16 TRG continues to languish in the shadow of Chishti’s tug-of-war

20 Banking sector’s banner year creates small business lending vacuum

22 Cash settled futures might be coming to the PSX. What are they and why do they matter?

24 Backed by Bank of Punjab, Gobi Partners is set to bet on Pakistan again. Why now?

28 OGRA’s gas price hike approval might make a small dent in the gas circular debt

29 The stock market’s rise is fueled mostly by banks parking assets in domestic mutual funds

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The Board of Directors of ZIL Limited has appointed

Muhammad Irfan-ul-Haq

as the Chief Executive Officer (CEO) of the company

ZIL Limited, a trusted name in beauty and skin cleansing since decades, is dedicated to delivering high-quality personal care products that elevate everyday care. With decades of innovation and a customer-first approach, ZIL has built a legacy of excellence, offering solutions that inspire confidence and satisfaction.

“This is to inform you that the Board has approved the appointment of Muhammad Irfan-ulHaq as Chief Executive Officer(CEO) of ZIL Limited w.e.f. [with effect from] April 01, 2025,” the notice read, he has been serving ZIL for 1.5 years in the capacity of Director.

Additionally, the company’s Board expressed gratitude for Mr. Mubashir Hasan Ansari’s exceptional leadership during his tenure of 12 years as CEO. Effective March 31, 2025, he will pass on the role, having successfully guided ZIL through this transition period.

“Mr. Mubashir Hasan Ansari will, however, continue to contribute as a valued member of the company’s Board of Directors, ensuring that ZIL benefits from his extensive expertise and management experience,” the notice further stated.

The Board also expressed confidence in Mr. Muhammad Irfan-ul-Haq’s ability to lead ZIL Limited to new heights of success. With over 18 years of leadership experience in various categories, both within Pakistan and internationally, Mr. Irfan-ul-Haq has a proven track record of driving growth, fostering innovation, and building high-performing teams.

This leadership change reflects ZIL Limited’s continued commitment to innovation and excellence in the beauty solutions sector. The company looks forward to achieving greater success under Mr. Irfan-ul-Haq’s leadership.

The ENGRO restructuring

The Dawood family takes a more direct approach to their shareholding in Engro, saving on taxes they probably should not have had to pay to begin with

By Farooq Tirmizi

This is one of those situations where a dramatic headline would belie a much more banal surface reality, while perhaps highlighting a more important deeper reality. It goes something like this.

Headline: Engro is being delisted from the Pakistan Stock Exchange.

Surface reality: It is a restructuring that means that the entity through which Engro investors will own their shares in the underlying assets is changing, but the change does not affect their economic ownership of Engro. The new entity will still be publicly listed, and will be called Engro Holdings Ltd.

Deeper reality: The move is being necessitated by a tax structure that is more punitive than anywhere else in the world, and good players like Engro and their major shareholders, the Dawood family, are being penalized for scrupulously playing by the rules, even when they are unfair.

This is an article about tax law, which most people find painfully boring, but we promise to not dive too deep into the technicalities and instead stay focused on the bigger picture which is that the Pakistani tax code disincentivizes good behaviour and highly incentivizes bad behaviour by Pakistani companies – particularly sponsors of publicly listed companies.

But first, we do need to explain what is happening. And for that, we need to explain why Engro is one of Pakistan’s most significant publicly listed companies.

Engro’s history as a public company

The entity known today as Engro was founded as Esso Fertilizer in 1965. The Standard Oil Company of New Jersey – one of the subsidiaries of the giant Standard Oil Company that was founded by American corporate titan John D Rockefeller – had discovered natural gas in Dharki, Sindh, in 1957. Esso was a brand name owned by the company (and is literally just the phonetic “S” “O” for Standard Oil spelled out), and that is the name they chose for their Pakistani subsidiary.

Why did an oil and gas company decide to create a fertiliser plant? This

was the early days of Pakistan’s natural gas. When Esso discovered gas at Dharki, it had been just five years since the 1952 discovery of the massive gas field at Sui. The gas pipeline from Sui to Karachi – the first, and for a long time the only, city in Pakistan to get natural gas – was only completed in 1955.

Selling gas to consumers in Pakistan, or the very few industrial users that existed in Pakistan back then, was a novel concept, and building a pipeline from a much smaller field than the one at Sui would likely have been an economic challenge.

It seems that Esso must have spent a considerable amount of time trying to make that happen, judging by the fact that they discovered the field in 1957 but did not start building the fertiliser plant until 1966. But at some point, they made the following decision: we cannot sell the gas directly to consumers, but we can sell it by creating a product on site that people in Pakistan have a use for. Since natural gas is the feedstock for fertiliser production, this makes economic sense.

Pakistan’s agriculture sector was taking off in the 1960s with increased crop production thanks to the Green Revolution powered by the research of American scientists like Norman Borlaug, employed by another American chemical company, DuPont. The need for fertiliser was rapidly increasing, so setting up domestic manufacturing capacity for fertilisers, particularly urea, was feasible.

It was not a cheap endeavour, however. Esso invested $43 million, which was the largest foreign direct investment in Pakistan at the time. Expressed in an equivalent percentage of Pakistan’s GDP, this would be equal to approximately $2.5 billion invested in Pakistan today in a single project.

Production began on the 173,000 tons-per-year plant in 1968, and that was also the year the company went public as Esso Fertilizer Pakistan Ltd (they have always used the American spelling in their name). Trading in Esso Fertilizer stock on the Karachi Stock Exchange began on August 9, 1968.

Since then, Engro has been one of Pakistan’s most important publicly listed companies. In 1978, when its parent company retired the Esso brand name and switched to Exxon, the company’s name was changed to Exxon Chemical Pakistan Ltd.

Why

Engro

matters as a public company

In 1991 came the legendary management buyout, when the employees – led by Shaukat Raza Mirza – bought the shares of Exxon after it decided to exit the global fertilizer business. This is a story worth telling in its own right, and we will do so in detail some other time, but suffice it to say, Engro became the first publicly listed company in Pakistan to be bought out by its erstwhile middle class employees, and became a model for entrepreneurial ambition within the corporate world in Pakistan.

In 2003, about 38% of the company’s shares were purchased by Dawood Hercules Fertilizers, a smaller publicly listed fertiliser manufacturing company owned mostly by Hussain Dawood. After some initial bumps (Hussain Dawood wanted to become CEO, but that move became subject to a lawsuit), the Engro management and Hussain Dawood – and now also other members of the Dawood family – came to an amicable arrangement whereby the Dawoods are active participants in strategic thinking at the level of the board of directors but allow considerable management autonomy in running the company.

Engro is, in some ways, among the most mature of Pakistani companies in terms of the evolution of corporate form. There is a family that owns a significant stake, but the company has a life and culture of its own that is independent of any individual shareholder. It has a well-compensated management that draws from the ranks of the most talented professionals in Pakistan, and then actually gives them room to make decisions – and be held accountable for them.

(Engro people: yes, we know your employer is not perfect, but it is better than just about anywhere else in Pakistan.)

It is also a company that has used the

considerable profits from its legacy fertiliser business to invest in new lines of business where economic opportunities arose in Pakistan and, crucially, offered the returns from those new opportunities to public market investors in Pakistan through separate listings of each of its major subsidiaries on the Pakistan Stock Exchange.

Engro is how we want companies in Pakistan to behave. Are there problems? Yes, and we have listed a few of them through the years, not least of which is its penchant for investing in sectors with excessive government intervention. But it acts with its employees and minority shareholders with a standard that can reasonably be compared with some of the best run companies anywhere in the world.

This context is important for explaining what we want to talk about next, which is the fact that none of this matters to the government of Pakistan, which looks upon all companies like Engro as merely a vehicle for extracting revenue because they have been transparent and compliant with the law, so the government knows exactly how much money they have.

Group taxation in Pakistan, and why it is high

One of the things we noted above is that Engro is a company that is both highly transparent, and one that tends to treat its minority shareholders fairly. It is also one that has several publicly listed subsidiaries to allow investors to choose which of its business lines they prefer to invest in. This is the part that ends up being costly for the company.

Hussain Dawood does not own Engro directly. He owns shares in Dawood Hercules, which then owns close to 40% of Engro Corporation, which in turn owns a majority

of nearly all of the Engro subsidiaries. Here is where the problem arises.

Every time a company make a profit, it owes a corporate income tax on it, which is currently set at 29%. From its after-tax profits, it can then pay a dividend which is received by its shareholders. Those shareholders then have to pay another income tax on it, currently set at 15%. This creates a double instance of tax on what is essentially the same income and takes the effective tax rate on that income to 44%.

The government’s retort to this, with some justification, is that if a company is to be treated as a separate entity than its shareholders by the law for the purposes of determining liabilities, then it should also be treated as a separate entity in terms of its tax liability. The company and its shareholders are separate entities, and as such, have their own separate tax liabilities.

Fair enough, but what of the case where a company owns another company? That is where matters get somewhat more complicated.

Corporate entities create subsidiaries for lots of reasons, including adding shareholders into separate business lines, or even simply to organise their business units more efficiently. Those corporate entities paying dividends to corporate parents is somewhat different from the case of individuals. The separation of personhood – and legal liability for debts and other matters – in the law is less clean. Paying a full tax rate on that seems a bit less justified.

To some extent, the government of Pakistan agrees. In April 2009, the Federal Board of Revenue introduced amendments to the 2001 Income Tax Ordinance that allowed for different rules to govern taxation of companies owned by other companies, a set of rules known as group taxation.

The rule in Pakistan is quite straightforward: if one company is the 100% shareholder in another company, then for tax purposes, the government will treat them as the same entity, and any dividends paid by the subsidiary to the

holding company are not taxable. As far as the FBR is concerned, it is as though the money moved from one bank account controlled by the company to another, not between two separate entities.

But what if the ownership is less than 100%? The group taxation benefit effectively disappears (with the exception of the ability to share tax losses to reduce tax liability).

For companies like Engro and Dawood Hercules – which operate several publicly listed subsidiaries where they, by definition, own less than 100% – this is a big problem. And crucially, it is a problem that is unique to Pakistani tax law and does not exist in more mature economies like the United States.

How the US taxes corporate dividends

In the more sophisticated market of the United States, it is understood that the relationship a company has with a corporate investor can vary, and is different from that of an individual owner. Hence taxes do not apply in quite the same that they do in Pakistan.

The rule for wholly owned subsidiaries is the same: since the two entities are the same for tax purposes, money movement between the two is not taxable, and hence dividends from a wholly owned subsidiary are not taxable.

However, US law extends the “wholly owned” treatment much further than Pakistani tax law. Specifically, the threshold for receiving that treatment is not 100% but rather 80%, which allows for the tax benefit to be shared minority shareholders in a way that Pakistani tax law makes impossible.

Even below the 80% ownership threshold, US law offers benefits. For companies that own 20% or less of another company, any dividends received are only 50% taxable, with the remaining 50% being exempt from taxes.

For companies that own between 20% and 80% of another company, any dividends they receive from it are 65% exempt from taxes, meaning that they pay taxes on only 35% of the dividend amount received.

What the tax rules mean for companies

This allows for a lot more minority shareholder-friendly policies in the US, and allows US companies to move money between related entities without having to undergo the kind of shenanigans that are commonplace among Pakistani conglomerates – often involving company money being used in ways that explicitly cuts out minority shareholders being able to gain from company resources being invested.

Consider, for example, a holding company that wants to move money to its holding company. Faced with the kind of taxes that they would in Pakistan, they might do an inter-company loan rather than a dividend payment from which minority shareholders might also benefit, a rather common practice among Pakistani group companies.

But more than that is the question of tax fairness. The government of Pakistan’s policy on taxation is quite simply: “Tax what you can, not what you should.” The most productive companies in Pakistan – including ones that play by the rules and are transparent about their revenues and profits – find themselves in the crosshairs every time the government wants to raise revenue for this year, incentives for long-term behaviour be damned.

Excess taxation for Dawood Hercules

Dawood Hercules, for instance, has paid a significant amount more in taxes over the past decade than it would have had the government

of Pakistan offered the kind of concessions that are the norm in the United States and elsewhere.

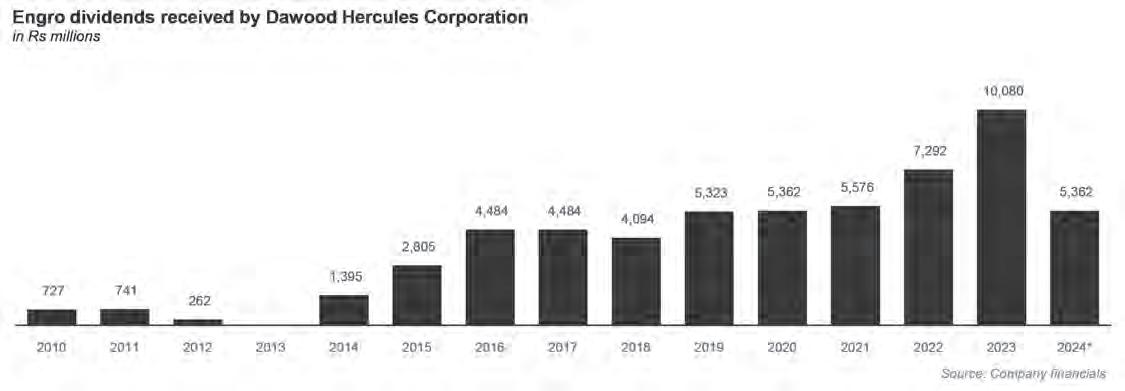

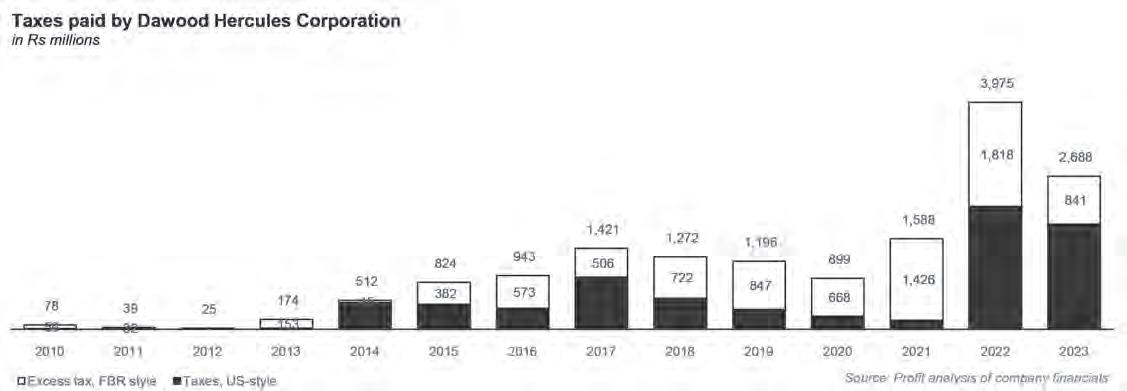

Since 2011, Engro has paid Rs57.3 billion in dividends to Dawood Hercules. And Dawood Hercules has paid Rs15.6 billion in income tax to the government based on the full taxation rate that the government of Pakistan charges. If, however, the government of Pakistan offered the kind of concessions to companies on group taxation that the US offers, Dawood Hercules would only have owed Rs7.6 billion in taxes.

In effect, Pakistan charged Dawood Hercules about Rs8 billion more in taxes than it would have, had the government adopted international norms on corporate taxation. It is to eliminate that excess tax that Dawood Hercules has decided to undertake a restructuring.

What the restructuring entails

The actual restructuring is relatively straightforward: what the Dawood Hercules shareholders want is to own Engro directly rather than through the Dawood Hercules Corporation. This requires them to do the following:

1. Eliminate the existing Engro Corporation Ltd holding company

2. Create a new holding company – Engro Holdings Ltd – into which Dawood Hercules places its ownership of Engro subsidiaries

3. Offer shares in Engro Holdings to existing shareholders of Engro Corporation in a manner that does not in any way dilute their ownership

It is a legally convoluted way of achieving a simple result. And through this, the Dawood family – and frankly, even the shareholders of Engro – will save on a level of excess taxation that should never have existed to begin with. n

TRG continues to languish in the shadow of Chishti’s tug-of-war

Once reputed as a clean, safe, stable bet on the stock market, the management of TRG is drawing up its defences in the face of another attack

By Zain Naeem

TThe saga has unfolded in the wake of the exit of Ziaullah Khan Chishti, the Pakistani-American founder who created TRG and Afiniti. Mr Chishti was ousted from TRG Pakistan as well as his company in the United States in the wake of accusations of sexual assault levelled against him by a former employee.

he fortune of TRG Pakistan has been nothing short of astounding. Once the darling of stock market investors, the company’s financial performance has been suffering from a constant tugof-war for control of the company.

And while his position in TRG has been displaced, his influence continues to inform the power-struggle that has become a persistent problem for the company.

The constant volatility and turmoil at the company is being reflected in its financial performance as well. Where will this saga end and who will come out on top? All that can be said for now is that the trenches are being dug and the war is expected to go on for the long haul.

The TRG story

The beginning of our story is rooted in success. Few can deny that the story of TRG Pakistan is steeped in entrepreneurial genius and commitment. The company came out of the entrepreneurial efforts of Zia Chishti. Established in 2002, the principal activity of the company was to create a venture capital investment which would invest in TRG International investing in technology and IT enabled services.

The company went on to become one of the pioneers in terms of its calling centre services. Due to the structure of the company, it has established TRG International which has many companies that it runs and operates under its umbrella. The companies owned by TRG International encompass outsourcing solutions, IT related services and call centres. Essentially, these companies raise the revenues which are then translated to TRG Pakistan through its investment in TRG International.

At the time that the current crisis began, TRG was actually doing pretty well. The company had one of its best years in 2021 with the share price trading at around Rs 182.17 and it was regularly giving out considerable dividends. It recorded its highest earning per share in the third quarter of FY 2020-2021 and it seemed like the good times would keep rolling on. TRG International had just set up Afiniti in its portfolio of investments which was becoming a big name in Artificial Intelligence as the technology was taking off. Having set up the company, Chishti was one of the major shareholders of TRG Pakistan and had a stake in its international subsidiary as well. Just when it seemed like things would keep on getting better, in November of 2021, Chisti was unceremoniously kicked out of Afiniti and TRG. The reason behind the ouster was the accusations of sexual assault made by a former employee. This started a battle of control over the company that is still going on three years later.

The ouster and the fight back

Chishti was asked to step down as Chief Executive Officer (CEO) of Afiniti and then TRG due to the allegations.The fall was completed when

an election of directors was called in January 2022 and he had to vacate his directorship as well. The man who had built the company to the behemoth it had become was no longer in the driver’s seat. Chishti was down but not out.

Since 2022, he has tried to take back control over the company from the outside. This was not a simple case of dismissing a CEO for bad behaviour. Chishti had built this company, and even though he had been removed as the head of the company, nobody could take his shares away from him. As such, he still had a voice within the company. Profit covered last year how he took out a full page ad in the leading newspapers of US and Pakistan asking for an Extraordinary General Meeting (EOGM) to be called and for the present directors to be voted out.

Before this, the fight was being carried out surreptitiously by acquiring shares of the company. This was the first time the tug of war was made public and Chishti was asking the other shareholders to band together and exercise their power.

In reply to the barrage of attacks from Chishti, the board of directors were able to negate or parry many of the attempts in one form or another. In October of 2022, Chishti tried to engineer a hostile takeover by joining with JS Group in order to gain a majority stake in the company. The company countered by going to the Sindh High Court and claiming that the JS Group was buying shares in the market and had crossed the 30% threshold at which point it had to make a public offer. The case stated that the group had crossed 34% of the shareholding and had violated the regulations. After this, the court restrained the group from exercising its voting powers as it had violated the law.

After this attempt was foiled, Chisti again tried to create a third party interest through his wife’s holding in order to attempt a hostile takeover, however, the court stepped in again and foiled this plot in January 2023. Seeing his attempts to take over the company failing and barred from acquiring more shares, Chisti tried to make the whole thing public by carrying out social media campaigns against the directors at the company. First a defamation lawsuit was filed leading to bailable arrest warrants being issued against the directors and then suspended in February of 2023. One of the directors, Asad Nasir, even filed a complaint against the company at the Securities and Exchange Commission of Pakistan (SECP) claiming that the company was not being run properly.

In September of 2023, Chishti also tried to oust the whole board and amend its Article of Association to improve governance. Under SECP regulations, a shareholder having more than 10% of the shareholdings can ask for an EOGM to be held and they can set the agenda as they want. The board of directors were able to get a stay order from the Sindh High Court

against this. Once he failed to get an EOGM organized, Chishti tried to add an addendum to the Annual General Meeting (AGM) which was supposed to be held by the company in October of 2023. The door of the High Court was knocked on again and a stay order was taken not to hold the AGM in the first place.

Battlelines redrawn

Seeing all his attempts fail, Chishti resorted to carry out his own media trial. An ad was taken out which claimed that the current CEO and directors at the company were destroying the value of the company. The ad claimed that Afiniti, one of the leading revenue generators, was being mismanaged leading to its collapse while Ibex, another portfolio company, had seen its price crash in the American market. Rather than building value into the company, the directors had created a cash reserve and were now buying shares of TRG Pakistan by setting up a company in Bermuda by the name of Greentree Holdings. The letter was an attempt to get support of the shareholders who could force the whole board to retire and to carry out new elections.

In reply to the ad, the directors issued a strongly worded statement saying that if Chishti came back to the company, it would damage the value and brand of TRG Pakistan due to the allegations made against him and the company was fighting off attempts by Chishti to take over control.

While the directors are fending off the attacks of Chishti on a regular basis, TRG Pakistan is also seeing its shares being bought by Greentree Holdings Limited. At the end of 2021, Greentree holdings had no shares of the company which stood at 28.54% at the end of June 2024. The recent attempt by Greentree holdings to acquire an additional 35.1% of the shares shows that the directors are looking to strengthen their position further. But why such an interest after all this time? Well that has to do with the fact that the directors will be ending their term in January of 2025 and law mandates that elections need to be held by then.

The elections that need to be held will be swayed by the person who has control of a greater shareholding which will translate to a majority of shareholders being appointed by them. Board of directors supervise the decision making and drive the company in the direction they desire. By having more than 50% of the shareholding, Greentree Holdings will be able to elect directors that it wants on the board.

In the meantime

While the two sides bicker over control, the financial performance does seem to be suffering. In terms of its

operations, it can be seen that from June 2023 to June 2024, the company has suffered losses that it has tried to claw back. At the end of June 2023, the company suffered a loss per share of Rs 2.45 which has grown since then.

The way TRG Pakistan is structured, it primarily has only one long term investment of TRG International on its books. As the portfolio investments of TRG International rise and fall in value, the value of TRG Pakistan’s investment moves along with it leading to profits or losses. Still, the way the subsidiaries are being run ultimately have an impact on the profit and loss of TRG Pakistan as well. TRG Pakistan has a say in how things are run by TRG International which is then able to impact how its subsidiaries are performing as well. Whoever has control over the Pakistani company has influence on the subsidiaries and their decision making.

As the new financial year started, TRG Pakistan made a loss of Rs 15.7 per share by September 2023 owing to its investments. By December end, the loss had increased to Rs 19.4 per share and by March 2024 it was Rs 30.7 per share in the form of losses. By June end 2024, the loss had piled up to Rs 56.6 per share.

In terms of the management of Afiniti, the claims made by Chishti do prove to be right to an extent as the company has seen colossal losses in 2024 related to its investments. Afiniti also used to be one of the biggest revenue generators for the company, however, now it seems that it has had to go through a restructuring deal. In September of 2024, a deal was reached between the lenders and the company to carry out a balance sheet restructuring plan that will help in improving the financial position of Afiniti. Some of the debt was reprofiled to long term debt and the lenders and preference shareholders were given equity in exchange. The interest payments were also reduced which increased the finances that were available. Even though this was a good development, it still shows that the management was not able to retain the profitability and growth of Afiniti as it once was.

The impact of the restructuring could be seen in the latest results as TRG Pakistan was able to show earnings per share of Rs 4.41 where it had suffered a loss of Rs 15.7 a year ago. TRG International was also able to sell its shareholding in Ibex to the company itself which raised additional finances for the investment company. With the company slowly getting back on its feet, it seems like the tussle is going to start once again.

The elections that had to be carried out at TRG Pakistan have to be completed before the term of the current board ends in January of 2025. Once the tenure of the current board

ends, the company is assumed to be running without any directors as they have all retired. In order to carry out the elections, formalities have to be started to get names of interested parties. No such process was carried out by the directors at TRG Pakistan. According to its disclosures, the company did announce recently that two shareholders had filed an injunction against the company to stop them from holding any such elections before the fact. The action was done to stop the board from calling any such elections which can carry out the formality with little interference from the outside. Based on the order, no elections can be held until the court takes back this order.

While the elections have been suspended for the time being, Greentree Holdings also made a recent move, showing an interest in acquiring additional shares of the company. Through AKD Securities, the company has disclosed that Greentree Holdings Limited is looking to acquire 35.1% of the shares through a public announcement of intention. Greentree Holdings is the alleged company which is being used by directors in order to buy the shares of TRG Pakistan to retain control and wrest it away from Chishti.

This acquisition would make up around 50% of the total free float of shares available in the market and can take the total shareholding to 64.7% from where it stands today. As Greetree is owned by TRG International, the shares would end up being held by TRG Pakistan in the end in this Kafka-esque holding structure of the company. Basically, Greentree is buying shares of TRG Pakistan which will benefit TRG International which is owned by TRG Pakistan. It has still to be noted that even if Greentree is successful, 16.12% will be held by Ziaullah Khan Chisti while JS Group holds around 4% and Chishti’s wife also owns a similar percentage of the shares which will be retained by them.

The filing of suit and the public intention for acquiring of the shares is just the most recent chapter in this long lasting saga that seems to have gripped the company. The recent skirmish involves the board of directors election where both sides will try to get their choice of board which can run the company. Based on the shareholding and the will to have complete control, both sides would want to come out on top in this all or nothing approach. While they quarrel with each other, the company still needs to be steadied to charter a new course for itself. The winner of the latest duel is yet to be decided and it has to be seen whether Chishti is willing to give up just yet or take this battle on a little longer. n

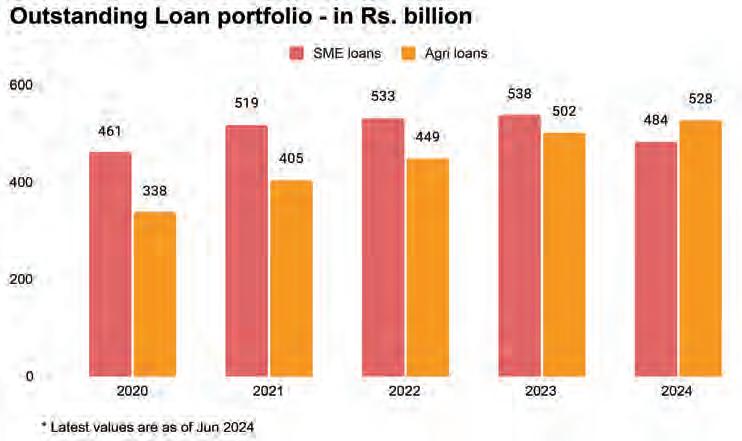

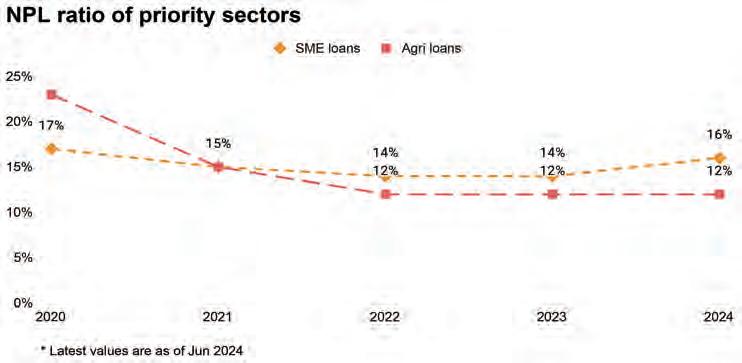

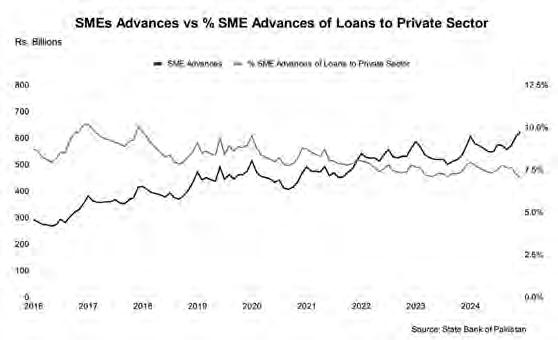

Banking sector’s banner year creates small business lending vacuum

SME credit crisis deepens as industry hurdles mount

By Ahtasam Ahmad

Pakistan’s commercial banks have been having a bit of a party, but it seems nearly the entire private sector missed the invitation.

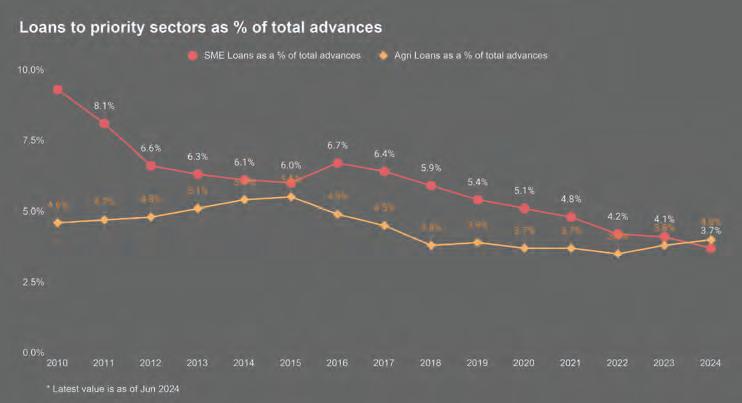

The numbers are quite astounding. The banking sector saw extraordinary profits on the back of government securities, arbitrage, and last-minute lending surges to avoid tax penalties. Yet beneath these headlines lies a fundamental challenge: an unprecedented drought in private sector credit that has particularly devastated the backbone of Pakistan’s economy: its SME and agricultural sectors. There are more than 50 lakh businesses in Pakistan that are characterised as being ‘small and medium enterprises’ (SMEs) in both the formal and informal sectors working in manufacturing, trading, and services. These enterprises power the economy, contributing 40% to the GDP, representing 90% of all private enterprises, generating 30% of export earnings, and employing 30% of the workforce. In a nation of 24 crore people facing intensifying poverty and unemployment, their vitality has never been more crucial.

Yet these businesses continue to struggle for affordable growth capital, primarily due to documentation gaps and insufficient collateral.

Of these 50 lakh SMEs nationwide, only 3.5% have been able to access bank financing. The agricultural sector faces similar constraints, with roughly 75% of farmers still dependent on informal credit sources. Overall financing to these vital sectors has steadily declined, now standing at less than 8% of total loans - with SME financing at 3.7% and agricultural lending at 4%. This represents a sharp decline from 2010 levels, when SME and agricultural lending comprised nearly 14% of banks’ loan portfolios.

To comprehend the depth of this financing challenge, we draw from PwC Pakistan’s Banking Publication 2024. This comprehensive annual report provides detailed insights into the banking sector, with particular attention this year to SME and agricultural financing. Its findings illuminate not just the scale of the current crisis, but also potential pathways toward financial inclusion.

Core challenges

Macroeconomic headwinds have hit SMEs harder than larger enterprises, with rising interest rates making formal borrowing nearly

impossible for many small businesses. Though SMEs continue to grow in both number and revenue, they increasingly rely on informal financing or equity funding to meet capital needs - options that circumvent traditional banking’s documentation and collateral requirements.

The barriers to credit access are structural, starting with banks’ limited physical presence and insufficient resources for financial advisory services. Bank of Punjab’s President & CEO, Zafar Masud, articulates this challenge in PwC’s report: “We, as commercial bankers, are not necessarily trained to deal with sectors like Agriculture and SME. Completely different skills, mindset and risk appetite is needed to promote banking facilities, including

financing, in these priority sectors.”

Masud advocates for a structural solution: “Specialized institutions under the PPP structure is the way to go. Without progress in these sectors, our human development index remains compromised and thus sustainable economic growth.”

This observation reveals a fundamental flaw in current banking structures, where SME and commercial banking operations share management at the branch level. Relationship managers naturally gravitate toward larger commercial clients to meet targets, while corporate-style documentation requirements create nearly insurmountable barriers for smaller businesses seeking financing.

Source:

Source: PwC

PwC

Also, the devastation from the 2022 floods and COVID-19 pandemic has left lasting impacts on banks’ SME and agricultural portfolios, with microfinance institutions bearing the heaviest burden. This trauma has fundamentally altered lending practices: even the microfinance sector, traditionally focused on unsecured lending, has shifted toward collateral-backed loans to mitigate risks.

As per PwC’s findings, banks actively engaged in priority sector financing now maintain approximately 90% of their portfolios as collateralized loans, with only 10% based on cash flow assessments or unsecured lending.

The absence of sophisticated credit scoring models presents another fundamental challenge in SME lending, making it difficult for banks to accurately assess and price risk. This challenge compounds with standardized loan processing procedures that fail to differentiate between small and large facilities, resulting in disproportionate operational costs for smaller loans. At the core lies a data crisis. The SME sector remains largely undocumented, creating significant information asymmetry between lenders and borrowers. Alternative data sources that could help bridge this gap - such as utility payments and telecom records - are either inaccessible or insufficient for credit assessment.

Strategic initiatives

The State Bank of Pakistan (SBP) has positioned access to financing as a cornerstone of its Strategic Plan 2023-2028. This agenda focuses on expanding financial services across the country, particularly in traditionally underserved sectors including agriculture, SMEs, microfinance, housing, and trade finance.

The central bank’s approach addresses multiple dimensions of financial inclusion. The strategy aims to improve credit-to-deposit ratios in underserved regions while creating an enabling environment for agricultural finance. The plan emphasizes developing a robust SME financing ecosystem and implementing the

We, as commercial bankers, are not necessarily trained to deal with sectors like Agriculture and SME. Completely different skills, mindset and risk appetite is needed to promote banking facilities, including financing, in these priority sectors.

Zafar Masud, Bank of Punjab’s President & CEO

National SME Policy, alongside initiatives to promote export diversification and import substitution.

SBP’s targets reflect this ambition: SME financing is projected to exceed Rs. 1 trillion within five years, accompanied by a fourfold increase in the borrower base. Several foundational initiatives support this goal, including an updated SME census, a revised SME definition aligned with current business dynamics, and an innovative risk-sharing scheme offering coverage of 20% for small enterprises and 10% for medium-sized businesses on a first-loss basis.

Risk management evolution

Pakistan’s economic volatility in 2023-24 has transformed credit risk dynamics, necessitating an overhaul of bank risk management strategies. With the Advances to Deposit Ratio at 37% by June 2024, banks face pressure to reconstruct risk frameworks while pursuing sustainable credit growth.

model validation across SME, agriculture, and consumer finance segments. The survey identifies critical challenges in data quality and skilled resource availability, emphasizing the urgent need to enhance national data infrastructure through comprehensive credit bureaus, land registries, and collateral databases.

Regular model validation and recalibration have become imperative, particularly for IFRS-9 compliance. While some banks conduct internal validations through Risk Management functions, the complexity of the current economic landscape often necessitates external validation support for independent assessment.

The way forward

The growing recognition of SMEs and agriculture’s importance to national development has highlighted the need for transformed banking approaches and ecosystem development. While few banks currently have specialized strategies for these sectors, an emerging trend shows collaboration between traditional banks and fintech platforms to provide beyond-basic banking solutions.

Source: PwC

Key challenges include digitalizing land records, accessing alternate data for informal sector lending, and developing digital platforms to generate cash flow histories for small businesses. Industry experts advocate for comprehensive ecosystem transformation, involving public-private partnerships, specialized institutions, and policy frameworks. With large-scale industry growth plateauing, small businesses and agriculture emerge as the natural catalysts for the next economic expansion. These sectors not only promise higher multiplier effects throughout the economy but also offer a more efficient path forward, requiring relatively lower capital investment. n

Cash settled futures might be coming to the PSX. What are they and why do they matter?

The new PSX CEO has hinted at the introduction of these derivatives which can decrease burden and increase liquidity in the market

By Zain Naeem

In a recent interview, Farrukh H Sabzwari, the new Chief Executive Officer (CEO) at Pakistan Stock Exchange (PSX), has hinted towards the fact that cash settled futures and options are being considered as being introduced to the local market. There are plans to introduce these derivatives in the market after testing them by March of 2025. This is expected to increase liquidity and is preferred by traders as they have low capital requirements. What actually are cash settled futures and how do they differ from the mechanism that is in place currently?

Some basics

To get an understanding of these future contracts, a basic comprehension of future markets is required. Usually it is understood that

investors can buy or sell a share in the market. When people talk about transactions being carried out, it is a given that the regular market is being discussed where shares are traded and settled within a given time frame of two days. Investors who are buying the shares are expected to pay for these shares in two days while the seller has to guarantee delivery of the shares to the buyer against which he will get his sales proceeds.

The next step in this progression is where future contracts are traded. In the futures market, a buyer makes a commitment some time in advance that he will buy the shares at a given date in the future. The price of these contracts is tied to an underlying stock or share and are called derivatives as their value is derived from the stock itself. A buyer will buy the shares in the market on the 3rd of the month and will commit that when the trades are settled in the future, he will put up the funds needed in order to complete the transaction. Let us assume that the shares

will be settled on the 30th of the month. Usually, the last Friday of the month is the final date of settlement.

Based on the expectations of the buyer, he can either buy the shares by the 30th or he has the option to close his position before the 30th arrives to sell his position in the market. Assuming that he bought the shares for Rs 10 and sees the price reach Rs 15, he can sell the contract to someone else interested in buying the shares, book his profit and square his position. One of the biggest attractions of the futures market is that he can put up a fraction of the price and get to own the future contract. In the normal market, he would have to put up the total Rs 10 and buy one unit. In the futures market, he can buy a larger number of shares by putting up a smaller amount and get a larger position which can magnify his profit or return. The buyer is expecting that the price of the share will rise and he will profit when that takes place.

On the other end of the spectrum is the

seller who is committing to sell the shares to the buyer at the date of settlement. The seller is expecting that the price of the share will fall so he has an opportunity to sell right now at a higher price. Over time, as the price will fall, the seller can either buy back the position and close the position that he has or allow the contract to expire and deliver the shares that he promised to do earlier.

This is an illustration of how the deliverable future contract market works. The value of the contracts is attached to the underlying asset or stock and the shares have to be delivered to the buyer by the seller at the contract expiry. The buyer needs to make sure that they have the funds by the expiry while the seller has to make sure that they have the shares that have to be settled.

The future markets

Future markets are usually used for two reasons. They are used by hedgers and speculators. Hedgers are the investors in the market who want to lock in the price of their purchase or sale at an earlier date. Consider a farmer who is going to plant a crop at the beginning of the season. While he is starting the process, he can go to the futures market and sell his crop months in advance by selling it in the future market. This way, he is able to lock in a sale price months in advance and guarantee a fixed return which will be realized in the future. With that being said, it has to be kept in mind that the farmer could have gotten a higher price if he had not gone to the future market and sold at a better price once the crop was harvested. Similarly, he could have faced a lower price as well in the future once the harvest was brought to the market. The hedging aspect of the future contract guarantees a return for the farmer months in advance.

Other than the hedgers, the future market is used by speculators who are expecting to get a greater return based on their outlook of the market and are looking to maximize their returns. A speculator expecting the price to go up will look to buy a contract right now at a cheaper price. Once the price of the asset increases in the future, he can sell at a higher price. A future contract allows him to put up a small part of his investment and look to make a higher return once his expectations are met. In the same vein, if he expects the price to fall, he can sell the shares right now and then buy them when the price falls and earn a profit.

One of the biggest complications of deliverable future contracts is that the seller has to physically hold the shares or stock and then make sure they are under his possession when the settlement is carried out. The buyer

also has to buy the stock and then hold it when they are settled and then transfer these shares to the next person when they are sold. This cost is much higher when the commodity market is considered. An investor looking to buy futures in the oil market will have to find storage solutions for his commodity once it is delivered. The cost of transporting and holding the commodity adds to the cost of buying the commodity and can become burdensome for the individual buying the commodity.

How it is in Pakistan

Pakistan’s stock market has a futures market that runs parallel to the regular market and the settlement that is used currently is deliverable in its nature. A seller has to have the shares in his possession before they can enter into a sale of a future contract. This could mean that the seller had to buy the shares from the market which would cost him a commission and charges that are applicable. Once the settlement is carried out, the buyer will also have to pay a commission in order to get the shares and then pay a fee to Central Depository Company which becomes the custodian of the shares.

A simple trade that can take place in the current scenario can be that the buyer buys the share for Rs 10 in December willing to sell the shares in March for Rs 15. The buying carried out in December would charge a commission to buy the shares right now. When the buyer sells his shares in the March contract, he is locking in a profit of Rs 5 but he will be liable to pay a commission on the sale as well.

One more wrinkle that is added around this time is the act of rollover. Rollover takes place where a buyer who is supposed to buy the shares in the settlement period squares off his position in the current month and then rolls over his position for the next month. The investor bought the future contract in December which meant that at the end of the month, he was committed to buy the shares. However, rather than putting up the funds, the buyer closes his position in the current year by selling a December contract and then buys a January contract rolling over his commitment to the next month. Many times, the positions are rolled over as the buyer expects the share price to increase further. As he does not want to put up the funds, he rolls over the position by using a fraction of his total funds again. This is the reason why, when the contract is near expiry, there is a large amount of activity that is seen as buyers and sellers both enter the market to roll over their positions in the deliverable futures market.

Cash settled futures simplify this whole process to a great extent. Rather than having

to put up the delivery of the shares, a final settlement price is determined and based on that price, the buyer or seller is either given a profit or expected to put up the loss that has been incurred. There is no compulsion to put up the shares or the funds for the purchase and only the difference is squared off. An investor bought the shares for Rs 10 at the start of the month and the seller committed to sell the shares at Rs 10. During the month, the price of the stock fluctuates. In order to make trading safer, losses or marked to market losses are taken from the person who has incurred a loss. If the price goes to Rs 8, the buyer is asked to cover the loss as his position has lost money. If the price goes to Rs 12, the seller is expected to cover this loss. The market to market losses make sure that in case a default takes place, there are some funds that can be used to cover the losses. Mind you, this mechanism is not specific to the cash for a settled futures. A similar mechanism is used to cover market losses in the deliverable contracts market as well.

At the end of the month, the settlement price is determined to be Rs 11. This is a gain for the buyer as he bought the contract at Rs 10 and now the price of the contract has increased. The seller has made a loss and has to end up paying the loss amount to the buyer. The seller pays Rs 1 to the buyer and the contract is seen as being settled. No need to pay commissions, fees or extra custody costs. This is the ease that is seen in the cash settlement market which does not exist in the PSX currently.

The new market will allow investors to be able to use more funds on trades which would have been used to pay for fees and charges that have to be paid on deliverable assets. This would increase the liquidity and funds circulated in the market.

The rolling over that takes place in the deliverable futures market will also be done away with as the current contracts can be rolled over by paying the difference between the current price and the price at which the contract was carried out. Rather than squaring off the whole of the positions, only a loss will have to be paid. There would be a reduced need to carry out rollovers and settlement near the settlement date. There would be no rush or activity in the market to cover the positions and the settlement date will not face the same amount of trading activity which is seen in the deliverable market. Cash settled futures are ideal for speculators who are more interested in gain and change in the price of the stock rather than having any interest in holding the asset. This turns the contract into a financial exchange of profit and loss rather than a transaction of physical commodities. n

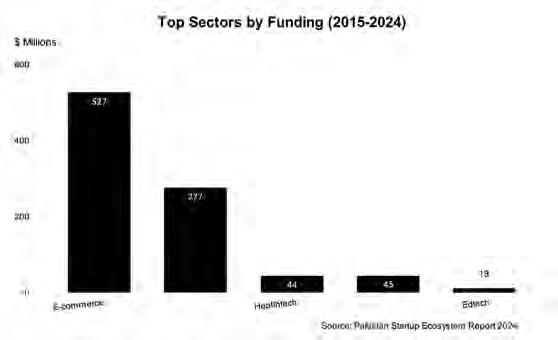

Backed

by Bank of Punjab, Gobi Partners is set to bet on Pakistan again. Why now?

The global venture veteran has forged an alliance with the Bank of Punjab to launch a new fund, Techxila Fund-II. But why now, and what is in it for the BoP?

By Hamza Aurangzeb

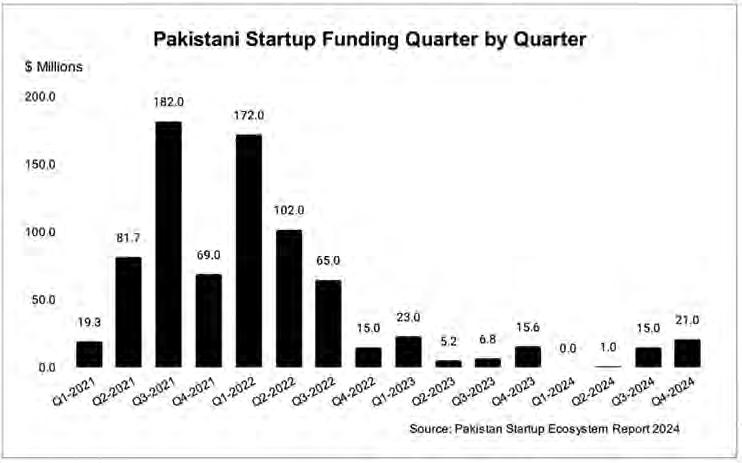

Battered, bruised, and severely under pressure, what remains of Pakistan’s startup ecosystem is looking at a $50 million injection that it desperately needs.

The current funding winter has lasted well over a couple of years at this point, with players once touted as future unicorns failing to make it through. Amidst this climate of caution, the global venture capital firm Gobi Partners has announced a $50 million fund for Pakistani startups.

This is undoubtedly good news, but what exactly has Gobi interested in Pakistan at a time like this? It shows that there is still an appetite amongst global investors for Pakistani products in the startup space. But this time around Gobi is entering Pakistan through an interesting model: They have partnered up with the Bank of Punjab (BoP).

But how will this partnership work, and

what has driven Gobi Partners’ desire to bet $50 million on Pakistani startups at a time when others have stepped back? Behind the decision, there is some interesting strategic calculus.

Pakistan’s venture capital landscape

Oh how things have changed. It feels like a lifetime ago, but it has really only been five years when Pakistan was fast emerging as a new avenue for global venture capitalists to invest in. Just go back to 2019 for a second. Here was a country that had adopted mobile internet less than a decade ago with a young population and a hunger for economic opportunity.

The signs were there for a startup revolution.The growth of local startups along with the acquisition of Careem by Uber in 2019, boosted the confidence of international VCs and persuaded them to take a bet on the

MENAP region including Pakistan’s burgeoning ecosystem. The entry of international VCs took the venture investment landscape in Pakistan to dizzying heights during COVID-19, when the chance to provide innovative new services was high. In 2020, alone, Pakistani startups gathered $65 million across 48 deals, but this was just the beginning.

Witnessing several renowned VCs like Global Founders Capital investing in the region created a FOMO effect among several leading VCs who also decided to get on the bandwagon. Thus, investments in Pakistan reached a new high of $352 million across 83 deals in 2021, where the country had merely attracted $253.5 million over the past six years.

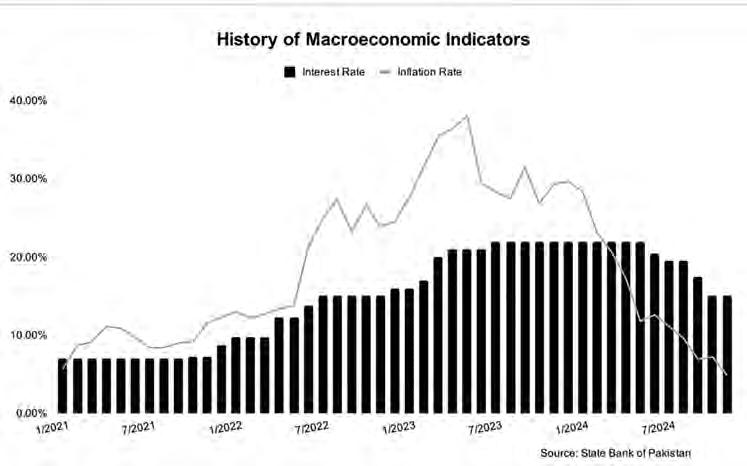

The beginning of 2022 also saw continued investor interest in the market as startups amassed $172 million in Q1-22, however, things took a turn when the Fed took a hawkish stance and commenced monetary tightening by increasing interest rates to counter high inflation. The situation was exacerbated by

Pakistan’s political turmoil and double-digit inflation that prompted the SBP to increase the policy rate. Thus, investments declined to $102 million in Q2-22, which further plummeted to $65 million in Q3-22, and finally dwindled to $15 million in Q4-22.

The situation worsened in 2023 as global inflation and interest rates continued to escalate at an alarming rate. Thus, the venture capital funding took a nosedive across the globe but it plummeted to record lows in recent years in Pakistan, as the startups only gathered $74 million in 2023. Investors only allocated $23 million to startups in Q1-23, and the startups only managed to scrape $5.2 million in Q2-23.

Further, no significant changes were observed in investment trends during Q3-23 and Q4-23, as only $6.8 million and $15.6 million were collected, respectively. These were the consequences of record-high inflation in Pakistan, which reached 38% in May 2023, coupled with an anomalous policy rate of 22% set by

the SBP to control record-breaking inflation. These indicators along with political volatility added to the woes of startups.

It gets worse.

The current year started with crickets. A grand total of $0 was raised in the first quarter of the year. In fact, this was the first time since 2015 that a quarter concluded with zero deals. The second quarter was not much better. It would have been another $0 but there was one deal worth around $1 million. However, owing to a decrease in inflation to 12.6%, SBP decreased the policy rate to 20.5%.

Since the easing of the economic crisis, the ecosystem has displayed modest signs of recovery driven by a declining policy rate which has fallen to 13% and macroeconomic stabilization, where the GDP growth rate for FY24 was recorded at 2.38%. During the third quarter of 2024, startups attracted more than $15 million, while they gathered around $21 million during the final quarter. Pakistani

startups concluded the year with a total investment of $37 million, with most investments attracted by post-seed startups.

This improving macroeconomic environment and the mammoth growth potential of startups in Pakistan are what fuel the optimism of Gobi Partners and the Bank of Punjab. Hence, Gobi Partners launched a $50 million venture capital fund and onboarded the Bank of Punjab to contribute towards the fund.

Gobi Partners and Fatima Group

Gobi Partners, one of the leading PanAsian venture capital firms headquartered out of Kuala Lumpur and Hong Kong was founded in 2002. It has an Asset Under Management (AUM) value of $1.6 billion spread across 15 countries and 19 funds, which have invested in more than 380 startups. The enterprise assists startups ranging from early to growth stages, with an inclination towards emerging markets.

The Fatima Group is a Pakistani conglomerate based out of Lahore, which traces its origin back to 1936, when it was established as a commodity training business. However, over time it has grown and transformed into a large conglomerate engaged in diverse spheres of business such as fertilizer, energy, sugar, mining, information technology, real estate, trading, textile, and venture capital.

In 2015, Gobi Partners and the Fatima Group launched a joint venture, Fatima Gobi Ventures, to support the development of the Pakistani startup ecosystem. The firm’s strategy is an amalgamation of the Fatima Group’s long entrepreneurial experience of the Pakistani landscape spread across eight decades and Gobi Partners’ expertise in nurturing sustainable and progressive unicorns around the continent of Asia over the past two decades.

In 2019, Fatima Gobi Ventures (FGV) backed by Gobi Partners launched its first Pakistan-focused venture capital fund, Techxila Fund-I, to promote local startups. The size of the fund was $20 million, where impact investors like British International Investment made an anchor investment of $5 million. The fund has thus far invested in 22 startups including PriceOye, Pakistan’s second-largest e-commerce platform; DealCart, a social commerce platform delivering affordable groceries; and Abhi, a financial wellness platform that advances credit lines to businesses and individuals.

The Launch of Techxila Fund-II

The success of Techxila Fund-I prompted Gobi Partners to launch another venture capital fund of $50 million and ink a Memorandum of

Understanding (MoU) with the Bank of Punjab to promote entrepreneurship and fortify economic cooperation in Pakistan.

The establishment of the fund was officially announced during the Pakistan Investment Conference in Shanghai. The fund was announced during Punjab Chief Minister Maryam Nawaz’s tour of China, and it is an indication that they managed to get the support of the Punjab government on this that they partnered with the provincial government’s bank. Without getting into the self-conglaturatory PR language the fund uses to market itself, the idea is simple. The $50 million will be invested into proven and high-growth verticals like fintech, e-commerce, logistics, supply chain, health tech, and SaaS. It is a low-risk strategy.

What the fund hopes to tap into is the raw potential of the Pakistani market. With two-thirds of its population under 30, a high broadband penetration rate of 58.4%, and an increasing demand for tech-driven solutions, Pakistan still very much has the raw ingredients to be a good playing field for tech-startups.

Another reason for Gobi’s renewed interest in Pakistan might be a desire to be the early bird. While the worms have been sparse in the past few years, they might be thinking the downturn in Pakistan was trigerred by a global recession. With global economies improving, it might mean startups could be stirring once again, and Gobi would want to get a head-start. With this fund in place, the firm can acquire high-potential startups at more favorable valuations during this funding drought, positioning itself for bigger returns once the market recovers. This strategy will not only enable them to completely utilize the current market conditions but also reinforce confidence among other investors by strengthening the resilience and enriching the profound visions of startups.

It is still a risky move. Pakistan is a market which has attracted more than $1 billion over the past decade, but it remains largely unexplored. Pakistan harbors an

incipient startup ecosystem compared to the startup ecosystems of India and Indonesia, which are leagues ahead in terms of advancement and maturity. Nevertheless, Pakistan is fast emerging as a technology hub, the country was termed “Tech Destination of the Year” at GITEX held in Dubai in 2024. Thus, Gobi partners intend to boost its position in the country by investing in Pakistani startups, bracing itself for expansion across the MENAP and Southeast Asian region, when the tides turn.

Yes, all of this makes sense for Gobi Partners. But why is the Bank of Punjab interested. Here’s the deal.

Why it works for the Bank of Punjab

Commercial banks in Pakistan are typically characterized by risk-free lending to the government through treasury bills and similar instruments. They refrain from increasing exposure to the private sector significantly, particularly SMEs, where taking exposure to startups, a subset of SMEs, is unheard of. This could be corroborated by the credit extended to the private sector, which stands at just Rs. 10.1 trillion, which is 23.2% of the total outstanding credit as of Nov 2024. Furthermore, SME advances hover around Rs 624 billion, which is just 7.0% of the loans provided to the private sector.

The Bank of Punjab, although majority-owned by the provincial government of Punjab, is managed by veteran banker Zafar Masud, the CEO and President of the bank. Within the banking sector, Mr Masood is what you would consider a progressive. As such, the bank leadership is cognizant of the significance of startups and the role they play in societal progress. This has informed the development of an institutional ethos, which is modern and embraces exposure to segments like SMEs and startups, where most other banks tread cautiously. It is with this institutional view that the Bank of Punjab has partnered with Gobi Partners to provide impe-

tus to the expansion of Pakistani startups.

Speaking to Profit, Umer Khan, Head of FI, Correspondent & Investment Banking, elaborated that they are looking to invest in startups which are current and upcoming portfolio companies of Gobi Partners in Pakistan as these companies need growth capital to flourish but raising necessary funding has become an arduous task for them. Thus, BoP aims to provide a helping hand by extending debt financing at preferential rates, equity investments of up to 10% in select high-growth startups, credit lines for working capital, and other customized financial products, including credit guarantees.

The credit evaluation criteria for these startups will borrow heavily from the existing robust credit evaluation framework used by the bank but with due consideration to cash flow-based lending since startups typically have a dearth of tangible collateral on offer. This approach is becoming increasingly popular in the banking industry and aligns with SBP’s initiative of Digital Supply Chain Finance. However, this facility will only be available to companies, which fulfil the robust credit evaluation criteria of the bank.

This strategy will allow the bank to diversify its portfolio and get preferential access to the deal flow from Gobi Partners, giving an edge to the bank in discovering high-potential startups that align with its investment objectives. Mr. Khan further affirmed that the bank believes this is the right time to commence this scheme as the interest rates are declining and the economy is on a recovery path.

This landmark partnership between a leading commercial bank and venture fund signals a strategic evolution in Pakistan’s startup landscape. As traditional venture capital funding becomes more selective, the ecosystem is adapting by embracing conventional financing channels. Beyond its immediate impact, this collaboration may spark a broader transformation, dissolving the traditional boundaries between SMEs and startups, and opening new avenues for growth capital in Pakistan’s entrepreneurial future. n

OGRA’s gas price hike approval might make a small dent in the gas circular debt

Sui companies expected to be able to reduce their massive piles of receivables and payables, improving liquidity throughout the energy supply chain

Profit Report

In a move that make some progress towards address the burgeoning circular debt in Pakistan's gas sector, the Oil and Gas Regulatory Authority (OGRA) has approved substantial price increases for the country's two main gas distribution companies. The decision, announced on December 18, 2024, allows Sui Northern Gas Pipelines (SNGP) and Sui Southern Gas Company (SSGC) to raise their gas prices by 8.8% and 26% respectively.

This regulatory action is part of a broader strategy to tackle the complex issue of circular debt that has plagued Pakistan's energy sector for years. The price hikes are expected to help these state-owned companies reduce their receivables and improve their financial health, potentially easing the strain on the country's economy.

OGRA's decision comes in response to review petitions filed by both Sui companies for their revenue requirements for the fiscal year 2025. The regulatory body has recommended these price increases as part of the ongoing efforts to align gas tariffs with the actual cost of supply.

For SNGP, OGRA has allowed an Average Operating Asset (AOA) of Rs108.6 billion,

which is largely in line with the previously approved figure from May 20, 2024. The required return on assets has been set at 25.9%. Additionally, OGRA has now permitted 50% of the finance cost on running finance to be passed through, an increase from the earlier approval of 25%.

These adjustments are expected to have a significant impact on SNGP's financial performance. With the approved assets and return rate, SNGP's return on assets is projected to be Rs37.8 billion, including a Rs9.7 billion return on RLNG assets. After accounting for Unaccounted for Gas (UFG) disallowance and finance costs, analysts at Topline Securities estimate SNGP's earnings could reach Rs17.3 per share, with potential to increase to Rs28.2 per share if 100% finance cost on running finance is allowed.

The circular debt firing squad

To fully appreciate the significance of this decision, it helps to understand the concept of circular debt and its impact on Pakistan's energy sector. Circular debt in the gas sector occurs when the total cost of delivering gas exceeds the revenue generated from gas sales and govern -

ment subsidies. This shortfall accumulates over time, creating a cycle of unpaid bills that ripples through the entire energy supply chain.

The problem has grown significantly in recent years. By September 2024, the total circular debt in Pakistan's petroleum sector had ballooned to a staggering Rs2,897 billion, including Rs814 billion in interest. This figure represents a substantial portion of Pakistan's GDP and poses a significant challenge to the country's economic stability.

The roots of this crisis can be traced back to 2013 when gas prices were not allowed to increase despite rising production costs. This led to unfunded subsidies as the revenue from gas sales was insufficient to cover the growing expenses. The situation was further exacerbated by the introduction of expensive RLNG (Regasified Liquefied Natural Gas) into the system without a corresponding increase in consumer tariffs.

Historical context: SNGP and SSGC

To better understand the current situation, it's worth looking at the history and roles of SNGP and SSGC in Pakistan's gas sector.

Sui Northern Gas Pipelines Limited (SNGP) was incorporated as a private limited company in 1963 and converted into a public limited company in 1964. It has since grown to become the largest integrated gas company in Pakistan, serving more than 7.22 million consumers across Punjab, Khyber Pakhtunkhwa, and Azad Jammu & Kashmir.

SNGP's extensive network includes over 9,320 km of transmission pipelines and 142,998 km of distribution pipelines. The company's operations span 16 regional offices, covering 5,284 main towns and adjoining villages. In the fiscal year 2019-2020, SNGP's annual gas sales to consumers reached 623,724 million cubic feet (mmcf).

Sui Southern Gas Company (SSGC), on the other hand, has an even longer history. Founded in 1954, it is the oldest gas distribution company in Pakistan. SSGC's operations cover the southern regions of the country, primarily Sindh and Balochistan. The company's transmission system comprises over 3,220 kilometers of high-pressure pipeline, with distribution activities spanning more than 1,200 towns.

Both companies play crucial roles in Pakistan's energy infrastructure, but they have also been at the center of the circular debt crisis. The financial strain on these companies has implications not just for their operations, but for the entire energy sector and, by extension, the national economy.

Implications of the price hike

The approved price increases are expected to have effects on various stakeholders in the gas sector.

1. Consumers: The most immediate impact will be felt by consumers, who will see their gas bills increase. While this may cause short-term financial strain, it is argued that this is necessary for the longterm sustainability of the gas sector.

2. The Sui companies: SNGP and SSGC, the price hikes represent a much-needed financial boost. The increased revenue is expected to help them reduce their payables to upstream gas producers and LNG suppliers, potentially easing the circular debt burden.

3. Upstream companies: Gas exploration and production companies like Oil & Gas Development Company Limited (OGDCL) and Pakistan Petroleum Limited (PPL), which have been bearing the brunt of unpaid bills, may see improvements in their receivables position.

4. Pakistan State Oil (PSO): As a major supplier of RLNG, PSO has been significantly impacted by the circular debt. The price hikes could help in reducing PSO's receivables, improving its financial health and ability to

meet obligations to foreign RLNG suppliers.

5. Overall Energy Sector: By addressing one of the root causes of circular debt, these price adjustments could contribute to the overall stability and sustainability of Pakistan's energy sector.

While the price hikes are seen as a necessary step by many experts, they are not without challenges and criticisms.

Higher gas prices could contribute to overall inflation, potentially impacting the cost of living and industrial production costs. There are concerns that increased energy costs could affect the competitiveness of Pakistan's industries in the global market. The price hikes may disproportionately affect lower-income households, raising questions about energy affordability and social equity. Given the potential unpopularity of price increases, there may be political resistance to fully implementing these measures.

While the approved price hikes are a significant step, they are part of a broader set of reforms needed to address the circular debt issue comprehensively. The World Bank, in its latest update on circular debt, has emphasized the need for continued electricity and gas sector tariff reform to align tariffs with the cost of supply.

Other recommended measures include:

1. Implementing WACOG: Fully

implementing the Weighted Average Cost of Gas (WACOG) law to rationalize gas pricing.

2. Eliminating cross-subsidies: Phasing out cross-subsidies between different consumer categories to reflect true costs.

3. Restructuring distribution: Considering the restructuring of the gas distribution business to improve efficiency.

4. Incentivizing local exploration and production: Offering better rates to local Exploration and Production (E&P) companies to boost domestic gas production.

5. Developing gas storage: Investing in gas storage facilities to manage supply fluctuations more effectively.

The approval of gas price hikes for SNGP and SSGC is part of Pakistan's ongoing efforts to address its energy sector challenges. While it may cause short-term discomfort for consumers, it's seen as a necessary measure to ensure the long-term sustainability of the gas sector and to tackle the persistent issue of circular debt.

As Pakistan continues to navigate its energy challenges, balancing the needs of consumers, industry, and the broader economy will be crucial. The success of these measures will depend not only on their implementation but also on complementary reforms across the energy sector. n

The stock market’s rise is fueled mostly by banks parking assets in domestic mutual funds

Investors have shifted their asset allocation from fixed income and money market funds in a declining interest rate environment and towards equity mutual funds, which in turn has spurred the market rally

Profit Report

The Pakistan Stock Exchange (PSX) has been on a remarkable upward trajectory since September 2024, with the market delivering an impressive 35% return in both Pakistani Rupee and US Dollar terms. This surge is primarily attributed to a significant shift in investor sentiment, as local mutual funds – powered by inflows from banks

– have injected a substantial Rs58 billion (US$207 million) into the market during this period. The influx of capital marks a notable transition from fixed income instruments to equities, reshaping the investment landscape in Pakistan.

According to a recent research report by the equity research team at Topline Securities, a Karachi-based investment bank, there are several reasons behind the market rally.

1. Falling yields on fixed income instruments: A key factor propelling this market

rally is the sharp decline in yields on fixed income securities. Treasury Bills, once offering peak yields of 24.73% for 12-month and 24.51% for 6-month tenors in September 2023, have seen their returns plummet by over 1,250 basis points. As of December 19, 2024, these instruments were yielding 12.20% and 11.9% respectively, significantly diminishing their appeal to investors seeking higher returns.

2. Limited alternative investment options: Unlike previous market cycles where investors had a variety of high-yield alternatives such as foreign currency, real estate, gold, and prize bonds, the current economic environment has narrowed these options. Stricter regulations on foreign currency purchases, increased taxation and compliance requirements for real estate transactions, and the discontinuation of high-denomination unregistered prize bonds have collectively steered investors towards the stock market.

3. Mutual fund asset growth: The mutual fund industry in Pakistan has experienced remarkable growth, with Assets Under Management (AUM) reaching Rs3.8 trillion (US$13.7 billion) in November 2024. This represents a substantial increase from Rs2.8 trillion in July 2024 and Rs1.6 trillion in December 2023, translating to a staggering 135% growth in just 11 months.

Interestingly, approximately half of the 135% increase in mutual fund assets occurred after July 2024. This surge is partly attributed to the banking sector's Advance to Deposit Ratio (ADR) issue, which prompted a redirection of deposits from banks to Asset Management Companies (AMCs) and other investment avenues.

The reallocation of funds has led to significant growth in specific mutual fund categories. Money market funds, both Shariah-compliant and conventional, saw their combined size expand to Rs1.54 trillion in November 2024, up from Rs902 billion in December 2023. Similarly, fixed rate/return funds experienced substantial growth, increasing from Rs92 billion in December 2023 to Rs306 billion in November 2024.

Equity allocation analysis

To accurately assess the potential for further equity market inflows, analysts have employed a nuanced approach in evaluating the current allocation to equities within mutual funds.

The analysis excludes money market funds and fixed rate/return funds, as these typically attract investors with lower risk appetites who are less likely to shift to equities. Additionally, 30% of income funds were removed from the calculation, accounting for

corporate treasury investments aimed at fixed income capital gains rather than potential equity conversion.

After these adjustments, the analysis reveals that equities currently represent 20.7% of the adjusted AUMs and 8.2% of total AUMs. These figures are significantly below the 10year averages of 45.6% and 28.9% respectively, suggesting considerable room for increased equity allocation.

Given the current allocation levels compared to historical norms, there is a strong possibility of sustained inflows into the equity market. Analysts estimate potential inflows ranging from Rs130 billion to Rs165 billion over the next 12 months, translating to a monthly net inflow of Rs11-14 billion or US$39-50 million.

Based on these projected inflows and assuming stable economic conditions, some market observers anticipate the PSX index could potentially cross the 150,000 mark by December 2025. This projection factors in an estimated price-to-earnings ratio of 5.2 times and a dividend yield of 9%.

Economic context and market drivers

The bullish sentiment in the stock market is further supported by optimistic economic growth projections. The State Bank of Pakistan has forecasted GDP growth for the fiscal year 2025 to be in the upper half of the 2.5-3.5% range, an improvement from the 2.52% growth recorded in FY2024[1].

Analysts are also positive about corporate

earnings prospects, with expectations of double-digit growth in the coming year. This anticipated earnings growth is seen as a crucial factor in sustaining the market's upward momentum.

Despite the overall positive outlook, several factors could potentially impact the market's trajectory. Fluctuations in international markets and geopolitical events could influence investor sentiment. Any increase in political uncertainty may dampen investor confidence. Future decisions by the State Bank of Pakistan regarding interest rates could affect the relative attractiveness of equities versus fixed income instruments.

Implications for investors