Market Update

Our purpose

To create a place where we can facilitate our people’s growth.

To create a place where we can facilitate our people’s growth.

Our colleagues are our broader family, assist when needed and when in need

Mutuality

Respect our colleagues and our clients as you would like to be respected

Embrace change

Strive for excellence; be open minded and willing to embrace change

Realising potential

Unlock your full potential, encourage and support your colleagues

Health and energy

Work towards being well balanced within yourself

Dean O’Brien

Unfortunately, Melbourne’s property market continues to fall In September, the median value for combined homes dropped by 0 1%, according to Corelogic. Nationally, property values went up by 0.4%. Most of Melbourne’s losses in the last 12 months happened in the last three months, with values dropping by 1 1%

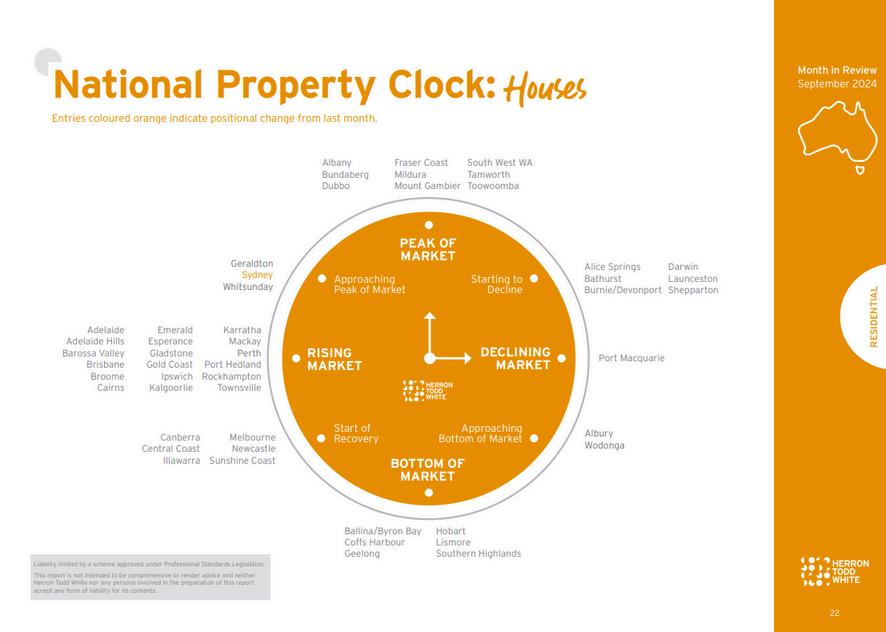

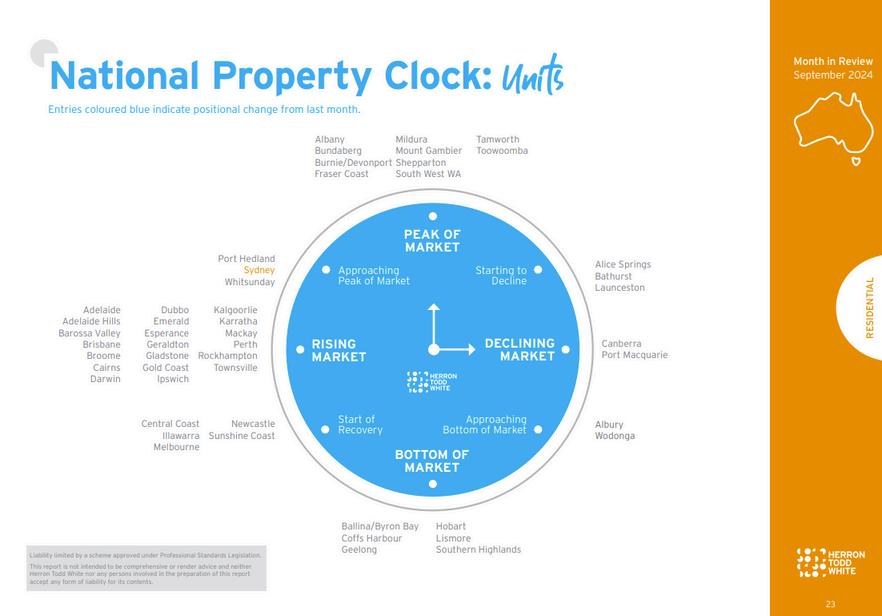

Recently, the PropTrack Housing Affordability Index showed that households across Australia can afford fewer homes than ever before A typical household earning just over $112,000 a year can afford only 14% of all homes sold Looking at the graph below, you will see that this is the lowest share since 1994-95. Three years ago, a median-income household could afford 43% of homes sold In Melbourne, people can only afford 12% of the homes Melbourne is the third most expensive capital city in the country. Even though property prices in Western Australia have grown by over 24% in the last year, it remains the most affordable state to buy in For homes to become affordable again, incomes will need to rise significantly.

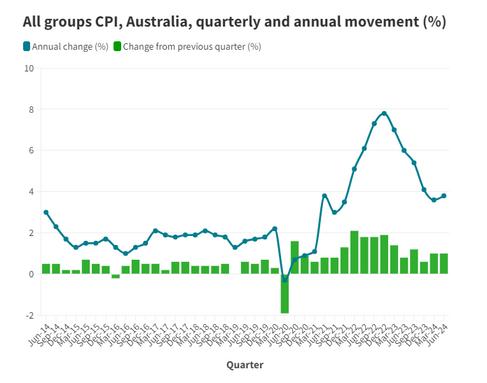

Inflation for August was released last week, showing 2 7%, down from 3 5% in July This is the lowest inflation reading since August 2021 Lower inflation sounds like good news for future interest rates, which may help people afford loans But there might be less credit available, as the Reserve Bank of Australia (RBA) warned in its September Financial Stability Review The RBA is concerned that if households take on too much debt, it could make the property market more unstable

Looking at the graph below, Melbourne is last in growth and property values among the five most expensive capital cities. The total annual change in median values for combined homes has fallen by 1 4% Houses have dropped an average of $7,519 over the last 12 months, while unit prices have stayed the same

Finally, the Australian Bureau of Statistics just released data on building approvals for August Nationally, approvals fell by 6 1%, and in Victoria, they fell by 3 0% That’s all for this month. Please remember that the information provided is general, and you should always get independent legal, financial, or tax advice for your specific situation

Regards

Dean O’Brien

Step 1: Assessment

Simply call and speak to our experienced Growth Specialist who will review and assess, collecting some information to commence the hand over process

Step 2: Authorise

At this stage, we will gather all required documentation authorising our team to take over the file and begin an in depth analysis of your property

Step 3:

OBrien Real Estate hand over We take it from here, managing contacts, assessments, and file transfers We'll also liaise with your tenant for inspections or introductions

$730,000

$1,050,000 - $1,150,000

$930,000 - $1,020,000

$560,000 - $615,000

$730,000 - $803,000

$800,000 - $880,000

$730,000 - $800,000

$975,000 - $1,035,000

$600,000 - $660,000

$575,000 - $630,000

$670,000 - $710,000

$720,000 - $770,000

$760,000 - $810,000

$750,000 - $820,000

$485,000 - $505,000

$1,665,000 - $1,745,000

$480,000 - $525,000

$1,300,000

$780,000 - $848,000

$460,000 - $500,000

$480,000 - $525,000

$660,000 - $720,000

$770,000 - $825,000

$487,000 - $535,000

$899,000 - $939,000

$1,700,000 - $1,800,000

$930,000 - $990,000

$650,000 - $710,000

$560,000 - $575,000

$950,000 - $999,000

$790,000 - $868,000

$750,000 - $825,000

$1,140,000.00

$930,000 $930,000 $650,000 $690,000 $1,140,000 $1,050,000 $620,000 $800,000 $850,000 $775,000 $990,000 $688,000 $616,000 $687,500 $755,000 $775,000 $765,000 $490,000 $1,600,000 $480,000 $1,300,000 $905,000 $490,000 $516,500 $700,000 $775,000 $528,000 $910,000 $1,715,000 $935,000 $672,000 $565,000

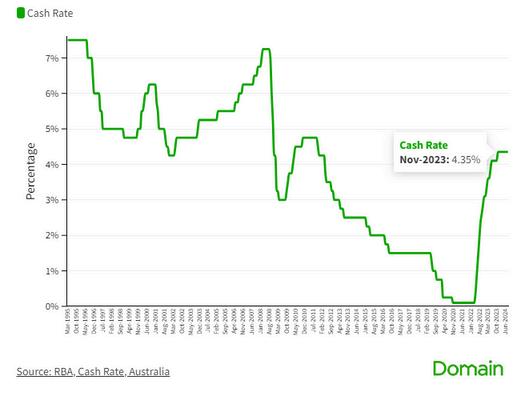

The Reserve Bank of Australia (RBA) has held the cash rate at 4 35 per cent, despite June quarter consumer price index (CPI) figures showing an uptick in inflation

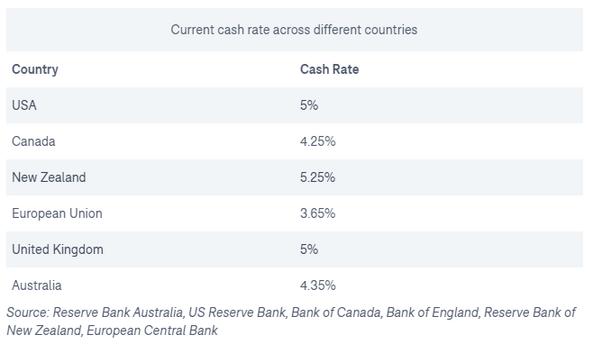

While it may be frustrating to see other countries like the United States cutting interest rates, economists say Australia’s sticky inflation figures mean our cash rate will stay on hold until the RBA hits its 2 to 3 per cent target

“There are a couple of reasons why the RBA has chosen to hold,” says PRD real estate chief economist Dr Diaswati Mardiasmo

“When it comes to our inflation rate, it’s still quite high It hasn’t come down as much as the RBA would like it to, and in their forecast, they’re forecasting that there might be a couple more rises in our inflation rate ”

RBA interest rate rises and cuts

Cash rate target, Australia

“If we were to cut and then go back up again, it would shock the economy even more because then people would feel that they have more money and might spend more Then inflation will go up even further, and the RBA will be forced to increase the cash rate again,” says Mardiasmo

“That sort of economic effect is going to be worse for us Whereas keeping it steady right now is keeping everything stable with the possibility of a cash rate cutting down the line ”

The quarterly CPI, an indicator of inflation, rose by 1 per cent in the June 2024 quarter, and annual inflation rose to 3 8 per cent, above the RBA’s 2 to 3 per cent target, but well below its December 2022 peak

“The annual rise of 3 8 per cent for the June quarter is up from 3 6 per cent in the March quarter,” says Australian Bureau of Statistics (ABS) head of prices statistics Michelle Marquardt

“This is the first increase in annual CPI inflation since the December 2022 quarter ”

The most significant contributors were housing, food and non-alcoholic beverages

“The continuing tight rental market and low vacancy rates caused rental prices to go up 2 per cent for the quarter, following a 2 1 per cent rise in the March 2024 quarter,” says Marquardt

Sean Langcake, head of macroeconomic forecasting at BIS Oxford Economics, says: “The RBA is kind of choosing between two bad things here They could have tolerated this inflation running a bit hot for a while, which is what they’re doing, or they had the choice to take interest rates even higher, which would have put more people out of work

“It’s not like they’ve chosen to tolerate this inflation without thinking of alternatives It’s just that it’s been deemed to be the best of bad options,” he says

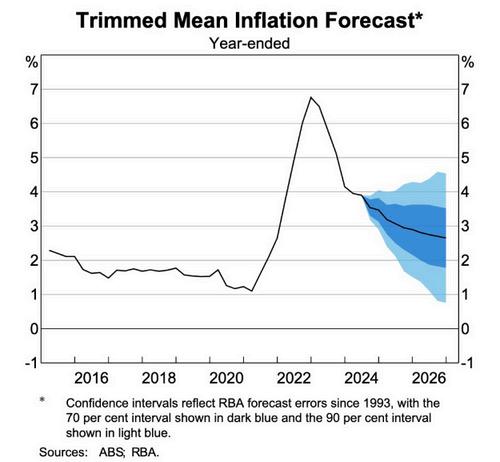

In the August 2024 Statement on Monetary Policy, the RBA said inflation targets will take longer to reach than previously calculated in May

“Underlying inflation is expected to be inside the target range of 2 to 3 per cent in late 2025 and approach the midpoint of the band in 2026,” said the statement

“It is a difficult balancing act Inflation is still a bit too high, but we are now seeing signs of weakness in the economy,” says Ray White Group chief economist Nerida Conisbee

“We are not in recession but have now seen three quarters of almost zero growth Unemployment is creeping up and now sits at 4 2 per cent ”

This prolonged hold period is “the stability Australians are looking for,” says Domain chief of research and economics Dr Nicola Powell “A cut is unlikely to happen until next year But this stable environment is great for confidence as well We’ve seen that in terms of sellers listing their homes ”

The most recent Domain Market Insights revealed new listings have increased by 13 1 per cent in the past month and 8 1 per cent annually

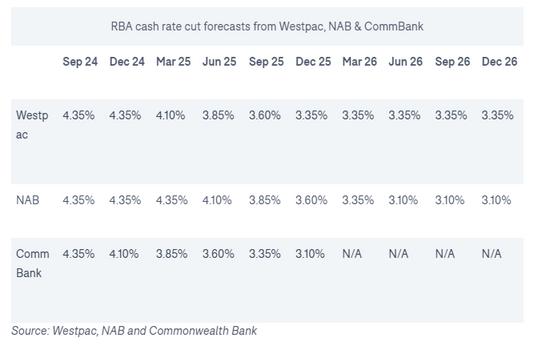

While today’s announcement was a hold, three major banks forecast that the first RBA cash rate cut will come in 2025 Commonwealth Bank estimates that it’s still possible to see a rate cut by the end of 2024

“Compared to other countries, the RBA clearly didn’t go as hard on bringing things back to earth. That’s why we have higher inflation for longer, but it’s also why we have a jobs market that’s in better shape,” says Langcake.

Last week the US Federal Reserve cut the cash rate for the first time in four years by 50 basis points to 5 per cent, despite US inflation not reaching its 2 per cent target. Other global markets like Canada, New Zealand and the EU have also cut their cash rates.

“The US and Canada, EU and all of the other countries, they increased their cash rate much quicker than we did. We were lagging behind them,” says Mardiasmo.

“The US and New Zealand increased their cash rate about three to six months before us If you look at it from that time frame, it makes sense that we’re also three to six months behind in cutting the cash rate ”

A country cutting the cash rate before hitting its inflation rate is a matter of timing to boost its economy, says Conisbee

“The US economy is just looking so weak [compared to Australia],” she says “The balancing act between not destroying the economy and keeping inflation under control is quite a delicate balance

“The US must have come to the conclusion that it’s better to just give it a bit of a boost, as opposed to continuing to try and get inflation within that target level ”

For those desperate for a rate cut, Langcake says patience is key because cash rate impacts come with a lag “If we’re patient and kind of ride it out, then the fact that inflation is slowly coming down is going to help with cost of living pressures,” he