08 Stock splits can be the best of both worlds for the stock exchange

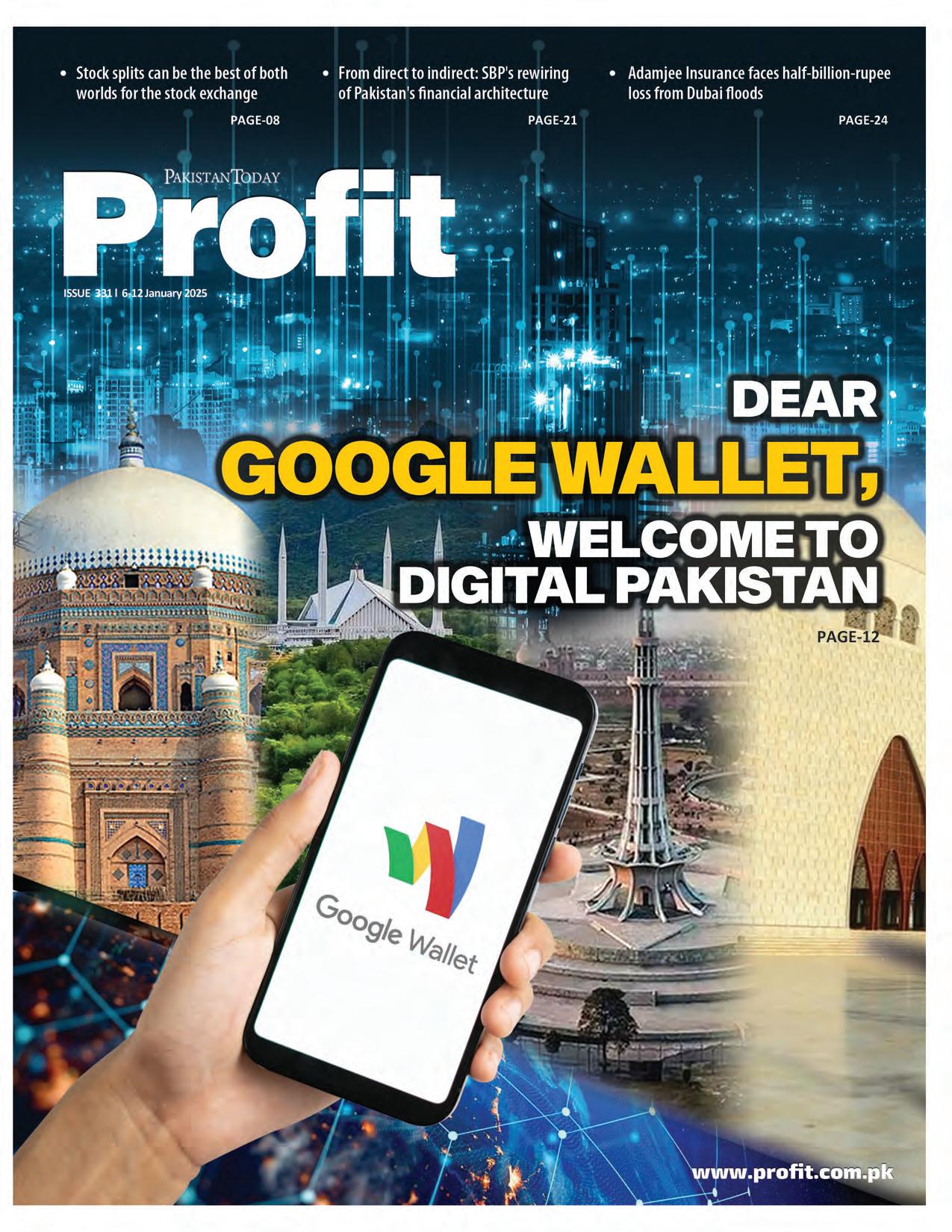

12 Dear Google Wallet, welcome to Digital Pakistan

19 The Lucky Conglomerate is entering the asset management business. Their new CEO comes with baggage

21 From direct to indirect: SBP’s rewiring of Pakistan’s financial architecture

23 What surprises lay in wait for Pakistan’s Auto Market in 2025?

24 Adamjee Insurance faces halfbillion-rupee loss from Dubai floods

25 Fertilizer volumes to see strong December rebound, but 2024 sales still lag

28 A catastrophe looms on our doorsteps

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Stock splits can be the best of both worlds for the stock exchange

With SECP approving the guidelines, this can open the floodgates for stock splits in the coming future

By Zain Naeem

From June 2023 to December end 2024, the stock market has seen the index increase by almost 200%. As recently as 23rd of June 2023, the index was barely able to maintain the levels of 40,000 points. Less than 18 months later, it seems like a figment of the imagination where the index touched 117,000 points on 17th of December 2024. With the index increasing, its constituents’ stocks have also seen their values increase. The increase in value ends up becoming an impediment of sorts. Investors and other participants in the market were able to buy a bigger number of shares two years back with the same level of investment than they can now.

As the price of the shares becomes too high, the same amount of investment is buying a lower number of shares. As the buying capacity falls, there are fewer trades taking place which dries up the liquidity and movement. This is the reason why companies like Unilever foods only sees 30 day daily average trades of less than 100 shares due to its price being in excess of Rs. 21,000 per share. In comparison to this, a share like K-electric sees 30 day daily average trade of 70 million shares as its price is less than Rs 10 per share.

As Securities and Exchange Commission of Pakistan (SECP) approves the new guidelines for stock splits, this can prove to be a solution that is able to kill two birds with one stone. It will allow companies to reduce the price of their shares and protect themselves from any additional value destruction that might take place. Here is how it is going to work.

In terms of the situation that exists, the tools that are available at the disposal of the company is to either give out cash dividends or bonus shares which can reduce the price of the shares with no additional investment on the part of the investors. Breaking down the mechanics of both of these tools is rooted in the fact that the portfolio value remains the same before and after the dividend was given out. For example, a share price of a company is trading at Rs 10 and they announce a dividend of Rs 1 per share to be given out. When the dividend is given to the investor in their account, they will receive the dividend in their bank account and now the share will trade at Rs 9 once the trading starts the next day. Even though this sounds simple, there is some value destruction as the investor will receive the dividend after 15% withholding tax has been deducted. This would mean that the investor will actually get Rs 0.85 and his investment would have fallen by Rs 0.15 as it has been handed over by the company.

When taken to its extreme, this value destruction can compound and add up in the end. The case of Pakistan Hotel Developers has taken place recently which illustrates this point. The hotel company was selling off its assets and felt that the best way to liquidate the invest-

ment of the investors was to give out a one time cash dividend. This culminated in a historical dividend announcement of Rs 725 per share. The dividend being paid out might be a good return on investment for the investor, however, once the withholding tax is accounted for, the investors actually ended up paying Rs 108.75 per share in the form of withholding tax.

The impact of the dividend actually broke the inner workings of the market. On the last day of trading, the share price of the company closed at Rs 695. Normal operations would have meant that the share price should have opened at -Rs 30 as the dividend was given out. This could not be done so the share price opened at Rs 0.01. An investor who bought the share for Rs 695 would have earned Rs 725 in terms of dividend and still be able to sell his shares for Rs 0.01 earning Rs 725.01 for an investment of Rs 695. An instant return of Rs 30. However, this fails to take into account the value destruction that was taking place. An investor who would have bought the shares for Rs 695 would actually only get a dividend of Rs 616.25. Even if the investor held the shares and sold them later at the high it has seen since, they would have sold it for Rs 65 which still means that they lost Rs 14 from the initial investment they had carried out. The tax deduction becomes a burden for the investor and sees their investment actually lose value.

The second way of reducing share price takes place in the case of bonus shares. The company has reserves that it has built up over time and it feels that it can use these reserves to give out a bonus share as dividend to its investors. The most recent example of this took place in the share of Mari Petroleum which gave out a cash dividend of Rs 134 and a bonus of 800%. This meant that investors would get Rs 134 and they would also receive 8 bonus shares for every one share they held in the company. The price of the stock was trading at Rs 3537 on the last day before the dividend was credited. Once it was credited, the new price opened at Rs 378 once the market opened the next day.

According to the tax policy implemented by the Federal Board of Revenue (FBR), the company was supposed to deduct 10% of the bonus shares as tax. Once the shareholders paid the tax that was liable on them, these shares would be released to them. The flaws in this law have been discussed by Profit before in terms of the fact that this tax is not seen anywhere in the world and is not levied on any realized gain or profit that has been accrued to the investor.

Even when this law was applied by the management at Mari, they saw that they had to collect tax at Rs 457 per share when the price after it became ex was set at Rs 378. As the share price fell below Rs 457, the investors felt that they could buy the shares from the market at a cheaper rate rather than pay a higher cost to the company to get their shares released. The compa-

ny felt that they would be left holding the bag in terms of paying the higher amount of taxes and they got an additional freeze on the shares placed by Islamabad High Court. The impact of this was that many of the investors ended up seeing a higher amount of their shares being held by the company and this led to additional cost that they had to pay for the inaptitude of the law in the first place.

These recent examples show that the tools that are available with the companies can be utilized, however, there is value destruction and gaps that exist which mean that the investors and companies are on the hook to pay the cost of these measures. This can be cured through the use of stock splits.

Stock splits are a measure in which the company is able to increase the number of its shares floating the market and reduce the par value of each of these shares. The economic reality still persists where the portfolio value of the investor remains the same. Before a stock split was announced, an investor had 100 shares of a company at Rs 10 taking his total investment to Rs 1,000. Now, the company carries out a stock split of 2-for-1 which means that one share is divided into two. Now the share price of the stock will be Rs 5 and the investor will have 200 shares where he used to hold 100. His investment will still be worth Rs 1,000 but now he has more shares in his hand.

The biggest benefit of this move is that companies that have a high price can use this to reduce the price of their shares and make sure that the trading volume does not fall. As buyers retain an interest in the shares of the company, the sellers will have a market where they can sell their shares. This leads to greater market depth where buyers can absorb the selling taking place in the stock without the seller seeing the price fall by a great deal.

Market depth also means that price discovery or setting the price of a stock is more prevalent. If Unilever feels that they want trading interest to be retained in the market, they can carry out a stock split which can increase its trading volume. Lower prices also make sure that there is greater access for retail investors who can trade with convenience.

The company can also benefit from this measure as they can carry out secondary share issues, through an Initial Public Offer, or seek additional investment by offering the shares through a right issue. More investors would be willing to apply for an issue of shares if the price is more affordable and accessible to them.

The stock split also becomes beneficial when the recent increase in share price is considered. A year ago, with the index languishing at 40,000 points, many of the stocks were trading at lower values. As the prices have increased, many shares are seeing lower trading volumes which can be stimulated once a stock

split is carried out.

The guidelines that were issued by Pakistan Stock Exchange (PSX) and approved by SECP have been carried out now as the exchange felt that the trading volume was decreasing which reduces the interest of investors in the market. Stock splits have already been allowed by SECP under Section 85(1)(c) of the Companies Act 2017 which allow for the move to be carried out after a special resolution has been passed by the board of directors. Before this, Companies Ordinance 1984 mandated that any such move had to be presented in the Annual General Meeting of the company.

This restricted the companies to some extent as they could only exercise this power once every year and they had to do so formally in a meeting. Companies Act 2017 reduced this requirement and allowed for a special resolution to be passed by the board and the members of the company at a general meeting now.

In the history of the capital markets, there have been only three occasions where such a stock split has been carried out. In October of 2014, Hum Network carried out a stock split where they gave out 9 shares for every 1 share held, reducing its share price from Rs 171.8 per share to Rs 17.18 per share. The company also saw its par value per share decrease from Rs 10 to Rs 1. Once the split was carried out, the company saw 1-month trading volume of 74 million shares a month after the split which had been around 28 million shares before that split.

A similar step was taken by National Foods which also carried out a stock split of 2-for-1 in October of 2014 reducing its par value from Rs 10 to Rs 5. Before the split was carried out, the company saw monthly average volumes of less than 100,000 shares which increased to almost a million shares in the month after the split. The most recent stock split was carried out by Synthetic Products Limited which carried out a 2-for-1 stock split seeing its monthly average volumes increase from 0.5 million shares to 3 million shares after the split was carried out.

One of the biggest benefits that is accrued in the face of a stock split is the fact that investors end up owning more shares of the company, however, there is no tax liability that is levied on them. As now additional value is generated and realized, the current tax code does not see any benefit from a stock split and this means no value destruction is taking place. This allows the company to keep the share price affordable while no additional tax liability is created after the split has been carried out. Knowing the efficiency of FBR babus and the geniuses in Q-block, nothing can be said with certainty whether these will be taxed in the future though.

In terms of the cost and resources that need to be used, stock splits might lead to a change in the memorandum and articles of associations of the company which have to be handled by its legal counsel. Once the approval of the members has been taken, the necessary fees and paperwork has to be filed to the SECP in order to complete the regulatory formalities of a stock split. The exchange also has to be made aware once the resolution is passed so it can be disseminated to the shareholders. Central Depository Company also charges an additional 0.16% of the market value of shares and stamp duty has to be paid by the company which is miniscule compared to the benefits derived.

Some of the market experts feel that this can be a starting point where many of the companies will start to use stock splits in order to impact the price in the market rather than give out dividends in the first place. Mohammad Aitazaz Farooqui, Head of Research Providus Capital, feels that “If (the new guidelines) are conducive, general action should be for companies to go for splits rather than bonus to avoid tax on bonus.” The value destruction seen due to dividends are a burden on the companies and investors which can be circumvented.

Others are a little cautious like Yousuf Farooq, Director Research at Chase Securities, who says that there will be “(n)o fundamental impact on the value of companies…..(stock splits) could improve liquidity going forward.” Experts also feel that any such move can fuel the rally to continue in the market as the interest of buyers will be sustained based on the lower prices.

The function of capital markets is to allow for companies to gain access to funds from the investors by selling their shares in the market and getting additional funds for their operations. In order to make sure this access is unrestricted, the share price needs to be at a level where investors find it affordable and can easily trade in the market. In case the price gets too high, the companies see this source dry up.

Even for investors trading with each other, a high price for a stock can become a barrier for trading as many of the investors would not be able to purchase at such high prices. In the face of this, the companies usually look to give out dividends in the form of cash or bonus shares in order to reduce the prices. The only problem with that is due to the tax implications, the investors actually see the value of their portfolio fall. Stock splits can be an option where investors will be able to retain their investment while the share price falls for the company. This can prove to be a more elegant solution available to the companies who can do so without using any cash or reserves available to itself. The issuing of the guidelines can trigger a flood in the coming months. n

By Hamza Aurangzeb

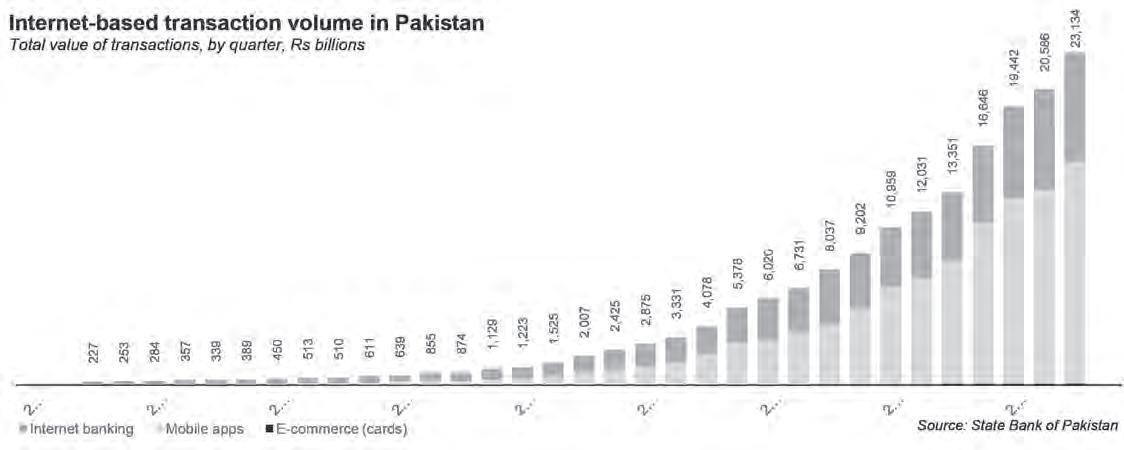

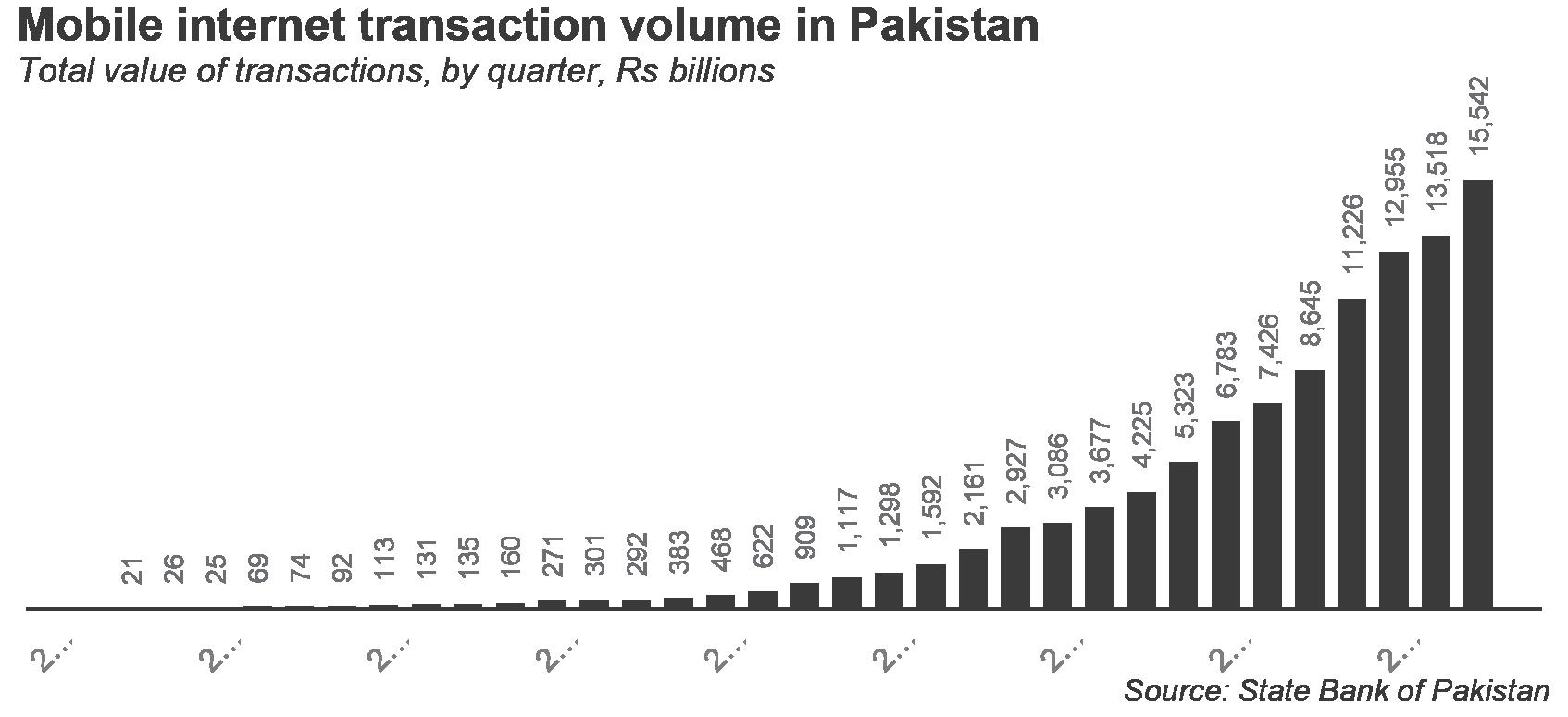

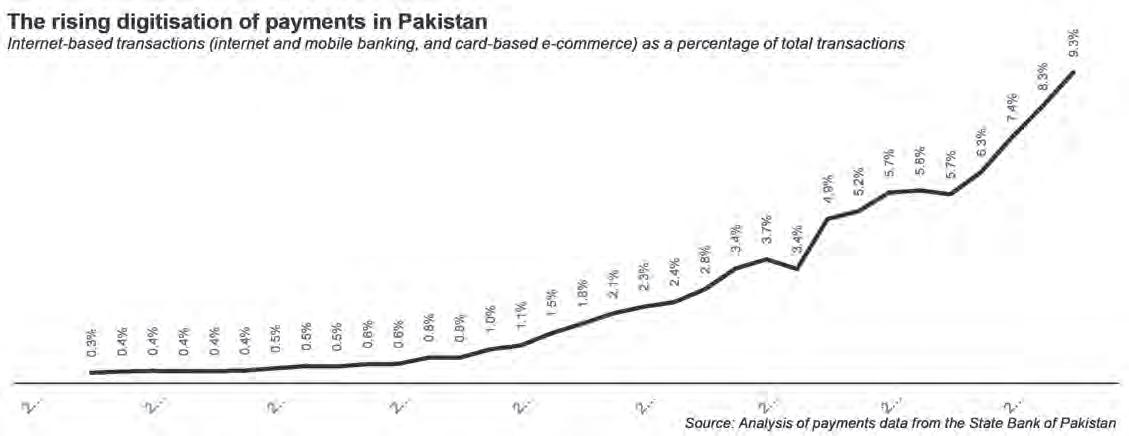

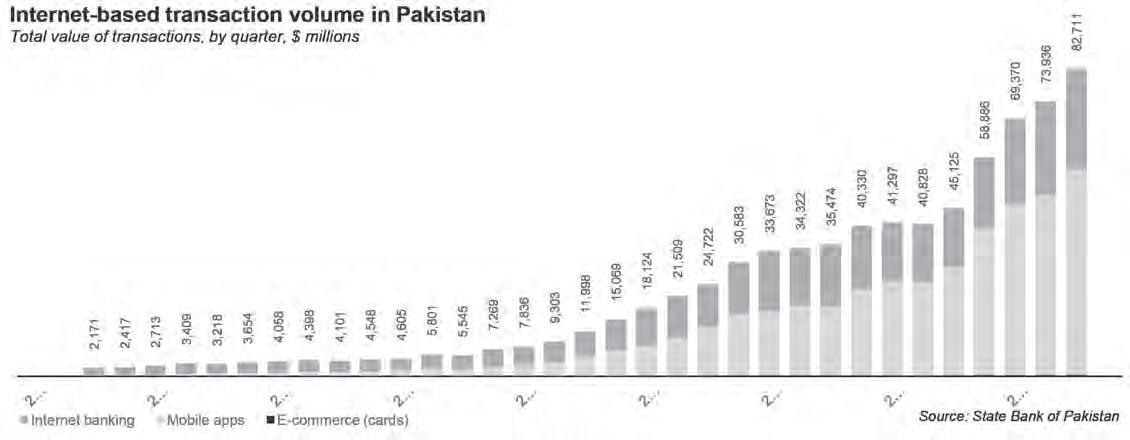

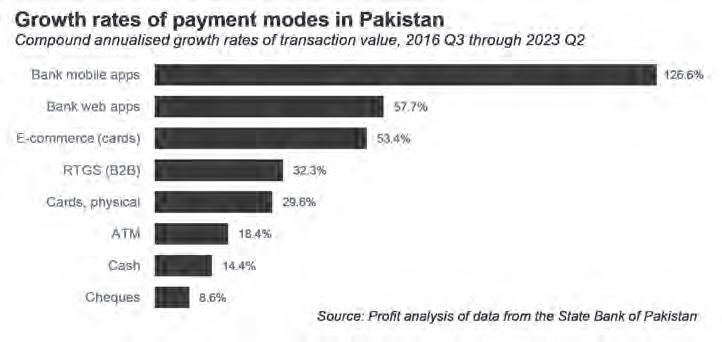

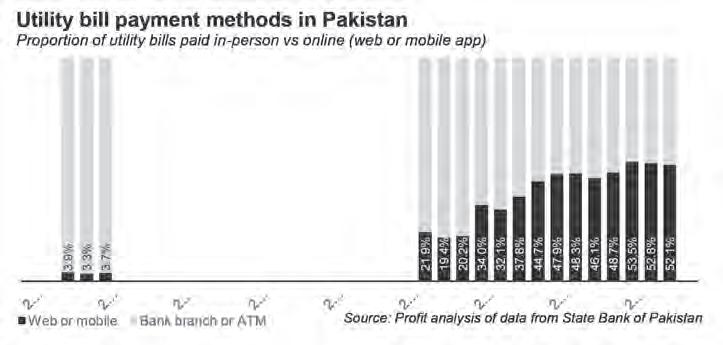

Over the past year, the following two milestones have been crossed: Pakistanis conducted a higher value of transactions from their bank’s mobile and web apps than they withdrew in cash from ATMs, and the majority of utility bills in the country are now paid online.

Digital Pakistan is here, and despite most people assuming that Pakistanis like dealing in cash, the fact remains that electronic payments now account for 9.3% of the total value of all transactions that take place in the country, a number that has doubled over the past two years. That estimate is based on Profit’s analysis of data published by the State Bank of Pakistan.

While cash remains king in Pakistan - with nearly 36% of all transactions in the country taking place in physical cash between two parties where neither uses their bank account - digital payments are by far the fastest growing segment.

it appears that global tech powerhouses are beginning to take notice.

A week ago some internal documents from Google were leaked, which instigated conjectures of Google Wallet’s entry in Pakistan. Although there has been no formal announcement from Google, the notion that it is set to launch in Pakistan by early 2025 is widespread. In this story, Profit tries to reimagine the digital payments space in Pakistan after the debut of Google Wallet.

The evolution of Google Wallet and Google Pay

The digital payments landscape has undergone a radical transformation over the past decade or so and the overview of this paradigm shift in digital transactions would be incomplete without discussing two flagship financial products of Google, Google Wallet and Google Pay. These platforms epitomize how technology has reshaped financial transactions.

Google explored the domain of digital payments by introducing Google Wallet in 2011. It was envisioned as a comprehensive digital wallet, enabling users to store their credit and debit cards, loyalty cards, and gift cards in one place. At its core, Google Wallet aimed to enable peer-to-peer (P2P) money transfers and simplify payments through NFC (Near Field Communication) technology, allowing contactless transactions at physical stores. This platform despite its innovation faced numerous obstacles, where scarce NFC-compatible terminals, a nascent mobile

payments market, and cutthroat competition from established financial services adversely impacted its adoption.

In 2015, Google introduced Android Pay, a refined mobile payment service designed to streamline the user experience. Unlike Google Wallet, Android Pay focused solely on enabling transactions, allowing users to make contactless payments and purchases within apps. This shift marked the beginning of Google’s efforts to develop a holistic payments ecosystem, which remained fragmented up till then.

By 2018 Google realized that it was better if they just merged Google Wallet and Android Pay into a single platform; and voila! Google Pay was born. This unified platform offered strengths of both services, Google Wallet’s peer-to-peer payment capabilities and Android Pay’s streamlined payment processes. Google Pay emerged as a versatile platform that enabled in-store payments, online transactions, and peer-to-peer transfers, all under one consolidated brand.

The rebranding not only simplified Google’s payment offerings but also aligned them with the global trend of consolidating financial services into all-in-one solutions. Google Pay’s chic user interface, complemented by Google’s entire suite of services, distinguished it as a leading player in the digital payments industry.

In 2022, Google Wallet resurfaced as

a distinct service from Google Pay. However, this time around the rationale was much more coherent. It was envisaged as a secure repository for digital cards, passes, and IDs. It provided users with a convenient way to store everything from transit passes to government-issued identification, focusing on organization rather than transactions. This bifurcation allowed Google Pay to remain dedicated to facilitating payments, while Google Wallet catered to the growing demand for digital credential storage.

The core functionality of Google Wallet

Although Google Wallet and Google Pay are distinct applications, their transaction flow for digital payments remains the same. The transaction flow within Google Wallet commences when a user opens the app on their smartphone. Afterwards, they are presented with a variety of stored payment methods, including credit and debit cards, gift cards, loyalty cards, and even digital passes like boarding passes or event tickets. Then the user selects the card or payment option they wish to use, however, the primary account number or PAN is not stored on the device itself, instead, it’s saved on a Google server. This step is designed for simplicity and efficiency, allowing users to quickly choose their preferred method from a

variety of payment options without the hassle of carrying their card around, a big relief for Pakistanis I suppose.

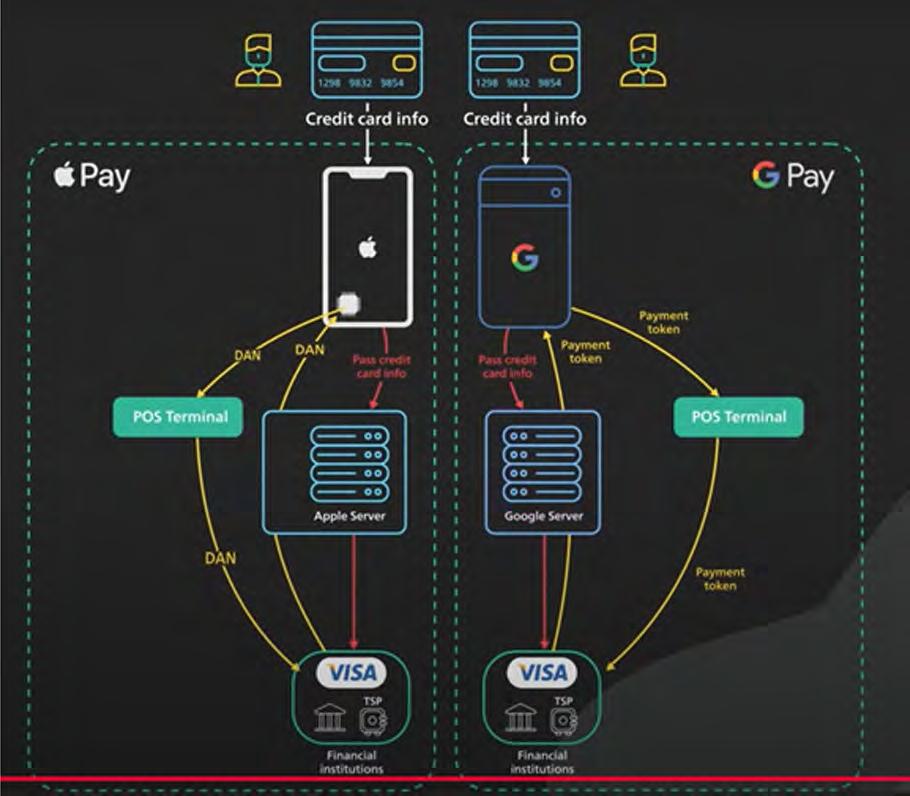

When it comes to in-person transactions, Google Wallet leverages the Near Field Communication (NFC) technology, where the user simply taps their device near the POS terminal, which then communicates wirelessly with Google Wallet, while in the case of online transactions, the user can simply select their stored payment method during checkout and confirm the payment via the app. Once the payment method is selected, Google Wallet tokenizes the card information, replacing the actual card details with a secure, encrypted token. This ensures that sensitive financial information is not exposed during the transaction, enhancing the security of the payment process.

Once the payment method is tokenized, the encrypted data is sent to the payment gateway for further processing. The payment gateway securely transmits this data to the bank or financial institution that issued the card. The bank verifies the transaction by checking the available balance or credit limit and ensuring that the tokenized card is valid. If the bank approves the payment, it sends the authorization back through the payment gateway and the merchant’s POS system. At this point, the transaction is authorized, and the payment is processed. After the payment is authorized, the merchant’s system confirms the successful transaction. The user typically receives a notification on their device, confirming that the payment has been processed.

Now the transaction flow of Apple Pay and Google Wallet are similar, however, they

differ in two ways. Firstly, Apple Pay does not store the card information of its users, unlike Google Wallet which stores the card information of its users on its servers. Moreover, Apple Pay generates a Digital Account Number which is stored in Secured Element on iOS smartphones to communicate with financial institutions. In contrast, Google Pay utilizes a payment token that is stored on its servers.

The impact of Google Wallet on digital payments

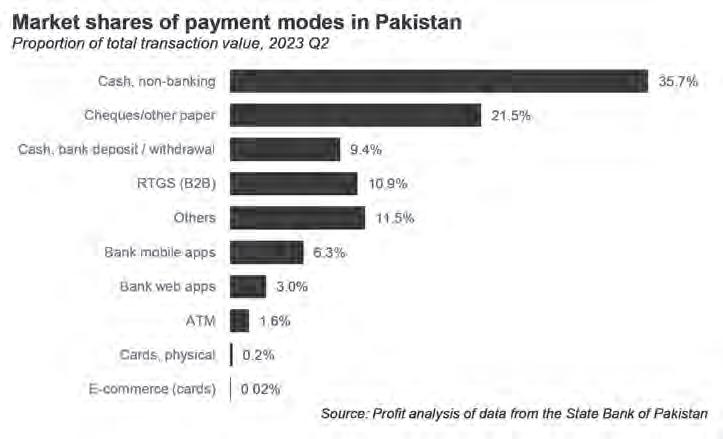

Over-the-counter (OTC) transactions involving cash and cheques are the dominant payment stream in Pakistan despite the recent

surge in digital payments. OTC transactions constitute around 16% of total transactions in the country and these could be further divided into 9% via bank branches and 7% through branchless banking agents. The transactions conducted via bank branches hold a share of 82% in terms of value, while the share of agent-based branchless banking transactions stands at just 1%.

In Pakistan, there are only 55.6 million payment cards as of Sep 2024, which means less than a quarter of Pakistanis have payment cards and there is a high-level duplication among these payment card owners. Moreover, most of them reside in urban areas, whereas people in rural areas rarely use a payment card for transactions. During 1QFY25, around 360 million payment card transactions were registered, where three major channels ATM, POS, and E-commerce were utilized. ATM led the charts with 243.4

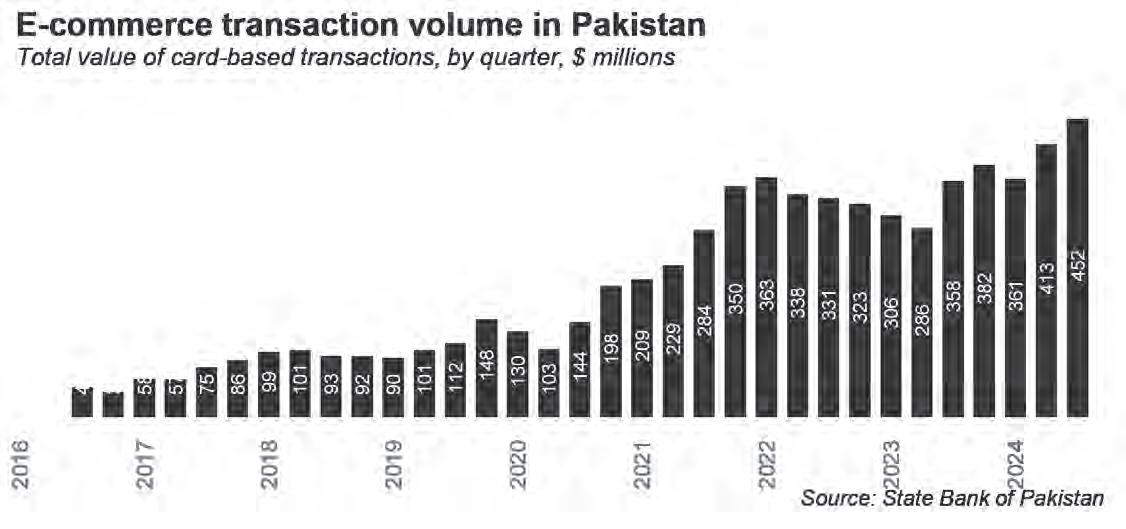

million transactions, POS stood at second place with 92.4 million transactions, while E-commerce claimed the third spot with 24.6 million transactions. The value of ATM transactions clicked at Rs3.8 trillion, while POS and E-commerce transactions moved funds worth Rs483.8 billion and Rs126.4 billion, respectively.

Banking veterans believe that the introduction of a digital application like Google Wallet, which is compatible with payment cards of any financial institution will accelerate the expansion of digital payments through POS machines and E-commerce websites.

A senior financial services consultant elaborated that major acquirers in Pakistan are ready to be integrated with Google Wallet and they would forge this strategic partnership with alacrity if it enters the market soon. He further affirmed that the majority of the POS machines in Pakistan after 2023 are

NFC-enabled and the ones which are not are being replaced.

The widespread availability of NFC-enabled POS machines will be instrumental in ensuring that card-based payments flourish. Not to forget that Google Wallet can also be integrated with e-commerce websites, where the customer can pay using any payment card at the checkout, translating into a seamless user experience. This is great, isn’t it?

But what about the small merchants that run mom-and-pop stores?

Well, we have QR codes for such merchants. They can utilize the facility of QR codes to accept payments, which is congruent with the system of Google Wallet, where payments will be deducted from the payment cards of users. JazzCash processed Rs182 billion approximately through QR codes in 2024 alone, which showcases the growing popularity of QR codes in Pakistan.

Limitations of Google Wallet

It is indisputable that the introduction of Google Wallet in Pakistan will boost card-based payments in the country, but they only form 21% of digital transactions by volume, which represent only 12.0% of the value. Thus, what about other forms of digital transactions such as funds transfers, bill payments, mobile top-ups, and other miscellaneous payments?

It is expected that Google Wallet initially won’t offer full-fledged services in Pakistan including peer-to-peer funds transfer, unlike India, where Gpay provides all kinds of payment services. In fact, it is the second largest player and holds a 37% share of Unified Payments Interface (UPI) transactions in India. Therefore, the conventional modes of digital payments like mobile banking, mobile wallets, and EMI wallets will continue to dominate the scene for the time being in Pakistan. Google Wallet’s integration with networks like RAAST and 1Link which function as the foundation of digital payment infrastructure will be a gradual procedure that will transform the payment networks in Pakistan over time.

Moreover, the limited broadband penetration rate and the scarcity of POS machines in underdeveloped rural areas will act as predicaments for Google Wallet in expanding its services in the said areas. Nevertheless, we do have success stories of telco-backed mobile wallets like Jazzcash and Easypaisa that have played a colossal role in enhancing financial inclusion across the country, particularly in underdeveloped rural areas. Their persistence and endurance have borne fruit and now there are 122.9 million wallets in Pakistan out of which 55.4 million are active as of Sep 24.

Mobile Wallets like Jazzcash and Easypaisa manage their massive ecosystem in rural areas through an extensive network of branchless banking agents, which assist the rural population in depositing, withdrawing, and transferring money from one mobile wallet to another. In simple terms, these agents function as a mini bank. This community of branchless banking agents has now expanded to 693,178 as of Sep 2024. Hence, Google Wallet will prove to be ineffective in bucolic areas due to its dependence on robust digital infrastructure present only in urban areas and the absence of a broad network of agents required to serve the rustic localities.

Google Wallet’s Stealthy Expansion

During an interview with Profit, a senior financial services consultant stated that he believes Google intends to launch only Google

Wallet in Pakistan at first just to test the waters, get a feel of the market and understand the dynamics of the local financial system. It plans to expand its footprint, familiarize people with its services and harness strategic partnerships with key financial institutions along the way.

Once Google Wallet establishes a distinct place and integrates with key financial platforms, it will begin offering its full suite of financial services, which includes peerto-peer fund transfers, bill payments, mobile top-ups, all of that stuff and much more. These features will allow Google Wallet to compete directly with mobile wallets such as Jazzcash and Easypaisa along with EMI wallets like Sadapay and Nayapay. The niche created by established wallets in the segment of digital payments will become highly contested.

If we look at branchless banking, digital payments are the dominant mode of transactions in the segment as during the 1QFY25,

around 910.1 million transactions were initiated by mobile wallets in total, which amounted to Rs3.0 trillion. The sub-segment of funds transfer was miles ahead of the rest with 527.2 million (57.9%) transactions, which channelled Rs2.65 trillion (87.2%). On the contrary, agent-based branchless banking transactions accounted for only 110.1 million transactions, which represented a value of Rs839.0 billion.

The extension of Google Wallet in the service of peer-to-peer funds transfer, particularly, will have a detrimental impact on all contemporary wallets. Mobile wallets like JazzCash and Easypaisa might sustain Google’s assault due to their nationwide network that serves both urban and rural areas. However, EMI wallets such as Sadapay and Nayapay, which specifically focus on top-tier urban centres, might end up folding their businesses in the country, as they are already mired in a variety of complications, and their target market would coincide with that of Google Wallet.

Moreover, the transactions flowing through Google Wallet would introduce an additional dimension to Google’s services as they would provide heaps of data to the tech giant, enhancing its understanding of patterns like consumer spending, shopping preferences, saving habits, and payment methods, etc. It will use this accumulated data to improve its algorithms, which would showcase advertisements to users that adhere to their preferences like credit card offers, promotions of loans, food delivery discounts, or e-commerce sales. Furthermore, this stack of data will also empower Google to offer value-added services to merchants such as analytics, promotional

tools, and loyalty programs for customers. The prospect of Google Wallet’s launch in Pakistan has the potential to completely revolutionize the digital payments landscape. However, it will be a systematic transition which will take place over several years. Google Wallet will take its sweet time to

acclimatize to the local market and claim its territory but once the tech giant begins its onslaught, the existing digital wallets might find themselves in jeopardy. Hence, they should do their homework and brace themselves for the turning tides in advance to avoid being caught napping. n

The Lucky Conglomerate is entering the asset management business. Their new CEO comes with baggage

The conglomerate is expanding into a new field looking to build on its success by appointing Mohammad Shoaib as CEO, whose last appointment was at Al-Meezan Investments

By Zain Naeem

Mohammad Shoaib is far from a household name. He is not a politician, a cricketer, or a famous lawyer whose face is splashed on the front page of the papers. In fact, he isn’t even peripherally famous. But if you have ever had anything to do with Pakistan’s asset management sector, it is a name you will recognise very well.

At a time when mutual funds and investing were not even a concept in Pakistan, Shoaib established Al Meezan Investments. Not only was this an asset management company, it was a Shariah Compliant investment fund which allowed investors to invest in a way consistent with their religious beliefs. For nearly three decades, he shepherded a team that at its height grew to over 600 employees managing over $1.6 billion in assets.

He was one of the founding fathers of asset management in Pakistan, and under him Al Meezan grew to great heights. Then, early last year, he suddenly resigned from his position as CEO. Initially, it seemed he was just stepping back and preparing to retire. Then the rumours started to circulate. These were not corroborated

by the Securities and Exchange Commission of Pakistan (SECP), but managed to cause plenty of commotion in the asset management sector.

Now, nearly a year after he left the company he built from scratch, Mr Shoaib is embarking on building another. He has been appointed Chief Executive Officer (CEO) of Lucky Investments Limited, a new asset management company supported by one of the largest conglomerates in the country. The commitment of Lucky in terms of making this venture a success is clear as they have chosen Mohammad Shoaib to captain this ship. The man literally wrote the book on Shariah Compliant fund management in the country and has the skill set to do so. But will lightning strike twice for Shoaib?

Corporate Landscape

The corporate landscape of Pakistan is dotted with different companies and their unique structures. Many of the large groups operating look to invest in their own ventures through cross holdings or look to keep all of its investment ventures in house. This keeps the investment within their control and they get to use these funds in order to build their own position. In such a corporate

culture, there are business groups which look to expand their portfolio of services beyond the conventional fields. Lucky is the new one which has decided to set up its own AMC.

Asset Management is a field which is mostly run and handled by banks or financial institutions. The nature of an asset management company is to collect funds from the market and then invest these funds into assets that it is able to manage. These assets are categorised and separated based on the risk and return yielded which creates mutual funds that are maintained. New investors are sought to raise additional funds and old investors are allowed to liquidate their positions. In order to manage and run these funds, the AMC charges a fee for doing so which is tied to the assets it is managing. Banks and financial institutions are able to run AMCs easily as they deal with funds on a daily basis and they can use mutual funds in order to manage the risk and return that they require in order to remain profitable. They also encourage their depositors to invest in these funds in order to get a better return compared to fixed deposits.

In a field dominated by banks and financial institutions, there are certain groups which have looked to run their own AMC.

Atlas and Lakson are two of the bigger names which expanded their portfolio of services and added AMC as a service they provided in the market. Now it seems like Lucky is also interested in establishing its own company. There is a commitment at the company to look to venture into new business avenues that it has not contemplated before. As its first foray into this field, Lucky has acquired the AMC that was established by Interloop and now has a license to operate such a company. Interloop was only able to run one equity fund which had Rs 2.16 crores under management. It can be expected that Lucky will look to expand and increase the portfolio and funds it manages.

Lucky group is a gargantuan of the corporate world. Run by Younus Brothers group, the company has varied interests from power generation, chemical manufacturing, auto assembly, cement manufacturing, textile mills and a mall to name a few. The empire has been built on due to the ambition of its owners who are always looking for an opportunity to expand their footprint. This new venture is in line with this intent. The group feels that there is an opportunity which can complement its diversified revenue streams. This is normal for a company looking to grow out of its own shell. The thing that is raising eye brows is who they have chosen to run the company for them. Mohammad Shoaib has been chosen as the Chief Executive Officer for Lucky Asset Management Limited.

The Mohammad Shoaib story

Shoaib is known as being the person who built Al Meezan Investments from scratch up into the behemoth it is today. Al Meezan was set up in 1995 and the goal of the company was to establish itself as being a Shariah Compliant option available to its investors. Shoaib was able to use his education and practice what he had learned in his past and apply them to a fund management style which was still in its infancy in the country. He had studied at the Government College of Commerce and Economics and then finished his MBA at Institute of Business Administration in finance and marketing.

Shoaib’s professional career started at Pakistan Kuwait Investment in 1990 where he became the senior vice president of capital markets in a space of five years. In 1995, Shoaib felt that there was a dearth of investment opportunities in the country which could be availed by the investors. A small fund named Al Meezan was established whose sole purpose was to provide Shariah Compliant solutions to the market ranging from equity, sector, balanced, asset allocation, fixed income and voluntary pension funds.

During his tenure at Al Meezan, Shoaib

showed his dedication to his work by first becoming a CFA Charterholder in 1997. In terms of the finance industry, the CFA charter is considered the gold standard and is the most sought after certification by people interested in working in finance. Shoaib was also the founding president of the CFA Society in Pakistan in 2002. In addition to this, he has held many other voluntary positions from nominee director on the board of Pakistan Stock Exchange, board member of Institute of Financial Capital Markets and member of Academic Board of Institute of Business Administration. He has also held the position of Chairman at Mutual Funds Association of Pakistan which is the body that oversees the performance and issues related to the mutual fund industry.

After nearly three decades at the helm, Shoaib has been able to make Al Meezan into one of the leading AMCs. It is a testament to the work ethic and dedication of Shoaib that the AMC has assets under management of more than Rs 550 billion that it is managing currently. The company has an investor base of more than 300,000 investors which range from institutions to individuals.

In terms of the mutual fund industry, the fund is only second to Al Habib Asset Management which is leading the industry. The feat becomes even more exceptional when it is considered that Islamic banking and finance has only recently emerged as an alternative to conventional banking. In terms of Islamic finance, the fund is the market leader and trend setter with around a fifth of the market share when conventional AMCs are considered as well.

The resignation

In March of 2024, it was announced by Al Meezan that its CEO was leaving the company after 29 years of service at the company. The move was considered to be just a change at the top with Shoaib contemplating retirement and wanted to step back from his role. There were reports circulating around the time that a letter was sent by the SECP to the board of Al Meezan. As the letter was taken into consideration by the board, it was alleged that personal trades were being carried out by the CEO and his family which were against the regulations of the SECP. An allegation of front running was being made which would benefit the CEO at the cost of its investors and the capital markets.

While rumors around this letter were floating around, the resignation was given by Mohammad Shoaib. When SECP was approached to get access to any such information, it was stated that “(w)hile we cannot disclose specific details or documents pertaining to any individual or entity due to confidentiality, we

can confirm that no formal investigation has been carried out by the SECP against Mr. Mohammad Shoaib in connection with the matter referenced.”

In order to be appointed CEO of an AMC, SECP needs to provide an approval to make sure that the person is fit and proper to run the company and manage the funds of others. The CEO is not just running the affairs of the company which has appointed it but also has to make sure that the interests of the investors are kept in mind. Funds use the life savings of small investors and it has to be made sure that the person looking after these funds is fit enough to do so. As the powers of the CEO are huge, the SECP needs to consider the background in order to approve the appointment. In case of Shoaib, the SECP has stated that “(a)s part of the SECP’s regulatory framework, appointment of a Chief Executive Officer is subject to a rigorous fit-and-proper test which was also applicable on Mr. Mohammad Shoaib’s appointment as CEO of Interloop Asset Management Company (now Lucky Investments Limited).”

A new beginning

After a 29 year career working with Al Meezan, it is clear Shoaib is not quite done with the asset management business. Lucky Investments has recently acquired an AMC license from Interloop Asset Management which will allow it to manage and operate the fund under its own banner. The fund will be Shariah Compliant and Shoaib has been appointed to run it. The fact that such a huge name has been brought in shows that Lucky is committed to making this new venture work and they are prepared to bring in the big guns in order to do so.

As Lucky Investments embarks on its journey, it would be expected that the company is able to follow the footsteps of Al Meezan and create a fund which matches the size and magnitude of Shoaib’s earlier creation. The focus of the new fund is to take over the crown of Al Meezan as the market leader in the Shariah complaint industry. Lucky has a long way to go and has big shoes to fill but it seems like they have chosen the best man for the job to do so. As the company builds its team and fund managers, the goal would be to find avenues of investment which yield a higher return. This could be challenging considering how government securities are going through a negative yield curve and interest rates are falling. With assets seeing lower returns, the objective would be to outpace the benchmark which was easier when interest yielding assets were making higher returns. With stiff competition from Al Meezan and changing economic times, it feels like Shoaib will have his work cut out for him. n

From direct to indirect:

SBP’s rewiring of Pakistan’s financial architecture

A deep dive into how Pakistan’s central bank responded to lending restrictions by creating an elaborate system of regulatory accommodations and creative compliance. The result? A financial sector more intertwined with government debt than ever before

The passage of the State Bank of Pakistan (SBP) Amendment Bill through the Senate on January 28, 2022, was no smooth affair. With a razor-thin majority of just one vote (43 in favor, 42 against), and amid opposition protests decrying “financial imperialism,” the bill promised to end direct government borrowing from the SBP. The financial press celebrated this IMF-mandated reform as a triumph of central bank independence. But the SBP had other plans in mind, quickly setting up an alternative system that would prove even more effective at channeling money to government securities. What unfolded after independence was akin to a carefully orchestrated card game. As the house, the State Bank first changed the rules of play, then invited more players to the table, and finally showed remarkable flexibility about how strictly those rules would be enforced.

Our story follows this transformation: First, we will see how SBP redesigned the basic mechanics of money flow through creative

use of open market operations (OMOs). Then, we will watch as they expanded the player pool beyond traditional banks. Next, we will examine how the players exploited these changes, pushing leverage to unprecedented levels while the referee conveniently looked the other way. Finally, we will see how even other regulators joined in dealing cards from the same deck.

Dealing the first hand: OMOs reimagined

In the very same month it gained independence and was barred from lending to the government, the State Bank conducted an unprecedented 63-day OMO - the longest tenure ever seen in Pakistan’s financial markets. When Profit questioned this unusual duration (now 70 or 77-day operations raise no eyebrows), then-governor Reza Baqir’s candid response exposed the strategy: “The SBP cannot lend to the government, but we can step in and inject liquidity when needed.” The message was clear – direct lending might be prohibited, but SBP had found its workaround. Less than six months after independence,

SBP made its next strategic move. Through DMMD Circular No. 11, the central bank brought Development Finance Institutions (DFIs) into the fold, adding new participants to the market.

The central bank had engineered a powerful new mechanism for government financing. These two swift changes after independence – repurposing OMOs and adding DFIs to the mix – created an irresistible opportunity for financial institutions. The formula was simple but potent: buy government securities, use them as collateral to borrow more money, use that borrowed money to buy even more government securities, and repeat. Through this mechanism, institutions could multiply their balance sheets several times over while dealing primarily in “risk-free” government paper.

The players quickly learned to maximize their returns in this new game. PKIC emerged as the most aggressive player, while U Microfinance Bank showed early enthusiasm before exiting. On the commercial banking side, four major players – United Bank Ltd (UBL), the National Bank of Pakistan (NBP), Askari Bank, and Bank Alfalah – dominated the field, collectively handling over 80% of the State Bank’s

reverse repo operations. While commercial banks dealt directly with the SBP, DFIs played through intermediaries, despite having direct access.

Raising the stakes: the scale of expansion

The results were staggering in their magnitude. PKIC’s balance sheet exploded from Rs135 billion at the end of 2022 to Rs1,100 billion by the end of the third quarter of 2024 — an almost tenfold increase in less than two years. Commercial banks matched this aggressive pace, with the State Bank’s monetary policy assets –banking (the reverse repos) skyrocketing from Rs2 trillion to Rs8.8 trillion between January 2022 and June 2024. By December 2024, the figure stood at Rs8 trillion, with the two largest banks dominating the game.

The real story lies in the leverage ratios. One bank’s leverage ratio plummeted from 4.39% at the end of 2022 to 2.46% by the end of 2023 — an alarming drop for a D-SIB (Domestic-Systemically Important Bank) status institution. PKIC’s case was even more dramatic: their balance sheet expansion sent their leverage ratio crashing from 12.7% to 2.51% in one year, then further down to 1.37% by June 2023.

The leverage ratio represents how much equity the bank has to withstand losses in its loan book. PKIC has a loan book 40 times as large as its equity, meaning a 2.5% loss in its loan book would bankrupt the institution.

The House always wins: regulatory accommodation

The SBP’s response to these developments revealed a pattern of extraordinary accommodation that raises serious questions about its supervisory priorities. Take the case of a D-SIB whose leverage ratio fell from 4.39% at end-2022 to 2.46% by end-2023. Instead of requiring a quick correction – which was entirely possible given the decline was purely due to OMO exposure that could be unwound within weeks – the State Bank granted a full year’s extension to bring the bank back to compliant levels of leverage.

More telling, it allowed leverage ratios to drop to 2% when 3% was the requirement. The bank’s response? It pushed the ratio even lower to 2.11% in the subsequent quarter while becoming the State Bank’s largest borrower, accounting for 50% of all reverse repos.

PKIC’s case proves even more revealing. When their leverage ratio crashed to 1.37%,

SBP permitted operation at 1% - a buffer so generous it essentially gave them free rein. The improvement to 2.44% by June 2024 came not from reducing exposure but from realized gains on their associate company investments. Once again, SBP allowed a 2% minimum until December 2024.

The transformation became so apparent that the IMF could not ignore it. In their September 2024 $7 billion Standby Arrangement, they explicitly warned about DFIs straying from their development mandate into government securities investments. More critically, they flagged the strengthening sovereign-bank nexus — the very thing the SBP’s policies were intensifying.

A new dealer joins: the FBR intervention

In what appeared to be an unprecedented encroachment into central bank territory, the Federal Board of Revenue (FBR) introduced a tax on banks based on their levels of advances (loans) to deposits. Banks that had too much exposure to government lending would be required to pay an additional tax of 10-15% of operating income depending on how much government lending each bank had.

Essentially, the FBR noticed the gravy train and decided it wanted a piece of the action.

What is striking is not just the intervention, but the State Bank’s response – or lack thereof. When it became clear that the SBP would not defend its regulatory turf, banks got the message. In October 2024 alone, they rushed to lend approximately Rs900 billion to commercial borrowers, with estimates suggesting around 80% was secured against government securities. An additional Rs40 billion flowed into personal loans, again primarily against government paper.

The central bank’s silence spoke volumes – as long as the new scheme maintained demand for government securities, the SBP was content to let another regulator deal the cards.

The wake-up call that wasn’t

The SBP finally appeared to acknowledge these risks in its December 2024 circular, introducing haircuts on securities used as collateral and requiring institutions to meet prescribed solvency ratios. But even this apparent move toward stricter oversight revealed SBP’s true priorities – instead of immediate implementation, or even a start-of-year timeline, these crucial safeguards would only take effect from July 2, 2025. A full six months of continued operation under the existing framework, suggesting a central bank more concerned with maintaining

the status quo than addressing systemic risks. Banking sources suggest SBP orchestrated this elaborate system to ensure participation in their operations and keep government borrowing costs low. By enabling this financial engineering, SBP effectively turned the entire financial sector into what they themselves were no longer allowed to be: the government’s primary source of funding.

The Final Tally

The transformation since the “independence” mandate is remarkable in its scope and calculation. SBP has masterfully:

1. Engineered a backdoor financing system through OMOs that dwarfs its previous direct lending – from Rs2 trillion to Rs8 trillion in just two years

2. Created a self-reinforcing cycle where financial institutions multiply their balance sheets by repeatedly using the same government securities as collateral

3. Provided extraordinary regulatory cover by:

- Allowing institutions to operate well below required leverage ratios

- Granting year-long compliance periods for issues that could be fixed in weeks

- Setting new regulatory floors that legitimized high-risk positions

4. Enabled DFIs to abandon their development mandate, with some institutions expanding their balance sheets tenfold primarily through government securities

5. Remained strategically silent when FBR’s intervention created yet another channel for government paper, resulting in PKR 900 billion of lending in a single month

6. Even when finally acknowledging risks through the December 2024 circular, chose a deliberately delayed implementation that allows these practices to continue well into 2025

7. Perhaps most critically, strengthened the sovereign-bank nexus that the IMF explicitly warned against, creating a financial sector more dependent on government debt than ever before

The Bottom line

The irony is unmistakable. In trying to prove they’re not the government’s ATM anymore, SBP has engineered a transformation of our entire financial sector into one. What we’re witnessing isn’t just creative financial engineering—it’s the systematic rewiring of Pakistan’s financial architecture, with commercial banks morphing into pseudo-hedge funds and DFIs abandoning their development mandates. And at the center of it all, a supposedly independent central bank that seems more focused on finding innovative ways to keep the government’s borrowing costs low than maintaining financial stability. n

OPINION

Syed Shabbir Uddin

What surprises lay in wait for Pakistan’s Auto Market in 2025?

As 2024 draws to a close, it is worth looking back at where we thought Pakistan’s auto market would stand by now. In early January, the outlook was shaped by easing interest rates, rising pent-up demand, and the quiet but steady emergence of new young customers into the car buying age. With the facts now in hand, it’s clear these themes played out in ways that speak to the market’s resilience to rebound — and hint at what 2025 might bring.

At the start of the year, our forecast suggested policy rates would ease up to 15% from their record high of 22% fueling both consumer and industrial confidence. However, that benchmark was crossed on 16th of December when the policy rate was dropped to 13% creating a positive wave. About three months after the first cut, just as expected, demand perked up as per PAMA reports. September car sales jumped to 10,297, a 18% month-on-month increase, while October jumped another 27% over September. Although November dipped as the year ended, this timing matched earlier predictions, showing how interest rates remain a critical lever in guiding market sentiment.

Demand that defied the odds

Historically, the first half of any given year accounts for over 55% of total annual vehicle sales. In 2024’s first six months, the market averaged around 10,000 units per month. If that

The author has two decades of experience in the automotive industry. He can be contacted on the platform X, @Shabbir_uddin, or on LinkedIn: www.linkedin.com/ in/shabbiruddin

baseline had persisted, the second half should have hovered around 8,400 units monthly. Instead, it hit nearly 10,200—a full 21% above “business-as-usual” projections. By year-end, total sales are expected to reach about 140,000 units, a 34% gain over last year’s 105,000. This surge underlines that the industry’s rebound wasn’t a fluke; it’s rooted in underlying strengths, consumer confidence, and improved financing conditions.

Looking ahead, 2025 may have even more surprises in store. Without adding anything new, the general demand pattern could push volumes to about 168,000 units. But there’s plenty of fresh products on the horizon. Suzuki’s Every has replaced the aging Bolan, potentially pushing the monthly volume of Suzuki vans from 500 to 800 units. A Chinese brand BYD has planned CBU imports of EVs in the first quarter that will broaden choices, while Hyundai’s Elantra Hybrid—despite its premium pricing—still managed to draw 150 units in its opening month.

Meanwhile, the upcoming Kia Sportage with Hybrid technology would push the volumes the most. Sportage pioneered the crossover SUV in Pakistan since its launch in 2019 and managed selling over 45,000 CKD units in five years. Spy shots of the new model test mule have been circulating across social media, sparking conversations in living rooms and online forums. Its anticipated launch in 2025 could be the spark that pushes demand skyward once again. If these new models weren’t enough, news reports suggest the government may raise the auto financing limit from Rs 30 lakh to Rs 60 lakh. Such a move would unleash a wave of pent-up demand. Combining new models with easier credit access could push 2025’s total beyond 180,000 units or possibly over the 200,000 mark if the agricultural rural economy produces good yield and receives good rates—a milestone many didn’t expect until 2026.

The end beneficiary

It is not just about automakers profitability. Each sale fuels a broader ecosystem: the component makers, service centers, logistics providers, and, most importantly, the skilled workers and their families, whose livelihoods rest on a stable market. Observing how closely this year’s outcomes tracked earlier expectations offers a clearer understanding of the forces at play—and suggests that careful attention to data, policy, and consumer sentiment can shed light on what’s next.

The real message here is crystal clear: 2024 proved that well-timed rate cuts, smart product launches, and evolving consumer preferences can ignite extraordinary results. The overall economic activity, potential financing reforms, and a pipeline of volume selling fresh models like Suzuki Every and Kia Sportage promise more than incremental growth— they herald a genuine leap to industry recovery. Stay tuned, because 2025 is gearing up to break records with new models and financing reforms.

Adamjee Insurance faces half-billion-rupee loss from Dubai floods

The company’s Pakistan operations remained profitable, but losses from its UAE auto business severely dampened overall net income

Profit Report

In a surprising turn of events, Adamjee Insurance Company Limited (AICL), one of Pakistan's largest and most established insurance providers, has reported a significant loss of approximately 500 million rupees due to claims resulting from the catastrophic flooding in Dubai in April 2024. This revelation came during an analyst briefing held by the company to discuss its business performance and future outlook.

The floods, which wreaked havoc across the United Arab Emirates (UAE) and particularly in Dubai, have had far-reaching consequences, not only for the affected regions but also for international businesses operating in the area. Adamjee Insurance, with its substantial presence in the UAE market, found itself exposed to considerable financial risk as a result of this extreme weather event.

The April 2024 floods in Dubai were part of a larger pattern of increasingly severe weather events affecting the Arabian Gulf region. Dubai had already experienced what was then described as the heaviest rainfall in 75 years. Some areas recording more than 250mm of rain in less than 24 hours, far exceeding the country's average annual rainfall of 140-200mm.

Climate scientists have pointed to human-induced climate change as a significant factor in the intensity of these storms. A study by the World Weather Attribution group concluded that the heat pumped into the atmosphere by human activities made the record rainfall 10-40% heavier. This finding underscores the growing risks that climate change poses to businesses and communities worldwide, particularly in regions traditionally considered arid.

The floods caused widespread disruption, with Dubai International Airport – the second busiest in the world – forced to cancel hundreds of flights. Roads were submerged, buildings inundated, and tragically, lives were lost across the affected areas.

Founded on September 28, 1960, Adamjee Insurance Company Limited has long been a cornerstone of Pakistan's insurance industry. Listed on the Pakistan Stock Exchange, AICL has built its reputation on financial strength, and a diversified business portfolio.

The company's expansion into the UAE market was a strategic move to tap into the growth potential of the region and diversify its risk portfolio. However, this decision has now exposed AICL to the increasing climate-related risks facing the Gulf region.

In the analyst briefing, AICL's man-

agement revealed that while the company's Pakistan segment had achieved an underwriting profit of approximately Rs700 million in the first nine months of 2024, the overall profit was significantly reduced due to losses from the UAE segment. The impact of the UAE rain-related losses, amounting to around Rs500 million, has highlighted the vulnerability of AICL's heavily motor-focused UAE portfolio to extreme weather events.

Adamjee Insurance's UAE operations, which account for nearly 30% of its non-life premium income, have been a significant driver of the company's growth in recent years. However, the concentration of this business in the motor insurance segment – comprising 85-90% of AICL's UAE portfolio – has left the company particularly exposed to the type of widespread flooding experienced in Dubai.

The management acknowledged that the UAE segment has suffered losses in both 2023 and the first nine months of 2024, primarily due to three rain-related flooding events that have increased claims from the motor insurance segment. This series of events has not only impacted the company's bottom line but has also raised questions about the sustainability of its current business model in the face of increasing climate-related risks.

In response to these challenges, AICL's

management has outlined plans to diversify its UAE business beyond the motor segment. The company aims to expand into other areas such as health and marine insurance, although growth will still be driven by the motor segment, particularly as interest rates decline in the UAE.

The management expressed optimism about the future profitability of the UAE segment, barring any similar unexpected events in 2025. However, they also cautioned that reinsurance costs are likely to increase in light of these floods, which will have an impact on margins.

The losses faced by Adamjee Insurance are part of a larger industry-wide impact. Reinsurance broker Gallagher Re has estimated that the property market insured loss from the April 2024 flooding in the UAE alone could be between $1.8 billion and $2.3 billion, with additional motor insurance losses ranging from $350 million to $650 million.

These figures underscore the magnitude of the challenge facing the insurance industry as climate change increases the frequency and severity of extreme weather events. For companies like Adamjee Insurance, with significant exposure to regions at high risk of climate-related disasters, the need for robust risk management strategies and potentially, a reevaluation of their geographical focus, has never been more pressing.

Despite the setbacks in its UAE operations, Adamjee Insurance remains a formidable player in the Pakistani insurance market. The company's business mix in terms of gross written premiums (GPW) as of 2023 stood at 44% fire, 35% motor, 12% health, 6% marine, and 3% miscellaneous. The most profitable segment is miscellaneous, which includes crop loan insurance and bank-related insurance.

AICL's investment strategy has also played a crucial role in its financial performance. The company earned 3.9 billion rupees of investment income in the first nine months of 2024, matching its performance for the entire year of 2023. This income was derived from a mix of 67% equities, 20% term deposits, 8% fixed income securities, and 5% income from subsidiaries.

The company's management has indicated that the equity investment mix, which has remained relatively stable at 67-69% for the last three years, consists of strategic long-term investments that are likely to remain in place going forward.

As Adamjee Insurance navigates the aftermath of the Dubai floods and their impact on its financial performance, the company faces both challenges and opportunities. The increasing frequency and severity of climate-related events in the Gulf region will necessitate a reevaluation of risk models and pricing

strategies, particularly in the motor insurance segment.

However, the company's strong position in the Pakistani market, coupled with its diversified investment portfolio, provides a solid foundation from which to address these challenges. The management's plans to diversify the UAE business and potentially expand into new segments could help mitigate future risks.

Moreover, the expected growth in all general insurance segments due to declining interest rates in Pakistan presents opportunities for AICL to strengthen its domestic operations. The company is well-positioned to capitalize on potential growth in the motor segment, particularly if the State Bank of Pakistan increases the current Rs3 million-per-car auto financing limit.

The significant losses faced by Adamjee Insurance due to the Dubai floods serve as a stark reminder of the far-reaching impacts of climate change on the insurance industry. As

extreme weather events become more frequent and severe, insurance companies will need to adapt their strategies, diversify their portfolios, and potentially reassess their geographical focus.

For Adamjee Insurance, the path forward will likely involve a delicate balance between maintaining its strong position in the Pakistani market, diversifying its UAE operations, and implementing more robust risk management strategies to account for climate-related events.

As one of Pakistan's oldest and largest insurance providers, AICL's response to these challenges will be closely watched by industry observers and could set a precedent for how other insurance companies in the region adapt to the realities of climate change. The company's ability to navigate these turbulent waters will not only determine its own future but could also shape the broader insurance landscape in Pakistan and the Gulf region for years to come.

Fertilizer volumes to see strong December rebound, but 2024 sales still lag

Engro Fertilizers is expected to emerge a winner from the year-end sales surge on the back of its price cuts and more aggressive marketing campaigns

Profit Report

In a promising turn of events for Pakistan's agricultural sector, the country's fertilizer industry is poised to end 2024 on a high note, with urea sales expected to surge in December. However, this late-year rally isn't quite enough to offset the overall decline in fertilizer sales for the full year, according to recent reports from two of Pakistan's leading investment banks.

Both Topline Securities and BMA Capital, Karachi-based investment banks, project a significant uptick in urea sales for December 2024. Topline Securities anticipates urea sales to reach 1.002 million tons, marking a substantial 60% year-onyear increase compared to December 2023's 628,000 tons. BMA Capital's forecast is similarly optimistic, projecting December urea sales at 1.000 million tons, representing a 59% year-on-year growth.

This sharp increase is attributed to

seasonal demand during the peak Rabi season, with both reports noting a month-onmonth growth of 53% from November 2024. The surge in December sales is particularly noteworthy when compared to the five-year average for the month, which Topline Securities reports as 857,000 tons.

Despite the strong finish to the year, both investment banks report that the overall urea sales for 2024 are expected to show a slight decline compared to 2023. Topline Securities projects total urea sales for 2024 at 6.587 million tons, down 1% from 6.64 million tons in 2023. BMA Capital's estimate is nearly identical, forecasting 6.585 million tons for 2024, also representing a 1% year-on-year decrease.

This marginal decline in annual sales underscores the challenges faced by the fertilizer industry throughout much of 2024. Topline Securities notes that urea sales in the first 11 months of 2024 were down by 7% year-on-year, totaling 5.58 million tons. The strong December performance, while en-

couraging, was not quite enough to completely offset the slower sales earlier in the year.

While urea dominates the fertilizer market in Pakistan, DAP sales also play a significant role. Both reports indicate a modest increase in DAP sales for December 2024 and the full year.

Topline Securities expects DAP sales in December 2024 to reach 151,000 tons, up 9% year-on-year but down 40% month-on-month. For the full year 2024, they project DAP sales of 1.641 million tons, a 4% increase from 2023.

BMA Capital's figures are slightly more conservative but follow the same trend. They anticipate December 2024 DAP sales of 149,000 tons, an 8% year-on-year increase, and full-year 2024 sales of 1.639 million tons, also up 4% from 2023.

Engro vs Fauji

The reports provide detailed insights into the performance of Pakistan's major fertilizer manufacturers, with Engro Fertilizers (EFERT) emerging as the clear frontrunner in the December sales surge.

Both Topline Securities and BMA Capital highlight EFERT's exceptional performance in December 2024. Topline Securities expects EFERT to record a 100% year-on-year increase in urea sales, reaching 422,000 tons for the month[ BMA Capital's projection is even more optimistic, forecasting 423,000 tons, representing a 101% year-on-year growth.

This remarkable growth is attributed, in part, to EFERT's strategic pricing decisions. Topline Securities reports that EFERT announced an incentive of Rs100 per bag for dealers in December 2024, continuing a strategy mentioned in their last analyst briefing. BMA Capital notes that EFERT offered a discount of Rs30 per bag to recoup market share.

Despite the strong December performance, both reports indicate that EFERT's full-year 2024 urea sales are expected to decline by 9% compared to 2023[1][2]. This suggests that the company's aggressive yearend strategy was aimed at recovering ground lost earlier in the year.

Fauji Fertilizer Company (FFC), traditionally EFERT's main rival, is also expected to see significant growth in December, albeit not as dramatic as EFERT's. Topline Securities projects FFC's December urea sales at 309,000 tons, up 35% year-on-year, while BMA Capital forecasts 307,000 tons, a 34% increase.

For the full year 2024, both reports anticipate FFC to buck the industry trend with a 5% increase in urea sales compared to 2023. This growth, while modest, positions FFC as one of the better performers in the industry for the year.

Other major players

Fauji Fertilizer Bin Qasim (FFBL): Both reports project substantial year-onyear growth for FFBL in December 2024. Topline Securities expects FFBL's urea sales to reach 68,000 tons (up 175% YoY), while BMA Capital forecasts 69,000 tons (up 180% YoY). For the full year 2024, both reports anticipate a 55% increase in FFBL's urea sales compared to 2023.

Fatima Group: Topline Securities projects Fatima Group's December urea sales at 146,000 tons (up 34% YoY), with BMA Capital forecasting a similar 144,000 tons (up 32% YoY). Both reports expect Fatima Group to see a modest 4-5% increase in full-year 2024 urea sales.

Competitive landscape

The December 2024 sales surge has reshaped the competitive landscape of Pakistan's fertilizer industry, particularly in the urea segment. EFERT's aggressive pricing strategy and resulting sales growth have significantly altered market shares for the month.

According to BMA Capital's data, the December 2024 urea market share breakdown is as follows:

- EFERT: 42.3%

- FFC: 30.7%

- Fatima Group: 14.4%

- FFBL: 6.9%

- Others: 5.7%

This represents a substantial shift from historical norms, with EFERT gaining significant ground against its traditional rival, FFC. The rivalry between these two industry giants has long been a defining feature of Pakistan's fertilizer market, and EFERT's December performance suggests a potential reshaping of this dynamic.

However, it is important to note that this dramatic shift in December may not be indicative of the full-year picture. Both companies have seen different trajectories over the course of 2024, with FFC managing to grow its annual sales while EFERT faced a decline despite its strong finish. The surge in December sales has had a significant impact on urea inventory levels. Topline Securities estimates that the closing inventory of urea will be around 373,000 tons in December 2024, down from 756,000 tons in November 2024. BMA Capital provides a similar estimate of 375,000 tons for December 2024.

This sharp reduction in inventory levels could have implications for pricing and availability in the early months of 2025. While the current inventory levels are still higher than the 104,400 tons reported in December 2023, the rapid drawdown could lead to tighter supply conditions if demand remains strong.

Topline Securities provides a break-

down of company-wise inventory levels, with Fatima Group holding the highest at 162,000 tons, followed by EFERT at 117,000 tons, and the combined inventory of FFC and FFBL at 39,000 tons. This disparity in inventory levels could influence competitive dynamics in the coming months.

DAP market dynamics

While urea dominates the headlines, the DAP market also shows interesting trends.

FFBL emerges as the clear market leader in DAP sales for December 2024, with both reports projecting sales of around 70,000-71,000 tons. This represents nearly half of the total expected DAP sales for the month.

FFC and EFERT play smaller roles in the DAP market, with December 2024 sales projections ranging from 18,000-20,000 tons for FFC and 12,000-13,000 tons for EFERT.

The DAP inventory situation differs from urea, with closing inventory expected to increase year-on-year. BMA Capital projects DAP closing inventory at 85,000 tons in December 2024, up from 24,700 tons in December 2023. The strong finish to 2024 sets an interesting stage for Pakistan's fertilizer industry in 2025. Several key factors will likely influence the market:

1. Pricing strategies: EFERT's success with its discount strategy in December 2024 may prompt other companies to reconsider their pricing approaches. However, Topline Securities notes that EFERT has pulled back its Rs100 per bag discount effective January 2025, suggesting that the company views the strategy as a short-term measure.

2. Inventory management: The significant reduction in urea inventory levels could lead to supply pressures in early 2025 if demand remains strong. Companies with larger inventory positions, like Fatima Group, may be better positioned to capitalize on any supply constraints.

3. Market share battles: EFERT's aggressive move to reclaim market share in December 2024 may spark intensified competition in 2025. FFC, as the traditional market leader, will likely respond to protect its position.

4. Agricultural Outlook: The fertilizer industry's performance is closely tied to agricultural conditions. Factors such as weather patterns, crop prices, and government agricultural policies will play crucial roles in shaping fertilizer demand in 2025.

While the December 2024 surge in fertilizer sales, particularly urea, provides a positive note for the industry, it also sets the stage for an intriguing and potentially volatile market in 2025. The shifting dynamics between major players like EFERT and FFC, coupled with broader economic and agricultural factors, will require close monitoring as the industry moves into the new year. n

A catastrophe looms on our doorsteps

Pakistan’s mountains, rivers, and ports face unique challenges posed by climate change. All of them are far more interconnected than one might think.

Profit report

There is no hiding from climate change, especially not in a country like Pakistan. This is not exactly news. The effects have been apparent to anyone with eyes to see. But the past couple of years have shown the extent of the devastation climate change has brought to this country.

Since 2022, the ravages of climate change have been swift and fast in Pakistan. Take the example of Sanghar.

In May 2022, reports began to emerge that the cotton crop in Sindh was wilting. In Sanghar, one of the largest cotton producing districts in Sindh with cotton grown on 300,000 acres of agricultural land, less than 200,000 acres were being used to cultivate cotton. And on the 200,000 acres that were being used to grow cotton, crop performance was abysmal.

Over the past 10 years, according to figures available with the Pakistan Cotton and Ginners Association, Pakistan’s cotton yields have fallen by 26% from 880 kg per hectare to 652 kg per hectare over the last decade. While the cotton crop in Sanghar suffered, other agricultural areas dependent on the down-river water from the Indus were affected as well. In Thatha, fishing villages were left without any source of livelihood as the nearly three kilometre stretch of river that crossed the region dried up completely and was replaced by huge deposits of sand. At the Kotri Barrage of the Indus in Sindh, water levels had fallen from 15,000 cusecs of water to barely over 2000 cusecs.

The numbers coming in from the Indus River that year were alarming. They revealed a major dip in the Indus of 10,000 cusecs (an outflow of 105,000 cusecs on May 19 and 95,000 on May 20) occurred at Tarbela dam, raising fears that the dam may have hit dead levels. Its inflows plunged to 77,900 cusecs from 98,000 cusecs within a week. All of this was in May, the beginning of the summer season when the river needs to be flowing to maintain the vast swathes of agricultural lands all along Punjab and Sindh. The economies of both provinces rely heavily on this river.

And then came the floods.

Early in August, Sindh and Balochistan received monsoon rains the likes of which they had never seen before. The two provinces saw the highest amount of water fall from the skies in living memory, recording 522 and 469 percent more than the average downpour. The

abnormally high rainfall caused hill torrents in Balochistan, which are a distinct type of waterway in which water drains from the mountains and hits localities and infrastructure in its path at an enormous speed. More than 200 of these hill torrents came hurtling towards the South of Punjab and Sindh, causing mass devastation in their wake.