16 Is China the next stop for Pakistan’s meat exports?

22 Saudi Arabia confirms $1 billion investment into Reko Diq, diluting Pakistan’s ownership to less than 50%. What about the logistical challenges?

25 Dewan Farooque Motors revival: is it real this time?

26 Bilal Fibres, a bankrupt textile mill, wants to launch a TikTok competitor

28 Can Retailo’s SaaS gamble pay off?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

TBy Abdullah Niazi

wo years. That is how long the Punjab Government has to phase out the wheat support price it issues every year. It is a subsidy addiction that has afflicted the entire country since at least 1968, but Punjab has year in and year out been the biggest offender.

The death knell for Pakistan’s massive wheat subsidy programme was sounded by the International Monetary Fund, which announced in early September that provincial governments would be barred from setting crop prices as part of its $7 billion bailout package, board approval for which Pakistan secured only a few weeks ago. It is possibly one of the reasons why the Punjab Government has abolished the provincial food department, replacing it with a new autonomous body.

The wheat support price is a bigger problem than one might realise. The concept behind wheat procurement is that the government buys wheat from farmers at a set rate which is higher than what they would get on the market so they continue to grow what is a strategically important crop. The problem is, provincial governments borrow heavily from commercial banks to fund these operations.

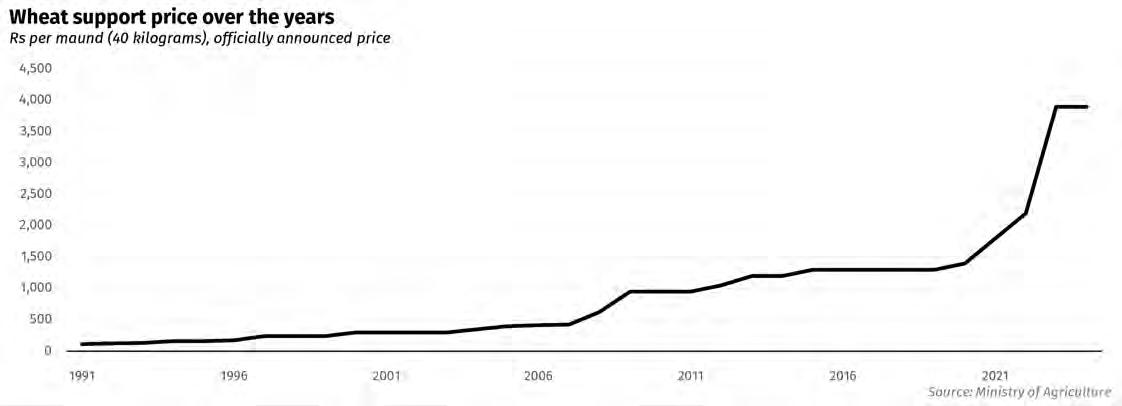

In 2023, for example, the wheat procurement target was 40 lakh tonnes and the government had set a price of Rs3,900 per maund (a unit of measuring weight equal to 40 kilograms), or around Rs97.5 per kilogram. To buy this much wheat from farmers at this rate, the government would need around Rs394 billion. Now, the government sells the wheat they acquire to flour mills at this rate so they do recover this money. However, the government relies on borrowing this sum from commercial banks. At an interest rate of 23% in 2023, the government would be paying around Rs90 billion in monthly instalments of 10 months through selling wheat to flour mills. The government also always procures more wheat than it needs and consistently has leftover grain from previous years in storage.

On top of this, the government also needs to spend tens of billions of rupees on handling, transportation and storage costs incurred by the PASSCO on a federal level. The government regularly fails to live up to its commitment with commercial banks, and over time, this has led to circular debt. In 2020, this had risen to Rs757 billion.

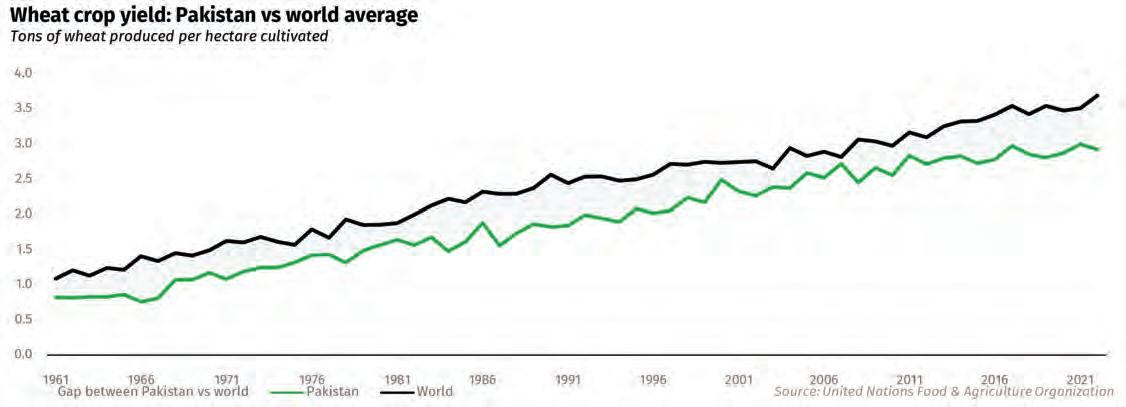

Why then do we insist on having these wheat support prices every year? The government will tell you that their aim is to give confidence and provide security to poorer farmers, as well as get cheap flour to the markets. They are lying. All indicators and an impressive body of academic literature on the topic tells us leaving crop prices up to market forces is what is best for farmers.

Farmers would make more money without a wheat support price, even though they have become heavily dependent on it. But breaking that habit might be a good thing. The removal of the wheat support price will allow farmers to possibly look towards other crops as well, and if the government moves on allowing GMO crops such as maize and corn, it can prove to be a gamechanger.

But before we get into that, it is important to understand the nature of the problem and how deep that runs. And that requires answering a basic question: How does the current wheat procurement system work?

The centrality of wheat in Pakistan’s economy

What is today modern Pakistan is the result of the British Empire’s appetite for wheat.

The British constructed railways in what is now Pakistan in 1855, in no small part due to a desire to connect the wheat-growing parts of Punjab and Upper Sindh to the port in Karachi.

In 1886, the British were able to start building the Punjab Canal Colonies, which were a series of large, previously sparsely inhabited areas in Punjab, that were brought under cultivation through the use of canals that diverted water from the province’s five rivers. Those canals allowed for previously landless and poor farmers to settle in newly cultivable regions, and the railways helped them sell their surplus crop to the rest of the British Empire.

The British would begin building similar infrastructure for Sindh and Balochistan in 1923, with the construction of the Sukkur Barrage.

With the completion of these large rail and irrigation projects, the volume of commerce between Punjab and Sindh, in particular, exploded. On the eve of the First World War in 1914, Karachi had gone from being a small town on the coast of the Arabian Sea to becoming the largest grain port in the British Empire, and Punjab had become its principal bread basket. Karachi’s significance to the world was as the entrepot that provided access to Punjab’s wheat.

So central is wheat to Pakistan’s conception of itself that it is one of the four crops in the State Emblem (the other three being cotton, tea, and jute; the latter two were the principal crops of East Pakistan, but we will not spend too much time on that awkward remnant of history).

Yet despite this centrality of wheat, at independence, Pakistan’s population had grown so rapidly that it became a net importer of wheat. Indeed, a major initial bone of contention in the Cold War was the race between the United States and the Soviet Union to supply Pakistan with wheat. Between 1949 and 1952, nearly all of Pakistan’s wheat imports came from the Soviet Union. The US considered it a major foreign policy victory to get Pakistan to accept imports from the United States from 1953 onwards.

Within Pakistan, however, the reliance on imported wheat was seen as a national embarrassment, and one of the handful of the successful policies initiated by the preAyub governments was to embark on a program to help Pakistani farmers improve the quantity of wheat produced in the country. By the latter half of the Ayub era, the government succeeded.

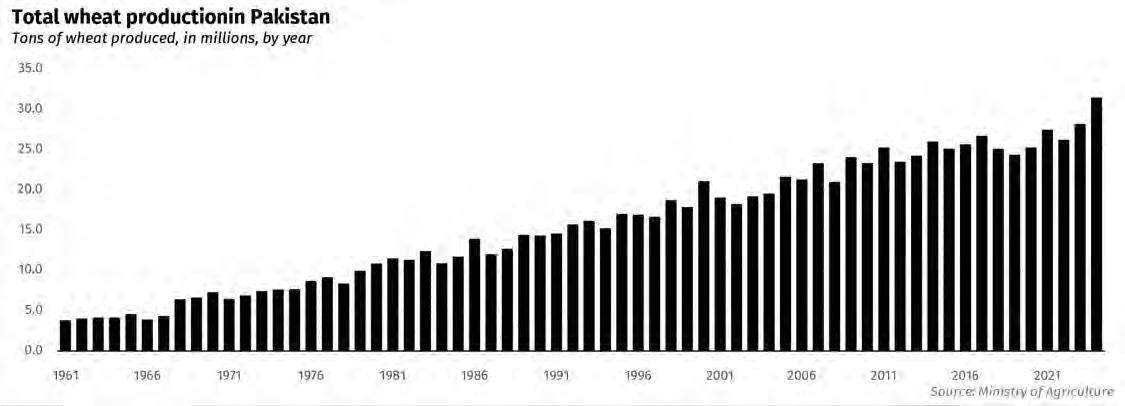

As a result of this, in 1968, Pakistan had a massive increase in wheat yield. This was the second year running this had happened, and farmers were struggling because the markets had not cleared all of their crop. This was a little embarrassing for the government, which had incentivised growing more wheat since at least the early 1960s to account for food security. Wheat makes up nearly a third of the caloric intake by an average Pakistani, and Pakistan’s per capita consumption of wheat is 124 kilograms annually, which is the highest in the world.

The government decided they would buy the excess wheat from the farmers and store it for a rainy day. This would give the farmers a buyer, their crop would not go

to waste, and they could reliably plant it again next year. This was a slippery slope. Gradually, the government became the principal buyer and the private sector’s role shrank. To keep flour prices low for poor households, it established an extensive network of ration-shops, which provided subsidised wheat flour to low-income households. The ration system was abolished in 1987 due to partial targeting, inefficiencies and corruption.

The ration system was replaced with a subsidy on wheat issued to flour mills by the government from its procured stocks. Thus, a targeted subsidy was replaced by a general subsidy that ultimately became far more expensive than the one it replaced. The twin requirements of clearing stocks during harvest season and providing subsidised wheat to flour mills later in the year led the government to procure progressively larger volumes of wheat each year.

The next big change came in 2008, when the 18th amendment was passed and the provinces were made responsible for setting procurement prices and getting the wheat. This is where the current system in Punjab comes into play. How does it work?

Bureaucratic hell

In Punjab, the government’s wheat procurement system is a bureaucratic labyrinth designed, in theory, to support small farmers by purchasing their wheat at premium prices. But in practice, it is a spectacle of inefficiency, political patronage, and frustration, where the people it is supposed to help are often left out in the cold—sometimes literally, since the wheat they grow has a better shot at being stored under plastic sheets than fetching a fair price.

Remember, of all the wheat that Pakistan produces around 60% of it is consumed by the growers either directly or for seed purposes. Of the remaining 40%, the government consumes

around the lion’s share leaving only around 10% that sells directly to flower mills which give much lower prices than the government gives.

Every year since 2008, the Punjab Food Department (PFD) purchases about 18.6% of the province’s wheat production. However, the system is not tied to actual needs, like the production levels or what flour mills demand. No, the PFD often buys just enough to ensure its granaries are stocked to the brim, with significant leftover stock gathering dust—and storage costs—year after year. This inefficient hoarding occasionally results in millions of tons of carryover wheat, as was the case in 2009 when the PFD procured 5.78 million tons, resulting in 2.93 million tons of carryover stock the following year. The price tag on storing all that wheat? Huge. And it is the kind of inefficiency that makes a small farmer’s heart sink.

For the farmers, especially the smallholders for whom this system is supposedly built, the journey begins with an infuriating step: getting their names on the patwari list. This list, managed by local land record officials, is the golden ticket to even start the procurement process. But if you are a tenant farmer—or worse, a politically unconnected one—good luck. Tenants are often left off the list, thanks to landowners who do not want them included, and the unholy trinity of bureaucracy, politics, and poor record-keeping means even legitimate farmers frequently find their names missing. Sure, you could technically appeal, but that means preparing tenancy agreements (many of which are verbal) and making endless rounds of government offices. For most, it is easier to sell their wheat at a loss to middlemen than try to fight the system.

Once you have made it past that hurdle, you are handed another one: bardana, the jute or polypropylene bags that you must use to supply your wheat. The bags are rationed out by PFD, and like so many things in the wheat

procurement system, who gets them depends less on their crop yields and more on their connections. Well-connected farmers can secure them swiftly, while others wait in agonisingly slow-moving queues. For the average farmer, this means navigating a carefully cultivated system of political favours to ensure a steady supply of bags, all while paying a deposit at a bank (Rs134 per jute bag or Rs38 for polypropylene) before the bags can even be issued. The entire back-and-forth between procurement centres and banks can stretch out for days or weeks.

Once the bardana is secured, it is a race against time. Farmers who have their bags filled must transport them to their designated procurement centres. This requires renting a trolley—an expense most small farmers can ill-afford—since only the largest farms have the means to transport all of their stock at once. An average trolley can carry 100 bags, but many small farmers do not produce enough wheat to justify multiple trips. And even those who manage to get their wheat to the centre face a gamble: not all centres have a weighbridge, so a random 10% sample is weighed, meaning some unlucky farmers find themselves shortchanged during the process.

The worst part? Farmers have to bear all transportation costs and labour expenses. Casual labour at these centres is hired to help unload the bags, stitch them, and weigh them, and while PFD offers a Rs. 9 per bag reimbursement for labour, they don’t cover the costs of filling or stitching the bags or transporting them to the centres in the first place. Farmers are left holding the bill for this, on top of the 5-6% losses that occur in open storage—losses that PFD is happy to shove off onto them.

And let’s not forget the waiting. PFD likes to spread out its procurement operations from mid-April to the end of May, with each farmer being assigned a preferred delivery date.

On paper, it should take five to six hours to complete the transaction, but in reality, it can take far longer. If you show up early or late, or if the centre’s having a busy day, you could be stuck for an entire day without compensation for your time. And should the centre’s storage hit its unofficial target early, it might just stop procuring, leaving the less-connected farmers out in the cold.

Even when they do manage to sell their wheat, the payment process is another grind. For smaller consignments, farmers might get cash on the same day. But if they’ve sold more than 50 bags, they receive a slip, which means yet another trip—this time to a designated bank. By the time all is said and done, a farmer may have visited the procurement centre three times and the bank twice, burning between seven and ten days just to get paid. And for what? A system that claims to support small farmers but makes them jump through hoops, wasting valuable time they could spend on the next planting season. The losses pile up— whether in the form of the 1 kg per maund PFD shortchanges during delivery or in the form of delayed payments that stop farmers from paying off debts or ploughing their fields in time for the next crop.

For small farmers strapped for time and cash, the option to sell at lower market prices to intermediaries becomes increasingly appealing. Farmers often need quick cash to settle debts, rent tractors, or pay for inputs like fertiliser and seeds for the next planting season. As one farmer put it, “I had only 15-20 days after the wheat harvest during which I had to plough my land to clear it of weeds and to get it levelled. I do not have a tractor, so I rent it. But I can either rent one before everyone else needs them or after they’re done. I can’t possibly make the rounds to banks and food centres.”

In bumper years, like 2017 and 2018, the government’s incompetence shines even

brighter. Unable or unwilling to buy all the wheat, the PFD conveniently adopts a “goslow” strategy, rationing bardana to only a select group of politically favoured farmers. The rest are left in a queue that moves so slowly, they are forced to sell their wheat to private traders at lower prices. In those years, market prices hovered between Rs1,100 and Rs1,250 per maund, while the government price was Rs1,300. But with the government sitting on massive carry-forward stocks and reluctant to buy, only the well-connected made it through the system.

In the end, what should be a safety net for small farmers becomes an entangling trap. A web of bureaucratic red tape, political patronage, and inefficiency forces them into a system where they are chronically shortchanged. They look up to the PFD for aid, but all they receive are delays, lost wages, and mounting frustrations. At every turn, they face a system designed to exclude the very people it claims to serve, leaving them with little choice but to sell at a loss or spend days navigating a bureaucratic maze. If anything, the wheat procurement system feels less like public intervention and more like a slow-motion betrayal of the people who feed the nation.

So who benefits?

Data for wheat procurement is not updated, with the latest collected information available up to 2020. That is why in our explanation we focused so much on the 2018-19 season, which marked the 10 year mark since the Punjab government began this operation on its own.

What becomes clear is that farmers are not benefitting from this. Data on wheat production by farm size in Punjab shows that 13.3% of farms do not produce wheat at all. Of the 86.7% farms that produce wheat (comprising 63.7% of the total area of private farms), 90.5% percent are smaller than 12.5 acres. This

means 78.5% of total farms producing wheat are small farms. These farms are only 40.5% percent of the total farm area and 63.6% of the area of farms reporting wheat. Very small farms of less than one acre do not sell wheat because they do not have a marketable surplus.

Data on wheat production by farm size are not available, but assuming that they produce at the national average of 800 kg wheat per acre and consume wheat flour at 140 KG per person, with an average household size of 6.3, they produce less than their own consumption even when they allocate the entire area to wheat production. Together, non-wheat-producing farms and very small farms are 22.2% of all farms in Punjab.

Then who is benefitting from this? One answer might be commercial banks. On paper, the Punjab Food Department’s (PFD) subsidy structure is meant to stabilise the market, protect farmers, and deliver cheap wheat flour to consumers. In reality, it is more of a balancing act on a tightrope of debt, where the government throws money around with one hand while borrowing furiously with the other. And as you might expect, it is the farmers—and the taxpayers—who ultimately bear the cost.

The subsidy system is straightforward in its premise: PFD buys wheat from farmers at a price that is often higher than the open market and then turns around to sell it to flour mills at a below-market rate. The idea is to keep flour prices stable, prevent market crashes that would hurt farmers, and provide cheaper wheat flour to consumers. On one front, it works—PFD has largely succeeded in smoothing out seasonal price fluctuations, reducing volatility, and keeping flour prices from skyrocketing (a win in a country where food inflation can lead to serious political unrest). But that is about where the good news ends. Take 2017-18 as an example. That year, PFD’s wheat operations racked up a staggering cost of Rs.34.4 billion, with the bulk of this

cost (over 70%) attributed to something that has little to do with actually feeding people: bank mark-up. The PFD borrows money every year to purchase wheat, and while it manages to sell that wheat to flour mills, the government never quite gets around to repaying the entire amount. Instead, it kicks the can down the road, paying off only part of its debts and leaving the remainder to accumulate. This results in PFD not only having to pay interest on its current loans but also on its mounting, unpaid liabilities. For the past five years, this interest alone has averaged Rs19.6 billion per year—just the cost of borrowing money to keep the wheels of wheat procurement turning.

This enormous financial burden has not stopped the government from charging ahead with its operations. PFD continues to borrow from a consortium of banks every year, and the amount it borrows always exceeds what it manages to repay. On paper, this looks like a government subsidy helping farmers, but in reality, the system is bleeding money. Since 2008, except for a couple of rare years, PFD has borrowed more than it has repaid, with no real plan to clear the outstanding debt.

The Punjab government, meanwhile, allocates a modest Rs10 billion each year for wheat operations, knowing full well that this amount is just a drop in the ocean of what is actually needed. The unspoken agreement seems to be that the government will pay off only the interest on the loans (or at least part of it), while the debt continues to balloon in the background.

This cycle of debt does not just hurt the government—it adds to the frustrations of farmers who are already navigating a flawed procurement system. While the government likes to boast about the high prices it offers to farmers, those prices come with significant caveats. In years when the open market price is higher than the official price, PFD imposes

bans on inter-provincial wheat movement to force farmers to sell to them. So, the small farmer—already boxed in by bureaucracy and patronage games—finds himself trapped once again, this time forced to accept a lower price because the government needs to meet its procurement targets.

What about the end consumer?

And this is what it comes down to. How expensive is atta for you and me sitting in our homes in urban centres. The government would like to argue that due to their procurement wheat becomes cheaper. It is an argument that has been very succinctly refuted by Ahsan Rana, a professor at LUMS, in a paper he wrote a few years ago:

“Will the price of wheat flour rise by the amount of subsidy if PFD stops wheat operations? Certainly not. Instead, flour prices may decrease due to two reasons. First, in the absence of public intervention, the wheat price will fall at the harvest time and traders will stock up at these low market prices. Second, the private sector’s wastage and storage/ transportation costs will be lower than PFD incidentals. Thus, mills’ net cost will be lower than it is in the current interventionist regime. What will be the net effect if PFD procures wheat but without having to pay interest on the piled-up outstanding debt? Data shows that borrowing in 2017 accounted for only 36.6% of the total PFD debt. If PFD had to pay mark-up only on its borrowing for current operations, its incidentals would be correspondingly less. Adjusting the mark-up gives us a figure of Rs. 205 per 40 kg for PFD incidentals, where there is no outstanding debt. If PFD procures wheat at the official price and if it pays mark-up only on new borrowing, its cost price of wheat at the time of issuance to flour

mills will be Rs(1,300 + 205.19 =) 1,505 per 40 kg. If PFD provides no subsidy at the issuance of wheat, cost of flour will increase by Rs205 per 40 kg; if it provides subsidy at the current level (viz. Rs. 379 per 40 kg), cost of flour will decrease by Rs(205.19 - 379 =) 173.81 per 40 kg, ceteris paribus. In other words, consumers are paying Rs173.81 extra per 40 kg for Punjab government’s failure to retire its outstanding debt.”

It shows in the receipts

All of this points towards why wheat procurement has been such a consistent problem in Punjab. Perhaps nothing points towards this better than the billion dollar wheat import scandal of 2023-24 that the Punjab and federal governments are still suffering from.

It is the latest chapter in Pakistan’s broken wheat procurement system—an emblem of everything wrong with how the country handles its most essential crop. In this case, the ruling Pakistan Muslim League-Nawaz (PML-N) found itself embroiled in internal tensions over how to address a scandal that is as much about political manoeuvring as it is about financial mismanagement. Former Prime Minister Nawaz Sharif pushed for strict accountability against the caretaker government that oversaw the import of 1.2 million tonnes of surplus wheat. However, his brother, current Prime Minister Shehbaz Sharif, hesitated, reluctant to implicate members of his own coalition, including those with ties to the establishment.

The roots of the scandal go back to a bureaucratic blunder that allowed wheat imports far beyond what was necessary to compensate for the 2022 floods, allegedly driven by kickbacks to the caretakers. The result?

A staggering loss of over $1 billion in foreign exchange at a time when Pakistan’s economy

is in shambles, coupled with Rs300 billion in losses for farmers, who were left struggling to sell their wheat amid a surplus and crashing prices. Meanwhile, flour millers and traders are believed to have reaped enormous profits at the expense of both the government and the agricultural sector.

The handling of this scandal—and the broader wheat procurement process—has been chaotic. While the government set up inquiry committees, they have been hesitant to fully investigate key figures in the caretaker government. The Punjab government’s response to farmers’ protests was heavy-handed, deploying force to quell dissent rather than addressing the root cause of their grievances: a procurement system that is deeply flawed.

This scandal is not an anomaly—it is symbolic of a wheat procurement system plagued by inefficiency, cronyism, and an inability to balance the needs of farmers with broader economic realities. From bloated subsidies to reckless imports, Pakistan’s wheat policy has long been a patchwork of short-term fixes that only serve to deepen the long-term problems. By 2024, the situation had deteriorated even further, with wheat imports crashing domestic prices and leaving farmers in financial ruin—exactly the kind of breakdown that has come to define the country’s toxic relationship with its agricultural sector.

So what now?

Well, the good thing is that the provincial governments will have to do something about removing the wheat procurement system because the IMF has said so. It will be politically difficult, and they might drag their feet, but they will not really have much of an option if Pakistan is to keep looking towards the IMF to survive for the foreseeable future.

What will be interesting to see is how the farmers react. For many decades they have

become used to procurement and government prices. And in the future, it might be a little worrying for them to plant as much wheat as they once would. Some fear this could lead to a food security issue given how much of a caloric input wheat has on the Pakistani population. However, farmers may also end up turning towards other crops such as canola, mustard, sunflower, chickpeas, and maize. There could also be a resurgence in cotton, which has seen its fate suffer thanks to a shift towards sugarcane. However, such a significant change will require Pakistan to rationalise its attitudes towards GMOs. Take Maize as an example, and incredibly versatile crop that can have very high yields with the right seeds. Presently, Pakistan exports around $13 million worth of maize and/or its derivative products; of these, less than $3 million products are exported to Kenya (with existing trade restriction on GM maize) by Rafhan, which is 1% of Rafhan’s total sales. Sourcing non-GM maize grain in Pakistan for exports to non-GMO countries can easily be made possible, resulting in zero impact on export trade. It is estimated that such exports will require less than 30,000 tons of maize grain as raw material; a quantity easily available from KPK Province where white corn is planted. However, a majority of

But Pakistan has a huge block when it comes to considering GM foods.

The reality is that farmers and agricultural scientists have been involved in genetically modifying the food we eat for a very long time. “For many decades, in addition to traditional crossbreeding, agricultural scientists have used radiation and chemicals to induce gene mutations in edible crops in attempts to achieve desired characteristics,” reads an article by Jane Brody published in The New York Times back in 2018.

“Although about 90% of scientists believe GMOs are safe — a view endorsed by the American Medical Association, the National

Academy of Sciences, the American Association for the Advancement of Science and the World Health Organization — only slightly more than a third of consumers share this belief,” states a report from the United States Food and Drug Administration (FDA). And that is the crux of the problem. Even though the scientific evidence is overwhelmingly in the favour of GMOs, the public perception of GMOs is unfavourable.

This is mostly coming from the same brand of pseudo-science that promotes homoeopathic remedies over actual, tested, medicine that works and peddles crystal therapy and all manners of snake-oil. Robert Goldberg, a plant molecular biologist at the University of California, Los Angeles, says that such fears have not yet been quelled despite “hundreds of millions of genetic experiments involving every type of organism on earth and people eating billions of meals without a problem.”

Meanwhile, the benefits from GMOs have been authoritative. By engineering resistance to insect damage, farmers have been able to use fewer pesticides while increasing yields, which enhances safety for farmers and the environment while lowering the cost of food and increasing its availability. Yields of corn, cotton and soybeans are said to have risen by 20% to 30% through the use of genetic engineering. Similarly in the case of Maize, provision for GM seeds would drastically increase yields and give farmers in a post-procurement Pakistan a crop that would make for very good farm economics. This is because there is a wall to how high yield can get just by improving farming practices and mechanising, something that is already difficult in a country like Pakistan where farmers do not have easy access to credit. The government has essentially been forced into getting rid of their decades old wheat subsidy. Only time will tell if they will take the opportunity to go in a direction that is good for farmers and the country. n

Is China the next stop for Pakistan’s meat exports?

Can Pakistani meat find another destination besides the GCC?

By Hamza Aurangzeb

Pakistan’s meat industry stands at a critical juncture, facing both significant challenges and promising opportunities. Despite being a major producer of meat, with an output of 5.809 million metric tons in 2024, the country’s export potential remains largely untapped due to structural issues plaguing the sector. These challenges range from the absence of a robust livestock traceability system to the prevalence of Foot and Mouth Disease (FMD), and from the lack of large-scale feedlots to the persistence of informal, undocumented supply chains.

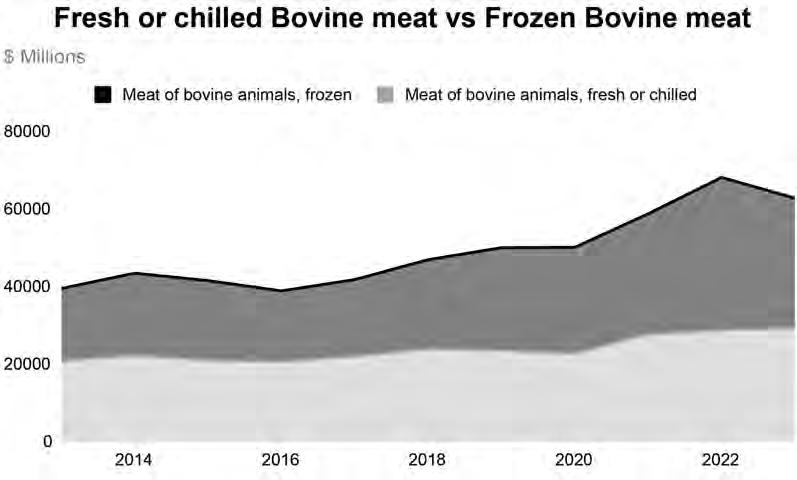

However, amidst these obstacles, a ray of hope emerges in the form of Pakistan’s strategic geographical position and its growing presence in niche markets. The country has carved out a significant market share in the Gulf Cooperation Council (GCC) countries, particularly in the fresh or chilled bovine meat segment. This success, while noteworthy, also highlights the need for diversification as global meat consumption trends shift towards frozen and processed products.

The recent breakthrough of The Organic Meat Company Limited (TOMCL) in the Chinese market serves as a testament to the untapped potential of Pakistan’s meat industry. This development opens up new avenues for Pakistan’s meat sector, but does it have the potential to convert Pakistan from a regional player to a global competitor?

Structural Issues in Meat Supply

Numerous structural roadblocks hinder the growth of Pakistani meat exports. The first one is the traceability of livestock. It is an arduous task to trace animals due to the absence of a basic tagging system along with a national livestock database.

Farmers in Pakistan are not interested in meat production on a mass scale; therefore, they are reluctant to purchase expensive tags and related equipment. Moreover, the development of infrastructure for a tagging system needs substantial investment, which would increase costs of meat production significantly, leading to lower profit margins specifically for small-scale farmers who work informally.

The entire meat value chain in Pakistan is for the most part undocumented, informal and highly fragmented, governed by an archaic arthi-based system, which further complicates the task of traceability, due to the unavailability of animal

sales records and history of animals like birth, vaccinations, and genetics.

Secondly, Foot and Mouth Disease (FMD) is prevalent across livestock in Pakistan due to flimsy veterinary infrastructure, which fails to cater to livestock in rural areas, where most of the livestock is concentrated. Furthermore, the lack of a national FMD control programme, scarcity of disease-free zones and inadequate ability of the government to track livestock have exacerbated the situation.

High-income markets like the United States, European Union, and Japan require meat exporting countries to demonstrate that they are a country free of FMD or have contained the spread of FMD through stringent controls, however, in case of the latter the country needs to ensure that the meat exported is only from FMD free zones and complies with food safety standards like HACCP (Hazard Analysis Critical Control Points). Since Pakistan fails to meet these standards its meat exports to these markets are minimal.

Thirdly, farmers in Pakistan only sell livestock for meat production when it is unable to work in the fields and its milk yield falls to negligible levels. Therefore, there is a dearth of large-scale feedlots or fattening farms. Furthermore, most of the country’s native breeds constitute milk breeds, which have poor feed conversion rates, resulting in low average carcass weight and low meat yields. The average carcass weight in Pakistan is 130 Kg/animal, therefore, slaughtering the buffalo would only get the farmer Rs.130,000, while an average buffalo produces milk for a decade resulting in earnings above Rs. 2.5 million for the farmer.

Lastly, we observe rampant smuggling of livestock across the border into neighboring countries, Iran and Afghanistan, which reduces its supply in the domestic market, resulting

in increased prices of livestock in the country. The government imposed a complete ban on the export of live animals in July 2013 to stabilize the prices of live animals in the domestic market, however, the ban has had little to no impact on the smuggling of live animals.

Landscape of Pakistan’s Meat Exports

Although the above-mentioned structural issues impede the growth of meat exports of Pakistan, meat production for the domestic market continues at a massive scale. Pakistan produced around 5.809 million metric tons of meat in 2024, where 2.630 million metric tons of beef, 2.362 million metric tons of poultry meat, and 0.817 million metric tons of mutton were produced.

Most of the animals in Pakistan are slaughtered at unregistered and unregulated slaughter slabs, slaughter houses, and abattoirs. Such facilities typically lack hoisting facilities, a lighting system, and a regular water supply. Hygiene standards are often ignored, while both wet and solid waste disposal are poorly managed.

On the contrary, we have 34 Animal Quarantine Department approved slaughterhouses that focus on exports for international markets. These facilities encompass imported machinery along with expert labour and accredited financing. According to the Board of Investment (BOI), these facilities are estimated to be operating at 25% to 40% of their peak capacity due to insufficient livestock raised for meat production and limited access of Pakistani meat exporters to international markets. The output of these

Source: International Trade Centre

facilities could be doubled or tripled if their access to international markets is enhanced.

The export-oriented facilities follow stringent hygiene requirements and quality standards including traceability of meat, unlike unregulated slaughter houses. This increases their production costs, restricting their ability to compete in the domestic market, increase production, and diversify their portfolio, resulting in the concentration of meat exports in particular segments.

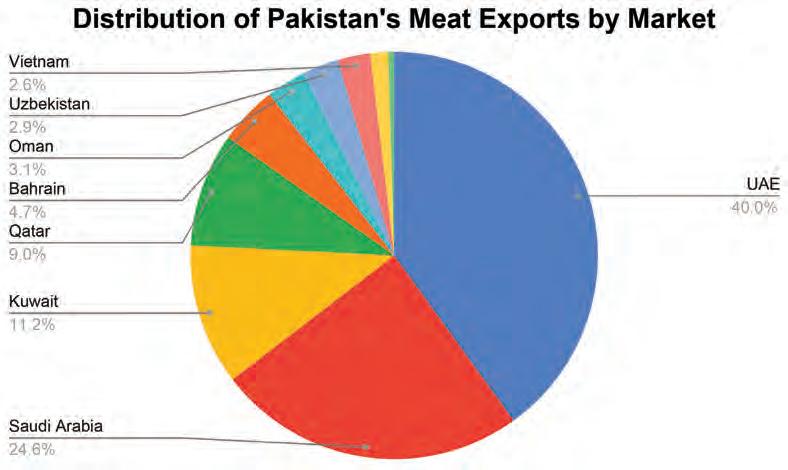

Pakistan’s meat exports are limited to only a handful of markets that permit the import of its meat despite the prevalence of FMD in its livestock. Pakistan’s export destinations are led by six GCC countries, which include the United Arab Emirates, Saudi Arabia, Qatar, Bahrain, Kuwait, and Oman. These countries account for $444 million (92.7%) of Pakistan’s total meat exports, while 88% of Pakistan’s meat exports are concentrated in the category of fresh or chilled carcasses and half carcasses for both beef and mutton, with beef and mutton representing shares of 82.3% and 17.7%, respectively.

Source: International Trade Centre

segment. As per the estimates of 2021 by the Pakistan Business Council, air freight of fresh and chilled meat to the Gulf costs around $1 to $2 per Kg, while sea shipments cost only $0.2 per Kg.

The country’s proximity to the GCC gives it a competitive advantage in supplying halal fresh and chilled carcasses at a reasonable rate to the region. Moreover, Pakistan is increasingly exporting its fresh and chilled meat to the region through sea rather than air in order to be more competitive in the

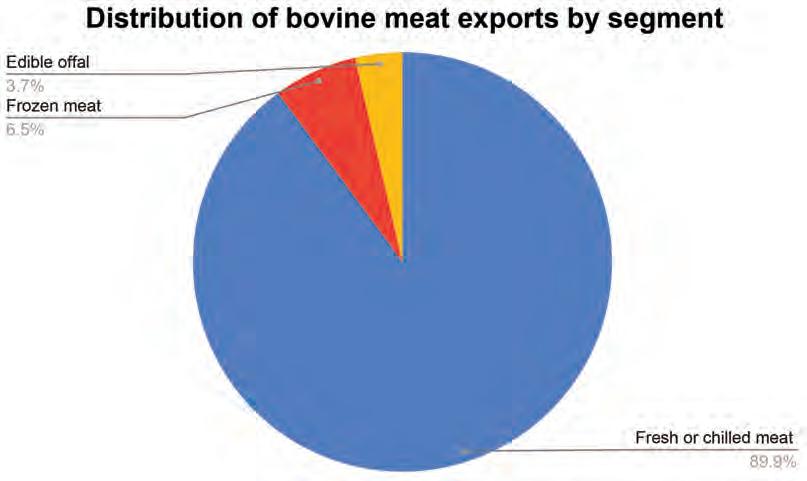

Pakistan is the largest supplier of fresh or chilled bovine meat to the GCC countries, it controls a market share of around 45%. Fresh or chilled carcasses of bovine meat exported to GCC countries amounted to $348.417 million, approximately 72.7% of the total meat exports of Pakistan in 2023. Nevertheless, this moat is limited to the segment of bovine meat products that have not been processed further like carcasses, half carcass -

es, and cuts with bone in. Pakistan has no share in the space of boneless fresh or chilled bovine meat segment.

When it comes to frozen meat, Pakistan has limited operational capacity. Moreover, since frozen meat has a longer shelf life, it is feasible for countries to import from anywhere in the world, disarming Pakistan of its advantage of being in the vicinity of the GCC.

Local meat processors in Pakistan fail to outdo their international competitors like Brazil and India due to high production costs led by high costs of animal sourcing and low meat yield. According to estimates, Pakistan’s production costs are $4/Kg for exports of frozen meat, whereas India produces the same products at $3/Kg. The price competition is even more intense in the frozen market segment.

Source: International Trade Centre

The country managed to only export frozen meat worth $11.276 million to the GCC region and $26.954 million across the globe in 2023. Frozen bovine products amounted to 25.528 million (94.7%) out of the total and were primarily supplied in the form of carcasses and boneless meat which held shares of 51.2% and 34.8% of the total frozen bovine meat exports. Apart from that, Pakistan also managed to export frozen mutton products worth $1.426 million, which was dominated by the boneless category, making up 88.6% of the total frozen mutton exports.

But why should Pakistan be

worried even if its meat exports are highly concentrated in the category of fresh and chilled carcasses of bovine meat in the GCC region? Let’s find out.

The Growing Transition towards Frozen Meat

Well for starters, fresh and chilled carcasses of bovine meat is a declining market segment on a global scale, it represents only 3.8% of the total global bovine meat imports. Although Pakistan has developed a strong foothold for the category in the GCC region, the depletion of the segment on a global scale is a matter of grave concern for Pakistan. Moreover, an emerging trend which has been observed globally is the transition of consumer demand from fresh or chilled beef to frozen beef products. The overall bovine meat segment witnessed a growth of 4.7% over the past decade but the growth of frozen bovine meat segment outpaced the growth of fresh or chilled bovine meat segment. The frozen bovine meat segment represents a share of 53.4% whereas the share of fresh or chilled bovine meat hovers around 46.6%.

Source: International Trade Centre

The global demand for bovine meat is highly concentrated in the segment of boneless meat including both fresh or chilled and frozen types, it dominates consumer demand which amounts to 82.3% of the total imports of bovine meat. On the contrary, the demand for carcasses, a segment which Pakistan has a

firm grip over, represents a share of only 4.3% of the overall global bovine meat imports This transition is led by the massive demand for frozen meat due to high population growth, rapid urbanization, and increasing per capita income in developing countries, particularly in Asia. Frozen meat products have a longer shelf life and are offered at lower prices to these price-sensitive markets which is made possible by transportation through sea at competitive rates. A conspicuous example of this phenomenon is the neighboring country of Pakistan, China, where a massive increase in demand for frozen meat products has been observed in recent history.

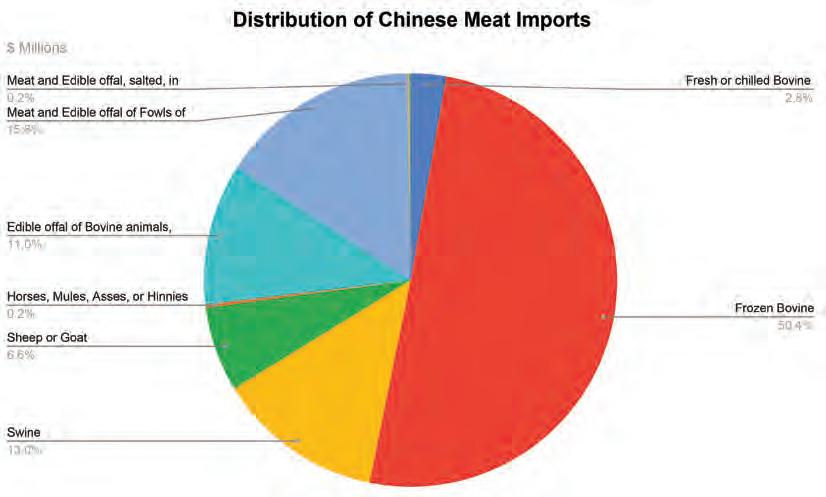

China’s imports of meat products mostly consist of frozen beef, which exceeded $13.4 billion in 2023, as it expanded by eleven times from 2013 to 2023. China imported around 26.735 billion of meat products from around the globe and half of them belonged to the segment of frozen beef in 2023. It imported 2.74 million metric tons of beef in 2023. Apart from this, we are also witnessing considerable demand for frozen beef emanating from East Asia and Southeast Asia. Nevertheless, the largest importers of bovine meat are China, United States, and Japan, which control market shares of 22.6%, 13.6%, and 4.7%. There has been a huge spike in meat consumption in China due to rising income levels, higher disposable income, and a flourishing middle class.

Since the country does not have the capacity to meet its domestic demand, the Chinese government is looking for trading partners to fill this demand gap. Thus, it has granted duty-free access to Pakistani meat products like fresh or chilled bovine meat, frozen bovine meat, and processed meat products such as heat-treated meat under the China-Pakistan Free Trade Agreement II (CPFTA-II). However, the rigorous quality regulations and stringent phytosanitary standards make it unpragmatic for Pakistani companies to export meat to China.

Source: International Trade Centre

Pakistan’s meat exports have immense potential for growth as the country is strategically located in proximity to huge markets like

Note: The CAGR for company’s exports has been calculated in USD.

China, East Asia, Central Asia, and the Gulf, where demand for frozen bovine meat products is increasing rapidly.

TOMCL seizes the Chinese opportunity

Although Pakistan has historically struggled to enter the Chinese meat market, the Organic Meat Company Limited (TOMCL), a publicly listed company involved in the processing, sale and export of halal meat and related products succeeded recently. TOMCL became the first Pakistani company to be granted approval by the General Administration of Customs China in October 2023 and managed to ink a contract of $12 million to export frozen cooked beef meat to China in 2024. Its initial consignments of frozen cooked beef meat have received positive reviews. The exports to

China accounted for 2.1% of the total revenue of the company during 9MFY24.

It is indeed a significant development as the company’s revenue stood at only $22.89 million in 2023. This endeavor will not only allow the company to scale its business verticals but also enable it to establish its footprint in an international market like China which has a growing demand for frozen cooked beef meat products. This partnership perfectly aligns with Pakistan’s meat export strategy and the company’s vision of diversifying its meat products and expanding into new markets.

Assuming the company’s entrance in China will enable it to continue its growth in exports and local sales at breakneck speed which would have slowed down otherwise, the company’s revenue and net income are expected to reach Rs. 32.6 billion and Rs.1.1 billion by 2029.

Source: International Trade Centre

Source: Company Financials

The company firmly believes that this endeavor will generate healthy returns for its shareholders and it has proven to be true thus far as it has provided a return of 50.4% since the beginning of the year when this news was disseminated.

The company has also augmented the production capacity of frozen cooked beef meat by 300 Metric Tons (MT) per month. The company invested a colossal amount of Rs. 600 million to expand its meat chilling and freezing capacities to fulfil the demand of heat-treated/cooked frozen beef meat products from China.

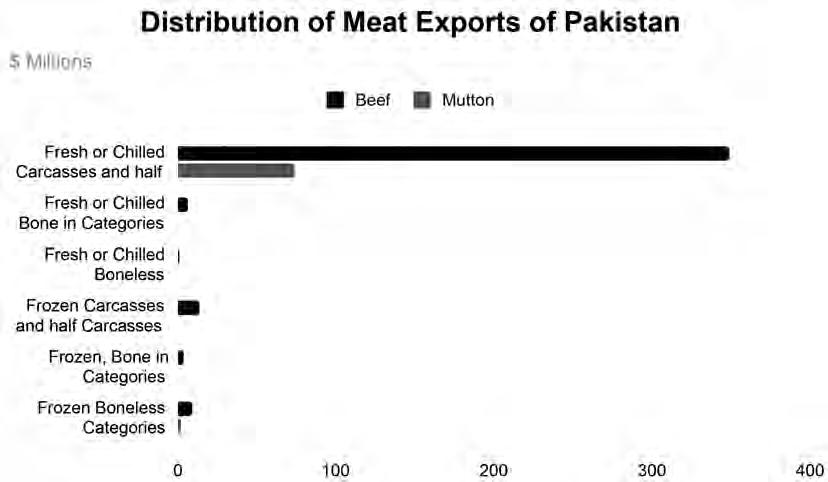

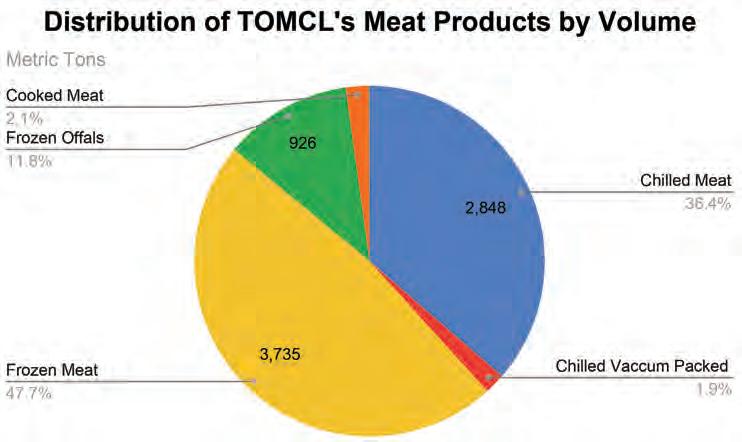

TOMCL is the largest exporter of frozen cooked beef meat to China and one of the only two South Asian companies which have been granted a license by China to export frozen cooked beef meat to its territory The company exports meat products to 18 markets around the globe, where most of its exports are destined for middle eastern countries. However, it has also commenced the supply of pet food material to the US and Europe. Moreover, the company has a decent presence in the Far East, Commonwealth of Independent States (CIS) and South Asian markets. The distribution of company’s meat products by volume is given below.

All in all, the Chinese market presents a mouth-watering opportunity for Pakistani meat exporters. However, a conducive environment for export-oriented meat processing plants needs to be harnessed through the development of a holistic national vision for upgrading the processes of the meat industry. This would not only boost exports but also enable the domestic market to flourish as well. Moreover, meaningful investments need to be made in the industry to raise the standards of Pakistani meat, introduce innovation and diversify meat products, which would allow the country to cash in on this huge opportunity. n

Saudi Arabia confirms $1 billion investment into Reko Diq, diluting Pakistan’s ownership to less than 50%.

What about the logistical challenges?

The Saudi investment is part of the promised $5 billion investment package for Pakistan. It will not solve any of the countless logistical problems that exist in Reko Diq, including transportation and power

By Abdullah Niazi

Saudi Arabia’s Minister for Investment, Sheikh Khalid Bin Abdul Aziz Al Faleh, has confirmed that the Gulf State’s Manara Minerals will invest $1 billion into the Reko Diq Mining project in Balochistan. This comes at a time when the project, which is aiming to have production by 2028, is still facing serious logistical challenges.

The announcement is already being spun by the federal government as a major success. Manar Minerals Investment Company is a new entity created through a partnership between the government’s state-owned Saudi Mining Company (Ma’aden) and the country’s sovereign wealth fund. For all intents and purposes it is a direct investment into Reko Diq by the Saudi Government, which was promised by Saudi Crown Prince Muhammad Bin Salman in April.

The details of the deal are not clear yet, but Saudi Arabia will be buying a minority stake in the project by acquiring part of the Pakistani government’s stake.

Currently, the Reko Diq Project is 50% owned and operated by Canadian mining com-

pany Barrick Gold, which has been involved in the project for many years now through the highs and lows of legal challenges. The remainder of the project is owned 25% by Pakistan’s federal government, and 25% of it is owned by the province of Balochistan.

Logistical challenges

As the project looks to take off, there are some difficulties it will face which the Saudis will be watching closely. The project site is fairly remote and access to shipping is extremely difficult. It is marred by logistical and infrastructural shortcomings, a concern that has always been there. A major challenge, for example, is picking what port to transport the minerals to. From a location perspective, Gawadar Port would make more sense. However, neither does the Gwadar port have a bulk container terminal nor does it have … the optimal amount of ship traffic. Under the present circumstances it would not be feasible for them to use this port, whereas in the long-term plan they would prefer using Gwadar port when the situation improves. Member Planning Commission informed that the commission, under the guidance of the

SIFC, was already working on the connectivity to Gwadar Port to Chaghi District for shipping purposes. However, the proposed route to Karachi is also not easy. Major logistical intricacies become apparent as RDMC plans a branch railway line from Noukandi to the project site (almost 80 kms). This would allow them to use the existing railway infrastructure of Noukandi-Rohri-Karachi.

The RDMC (Reko Diq Mining Company — the entity created to run the project) has in the past expressed support for transporting the load via Railway lines (ML1 & ML3) and exporting it from Port Qasim after studying facilities available there.

The branch railway also requires RMDC to substantially invest in a dedicated rolling stock (locomotives and wagons) and containers. Foreseeing two trains of twenty wagons each per day, increasing to five trains a day, the feasibility study requests crucial data from Pakistan Railway. The problem is more than just the branch railway line. The Secretary of the Railway Board unravelled that there are further complexities on ML1 and ML-3, where a mix of trains, including passengers and freight, congest the ML1. Operational hurdles on ML-3, marked by step gradients limiting

load capacity to 300 tons per train, necessitate a piecemeal transport approach, extending turnaround time by over 10 days and hiking operational costs. Adding to the intrigue, the use of Banking Locomotives, as planned by RMDC, further elevates costs, while the 400-km Noukandi section requires substantial upgrades, with lingering challenges even post-rehabilitation.

The mere distances to Karachi and Gwadar ports from Noukandi, hint at very high potential operating costs if Port Qasim is favoured. The balancing act between existing limitations and long-term aspirations becomes pivotal in finalising the medium and long-term routes. It also does not help that the road options for Reko Diq are deemed unviable due to an overloaded Quetta-Karachi section. The pragmatic alternative points towards utilising the existing railway network, albeit with a hefty $200 million upgrade. Discussions around road connectivity reveal ongoing progress in the Noukandi-Mashkel section’s construction.

The future hinges on the processing of PC-1 for Mashkel-Panjgur and upgrading Panjgur to Gwadar sections, waiting for increased volumes to trigger action. The debate between Port Qasim and Gwadar Port intensifies, considering the operating cost implications over the next 45 years. The direct route from Noukandi to Gwadar Port is significantly shorter than the route to Port Qasim, potentially minimising operational costs. It is important to remember here that a similar problem prevailed in the case of the Saindak silver mine located in Shanghai. The silver ore

extracted from the mine has to be transported 1,127 km from the site to the port in Karachi by trucks. The costs associated with using trucks had an adverse effect on the bottom line and overall feasibility of the project. In a bid to address these challenges, a Sub working group for railway connectivity, having representatives from each stakeholder, has been formed to meet every two weeks, reviewing progress and resolving bottlenecks.

Water and electricity woes

Another historical concern, water supply, continues to be a critical issue.

The Risk Assessment Report from 2007 highlighted water as the project’s “most critical” challenge, emphasising the need for a sustainable water source for the next 45 years in the remote mining location. Developing infrastructure and ensuring a consistent water supply remain formidable tasks. Something that is yet to be revealed by the RMDC. The supply of electricity to the region has also emerged to be another grave concern. Initially requiring 150 MW by 2028, the appetite is set to double by 2031, reaching an impressive 300 MW. Studies present three potential transmission routes to plug into the National Grid. The options range from the Dadu-Khuzdar-Panjgur-Reko Diq line (880 km at $385 million) to the China Hub-Awaran-PanjgurReko Diq line (820 km at $405 million) and the Mustang-Dalbandin-Reko Diq line (530 km at $320 million). All these come at a significant cost that has to be borne by the stakeholders.

After an animated debate, the meeting decided to unbox the technical requirements. The Country Director of the Provincial Disaster Management Committee (PDMC) is greenlit to share the intricate details, from initial and peak transportation volumes to power, gas, and water needs.

Background

The Reko Diq project has been in the works for decades, with Barrick Gold and subsequently the Pakistani government facing serious legal challenges. However, the project was put back in track in December 2022. The closing of the Reko Diq deal seemed like a monumental triumph for Pakistan. The legal hurdles were cleared, and Barrick Gold Corporation enthusiastically declared its commitment to transforming Reko Diq into a world-class mine, anticipating significant economic benefits for both the company and Pakistan.

The project was divided into two phases, with a total projected capex cost of $7 billion, with the first phase requiring $4 billion and the second phase requiring $3 billion. In addition, the project’s total entry amount is $2.2 billion, bringing the entire project size to $9-10 billion.

Annual copper output was predicted to be between 650 and 700 million pounds per annum for the first ten years, increasing to 800 to 850 million pounds per annum when phase 2 is completed. Furthermore, gold production was estimated to be 300,000 to 350,000 ounces on yearly basis for the first ten years (first phase) before increasing to 450,000 to 500,000 oz. following the planned expansion. n

What is the ‘nexus’ between banks, the

SBP

and the govt the IMF is pointing towards?

In its report, the IMF says that 60% of the assets held by the commercial banking sector are government debts.

Profit Report

The recent report by the International Monetary Fund (IMF) on the $7 billion bailout package it has extended to Pakistan contains some truly eye-opening information.

In a very small but well summed up section, the IMF’s report points towards a nexus that exists between the state, the central bank, and the banks they are supposed to regulate. The report points towards a damning statistic. Currently, 60% of the assets held by the commercial banking sector in Pakistan are domestic government debts. This means if we were to tabulate the balance sheets of all of Pakistan’s commercial banks in one place, nearly two-third of their total assets would be money the government owes them and not money they have in their hands.

It is truly bleak. The share of government debt as 60% of all assets is three-times higher than the average for Emerging Market Economies like Pakistan.

How did we get to this place? Well, the banks have been in a very comfortable position for the past few years. In fact, it almost seems they have become unwilling to perform their actual function.

Very basically explained, a bank’s business is to accept deposits from customers and lend funds to other customers. But over the past few years, the interest rate in Pakistan has gone through the roof. Pakistan’s central bank cumulatively raised the policy rate by 15% between September 2021 to June 2023, when it hit an all-time high of 23%. So even though a bank’s business is to accept deposits from customers and lend funds to other customers, with inflation hitting record highs and interest rates still capped at 22%, businesses weren’t exactly lining up for credit. So what do the banks do? They lend to the one entity that does constantly need money no matter what: the government.

Lending to the government is profitable at a time like this. The inherent risks associated with engaging in lending operations, particularly in the current high-risk environment, have also constrained the growth of the banking sector’s credit portfolio. This is reflected in a low Advances-to-Deposit Ratio (ADR) of only 44% as of the end of 2023. This means Pakistan’s banks lent Rs 0.44 for every rupee they received from their depositors in

2023, reflecting a poor state of affairs in private credit. Whereas investment to deposit ratio stood at 91%.

At the end of March 2024, ADR trimmed down to 42% while IDR inched up to 93%. This means that the majority of the deposits with the banking sector are being lent to the government, resulting in crowding out of the private-sector. The government’s never-ending appetite for deficit financing means that the local financial institutions have ample liquidity in the form of benevolent lending by the SBP aka repo transactions. Consequently, the banking sector reported record-high core income and profitability despite high inflation and a 50% tax rate. Commer¬cial banks posted an impressive 83% earnings growth during 2023, with almost all banks recording historic profits. At the same time, some financial institutions increased the size of their balance sheet by multiple times, while other businesses struggled.

As the IMF report also points out, “Persistently high fiscal deficits, coupled with the impact of recent external shocks, has had significant implications for the sovereign-bank nexus in Pakistan. With limited access to external funding government debt has increasingly been taken up by the banking sector.”

What the report also points towards, however, is how interconnected the balance sheets have become between the government of Pakistan, the State Bank of Pakistan (SBP), and the commercial banks. For all intents and purposes, we are stuck in a situation where commercial banks have continued to maintain profitability, in fact make record profits at times, during an economic slump. They have done so simply because the government needs to borrow money, and the SBP is more than happy to provide the logistics.

Of course, this nexus that the IMF points towards was created in a particular environment. And with the fall in the policy rate and changes in the economy, trends have been shifting. Following a sustained period of increasing income, the core earnings of Pakistan’s banking sector took a downturn in the first quarter of 2024, marking an end to a 12-quarter streak of uninterrupted growth, as indicated by a research report from JS Global. This is the first time since the first quarter of 2021 that net interest income (NII) has fallen on a quarter-over-quarter (QoQ) basis. This comprehensive assessment focused on a sample

size of 12 banks, which collectively represent a whopping 85% share of the entire banking sector market. This decline was driven by a decrease in asset yields, while funding costs remained flat.

Of course, the problems do not end there. While banks have seen an increase in deposits, there have not been enough zero-cost deposits for them to feel bolstered by this. On top of this, the government once again decided to drop the Advance to Deposit Ratio (ADR) based income tax on banks.

The ADR has been a contentious issue for the past couple of years. In a bid to force banks to lend more rather than just buy government-backed securities, the government placed an additional tax on any bank with an ADR lower than 50% in 2022. ADR is basically advances (lending) divided by deposits. Banks had to pay a 10% additional tax if the ADR is between 40% and 50%, a 16% additional tax if the ADR falls below 40%, and no additional tax if the ADR is above 50%. This additional tax was applicable on income from federal government securities. This was seemingly a way to encourage banks to lend more and encourage business at a time when the economy has been in the doldrums. But a lot went down behind the scenes, and the banks were able to window dress their accounts to avoid these taxes despite successive finance ministers doubling down on it.

To avoid paying hefty taxes, the banks had no option but to increase their lending. The policy did not last long. In 2023, banks were exempted from this tax as announced in the fiscal year 2024 budget, so that banks had enough liquidity to lend to the cash-strapped government. However, the tax was to be effective in the calendar year 2024. The removal of tax in 2023 resulted in rebound in deposit growth. As per JS research report, deposits grew by 24% year on year in 2023 as compared to 2022, while the ADR dropped to 44%.

And while an ADR tax was initially part of the budget, the banks managed to have the ADR dropped again especially since the government was also planning to borrow heavily in the coming year. For the next fiscal year, the government plans to borrow Rs 24 trillion from banks to service existing debt. Thus, the removal of ADR tax presents a positive development for the government facing a widening fiscal deficit and limited borrowing avenues. n

Dewan Farooque Motors revival: is it real this time?

The perennial problem child of Pakistan’s automobile assembling industry, the company claims to have already begun assembling electric vehicles; is this attempt at a revival real?

Profit Report

In the world of corporate Lazarus acts, Dewan Farooqueue Motors is trying its umpteenth attempt at emerging from a 15-year slumber, claiming to have found the key to resurrection: electric vehicles (EVs). Yes, the same Dewan Farooque Motors that sputtered into obscurity following the 2008 financial crisis is now back, boldly asserting that it is ready to revolutionize Pakistan’s automotive industry by assembling EVs. What could possibly go wrong?

The timing is impeccable—EVs are all the rage globally, and Dewan Farooque seems to be hoping that some of this green energy glow will rub off on its dusty, long-idled facilities. In case you’ve forgotten, this is the company that once sold a smattering of Korean sedans to the Pakistani market – the Hyundai Santro – and light trucks – the Kia Shehzore – before being relegated to the graveyard of defunct manufacturers. Now, they are banking on electric vehicles to reignite their fortunes. If this sounds too good to be true, it probably is.

According to the company, they are working with a previously unheard-of manufacturer named ECO-Green Motors to bring affordable EVs to Pakistan, a country where public infrastructure for electric cars is virtually non-existent, power outages are part of daily life, and consumers are famously wary of new technology. But hey, who needs charging stations when you have enthusiasm, right? Dewan Farooque appears to believe that it can leapfrog over all the obstacles, despite having been inactive for over a decade in an industry that has since moved light-years ahead.

Their bold claims raise a few questions— chief among them: Why now? After 15 years of doing nothing, what suddenly qualifies Dewan Farooque Motors to lead Pakistan’s EV revolution? The company has not exactly been a beacon of innovation or operational success in the past, yet here it is, suddenly ready to compete in one of the most cutting-edge segments of the global auto market. It is a bit like an old flip phone company announcing a comeback by manufacturing the next iPhone.

Of course, assembling cars is not the same

as building a brand, let alone creating consumer trust. Dewan Farooque’s track record isn’t exactly inspiring confidence. After all, when a company disappears from the map for 15 years, people tend to forget it existed at all. But apparently, Dewan’s management is banking on the public having short memories and even shorter patience, hoping that the allure of electric cars will blind everyone to the glaring logistical and operational gaps in this revival.

As for the actual assembly process, details are scant. How does a company that has been out of commission for over a decade suddenly pivot to EV assembly? Dust off the old assembly lines, slap a few EVs together, and hope for the best? The silence on how exactly Dewan plans to overcome the vast technological and supply chain challenges that come with EV manufacturing is deafening.

Then there is the mystery of exactly who is ECO-Green Motors and what is the Honri brand of electric vehicles? It sounds like brand that is plausibly Chinese, like the brands many of its rival auto assemblers have gone into business with. But there is no record of Dewan Farooque’s partner being a major manufacturer of electric vehicles in any country in the world.

And then, of course, there is the financial question. Dewan Farooque Motors was hardly a bastion of fiscal health when it closed shop in

2008. How it plans to finance this grand foray into EVs—an endeavour that even the most established automakers struggle to fund—remains unclear. Perhaps they are counting on the fact that “electric vehicles” is a trendy enough phrase to attract investors who do not bother with due diligence. After all, it is not the first time a company has tried to surf on a buzzword.

And some investors certainly seem to be falling for Dewan Farooque’s buzz. The company’s stock price was below Rs4 per share for most of 2022, but by August 2024 had scaled past Rs50 per share with absolutely no increase in revenue whatsoever. Far from it, the company is effectively nothing more than a shell, despite two years of rumours of a prospective revival.

So, where does this leave Dewan Farooque Motors and its EV ambitions? If history is any guide, the road ahead is likely to be as bumpy as ever, with plenty of speed bumps in the form of consumer scepticism, infrastructure limitations, and the company’s own rusty corporate machinery.

But perhaps Dewan Farooque does not care about these pesky details. After all, if they can pull off even a modest revival, they’ll have something they have not had in years: relevance. And in the world of corporate resurrection, that is worth its weight in batteries. n

Bilal Fibres, a bankrupt textile mill, wants to launch a TikTok competitor

The company appears to have no previous discernible expertise in the market, outlines no compelling case, offers a business plan filled with buzzwords, and is hoping for the best. The stock is up 8 times on the rumour of this turnaround

Profit Report

In the annals of corporate reinvention, few sagas are as bold—or baffling—as that of a struggling textile company pivoting into the digital economy. Yes, you read that correctly. After years of hemorrhaging money — Rs538 million in accumulated losses to be precise— this firm has decided that the best way to save itself is by selling off its factory equipment and becoming, of all things, a tech company. The transformation involves shedding its looms and weaving machines and diving headfirst into a field it has no discernible experience in: ICT (Information and Communication Technology).

It is a daring gambit, considering that this same company has seen its liabilities outpace assets by nearly Rs1 billion. Yet, despite a loss of Rs20 million last year and its appearance on the Defaulter counter of the Pakistan Stock Exchange, the Board of Directors is brimming with confidence. Their solution? A business plan that reads like a tech-bro fever dream, filled with jargon like “digital platforms,” “blockchain,” “creator economy,” and “AI-driven content moderation.” At first glance, it sounds like a last-ditch attempt to woo investors with buzzwords.

The cynic in us might wonder: What exactly qualifies a company that could not keep up with cotton prices or energy shortages to suddenly master artificial intelligence or cloud computing? The Board’s plan includes “innovative technologies” and fintech ventures, areas which typically require not just deep expertise but significant capital investment. This is not some minor pivot; it is an industry leap that many more competent firms have struggled to make.

And what of the finances? The company proposes to sell its factory assets, including old machinery and real estate, to raise an estimated Rs200 million to fund the first phase of this tech pivot. This, despite the reality that

proceeds from the sale will first have to be used to settle liabilities. Essentially, the company is gambling that there will be enough left over after paying off its debts to fund a new venture in a highly competitive sector. Call us sceptical, but this feels like a game of corporate Monopoly, where the sale of factories is akin to mortgaging properties in a desperate attempt to stay in the game.

The so-called “digital economy” is presented as the company’s saving grace. The Board points out Pakistan’s growing number of internet users and mobile adoption rates, as if these demographic trends alone will propel the company to success. It is almost as if they believe throwing around terms like “fintech” and “AI” will magically turn red ink into black. Never mind that actual digital transformation requires more than a name change and a new business line—an overhaul in infrastructure, technical skills, and market understanding is crucial. So far, none of that has been evidenced.

The new venture, dubbed BFL Technologies Limited (because, of course, a new name is in order for this shiny new business), intends to develop a TikTok-like social media platform. The business model revolves around content creators and monetization strategies like ad revenue sharing and virtual gifts— something that global tech giants already dominate. How a flailing company in Pakistan plans to compete with the likes of TikTok, Instagram, or YouTube in their own arena is not entirely clear. The marketing plan? Influencer partnerships, social media ads, and contests. Groundbreaking.

Incredibly, the Board expects the company to break even by Year Two, with revenue projections of Rs85 million by Year Three. But revenue forecasts in business plans are famously optimistic; one is tempted to ask if these figures are plucked from thin air or grounded in any real analysis of market potential.

There is also the small matter of regulatory challenges, cybersecurity threats, and intense competition—risks that the business plan waves away with a few lines about “AI-driven content moderation” and “proactive engagement with regulators.” In reality, these are deep-pocketed concerns that can derail even seasoned tech firms. Given this company’s track record, confidence in their ability to navigate such complex issues is, to put it politely, misplaced.

In sum, the revival business plan appears to be less about strategy and more about sheer hope. What began as a textile company limping along in the red now wants to remake itself as a tech powerhouse, powered by little more than asset sales and a prayer. It is a tale as old as time: the buzzword-filled pivot as the last refuge for a business in distress. If history is any guide, it will not end well.

Unfortunately, at least some stock market investors appear to be falling for the shtick. The company’s stock has languished below the Rs3 per share mark for most of the year in trading on the Pakistan Stock Exchange, but starting in late August, started a massive and rather suspicious surge in price, skyrocketing from Rs2.82 per share on August 26, 2024 to Rs21.42 per share on September 23. The exchange appears to at least be making inquiries about the nature of that stock run-up, especially since it came before any announcement from the company. n

Can Retailo’s SaaS gamble pay off?

From logistics woes to a SaaS dream, will Retailo finally find its footing?

By Nisma Riaz

Afew years ago, a quiet tech revolution began brewing in Pakistan’s labyrinthine retail sector. As Pakistan’s tech sector finally started to attract serious amounts of venture capital from global investors, the sector that attracted the most money by far were the multiple players that set about trying to modernise this large segment of the Pakistani economy.

Four companies jumped into the fray, and each raised massive sums of money, or at least massive by Pakistani standards: Bazaar ($108 million in total capital raised), Dastgyr ($41 million raised), Retailo ($60 million raised), and Tajir ($19 million raised).

The thesis was straightforward: the retail sector may have narrow margins, but its filled with multiple layers of middlemen for every product. Cut out the middlemen, pass on part of the savings to the retailer, and therefore the consumer, and create a comfortable margin for yourself. And the pandemic made Pakistanis more open to transacting online, which made the opportunity even more irresistible. Three of the four companies got their start in 2020, with only Tajir having started earlier in 2018.

But the streets of Pakistan are paved with more than just ambition. As the kiryana store owners watched these tech whizzes roll in with their apps and promises of efficiency, many could not help but smirk. After all, their shelves were stocked with stories of failed revolutions. Retailo, however, believed it could be different. They aimed to digitise and streamline the procurement process, cutting out the middlemen and giving these small shops access to products with a click of a button, promising next-day deliveries and the ease of a digital marketplace.

Fast forward a few years, and only Bazaar appears to be largely committed to that initial vision with some degree of success. Most of the others have seen the hype die down. And Retailo, it seems, has decided to go off into a different direction entirely.

The startup faced a grim reality: Pakistan’s logistics landscape was far more stubborn than the founders initially envisioned. Dreams of a streamlined B2B distribution model started to buckle under the weight of harsh market realities—rising costs, entrenched competitors, and a bruising economic landscape that seemed unwilling to budge. And so, with survival on the line, Retailo turned to something that tech founders are famously good at:

the pivot. The new buzzword? SaaS—Software as a Service. But can this pivot truly be Retailo’s knight in shining armour, or is it just another desperate gambit to stay afloat?

Retailo’s original vision

To understand Retailo’s early model, it is important to grasp the context of Pakistan’s retail sector. With an estimated 600,000 small kiryana stores, each selling an average of around $40,000 worth of goods annually, with average gross margins of around 6%, the market is vast— worth approximately $60 billion—but highly fragmented, operating through inefficient supply chains.

Specifically, every single product typically has multiple layers of middlemen in its supply chain. There are layers of middlemen between the farmer who produces the raw materials and the manufacturers, and there are then typically still more layers of middlemen between the manufacturers and the retailer who finally sells the product directly to the consumer. For some minimally processed food products such as rice, there can be as many as 12-15 layers of middlemen between the farmer and the consumer.

None of these earns a particularly high margin, but they exist for a reason: they are solving the informational asymmetry problem between the producers and end-consumers. How much raw food is being produced at every farm, where are the small factories located that can process it all, where can I store goods between the times they are needed and the times they are made available, and then how much of the product is needed at each retailer that actually sells to consumers?

Informational asymmetry is a problem that lends itself exceptionally well to being solved by a marketplace software that connects the seller directly to their end-buyer and keeps a fraction of the transaction for itself as its takerate for facilitating a more efficient transaction. And given the fact that food is still by far the largest component of consumer spending in Pakistan, it makes sense that software-focused tech startups decided to focus on this sector: a large prize, no dominant player, and lots of inefficiency that software can actually help solve.

Retailo’s product offered small stores a one-stop solution for their procurement needs. The idea was simple: store owners could use Retailo’s app to order everything they needed, with deliveries arriving the next day. Retailo aimed to aggregate demand, negotiate better

prices, and ultimately cut out middlemen to bring manufacturers closer to retailers.

The challenge to building a marketplace software and having it be successful is that you need to induce demand at both ends of each transaction. You need to offer incentives to both buyers and sellers to want to come to your platform, which is typically quite expensive and requires a startup that wants to be successful in this business to be able to raise large sums of money. Having brought in $60 million in venture capital funding, the second largest in the industry, Retailo probably felt like they had a chance at success.

Despite the appeal of its value proposition—saving time, offering competitive pricing, and providing efficient delivery—Retailo faced a number of challenges. While its vision seemed compelling, the scale required to achieve real market influence proved elusive. The company reached a peak of $50 million in annual sales, which represented only 0.1% of the potential market. This minimal market share reflected the inherent difficulties of scaling in Pakistan’s highly fragmented retail landscape.

This struggle for scale was not unique to Retailo. In a market dominated by deeply entrenched practices, even the best ideas can find themselves running headfirst into the walls of tradition. Was Retailo’s original vision simply too ambitious, or was it a case of failing to adapt quickly enough to the market’s realities? Spoiler alert: it is probably a bit of both.

Why do logistics startups struggle in Pakistan?