25 The Al-Qadir Trust Case: How one transaction brought down Imran Khan and Bahria Town

27 Imperial Limited, a once proud sugar-plant, pitches an out-of-the-box solution to its woes

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Multiple banks miss financial reporting deadlines, raising alarm over sector’s health

By Ahtasam Ahmad

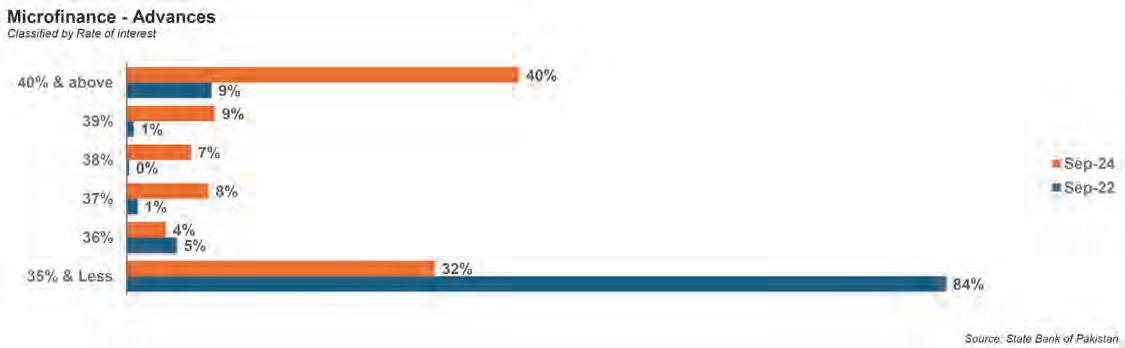

Pakistan’s quest for financial inclusion has taken a bold new turn with the State Bank’s latest National Financial Inclusion Strategy (NFIS) for 2024-2028. Yet this ambitious roadmap, aimed at bridging the gap with regional peers in financial services access, arrives at a peculiar moment - one where its primary vehicle, the microfinance sector, stands on increasingly shaky ground.

The numbers tell a troubling story. While the first half of 2024 saw microfinance banks’ deposit base grow by 6.7% to Rs. 637 billion, loan portfolios barely moved, inching up just 1.4% to Rs. 413.8 billion. More alarming is the sector’s infection ratio, which surged from 6.6% to 10.5% since the end of 2023. Losses have mounted to Rs. 12.1 billion, up from Rs.

8.1 billion, while the sector’s equity base has contracted sharply from Rs. 37.4 billion to Rs. 22.6 billion. Perhaps most concerning is the Capital Adequacy Ratio’s (CAR) fall to 5.7%well below the regulatory requirement of 15%.

This stark contrast - between ambitious policy and ground reality - raises a crucial question:

How did a sector meant to be the cornerstone of Pakistan’s financial inclusion journey end up in such dire straits? The answer lies in a complex web of factors, which we’ll unravel in this analysis.

How did we reach here?

The MFB sector’s current challenges run deep - deteriorating asset quality, mounting losses, and a weakened CAR. This trifecta of issues stems

from a chain of events: the COVID-19 pandemic in 2020, devastating floods in summer 2022, and the economic slowdown of 2023.

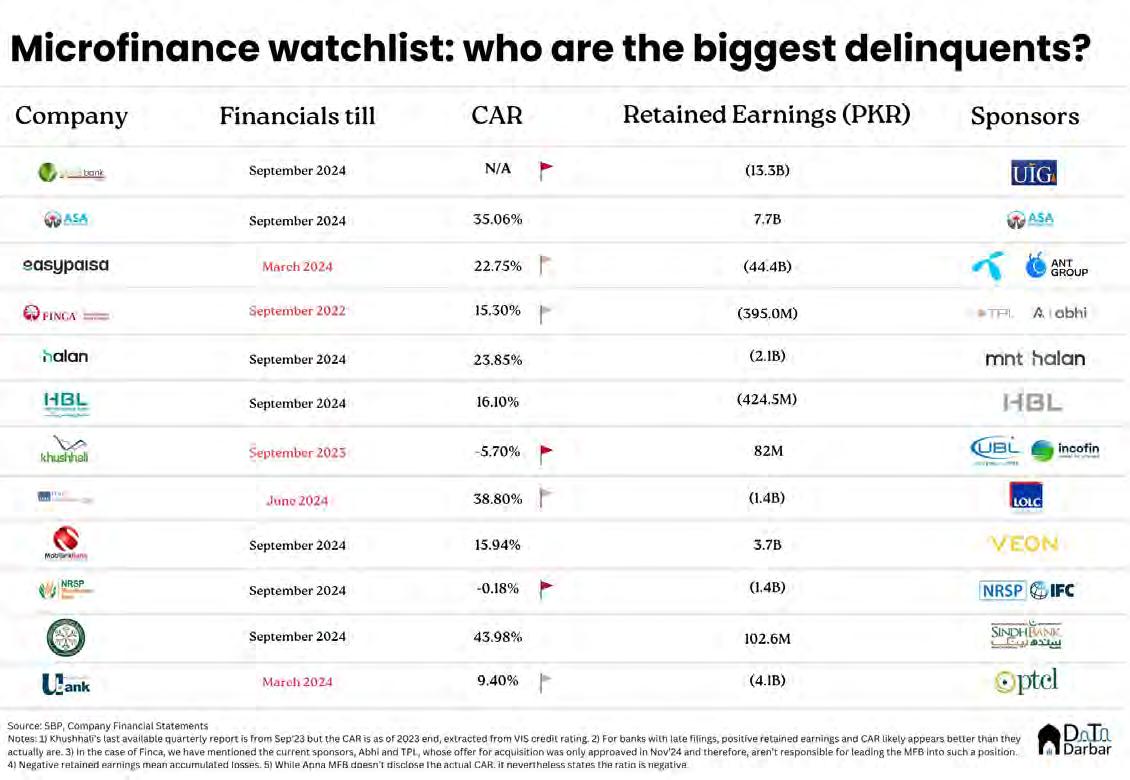

Currently, there are 12 MFBs in the country, with HBL Microfinance Bank, UBank, and Khushali Bank being the largest in terms of lending book size. The industry’s prominent sponsors include commercial banks, NGOs, and telecom operators, reflecting a diverse range of stakeholders.

MFBs have demonstrated significant progress over the past five years. The asset base of MFBs has shown robust growth, with an average year-on-year growth of around 19%. Equally impressive is the substantial increase in the gross loan portfolio, which has almost doubled from Rs. 214 billion in December 2019 to Rs. 423 billion in September 2024.

This growth is not just financial; it’s also reflected in the sector’s expanding reach.

The number of active borrowers has increased significantly, rising from 3.6 million to 7.5 million during the same period, but largely driven by nano loan customers.

Yet beneath these numbers lies a more complex story. The growth appeared stable until Covid, when it took an unexpected turn. In 2020, as banks grappled with the pandemic’s impact, the SBP offered a lifeline through loan rescheduling and rollover options. What

followed was an aggressive - perhaps overzealous - restructuring of portfolios, often exceeding genuine distress levels.

The 2022 floods triggered another wave of restructuring and rollovers, deepening existing issues. The economic distress of 2023 only added to the mounting pressure on portfolios. Throughout this period, banks, struggling with recoveries, repeatedly rolled over these portfolios, incorporating accrued

markup into principal at each rollover - effectively inflating their balance sheets.

The sector’s practices came under scrutiny when SBP began conducting audits in late 2022, signaling an end to regulatory forbearance. By end-2023, major players like Khushali Bank, Ubank, and NRSP were showing signs of serious strain.

The implementation of IFRS-9 in 2024 brought additional challenges, particularly

through its Expected Credit Loss (ECL) Model requirements for financial instruments. For loans, this meant periodic assessment of recoverability, with provisions required for potentially unrecoverable amounts. The model’s staging system categorizes credit risk, with restructured or repeatedly rolledover loans requiring higher provisions.

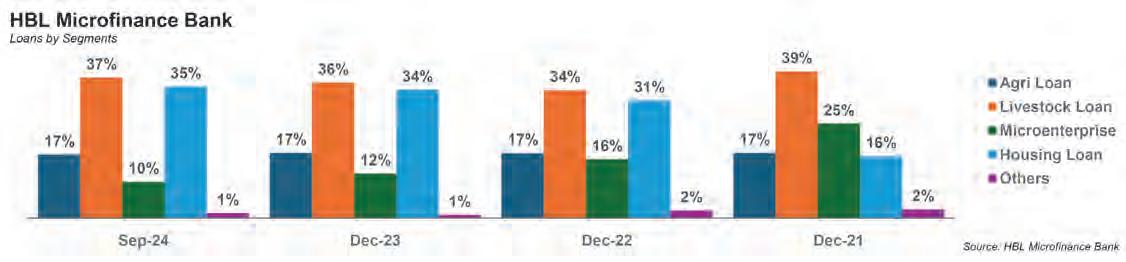

HBL Microfinance Bank’s experience illustrates these impacts: IFRS-9 implementation led to a 4x increase in provisioning expenses, reaching Rs. 5.4 billion. These factors, along with high-cost deposits and lower advances, resulted in a loss of Rs. 4 billion by third quarter 2024. To address this, the Bank issued Rs. 1.5 billion Tier-II subordinated debt to various investors, while the sponsor injected Rs. 6 billion in equity, raising the CAR to 16.1% by end Sep 24.

Adding to the sector’s challenges, rising interest rates dealt a severe blow to borrower affordability. With financing costs soaring, many borrowers found themselves unable to service their loans, triggering a cascade of defaults. This dynamic was particularly damaging for microfinance clients, who operate on thin margins and are especially vulnerable to increased borrowing costs.

State of play

The severity of these sector-wide challenges has caught the IMF’s attention. In its October 2024 review, the Fund explicitly warned about the sector’s systemic risk to Pakistan’s financial system. This warning, according to sources, has spurred the regulator into action, with efforts underway to resolve the capitalization crisis before the IMF’s next review in March.

The crisis runs so deep that multiple banks have skipped filing financial statements for several reporting periods. The apparent reason? The figures are so concerning that disclosure would damage the reputation of all stakeholders involved. Sources suggest these banks face serious financial challenges, prompting the regulator to push for either recapitalization or mergers.

Banks within the sector are charting di-

verse paths forward. There’s broad agreement that the era of unsecured lending is drawing to a close, with secured portfolios - particularly gold-backed lending - emerging as the preferred direction. Even if unsecured lending continues, microenterprise and agricultural sector financing appear unlikely to receive priority in the near term. HBL MFB’s pivot illustrates this shift: the bank has significantly expanded its housing finance portfolio, which grew from 16% in 2021 to 35% by September 2024.

Meanwhile, telco-backed institutions like Mobilink Microfinance Bank have fully embraced nano loans, which are projected to generate nearly 50% of the bank’s markup income in 2024, offering annualized returns of around 365%.

Among the hardest-hit institutions, Khushali and NRSP - both reporting negative CARs by end-2023 - have initiated contingency measures. While Khushali’s progress remains unclear due to lack of data since September 2023, NRSP shows signs of recovery. Its equity base expanded from Rs. 89 million in December 2022 to Rs. 2.0 billion by December 2023, further growing to Rs. 3.0 billion by September 2024. Though still challenged, NRSP’s CAR has improved from -6.02% in December 2023 to 0.05% by September 2024, with sources suggesting year-end figures might reach 2-3%.

Another institution in distress is Ubank. The telco-backed microfinance bank has missed two crucial reporting deadlines - June and September 2024. The bank’s last reported CAR stood at 9.4%, already well below the regulatory threshold, and industry observers suggest the situation has deteriorated further. However, with the bank’s continued silence on its financials, the full extent of its challenges remains obscured.

What’s next?

The current crisis appears to be accelerating industry consolidation, with mergers and acquisitions emerging as a key trend. FINCA’s recent acquisition, approved by the Competition Commission of Pakistan (CCP),

follows close on the heels of Advans MFB’s acquisition just nine months prior.

Industry sources indicate that the long-running cycle of portfolio rollovers has finally been curtailed, with recent equity injections expected to provide crucial buffers for impending write-offs. Yet the sector continues to grapple with fundamental issues, particularly in credit assessment. The current approach, heavily reliant on basic cashflow assessment techniques, is undermined by loan staff incompetence or bias.

A path to recovery exists, but stakeholders are clear: further capitalization hinges on a more conducive operating environment. While recent interest rate declines offer some relief, industry operators are looking for more substantial reforms. The State Bank seems to acknowledge this in its Financial Inclusion Strategy, proposing to bring the microfinance sector under the umbrella of the newly established National Credit Guarantee Company (NCGC).

However, challenges persist. The NCGC’s expected capitalization of $30 million appears insufficient to meet the microfinance sector’s ($1.5 billion loan book) credit guarantee needs, especially given the facility’s mandate to serve multiple sectors. The State Bank’s strategy suggests an alternative solution: leveraging multinational and donor agencies to recapitalize these credit guarantee institutions, particularly to fund SME focused microfinance loans.

While industry insiders point to aggressive portfolio expansion by banks’ business divisions as having distorted the sector’s original mission, the deeper issue lies in regulatory oversight. The State Bank’s delayed intervention allowed these practices to become entrenched, creating vulnerabilities that will take years to unwind. The unfortunate reality is that the core microfinance customer base has stagnated and the only growth being reported is through nano loans.

As the sector struggles to realign with its foundational purpose of financial inclusion, its ability to serve as the cornerstone of the central bank’s new inclusion strategy remains uncertain. n

How profitable is Islamic banking?

The perception of Islamic banking is that it takes advantage of people’s faith. How high are the industry’s profits, and where do they come from?

By Farooq Tirmizi

The record profitability of the Islamic banking sector is, by now, a wellknown fact and, besides raising accusations of hypocrisy and taking advantage of people’s religious faith, it has also provoked a policy response from the State Bank of Pakistan. But exactly where does the profitability of this sector come from, and how structural is it? Specifically, are the record profits at Islamic banks – which are undeniable – the result of rent-seeking behaviour on the part of the Islamic banking sector, or are they simply a cyclical rise in profitability that can come from a time of high interest rates?

In this story, we will attempt to answer these questions by comparing the profitability of Islamic banks to the industry as a whole, the bulk of which is still conventional, and examine the determinants of that profitability. What we will not do is comment on the religious foundations of Islamic finance. We are not religious scholars and will not pretend otherwise, nor insert ourselves in a debate in which we cannot offer informed comment.

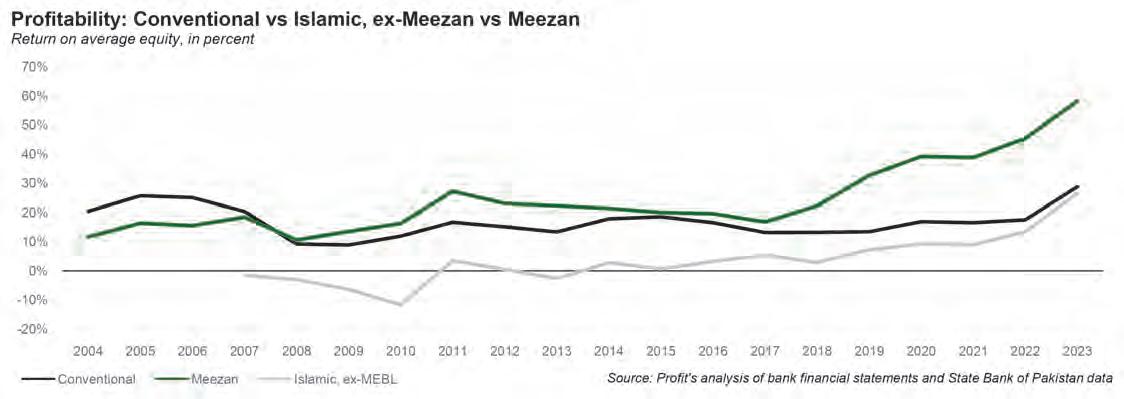

As always, we will dispense with the suspense up front: Profit’s analysis of the data from the banking sector suggests that while there appear to have been some regulatory advantages available to Islamic banks until recent changes, the industry’s profitability has less to do with that regulatory arbitrage and more to do with the fact that it is dominated by what is clearly one of Pakistan’s best run banks: Meezan Bank.

Here is the summary of our evidence for the above statement: remove Meezan Bank from the Islamic banking industry’s statistics, and then calculate their profitability and you will find that the Islamic banking sector, ex-Meezan, has underperformed the conventional banking sector in terms of return on equity for every single year for the past 15 years for which we can gather consistent data.

So what exactly is going on? Is the Islamic banking industry not a profit powerhouse for the banking sector as a whole? Aren’t all the major banks looking at Islamic banking as a major component of their expansion strategy, or at least were until the recent court rulings that require the entire industry to convert to Islamic banking? And would the entire industry converting to Islamic banking result in a more exploitative banking sector for their customers?

To answer these questions, we will go about our analysis in the following way:

1. Has the Islamic banking sector always been more profitable than the conventional banking sector, and if not, when did trends turn?

2. How much of the Islamic banking sector’s superior profitability has been due to the performance of Meezan Bank alone?

3. What are the determinants of the

sector’s higher profitability beyond just Meezan Bank?

4. What will the answers to all of the above questions mean for Pakistani banking customers when the entire industry is made to shift its model towards Islamic banking?

But first, a note on how we did this analysis.

Method of analysis (feel free to skip)

The core of this analysis is our attempt at a 5-step Dupont analysis on the Pakistani banking sector, broken out into its various components. Strictly speaking, a Dupont analysis on the banking sector is not normally done, since the Dupont analysis was developed for conventional companies, and banks have financial statements that are very different from ordinary companies.

For those unfamiliar, a Dupont analysis views return on equity as the most important measure of profitability for a company based on the logic that it represents the profitability as measured from the perspective of the owners of the company. It then disaggregates the components of return on equity to understand where the drivers of under or overperformance are coming from.

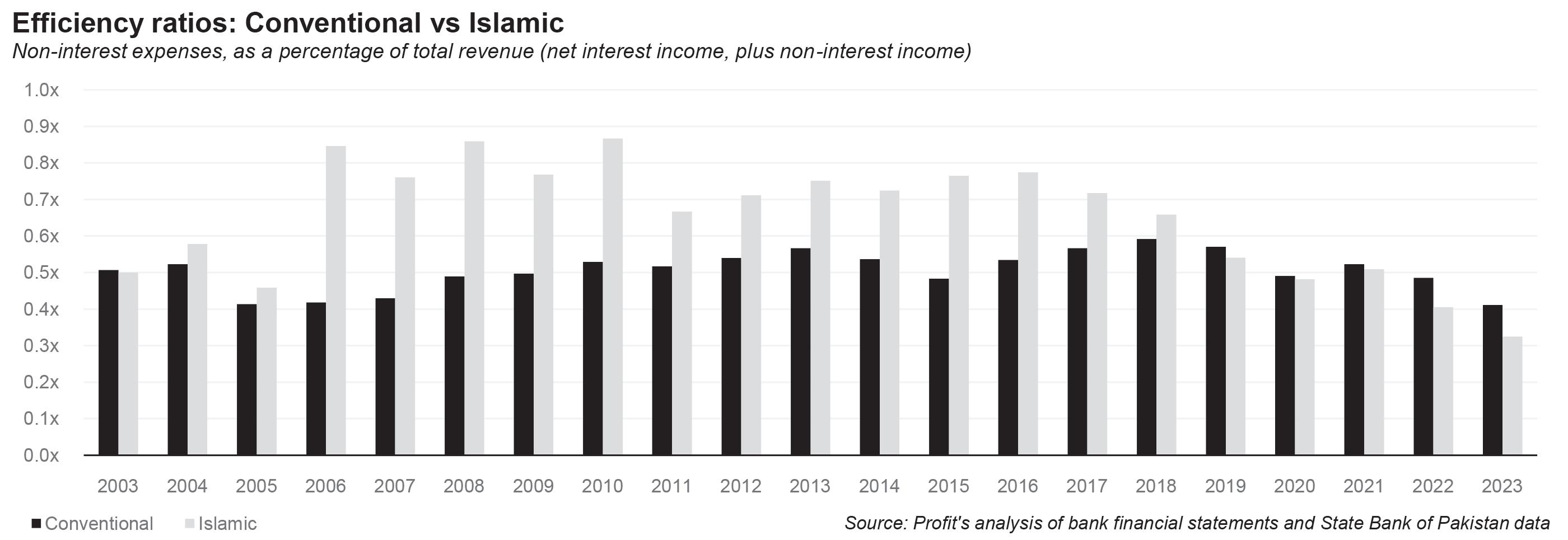

As we stated, since banks have very different financial statements, a strict Dupont analysis is not something we have been able to complete, though we have gotten somewhat close to it. We have compared return on equity, of course, since that is also the most important measure of profitability for banks. And while financial leverage operates differently in banks than it does in other companies, it is nonetheless useful to compare those in much the same way one would for a manufacturing company. We also looked at operating margin, though the metric we used is the efficiency ratio, which is the non-interest expenses for the bank divided by its total revenue (defined as net interest income and total non-interest income).

But instead of asset turnover, we have looked at net interest margin – and its components – since that is a more relevant metric for banks. Interest burden would not be a relevant metric since interest operates very differently for banks than it does for other companies. And given the fact that we are looking at companies in the same sector, we ignored the tax burden metric.

For each of these metrics, we examined financial data for the banking sector utilizing data from their financial statements – as well as from the State Bank of Pakistan. This data goes back to 2003 from some metrics, though not all of them were directly comparable.

For the Islamic banking sector, we utilized data for just the pure-play Islamic banks and did not include the banks that only recently converted to purely Islamic banking (such as Faysal Bank and Bank Makramah) to avoid the lumpy changes that came during the years these banks transitioned from conventional to Islamic. We compared these

data points to those of the banking sector as a whole, not just the conventional sector. A more thorough analysis would more completely separate conventional vs Islamic, but since the overwhelming majority of the banking sector is still conventional, it serves as a useful proxy for the conventional sector’s data.

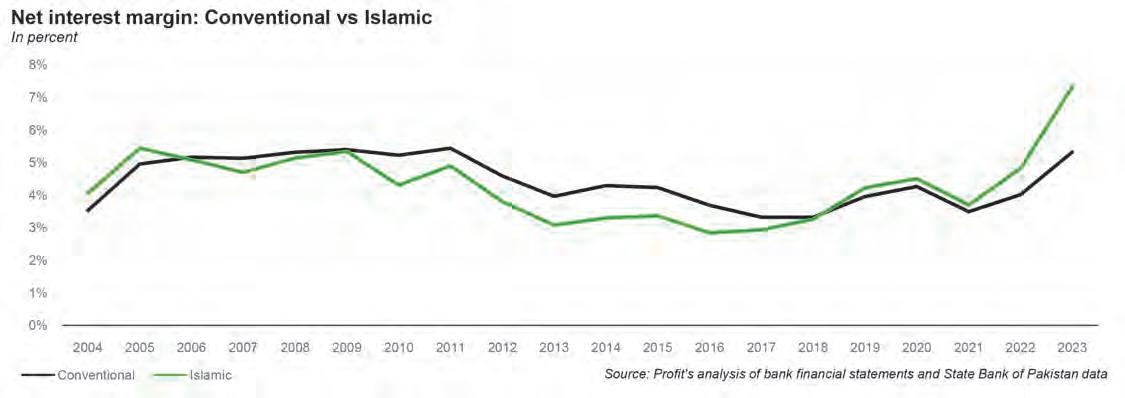

The Islamic banking profit boom is recent

One of the biggest critiques against the Islamic banking industry is that its profitability is the result of its ability to generate higher net interest margins than conventional banks because of regulations that limit the net interest margins for conventional banks but exempt Islamic banks from such limitations.

The rule in question is the minimum deposits rate (MDR) rule, which the State Bank of Pakistan implemented in 2008 towards the end of the Musharraf-era banking boom. Back then, the banks would offer very low interest rates on savings deposits almost regardless

of what the benchmark lending interest rates would be, allowing themselves to generate high net interest margins. The net interest margin is the difference between the interest rate that banks earn on their loans and the interest rate they pay out on deposits. It tends to be the largest component of any bank’s revenue.

The State Bank initially implemented a minimum interest rate of 5% on all savings accounts. The Islamic banks argued that Shariah compliance requirements would not permit them to offer a guaranteed rate of return on savings accounts. The State Bank relented and exempted Islamic banks from the MDR requirement.

The rule ended up not having much effect in the first five years of implementation. During that time, the benchmark SBP discount rate never went below 10%, which meant that a 5% minimum rate on savings accounts had a minimal impact. So in September 2013, the State Bank made the rule even more stringent, making them pay an interest rate that could only be 50 basis points below

the SBP Repo Rate (Interest Rate CorridorFloor), which in effect meant about 3% below the benchmark discount rate. Again, however, the Islamic banking sector was exempted from this requirement.

One would think that, if the MDR exemption was the main driving factor behind the industry’s outperformance, it would have had a near immediate impact on its profitability. But the fact remains that until the end of 2018, the conventional banking sector had a higher return on equity than the Islamic banking sector. In other words, for a full 10 years after the MDR regulations were introduced in a supposed disadvantage to conventional banks, the conventional banks continued to outperform the Islamic banks.

What changed in 2018 to cause the advantage to suddenly appear? More importantly, why did this exemption not have an effect in the first decade of its implementation. One can only conclude that the MDR regulatory loophole is, at best, an insufficient explanation for the recent boom in Islamic banking profits.

To profit from Islamic banking, be Meezan

To be clear, Meezan Bank started outperforming the conventional banking sector in 2008 and has had a higher return on equity than the industry average for every year since 2008. But one bank outperforming the conventional banking industry – and all the others collectively underperforming – seems far less like a compelling case for regulations explaining the divergence and more a case of one bank doing exceptionally well and the others struggling to catch up.

The dominance of Meezan is by this time a well documented fact. Despite a mass of competitors having jumped into the industry, Meezan still accounts for about 33% of Islamic banking deposits in Pakistan as of the end of 2023. More impressively, it accounts for 43% of the industry’s profits.

Of course, this dominance has been waning of late. While Meezan is still growing its deposits at a rapid clip, there are other Islamic banks that are growing faster, including MCB

Islamic Bank and Dubai Islamic Bank. But the scale and profitability of Meezan are clearly still a unique asset for the bank.

The charge against the Islamic banking industry is that they underpay returns to their depositors and take advantage of their religious faith, since many depositors for whom Islamic banking is important are willing to accept lower returns on their savings and other deposits in order to ensure that their money is in an institution that aligns with their beliefs.

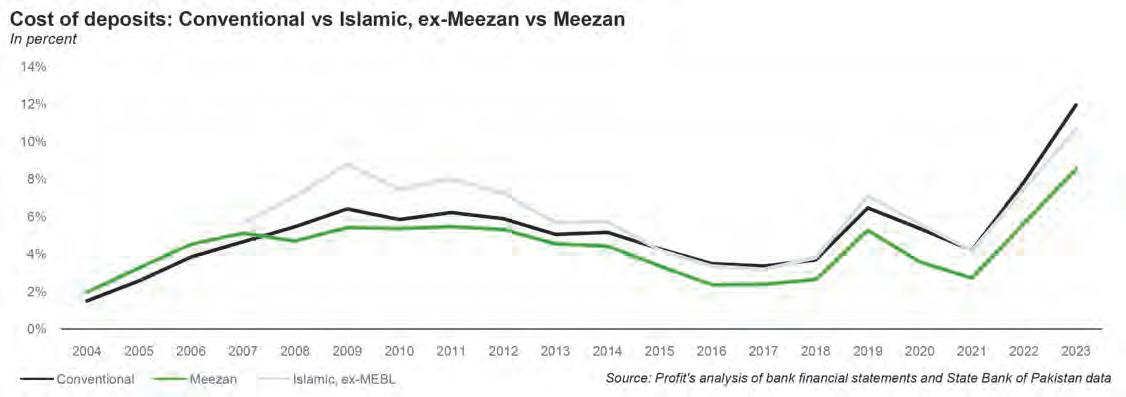

What needs to be understood is that this is true, but only for Meezan Bank. All other Islamic banks still need to compete for deposits by offering higher rates of return. As recently as 2021, the average cost of deposits at Islamic banks not named Meezan Bank was higher than that of conventional banks. The Islamic average is brought down below that of conventional banks by Meezan, which has a very high ratio of people with current accounts.

This is where the statistic we cited earlier comes in: in terms of both cost of deposits and return on equity, Meezan Bank has done better than the conventional banking sector,

but the Islamic banking sector has, for the most part, done worse than the conventional banking sector.

In other words, there is only one rule to earn higher-than-average profits from the Islamic banking sector in Pakistan: be Meezan Bank.

Determinants of profitability

Across most other measures of financial performance of banks, it is much the same story: Islamic banks do better than conventional banks, but only if you include Meezan. One metric where Meezan does worse than conventional banks is that it earns a lower rate of return on its lending activities compared to the interest earned by conventional banks on their lending books.

The principle in Pakistan’s Islamic banking sector is: you may be able to persuade the depositor to accept a lower rate of return, but you will also be able to command a lower

rate of return on your lending, because the borrowers know that you have more deposits than you know what to do with, and so they are at an advantage in any negotiation on the price of money.

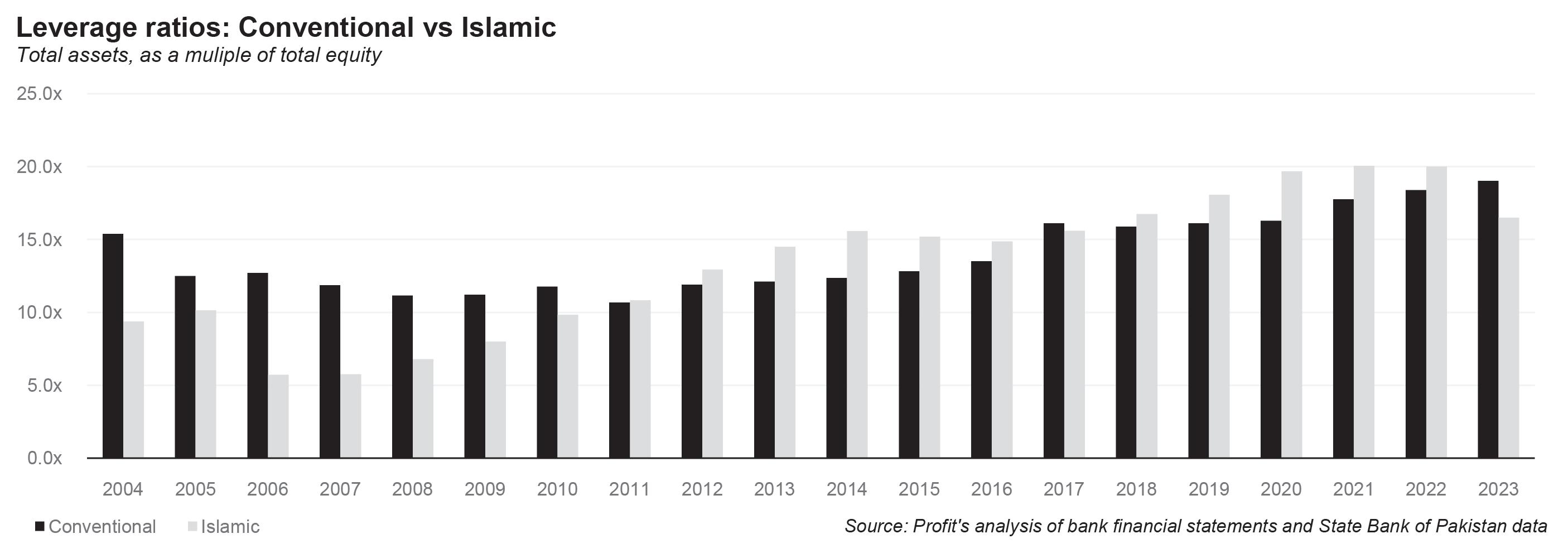

Another metric with somewhat surprising results: Islamic banks have historically been more leveraged than their conventional counterparts. This means that they tend to have less capital on their balance sheet relative to the loans that they give out. While this year Islamic banks are operating at a lower leverage ratio compared to conventional banks (assets at 16.5x equity compared to 19x for conventional banks), over the past decade, Islamic banks have averaged a leverage ratio of 17.2x equity compared to 15.8x for conventional banks.

One data point that could potentially be useful to measure if the data was readily available (but is not): the cost of running a conventional branch versus running and Islamic one.

Nonetheless, the broader result is clear: the Islamic banking industry – despite appearances – faces the same competitive pressures that conventional banks do, and Meezan Bank’s advantage in the industry appears to be not too dissimilar to the kind of advantage brand-name banks in mature markets have.

JPMorgan Chase Bank – the largest bank in the United States – offers far lower interest rates than most of its smaller competitors, because the people depositing their money at JPMorgan Chase want to do business with the bank famous for its “fortress balance sheet” and are willing to accept lower returns to do so. Meezan Bank is able to offer lower returns because people in Pakistan would like to deposit their money in Pakistan’s most wellknown Islamic bank and are willing to accept lower rates for the privilege.

Islamic banks also appear to have an inconsistent advantage with respect to conven-

tional banks with respect to non-performing loans. Some years, the Islamic banks do better than conventional banks, and some years it is the opposite.

What does this mean for the system-wide Shariah conversion?

All of this gives us a preview of what may come should the country’s entire financial services sector be converted to Islamic finance over the next few years.

The idea that Pakistan must abolish conventional banking has been a long-time coming. In April 2022, the Federal Shariat Court ruled that “riba” (interest) was prohibited in all forms and mandated Pakistan’s shift to an interest-free economy by December 2027. This ruling requires the removal of the term “interest” from all applicable legal clauses and necessitates amendments to relevant laws.

On January 21, 2024, Pakistan’s parliament passed a constitutional amendment bill stipulating that all forms of “riba” or interest must be eliminated before January 1, 2028. This amendment changes Article 38 (f) of Pakistan’s constitution, which previously called for the elimination of interest “as early as possible.”

The key thing to note is that the common misconception about Islamic banking – that it relies on its customers being willing to accept lower rates of return – turned out to not be true upon closer examination. Oddly enough, the evidence seems to suggest that despite laws explicitly allowing Islamic banks to offer lower returns than conventional banks, the actual rates offering to Islamic banking customers were determined not by that regulation but instead by the relative strength of the brand of each Islamic bank.

What this means is that when the banks

are made to move towards Islamic banking, the competitive dynamics that determine interest rates for both deposits and loans are unlikely to materially change.

There is nothing systematic about Islamic finance lowering the cost of borrowing, or lowering the rate of return being made available to fixed income security holders. It is entirely a function of the fact that since the industry is a small portion of the overall banking market in Pakistan, one well-run, dominant player appears to be skewing the stats on the industry as a whole.

That, in turn, means that Islamic banks are unlikely to be rent-seekers. This does not mean, of course, that there are not significant problems with the Islamic banking sector. It just means that there is nothing inherently worse or better about Islamic banking from a purely microeconomic perspective.

In short, the transition to Islamic banking in Pakistan is unlikely to fundamentally alter the competitive landscape or the core dynamics of the banking sector. The perception of Islamic banks’ superior profitability is largely driven by the exceptional performance of Meezan Bank, rather than systemic advantages inherent to Islamic banking.

As the entire sector shifts towards Islamic models, banks will continue to compete on familiar grounds such as service quality, technological innovation, and pricing. The regulatory changes, while significant in form, may not substantially change the substance of banking operations or customer experiences. Ultimately, the success of individual banks in this new landscape will depend on their ability to adapt, innovate, and efficiently meet customer needs, much as it does in the conventional banking sector.

The transition to Islamic banking, therefore, represents more of a change in packaging than a fundamental shift in the economic realities of banking in Pakistan. n

Does Pakistan need Starlink?

Can the Elon Musk backed venture disrupt Pakistan’s internet landscape as it has in other parts of the world?

By Hamza Aurangzeb

Decades ago when the cold war was at its peak, the US and the USSR were engaged in a gruelling space race, where each intended to sprint past the other to establish its technological superiority over the other. The competition led to some of the fastest advances in technology and infrastructure for space exploration in modern history. Back then, this race was driven by ideological reasons. It was a question of national pride and internal security.

Today, a new space race propelled by

profits and ambition has emerged. The commodification of space discovery was inevitable. What is interesting is how it has developed. A case in point is satellite internet service companies. The tech for this has been around for quite some time. In fact, the first company to acquire permission to transfer files through satellites in space was Hughesnet in 1993, barely a year after the dissolution of the Soviet Union. By 1996, the company had proven that downloading files through these satellites could drastically reduce download times.

But when the advent of commercial internet started rolling around all over the world at the end of the 20th century, most

internet service providers focused on using ground cables. Over time, all over the world, this has become the primary infrastructure for the internet. In fact, around 95% of the world’s communication is carried by cables, and the rest by satellites.

But there is agreement that satellites will likely be the future. Which is why the industry has seen some intense competition over the years. There are several internet service companies operating satellites all over the world. Some, such as One Web and Shanghai Spacecom, have expressed interest in operating in Pakistan. None are as famous or as well known as Starlink, the company owned and

operated by Elon Musk, the billionaire from South African who owns Tesla, X, and SpaceX among other enterprises, and is currently one of the most politically influential people in the United States.

Starlink is one of the many satellite internet service companies interested in Pakistan, None of them have gained regulatory approvals and licenses from the respective government bodies, thus far. But Starlink has emerged as the frontrunner in being granted all the necessary permits as it has been engaged in an active negotiation with the Government of Pakistan for a considerable time and its application process is ahead of the rest of the competition.

The question is, why is Starlink interested in Pakistan? Well, Pakistan is one of the many markets that these satellite internet providers are targeting. The developing world has a large appetite for the internet, and the introduction of reliable high speed internet can change a country and its economy. We have seen this in Pakistan as well, where high speed mobile broadband was introduced around 2010, and has in the decade-and-a-half since changed how we bank, do business, and run the economy. It has also been a major catalyst in Pakistan’s startup industry.

Companies like Starlink want to provide this internet infrastructure to developing countries. In fact, they have seen great success in a number of places. In Africa, Starlink is cheaper than most ISP providers that have on-ground infrastructure. However, this is the case for a region where there was essentially no existing internet infrastructure, or at least not an infrastructure that was affordable to the vast majority of people. Pakistan already has internet infrastructure. It also has relatively cheap internet. So what exactly will Starlink provide? Well, for starters, the government will no longer have control of our internet infrastructure to flick the switch whenever

they want. The question is, will that be enough of an incentive? Or is there something more to satellite internet?

SpaceX and Starlink

Space Exploration Technologies Corp., famously known as SpaceX, was founded in 2002 by Elon Musk with the ambitious goal of making space transportation more accessible and affordable, enabling the potential colonization of Mars. Over the years, SpaceX has revolutionized the aerospace industry with its groundbreaking innovations, including reusable rockets and successful missions to the International Space Station (ISS), which has indeed made space exploration accessible and sustainable while broadening the horizons of human achievements in space.

In the beginning of 2015, SpaceX publicly introduced Starlink, a project aimed at deploying a constellation of Low Earth Orbit satellites, which typically provides high-speed, low-latency internet globally, particularly in

Source: Starlink Progress Report 2024

remote and underserved regions with dearth of terrestrial coverage. Starlink, which is now a wholly owned subsidiary of SpaceX, represents a natural extension of SpaceX’s vision of connectivity and exploration, where it intends to provide high speed internet services through satellite not only to abridge the digital divide on Earth but also provide the capital to SpaceX that seeks to fund its broader space ambitions, including future missions to Mars.

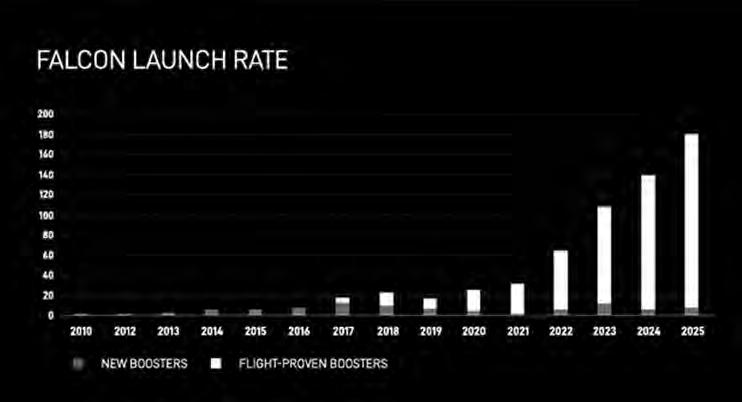

SpaceX and Starlink maintain a mutually supportive relationship, with SpaceX handling the design, production, and launch of Starlink satellites via its Falcon 9 rockets, ensuring affordability and rapid deployment.This integrated approach allows Starlink to benefit from SpaceX’s advancements in aerospace technology, such as reusable rockets that have significantly lowered launch costs. The largest portion of the launch cost is incurred during developing a rocket, which traditionally used to fly once until SpaceX arrived at the scene with their rockets. The ability of SpaceX to reuse Falcon’s first stage booster and payload fairings has proven to be a transformative disruption in the industry that has significantly diminished the cost of access to space.

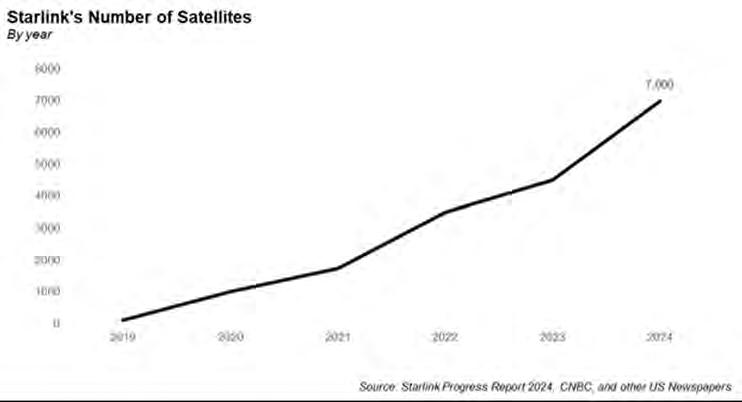

Space X launched the first batch of 60 Starlink satellites in May 2019, and since then Space X has concluded 439 Falcon-9 launches, positioning more than 7,000 Starlink satellites in orbit, where each launch contributes to the capacity of the constellation and enhances coverage, creating an ever more digitally inclusive planet for digitally starved communities in distant regions. Starlink is the most dominant player in the segment LEO-satellite based internet services across the globe, with its 7,000 LEO satellites, OneWeb is a distant second with 648 satellites, while Iridium holds the third spot with a measly portfolio of 66 satellites.

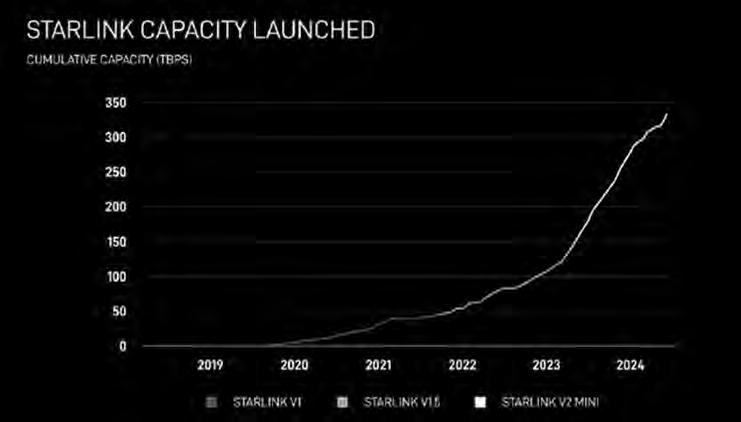

The new generation of Starlink’s satellites, Starlink V2 Mini equipped with Space X’s KA+E-band technology, are capable of

handling four times more data than their previous generations and communicate with each other through advanced laser beams compared to the previous generations of satellites. The futuristic configuration of V2 Mini satellites and acceleration in Falcon 9 launches together have augmented the total capacity of Starlink’s network to more than 300,000 Gbps.

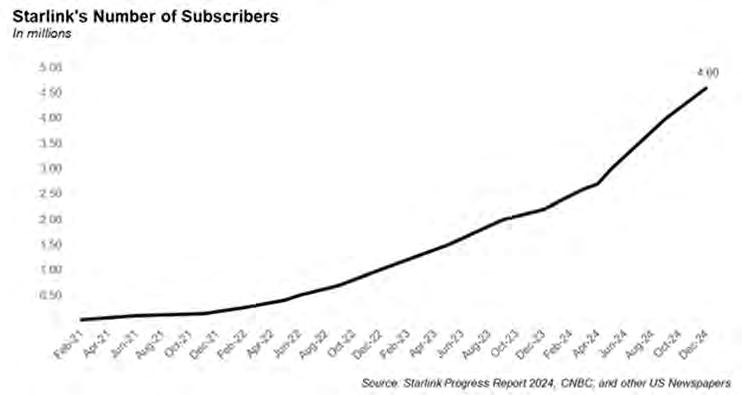

The technological advancements and capacity augmentation achieved by Starlink has enabled the company to accomplish a low latency of 26ms and download speeds of approximately 100 Mbps across its network. It has created a network that spans 118 countries and territories across seven continents, which is accessible to 2.8 billion people. Its user base has grown from an esoteric group of 10,000 in Feb 2021 to a global community of 4.6 million customers by Dec 2024, recording an annual growth rate of 220%.

How Does the Starlink System Work?

The Starlink system leverages a LEO satellite constellation, which consists of thousands of small satellites that work together to provide seamless and reliable coverage. Unlike traditional satellites, which are located in geostationary orbit, thousands of Kms away from Earth, Starlink’s satellites orbit much closer—at altitudes below 600 Kms. This proximity significantly reduces latency, allowing for a more responsive internet experience, especially when compared to traditional satellite internet. The sheer scale of Starlink’s network, with thousands of satellites working in tandem, ensures that users can maintain a connection at all times, even in the most remote and sparsely populated areas.

Starlink’s unique design and functionality allow for the rapid transmission of data through a combination of satellite commu-

Source: Starlink Progress Report 2024

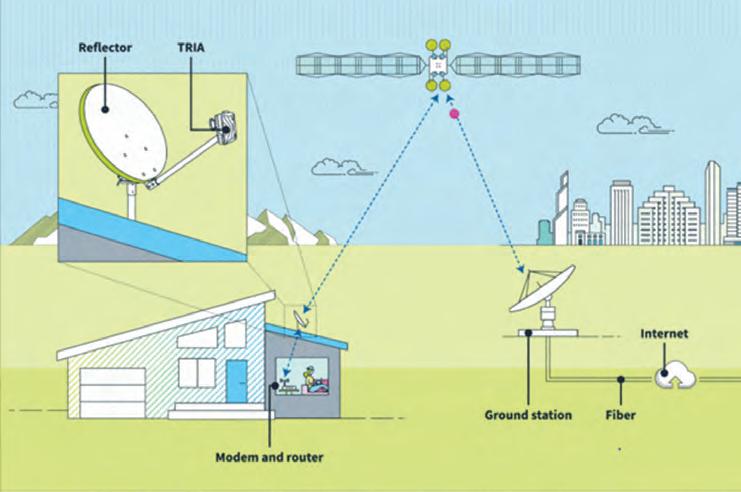

nication and ground-based stations. When a user connects to the internet, data travels from their device to a flat Starlink terminal which uses phased array antennas to relay data to the nearest satellite. The satellite, in turn, transmits the data to a Starlink ground station that is connected directly to the internet backbone through fibre optic infrastructure.

Starlink relies on a network of strategically placed ground stations that connect the satellite constellation to terrestrial internet infrastructure. These stations act as gateways between the satellites and the internet, ensuring the smooth flow of data. In case the satellite is unable to directly communicate with a gateway, they communicate with other satellites through inter-satellite communication links. The integration of inter-satellite communication links in V2 Mini satellites is one of the most important innovations within the Starlink system as it is not available in V1 and V1.5 satellites. This dynamic routing process occurs in real-time, optimizing performance based on satellite positions and user demand.

With this advanced system, Starlink not only provides high-speed internet access but does so with an unprecedented level of flexibility and reliability, even in places where traditional broadband infrastructure cannot reach. So for example, if an individual residing or a corporation mining in a remote region of Balochistan, where they have a Starlink Terminal but no ground station in the area, the users can send their data to a Starlink satellite through the terminal.

This data will then be passed on from satellite to satellite until it reaches the satellite which is connected to a ground station, which in turn is actually connected to the rest of the internet through fibre optic infrastructure. This minimizes the role of fibre optic infrastructure in treacherous terrains and bucolic regions. However, the Starlink network isn’t entirely independent of the fibre optic infrastructure because it needs fibre to connect its gateways to the internet backbone but its dependence is significantly less. Nevertheless, Starlink’s communication system of inter-satellite communication links is not full proof as not all satellites are capable of communicating through this method.

Charting its path to regulatory approval and licensing in Pakistan

Starlink’s plans to establish its presence and commence operations in Pakistan has generated considerable interest among the public and corporations alike. But how will Starlink operate in Pakistan? To start off, Starlink is going to have to deal with what is perhaps not its biggest challenge to date, but possibly its most frustrating: Pakistani bureaucracy.

Starlink has been actively negotiating with the Government of Pakistan and its

regulatory bodies for a while now and as a first step. It has successfully registered itself as a legal entity with the Securities and Exchange Commission of Pakistan (SECP), ensuring compliance with local corporate laws. However, Starlink must also adhere to the legal interception requirements mandated by the government that is indispensable for safeguarding national security.

Starlink provides internet services via satellites, since it is an unconventional medium in Pakistan—it must navigate approvals from three key regulatory bodies: the Pakistan Space Activities Regulatory Board (PSARB), the Frequency Allocation Board (FAB), and the Pakistan Telecommunication Authority (PTA).

The journey begins with securing a No-Objection Certificate (NOC) from PSARB, which governs activities in outer space and upper atmosphere; ensuring all foreign satellite operators are registered. This step is critical to align Starlink’s operations with Pakistan’s policies on space activities.

Next, Starlink must approach the FAB to obtain permission to use a specific frequency spectrum within Pakistan’s jurisdiction. This would ensure that Starlink’s operations do not interfere with the radio signals of other operators, maintaining orderly spectrum allocation and avoiding signal distortion.

Finally, Starlink will require two critical licenses from the PTA: the Long Distance and International (LDI) license and the Fixed Local Loop (FLL) license. The FDI license is essential for facilitating end to end communication between points that are located in Pakistan with points that are located outside of Pakistan, while the FLL license will allow the company to offer internet services and establish infrastructure, particularly in underserved regions where connectivity has historically been limited.

It is important to note that Pakistan has 14 defined telecom regions, and Starlink will need a separate FLL license for each region in which it plans to operate. This regulatory landscape presents challenges but also underscores the potential for Starlink to address connectivity gaps across the country. According to industry experts, it will take up to a year or more for Starlink to secure the necessary permits and begin commercial operations in Pakistan.

Who will use Starlink in Pakistan?

This is the other important question. Although Starlink’s mission is to provide access to high-speed internet throughout the globe, its primary target for the moment happens to be remote and underserved regions which lack dependable internet connectivity. Starlink with its standard residential plan provides internet at speeds up to 100 Mbps with unlimited data for

$50 a month, where an additional hardware cost of $389 is required to set up the terminal. However, they also have a residential lite plan, which offers unlimited deprioritized data at the same speed for $35 a month. This amount might be affordable for the rural population of developed countries but not for their Pakistani counterparts. Thus, it is highly unlikely that the majority of the customers in rural areas would be surfing the internet using Starlink’s services, if at all.

Our suspicion is Starlink will be able to establish a niche market in urban areas within Pakistan as it has placed its product at a competitive pricing, when it comes to 100-135 Mbps packages of major internet service providers in Pakistan. We compared the prices of all major internet service providers in Pakistan, and it seems Starlink has done the math.

Starlink’s Residential Lite plan will be cheaper than the average price of Pakistani residential 100-135 Mbps plans, which is $37.96. Moreover, although its standard residential plan, while not cheaper than the average, it is still competitively priced for people who intend to enjoy priority services.

Notwithstanding, Starlink will be competing with all the other internet service providers for customers who prefer premium services, while the average customer in urban areas will continue to opt for service plans of traditional internet service providers because one can get internet services for as low as $8 a month.

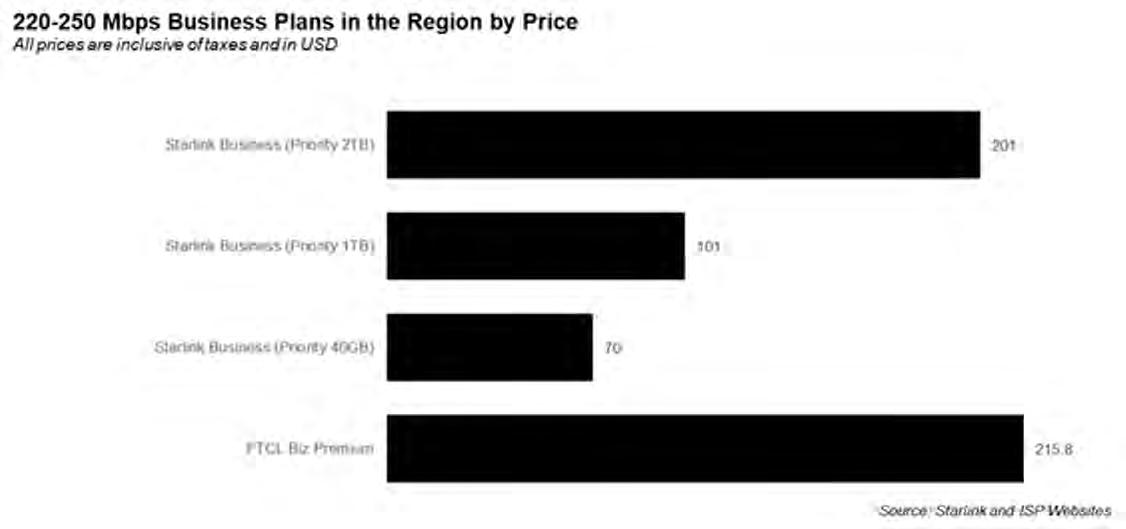

As far as the businesses in Pakistan are concerned, we believe that they would be much more enthusiastic and willing to transition to Starlink’s services. Starlink has three business plans which offer speeds up to 220 Mbps, starting at $70 a month that offer priority data of 40 GB, while the rest of the

two offer priority data of 1TB and 2TB for $101 and $201, respectively.

All three plans offer unlimited standard data, while the customer can purchase additional priority data by the GB. On the contrary, the main competitor of Starlink is the Pakistan Telecommunications Company Limited, which controls 85% of the Fixed Local Loop market and the most widely recognized one, which offers comparable speeds. PTCL’s premium business plan offers speeds up to 250 Mbps at $215.8 a month with a cap of 20TB data.

What about the telcos and other internet service providers?

There is a widespread notion that Starlink is a direct competitor of telcos and internet service providers, while that is the case to an extent but Starlink also complements existing telcos and internet service providers in Pakistan.

Starlink provides internet services both directly to customers and also acts as a backhaul service which offers wholesale internet access to Internet Service Providers (ISPs). ISPs can establish facilities in remote or rural areas using Starlink terminals and equipment or integrate their systems with Starlink gateways in urban areas and then act as distributors where they can distribute internet to retail customers in both urban and remote areas. This strategy of internet service providers will incentivize more and more customers to procure internet from ISPs which is backed by Starlink as the customers won’t have to bear the cost of hardware equipment. Moreover, a growing user base will persuade Starlink to decrease prices further in order to leverage

economies of scale.

Similarly, telcos which already procure wholesale internet access from backhaul services like PTCL can forge a partnership with Starlink to utilize their services through installing Starlink’s equipment on cellular towers and diversify their sources for accessing the internet. Telcos can also establish new cellular towers in rural areas and connect them to the internet through Starlink’s equipment. This approach would eliminate the need for establishing fibre optic infrastructure to connect these towers to the internet. While Starlink would be competing with PTCL in the backhaul space to enhance connectivity, particularly in far flung areas, it can’t function

independently of PTCL as it requires their fibre to connect their ground stations.

Telcos can also leverage Direct-to-Cell technology to expand their coverage and enhance service reliability, particularly in remote and underserved areas. Direct to Cell satellites employ eNodeB modems, which act as cellular towers in space. This enables telcos to integrate satellite connectivity into their networks and offer seamless mobile services like texting and lite data without requiring additional infrastructure, where voice calls would become possible eventually as well. This technology will allow telcos to ensure connectivity in disaster-hit regions, rural areas, and during network outages. Telcos can incorporate

Direct-to-Cell services into existing plans as a premium feature, attracting customers who value uninterrupted coverage.

The entry of Starlink brings in a whole spectrum of possibilities for the internet landscape in Pakistan, where it stands to usher in a new era in the country. Although Starlink might outcompete and diminish the influence of the competition in the future, for the time being it must cooperate with all the major stakeholders in the telco industry to fortify its place in the segment and develop a moat. Pakistan is heading into interesting times, with competition in the telco industry, particularly in the internet space poised to reach an entirely new level. n

OPINION

Qamar Nawaz

Rescuing Protein-istan?

There is simply one poor policy decision that caused destruction to everything around the dairy ecosystem in the last few decades, and that is the government’s obsession to control milk prices, rather than milk quality

Iremember vividly the scenario of our family farm three decades ago. We were an average sized farming family from Central Punjab, and our output back then is telling.

Let us start with some basic statistics. My grandfather would have, on average, three milking animals. On average, each one would yield eight liters of milk daily at 40 grams of protein per liter. That comes to 320 grams per animal and a total of 960 grams of protein on a daily basis. For a good-sized family of 10 family members, it would be almost 96 grams per member. The only dairy product we could sell was desi ghee, or the ‘fat’.

This meant all of the protein was left for ourselves. It would either be consumed either by the family or shared within our village as ‘lassi’, which came as a by-product of the ghee making process. Now imagine only half the population of our village as animal owners, which translates into approximately 50 grams of protein for each member of our village. Of course,

The author is a robotics engineer, food production entrepreneur with 15 years of experience, and a student of economics. His work explores agricultural economics, food value chains, global consumption trends, and policies affecting rural communities

the distribution was not exactly equitable, but the overall average for our fellow villagers was much more than the World Health Organization recommendations of at least 0.8 grams of protein per kg of body weight per day.

Any serious effort to understand ‘malnutrition’ in Pakistan must focus on the most critical macro nutrient: protein. Pakistan, except for some parts, was blessed to have a great source of high-quality protein. Up until the 1990s, an average Pakistani would have a lot higher muscle mass and taller stature than today’s youth. We may attribute it to many factors, but the consensus among health experts suggests nutrition as contributing around 80% to overall wellness. This means the unavailability of ‘affordable’ and quality protein has led to this visible and costly decline in public health.

We have badly failed to maintain the production of protein as our population has multiplied in recent decades. Our region has been inhabited by pastoral farmers for millennia. Even today, Pakistan has one of the highest animal head counts and remains a big player in milk production. Sadly, the production remains seriously suboptimal, and we import milk products around the globe to meet our local demand, even at historically low consumption levels. Imagine Pakistan imports dairy products from Saudi Arabia, that too at highly competitive rates.

One of the ‘mediocre narratitives’ being thrown around is labeling Pakistan as a place where ‘pure milk’ is not available. This is nothing more than ‘moral policing’ of an economic failure. Being a farmer producing milk commercially, it pains me to see both producers and consumers suffering from policies that are ‘poisonous’ for both these groups. There is simply one poor policy decision that caused destruction to everything around the dairy ecosystem in the last few decades, and that is the government’s obsession to control milk prices, rather than milk quality.

While the world controls and regulates quality, our state employees are paid to keep prices well under production costs. This literally translates to ‘incentivizing’ adulteration. Hence, a large number of middlemen operate to cash it. When adulteration is unchecked, farmers get prices at middleman’s diktat because free markets supply and demand are not applicable.

A farmer operating at such low margins would actually be making losses but would be unaware of this fact because he would not understand the opportunity cost for renting the same land to someone else. In recent years, modern dairy farming has been quite popular, with farmers making serious investments in importing animals and setting up advanced infrastructure, but the business feasibility remains a very tough one, with a very high percentage of closures. The only route to maintaining profits is the ‘ farm to table model’, wherein the farmers take control of the post production supply chain and target affluent classes to get the right price of their product. This is done by packaging the milk

to bypass government regulation of prices. This creates a parallel regulation regime, keeping the majority of producers in miserable conditions.

Except for the routine media reports regarding discarding of adulterated milk, no serious effort is being done to actually ensure that only pure milk reaches the consumer. Pakistan’s Diabetic Incidence rate is second only to a small city state of Kuwait, with nearly 30% of Pakistanis above 30 years being stricken by this metabolic catastrophe. Such humungous numbers cannot be catered by our healthcare system, nor can these chronic patients be considered productive members for the economy in the longer term. In the absence of affordable protein, we tend to consume calories from unhealthy sources like fats, carbs or sugars,

which have led us to this pandemic.

The latest understanding among health professionals requires high muscle mass in young age to be maintained until later in life, as a guard against such metabolic disorders, which means intake of sufficient high quality protein food, like milk. Controlling adulteration would certainly breathe life into our giant dairy sector. The rural economy has enough dairy infrastructures to respond to any incentive, attracting more investments, creating employment opportunities and bringing efficiency, leading to competitive prices in the long run. As someone who has worked as a farmer and observed dairy business models around the globe, I believe we can produce high quality milk at globally competitive prices leading to surplus production for all kinds of

value additions.

Pakistan’s livestock sector is nearly 12% of our GDP, where dairy is the most significant sub sector, with the potential to revolutionize the rural economy. Our policy makers need to understand that the only route to creating exportable surpluses is to allow producers to become competitive in a free market. Our dairy sector has the potential to attract billions of investments, employ hundreds of thousands, and usher a white revolution. It’s a very low hanging fruit, only if the government can commit to just two measures, adulteration of milk be criminalized as a serious offense AND price controls be abolished. Otherwise, the present decay will continue and an undernourished, protein-deficient nation’s fate is not difficult to predict. n

The Al-Qadir Trust Case:

How one transaction brought down Imran Khan and Bahria Town

The strongest legal challenge Imran Khan faces, the Al-Qadir Trust Case has landed him and his wife 14 and 7 year jail terms respectively. The case also proved the downfall of Bahria Town

By Abdullah Niazi

Former prime minister Imran Khan has been convicted in the Al-Qadir Trust Case, with an accountability court handing him a 14-year jail sentence at the end of a trial that has lasted nearly two

years. The sentence also convicted the former premier’s wife, Bushra Bibi, handing down a seven-year jail sentence to her.

The Al-Qadir Trust case has been the largest and most pivotal legal challenge the former prime minister has had to face since being ousted from office in 2022. It has been a sprawling investigation that has embroiled

among others Bahria Town founder Malik Riaz, the Supreme Court’s dam fund, and members of Khan’s former cabinet. In the two years since it appeared as a prominent legal threat, the case has become the reason not just for Imran Khan’s initial arrest in May 2023, which then led to the events of 9th May, it has also brought the once mighty Bahria Town to

the brink of default.

But what exactly are the details of the Al-Qadir Trust Case? To put it mildly the case is perhaps one of the most clouded and murky webs from the Imran Khan administration. It involves accusations of bribery, corruption, and kickbacks against the Khan administration, and all of these claims go back to a single transaction that took place in 2019.

Ripples from the UK

In 2019, the National Crime Agency (NCA) of the United Kingdom agreed to a settlement worth £190 million with the family of property tycoon Malik Riaz. The settlement was the largest ever in the history of the NCA, and since it was out of court, came with the stipulation that it did not “represent a finding of guilt”.

To understand this, the NCA is a national law enforcement agency in the UK that investigates money laundering and illicit finances derived from criminal activity in the UK and abroad. If the NCA is investigating a case outside of the UK, it returns the stolen money to the affected state. So if the agency is investigating fraud or money laundering in Pakistan, it will prosecute or make a settlement in the UK and return the money to the Pakistani government. That is what happened in the case of Malik Riaz. His family had been under a ‘dirty money’ NCA investigation for a while, which reached its conclusion with Malik Riaz paying £190 million to the NCA. This money was then supposed to be sent to the Pakistan government.

However, the matter gets murky with the entrance of Special Assistant to the Prime Minister on Accountability Shahzad Akbar. On Dec 5, 2019, Mr Akbar announced at a press conference in Islamabad that £140m had been repatriated to Pakistan.

But there was a problem. This money had not gone back to the federal government. Instead, the money had been transferred directly into the account of the Supreme Court. But why would the money go to the SC?

Well, 2019 was the same year that Bahria Town was in some serious trouble. This was the year the company was subject to a decision of the Supreme Court of Pakistan that fined it Rs 460 billion. To cut a very long story short, Bahria Town had acquired land from the Malir Development Authority for its superhighway project in Karachi. That land, originally owned by the Sindh government, was declared illegally acquired. In March 2019, the court accepted Bahria Town Karachi’s Rs 460 billion offer for the lands it occupies in the Malir district of Karachi and restrained the National Accountability Bureau (NAB) from filing references against it.

Bahria Town would have to make the

payments over the course of seven-and-a-halfyears. They would have to pay Rs 25 billion by August 2019, followed by monthly installments of Rs 2.25 billion for the next three years. If they failed to make the payments for two months straight, the company would be considered a defaulter.

At the same time, the NCA also ordered Bahria Town to pay them £190 million. Bahria Town paid the NCA, but they did not have the liquidity to pay the Supreme Court. This is where the problem starts. When the NCA repatriated the money back to Pakistan, it was deposited in the account designated by the SC for the payment Bahria Town was supposed to make in the transfer of land case regarding Bahria Town Karachi.

The direct transfer of the £140m into the special SC account raised alarm bells since it basically meant that the money Malik Riaz had paid to the NCA which was supposed to come back to Pakistan had simply gone back to Malik Riaz. This was particularly crucial since Bahria Town faced the threat of default if it had not paid the fine the SC had imposed.

The government’s involvement

This leaves us with a pretty simple question. Why would the Imran Khan government give Malik Riaz his money back? The answer, as claimed by the case against Khan and his wife, is kickbacks. Particularly kickbacks regarding the Al-Qadir Trust.

The case alleges mran Khan and his wife Bushra Bibi of accepting billions in cash and hundreds of kanals of land from Bahria Town in return for the help that Khan’s government gave to Riaz during his investigation by the NCA. Interior minister Rana Sanaullah claimed that Bahria Town entered an agreement and gave a 458-kanal land with an on-paper value of Rs 530 million to a trust owned by Imran Khan and Bushra Bibi. The land was donated to Al-Qadir Trust, and the agreement bore signatures of the real estate’s donors and Bushra Bibi.

The then PDM government claimed that Imran’s aide Shehzad Akbar had “settled” the entire case, while the Rs 50 billion-which belonged to the national treasury-was adjusted against Bahria Town’s liability. He said Imran had received a graft of Rs 5 billion as “his share” through Akbar before the case was wrapped. He further said that Bahria Town, after its Rs 50 billion was protected by the then PTI government, had allotted 458 Kanal land with an on-paper value of Rs 530 million to a trust owned by Imran and his wife. He further said that another 240 Kanals were transferred to “Farah Shehzadi” commonly known as Farah Gogi — a close friend of Bushra Bibi.

It is these 458-kanals that have now come under the scrutiny of the accountability bureau. During the case proceedings, a bombshell revelation was made when a prosecution witness claimed during their testimony that the son of property tycoon Malik Riaz, Ali Riaz Malik, bought land for Farah Shahzadi in Bani Gali. Farah Shahzadi is a known associate of former first lady Bushra Bibi and has been linked in the case as well. According to the details provided by the witness, who is a patwari of Circle Mohra Noor (Banigala), claimed that nearly 245 Kanals of land in Bani Gala had been transferred in the name of Farah Shahzadi at a declared cost of Rs 53.28 crores.

The witness came armed with fourteen mutations that showed the different phases in which the land was transferred. The words of the testimony, as reported by Dawn, said “the land measuring 100 kanals, one marla was transferred in the name of Farhat Shahzadi against the consideration of Rs25 crores and 1 lakh 25,000, while the land measuring 100 kanals, five marlas was transferred in the name of Farhat Shahzadi for the consideration of Rs 25 crore, 6 lakhs and 25000, while the land measuring 40 kanals was transferred in the name of Farhat Shahzadi for the consideration of Rs 3.2 crores.”

At the same time, the witness also clarified that there seemed to be no direct involvement of former prime minister Imran Khan and his wife Bushra Bibi, since “as per record, the names of accused Imran Ahmed Khan Niazi and Bushra Imran are not mentioned there as witnesses or in any manner whatsoever”

Meanwhile, things were getting bad for Bahria Town as well. The accountability court froze the properties of property tycoon Malik Riaz and his son. Rumors started circulating that Bahria Town properties were falling in value and the organisation was undertaking layoffs.

The conviction

The judgement in the case had been made a while ago, but the conviction was repeatedly delayed. While the conviction was being delayed, the government was engaging in negotiations with the PTI. Following his arrest, the PTI has gained much popular support, as seen in the recent general elections, and many of the party’s leaders allege the timing of the case is politically motivated.

The Al-Qadir Trust case is far from the only case Khan is implicated in. While appeals courts have given him relief in a number of these cases, the Al-Qadir Trust Case was the strongest and most threatening legal challenge for the former prime minister. The PTI has promised to fight the conviction, however the new jail term adds pressure to ongoing negotiations with the PTI. n

Imperial Limited,

a once proud sugar-plant, pitches an out-of-the-box

solution to its woes

The company is hedging its bets on success of its hydroponic plant as a last throw of the dice. Will it work out for them?

By Zain Naeem

An eerie silence remains suspended over Phalia and Mian Channu. In the background, massive grey structures loom large, their silence telling a story words could not. In this small section of rural Punjab, the slow, crackling sounds of sugarcane being pressed and the hum of machines that once worked overtime has not been heard in some years.

The sugar plants, once a bustling part of the landscape, have not crushed a single reed of sugar cane in more than a decade. The reality

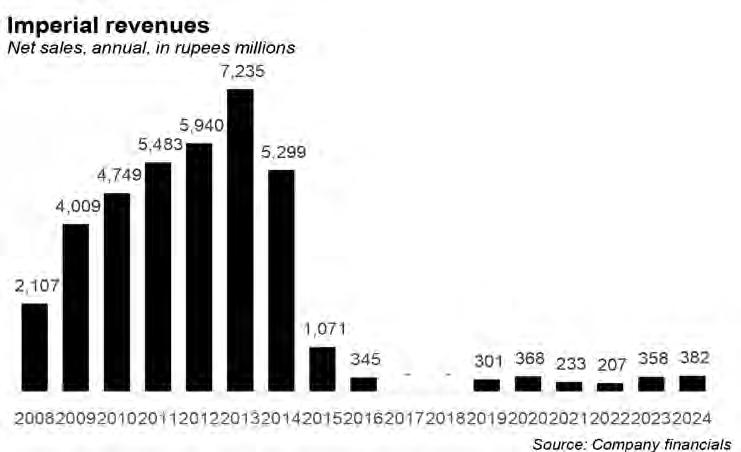

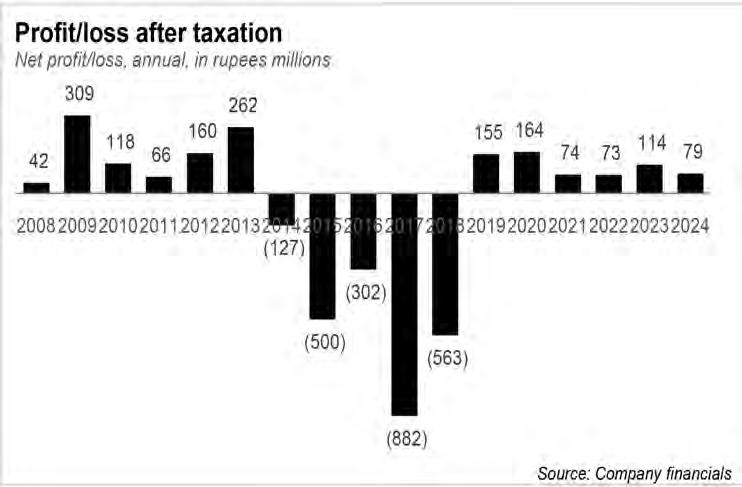

seems even starker when it is considered that the plant was set up less than two decades ago. Established in 2007, Imperial Limited used to be called Colony Sugar and Imperial Sugar in the previous iterations before the new name was finalized. From the very beginning, the company was marred in terms of its performance. It registered a profit of Rs 4 crores in its first year before turning into consistent losses since 2014. The initial problem was the fact the cost of production was too high which restricted profits from being earned.

As losses became the norm, the management decided to shut down production at the end of 2014. Since then, the management has

tried to find new avenues of production and revenue generation. First of all, the company put up its plant for sale in order to recover some of its investment back. The funds which were being raised were invested in mutual funds which could generate returns for the investors and Imperial itself. Proactive measures were taken to find business opportunities which could be capitalized on. Two paths were charted out. One was to invest in real estate where land would be bought and developed into residential projects. This decision was taken based on the wave of investment taking place in the real estate sector in Lahore. With mixed results, this decision has failed to take

off as the property market faced a slump.

The other route which was taken was to develop a hydroponic business by carrying out vertical farming to grow vegetables in an efficient manner. This project faced hiccups as it was being developed and took four years to come to fruition. Imperial has recently announced that the infrastructure has finally been completed and the first seeding would be carried out in February with the first harvest expected in May. Could this be the catalyst for the company to become profitable yet again?

History of Imperial Limited

In 2007, the management at Colony group of companies decided to enter the sugar manufacturing industry. In Pakistan, business groups have certain traditional industries that they are willing to expand into. Sugar manufacturing is considered one such industry where the raw material, sugar cane, is sourced from local farmers and there is a constant demand for the final product. The small grain of a sugar crystal acts as a prism for the expansion in revenue and profits earned. Due to the stability and certainty, Colony group also entered the saturated industry by establishing its own plant in 2007 as Colony Sugar Mills.

Looking at the revenues earned, it could be said that the mill was able to rationalize the investment. In its first year, the plant was able to earn revenues of Rs 2 billion which grew to Rs 7 billion by the end of 2013. The growth seen in the revenues was not translated into higher profitability, however, as gross profits earned by the company went from Rs 67 crores in 2008 to Rs 62 crores in 2013. If the profits had increased in lock step with the revenues, they should have been around Rs 2 billion.

The reason for losses being made was based on rising costs as the sugar manufacturer saw their gross margin fall from 32% in 2008 to less than 9% in 2013. Even as far back as 2009, the company had recognized that it was purchasing sugar cane at high prices in order to make sure they could keep operating the plant. They were expecting a similar increase in selling price of sugar which would maintain the margins that the company was earning in 2008. Over time, the selling price did not respond and cost of production kept increasing leading to lower gross margins.

The cost of production for a sugar facility is dependent on the price of sugar cane at which the farmer sells his produce to the manufacturer. Punjab and KPK have mandated that the support price, paid to the farmer, is to be set by the provincial government. In addition to that, the selling price of sugar is also regulated to an extent at the district level which means that manufacturers have little control

The sugar business

Much like many other industries in the country, partition meant a new beginning. In August 1947, there were only two sugar factories in the newly minted state of Pakistan. Most of the sugar mills set up in the colonial era were on the Indian side of the border, and the two in Pakistan were not nearly enough to meet domestic supply.

This was an opportunity. For the first few years of the country’s existence sugar had to be imported which was a major drain on a new state with very little trading power. At the same time, sugar was a high-demand commodity in the subcontinent and plenty of sugarcane was grown in the new state. The 1947-48 production numbers for sugarcane in Pakistan were over 54 lakh tonnes. Nearly 75% of this sugarcane was grown in the Punjab. Since at the time the country’s landed elite were also its political elite, it became clear that many of these landowners that were growing sugarcane would now set up sugar mills, process the sugar and make more money.

The experiment was successful. Keeping in view the importance of the sugar industry, the government setup a commission in 1957 to frame a scheme for the development of the sugar industry. In this way the first mill was established at Tando Muhammad Khan in Sindh province in the year 1961. By 1962 there were six mills in the country and in 1964 the Pakistan Sugar Mills Association (PSMA) had been established and almost every single sugar mill in the country had a member of parliament on its board of directors.

The interests of the sugar industry were disproportionately represented in the legislature and the political patronage that came with this allowed the industry to boom. According to a report of the Competition Commission of Pakistan, the number of mills increased to 20 by 1971 during a period when cane cultivation was incentivized in Sindh through establishment of sugar mills. The size of the industry further increased to 34 by 1980.

But by this point mills were facing a problem. Pakistan’s sugarcane was uncom-

over the cost and revenues they generate. Facing these barriers, companies have to pay out a floor price on their cost of production while their revenues are locked with a ceiling on top. These manufacturers have to operate within a thin margin and expect to turn a profit when the conditions of business can change from one year to the next based on the crop yield and the prices set by the government.

petitive. Production was low compared to the global average yields and so was sugar extract percentage. This meant imported sugar could actually compete with the local product. To counter this, government policies placed tariffs on imported sugar and even banned it while giving subsidies to local sugar mills. As a result, the number of mills grew and so did the number of farmers growing sugarcane.

In fact, the number of mills grew at such a rate that the government eventually had to stop giving licences because of capacity maximisation issues. Through political patronage and protection through tariff and non-tariff restrictions on imports and generous subsidies, Pakistan went from 41 mills in 1987 to 91 by the mid-2000s before a ban was placed on the establishment of new factories due to excess installed capacity.

During this era in particular the Sharif family was prominent in entering the sugar mill business. They started with the Ramzan Sugar Mills and continued on to establish Ittefaq Mills and many others. There was a crucial difference however. In the beginning, many of the mill owners had also been farmers. The Sharifs were hard-boiled industrialists with not a single green thumb in the entire family. This was also part of a rising trend of non-agriculturalists with political clout entering the country’s sugar industry. If one were to believe what was said in those days, the annual profit from one sugar unit in that period used to be more than enough for setting up a new one.

Up until the early 2000s there was no restriction on establishing a new sugar mill. However, around 2005 the government of Punjab decided that new mills could not legally be established. One reason for this was that a lot of the mills coming up were being set up in South Punjab near Muzaffargarh. This was a major part of Pakistan’s cotton belt — which the country’s largest export oriented sector, textiles, relied heavily on. This essentially froze the sugar industry, leaving it entirely in the hands of around 40 individuals and their families.

Another factor that handicaps the industry is the fact that sugar cannot be exported without the approval by the government. If a manufacturer feels local prices are too low, they can export their production at a higher price and sell to the foreign market. The government does not allow the industry to export as they feel that decreased supply in the local market will push the price of sugar upwards in

the country. In order to make sure ample supply is available, exports have to be approved. The populist approach of the government limits the revenue and costs that are faced by the industry. Limiting exports also places an obstacle in terms of sales volume. This virtually ties the hands of the sugar manufacturer who has little say or control over either.

Colony fell foul of this as they faced rising production costs and low selling prices. In addition to that, as the production of the company was low, the Phalia plant was left non operational which created an increased burden on the financial performance. The plant had to be shut down as the company was facing restricted access to working capital. The impact of the policies and the market dynamics can be seen in the financial performance from 2008 to 2013. In 2008, Colony Sugar made sales of Rs 2.1 billion generating gross profit of Rs 67 crores and net profit of Rs 4 crores. Over the next 5 years, the revenue of the company increased to Rs 7.2 billion, however, gross profits actually fell to Rs 62 crores and net profits were registered around Rs 26 crores. Even though profits were falling, the financial health of the company was not impacted as profits were still being earned.

The company could only resist the reckoning that was coming for so long as 2014 and 2015 proved to be the proverbial shoe dropping. In 2014, revenues of Rs 5.3 billion were realized, however, the cost of production increase meant that the company earned a gross profit of only Rs 25 crores. Gross profit margin had fallen to its lowest level of 4.7% in its history. The mill saw its first loss of Rs 13 crores and it was an omen for the future to come. Seeing the writing on the wall, it was decided to shut down production completely. As production halted, 2015 and 2016 saw sales of Rs 1 billion and Rs 34 crore respectively. The gross profits of 2014 became gross loss of Rs 9 crores in 2015 and net losses totalled around Rs 50 crores. The fate of the plant was sealed for the sugar business.

As its principal activity came to a halt, the management tried to look for new business opportunities. With loans of around Rs 2 billion, the company felt that the assets could be diverted towards new business ventures in order to generate a profit for its shareholders, management and creditors. As a vote of confidence, sponsors of the company also committed to lend to the company to put their money where their mouths were. The name of the company was also changed from Colony Sugar Mills to Imperial Sugar Mills in May of 2015. Lastly, a decision was also taken to sell the closed down factory to the highest bidder which would generate the funds that can be used to finance the new projects under consideration.

As new projects were being contemplated, the management made the decision to use the funds raised through asset sale and invest them in different short term investments which could generate a considerable return. This meant that, even though the plants were closed, the company was able to earn income from other sources. This was able to dampen some of the losses, however, losses of Rs 30 crores, Rs 88 crores and Rs 56 crores were made from 2016 to 2018 respectively. From 2019 onwards, these investments were actually able to return a profit as the company became profitable again.

Charting a new path

During the period of inactivity, the management did not sit idle. New business proposals were being sought. There were plans to establish an Independent Power Producer (IPP) project of 225 MW with the use of Liquified Natural Gas after regulatory approval. The proceeds of asset sales were going to be used in order to set up the new project. As the government failed to approve the IPP project, an alternative business plan was drawn up. The company was now going to get involved in real estate and corporate farming in order to resurrect the company. According to the business plan, a state-of-the-art hydroponics project would be set up with 17 greenhouses and a commercial nursery. The goal of the project would be to produce high quality vegetables for local and international markets and to capture a large market share as this was an industry with few participants in it.

Another project was also presented where real estate development would be carried out by making 60 residential units in Lahore. Land would be bought and residential projects would be developed which would be

sold for a profit which would be distributed to the shareholders. As the sugar business was slowly being taken apart, the name did not seem to fit any longer and Imperial sugar was renamed to Imperial Limited in 2020.

In terms of success, the real estate development business saw mixed results. After the properties had been developed, the real estate industry experienced a downturn as demand fell. This meant that as the properties came for sale, there was little interest in the market and the turnover of the property was low. Seeing lower than expected profits, the company is now pitching its wagon to the hydroponic bandwagon in order to resuscitate the company.

Imperial has carried out extensive research and analysis in relation to its hydroponics project. The machinery and infrastructure needed to set up the project has been imported from China and most of the deployment of the plant has already taken place. The sales proceeds generated from the sale of the sugar plant have been used to fund this project. The plant was supposed to go live in 2022 and then in 2023, however, there were different hurdles that were seen. A Chinese delegation of experts had to visit the country in order to help in setting up the facility and train the local labour force to be able to make it operational. The government wanted the company to employ security for the Chinese staff and get approvals from the Home Department before they could be allowed to come to the country. Due to the bureaucratic red tape, the plant was being delayed through no fault of the company itself.

After many false starts, Imperial now feels that it has everything in place. The necessary visits have taken place and the facility is recruiting labour in order to carry out its first seeding in February. The first harvest is expected to be completed by May when the

Hydroponics and its benefits