17 22 12

17 22 12

08 The Punjab Govt just got something right. What could it mean for livestock farmers?

12 The bifurcation of payments

17 Jute, once Pakistan’s most important crop now an embarrassing anecdote, might be caught up in a PSX pump-and-dump

22 Say hello to Pakistan’s first digital bank

25 Rising above the noise: Highnoon’s stellar performance and steady ascent

27 How Butterfly stayed in business and beat back P&G’s Always

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The Punjab Govt just got something right. What could it mean for livestock farmers?

The CM Punjab Livestock Card gives farmers financing to expand and improve their herds. If done right, it could be a model for how provincial governments should bolster agriculture

By Abdullah Niazi

This is the story of two subsidies. The first is from two years ago, announced in a panic and in response to the most colossal agricultural crisis this country has seen in decades. The latter, only announced a few months ago and still underway, is tailored to a more specific purpose.

Both were introduced by governments of the same political party, the PML-N, although one was a federal subsidy package and the other was from the provincial government in Punjab.

The first was the Kissan Package introduced in November 2022 in response to the destruction from the devastating floods that year. The second package came around two years after in November 2024, aimed at providing cheap loans and financing for livestock farming.

The two subsidies were introduced in very different circumstances. They also represent two very different attitudes towards government aid for agriculture. The Punjab CM’s Livestock Card is essentially the allocation of a Rs 20 billion fund meant to provide interest free loans to livestock farmers. The scheme ticks a lot of boxes. The government has initiated the scheme in partnership with the Bank of Punjab, which will help with the disbursements, management, and loan collections. It is not a handout, so even though there will be losses, it is an attempt by the government to invest in farmers rather than make a splash and try to get some publicity out of it. Perhaps most importantly, it is sending financing into a sector that has largely been ignored by the government and private sector corporate banks. So how does it work?

Let us get this straight. It takes a lot for this publication to give a nod of approval to anything the government does. Our natural position on anything coming from government quarters is suspicion. So when some new program or scheme comes out, the assumption is it will become a victim either to incompetence (at best) or malice and corruption (at worst).

Just look at the last major agriculture subsidy scheme Pakistan saw. In 2022, Prime Minister Shehbaz Sharif, then in his first tenure, announced a Rs1,800 billion subsidy package for farmers affected by this year’s catastrophic flooding. It was a splashy announcement that promised among other things loans, sufficient availability of fertilisers, cheap financing for tractors, and a reduction in electricity tariff to a fixed rate.

It was a pressing matter to introduce some relief to the farming community. In an economy majorly reliant on agriculture, climate change and its effects have been a major blow to rural economies. With international agencies estimating losses over the $40 billion mark, there was a dire need for agricultural reforms

Under the package, the government will give Rs10.6 billion loans to small farmers across the country while small farmers of flood-hit areas would get loans worth Rs 80 billion. In addition to the interest-free and subsidised loans, subsidies will also be given on farm imports such as fertilisers, electricity, seeds, and even tractors.

Given the circumstances, it was a fair enough deal. If it had been implemented strategically, the Kissan Package could have had a wide-reaching impact in helping farmers affected by the floods. But this was very much a stop-gap solution. The scale of the problems faced by our agricultural sector cannot be fixed by solutions of this nature, even if they are well-intentioned.

At most, any subsidy will provide temporary relief. For too long the state has allowed the country’s agriculture to suffer and have offered only stop-gap solutions such as subsidy packaged. We have been papering over the cracks for so long that our entire agrarian economy has grown dependent on subsidy packages.

So what is the reason? How did Pakistan, a country with vast swathes of rich agricultural land, find itself in a position where its agricultural sector has been

on the decline for decades? There are two facets to the problem, The first is that for decades Pakistan has been falling behind on agricultural competitiveness. While the rest of the world has developed through research, mechanization, and technological advancements we have lagged behind. On top of that now our farmers are facing the harsh and unpredictable realities of climate change.

One of the things we need most in such an environment is agricultural financing, which is a subject that has been ignored by Pakistan’s commercial banks for a very long time, and only recently has started getting some attention. With climate change pressing and a lack of financing, Pakistan’s agriculture has fallen behind.

You don’t have to look too far back to find how underserved the agricultural sector is by Pakistan’s banks. In 2022 for example, according to a PWC study, allocation of loans to priority segments, namely Small and Medium Enterprises (SME) and Agriculture, was relatively low. In total, these kinds of loans accounted for less than 8% of the total loans. Specifically, SME loans constitute 4.2% of the portfolio, while Agriculture loans accounted for 3.6%. This means that despite making up 23% of the annual output, financing extended to agriculture makes up less than three percent of the total asset base of banks in the country. It is ridiculous when you think about it. Agriculture provides a living to nearly two-thirds of the population, contributing to approximately three-fourths of the country’s export earnings. It accounts for 23% of the GDP and employs 37.4 percent%.

But over time this trend has been changing, and the banking industry seems to be realising the importance of focusing on this massive yet largely unbanked sector of the economy. In 2023, for example, the agriculture sector saw a 27.5% growth in agri loans, after the agriculture lending financial institutions disbursed Rs 1.22 trillion on account of agricultural financing during the first nine months (July-March) of

The scheme will benefit 80,000 livestock farmers, preparing 400,000 animals for the fattening program, which will not only fulfil local meat demands but also support exports

Syed Ashiq Hussain Kirmani, Provincial Minister for Livestock and Agriculture Punjab

Formal credit outreach in rural areas is limited, leading many farmers to rely on informal sources like moneylenders, which often charge high-interest rates. To address this gap, there is a growing need to improve access to finance for farmers through digital solutions

Syed Irfan Ali, executive director of the SBP’s financial inclusion group

this fiscal year.

This is exactly what the government in Punjab is ensuring with its livestock card. The Livestock Card is an interest-free loan program worth Rs 11 billion for livestock farmers. “The scheme will benefit 80,000 livestock farmers, preparing 400,000 animals for the fattening program, which will not only fulfil local meat demands but also support exports,” explains Provincial Minister for Livestock and Agriculture Syed Ashiq Hussain Kirmani.

The Provincial Minister further elaborated that interest-free loans will be provided for four months in equal installments, with each animal eligible for a loan of Rs 27,000. Farmers can access loans ranging from Rs 135,000 to Rs 270,000.

It is a pretty simple partnership. The BoP gets to increase their agriculture portfolio, something the State Bank of Pakistan has been trying to get commercial banks to do, and the government funds the loans to these farmers. The card has been active since the 15th of December, and the response has been good.

Essentially, you have a system in which the government is providing funds for livestock farmers to grow and improve their herds. The goal is to get livestock cards to at least 40,000 farmers, and the loan amounts will likely be enough to cover around 4 lakh cattle, which are the intended kind of livestock for the scheme.

With the Bank of Punjab on board, the process for farmers to get these interest-free loans is pretty easy as well. Applicant’s mobile phone should be SIM active and registered in his/her name, applicant should own at least five to ten (cows/calves), and applicants having more than ten calves will also be eligible for loan. However, they will be given a loan facility only for ten animals. Cattle breeders who wish to take loans text their identity card number Sent to 8070. The applicant must have a clean credit history (no default) verified by the Electronic Credit Information Bureau. Applicant’s identity and character will also be verified by NADRA and NACTA agencies.

To avail it, all a farmer has to do is apply online on the Punjab Information Technology

Board application. The total tenure of the loan will be maximum 150 days (five months), and using the loan tenure will be 120 days (four months).The next 30 days (one month) will be the period for full repayment of the loan. Cattle keepers will be provided interest free loan through Chief Minister Punjab Livestock Card. The amount of interest or profit will be borne by the Government of Punjab.

Now here’s the rub. The scheme sounds great and has a solid model. The main issue is going to be disbursement. For now, it seems to be going pretty smoothly. At a recent event in Pakpattan, for example, livestock farmers showed interest in loans for rearing and fattening their cattle. Nearly 1600 farmers applied for the scheme, and 578 cards have been received. Clearly there is an interest in this scheme. The question is, can the government and the BoP band together to provide the services they have promised? The government is claiming it will do a lot, including providing tagging, vaccination, and insemination services for these animals. Farmers rearing healthy animals will be linked to major exporters in Punjab.

All of this needs to be taken with a grain of salt. The government regularly over promises and focuses on the wrong things. In this case, all they need to do is make sure the funds are available, there are no technical glitches with farmers signing up for the card, the loans are given by the bank to each farmer for the amount of time they need it for, and that the appetite for pulling this off does not disappear.

Providing financing for sectors such as livestock farming is incredibly important. It has even been a recent mission of the SBP to promote this segment of the banking sector, and there is a great chance for provincial banks in particular to jump on such schemes along with their respective governments.

“Formal credit outreach in rural areas is limited, leading many farmers to rely on informal sources like moneylenders, which often

charge high-interest rates. To address this gap, there is a growing need to improve access to finance for farmers through digital solutions,” said Syed Irfan Ali, executive director of the SBP’s financial inclusion group, in an earlier comment for Profit.

“Digital platforms, mobile banking, and fintech services can simplify loan processes, reduce costs, and ensure timely credit delivery. These innovations can empower farmers with better financial options and support agricultural growth.”

In Pakistan, more than 90% of farmers hold less than 12 acres of land. And above this as well, the stratification of the biggest land owners compared to small landowners is mind boggling. This is especially worse when you consider these smaller landholders need more tailored products since they cannot buy products and machinery is massive quantities. And this is landed farmers who are still regularly in the spotlight. Small scale livestock farmers are rarely talked about.

For these segments, such schemes can be life changing and inject the sector with some vitality. It is not impossible to pull off. For starters, the financial landscape in rural areas has transformed significantly, with the surge in 3G and 4G connectivity and the widespread use of mobile wallets. A large portion of the rural population can now be considered “banked,” though efforts are needed to convert mobile wallets into accessible banking accounts and, eventually, financing tools. A strong case has also emerged to scale agricultural financing in Pakistan by leveraging public datasets and digital infrastructure. The question is whether or not financial institutions can look at agricultural financing as a profitable opportunity rather than just part of a regulatory checklist that the SBP wants them to fulfill.

This means as long as the tech works and farmers can be connected to financing, it will bolster livestock farming in Punjab. More importantly, with the big caveat of the government staying the course, this is the kind of government intervention that is a win-win for all stakeholders involved. n

Electronic payments are gaining market share, but cash is not ceding ground either.

By Farooq Tirmizi

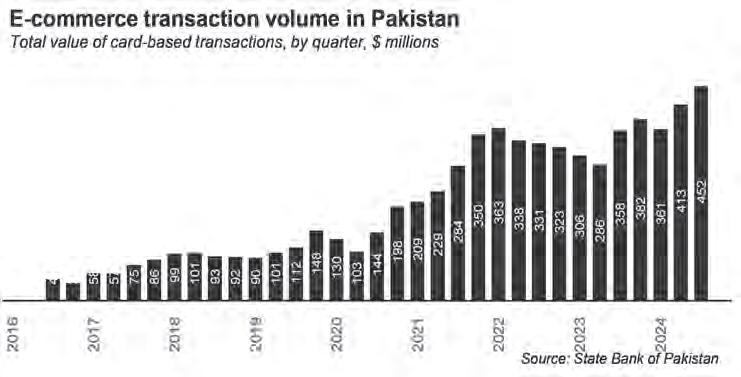

By now, the rise of electronic payments in Pakistan is quite clear and has been covered extensively by many publications, including this magazine. What is less clear is that what should be the implication of the rise of digital payments –that the proportion of payments in Pakistan made in physical cash is going down – has not happened yet, or at least not nearly as much as the rise in digital payments might imply.

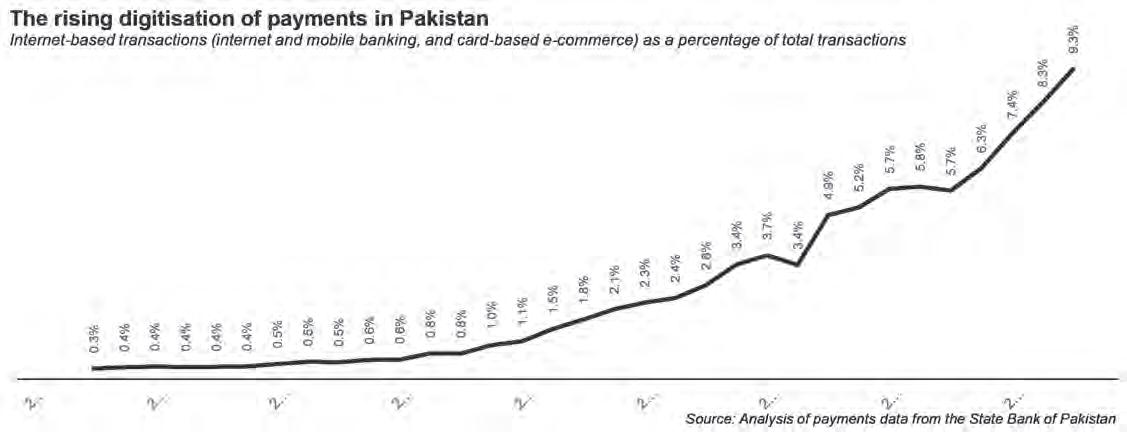

During the third quarter of 2024, digital payments – bank apps, websites, and cardbased e-commerce payments – have increased to approximately 9.3% of the value of all transactions that take place in Pakistan, up from just 0.3% in the same quarter in 2016, which is

a nearly 31x increase in market share for digital payments, according to data from the State Bank of Pakistan.

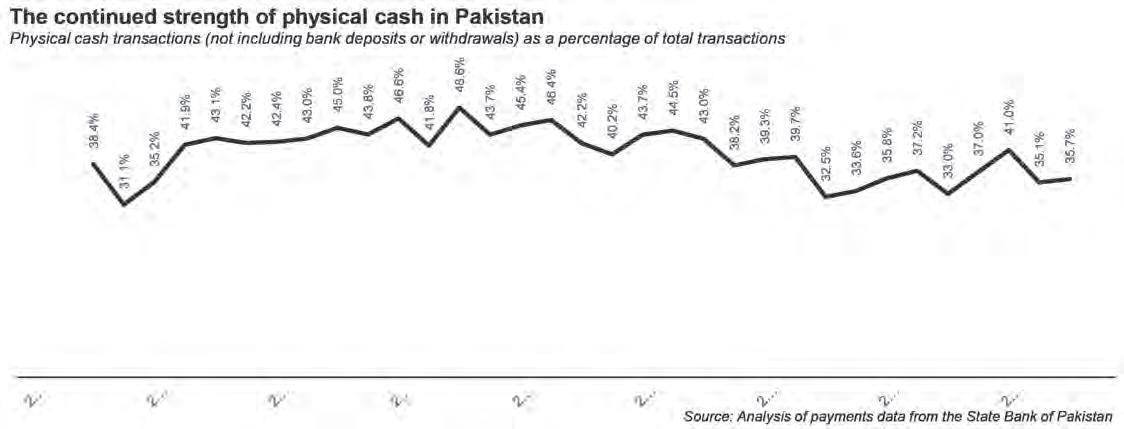

You would think that cash would have fallen by a corresponding percentage, but you would be wrong. According to Profit’s estimates based on data from the State Bank, the proportion of transactions in Pakistan that took place purely in physical cash (which means excluding cash deposits and withdrawals from bank branches and ATMs), were approximately 35.7% of the value of all transactions that took place during the third quarter of 2024. Eight years ago, in 2016, that number was 38.4%, so cash is down slightly from where it was almost a decade ago.

But not by nearly as much as that rise in digital payments number might have led you to think. So what is going on? Reality has a habit

of being complicated and not lending itself to a simple narrative, and the evolution of how people in Pakistan pay for things is one such matter.

There is absolutely no question that digital payments are on the rise, and that those businesses that are gearing up to either facilitate or otherwise take advantage of this rise will stand to benefit. But equally importantly, that rise is mostly coming at the expense of non-cash paper payments (cheques, demand drafts, etc.). Only about 30% of the rise in digital payments is coming from removing the need for physical cash transactions.

In other words, Pakistanis are both adopting new techniques and sticking to the oldest ways of doing business.

In this story, we will examine how the methods of payment are changing, and what is staying the same, and look into some data

points that may provide insights as to why this bifurcation of trends is happening.

But first, a note on the sources of our data, and the methodology used to analyse it.

Abrief note on the data and methodology used in this article. The data comes from the State Bank of Pakistan’s quarterly and annual Payment Systems Review reports from the third quarter of calendar year 2016 through the third quarter of calendar year 2024. The reports extend much further back into the past as well, but the data appears to be compiled using a different methodology in prior years, and we included only data from the years where it seemed most directly comparable. Unless we specify otherwise, all growth rates mentioned in this article refer to the total value of transactions, not volume.

Profit has not just compiled the data, but also combined it with other banking sector data to create as holistic a picture of payments in Pakistan as possible.

While the data for every other payment method is available in that report, what is not available is the volume of cash transactions that do not touch the banking system at either end (i.e. neither the giver nor the receiver of the cash is a banking or financial entity). While the volume of cash transactions is not directly measured by the State Bank of Pakistan, because it issues bank notes, it has a fairly good idea of exactly how much physical cash is in circulation at any given moment in time.

We made a simplifying assumption that the velocity of transactions involving physical cash is approximately the same as that involving the payments system in any given period. We are not certain as to how accurate this

assumption is likely to be, but we also do not have a better number to go on.

Having calculated the total value of transactions involving cash, we then subtract from that the value of cash transactions involving the banks (ATM or branch withdrawals and deposits) to arrive at an estimate of the size of the cash-only transactions economy. This estimate is then plugged into any calculations involving market share of cash vs electronic payments.

One other note: we excluded interbank settlements and government bond transactions in our analysis, since those are transactions that are needed to keep the payments and banking system running. Counting them would likely end up double-counting many transactions and hence result in a skewed picture of what people are actually using to make their payments.

One final bit: we are putting in US dollar equivalents for many numbers in this story to help illustrate the scale of what we are talking

about. Since almost all of the numbers involved represent flows over a period of time, we will adopt the convention of utilising the average exchange rate during that period, defined as the midpoint of the open market buying and selling exchange rates as published by Business Recorder.

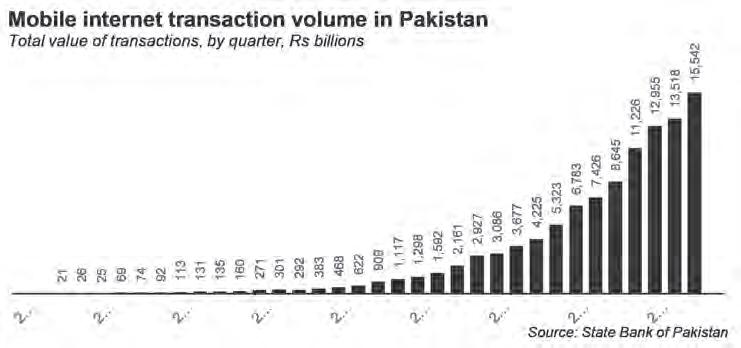

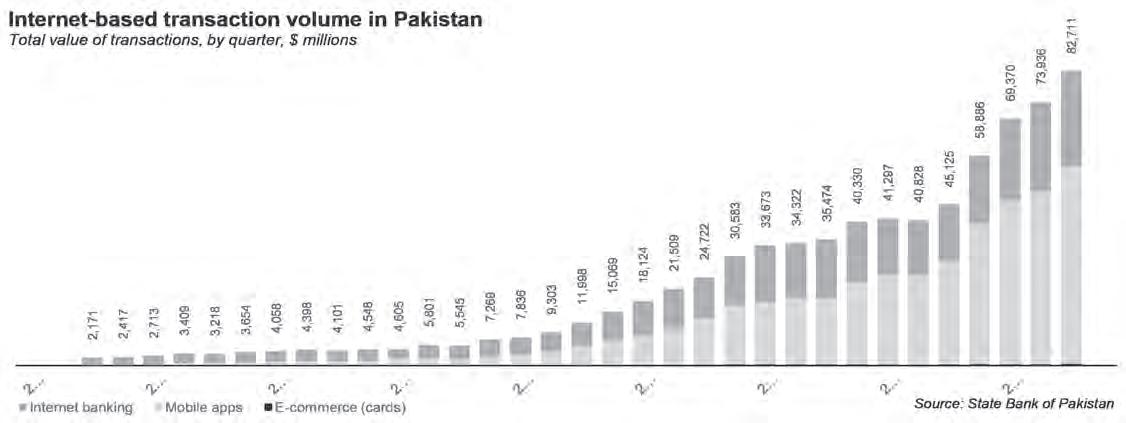

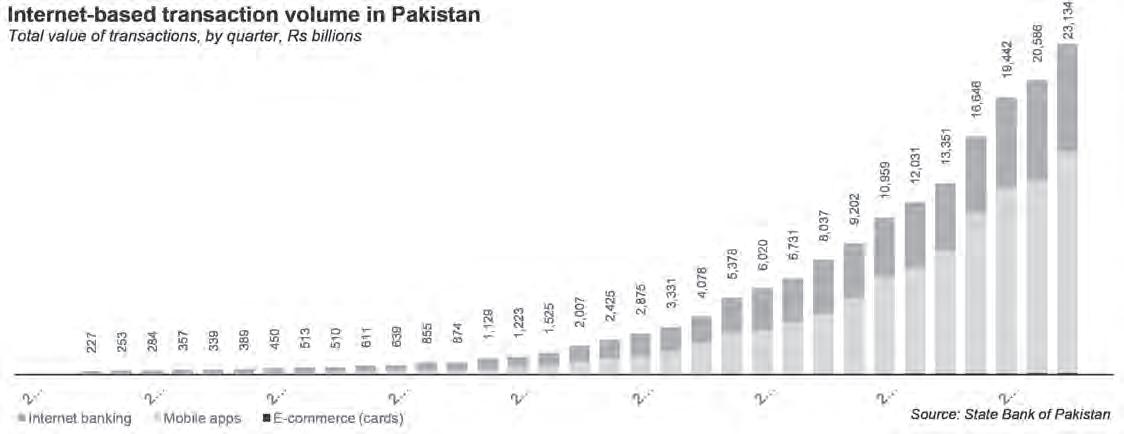

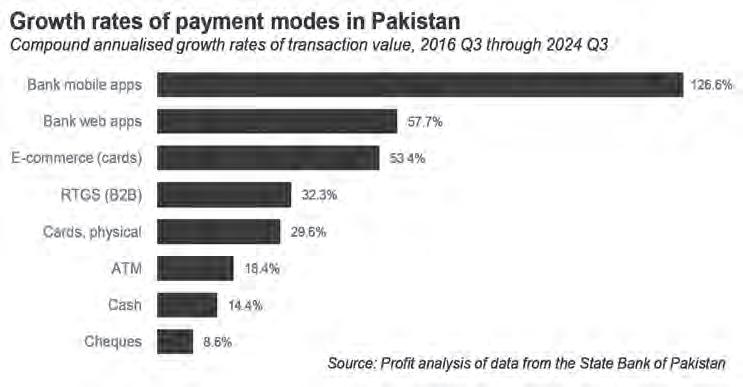

Two-thirds of the value of electronic payments in Pakistan is through the mobile apps of banks. Digital payments in Pakistan happen through bank apps on smartphones more than any other method of payment, meaning effectively that they happen through the Interbank Fund Transfer (IBFT) system and now through the State Bank’s new payment rails, Raast. It is not just that this is the fastest growing segment of the payments ecosystem –

growing at an average annualized rate of 127% per year for the past 8 years – it is that the numbers are now starting to get interesting.

During the 12 months that ended September 30, 2024, the total value of money that moved through the banks’ mobile apps was Rs53 trillion ($190 billion)

Massive amounts of money are moving through the banking system’s mobile apps, and on this front, the State Bank of Pakistan deserves to take a victory lap: at least part of this stunning rise is due to the central bank’s insistence on capping the costs of transactions being made electronically, and now in the case of Raast, transaction costs have been eliminated completely for all person-to-person transactions.

What are people using the bank apps for? Mostly paying other individuals, based on the State Bank’s data. But these supposedly person-to-person payments are likely hiding a considerable amount of commercial activity since most small businesses in Pakistan are sole proprietorships, which means that their

bank accounts are those of individuals, and hence commercial transactions with sole proprietorship businesses look like person-to-person transactions.

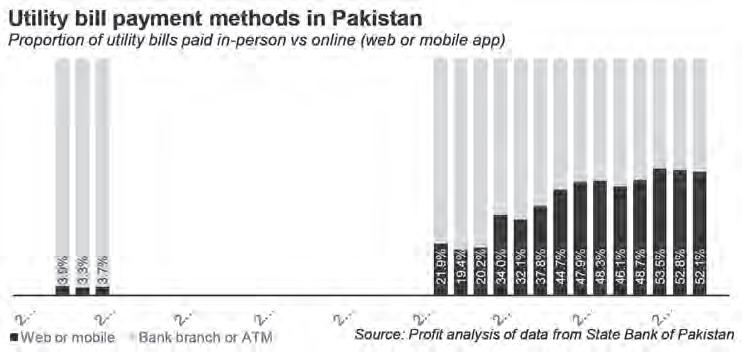

One milestone that has now been crossed by the payments system: the majority of utility bills are now paid online, mostly through bank

websites or mobile apps.

The next most popular digital method of payment is through the banks’ own websites, which accounts for almost the entirety of the remainder of digital payments. It appears that Pakistanis have largely decided that they trust the banks with their money.

So why the distinction between the mobile apps and the bank desktop websites? It seems mostly to be a matter of size. When conducting larger transactions, Pakistanis appear to be more comfortable with a desktop experience, not a mobile one.

During the third quarter of 2024, the average transaction size conducted on the banks’ mobile apps was Rs43,400 while the average transaction conducted on the banks’ desktop website was Rs125,000. Whether this is the result of richer people preferring desktops or whether the same person makes a decision about which platform to use depending on the size of the transaction is not entirely clear from the State Bank’s data.

Then there is the rise of the card, which in the case of Pakistan is mostly the debit card. About 87% of the use of these cards is the with-

drawal of cash from an ATM, with a much smaller fraction going to payment by card at a physical point-of-sale or by entering the card information online on an e-commerce website or app.

However, the current strength of the ATM is likely to be illusory. Card-based e-commerce payments – albeit from a much smaller base – is among the fastest growing payment methods in the country (yes, despite the popularity of cash-on-delivery), growing at an average rate of 53.4% per year for the past 8 years, crossing $1.6 billion during the 12 months ending September 30, 2024, the latest period for which data is available.

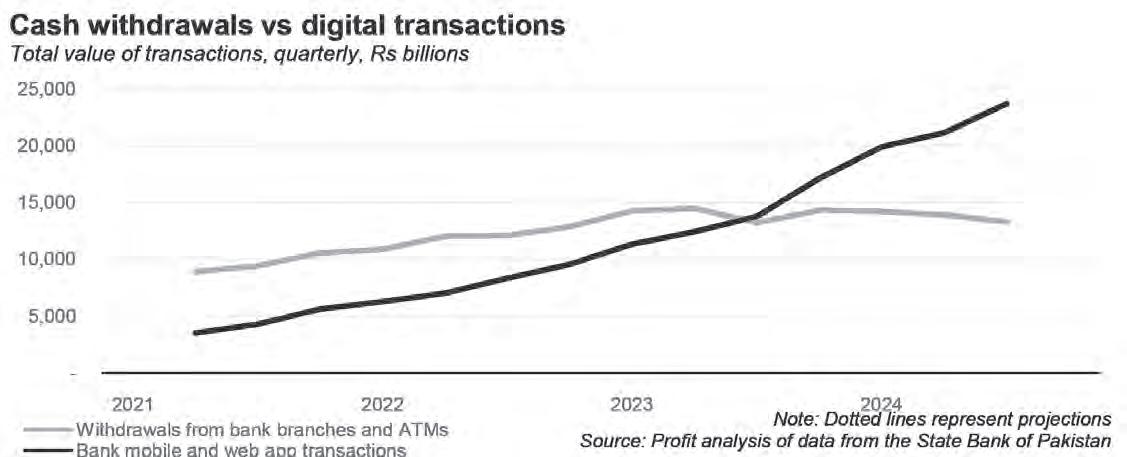

Even the use of card-based payments at physical stores is rising faster than cash withdrawals at ATMs, growing at 29.6% per year for the past 8 years, compared with just 18.4% per year for ATM transactions during that same period. For the past 12 months, Pakistanis spent $6.2 billion by swiping their cards at physical retail outlets.

Indeed, over the past year, a big milestone was crossed: Pakistanis conducted a

higher value of transactions from their bank’s mobile and web apps than they withdrew in cash from ATMs.

One would think that – with such stellar growth numbers – digital payments would be eating into the use of physical cash, but as we have stated earlier, that is not the case in Pakistan. So where is this expansion in market share coming from.

Simple: the transactions that were both documented and took place through physical means – cheques, transactions at bank branches – are the ones that are seeing decline. By far, the single biggest decline has come in the use of cheques and other paper instruments. As recently as the third quarter of 2016, they commanded a 39% share of the total value of payments in Pakistan. That is now down to just 21.5% as of the third quar-

ter of 2024.

Physical cash itself? People are giving it up, but relatively slowly.

Profit’s calculations of physical cash transactions as a percentage of total transaction value relies on the simplifying assumption that that the velocity of money for physical cash is the same as that for other means of payment. But that is about all that we have assumed about physical cash transactions. While there are lots of anecdotes about how cash is used, there is no concrete data to tell us what the cash is being used for.

We do, however, know the following facts. For the third quarter of 2024, according to the State Bank’s data, the average cash deposit at a branch was Rs304,000 and the average cash withdrawal was Rs215,000 (people conduct smaller withdrawals from ATMs, so only the larger withdrawals happen at branches). The total number of these transactions was almost completely stagnant, but the per transaction amount increased, albeit basically by inflation.

For every other form of payment, it is not just the value of transactions that is increasing, it is also their number. For cash deposits and withdrawals – which presumably happen after at least one or two layers of both-sides-physical-cash transactions – the number is up by a measly 2% per year since 2016.

If we had to guess, we suspect that the number of people who are conducting cash-only transactions is not materially increasing in Pakistan, and the total value is increasing basically only in line with inflation. These are obviously a relatively well-off group of people, which means they are likely both older and less technology savvy than younger people. And their wealth does not appear to be increasing as a percentage of the total economy, and in fact, appears to be slightly decreasing.

Based on the above data points and inferences, we think it is reasonable to assume that cash is mostly used by older businesses that were set up as cash-based sole proprietorships, and now have a hard time formalizing their businesses, so they keep doing business in cash. Their number and size is not growing relative to the size of the economy, and the growth in the economy appears to be coming from the formal sector, not the informal sector as is commonly stated by economic analysts.

These businesses have staying power for now, which is why the use of cash is not completely collapsing the way one might

have expected it to with the rise of digital payments. But they are clearly the past and will likely reach a point in the next decade or so where they either adapt to new realities or die off as a meaningful corner of the economy.

The size of the strictly-cash focused part of the economy – as much as we have been able to calculate – also indicates that the notion that there is some massive informal sector of the economy that is not captured in the gross domestic product (GDP) numbers is

likely not accurate.

Cash is still king in Pakistan, and clearly is sticking around a lot longer than any modernizing sensibility might have hoped for. But details of its use – the minimal amounts we are able to surmise – leads us to conclude that its days are numbered, and it will eventually make way for a nearly completely digital payment system.

The future is on its way. Just a bit slower than hoped for. n

Jute, once Pakistan’s most important crop now an embarrassing anecdote, might be caught up in a PSX pump-and-dump

It has been a long time since jute was vital to Pakistan. So could unusual activity in the share price of a jute miller indicate a pump and dump scheme?

By Zain Naeem

In the middle of the state emblem of Pakistan, right there for the entire world to see, resides an embarrassing secret. Surrounded by a wreath of Jasmine, Pakistan’s national flower, is a quartered shield. In each of the four sections there is the image of a crop.

From left to right these are cotton, wheat, tea, and jute. In 1951 when Pakistan ceased to be a dominion of the British Empire and became a republic in its own right, these were the most important crops grown in the entire country. Two of them, tea and jute, were grown in erstwhile East Pakistan.

Today, Pakistan imports both of these products. Last year, imports of tea were worth close to a billion dollars. While the vast majority of this came from Kenya, there were also tea imports from Bangladesh close to $90 million. The import of jute is far less extravagant, costing Pakistan over $52 million in 2023, with nearly all of that coming from Bangladesh. While Pakistan is not a big exporter, jute is a major cash crop for Bangladesh, and a pillar of their textile industry. In 2024, the export of jute yarn, sacks, and products constituted nearly $900 million. In fact, before Bangladesh gained independence in 1971, jute was the single largest export oriented product in United Pakistan.

Today, jute is little more than a shameful and shoddy remnant, and not just on the state emblem. After 1971, what remained of Pakistan still needed jute. Industries, packaging, and trade were all reliant on jute bags. As a result, a number of jute mills began popping up in West Pakistan in the late 70s. These mills would import jute fibre and turn them into bags before either exporting them or selling them on the local market. This industry still remains, although it has been a bit of a startstop affair.

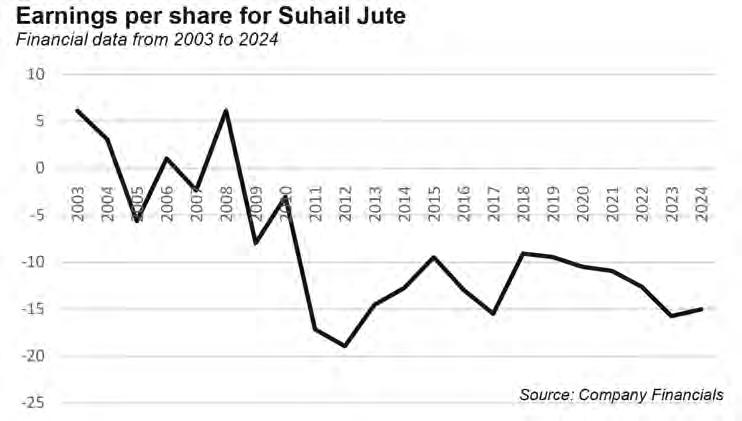

Take, for example, Suhail Jute. The company was established in 1981 and has been involved in the production of jute related products. It was involved in manufacturing of twine, Hessian clothes and sacking cloth. From the beginning, the financial performance saw highs and lows as earnings flipped flopped between profits and losses.

But in recent days Suhail Jute has been the epicenter of something strange. In a space of just 18 days, the company’s share price has

seen an increase of nearly five times. This is, of course, in a market that has witnessed an increase of almost 300% since June of 2023, so companies performing well are not suspicious by nature. But the exchange increased over a span of one and a half year, which means that the yearly return earned by the exchange was around 200% while Suhail Jute will see an annualized return of 60 times if the same trend was expected to continue.

So what is going on? By all accounts there is no jute resurrection in Pakistan. Has Suhail Jute uncovered a pot of gold? Or is there more to it that the Pakistan Stock Exchange (PSX) should be looking into?

In the summer of 1964, Time Magazine ran an article titled Pakistan: Jute King. Nearly two-decades into statehood, jute was probably the most recognisable product coming out of Pakistan. Within the Indian subcontinent it had long been known. Its earliest recorded mention can be found in the Ain-i-Akbari, the 15th century text recording the reign of Mughal Emperor Akbar. Jute at the time was used as a low-grade fabric to make clothes. It was then simply a cheap alternative to cotton.

But the influence of jute, particular jute from Bengal, has been felt all over the world. In fact, in the colonial era it was a very important crop that often was useful during times of international conflict.

It was during the Napoleonic wars that Britain’s supply of Russian flax was interrupted, making jute an important and immediate alternative. Initially, there were difficulties. Jute was difficult to process and turn into sacks in European flax mills. Bengali kareegars would make jute fibre by hand on smaller cotton looms in the off-season. By the 1830s, however, Scottish firms Balfour and Melville cracked the puzzle of processing jute for industrial use, employing water and whale fat to soften its coarse fibers. Their breakthrough turned jute into a viable material for European mills. Orders soon flooded in for burlap sacks destined for sugar plantations in Dutch-controlled Java. Bengal’s abundant jute fields suddenly became a vital cog in the machinery of global trade.

Jute, once the coarse thread used to make cheap clothes, quickly became known as the “golden fiber”, becoming the lifeblood of

Bengal’s economy. In 1855, the first jute mill in British India opened in Rishra, near Kolkata, heralding the dawn of industrial-scale production. By the late 19th century, Kolkata had cemented itself as the epicenter of the jute trade, with mills multiplying rapidly. By 1901, 51 mills employed over 10,000 workers, exporting sacks, ropes, and fabrics as far afield as the United States and Australia. For British India, jute became the second-largest industry after cotton.

But the success wasn’t without its fractures. Most mills were owned by foreigners, while the labor force remained predominantly local. The economic ebbs and flows of the early 20th century—a price surge in the 1920s followed by a collapse in the 1930s—exposed the vulnerabilities of an industry tied to fickle global demand. Reports commissioned by the British Raj in the Great Depression painted a grim picture of the boom-and-bust cycles haunting the trade.

But jute would not stay down. The second world war brought renewed interest, and by the time of partition it was the most important crop and export product in the newly minted state of Pakistan. Partition brought new problems. Most of the jute was grown in East Bengal, now known as East Pakistan, but jute mills were mostly in West Bengal, and had been a major cash cow for Calcutta industrialists. Pakistan and India were at an impasse.

This proved to be one of the early moments of industrial zeal and ingenuity in Pakistan. Instead of relying on exporting the raw product to West Bengal and making an easy buck, Pakistan embarked on an ambitious industrialization drive. By 1951, Adamjee Jute Mills—a project supported by the Pakistan Industrial Development Corporation (PIDC)— emerged as a beacon of this effort. It was joined by other mills like Bawa Jute Mills Ltd. and Victory Jute Products Limited, propelling Pakistan into the global jute market.

Investors from West Pakistan such as the Bawanis, Adamjees, Isphahanis, Dawoods and many others flocked together in setting up a good number of jute mills in Narayanganj, Khulna and Chittagong. The Adamjee Jute Mills set up by the well-known industrialist Abdul Wahid Adamjee in 1951 became the largest jute mill of the world employing around 30,000 workers. By 1960, East Bengal boasted 14 mills, 12 of which owed their existence to PIDC backing. However, most of

these ventures were spearheaded by non-Bengali entrepreneurs from West Pakistan.

In 1970, a year before Bangladesh gained independence, East Pakistan had 77 jute mills employing 170,000 workers and had become the world’s largest exporter of jute, contributing 46% of Pakistan’s foreign revenue.

Pakistan was now left with a problem. There were 12 jute mills in West Pakistan and there was no jute. It was the same problem India had faced in 1947, and much like West Bengal, Pakistan accepted the new reality and the mills began importing raw jute from India. Efforts have consistently been made to grow jute in Pakistan, but they have largely been unremarkable at best and woeful at worst.

In the midst of all this, Suhail Jute was incorporated in 1981. The challenges for a jute company at this juncture were clear, and Suhail Jute’s performance reflects this. A snapshot of the past two decades is revealing. Going as far back as 2003, the company experienced profits in some years while it has suffered losses in others. Earning per share was at its highest in 2003 registering at Rs 6.13 per share which was quickly followed by a hugely loss making year where a loss per share of Rs -5.63 was made in 2005. The volatility that was caused was due to the cost of raw materials that the company was paying in order to manufacture its products.

Even though the performance was volatile, the profits earned meant that the operations could be continued. One strategy that was being used in order to remain profitable was through purchase of National Investment Trust units which were complimenting the profits. From 2006 to 2008, this source of income raised Rs 17 crore from which around half were earned in 2008 alone. What worked in the good years turned disastrous in 2009 when the stock market saw a freeze and it ended up making a loss of Rs -7.96 per share.

While the investments were making losses, the gross profits earned were one of the highest in its history as it earned 5 crores as gross profits in 2009. In 2010, Suhail Jute was able to reduce these losses as gross profits stayed high while some of its investments recovered. This showed that the business model was generating ample amounts of return to justify production to be carried out.

It seemed that despite the raw material being imported, jute mills had figured out a way to be profitable in Pakistan. All of this changed in 2010. In the summer of that year,

Pakistan’s entire economy is tightly interwoven with jute, which is second only to cotton as the world’s most widely used natural plant fiber. Last week Pakistan’s vital jute industry was snarled in a strike of nearly 60,000 workers who are demanding higher wages. Some mills were the scenes of clashes, and others resolutely evicted all workers. The mood was different at the mills of one jute maker, who has retained the good will of his striking workers by continuing to provide them with their regular fringe benefits of inexpensive company housing and rice at below-market prices.

Such shrewdness irked other mill-owners, but it came as little surprise. Gul Mohamed Adamjee, 44, has not only made his mills a South Asia showcase of enlightened management (Queen Elizabeth and Prince Philip have visited them) but has propelled himself into the industry’s top position as Pakistan’s “Jute King.” His Adamjee Jute Mills Ltd. produce a third of Pakistan’s jute goods and consume more raw jute than all of the mills in Britain, which ranks second to Pakistan in the manufacture of jute products.

Bags & Tea. In an industrial complex near Dacca, East Pakistan, some 20,-000 Adamjee workers annually produce 70 million burlap bags and 90 million square yards of cloth to be used in products as diverse as automobile seats and jute suits. Nearby, Adamjee has just opened a new factory that will ensure even greater use of Pakistan’s jute crop by producing particle board out of jute stems, providing a low-cost wood substitute for lumber-poor Pakistan. He is also almost single-handedly diversifying Pakistan’s industry, using jute profits to build a $2.1 million cotton mill, a $6.3 million sugar refinery, a tea company and a vegetable-oil plant in other locations.

Until the Moslem-Hindu partition that created Pakistan in 1947, the Adamjee family owned a jute mill near Calcutta and ran a thriving export business. Then partition left Pakistan with 42% of the world’s jute crop and no jute mills. To Adamjee, a Moslem, his duty was clear. He liquidated his substantial holdings in India, moved his entire family to Pakistan, where the grateful government helped him finance the new nation’s first jute mill. Today, the family’s assets are $75 million. In West Pakistan, Adamjee’s two brothers have constructed a $6.3 million cotton mill, a $5.2 million paperboard mill and a chemical factory. A family holding company, Adamjee Sons, Ltd., established and owns Pakistan’s second-largest insurance company and a major bank with 120 branch offices.

Mohamed’s Mosque. “I suppose I am a millionaire,” says Adamjee, “a poor Pakistani millionaire.” He has attempted to repay Pakistan’s hospitality by establishing a $420,000 science college and contributing $100,000 a year to charity. As for his workers, whom he expects to see back on the job soon, Adamjee pays them double time for overtime, also provides a pension plan, free medical care and schooling. On the company grounds at the Dacca complex, the benevolent boss has built a house of worship that his workers have respectfully nicknamed the “Adamjee Mosque.”

Excerpt from Time Magazine, December 4th, 1964

the manufacturing plant was left devastated when the country suffered from floods. Due to the damage caused, production had to be halted and the machines were turned off for the last time. The extensive damage and deterioration meant that the production had to be stopped in order to carry out the necessary repairs. It was expected that once these had been done, the plant would be humming once again.

This never came to pass as Suhail Jute started to spiral downwards. In 2011 and 2012, it was able to see some sales, however, the losses booked due to damage to raw material meant that the losses were too large. In 2011, the company saw losses of Rs -17 per share which increased to Rs -19 per share in 2012. With rising costs of raw material, rising administrative costs and losses being made by their investments, it proved to be the perfect storm leading to magnified losses. The plant

had already been shut down and now the sales dried up as well.

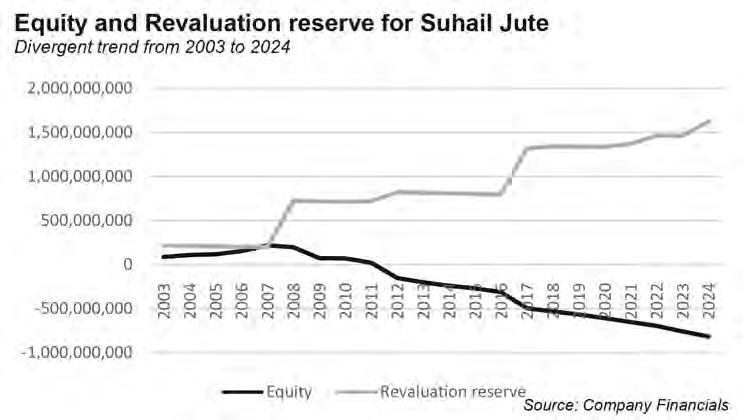

The impact of the losses started to weigh down on its equity. The equity was valued at around Rs 22 crores as far back as 2007, however, the losses of 2011 and 2012 meant that this became negative in 2012. Due to the magnitude of the losses, equity of Rs 37 crores was wiped out in a matter of 5 years. The only element protecting the equity was the revaluation reserve which had increased from Rs 22 crores in 2003 to Rs 82 crores in 2012. In order to fund some of the gap created by the losses, directors had to provide a loan while short term liabilities were used in order to accrue the expenses that were coming due. This led to short term liabilities increasing from Rs 9 crore in 2003 to Rs 25 crore by year end of 2012.

Suhail Jute is part of a group of companies that included Colony Sarhad Textile Mills.

Even before Suhail experienced its own hardships, Sarhad textile mills were seeing their own troubles as the textile mills were facing their own crisis. In order to help an associate company out, Suhail had lent money to Sarhad which was standing at Rs 7 crores by the end of 2012. There were few chances that Suhail would see these funds in the near future which meant that its assets were overvalued from where they would be realized at.

With such a dire situation, things were only going to get worse as production was stopped and administrative expenses were still being paid. From 2013 to 2024, the earnings per share have been consistently in the red with cumulative losses of Rs 1 billion being made. With no source of income or cash generation, it was felt that there was not enough working capital available with the company to justify production. With no source of funds, the repair work could also not be carried out. Suhail Jute was stuck in a Kafka-esque nightmare as it was not able to carry out production due to lack of funds and it was not able to raise any funds as no production was possible.

The challenges were mounting, and their lenders went to court in order to recover anything from Suhail. With no access to additional borrowing, the directors stepped in to make sure that salaries could be paid and the basic skeleton of the company could be maintained. What started off as a loan of Rs 2 crores has increased to Rs 34 crores by the end of 2024. Similarly, the accrued expenses have also increased from Rs 27 crores to Rs 50 crore by 2024. As the losses have continued to pile up, the equity has fallen to Rs 81 crores in the red. The only saving grace is the fact that the revaluation reserve has gone to Rs 1.6 billion which

is able to sustain the equity to some extent by keeping it positive.

In terms of its loan to Sarhad, a merger was carried out between Sarhad and Suhail where the land and production facility of Sarhad was sold to Suhail in exchange for the outstanding loan. In 2017, the merger was finally carried out and the loan of the associate was wiped off. It was felt that the merger would increase the assets and reduce the negative equity that existed on the balance sheet. There was also a likelihood that the assets could be used for further financing from banks.

The management at Suhail was confident that they would be able to revive itself and showed their commitment by providing loans to the company at no interest in order to put their money where their mouth was.

As the production facility stays dormant, the reality has changed little and it seems that the company is standing at the precipice right now. In this condition, the management at Suhail has realized that it would be impossible to restart production and there are active efforts being made to carve out the assets of the

company and to sell them piece meal in order to generate as many funds as possible.

From an outsider’s perspective, the affairs of the company were regularly being assessed by its auditors who kept raising red flags at the things within the company. The auditors kept feeling that the receivable from Sarhad was going to become obsolete and the company needed to write off this asset from its books. The management stated that the sale of land would make this receivable redundant. The auditors also felt that the losses being made and the factory being closed raised concern over whether the company could continue into the future as a going concern. The management was able to show their commitment by injecting necessary funds.

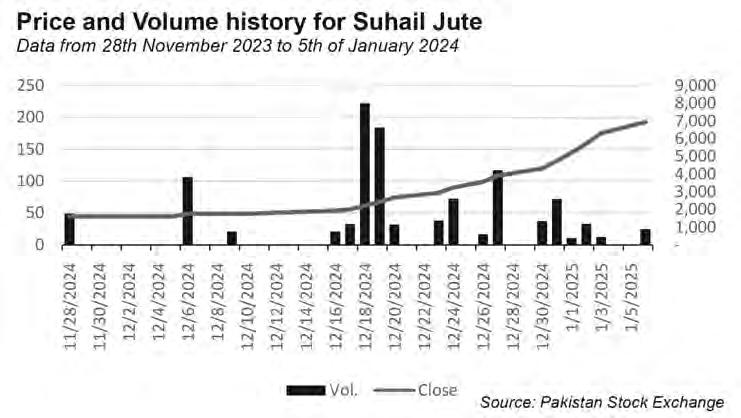

In short, all of this shows that the conditions at the company are bleak to stay the least and something monumental would have to change before any recovery could be envisaged. But it seems that the stock market is already expecting things to change before anything substantial has been disclosed. An increase of share price by five times is already extraordinary. When it is being seen in a company which is weighed down by debt and is shut down for more than 10 years, then suspicions start to rise.

Going as far back as 1995, it was seen that the share price was hovering around Rs 3. The shareholding has mostly been held by the directors and associates and the volume has been thinly traded. As there are few shares available for trading, the share is seldom traded seeing very low volumes. The share price rose to Rs 30 when the financial position of the company was improving and profits were being earned before it fell back to Rs 10 when

the plant was shut down. From 2015 to 2021, Suhail failed to deposit the necessary fees to the exchange which led to suspension of its shares trading altogether.

Once trading restarted, the share price floated between Rs 10 and Rs 60 while the volumes were again low considering the rest of the market. In December 2024, things changed. The share price was traded at Rs 40.21 on 5th of December and in a course of a month, it has reached Rs 193 by 6th of January. From 17th December, the price has consistently increased by 10%, maximum allowed for a day, for 13 consecutive trading sessions. The average daily volume of the trades are only 3,300 shares. So what exactly has changed which has warranted such an increase in share price? According to the company’s disclosures, there seems to be no material information which justifies this increase.

Based on the Pakistan Stock Exchange (PSX) rulebook, the listed companies compliance sends a letter to the company asking them to explain the reason behind the increase in price and to release any material information that might not have been disclosed. This is just a letter that is sent and the listed companies have a simple reply to these letters that they are not aware of any material information. A basic shrug of the shoulders phrase of “I don’t know” in reply to the question asked. The letter is taken as final and no subsequent investigation is carried out. The formalities are completed and nothing takes place after that.

The problem with this measure is that investors are the ones who lose out at the end. As the share price is improving, there is a feeling that something has taken place at the company and that things might be changing. Fueled by the price increase, rumors are circulated in the market which start to confirm the suspicions and interest in the company starts to gain traction. The price keeps increasing and investors sit up and take notice. With little information to go by, they invest their hard earned savings expecting the share price to keep going upwards. This is how the classic pump and dump works. A company starts to see its share price increase out of nowhere. As investors start to get involved, the price initially increases and then once the manipulator feels he has seen the apex of the share price, he starts to dump the shares in the market to earn a quick profit. The investor who was pumping the price from the beginning starts to sell his shares at a higher price and leaves the other investors to be left holding the bag. Since the 6th, the share price has crashed in reverse and the share price was at Rs 140.74 on the 9th of January. Investors

who would have bought at Rs 193 have seen a quarter of their investment evaporate into thin air.

The shareholding pattern shows that less than 4% of the shares are free floating and the thinly traded nature of the shares means that the price can be increased or decreased with very few shares being traded leading to large price changes. There have been cases of pump and dump that have taken place in the recent rally as companies with shut production plants have seen their share price increase before crashing back to where they had started their rally. The examples of Bela Automotive, Data Agro and Chakwal Spinning are just to name a few. All of these companies have seen their share price increase manifold before coming back down again. Of course, cases only become clear over time and with investigation. Even then they are often left unsolved. But there have been plenty of cases to raise alarm bells when something like this happens.

So what can be done in order to not let pump and dump strategies take place/ Well for starters, the company can be proactive on their own part and try to distance itself from any such activity. When Bela Automotive was seeing its price increase, the management and the majority shareholders actually sent a letter to the exchange saying that they were cognizant of the increase in price and that they were asking for an investigation to be launched. Something similar can be called for by Suhail Jute which will protect them from being accused of any such allegations. It will also take some air out of the bubble and bring some transparency into the market. What can the regulatory bodies do? For starters, the PSX needs to be more vigilant. With people’s money being at stake, the exchange should look to be stricter. Rather than just sending a letter, the exchange needs

to investigate who is trading in the shares and whether they are perpetuating a pump and dump strategy to earn a quick buck at the expense of the investors. Trade data is available with the exchange which can shine some light on how the share price has increased. The fact that the company is suffering financially only magnifies the point that the price was being increased with no fundamental reason or rationale behind it. The subsequent crash in the price only compounds the feeling that a pump and dump has been carried out and someone needs to be punished for taking the investors for a ride.

The Securities and Exchange Commission of Pakistan also has jurisdiction if it feels that markets are being manipulated at the expense of the investors. In relation to Suhail Jute, the SECP was asked for a comment in which it stated that “(W)ith reference to the query regarding share price of Suhail Jute Mills Limited (“SUHJ”). This is to apprise you that share price in stock market is driven by demand/supply forces and closing price of the share is determined by mechanism given in Rule Book of PSX.”

“Furthermore, we would like to inform you that we are actively monitoring trading activities in the stock market to detect any potential market abuses and other forms of unlawful practices. In case any instances of market abuse is identified in relation to the stock of SUHJ, appropriate actions will be initiated as per law.”

Rather than sending just a letter, the exchange should launch an investigation using the trade data and make the market aware that they are launching an inquiry to figure out what was actually taking place. The PSX has been one of the top performing exchanges in the last year. In such a situation, adding these guard rails and checks and balances will only build the trust of the investors in the transparency and fairness as well. n

The process has been long and some strong contenders have failed to make it to the other side. Will Mashreq Bank live up to its expectations as a digital bank in Pakistan?

By Hamza Aurangzeb

In case you missed it, a great battle has been underway in Pakistan’s banking sector for nearly three years now. It started in March 2022, when the State Bank of Pakistan (SBP) announced it had created a digital banking framework. The announcement had the entire banking sector on its toes. This was a chance to be an early mover in the future of banking. Everything about digital payments and EMIs in Pakistan had shown commercial banks that digital was the way to go in the future. And what is the harm if you can have a full-fledged bank without incurring the massive capital cost of opening branches?

Everyone scrambled to put together propositions to the central bank. They received as many as 20 applications from leading banks such as HBL, UBL, Alfalah and JS, microfinance banks, domestic fintech companies, foreign fintech companies and large business groups that formed a consortium with partners that know banking.

From this initial glut of applicants, the SBP began a weeding process. It took them nine months, but in January 2023 they whittled this down to five candidates. The state bank granted NOCs to five institutions — namely Easypaisa, Hugo Bank, KT Bank, Mashreq Bank, and Raqami Bank — to set up digital banks. It would take another nine months, but in September 2023, these institutions were subsequently granted in-principle approval. Up until this place the chosen-five were neck and neck.

Now, nearly two whole years after the shortlisting, a frontrunner has emerged. Mashreq Bank has been granted the first restricted license to begin pilot operations in the country this past week. This means that within an enclosed group of people, the bank can begin its operations with the SBP closely observing how it goes.

Mashreq Bank has always been a strong contender. While it is not a name as recognisable as Easypaisa, probably the most household name in the entire list, it has some strong backing. It is one of the largest conventional banks in the Middle East and also has a brickand-mortar presence in Pakistan. Mashreq Bank’s digital bank offerings in the Middle East include specialised banking solutions for startups and SMEs, and calls itself the “Best Digital Bank” in the MiddleEast.

Digital Banks require some serious investment as well. While the initial capital requirement may be $25 million, to run a successful operation it will stretch to much more. According to some estimates, it could go as high as ten-times that figure.

Mashreq Bank is the oldest private bank in the MiddleEast, having been founded in 1967. Its founder, Abdul Aziz Ghurair, sits on a multibillion dollar fortune according to Forbes and the bank is majority owned by the Ghurair family – one of the richest families in the MiddleEast – through two different investment firms. They also have the technological experience, being the first to make a digital only bank for retail called NeoBiz.

All of these are signs for why Mashreq Bank could be the real deal in the digital banking space. But being first does not always guarantee you will win. There are other strong contenders still hoping to break through, and even if the competition is far, the terrain of Digital Pakistan is not the easiest to traverse, especially when you are first on the scene. After all, you do not want to become an example others learn from.

The SBP’s regulatory framework for Digital Banks was introduced in January 2022 and established two distinct categories: Digital Retail Banks (DRBs) and Digital Full Banks (DFBs). While DFBs can serve all customer segments, DRBs primarily focus on retail customers. Though DRBs may offer services like e-wallets and digital payment accounts to corporate or commercial segments, these accounts must not exceed 40% of total deposits, excluding P2G, G2P, and utility payments. DRBs must maintain stringent capital requirements, including a minimum Capital Adequacy Ratio of 15%, comprising 9.5% CET1 CAR, 12.5% total CAR, and a 2.5% Capital Conservation Buffer.

Within this framework, the central bank also laid out a structured path for what to do if an entity wants to establish itself as a digital bank. It starts off pre-application consultations with the SBP. Applicants must submit comprehensive documentation, including a feasibility study and business plan, along with

a Rs 10 lakh processing fee. They must demonstrate their financial capacity to meet capital and liquidity requirements. Success at this stage leads to a No Objection Certificate from the SBP, allowing incorporation as a public limited company with the SECP.

Following incorporation, you enter a 12-month In-Principle Approval phase. Upon achieving operational readiness, a restricted license for pilot operations lasting three to nine months is granted. During this pilot phase, operations are limited to select groups such as sponsors, employees, and their relatives.

With an initial Minimum Capital Requirement (MCR) of Rs 1.5 billion, deposits are capped at 25% of MCR with individual limits of Rs 5 lakh, while lending cannot exceed 50% of the deposit base. This controlled environment allows for thorough testing of systems, products, and customer engagement protocols.

The final stage begins with commercial launch, initiating a three-year transition phase. The MCR increases to Rs 2 billion initially, rising to Rs 4 billion by the third year. This phase implements progressive caps on deposits and lending to ensure controlled growth. Deposit limits start at six times MCR, expanding to twelve times by the third year, while the Advances to Deposit Ratio (ADR) gradually increases from 50% to 70%. Consumer finance remains restricted to 40% of total advances throughout. Upon completing the transition phase, deposit limits are removed and ADR increases to 80%, though the consumer finance cap persists at 40%.

Digital retail banks like Mashreq Bank represent a fundamental shift in banking, offering streamlined services that traditional banks cannot match. The key differentiator is end-to-end digitalization: from online KYC verification to instant loan decisions based on automated credit scoring that considers income, credit history, and digital footprint. This eliminates weeks of manual processing typical in conventional banking.

The digital advantage extends beyond basic services. While Electronic Money Institutions (EMIs) excel in payments and transfers, digital retail banks offer a comprehensive suite of financial products including investments, lending, and insurance. Their

platforms typically provide superior user experience compared to traditional banks’ often problematic mobile apps.

Both Mashreq Bank and Easypaisa enter this space with significant advantages. Mashreq leverages its existing back-office operations in Pakistan, while Easypaisa builds on its extensive branchless banking network, giving them solid foundations for digital banking operations.

According to banking experts, these digital banks primarily target urban millennials and Gen Z, though their services extend to older generations with larger deposits. Millennials, with established credit histories and stronger earning potential, are immediate prospects for credit products. Gen Z, while currently focused on basic transactions, represents future growth potential. SMEs and corporate clients will receive limited services initially, with rural expansion planned for later stages.

However, the path to digital banking success in Pakistan isn’t straightforward. The prevalence of traditional bank branches across the nation underscores a crucial reality: establishing a viable digital retail bank in Pakistan’s unique market conditions presents significant challenges beyond the apparent technological advantages.

Digital retail banks face several challenges that could impact their ability to grow and operate efficiently in a highly competitive and rapidly evolving financial landscape.

The primary obstacle for Mashreq Bank, like any other digital bank operating in Pakistan, will be raising deposits. Unlike traditional banks, which benefit from physical branches where customers can directly deposit cash, digital banks like Mashreq Bank rely on digital channels to gather funds.

This presents a challenge in attracting customers to deposit money, as many consumers are still accustomed to the traditional brick-and-mortar experience. Furthermore, they also lack the extensive physical infrastructure and personal relationships that help traditional banks maintain high levels of deposits. Thus, Mashreq Bank may struggle to convince customers, particularly former generations with enormous deposits, to entrust them with their funds due to the absence of trustworthy relationships. As they say, “the more hands you shake, the more money you make.”

Another significant challenge for Mashreq Bank is managing liquidity, particu-

larly regarding where customers can deposit and withdraw money. Since it will primarily operate through online platforms, it will face limitations in offering easy access to physical cash and facilitating cheques. The convenience of accessing cash and using cheques with digital banks may not be as immediate or widespread as with traditional banks that have an extensive network of branches and ATMs. Furthermore, it must maintain adequate liquidity to meet withdrawal demands while optimizing its investments. This balance is critical for maintaining financial stability and trust among customers who expect quick and seamless access to their funds at all times.

While the above two might seem like daunting tasks, another pressing concern for Mashreq Bank is cybersecurity, the foundation on which its existence depends. As a digital-first institution, it is vulnerable to a range of cyber threats, including cyberattacks, phishing schemes, and data breaches. These threats not only jeopardize the security of customers’ personal and financial information but also damage the reputation of the bank. Moreover, digital financial literacy remains restricted in Pakistan, which poses a significant challenge, particularly as the adoption of digital banking grows. Many customers are unfamiliar with secure online banking practices, making them more vulnerable to online scams, fraud, and unauthorized transactions. The gap in awareness about managing passwords, recognizing legitimate communications from banks, and avoiding cyber threats often leads to security breaches. This limited understanding hinders trust in digital platforms, slowing the transition from traditional to digital banking.

While digital retail banks such as Mashreq Bank offer innovative services and convenience, they must navigate significant challenges related to raising deposits, liquidity management, and cybersecurity. The effective resolution of these issues is essential for their progress in the modern financial ecosystem.

Mashreq Bank, in order to amass gigantic sums of deposits might offer enticing financial incentives to customers such as higher savings yields, lower credit card rates, and innovative reward programs such as cashback, travel perks, or exclusive benefits. These offerings will not fill their treasuries with funds but encourage customer engagement and drive long-term loyalty. Moreover, it could introduce tiered benefits based on account activity or balances, which can further incentivize customers to deposit and maintain higher funds with the bank. These schemes will not only

enable them to appeal to a broader audience but also persuade millennials and Gen Z to prefer them over traditional banks.

As far as high-net-worth individuals (HNWIs) are concerned who like to do things the customary way, Mashreq Bank might opt for personalized services, such as virtual relationship managers for them. These virtual assistants can offer tailored financial advice, assist with complex transactions, and provide a human touch in the digital banking experience. Mashreq Bank might attract and retain a key segment like HNWIs through this initiative of virtual assistants, where a human is ready throughout the day to help them with alacrity.

Another effective method for Mashreq Bank to overcome its operational challenges could be forging partnerships with conventional banks. Traditional banks can provide their APIs to Mashreq Bank, which will enable it to access customer data, allowing it to evaluate the creditworthiness of an applicant more accurately and extend loans more effectively. Additionally, it can leverage conventional banks’ ATM networks for cash withdrawals and deposits, eliminating the need for establishing its own infrastructure.

On the contrary, traditional banks can generate additional revenue by extending their APIs, customer data, and ATM networks, while simultaneously getting a shot to crosssell their financial products to young and tech savvy customers. Moreover, there is a possibility that both parties could collaborate to come up with new ingenious financial products.

Another prerequisite for Mashreq Bank must be to invest heavily in advanced cybersecurity measures, given the rising threat of cyberattacks, where features such as encryption, multi-factor authentication, and real-time threat monitoring are essential to protect customer data and assets. They should also conduct regular customer education campaigns to raise awareness about phishing scams and online safety practices among customers. This way it can empower customers to recognize and avoid cyber threats by fostering digital financial literacy among them, building their trust in digital platforms and ensuring rapid expansion of Mashreq Bank.

The evolving demands of Pakistan’s population, especially its younger generations, make a strong case for the introduction of digital banks like Mashreq. These institutions have the potential to revolutionize financial access and meet the expectations of tech-savvy consumers. However, establishing a financial entity like a digital bank, specifically in Pakistan, a country characterized by a volatile economic environment and complex regulatory challenges will definitely prove to be a strenuous task if not impossible. n

How a home-grown pharmaceutical company is redefining resilience and leading Pakistan’s healthcare transformation

IBy Partner Content

n 2023, Pakistan’s pharmaceutical industry grappled with significant economic pressures. Soaring inflation, a steep currency devaluation, and shrinking profit margins created

an environment where many companies found it difficult to survive. Amidst these challenges, however, Highnoon Laboratories Ltd emerged as a standout performer, defying industry trends with remarkable resilience and ambition.

Founded in 1984 in Lahore, Highnoon has grown from a modest local

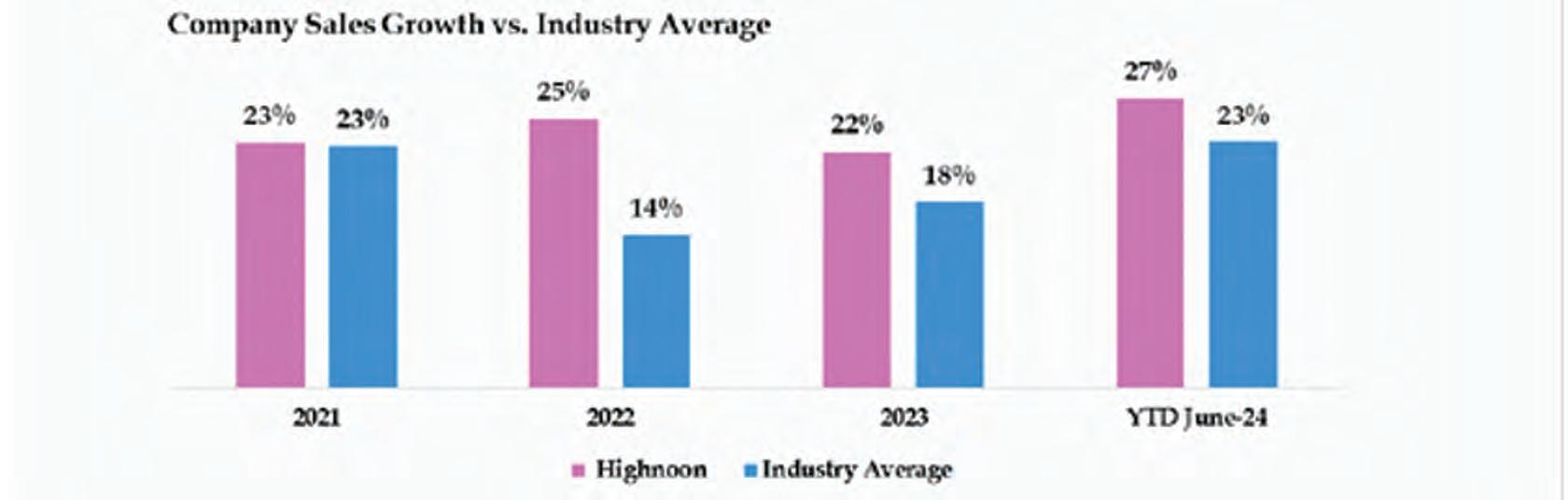

enterprise into one of Pakistan’s most reliable healthcare brands. Achieving an impressive 22.8% year-over-year revenue growth in 2023, reaching PKR 19.4 billion while maintaining earnings at PKR 2.4 billion (PKR 45/share). These results are particularly impressive in a year when the overall earnings of listed pharmaceutical companies in Pakistan fell by a staggering 42%.

Over the years, the company has solidified its reputation as a trusted partner for healthcare, an investor favourite, and a consistent market performer. This achievement is rooted in Highnoon’s strategic agility. Its legacy brands like Ulsanic, Combivair, and Triforge continue to drive consistent demand, while its portfolio expansion has allowed it to tap into unmet needs in therapeutic categories. With a 10-year CAGR (Compound Annual Growth Rate) of 20%, the company has consistently outpaced the industry’s growth trajectory.

Now, with its sights set on international expansion, Highnoon is strategically diversifying its revenue streams to sustain and elevate its position.

Pakistan’s pharmaceutical exports reached $341 million in 2023-24, a fraction of India’s $28 billion. Despite this disparity, a former chairman of the Pakistan Pharmaceutical Manufacturers’ Association (PPMA) stated that the country has the potential to grow exports to $3 billion within five years if supported by favorable policies. Highnoon is already contributing to this effort, steadily increasing its share of export revenue.

The company’s export revenue share has increased from approximately 4% in 2019 to around 6% in 2023, slightly ahead of industry hovering between 4%to 5% during this period. While this growth aligns with broader industry trends, it underscores Highnoon’s commitment

to expanding its global footprint. The company now plans to accelerate this momentumand channel checks indicate that the export share proportion in the company’s revenue is expected to reach around 8% in 2024, with higher targets set for the upcoming periods.

The company’s efforts were further recognized with the Pakistan Pharma Export Summit & Awards (PESA 2023), a testament to its role in driving Pakistan’s pharmaceutical footprint globally.

The government’s historic focus on stringent price controls hindered growth and drove multinationals out of Pakistan. Companies like Merck, Roche, and Johnson & Johnson exited due to unsustainable pricing policies. However, recent revisions in the pricing framework, particularly for non-essential drugs, have given companies like Highnoon a competitive edge.

Highnoon stands out as one of the few companies whose share of non-essential drugs exceeds 50%, alongside peers like AGP, Abbott, and Haleon. According to IQVIA data, Highnoon’s unit growth is significantly higher than the industry average, indicating that while many companies have capitalized on price increases under the new drug policy, Highnoon has largely focused on driving growth through volume rather than price adjustments. This strategy leaves the company well positioned to continue benefiting from the policy shift.

With aspirations to rank among Pakistan’s top five pharmaceutical companies by 2027, Highnoon’s

Source: IQVIA Report

vision is both ambitious and achievable. The company plans to build on its legacy through portfolio diversification, strategic international expansion, and innovation-driven growth. By balancing its rich heritage with a forward-looking approach, Highnoon is shaping a future defined by sustainable success.

Recent accolades, including being recognized four times in the past five years by Forbes Asia’s Best Under a Billion, highlight the company’s commitment to excellence. With a unique blend of legacy and leadership, Highnoon is not just aiming for the future—it is setting the pace for the pharmaceutical industry in Pakistan.

In an industry often scrutinized for legal and ethical challenges, Highnoon has made regulatory compliance and ethical standards central to its operations. The company’s leadership goes beyond business growth, ensuring adherence to all regulations and setting a benchmark for corporate integrity.

From its humble beginnings in Lahore to its consistent growth, Highnoon has turned challenges into opportunities. The company is steadily advancing toward solidifying its position within the pharmaceutical landscape. By blending a rich legacy with forward-thinking leadership, Highnoon continues to shape the future of healthcare, quietly yet confidently contributing to the broader industry’s evolution. n

In 2018, Always was the premier feminine hygiene product in Pakistan’s retail market. In only a few years, Butterfly has taken away a chunk of their market share. What happens next?

PBy Nisma Riaz

akistan’s homegrown sanitary napkin brand Butterfly is making waves in a market long dominated by international giants like Procter & Gamble. Santex’s Butterfly has managed to achieve what many considered impossible– doubling its market share from 12% to nearly 25% in just a few years. And this is not a sudden change spurred on by external circumstances. Santex has been on a mission and has seen consistent growth, with customer preference changing fast. As a result, a battle has ensued between P&G and Santex.

Butterfly has been around for a while. The sanitary napkin brand was first launched by Santex in 1983. In a market that was still developing, this was Pakistan’s first local feminine hygiene product to hit pharmacies and the retail market. But Butterfly’s story begins with a bit of failure. Despite its unique positioning as the only authentic and branded local pad manufacturer, the brand struggled to maintain its position against international competition. In the mid-1990s, P&G introduced the Always brand to the Pakistani market and for all intents and purposes blew Butterfly out of the water. Their products were not well known, or well-stocked.

It was part of P&G’s strategy of coming in hard in new markets. Just think about it. For an entire generation of Pakistanis, the word ‘Pampers’ is synonymous with the word diaper, even though pamper is the brand name

of P&G’s product. It is the same way washing powder is known as Surf no matter what brand it is, simply because Unilever’s Surf Excel had gained such popular appeal and recognition. In the same way, sanitary pads were known as Always.

What Santex did right in the face of this assault was to not give up. From the mid 1990s all the way up to now, they have continued to produce, market, and sell. Over the years, the number of Pakistani women entering the formal workplace has increased. The female labour force participation rate rose from under 16% in 1998 to a peak of 25% in 2015. And this is the labour participation rate, meaning the number of women increasing in the work force proportional to the overall population. All in all, as the population has increased, millions of women have become a part of the workforce.

A result of this has been the increased use of convenient sanitary products such as Always and Butterfly that are easy to find and reliable. According to the National Institute of Health, nearly 20% of women use menstrual pads in the country, while 66% still use traditional cotton cloth. While this number is low, the study noted it has risen from close to nothing at the turn of the century. And to cater to this need, Always was the dominant player in the market.

Until 2018 that is.

The turning point for Santex came with a trend all the way in Kenya.

Butterfly’s resurgence started far away. In 2018, the hashtag #myalwaysexperience started trending in Kenya, where many women took to the internet to share horror stories of infections Always

pads had been causing them. Soon after, P&G found itself in a controversy with accusations of selling subpar quality sanitary napkins in many third world countries.

A widely shared 1996 study from the Canadian Medical Association Journal highlighted 28 women who experienced vulvar itching, burning, and contact dermatitis after using Always pads. These symptoms disappeared for 26 when they stopped using the product, and seven reported recurrence upon reuse. Facing mounting evidence and public outcry in 2019, Always executives held closed-door meetings but largely maintained their denial, likely to avoid litigation. In response to criticism, Always Kenya claimed it had upgraded the quality of its PE films, though concerns remained. In a 2020 roundtable, activist Wanjiru Nguhi noted that the changes don’t address the core problem, particularly for women reliant on the lowest-priced options.

The experience was not limited to Kenya. In fact, women from all over the world began complaining about their experiences with Always pads. Pakistani women were experiencing something very similar and started considering switching brands. A number of women began posting in women-only facebook groups and the word began to spread. As women shared their stories, they also began suggesting alternatives. One name that came up again and again was Santex’s Butterfly. This was the beginning of something new for Butterfly.

Around the same time, Santex was also going through a change in leadership. As Santex’s Marketing Manager Dione Rodrigues-Almeida

explained to Profit in an earlier interview, “When Talha Rahman joined Santex in mid2018, the company had already undergone a change in leadership a few years earlier with a young, second generation director coming on-board.” Rahman, a nephew of the first generation of owners, brought a fresh perspective and a commitment to innovation that would prove transformational.

This was the perfect time for Santex to establish its position in the market, considering that Always pads had been facing strong backlash from the market, not just in Pakistan but from other developing countries, as well.

The foundation for Butterfly’s comeback was laid with a renewed focus on product innovation. While they did not lean into the controversy directly, their marketing did promote ideas such as comfort, breathability, and addressed many of the complaints people had with their usual products. Erum Anwar, Lead Corporate Communications and CSR at Santex explained, “We recognised that many women in Pakistan were struggling with challenges such as skin irritation, infections, and odor during their menstrual cycles. While breathable technology was already an established solution internationally, it wasn’t widely available locally.”

“We saw an opportunity to address these unmet needs by introducing this advanced feature, enabling women to manage their periods more comfortably and confidently. Since its launch, the technology has been well-received, with our napkins becoming a preferred choice for their superior comfort and reliability.”

This insight led to the launch of Butterfly Breathables in 2014, featuring microscopic backsheet technology that promotes breathability and helps prevent odor, rash, and bacteria buildup. The innovation addressed a critical market need and gave Butterfly a unique selling proposition.