AN IDEAL LOCATION FOR OIL AND GAS EXPLORATION

South Africa’s strategic geographical location, proximity to major shipping routes, and well-developed financial sector, alongside an abundance of indigenous natural resources, combine to present an ideal location for onshore and offshore oil and gas exploration

Writer: Lily Sawyer | Project Manager: Josh Edwards

Poised to capitalise on growing market opportunities, South Africa’s (SA) positioning within sub-Saharan Africa renders the country a well-established industrial base for upstream and midstream oil and gas exploration.

In fact, this sector has seen some development over the past decade, whilst the country’s infrastructure, skilled workforce, and well-established ports make it a prime industry location.

SA’s relative proximity to major international shipping routes and hydrocarbon deposits to the west and east of Southern Africa further enhances its appeal as a logistical hub for the broader African oil and gas space.

As such, the South African government has started to recognise the untapped potential of its resources and begun to implement policies to attract international investment and foster local industry growth as a result.

With the advent of advanced exploration technologies and a global push towards energy diversification, the country anticipates a surge in exploratory and developmental operations.

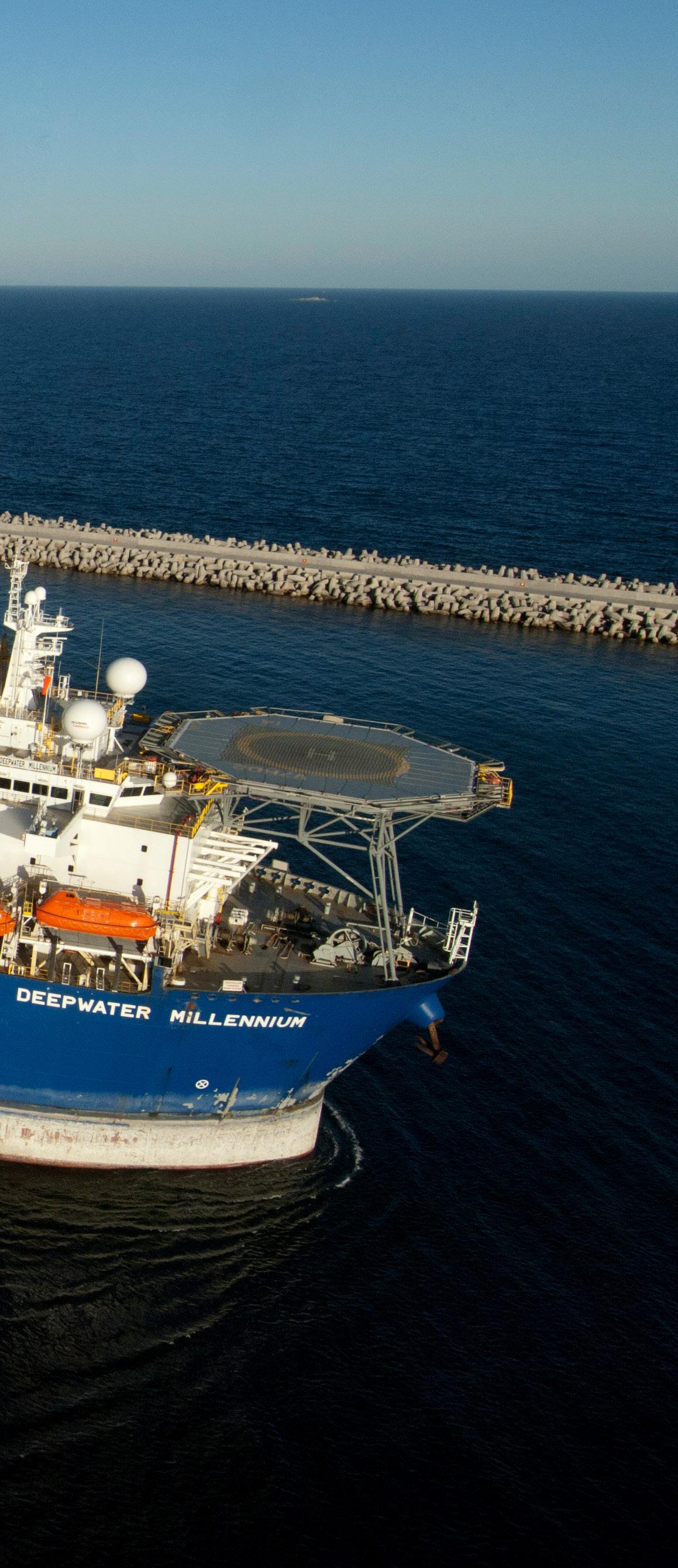

Therefore, although offshore activity is currently heavily focused in West, East, and Central Africa, increased activity off the coast of SA is expected to occur within the next few years.

Furthermore, the country’s well-developed financial sector and regulatory framework provide a stable environment for both foreign and domestic investors.

Meanwhile, as the global energy landscape evolves, the region’s oil and gas sector is expected to play an increasingly important role in meeting the continent’s energy needs. Its anticipated expansion is also likely to stimulate economic growth, create job opportunities, and enhance energy security not only for SA but also neighbouring countries.

It is hoped that this growth will additionally drive technological innovation and infrastructure development, further solidifying SA’s position as an important regional player.

Adrian Strydom, CEO of the South African Oil & Gas Alliance (SAOGA), outlines the overall goals of the organisation and provides commentary on how the region requires increased energy security to remain an attractive investment location

Africa Outlook (AO): Firstly, could you talk us through the origins and primary goals of SAOGA?

Adrian Strydom, CEO (AS): SAOGA celebrates its 21st birthday this year. We serve the interests of our members and the industry in the upstream and complementary midstream oil and gas and energy sectors, primarily in SA and regionally

across Southern Africa.

The organisation operates as an industry body, carrying out a range of development activities to promote the interests of SAOGA members.

It is overseen by an independent volunteer Board of Directors from within the sector, alongside a number of other key stakeholders.

Our aim is to be a primary industry body, servicing the upstream and midstream sectors of the oil and gas and energy value chain across Southern Africa, attracting investment and developing capacity within the region to service and supply the oil and gas industry with goods and services for the benefit of all stakeholders and our valued members.

We seek to play a key role in developing the industry by providing our members with a comprehensive platform, driving the growth of oil and gas and energy entities through aggregating relevant local and regional intelligence, facilitating networking events, capacity building, compiling knowledge, and maximising government, institutional, and private business resources.

We do this in close collaboration with industry and government partners.

Our popular industry events, conferences, and missions will continue to serve as important vehicles for networking and promoting the goods and services of our members.

Skills development and capacity building initiatives will stay in sharp focus well into the future as SAOGA is registered as a Joint Action Group with the Department of Trade Industry and Competition.

AO: What is your current take on the oil and gas industry in SA?

AS: The South African oil and gas landscape is both challenging and exciting. Whilst the country is relatively underexplored, several promising oil and gas discoveries have been made in the past. Therefore, we owe it to our people to continue with the exploration and production of our natural resources, particularly given the recent challenges with power outages that have demonstrated the need to focus more sharply on energy security.

AO: Who is SAOGA’s membership open to and what are its key benefits?

AS: Our member companies are the primary and preferential beneficiaries of all our activities, therefore we exist primarily for our members.

Their involvement and feedback is key and provides an opportunity to become part of a collective voice for the industry. Members help in working with public and private sectors to improve the overall competitiveness of the oil

and gas sector.

Both corporate entities and individuals can become members of SAOGA. Where relevant, company employees will receive the benefits of membership afforded to individuals.

SAOGA has historically had a two-tier membership structure, with an associate membership level open to all interested companies and a full membership level open to a subset of qualified organisations who meet defined quality and competence criteria.

Any institution, legal entity (private or public), individual, partnership, or firm that provides goods and services across the upstream and midstream oil and gas and energy industries can join SAOGA, as can members of the ship repair and boatbuilding sector, logistics, and other related industry value chains.

The alliance’s member companies form part of a searchable database, providing additional online exposure for members.

SAOGA is actively engaging with the industry, government, and stakeholders to promote participation in the following projects:

• SA offshore: Exploration activity off the coast of SA is expected to ramp up in the next 18 to 24 months.

• SA onshore: Onshore exploration for natural gas is continuing.

• Sub-Saharan Africa offshore: Offshore activity in Namibia is expected to continue, whilst significant growth can be anticipated from offshore activity in East Africa.

Offshore exploration:

• Northern Cape Ultra Deep (NCUD) exploration.

• Deep Western Orange Basin (DWOB).

• DWOB straddles the borders of Namibia and SA, with 60 percent of it on the South African side. This holds huge potential for the country’s oil and gas industry.

Onshore exploration:

• Kinetiko, Renergen, and D3 had several onshore discoveries.

• Renergen is producing helium and progressing to Phase 2.

• Kinetiko is about to drill appraisal wells.

• D3 has drilled exploration wells.

Future floating storage and regasification units (FSRUs) envisaged:

• Richards Bay will be starting with a floating storage unit (FSU)

Future pipelines envisaged:

• Orange Basin – Saldanha Bay

• Hydrogen Projects

• Pipeline from Namibia

• Lilly pipeline upgrade

• Secunda pipeline link

AO: How does SAOGA’S strategic geographic position provide a distinct advantage?

AS: Recent years have seen a dramatic increase in Southern African exploration activities. For example, Namibia, Mozambique, and Angola are making huge strides in oil and gas discovery.

SA is in a favourable position to support regional oil and gas exploration and production. More coordination and collaboration with these countries will optimise economic benefits for the region.

Our location also means that SAOGA’s industry missions give members access to regional business and networking opportunities.

AO: How extensively does SAOGA contribute, advise, and comment on policy, legislation, and regulatory frameworks which may affect the oil and gas industry?

AS: Legislative and regulatory certainty and clarity are key for investment attractiveness. We have unfortunately seen TotalEnergies recently indicate that it may not continue to develop its offshore exploration activities in the 11B/12B exploration block in Mossel Bay.

How can the South African Government of National Unity (GNU) turn this around? We need energy security and financial incentives –renewable energy alone will not cut it. The TotalEnergies of the world will simply opt to go elsewhere if the region does not become an attractive investment location.

The South African gas market is confronting a pivotal challenge: the decreasing supply from established gas fields in Mozambique. This decline, projected to impact availability between 2026 and 2028, underscores the urgency for alternative energy solutions to safeguard our country’s energy security. In this context, the importation of liquefied natural gas (LNG) emerges as the most viable solution to meet the substantial energy demands of our industrial sector, particularly given the existing pipeline infrastructure that South Africa already possesses.

However, the transition to LNG is not without its complexities. It necessitates considerable investment in port infrastructure, meticulous contract management, and a strategic approach to aggregating market demand to ensure the viability of LNG on a large scale. These are significant undertakings, but they are essential to the continued resilience and growth of our energy sector.

At SLG, we are acutely aware of these challenges and are committed to leading the charge in this energy transition. With over 23 years of industry experience, our comprehensive action plan is designed to facilitate a seamless shift to LNG, underpinned by our unwavering commitment to innovation, collaboration, and sustainability. Our objective is clear: to secure a robust and reliable energy future for our customers and the broader South African economy.

Our strategy is ambitious yet grounded in the realities of the market. SLG aims to aggregate 100PJ/a of gas and secure

the necessary Gas Supply Agreements (GSA) and Gas Transportation Agreements (GTA) by 2026. Drawing on our experience as a direct importer of gas from Mozambique, we are well-positioned to manage the upstream commercial risks associated with sourcing LNG, ensuring that we can offer our customers a supply that is both reliable and costeffective.

Collaboration is at the heart of our approach. By working closely with infrastructure owners, we are aligning demand profiles with infrastructure planning, ensuring that LNG supply integrates seamlessly into South Africa’s existing pipeline network. This includes active engagement in the development of LNG port infrastructure and the crucial connections to the transmission network.

Furthermore, through our subsidiary, SLG Power, we are spearheading significant gas-to-power projects. These initiatives are not only critical drivers of gas demand but also pivotal to the broader energy transition within South Africa. They represent our commitment to leveraging LNG as a cornerstone of our country’s future energy landscape.

SLG is unwavering in its dedication to the sustainability and growth of the natural gas industry in South Africa. As we look to the future, with LNG at the forefront of our strategy, we are confident in our ability to navigate the challenges ahead and to continue our journey as a leading energy partner in the region.

switchboard: +27 (0)31 812 0555 direct: +27 (0)31 812 0561 www.slgas.co.za

In addition to offshore and onshore projects, SAOGA is actively monitoring the delivery of oil and gas and hydrogen operations and related infrastructure development in South Africa and in the region.

SOUTHERN AFRICAN REGION:

• Namibia - Offshore and Onshore exploration and appraisal drilling by TotalEnergies, Shell, Galp, Sagittarius (Rhino), Chevron, BW Offshore are increasing rapidly.

• Mozambique - Mozambique has the third largest gas reserves on the continent.

• Tanzania - Tanzania is expected to become a significant gas producer.

• Uganda – The Uganda-Tanzania Crude Oil Pipeline project is making steady progress.

• Export potential to SA and the world is rapidly increasing.

• Hydrogen projects in Namibia are progressing well.

• LNG infrastructure development will increase rapidly over the following years.

• African Continental Free Trade Agreement-related programmes will increase.

• Gas and hydrogen pipeline infrastructure will be needed.

• The export potential of gas and hydrogen will increase.

SOUTH AFRICA:

• A gas-to-power request for proposal (RFP) was released for 2 gigawatts (GW) electricity supplyDecember 2023.

• An integrated resource plan (IRP) issued for 7.2-8.6 GW gas-to-power - January 2024.

• A draft Gas Masterplan was circulated for commentApril 2024.

• A draft Oceans Economy Masterplan to serve on parliament shortly.

• A proposed Richards Bay LNG Terminal - A Transnet National Ports Authority (TNPA) procurement process identified a Vopak lead consortium as the preferred bidder.

• President Ramaphosa is expected to sign the Upstream Petroleum Resources Development (UPRD) Bill into law soon.

SAOGA is an important stakeholder and actively involved with the government’s master-planning processes. We have made extensive legislative submissions to government departments, parliament, the presidency, and the National Council of Provinces (NCOP) on behalf of our members in the past and will continue to actively do so.

AO: Are you optimistic about the future of the oil and gas industry in SA?

AS: I am very optimistic. Gas is not only a transitional fuel in the future of energy in SA but an accepted European Union (EU) norm. In our case, it is also an enabler of renewable energy and an ideal supplement to solar and wind power.

It is important to note that more economically developed countries have gas readily available, which they can switch on when needed.

However, this is not the case in Africa. We have a totally different prevailing scenario that is not always understood, and the gas market and infrastructure in the continent are relatively underdeveloped.

Invariably, SAOGA member companies are also active in the renewables industry.

At the risk of stating the obvious, hydrogen is a gas. As such, pivoting from natural gas to hydrogen, if necessary, would be a relatively easy transition.

Therefore, I believe we should take a hydrogen-ready approach that will help SA to develop a balanced energy mix, although the importation of liquid natural gas (LNG) will be necessary in the interim.

Meanwhile, Africa will see significant population growth over the next 50 years, while the population of the rest of the world, except for China, will plateau.

Africa is energy-poor, yet we have a growing energy market ahead of us, and it is for this reason that we need to plan accordingly.

AO: Finally, what are SAOGA’s key priorities to continue serving the interests of upstream and midstream oil and gas sectors in Africa?

AS: SA must create an attractive environment for investment. The new GNU has its work cut out to facilitate this. It is not going to happen automatically – an intentional commitment and a strong partnership with industry is needed.

SAOGA has clearly indicated its willingness to support the GNU in co-creating an SA we want to live in and do business in – the nation and wider region has huge potential.

I believe the GNU is well placed to make a difference

“WORLD-CLASS SKILLS AND INDUSTRY CAPACITY BUILDING ARE NEEDED REGIONALLY, AND SAOGA WILL CONTINUE TO PLAY A KEY ROLE IN THIS RESPECT”

–

ADRIAN STRYDOM, CEO, SOUTH AFRICAN OIL & GAS ALLIANCE

in the lives of our people by making the country more attractive for the exploration of resources that we have been abundantly blessed with.

Further to this, energy security, industrialisation, and local oil and gas exploration and production are gamechangers in the war against unemployment and poverty in SA and the wider region. As such, SAOGA will continue to pursue opportunities to promote collaboration and develop the oil and gas and energy industry locally and regionally.

We have a critical role to play to help provide credible information about the sector and responsibly negotiate the path to net zero carbon emissions, without destroying opportunities for industrialisation, economic development, and job creation.

SAOGA will continue to lobby government to improve investment attractiveness and enhance legislative and regulatory certainty.

Ongoing engagement with communities that are

affected by exploration activities is also required to provide them with reliable information. SAOGA can play an important role in this sense as a trusted industry body, capable of building relationships with co-users of areas under exploration.

World-class skills and industry capacity building are needed regionally, and SAOGA will continue to play a key role in this respect.

A survey we did before the COVID-19 pandemic clearly indicated that appropriate skills will invariably translate into employment creation. We found that of the 2,000 beneficiaries who benefitted from SAOGA’s apprenticeship programme, 96 percent were gainfully employed.

This programme was rolled out in partnership with Technical and Vocational Education and Training (TVET) colleges, Sectoral Education and Training Authorities (SETAs), and government.

Tel:+27 21 425 8840 | info@saoga.org.za www.saoga.org.za