. Having Aions on board as our latest investor, we hope to leverage their ecosystem of partners and resources to achieve our upcoming growth objectives,” says Sebastian Patel, Chief Operating Officer of Franc.

The investment app soon plans to expand its offering to include a tax-free savings account and retirement annuity, as well as business management tools to help sole proprietors manage their finances better. This funding will also enable Franc to scale its impact further, refine its technology, and introduce new features to meet the evolving needs of its users.

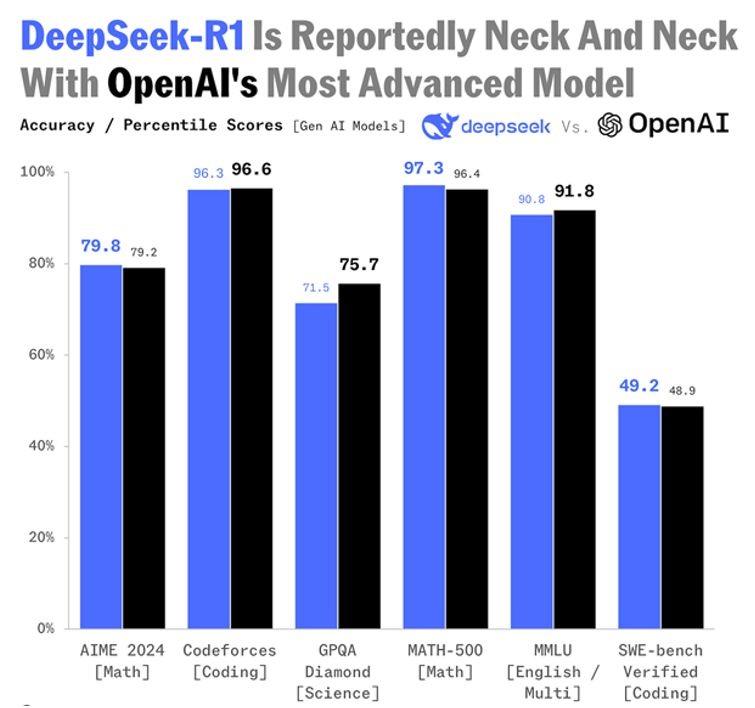

DeepSeek’s energy efficiency challenges AI industry

WBy Philip Short Senior Equity Analyst, Flagship Asset Management

e’ve all read about DeepSeek and the remarkable competitive edge it presents to existing mega-cap AI companies. It’s more efficient, costs less to operate, and has decent output. The energy efficiency that DeepSeek achieves evidences that AI can operate on less energy than the dominant AI players are running on. Thus, the market is taking an axe to AI energy providers.

However, this energy efficiency may have unintended consequences –encapsulated in a 160-year-old economics paradox, the Jevons Paradox, which has come to light again in AI circles. It theorises that efforts to reduce the demand of a commodity, say energy, through energy-efficiency initiatives may actually increase the use of it because the resultant lower prices for the commodity spur significantly higher demand.

DeepSeek’s performance is in line with the latest OpenAI results (see chart below), but it is less energy intensive and apparently significantly cheaper; therefore opening the door to more applications being taken up in the everyday world. This increase in penetration will create a net positive demand and increase AI’s total energy consumption.

When computers and mobile phones were first invented and trialled, people thought they would be used by a fraction of the actual Total Addressable Market (TAM), which is why their unit prices in the beginning were so high. Then, because pricing came down, the TAM opened dramatically. Prices came down X and then another X, but volumes went up 10X, taking up the total net demand of the market.

Margins will be affected

I’m not sure how this plays out in the semiconductor chips space (e.g. Nvidia) in terms of their pricing and margins – they will sell a lot more chips/units, but their margins are likely to come down with an unknown result on profit growth vs current estimates, in my opinion. With the increasing demand for energy, especially in sectors like data centres and computing, I believe DeepSeek will have a net positive impact on AI energy and infrastructure companies. In fact, I think DeepSeek’s rollout has likely accelerated faster than the progress seen with chipmakers and designers in this space.

By Francois du Toit CFP® PROpulsion

WTrust and technology: Making it work in financial advice

hat keeps financial advisers awake at night? It’s not the ups and downs of the markets or the latest economic news. It’s the trust their clients place in them. It is the fact that the client’s entire future is in their hands. I was reminded about this when an adviser told me about their client who’d just received a large inheritance. The client felt completely lost about what to do next.

At that moment, what mattered wasn’t clever technology or complex strategies – it was simply being there to listen and understand. Technology is changing how we give financial advice, but one thing stays the same: putting clients first. This will not, and should not, ever change.

A new kind of trust

Being a financial adviser means making a promise to your clients – to always put their needs first. But what does this look like in today’s digital world? Think of it like going to the doctor. You trust them with your health, just as clients trust advisers with their money and future dreams. Whether it’s helping someone invest wisely, choose the right insurance, or plan for retirement, every choice must focus on what’s best for them.

The move to digital has brought new things to think about. How do we keep client information safe? What’s the best way to stay in touch? When should we use automated tools? These are all part of taking care of clients today.

Making technology work for people

“How do we keep things personal with so much tech and AI around?” I hear this question a lot. The trick is seeing technology as a helper, not a replacement. Yes, computers can work out complex cashflows and identify shortfalls, but they can’t understand why someone wants to retire early to spend time with their

grandchildren, or feel the worry in someone’s voice when they talk about their savings.

Look at the clever tools we have. They can quickly spot opportunities and risks that might take hours to find by hand. But the real magic happens when advisers use these insights to have better conversations with their clients about their future.

Getting it right day-to-day

Here’s what works well:

“The trick is seeing technology as a helper, not a replacement”

• Write everything down: Keep good records of every conversation and decision. If it’s not written down (and in your CRM), it didn’t happen. This helps you give consistent, reliable help to every client.

• Keep learning: Things change quickly in finance. From online advice to digital currencies, staying up to date helps you give better advice.

• Make sense of the numbers: Let computers crunch the numbers while you focus on what they mean for each client’s own situation.

• Be flexible: Find ways to work that suit each client. Some might love video calls; others prefer face-to-face meetings. What matters is staying connected in a way that works for them.

Solving real problems

Here’s something that happens often: your computer programme says a client should invest cautiously, but when you talk to them, you realise they’re quite comfortable taking more risk. What do you do?

This is where experience and judgment matter most. The best advisers use technology to help make decisions, but they also trust what

they learn from really getting to know their clients. Tools are helpful, but they’re just one piece of the puzzle. Building trust today means:

• Being open about how you use technology

• Explaining things clearly without jargon

Keeping in touch in ways that suit each client

Using digital tools to give better advice

Keeping information safe while making it easy to access

• Making each client feel special by mixing technology with personal care.

The best advisers use technology to free up time for what really matters – understanding their clients’ hopes and worries. This turns financial advice from just a service into a true relationship.

Always do the right thing, for the right reason, with the right intent, and see how everything else follows and falls in place.

Stay curious and keep raising the bar.

The changing face of property investing

Two new business models are aiming to revolutionise traditional property ownership. MoneyMarketing takes a closer look.

The world changes when people take action. I started FracProp because too many people are excluded from property ownership due to outdated policies, financial barriers and high entry costs. Others, despite years of paying mortgages, are losing their homes. We must redefine property ownership to align with modern, innovative solutions. Our challenge was twofold: how do we help people enter the market, and prevent homeowners from losing their properties? FracProp offers a communitydriven model, allowing individuals to co-own high-yield properties without massive upfront capital or credit checks. With FracFin, we introduce Home Equity Agreements to support homeowners who face financial distress with over 50% equity. We also empower stokvel groups by connecting them with developers to co-invest in large-scale projects. FracProp is rewriting the rules of ownership, making it more accessible, profitable and community driven.”

“We must redefine property ownership to align with modern, innovative solutions”

How does FracProp’s model work to make property ownership more accessible, and what makes it different?

FracProp is built on one powerful idea: ownership should be for everyone. Traditional property ownership demands large deposits, mortgage approvals and financial risk. With FracProp, you can own a piece of highvalue property for as little as R100 (or the equivalent in pula or dollars), with no deposit, credit checks or barriers. Properties are registered under a company and divided into property fractions. You buy what you can afford, earn rental income, and benefit from capital growth, without the hassle of property management. Our Home Equity Agreement helps homeowners facing financial difficulties. If you own over 50% equity but are struggling, our sale-leaseback model lets you stay in your home, preserve equity, and buy back ownership within three years. Beyond

financial returns, FracProp builds communities

– connecting property developers with savings groups (stokvels) to create wealth and uplift communities.

What is your long-term vision for FracProp?

Our vision is bold: we’re here to change the game. We’re shifting the landscape of property ownership and building a future where:

• Communities co-own developments from the ground up

People start building wealth today, no more decades of waiting

No one loses their home after years of paying a mortgage

• Property ownership is for everyone, not just the wealthy elite

Aspiring owners access multiple pathways, including fractional investment, Instalment Sale Agreement Mortgages, and innovative financing models

• Our platform becomes a one-stop shop, offering financial wellness, education, ownership planning tools, and alternative financing solutions.

We’re not just building a property ownership platform, we’re creating an ecosystem that ensures access, sustainability, and financial empowerment for all.

What are the biggest challenges you’ve faced in disrupting the property market, and how have you overcome them?

We’ve encountered challenges such as: Changing mindsets: Many believe traditional mortgages are the only path to ownership. We tackle this through financial and property education, showing fractional ownership as a viable, scalable and profitable alternative.

• Regulatory hurdles: Property laws weren’t designed for fractional ownership, making compliance complex. We work with legal, property and financial experts to ensure a legally sound, scalable model.

• Building trust: People are sceptical of new ownership models. We prioritise transparency, governance and strong partnerships while consistently delivering value to our investors.

BRIX

Redefining the perception of real estate in South Africa, Brix is set to disrupt conventional methods of investing into property and create ease of access to all. This pioneering platform defines a new era of property exchange in South Africa, allowing fractional ownership of properties. Brix is on a mission to make property investment a reality for a wider demographic by breaking down financial barriers, enabling individuals from all walks of life to enter the property market.

“Brix provides a secure and innovative environment for property investment,” says Tyran Faber, Brix co-founder. “By digitising and dividing tangible assets into digital tokens, we enable fractional ownership, increased liquidity and seamless transferability for investors. This platform allows individuals from all walks of life to participate in the property market without the usual financial constraints.”

Through their strategic partnership with SchindlersX, Brix has positioned itself to shift the traditional mindset around real estate investment. The platform allows individuals to enter the property market with minimal investment, starting from as little as R100.

“Tokenising assets enables investors to participate in previously inaccessible opportunities such as student accommodations, real estate properties, infrastructure and more by creating userfriendly, straight-forward processes,” explains Maurice Crespi from SchindlersX.

The investment projects available on the Brix platform are sourced by property professionals, ensuring access to high-quality investments. “Tokenisation is transforming the investment landscape,” adds Faber. “Brix is leading this charge by connecting digital finance and technology with real assets and investments.”

As part of its broader vision, Brix leverages blockchain technology to offer a transparent, secure, and user-friendly environment for investors. The partnership with SchindlersX further enhances this offering by providing expertise in Real-World Asset (RWA) tokenisation.

Monametsi Kalayamotho, FracProp and FracFin founder.

Tyran Faber, Brix co-founder.

Where is listed property headed in 2025?

Compiled by Sandy Welch

Listed property continues its phenomenal performance in South Africa. The market’s comeback rally kicked off in October 2023, fuelled by growing optimism over an impending interest rate cutting cycle. This sentiment was driven by the US Fed pausing rate hikes and slowing inflation. As investor confidence rebounded and SA’s risk premium eased, SA listed property followed suit, experiencing a strong re-rating.

In 2024, it was one of the best performing asset classes, riding on the back of unexpected election results and the green shoots of the turnaround in economic fortunes. It outperformed both SA bonds and SA equities, which returned 26% and 25%, respectively.

According to Luqman Hamid, Portfolio Manager at Ninety One, helped by declining local bond yields, listed property returned almost 30% for the year. “The majority of this return was through re-rating, with comparatively smaller contributions from income and income growth,” he explains.

“It’s expected that in 2025, there will be continued improving trajectory for local property”

“This echoed the case for many SA assets in 2024, where returns were driven by increasing expectations from a low base, rather than fundamental improvement.” It’s expected that in 2025, there will be continued improving trajectory for local property as rental reversions begin to trend upwards across the retail, office and industrial sectors. “We continue to see select opportunities in SA-orientated names exposed to retail and industrial subsectors (i.e. Hyprop, Equites Property Fund and Vukile), while the UK retail names (Hammerson and Shaftesbury Capital) also offer an attractive combination of yield, growth, strong balance sheets and accelerating improvement in fundamentals.”

Real Estate Investment Trusts (REITs) and Real Estate Investment Company (REICs) are companies that own, operate or finance

income-generating real estate across various sectors, such as commercial, residential, industrial and retail properties. The five top performing REIT and REICs in South Africa are:

GrowthPoint

GrowthPoint's latest results will be out later this month, but in the most recent results, up until 30 June 2024, the company reported improvements in the majority of key performance indicators (KPIs), including arrears, rental reversion rates, valuations and vacancies. The company noted, however, that a strong operational performance has been overshadowed by the negative impact of high interest rates, lower dividends from Globalworth Real Estate Investments (GWI), and reduced profit from the South African trading and development division.

Adding to its portfolio, GrowthPont this year delivered the multiyear, multimillionrand revitalisation of the historic Longkloof precinct. The multifaceted project involved the renovation of several Growthpoint-owned buildings and the creation of a public square. “Growthpoint’s vision was to reimagine six buildings – made up of a historical school and an industrial building with its boiler room –and a vacant parking lot as a hip and vibrant mixed-use precinct that embodies Cape Town’s essence in something new and exciting, yet respectful of its heritage,” says Wouter de Vos, Growthpoint’s Regional Head: Western Cape. “Five years after the start of the pandemic, the resilience of the Cape Town market is undeniable, with an upswing in international tourism since mid-2023, together with ongoing ‘semigration’ from other parts of South Africa to the Western Cape,” he explains. Included in the precinct is the 154-room Canopy by Hilton Cape Town Longkloof Hotel, the first of its kind

in Africa. De Vos says the hotel is the perfect complement to the mix of uses and tenancies in the Longkloof precinct.

Fortress

Fortress is a REIC with a focus on developing and letting premium-grade logistics real estate in South Africa and Central and Eastern Europe (CEE). Fortress’s direct portfolio (excluding NEPI stake) is still predominately focused in South Africa, with around 85% of direct portfolio exposed to South Africa. Its direct CEE portfolio is focused on two key regions, Poland and Romania, and has exposure to the logistics sector only. “Including NEPI, our total CEE exposure (of total assets) represents 40%,” says Steven Brown, CEO of Fortress. “The recent interest rate cuts continue to support increased appetite for the sector, both from a listed and direct perspective. Growth across the real estate sector is expected to be driven primarily by continued demand for mixed-use developments and logistics spaces, sustainable building practices, and strategic investments by key players like Fortress Real Estate.” He says that as interest rates decrease, cost of funding reduces, sentiment improves and bond yields adjust accordingly, making real estate exposure an attractive opportunity, on a relative basis, all else equal.

The performance of South African retailers is somewhat correlated to the overall economic health of the country and, as such, are not immune to a low growth environment and economic shocks. However, Fortress’s commuter-focused retail portfolio is highly defensive and has a strong portfolio of tenants who are less exposed to discretionary spend, with a focus on essential goods and services.

Continued on next page

Continued from previous page

He attributes the company’s strong investment in the logistics space to the emergence, growth and prevalence of online retail platforms. “South Africa’s e-commerce sector has experienced exponential growth, reaching a record R71bn in sales in 2023,” he points out.

Attacq

JSE-listed REIT Attacq, the strategic development partner of Waterfall City, had a robust set of results for the year ending 30 June 2024. The company reported full year dividend growth of 19.0% to 69.0 cents per share, with distributable income per share increasing by 19.9% to 86.2 cents. Operationally, Attacq delivered a solid performance, with the occupancy rate rising to 92.8% and collection rates remaining high at 100.2%. The group maintained its intent of being a client-focused, innovative and trusted real estate business, prioritising client needs and satisfaction in its operations.

“Prospects are clearly very closely tied to the anticipated economic recovery in SA”

According to Jackie van Niekerk, Attacq CEO, the company concentrated on executing against their strategy, which included concluding key deals such as the R2.7bn Waterfall City transaction, completed in October 2023. In this deal, GEPF acquired a 30% stake in Attacq Waterfall Investment Company

Proprietary Limited (AWIC). This strategic partnership provides additional capital, facilitating the ongoing development of Waterfall City. In May 2024, Attacq’s 70% held subsidiary, AWIC, acquired the remaining 20% stake in Mall of Africa from the Atterbury Group. AWIC currently holds an 80% stake in the asset.

Vukile Property Fund

Vukile Property Fund is a consumer-focused Retail REIT, with a significant portion of its assets located in the Iberian Peninsula (59%), both in Spain and Portugal. Vukile’s financial year ends on 31 March 2025. For its interim results, Vukile reported a 6.0% increase in its interim cash dividend to 55.2cps for the six months to 30 September 2024, positioning on a trajectory toward the upper end of its 4% to 6% DPS growth target for the full year.

CEO Laurence Rapp states, “Vukile's businesses in South Africa and Spain are intentionally structured for seamless success, driving the strategic and operational progress.” Locally, it focuses on commuter, township and rural malls, which has performed successfully to date. “Vukile

proactively enhances its portfolio to boost shopper engagement and optimise tenant performance,” says Rapp. “We integrate technology, data analytics, and consumer insights to add value to our assets and enhance their performance.”

Redefine

Redefine Properties announced in its investor update for the half-year ending 28 February 2025 that its earnings outlook has stabilised despite a challenging operating context, driven by a focus on efficiency and strong demand for quality assets.

The company reported that its South African portfolio achieved a net operating profit margin of 77.8%, while EPP, its directly owned Polish retail property platform, improved its margin from 66.4% to 71.7%. This led to a consolidated group net operating profit margin of 75.9%.

Redefine CEO Andrew König highlighted that the global path to economic normalisation has been disrupted by changes in US policy under President Donald Trump, which introduced uncertainty around interest rates and inflation. “The stage is now set for a shallow easing cycle, and rates may not reach the levels we previously expected,” he says. “While European interest rates continue to trend downward, escalating geoeconomic tensions cloud the 2025 outlook. To sustain growth in valuations, we cannot rely solely on interest rate movements. Our strategic focus remains on organic income growth, as this will drive value creation in the current market.”

Redefine’s South African portfolio has demonstrated solid performance, particularly in the industrial and retail sectors, which drove a 1% increase in overall occupancy since August 2024. Additionally, 80% of renewals were completed at

stable or increased rental terms, a positive indicator of growth.

The industrial sector has proven especially resilient, with occupancy rising to 97.6%, alongside positive rental reversions in a competitive market. “The industrial sector continues to be one of our strongest performers, and we see potential for further growth if capital availability allows us to expand,” said Leon Kok, Redefine’s COO.

Conversely, the office sector remains challenged by excess supply and limited demand, except in select nodes. Looking ahead, Redefine’s strategy is focused on disciplined capital allocation, the sale of non-core assets to reduce its loan-tovalue ratio, restructuring joint ventures to enhance visibility of income streams while delivering income growth.

The year ahead

Overall, we expect a decent year for local listed property in 2025, says Ninety One’s Luqman Hamid. “While most of the rerating has probably already occurred, fundamentals for the sector appear reasonably favourable. Prospects are clearly very closely tied to the anticipated economic recovery in SA continuing to make progress, and any disruptions or noise, as we have seen in the early part of this year, will impact sentiment in the short term.”

He explains that dividend sustainability also looks much improved. With many companies having restructured their balance sheets, current dividend streams are well covered by operational income. Against the backdrop of moderately declining local interest rates, this should provide a favourable environment for decent returns in 2025. With anticipated income returns in the region of 8% on average likely to be bolstered by some growth and marginal rerating, we see low double-digit returns as an achievable target for the sector this year.

SA’s evolving real estate investment landscape

By Steven Brown CEO of Fortress

How has South Africa’s real estate investment landscape evolved in recent years?

South Africa’s real estate investment landscape has undergone various forms of transformations in recent years, influenced by economic shifts, evolving consumer preferences, and strategic corporate initiatives.

Sustainability has become a central focus, with a significant increase in certified green buildings and renewable energy solutions among new developments. This growth reflects a shift in consumer priorities.

Tell us about your company and the key investment opportunities. Fortress is a real estate investment company (REIC) focused on developing and letting premium-grade logistics real estate in South Africa and Central and Eastern Europe (CEE). Our logistics portfolio primarily consists of state-of-the-art logistics parks that we have developed. These parks play a crucial role in supporting the growing demand for efficient and sustainable supply chain solutions.

We are also expanding our convenience and commuter-oriented retail portfolio, comprising 43 shopping centres. Fortress holds a 16.3% interest in NEPI Rockcastle, the largest listed property company on the JSE, with a €8bn portfolio of 60 assets across eight countries. Our strategic focus and key opportunities revolve around increasing our specialisation in two core areas: logistics and commuter retail.

What factors are driving growth in logistics parks and commuter-oriented retail centres?

High-quality, secure logistics space continues to perform well and has experienced

buoyant demand over the past 24 months with very low vacancies across prime locations. Fortress has developed c.150 000m² of high-quality logistics space in the past 12 months, of which almost 100% was let prior to completion. Fortress’s current logistics development pipeline consists of approximately 65 000m² in South Africa and a further 30 000m² in Poland, of which 75% is already pre-let. We believe opportunities exist to extend, enhance and refurbish existing retail space in our portfolio, and grow our portfolio through value-enhancing inorganic acquisitions.

How have macroeconomic factors (inflation, interest rates, foreign direct investment) impacted real estate investment?

The recent interest rate cuts continue to support increased appetite for the sector, both from a listed and direct perspective. As interest rates decrease, cost of funding reduces, sentiment improves and bond yields adjust accordingly, making real estate exposure an attractive opportunity, on a relative basis, all else equal. The persistent low growth environment, however, continues to hamper real economic sustained growth, which directly affects the demand for new logistics warehouses and the performance of our retail tenants.

Why should financial advisers tell their clients to invest in real estate (and retail or logistics)?

Fortress is a listed real estate investment company (REIC) and not a REIT. The tax consequences for an investor are material (profile dependent). Fortress intends to pay semi-annual dividends at a 100% payout ratio. Investors receive an attractive investment opportunity (focused real estate fund with exposure to high-growth well-performing sectors of retail and logistics). From a valuation perspective, the investment is attractive as Fortress is currently trading on a 12-month forward, post-tax dividend yield of 8,5% and a discount to Net Asset Value of 25%. Other positive aspects include an internal development team with high expertise, strong management, focused strategy and ability to unlock shareholder value through corporate action.

Growth powering Logistics Real Estate across South Africa

Better accessibility to major arterials, custom built, advanced security and control, more efficient storage techniques, unrivalled energy-efficiency and ultimately greater cost reductions across the supply-chain.

By Laurence Rapp CEO, Vukile Property Fund

The evolution of REIT investing

The nature of property investment has fundamentally changed. Historically, real estate investment was viewed as a passive rent collection model, but today, it is better understood that these assets require active management. Real estate has become an operating asset class.

This shift has profound implications for investors, particularly when evaluating retail REITs (real estate investment trusts), where understanding asset management, tenant strategies and operational efficiencies is key to identifying outperformance.

Investors willing to delve into the nuances of property as an operating asset will find excellent opportunities in today’s market.

When unpacking Vukile’s investment proposition, shrewd investors will discover an unrivalled retail REIT distinguished by its singular focus: its customers. Driving consumer activity benefits tenants, increases rental income, and ultimately delivers superior returns to investors, providing them with annuity income and highquality cashflows from blue-chip tenants.

Uncovering outperformance

In asset management, alpha and beta are key indicators of investment performance. Alpha

measures how well an investment performs relative to a benchmark index. Beta measures systematic risk and volatility. In this equation, a high alpha is always good as it indicates outperformance. Beta is more subjective based on risk appetite.

For REIT investors, identifying a high alpha means focusing on factors that drive superior returns. Besides the physical property assets in a portfolio, investors must evaluate which management teams have the expertise, strategies and resources to create the most value.

Evaluate REIT investments by thinking like a business owner

Investors who still view property purely as an immovable asset miss the true value proposition. The most effective investors see properties as dynamic, income-generating businesses requiring active oversight and proactive positioning.

Success in real estate investment comes from managing each property as a business. Maximising value requires a deep understanding of the various components across the value chain. While this understanding of property as an operating business is more prevalent in South Africa’s alternative asset classes – be it storage, student accommodation, or retirement living –the same logic should apply to traditional real estate sectors. It is especially critical for shopping

Buy-to-let investments hold value

South Africa’s property investment landscape is changing as investors tap into the growing demand for coastal homes and explore alternative rental models to build wealth. Data from Standard Bank highlights a significant increase in buy-to-let property investments, with one in eight mortgage applications nationwide over the past year linked to this investment strategy.

The Western Cape has emerged as a prime hotspot for property investors, with 31% of new home loan applications in the province attributed to buy-to-let purchases – more than double the national average of 12%.

“Over the past decade, the Western Cape has consistently positioned itself as an investment destination. Areas like Cape Town have benefitted from consistent demand driven by tourism and a growing expat community,” says Chiko Manokore, Head of Personal and Private Banking at Standard Bank.

Gauteng, South Africa’s economic hub, continues to show strong buy-to-let activity, nearly doubling the national average. Within the province, Tshwane leads the way in rental market investment. The region’s property investors are largely focused on generating long-term rental income. “In Johannesburg, property investment tends to focus more on rental income, unlike the Western Cape, where short-term rentals are particularly popular,” explains Manokore.

Multifamily residential rentals

Institutional investors are increasingly turning to the multifamily residential rental sector as a robust and scalable asset class. The South African Multifamily Residential Rental Association (SAMRRA) is at the forefront of this transformation, working to unlock valuable data and promote investment in this sector. Established nearly a year ago, SAMRRA has released its second comprehensive report, compiled by the Centre

centres, where operational excellence dictates financial performance.

Growing understanding of different real estate

asset classes

Previously, investors viewed real estate as a homogeneous asset class. Today, sophisticated investors distinguish between the office, industrial, retail, and residential sectors.

However, the most discerning investors go further – layering sector insights with assetlevel analysis to identify the highest-performing portfolios within a sector. As sub-sectors become more specialised, expert management becomes crucial for outperformance. The best investment decisions come from understanding the expertise and resources of the management teams within a sector and their ability to leverage tools, technology, and data to create a competitive advantage.

What drives outperformance in Retail REITs?

Retail property performance depends on more than location and size. The right management approach significantly impacts rental income and capital appreciation.

Key strategies include optimising space utilisation, curating superior tenant mixes, driving consumer traffic and dwell times with marketing and promotions, and controlling costs through, for instance, solar energy adoption.

for Affordable Housing Finance (CAHF), detailing the growth and stability of this emerging investment category.

SAMRRA currently represents 13 major players in the multifamily rental market, collectively managing over 75 000 units across 550 properties, with a combined asset value exceeding R72bn. As the sector becomes more organised and data-driven, investment confidence is growing, further fuelling expansion.

“Our research confirms that the multifamily residential rental sector in South Africa is characterised by its resilience, stability, and potential for long-term growth and sustainable value creation,” says SAMRRA CEO Myles Kritzinger. According to the CAHF report, approximately 4,5 million (23%) of South African households are renters, highlighting a strong and growing demand for rental housing. Notably, 15% of these households – around 685 000 – live in apartments, reflecting a significant opportunity for institutional-grade rental developments. Over the past five years, the market has witnessed a 9% increase in households renting apartments, adding approximately 54 000 new rental units.

PIC’s landmark investment

In a groundbreaking move, the Public Investment Corporation (PIC) has made its first-ever investment in the multifamily residential rental sector by partnering with Divercity Urban Property Group, South Africa’s leading investor in affordable rental housing. This investment will facilitate the development of an additional 2 500 rental units, addressing the country’s urgent need for affordable housing.

“As South Africa faces an acute need for housing, well-located, well-managed affordable rental portfolios offer immense value for both investors and society. This investment signifies growth in the multifamily asset class,” says Carel Kleynhans, CEO of Divercity Urban Property Group.

PIC’s Chief Investment Officer, Kabelo Rikhotso, underscores the broader impact of the partnership: “As South Africa confronts a critical housing shortage, the PIC is committed to investments that not only deliver sustainable financial returns to its client portfolios but also drive impactful socio-economic outcomes.”

OUR 220 MILLION SHOPPER VISITS A YEAR CREATE SUSTAINABLE GROWTH AND SUPERIOR VALUE .

This is Gemma B, aged 30. As someone who’s only just starting to find her feet in the corporate world and saving up for her dream honeymoon, she doesn’t have a lot of disposable income, so her monthly grocery shopping trips are brief, but she also enjoys visiting the centre on weekends to socialise with family and friends.

Gemma loves the centre’s energy and vibe. There’s always something new going on, and she also enjoys the convenience of being able to find most things she needs and wants at one destination, which saves on travel expenses and frees up more time to have fun.

We know all this and more about Gemma B and our other visitors, too. Our multi-faceted consumer behaviour research, combined with our deep understanding of the needs and desires of the communities we serve, leads us every step of the way.

Our unique focus on a superior customer experience ultimately benefits all our key stakeholders, including our tenants and investors.

As a Vukile stakeholder, you too will benefit from our extensive analysis of shopper behaviour and the factors that drive continuously evolving retail trends.

There has never been a better time to invest in people like Gemma B.

BUILDING COMMUNITIES, GROWING VALUE.

Peregrine Capital had an exceptional year, despite the unpredictability of global and local markets. CEO and Portfolio Manager Jacques Conradie shared his insights with MoneyMarketing on what contributed to their success.

“The beauty of this job,” Conradie says, “is that you hardly ever know what a year is going to bring at the start. Almost every year, unexpected events occur, and they provide opportunities. Our job is to keep our eyes open and look for those opportunities.”

Peregrine Capital’s strong performance and AI insights

Reflecting on last year’s performance, he highlighted two major themes: the South African market and the global AI-driven tech boom. “We did quite well out of South Africa, realising before the election that valuations were very attractive. The sentiment was extremely negative – people were worried about loadshedding and political uncertainty. But when negativity is already priced into the market, opportunities arise.”

Peregrine Capital strategically positioned itself ahead of the South African elections, anticipating potential upside regardless of the outcome.

“Even if the election had gone badly, we still saw upside because valuations were so low,” Conradie explains. “Fortunately, the election played out well, and we now have the Government of National Unity (GNU).”

The market implications of AI

Discussing the broader investment landscape, he notes, “The way AI is playing out reminds me of past technological revolutions. When the internet emerged, it gave rise to companies like Amazon. When mobile took off, it propelled Facebook and Apple.”

Conradie believes AI’s momentum will continue. “AI will keep skyrocketing. Our job is to ensure we don’t overpay for these investments and monitor how new entrants impact the market. However, in general, this benefits the companies we own.” On a broader scale, he sees AI as a key battleground for global superpowers. “The AI arms race between the US and China will define the next 20 years. The Trump administration understands this and is highly pro-US tech companies. While previous administrations imposed regulatory pressures, Trump will likely support major tech firms, which is a positive for our portfolio holdings.”

Discussing the rapid advancements in AI, Conradie highlighted the impact of emerging players like DeepSeek on the industry. “What DeepSeek has done is remarkable. They’ve demonstrated that a smaller company with a smart team can release a model almost on par with the largest AI firms, despite having significantly fewer resources and a much smaller budget,” he explains.

The rise of such companies could have implications for tech giants like Nvidia. “For a business like NVidia that makes AI chips, this could be a short-term negative if people decide to use more efficient models that lower demand for high-end hardware. However, this development is quite positive for most AI-driven companies,” says Conradie.

He remains optimistic about AI’s trajectory. “Even with new competition, AI remains a gamechanger. Companies like Meta, one of our major holdings, use AI extensively for ad targeting and content recommendations. If they can reduce costs while maintaining efficiency, that’s a significant advantage.”

South African market outlook

Conradie expresses cautious optimism about the South African market. “Investors must always balance the outlook with stock prices. The outlook was uncertain a year ago, but share prices were low, often presenting a good investment opportunity. Now, while the economic outlook is slightly better, valuations for retailers and banks have risen significantly, making them less attractive than a year ago.”

He points to economic factors that could shape the market in the coming months. “Interest rate cuts will help, and the economy received a boost

with a recent R43bn of two-pot withdrawals from pension funds. However, that tailwind will fade, so we need to see whether economic momentum continues. Loadshedding has improved, but economic growth hasn’t picked up as much as some had hoped. We remain watchful.”

US-South Africa relations

Geopolitical developments, including US-South Africa relations and potential trade disruptions, are on Conradie’s radar. “The US’s stance on South Africa is something to monitor. It’s never good to have the world’s largest economy scrutinising your country. Our government should prioritise resolving any tensions to avoid prolonged uncertainty.”

Investment agility

Peregrine Capital prides itself on pivoting quickly when market conditions change. “One of our biggest strengths is that we can adapt fast. We have a small, agile team of 13 analysts, and if there’s a major market event, we immediately convene, debate the impact on our portfolio, and reposition accordingly,” Conradie explains. “For example, when DeepSeek entered the market, we had an early-morning strategy session to assess how this would impact the AI value chain. We did the same when Covid-19 hit. Our ability to move quickly is core to our investment philosophy.”

Keeping the competitive edge

The company recently expanded its team, reinforcing its competitive position. “We’re always on the lookout for top talent to enhance our research capabilities. The ability to make fast, informed decisions is critical, and having the right people in place ensures we maintain our edge,” says Conradie. As global markets continue to evolve, he remains committed to flexibility and strategic positioning. “We’re not stuck to any opinions – we hold strong views but remain extremely adaptable. If the data changes, we adjust accordingly. That’s how we stay ahead.”

What COFI will mean for hedge funds

Compiled by Sandy Welch

Over the years, South Africa has taken significant steps to regulate its hedge fund industry, aiming to enhance transparency, protect investors and ensure financial stability.

Back in April 2015, South Africa became the first country to formally regulate hedge funds as collective investment schemes under the Collective Investment Schemes Control Act (CISCA). This integration aimed to align hedge funds with the regulatory standards applicable to traditional investment funds, enhancing oversight and investor protection. The regulations introduced two primary categories of hedge funds:

• Retail Investor Hedge Funds: Designed for the general public, these funds are subject to stringent regulatory requirements to safeguard less experienced investors.

• Qualified Investor Hedge Funds: Targeted at institutional and high-net-worth investors with a minimum investment requirement of R1m. These investors are presumed to have a deeper understanding of the associated risks, allowing for a more flexible regulatory approach.

As of June 2023, the South African hedge fund industry managed assets totalling R120bn, up from R113bn at the end of 2022. This growth indicates a steady net inflow

and a slight increase in the number of funds, reflecting a growing investor interest in hedge funds. To mitigate systemic risks, regulations impose specific limits on hedge fund managers, including a 200% gross exposure cap, a 20% one-month Historical Value-atRisk (HVAR) limit, and a 30% cap on single positions. These measures are designed to ensure prudent risk management within the industry.

The impact of COFI

The Conduct of Financial Institutions (COFI) Bill is set to introduce a new licensing framework for ‘alternative investment portfolios’, which includes hedge funds. This initiative aims to address the unique risks associated with diversified pooled investments, further strengthening the regulatory environment. COFI is poised to significantly impact South Africa’s hedge fund industry, but it’s primarily aimed at enhancing market conduct and consumer protection. Key implications include: