09 The govt is kicking the wheat deregulation can down the road 14 Asset management taking off? Not yet

20 Crescent Star Insurance acquires significant stake in Tristar Power

22 Ghandhara Automobiles announces extension in distribution partnership with China’s Chery Automobile

23 Do big businesses undermine Pakistan’s competition laws?

26 In Pakistan’s high-end hairstyling business, a not-so-new player makes a move

28 Security Paper and the case of the delayed elections

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The govt is thekicking wheat deregulation can down the road

The state has been procuring and subsidising wheat production since 1968, claiming it is for the good of small farmers. In reality, it benefits everyone but the growers

Profit report

The long awaited process of wheat deregulation in Pakistan seems to be kicking off, but it is happening half-heartedly at best.

This comes as no

surprise, since wheat deregulation was not an idea that came from the government itself, but rather has been mandated by the International Monetary Fund (IMF), which has been ruthless in its direction to cut down unnecessary spending by the government. However, it seems the government has found a process with the IMF’s instructions. They

accept them, try to get away with doing not even the bare minimum but what looks like the bare minimum, getting reprimanded, and then finally acquiescing – sort of.

The IMF has stated clearly that provincial governments would be barred from setting crop prices as part of its $7 billion bailout package, board approval for which

Pakistan secured only a few months ago. It is possibly one of the reasons why the Punjab Government has abolished the provincial food department, replacing it with a new autonomous body.

As of now, the government is mostly just mucking about. They are forming a committee here, and a panel there, and trying to get away with handing wheat over to the free market. The reasons for this are purely political. Actually, the government thinks they are political. Somehow all governments in Pakistan, and particularly those in Punjab regardless of political party (but mostly the PML-N) think they will get votes if they can somehow magically control the price of wheat, both for farmers and end consumers. Historically, the kind of subsidies this has created have not been productive. But how exactly did we get here?

The centrality of wheat in Pakistan’s economy

What is today modern Pakistan

is the result of the British Empire’s appetite for wheat.

The British constructed railways in what is now Pakistan in 1855, in no small part due to a desire to connect the wheat-growing parts of Punjab and Upper Sindh to the port in Karachi.

In 1886, the British were able to start building the Punjab Canal Colonies, which were a series of large, previously sparsely inhabited areas in Punjab, that were brought under cultivation through the use of canals that diverted water from the province’s five rivers. Those canals allowed for previously landless and poor farmers to settle in newly cultivable regions, and the railways helped

them sell their surplus crop to the rest of the British Empire.

The British would begin building similar infrastructure for Sindh and Balochistan in 1923, with the construction of the Sukkur Barrage.

With the completion of these large rail and irrigation projects, the volume of commerce between Punjab and Sindh, in particular, exploded. On the eve of the First World War in 1914, Karachi had gone from being a small town on the coast of the Arabian Sea to becoming the largest grain port in the British Empire, and Punjab had become its principal bread basket. Karachi’s significance to the world was as the entrepot that provided access to Punjab’s wheat.

So central is wheat to Pakistan’s conception of itself that it is one of the four crops in the State Emblem (the other three being cotton, tea, and jute; the latter two were the principal crops of East Pakistan, but we will not spend too much time on that awkward remnant of history).

Yet despite this centrality of wheat, at independence, Pakistan’s population had grown so rapidly that it became a net importer of wheat. Indeed, a major initial bone of contention in the Cold War was the race between the United States and the Soviet Union to supply Pakistan with wheat. Between 1949 and 1952, nearly all of Pakistan’s wheat imports came from the Soviet Union. The US considered it a major foreign policy victory to get Pakistan to accept imports from the United States from 1953 onwards.

Within Pakistan, however, the reliance on imported wheat was seen as a national embarrassment, and one of the handful of the successful policies initiated by the pre-Ayub governments was to embark on a program to help Pakistani farmers improve the quantity of wheat produced in the country. By the latter half of the Ayub era, the government

succeeded.

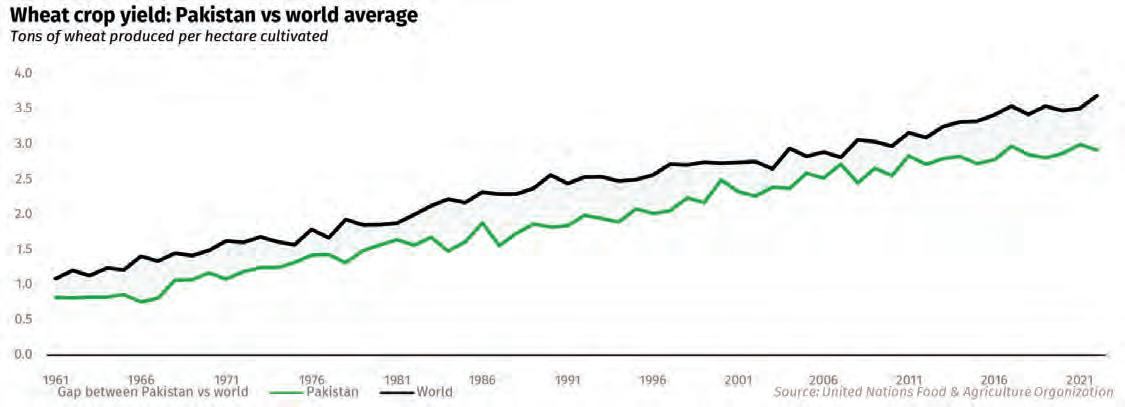

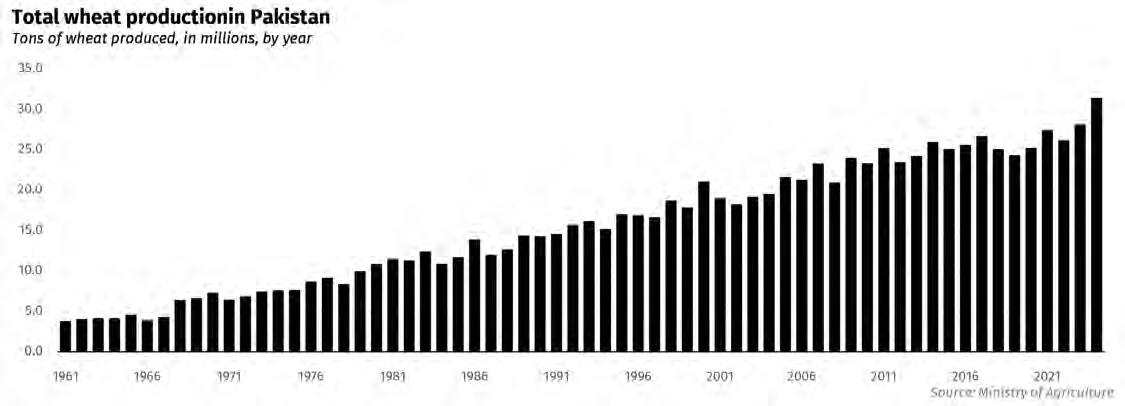

As a result of this, in 1968, Pakistan had a massive increase in wheat yield. This was the second year running this had happened, and farmers were struggling because the markets had not cleared all of their crop. This was a little embarrassing for the government, which had incentivised growing more wheat since at least the early 1960s to account for food security. Wheat makes up nearly a third of the caloric intake by an average Pakistani, and Pakistan’s per capita consumption of wheat is 124 kilograms annually, which is the highest in the world.

The government decided they would buy the excess wheat from the farmers and store it for a rainy day. This would give the farmers a buyer, their crop would not go to waste, and they could reliably plant it again next year. This was a slippery slope. Gradually, the government became the principal buyer and the private sector’s role shrank. To keep flour prices low for poor households, it established an extensive network of ration-shops, which provided subsidised wheat flour to low-income households. The ration system was abolished in 1987 due to partial targeting, inefficiencies and corruption.

The ration system was replaced with a subsidy on wheat issued to flour mills by the government from its procured stocks. Thus, a targeted subsidy was replaced by a general subsidy that ultimately became far more expensive than the one it replaced. The twin requirements of clearing stocks during harvest season and providing subsidised wheat to flour mills later in the year led the government to procure progressively larger volumes of wheat each year.

The next big change came in 2008, when the 18th amendment was passed and the provinces were made responsible for setting procurement prices and getting the wheat.

Bureaucratic hell

In Punjab, the government’s wheat procurement system is a bureaucratic labyrinth designed, in theory, to support small farmers by purchasing their wheat at premium prices. But in practice, it is a spectacle of inefficiency, political patronage, and frustration, where the people it is supposed to help are often left out in the cold—sometimes literally, since the wheat they grow has a better shot at being stored under plastic sheets than fetching a fair price.

Remember, of all the wheat that Pakistan produces around 60% of it is consumed by the growers either directly or for seed purposes. Of the remaining 40%, the government consumes around the lion’s share leaving only around 10% that sells directly to flower mills which give much lower prices than the government gives.

Every year since 2008, the Punjab Food Department (PFD) purchases about 18.6% of the province’s wheat production. However, the system is not tied to actual needs, like the production levels or what flour mills demand. No, the PFD often buys just enough to ensure its granaries are stocked to the brim, with significant leftover stock gathering dust—and storage costs—year after year. This inefficient hoarding occasionally results in millions of tons of carryover wheat, as was the case in 2009 when the PFD procured 5.78 million tons, resulting in 2.93 million tons of carryover stock the following year. The price tag on storing all that wheat? Huge. And it is the kind of inefficiency that makes a small farmer’s heart sink.

For the farmers, especially the smallholders for whom this system is supposedly built, the journey begins with an infuriating step: getting their names on the patwari list. This list, managed by local land record officials, is the golden ticket to even start the procurement process. But if you are a tenant farmer—or worse, a politically unconnected one—good luck. Tenants are often left off the list, thanks to landowners who do not want

What this leads to

The wheat support price is a bigger problem than one might realise. The concept behind wheat procurement is that the government buys wheat from farmers at a set rate which is higher than what they would get on the market so they continue to grow what is a strategically important crop. The problem is, provincial governments borrow heavily from commercial banks to fund these operations.

them included, and the unholy trinity of bureaucracy, politics, and poor record-keeping means even legitimate farmers frequently find their names missing. Sure, you could technically appeal, but that means preparing tenancy agreements (many of which are verbal) and making endless rounds of government offices. For most, it is easier to sell their wheat at a loss to middlemen than try to fight the system.

Once you have made it past that hurdle, you are handed another one: bardana, the jute or polypropylene bags that you must use to supply your wheat. The bags are rationed out by PFD, and like so many things in the wheat procurement system, who gets them depends less on their crop yields and more on their connections. Well-connected farmers can secure them swiftly, while others wait in agonisingly slow-moving queues. For the average farmer, this means navigating a carefully cultivated system of political favours to ensure a steady supply of bags, all while paying a deposit at a bank (Rs134 per jute bag or Rs38 for polypropylene) before the bags can even be issued. The entire back-and-forth between procurement centres and banks can stretch out for days or weeks.

Once the bardana is secured, it is a race against time. Farmers who have their bags filled must transport them to their designated procurement centres. This requires renting a trolley—an expense most small farmers can ill-afford—since only the largest farms have the means to transport all of their stock at once. An average trolley can carry 100 bags, but many small farmers do not produce enough wheat to justify multiple trips. And even those who manage to get their wheat to the centre face a gamble: not all centres have a weighbridge, so a random 10% sample is weighed, meaning some unlucky farmers find themselves shortchanged during the process.

The worst part? Farmers have to bear all transportation costs and labour expenses. Casual labour at these centres is hired to help unload the bags, stitch them, and weigh

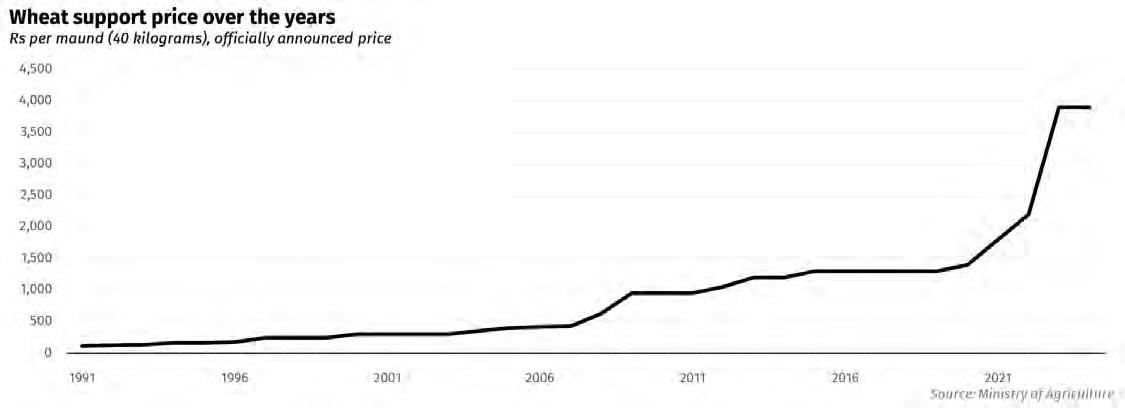

In 2023, for example, the wheat procurement target was 40 lakh tonnes and the government had set a price of Rs3,900 per maund (a unit of measuring weight equal to 40 kilograms), or around Rs97.5 per kilogram. To buy this much wheat from farmers at this rate, the government would need around Rs394 billion. Now, the government sells the wheat they acquire to flour mills at this rate so they do recover this money. However, the government relies on borrowing this sum from commercial banks. At an interest rate of 23%

them, and while PFD offers a Rs. 9 per bag reimbursement for labour, they don’t cover the costs of filling or stitching the bags or transporting them to the centres in the first place. Farmers are left holding the bill for this, on top of the 5-6% losses that occur in open storage—losses that PFD is happy to shove off onto them.

And let’s not forget the waiting. PFD likes to spread out its procurement operations from mid-April to the end of May, with each farmer being assigned a preferred delivery date. On paper, it should take five to six hours to complete the transaction, but in reality, it can take far longer. If you show up early or late, or if the centre’s having a busy day, you could be stuck for an entire day without compensation for your time. And should the centre’s storage hit its unofficial target early, it might just stop procuring, leaving the less-connected farmers out in the cold.

Even when they do manage to sell their wheat, the payment process is another grind. For smaller consignments, farmers might get cash on the same day. But if they’ve sold more than 50 bags, they receive a slip, which means yet another trip—this time to a designated bank. By the time all is said and done, a farmer may have visited the procurement centre three times and the bank twice, burning between seven and ten days just to get paid.

In bumper years, like 2017 and 2018, the government’s incompetence shines even brighter. Unable or unwilling to buy all the wheat, the PFD conveniently adopts a “goslow” strategy, rationing bardana to only a select group of politically favoured farmers. The rest are left in a queue that moves so slowly, they are forced to sell their wheat to private traders at lower prices. In those years, market prices hovered between Rs1,100 and Rs1,250 per maund, while the government price was Rs1,300. But with the government sitting on massive carry-forward stocks and reluctant to buy, only the well-connected made it through the system.

in 2023, the government would be paying around Rs90 billion in monthly instalments of 10 months through selling wheat to flour mills. The government also always procures more wheat than it needs and consistently has leftover grain from previous years in storage. On top of this, the government also needs to spend tens of billions of rupees on handling, transportation and storage costs incurred by the PASSCO on a federal level. The government regularly fails to live up to its commitment with commercial banks, and over

time, this has led to circular debt. In 2020, this had risen to Rs757 billion.

How the wheat subsidy feeds commercial banks

And if you think farmers are benefitting from this, you are sorely mistaken. Data for wheat procurement is not updated, with the latest collected information available up to 2020. That is why in our explanation we focused so much on the 2018-19 season, which marked the 10 year mark since the Punjab government began this operation on its own.

What becomes clear is that farmers are not benefitting from this. Data on wheat production by farm size in Punjab shows that 13.3% of farms do not produce wheat at all. Of the 86.7% farms that produce wheat (comprising 63.7% of the total area of private farms), 90.5% percent are smaller than 12.5 acres. This means 78.5% of total farms producing wheat are small farms. These farms are only 40.5% percent of the total farm area and 63.6% of the area of farms reporting wheat. Very small farms of less than one acre do not sell wheat because they do not have a marketable surplus.

Data on wheat production by farm size are not available, but assuming that they produce at the national average of 800 kg wheat per acre and consume wheat flour at 140 KG per person, with an average household size of 6.3, they produce less than their own consumption even when they allocate the entire area to wheat production. Together, non-wheat-producing farms and very small farms are 22.2% of all farms in Punjab.

Then who is benefitting from this? One answer might be commercial banks. On paper, the Punjab Food Department’s (PFD) subsidy structure is meant to stabilise the market, protect farmers, and deliver cheap wheat flour to consumers. In reality, it is more of a balancing act on a tightrope of debt, where the govern-

ment throws money around with one hand while borrowing furiously with the other. And as you might expect, it is the farmers—and the taxpayers—who ultimately bear the cost.

The subsidy system is straightforward in its premise: PFD buys wheat from farmers at a price that is often higher than the open market and then turns around to sell it to flour mills at a below-market rate. The idea is to keep flour prices stable, prevent market crashes that would hurt farmers, and provide cheaper wheat flour to consumers. On one front, it works—PFD has largely succeeded in smoothing out seasonal price fluctuations, reducing volatility, and keeping flour prices from skyrocketing (a win in a country where food inflation can lead to serious political unrest). But that is about where the good news ends.

Take 2017-18 as an example. That year, PFD’s wheat operations racked up a staggering cost of Rs.34.4 billion, with the bulk of this cost (over 70%) attributed to something that has little to do with actually feeding people: bank mark-up. The PFD borrows money every year to purchase wheat, and while it manages to sell that wheat to flour mills, the government never quite gets around to repaying the entire amount. Instead, it kicks the can down the road, paying off only part of its debts and leaving the remainder to accumulate. This results in PFD not only having to pay interest on its current loans but also on its mounting, unpaid liabilities. For the past five years, this interest alone has averaged Rs19.6 billion per year—just the cost of borrowing money to keep the wheels of wheat procurement turning. Why then do we insist on having these wheat support prices every year? The government will tell you that their aim is to give confidence and provide security to poorer farmers, as well as get cheap flour to the markets. They are lying. All indicators and an impressive body of academic literature on the topic tells us leaving crop prices up to market forces is what is best for farmers.

Farmers would make more money

without a wheat support price, even though they have become heavily dependent on it. But breaking that habit might be a good thing. The removal of the wheat support price will allow farmers to possibly look towards other crops as well, and if the government moves on allowing GMO crops such as maize, it can prove to be a gamechanger.

The politics behind it

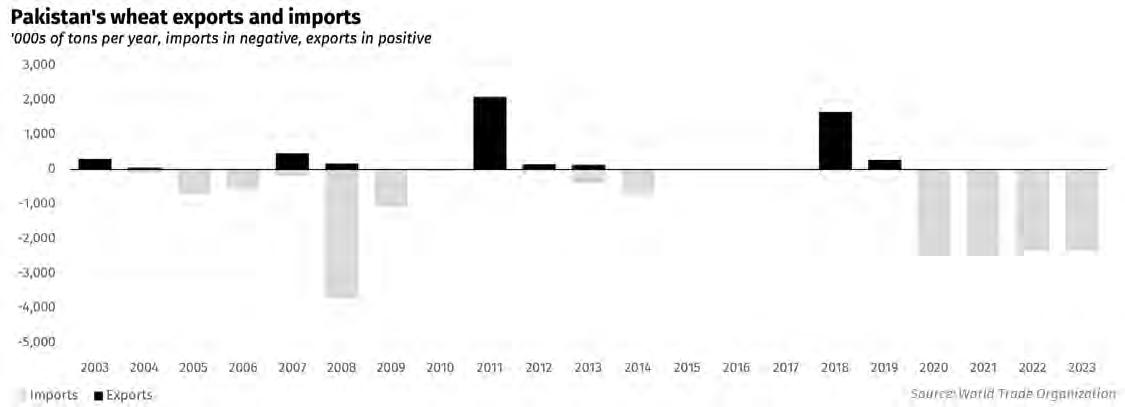

In many ways, wheat runs Punjab. Perhaps nothing points towards this better than the billion dollar wheat import scandal of 2023-24 that the Punjab and federal governments are still suffering from.

In this case, the ruling Pakistan Muslim League-Nawaz (PML-N) found itself embroiled in internal tensions over how to address a scandal that is as much about political manoeuvring as it is about financial mismanagement. Former Prime Minister Nawaz Sharif pushed for strict accountability against the caretaker government that oversaw the import of 1.2 million tonnes of surplus wheat. However, his brother, current Prime Minister Shehbaz Sharif, hesitated, reluctant to implicate members of his own coalition, including those with ties to the establishment.

The roots of the scandal go back to a bureaucratic blunder that allowed wheat imports far beyond what was necessary to compensate for the 2022 floods, allegedly driven by kickbacks to the caretakers. The result? A staggering loss of over $1 billion in foreign exchange at a time when Pakistan’s economy is in shambles, coupled with Rs300 billion in losses for farmers, who were left struggling to sell their wheat amid a surplus and crashing prices. Meanwhile, flour millers and traders are believed to have reaped enormous profits at the expense of both the government and the agricultural sector.

The handling of this scandal—and the broader wheat procurement process—has been chaotic. While the government set up inquiry committees, they have been hesitant to fully

investigate key figures in the caretaker government. The Punjab government’s response to farmers’ protests was heavy-handed, deploying force to quell dissent rather than addressing the root cause of their grievances: a procurement system that is deeply flawed.

This scandal is not an anomaly—it is symbolic of a wheat procurement system plagued by inefficiency, cronyism, and an inability to balance the needs of farmers with broader economic realities. From bloated subsidies to reckless imports, Pakistan’s wheat policy has long been a patchwork of short-term fixes that only serve to deepen the long-term problems. By 2024, the situation had deteriorated even further, with wheat imports crashing domestic prices and leaving farmers in financial ruin—exactly the kind of breakdown that has come to define the country’s toxic relationship with its agricultural sector.

Where we stand

It seems simple enough, does it not? The wheat subsidy benefits no one, it is a political disaster, and we should absolutely get rid of it, promote financing for farm -

ers, introduce robust policy that protects crops and land and let market forces handle the rest. Well, the government claims they are trying. Just for the sake of it, let us give you the spiel that the government has tried to give us in their own words:

“To formulate a comprehensive strategy, the Ministry of National Food Security and Research (MNFS&R) will host a National Workshop on Deregulating the Wheat Sector on Friday, January 24, 2025, in Islamabad. This initiative underscores the government’s commitment to transitioning towards a transparent and efficient wheat market while safeguarding national food security through strategic reserves.

Representatives from all provinces, including food secretaries and industry experts, will deliberate on key challenges and propose solutions for modernizing wheat procurement practices. The workshop will serve as a platform for stakeholders to address regulatory challenges, explore innovative approaches, and ensure that the deregulation process balances market efficiency with food security.

To encourage broad participation,

the ministry has arranged accommodations and travel for outstation attendees. Prime Minister Shehbaz Sharif had earlier tasked a high-level committee, led by Finance Minister Muhammad Aurangzeb, with devising a wheat procurement plan for the Food Year 2024-25 in line with IMF recommendations. The committee also includes the Ministers for National Food Security and Research, Commerce, and the Advisor to the Prime Minister on Political Affairs and Inter-Provincial Coordination. Their mandate includes reviewing wheat pricing, procurement mechanisms, and ensuring price stability.”

All of this, of course, means nothing. The government is essentially renting out a big fancy venue with catering and lots of important people strolling around. The point will be to discuss deregulating wheat instead of actually doing something. They will then take some pictures, stick them in a powerpoint, and try to show the IMF that this is them trying their best. The IMF will, of course, call them out on it. Will this be enough to finally spur them on? Possibly. We just wish they would get on with it. n

Asset management taking off? Not yet

By some measures, the Pakistani asset management industry is the largest it has ever been.

By other measures, it has not even recovered its 2008 peak yet

By Farooq Tirmizi

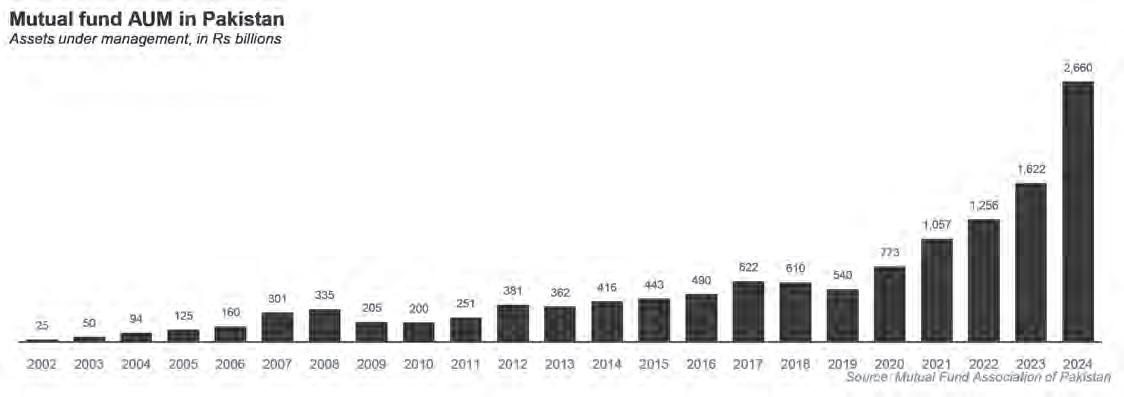

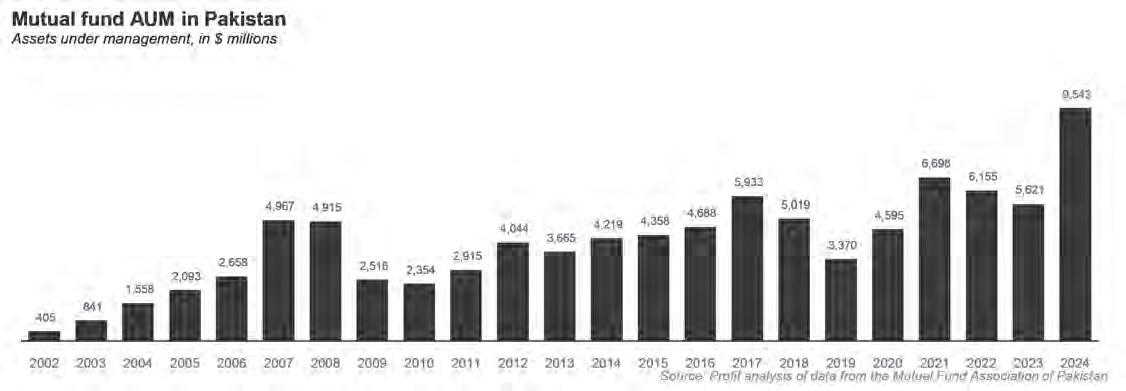

For the first time in its history, the asset management industry in Pakistan is managing more than $10 billion. A pittance though it may be by global standards, this feels like a milestone worth marking for the industry. Except that it is hard to get excited about the industry reaching milestones when, by some measures, it has yet to surpass its own records set in 2008.

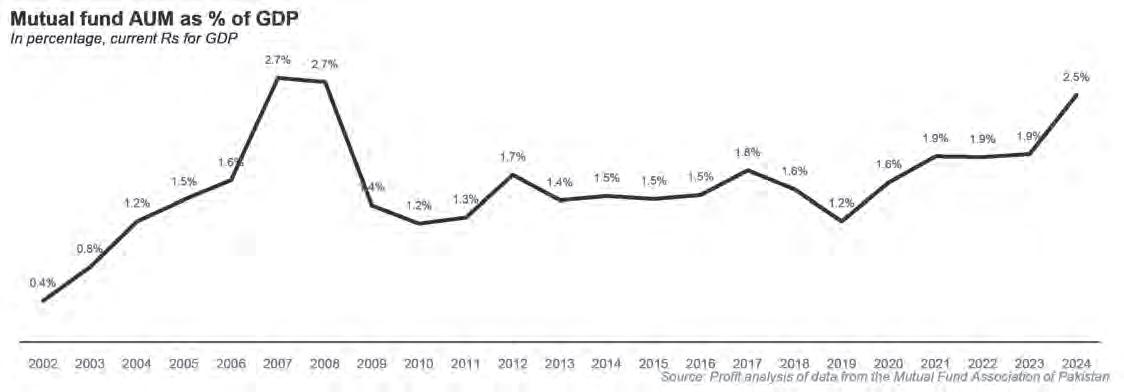

Measured in assets under management (AUM), whether in rupees or dollars, the industry is larger than it has ever been, and has been growing at a reasonably rapid rate over the past two decades. Measured as a percentage of the total size of the economy (gross domestic product, or GDP) or even as a percentage of total bank deposits, and the industry is still below levels it was able to surpass in 2008.

Despite a sharp rise in AUM over the past five years, the industry is still a relatively small corner of Pakistan’s financial services sector, and of the economy, despite what appear to be strong undercurrents favouring the industry, not least of which is a regulator that seems keen on helping the industry grow.

So why has the industry not yet taken off? Why does it even matter to the Pakistani economy that it grow? And what, if any, circumstances would need to change in order for the industry to start growing?

Disclosure: I am the CEO of Elphinstone, a Registered Investment Advisor regulated by the United States Securities and Exchange Commission, and of Trikl Pakistan, a company in the process of seeking a digital asset management license from the Securities and Exchange Commission of Pakistan, having recently concluded a stint in the SECP’s regulatory sandbox.

Is this article going to be me talking my book? Probably. But it might still be worth your time.

As ever, we begin our story with a history of how it all began and got to where we are today.

The history of asset management in Pakistan

The Pakistani asset management industry got its start through a government initiative. The National Investment Trust (NIT) was created in 1962 and launched a single mutual fund, on November 12 of that year, called the National Investment Unit Trust, which still exists as the oldest mutual fund – or indeed any kind of investment fund – in the country.

In 1966, the government created a second investment company called the Investment Corporation of Pakistan (ICP), which was given the mandate to launch twenty-six closed-end mutual

funds. Those closed-end mutual funds would be sold off to private sector asset management companies in 2002, in a privatization transaction.

All of this is before there were any regulations to govern the industry at all. The Investment Companies and Investment Advisors Rules were not enacted until 1971, which was rather poor timing as it so happened that the country was in the middle of a massive civil war. The rules codified the regulations under which private sector companies could start closed end mutual funds.

On May 1, 1983, more than a decade after those rules went into effect – and more than two decades after the government first started the asset management industry in the country – the first private sector entity created a mutual fund. The Golden Arrow Fund started then as a closed end mutual fund, and it still exists today as an open ended mutual fund managed by AKD Investment Management. It also has the best long-term track record in terms of average annual returns over long periods of time.

The industry as we know it today started taking shape in 1995, when a broader set of regulations came into effect and allowed open ended mutual funds to come into existence. On October 27, 1997, Abamco, a predecessor company to what we now know as JS Investments, set up the Unit Trust of Pakistan, the first open ended mutual fund set up in Pakistan.

Closed end funds buy assets once and then trade on an exchange. Open ended funds can continue to accept new investments from individuals and companies and keep on increasing their asset base, and hence are a more important component of asset management in any country’s capital markets.

It was sometime after this, during the second Nawaz Administration, that the government felt that its old corporate regulator – the Corporate Law Authority – was insufficient to govern what was rapidly becoming a multifaceted capital market in the country. It therefore decided to replace the Corporate Law Authority with a regulator with more expansive powers, which was named the Securities and Exchange Commission of Pakistan.

In 2005, the government created a tax-advantaged retirement savings vehicle called the Voluntary Pension Scheme (VPS), and in 2008, the law was changed to allow for Provident Funds and Gratuity funds to invest in – or be replaced by – VPS funds. (You may notice the tendency of the government to pass significant legislation relating to the capital markets at inopportune times.)

Meanwhile, the industry kept on adding new products, and kept on being encouraged to do so by the regulator. The first Islamic fund was launched also by JS Investments in December 2002. Money market funds were introduced in 2008. And the Mutual Fund Association of

Pakistan partnered with the then-Karachi Stock Exchange to allow for the electronic trading of bonds on the exchange. And the first real estate investment trusts (REITs) were launched in 2015.

But perhaps most importantly, in 2023, the Khyber-Pakhtunkhwa government announced that its new employees would no longer get guaranteed pensions and instead would have their retirement funds be invested in a defined contribution account that could then invest in mutual funds.

Why the industry has not yet grown

To be clear, the asset management industry in Pakistan is growing, and growing quite rapidly. Between 2002 and 2024 the industry has grown by an average annual rate of 15.6% per year in U.S. dollar terms, according to Profit’s analysis of data from the Mutual Funds Association of Pakistan (MUFAP). This is by no means slow, but when you consider just how rapidly the

rest of the economy has been growing, this is not fast enough.

Mutual fund AUM in Pakistan account for 2.5% of GDP which is less than the 2.7% of GDP that they constituted in 2008. In terms of percentage of bank deposits, mutual fund AUM hit 8.5% in 2024 after a decade and a half of rising almost consistently, but were still below the 8.7% reached in 2008.

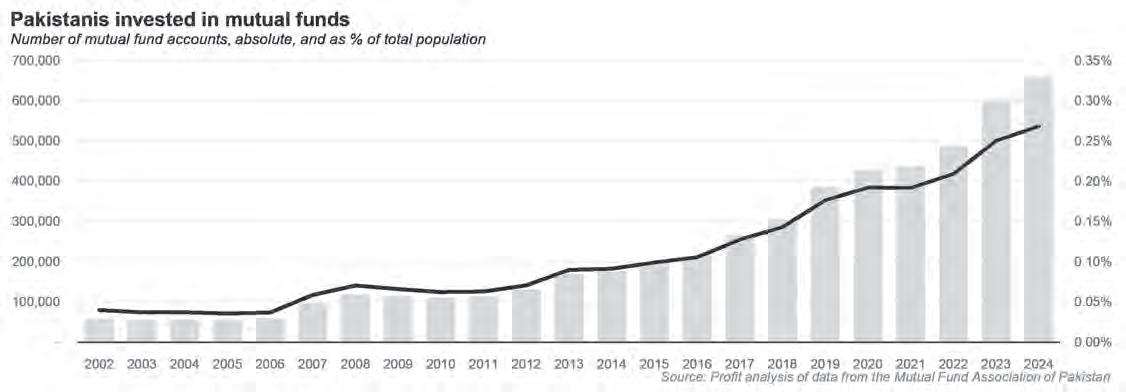

According to MUFAP data, just over 526,000 people have mutual fund accounts, which is less than 0.5% of the adult population of the country. In other words, well over 99% of the population does not invest in mutual funds yet. This is a bit better than the 330,000 people who have accounts to trade stocks on the Pakistan Stock Exchange, but is still fairly abysmal.

Why do more Pakistanis not have mutual fund accounts? Most of them do not have enough savings to have anything beyond a basic bank account. As we have stated earlier, there is a deep link between the demographics of a country and its ability to save. As a whole, Pakistan is both too young, and has family siz-

es that are still a bit larger than ideal, for there to be meaningful savings in the economy. Without higher savings levels, one cannot expect savings instruments of any kind to be growing. Mutual funds are no exception to that rule.

On top of this, what little growth has come to the industry has been stymied by a set of skewed incentives for the industry. Most asset management companies in Pakistan are owned by banks, and bank managements have a tendence to look upon their asset management divisions as forgotten step-children, not central to the core business of providing banking services – specifically deposit accounts – to their customers.

There are, of course, cultural habits around investing in real estate and a lack of trust in capital markets in general. But these are less likely to be factors in why the industry has not grown than the fact that its primary competitor is real estate and – for all practical purposes – an investor’s gains in real estate are taxed relatively little, if at all, whereas taxes on just about every formal

means of savings are higher.

Individual investors are making tax-optimizing decisions, and hence choosing to park their money in real estate and not in mutual funds.

Why does any of this matter?

This article will not delve into the fundamentals of personal finance in any detail, but one rule is inescapable and worth mentioning: your financial life is a struggle against inflation. Any amount of money you are saving will have to contend with the fact that money loses value over time in every country and in almost every era. That means that cash, in inflation-adjusted terms, is a money-losing proposition. Saving without investing is effectively the same and destroying your own wealth.

And any investments you make have to beat inflation over the time period that you are making the investment. This means that you need to have a good idea of what inflation is and what it is expected to be in the future. And

for that, it helps to know what inflation has been in the past.

Pakistan’s economic history has had periods of both high and low inflation. The average since January 1958 has been about 8.2% per year. However, one can reasonably make the case than the Pakistani economy has fundamentally evolved since 1958, and perhaps not all of those years provide relevant data points. A shorter period that still has a sufficiently long period of data might involve the time since the end of the Zia Administration in 1988. Since that time, inflation has averaged 9.4% per year.

In order to beat inflation consistently, you need to be invested in assets that can beat inflation over the long run. That is what mutual funds – in particular those with exposure to the equity markets – offer.

A mutual fund is a pool of investment created by an asset management company to make it easier for investors to invest their money without having to do research for themselves or even having large sums of money. They then take the money from all their investors, conduct their own research, and

then invest the money in a variety of different investments.

Mutual funds are classified by which types of securities they invest in. A stock mutual fund, for example, is not allowed to invest in anything but stocks. A fixed income fund is not allowed to invest in stocks. A balanced fund is allowed to invest in both stocks and bonds, but cannot be invested in just one category of investment.

For the overwhelming majority of investors, mutual funds are the most logical choice of investment. There are dozens of asset management companies in Pakistan and they offer a wide variety of mutual funds.

For any savings needs (retirement, children’s education, etc.) for which you need to save for a period longer than 10 years, stock mutual funds are the best way to invest. For periods between five and 10 years, balanced funds are a better option. And for periods shorter than five years, fixed income funds or National Savings bonds are likely the best option.

In short, for the average individual, the easiest way to park their savings in a set of assets that beats inflation is through mutual

funds. It is mathematically impossible for a middle class person with no independent sources of wealth to be able to save enough money to retire comfortably while putting money away in a savings account, or worse, a current account.

Hence, it matters how many Pakistanis are using mutual funds in order to invest their life savings.

What will change?

The biggest thing that will cause the industry to start growing has less to do with the industry and more to do with demographics. Specifically, when Pakistan’s fertility rate falls below 3.0 – something likely to happen around 2033 – the capacity of households in the economy to be able to save will start rising exponentially, which in turn will result in more people turning to savings products, including mutual funds.

According to research by Charles

Robertson, an economist at FIM Partners, a London-based investment firm, and author of the book The Time Traveling Economist, an economy that has between 3-4 children per woman has deposits equal to an average of about 30% of GDP, which is very close to the number Pakistan is at right now. When it goes below 3 children per woman, it sees a rapid increase in its household ability to save, and bank deposits as a percentage of GDP effectively double to about 60% of the total size of the economy.

Pakistan will hit that tipping point sometime around 2033, at which point the rise in savings, bank deposits and mutual fund AUM will become exponential.

One other thing that could change is the government moving away from defined pensions and towards defined contribution retirement systems, an initiative that the Khyber-Pakhtunkhwa government – led by former provincial finance minister Taimur Khan Jhagra – has already undertaken.

The point about retirement bears

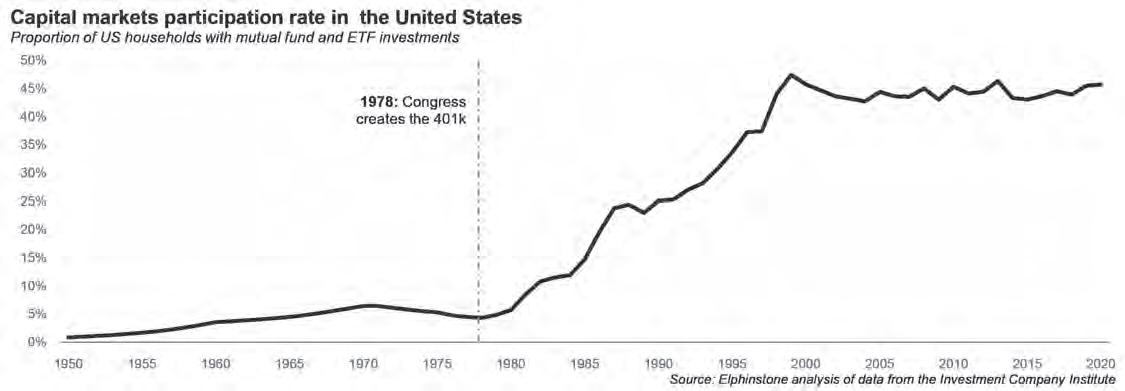

repeating: this is how mature capital markets like the United States have created a nation of investors: by moving retirement savings into individualized, customizable, tax-advantaged accounts that can be invested in mutual funds.

In the United States, this type of vehicle is called the 401k, and prior to its launch in 1978, the proportion of Americans who had any kind of capital markets account was about 3.8%, a proportion that skyrocketed in the two decades afterwards to reach over 50% of the population.

In Pakistan, the equivalent vehicle is called the Voluntary Pension Scheme, and it can be used to similar effect by both government and private sector employers to offer retirement savings benefits to their employees without bankrupting themselves in trying to pay out pensions to older employees long after they have left.

At some point, companies will start converting their retirement benefits to VPS, when they realise that the costs are becoming unmanageable. Employee retirement obligations are a bigger problem than you think. Total retirement liabilities for Pakistani companies have grown from 6.5% of operating profits in 2014 to 9.4% of operating profits by 2020, an alarmingly fast rise that is likely to have a significant impact on the financial health of most companies.

Most of the major asset management companies offer VPS funds, and about 100,000 Pakistanis now have VPS accounts. But at almost none of the major firms is the VPS product a core area of focus, and nor is it likely to become one until demand for the product organically grows through changing circumstances in the country’s political economy.

Until then, the industry is likely to continue posting good-but-not-exceptional growth numbers. This, more than anything else, is what will hamper the growth of Pakistan’s capital markets. n

Crescent Star Insurance acquires significant stake in Tristar Power

Move comes as part of a wider trend by Pakistani insurance companies to make significant investments in the energy sector

Profit Report

In a strategic move that underscores the growing trend of insurance companies diversifying their investment portfolios, Crescent Star Insurance Ltd has announced a substantial acquisition of shares in Tristar Power

Ltd. The transaction, which took place on January 20, 2025, marks a significant step in Crescent Star's investment strategy and highlights the increasing role of insurance companies as institutional investors in Pakistan's energy sector.

According to a disclosure statement issued by Crescent Star Insurance on January

21, 2025, the company has acquired additional voting shares of Tristar Power Ltd at a price of Rs. 6.45 per share. This recent purchase has elevated Crescent Star's total shareholding in Tristar Power to 2,203,997 shares, representing a 14.69% stake in the power company's total issued voting shares[1].

The acquisition represents a notable

increase from Crescent Star's previous holding of 2,071,919 shares in Tristar Power. This move not only strengthens Crescent Star's position as a significant shareholder but also signals the insurance company's confidence in the long-term prospects of Pakistan's energy sector[1].

Crescent Star Insurance Ltd, established on May 8, 1957, has been a stalwart in Pakistan's insurance landscape for nearly seven decades. Tristar Power Ltd, the target of Crescent Star's investment, is a key player in Pakistan's energy sector.

The energy sector in Pakistan has been a focus of both government and private investment in recent years, as the country works to address its power needs and modernize its electricity grid. Tristar Power's attractiveness as an investment target for a major insurance company like Crescent Star indicates its potential for growth and its important role in Pakistan's energy landscape.

The move by Crescent Star Insurance to increase its stake in Tristar Power is part of a broader global trend where insurance companies are becoming increasingly active as institutional investors, particularly in growth equity and infrastructure projects.

Insurance companies, with their substantial assets and long-term investment horizons, are well-positioned to invest in sectors that require patient capital and offer steady returns. This strategy allows insurers to diversify their portfolios, hedge against inflation, and potentially achieve higher yields compared to traditional fixed-income investments.

In the United States, this trend has been evident for several years. Major insurance companies have been allocating significant portions of their investment portfolios to various sectors, including energy, real estate, and technology startups.

For instance, New York Life, one of the largest mutual life insurance companies in the United States, has been actively investing in private equity and infrastructure projects. In 2024, the company announced a $1 billion investment in renewable energy projects across North America, demonstrating the insurance industry's commitment to both financial returns and sustainable development.

Similarly, Prudential Financial, another American insurance giant, has been expanding its alternative investment portfolio. In 2023, Prudential's investment arm, PGIM, allocated $5 billion to growth equity investments in technology and healthcare sectors, showcasing the insurance industry's appetite for high-growth opportunities.

In Pakistan, the trend of insurance companies investing in the energy sector is gaining momentum, driven by the country's

pressing need for reliable power infrastructure and the potential for stable, long-term returns.

The State Life Insurance Corporation of Pakistan, the country's largest state-owned life insurer, has been a pioneer in this regard. In 2023, it announced a significant investment in a solar power project in Sindh province, marking its entry into the renewable energy sector.

Adamjee Insurance, another major player in Pakistan's insurance market, has also been diversifying its investment portfolio. In 2024, the company acquired a minority stake in a wind power project in Jhimpir, Sindh, further illustrating the insurance sector's growing interest in energy investments.

The investment by Crescent Star Insurance in Tristar Power has several implications for Pakistan's energy sector.

This move signals growing confidence in the energy sector from institutional investors, which could encourage further private sector participation in power generation and distribution projects.

As institutional investors like insurance companies increase their stakes in energy companies, there may be a push for improved corporate governance and operational efficiency.

Insurance companies typically have long investment horizons, which aligns well with the capital-intensive nature of energy projects. This could lead to more stable, patient capital being available for crucial infrastructure development.

As more insurance companies enter the energy investment space, it diversifies the sources of funding for power projects, reducing reliance on traditional banking sector loans or government funding.

While the trend of insurance companies investing in the energy sector presents numerous opportunities, it also comes with challenges:

Insurance companies in Pakistan must navigate complex regulations governing their investment activities. The Securities and Exchange Commission of Pakistan (SECP) closely monitors such investments to ensure they do not compromise the insurers' ability to meet policyholder obligations.

Investing in energy projects carries inherent risks, including regulatory changes, market fluctuations, and operational challenges. Insurance companies will need to develop robust risk management frameworks to handle these investments effectively.

Insurers must strike a balance between seeking higher returns through energy investments and maintaining sufficient liquidity to meet insurance claim obligations.

As insurance companies increase their exposure to the energy sector, they will need

to develop or acquire specialized expertise in evaluating and managing these investments.

The investment by Crescent Star Insurance in Tristar Power is likely to be a harbinger of more such moves in the Pakistani market. As the country continues to grapple with energy challenges and seeks to modernize its power infrastructure, the role of institutional investors, particularly insurance companies, is expected to grow.

This trend could lead to several positive outcomes. Insurance companies, with their long-term outlook, may be more inclined to invest in renewable energy projects, aligning with global sustainability trends.

The influx of patient capital from insurance companies could accelerate the development and upgrading of Pakistan's energy infrastructure.

As insurance companies become more active investors, it could lead to the development of more sophisticated financial instruments and a deeper capital market in Pakistan.

Partnerships between insurance companies and energy firms could facilitate knowledge transfer, particularly in areas like risk management and corporate governance.

The acquisition of a significant stake in Tristar Power by Crescent Star Insurance marks an important milestone in the evolution of Pakistan's financial and energy sectors. It exemplifies the growing trend of insurance companies acting as institutional investors, particularly in critical infrastructure sectors.

As this trend continues to unfold, it has the potential to reshape Pakistan's energy landscape, bringing in much-needed capital, expertise, and a long-term perspective to the sector. However, it will be crucial for regulators, insurance companies, and energy firms to work together to navigate the challenges and maximize the benefits of this emerging investment paradigm.

The move by Crescent Star Insurance not only strengthens its own investment portfolio but also sends a positive signal to other institutional investors about the potential of Pakistan's energy sector. As the country strives to meet its growing energy needs and transition towards a more sustainable power mix, the role of insurance companies as strategic investors is likely to become increasingly significant.

This development represents a convergence of financial acumen and industrial progress, potentially heralding a new era of collaboration between Pakistan's insurance and energy sectors. As this story continues to unfold, it will be fascinating to observe how this partnership model evolves and what impact it has on Pakistan's broader economic development and energy security goals. n

Ghandhara Automobiles announces extension in distribution partnership with China’s Chery Automobile

Extension in agreement as both companies continue working towards a more permanent agreement

Profit Report

In a significant development for Pakistan's automotive industry, Ghandhara Automobiles Limited (GAL) has disclosed that its distribution agreement with Chinese automaker Chery Automobile Co., Limited is undergoing a transition phase. The announcement, made through a statement to the Pakistan Stock Exchange, reveals that the existing agreements between the two companies expired on January 25, 2025, but negotiations for a smooth transition are ongoing.

GAL's Distribution Agreement and KD Supply Agreement with Chery Automobile Co., Limited have reached their termination date. Both companies are currently in talks to finalize the terms of a transition. During this transition period, GAL will maintain its role in selling Chery brand vehicles and providing after-sales services to customers in Pakistan.

This development marks a pivotal moment in the partnership between the Pakistani and Chinese automotive entities, potentially reshaping the landscape of Pakistan's car market.

The collaboration between Ghandhara Automobiles and Chery Automobile has been a notable example of international partnerships in Pakistan's growing automotive industry. As the exclusive distributor and authorized representative of Chery in Pakistan, GAL has played a crucial role in introducing Chinese automotive technology to Pakistani consumers.

The continuation of sales and services during the transition period suggests that both companies are committed to minimizing disruptions for customers and maintaining market presence. This approach is likely to reassure current Chery vehicle owners in Pakistan and potential buyers who may have been considering a purchase.

The news of this transition comes at a time when Pakistan's auto sector is facing various challenges, including economic uncertainties and changing consumer preferences. The outcome of the ongoing negotiations between GAL and Chery could have significant implications for:

1. Market Competition: Any changes

in the partnership structure could affect the competitive landscape, potentially influencing pricing and product availability.

2. Consumer Choice: The continued presence of Chery vehicles in the Pakistani market depends on the success of these negotiations.

3. Industry Partnerships: This development may inspire other local and international automakers to reassess their strategies in Pakistan.

Ghandhara Automobiles Limited has been a prominent player in Pakistan's automotive sector for several decades. The company's history is deeply intertwined with the country's industrial development:

Established in the early years of Pakistan's independence, GAL has been a pioneer in the local automotive industry. Over the years, GAL has expanded its portfolio, engaging in the assembly and distribution of various vehicle types, including commercial vehicles and passenger cars.

The company has a history of collaborating with international automakers to bring global brands to the Pakistani market.: GAL has contributed significantly to Pakistan's efforts in localizing auto parts production, supporting the growth of the domestic supply chain.

Chery Automobile Co., Limited has emerged as one of China's leading automotive manufacturers and a significant player in the global market:

Founded in 1997 in Wuhu, Anhui Province, China, Chery quickly became one of China's largest independent automobile manufacturers. The company has aggressively pursued international markets, with a presence in over 80 countries.

Chery has invested heavily in research and development, particularly in new energy vehicles and smart car technologies. The company offers a wide array of vehicles, from compact cars to SUVs and electric vehicles.

The collaboration between Ghandhara Automobiles and Chery Automobile began as part of both companies' strategic expansion plans. The partnership was formed to introduce Chery's modern and affordable vehicles to the Pakistani market.

Chery's entry into Pakistan through GAL

was seen as a significant move to capture a share of the growing South Asian automotive market. The partnership introduced several Chery models to Pakistani consumers, offering alternatives to established Japanese and Korean brands. Plans were put in place for local assembly of Chery vehicles, aligning with Pakistan's auto policy aimed at increasing localization.

As Ghandhara Automobiles and Chery Automobile navigate this transitional phase, several scenarios could unfold:

1. Renewed Partnership: The companies might renegotiate terms and continue their collaboration under a new agreement.

2. Altered Structure: There could be changes in the partnership structure, possibly involving new stakeholders or a different operational model.

3. Potential Split: In the event negotiations don't lead to a mutually beneficial agreement, GAL might seek new international partners, or Chery could explore alternative distribution channels in Pakistan.

The outcome of these negotiations will be closely watched by industry analysts, as it could signal broader trends in international automotive partnerships in emerging markets like Pakistan.

The announcement by Ghandhara Automobiles Limited regarding its transitioning agreement with Chery Automobile Co., Limited marks a significant moment in Pakistan's automotive landscape. As both companies work towards finalizing a smooth transition, the industry and consumers alike will be keenly observing the developments.

This situation underscores the dynamic nature of international business partnerships and the evolving automotive market in Pakistan. It also highlights the importance of adaptability and strategic planning in the face of changing market conditions and partnership dynamics.

As the story unfolds, it will undoubtedly provide valuable insights into the future direction of Pakistan's automotive sector and its engagement with global automotive giants. The coming weeks and months will be crucial in determining the long-term implications of this transition for both Ghandhara Automobiles and the broader Pakistani auto market. n

Do big businesses undermine Pakistan’s competition laws?

The CCP has more than 500 pending cases languishing in the courts. Is that what makes them inefficient or is there more to the story?

By Ghulam Abbas

Why do we need a competition commission? The Competition Commission of Pakistan (CCP) in its current form was created by a 2007 Act of Parliament in an effort to meet the requirements of the World Trade Organization, which Pakistan joined in 1995.

Before the CCP, competition law was regulated by an aptly named and quite self-explanatory entity called the Monopoly Control Authority. That, at the crux of it, is the purpose of competition law. Most modern competition law emerged in the middle of the twentieth century, particularly with anti-trust laws in the United States. To cut a very long story short, governments realised the free market was prone to manipulation, and to avoid monopolies forming and resources being concentrated in individual hands, there needed to be laws governing how companies conducted business.

If making money was a game, this was the rulebook on how to play fair.

In developing countries like Pakistan, different autonomous bodies and commissions have come and gone. These bodies are responsible for implementing and regulating a country’s competition laws. A good competition

commission wears many hats. They are sometimes referees, other times choreographers. The job of the CCP, for example, is making sure they accept complaints, adjudicate between different players, and impose fines.

Of course there is the flipside. What if the CCP rules unfairly? That is where judicial oversight comes in. If you have a complaint against a decision of the CCP, you just go to the courts.

Sounds like a pretty neat system, right? In theory, yes. But there is far more than meets the eye. Profit recently examined internal documents from the CCP. These documents showed that the Competition Commission of Pakistan is currently entangled in over 500 cases across different courts, all filed by companies seeking to challenge its orders or obstruct its investigations. According to sources within the CCP, these companies use high-powered legal teams to exploit procedural loopholes, with powerful cartels and major corporations systematically undermining Pakistan’s competition laws.

To hear them speak of it, it is a legal Kamikaze attack. By engaging in relentless legal tactics and procedural roadblocks, these market giants not only delay investigations but also continue to generate unjust profits at the expense of fair market competition and consumer welfare.

Of course, there are other issues. Last

year in September, Profit reported on how the CCP awoke from what seemed a deep slumber to deliver its first order in more than 18 months. The CCP normally ends up issuing at least a handful of orders every year. In the years preceding the interlude, the body issued between 8-11 orders annually. So it was strange when the CCP went missing in action from January 2023 to the 31st of July 2024. The month of August, however, has marked a bit of a resurgence. In the span of the month of August, the CCP issued three different orders finally breaking its dry spell.

There are clearly inefficiencies within Pakistan’s competition laws and how they are implemented. The CCP claims to have resolved over 70 cases out of the 500-plus pending in various courts, but it is striking how the country’s only body mandated to ensure fair competition remains hamstrung. To some extent, their complaint is true. The majority of companies it investigates or issues notices to simply resort to the courts and obtain stay orders, effectively stalling enforcement and evading accountability. But should the companies they regulate have no recourse to their decisions?

To understand this, Profit looks at three prominent and recent examples of legal recourse taken in response to decisions made by the CCP, and the industries these decisions affect.

The confectionary business

One example of a case languishing in the courts are the proceedings against SFML commenced in 2018 accusing the company of trademark infringement, deceptive marketing, and misleading packaging. Without getting into the technical points of what was happening, those filing the complaint included Ismail Industries Limited, Hilal Foods Limited, and English Biscuit Manufacturers (EBM) joined the complaint in 2019. The CCP, after extensive inquiries, issued showcause notices to SFML in June 2020.

Rather than responding substantively, SFML chose to challenge the Commission’s jurisdiction in the Lahore High Court, arguing that, post-18th Amendment, trade and industry fell under provincial purview. The legal battle dragged on, with the Lahore High Court eventually dismissing SFML’s jurisdictional challenge in May 2023. However, SFML has since filed appeals. Despite multiple court dismissals, the case, which started in 2018, remains unresolved.

Those filing the complaints in this case are not exactly small businesses.

The largest players in the market are English Biscuit Manufacturers (EBM) and Mondelez Pakistan. EBM is a homegrown company that has been around for the past five decades and has produced household brand names such as Peek Freans and Modelez is the international company that owns and operates Cadbury among many other brands.

Together, EBM and Mondelez rule over the market for chocolates, confectionery, biscuits, and sugary sweets in Pakistan, which is worth just over Rs 250 billion. Since the share of the biscuits market is the largest out of all the categories EBM is also the biggest company in this business, controlling over Rs 80 billion in total retail sales. Mondelez is fast on its heels with total retail sales worth just over Rs 70 billion. Together the two control nearly two-thirds of the total pie with net retail sales of Rs 150 billion. And while Mondelez and EBM have created brands that have brought them this success over the course of decades, there is one other competitor that is not far behind.

Founded in 1988, Ismail Industries is another local player in the sugar snacks, chocolates, biscuits and confectioneries market that has made a name for itself. Under this Candyland brand name, Ismail Industries have produced some or the most popular snacks in Pakistan including Cocomo and Chilli Milli – both of which are market leaders in their respective categories.

While they are behind EBM and Mondelez it is not by much. Ismail Industries in 2022 recorded gross retail sales of nearly Rs 60 billion, indicating they have a market share of nearly one quarter. What is perhaps even more surprising

With 200 cases pending in the Supreme Court, 179 in the CAT, 46 in the Sindh High Court, 43 in the Lahore High Court, and six in the Islamabad High Court, the volume of litigation continues to pose a major hurdle to effective enforcement

Dr. Kabir Ahmed Sindhu, Chairman CCP

is the rapid pace at which Ismail Industries has grown and the diversification they have shown in their business.

The case of SFML is an example where most of the industry has banded together against a player, possibly because of their overall practices. It creates a situation that can be difficult. One can see the frustration of the CCP with constant appeals, but that does fall within the rights of the appellant.

Carbonated drinks

Asimilar pattern of obstruction is evident in the case against Mezan Beverages (Private) Limited. The dispute began in 2018 when PepsiCo Pakistan filed a complaint against Mezan, accusing it of deceptive marketing by closely mimicking PepsiCo’s energy drink packaging.

The CCP initiated an inquiry and issued a notice to Mezan in September 2018. Instead of cooperating, Mezan challenged the CCP’s jurisdiction in the Lahore High Court in October 2018 and obtained a stay order. Even after the court dismissed Mezan’s petition in October 2020, the company continued to delay proceedings through appeals. To date, six years since the initial complaint, the matter remains unresolved, demonstrating how companies leverage legal avenues to stall enforcement.

Once again, this is a case very similar to that of SFML in the confectionery business. It is a small player with copyright issues against larger players. Remember, this is a situation where a large player is complaining about a much smaller player.

According to the latest market data analysis by Euromonitor, there were 1.329 billion litres of carbonated drinks sold in Pakistan in 2023. This includes all products by Coke Pakistan and Pepsico as well as local competitors such as

Gourmet Cola, Cola Next, Sufi, and others.

This is actually a rare year in which the overall sales volumes of carbonated drinks have fallen. In 2022, the total sales volume of carbonated drinks was 1.38 billion litres, which indicates a 4% decrease. What is interesting is that carbonated drinks have seen consistently increasing sales volumes (around 18% annually) in at least the last 15 years for which accurate data is available.

The leading company in this entire mix was Coke Pakistan, which sold nearly 567.5 million litres of carbonated drinks. The biggest component of this was 451 million litres of Coca Cola, which makes up around 80% of the overall sales that Coke Pakistan made in 2023. Of the remaining 20%, over 11% (around 68 million litres) was made up by sales of Sprite, and the remaining 9% was made up of their other products including Mirinda, Coca Cola Light, and Sprite Zero. Pepsico sold just over 528 million litres of carbonated drink, giving them a total market share of 39.2% compared to Coke’s 42.7%. The breakup of their sales shows that Pepsi was their hottest seller at around 70% of their total sales. Their second biggest seller was 7Up, which sold over 86 million litres making up 16% of their total sales. The remainder of the 14% of sales were made up by Fanta, Mountain Dew, Pepsi Black, and 7Up Sugar Free.

Honda Atlas Cars: Exploiting non-cooperation and court orders

Another example is Honda Atlas Cars (Pakistan) Limited, which has similarly exploited legal delays to evade accountability. The CCP launched an

inquiry into Honda Atlas in 2018 over allegations of consumer exploitation and unfair business practices. Initially, Honda Atlas cooperated, but later, in June 2023, it filed multiple petitions in the Lahore High Court, questioning the CCP’s jurisdiction and securing a stay order. Despite over 15 court hearings, progress has been repeatedly stalled due to the company’s legal maneuvers.

This is another example of a big player going to the courts against the CCP. In fact, in the aut sector of Pakistan, there was until very recently a very clear oligopoly.

In 1980, the government decided to start a partial privatization of PACO. Suzuki was the first company to jump into this market, leading to the creation of Pak Suzuki Motor Company, which initially had just a 12.5% stake from Suzuki, with the rest owned by the government. The company started off with the capacity to manufacture 45,000 cars a year by taking some of the plants owned by PACO. By 1990, PSMC built a new plant at Port Qasim, an industrial suburb of Karachi, which took production capacity up to 50,000 cars a year.

In 1992, the government decided to allow private sector companies to outright own auto companies in the country, and placed minimal localization requirements on them. As a result, Suzuki bought out a majority of PSMC, taking its eventual share up to 74%, which is where it stands today. That same year, Honda extended its partnership with Atlas Group, which had been its partner in motorcycles since 1962, to passenger cars and created Honda Atlas Cars.

And in 1993, Toyota partnered with the Habib family to create Indus Motor Company.

There were a cast of other companies that came and went. Ghandhara Industries partnered with Isuzu to make trucks, and with Nissan to make cars. Dewan Farooque Motors worked with Hyundai and Kia to make hatchbacks and sedans. None of them ended up mattering, at least through the late 2010s.

From the early 1990s, the Big Three – as they soon became – came to a tacit agreement. Suzuki kept its monopoly on the hatchback category and Honda and Toyota slugged it out for the sedans. If any new entrants came onto the market (and many tried), they were quickly sullied and sent packing.

In this way, for nearly three decades there were essentially only six options for locally assembled ‘family cars’ in Pakistan. Suzuki at any given time was assembling three to four hatchbacks, with mainstays including the Mehran, the Alto, and the Cultus. Meanwhile Honda produced its cheaper sedan the Honda City, and it’s more expensive competitor to the Toyota Corolla the Honda Civic. Toyota focused on making just one car, albeit in different variants with different engine sizes.

Car production and domestic sales kept

limping along at levels below 50,000 vehicles sold in the entire country per year until about the mid-2000s, when the Musharraf Administration’s privatization of banks resulting in the rapid expansion of consumer credit, and car loans became available en masse for the first time in Pakistani history. Car sales took off from under 70,000 in 2003 to nearly 185,000 in 2007, an astonishing pace of growth.

The 2008 financial crisis brought that lending to a halt, and with it came crashing down car sales to a mere 85,000 units in fiscal 2009. Sales slowly crawled back up as both the economy and lending recovered, but were then supercharged during the latter half of the Imran Khan Administration, which encouraged the central bank to loosen regulatory requirements for auto lending, which led to a record-breaking pace of sales.

Judicial guidance on regulatory proceedings

The Supreme Court and various High Courts have consistently ruled that companies should not seek judicial intervention until a regulatory body has concluded its proceedings and issued a final order. In CCP v. Dalda Foods, the Supreme Court of Pakistan upheld the Competition Commission’s authority, reaffirming that it is fully empowered to monitor markets, collect information, and conduct inquiries. Similarly, in Sadiq Poultry (Private) Limited v. CCP, the Lahore High Court ruled that show-cause notices are not adverse findings but opportunities for companies to respond. However, despite these legal precedents, there seems to be no real mechanism to avoid long drawn out legal battles. What the CCP really needs is an appellate system of their own. Of course, this does already exist. It is just defunct.

Competition Appellate Tribunal (CAT)

The dysfunction of the Competition Appellate Tribunal (CAT) further exacerbates the problem. Established under Section 43 of the Competition Act, 2010, the CAT is supposed to serve as the primary forum for appeals against CCP decisions. However, for 7.5 out of the past 10 years, the Tribunal has been largely non-functional, creating significant legal and procedural hurdles. With the CAT unable to hear cases, companies exploit this vacuum by filing challenges directly in High Courts, further stalling enforcement. Currently, 212 cases are pending before the Tribunal, while 140 petitions are pending in various High Courts. The federal government’s appointment of Justice

(Retd) Mazhar Alam Miankhel as Chairman in November 2023 was a step toward restoring CAT’s functionality. However, his subsequent elevation to the Supreme Court in June 2024 rendered the Tribunal ineffective once again. Despite these obstacles, the CCP claims that it has made notable progress in recent years. In 2024 alone, the Commission imposed Rs 27.5crores in penalties for cartelization, collusion, and deceptive marketing in key sectors, including paint manufacturing, pharmaceuticals, dairy products, and FMCG. It issued 32 show-cause notices for potential competition law violations in fertilizer, real estate, education, public procurement, pharmaceuticals, and FMCG. Additionally, it launched seven new inquiries into transportation, telecommunication, construction, and FMCG sectors, approved 64 merger applications, and granted 56 exemptions across various industries. The CCP’s Market Intelligence Unit identified over 125 instances of potential market manipulation, further underscoring the Commission’s commitment to enforcement despite legal roadblocks.

Chairman CCP, Dr. Kabir Ahmed Sindhu, acknowledged the challenges faced by the Commission. He noted that the restructuring of CCP’s legal team had led to the resolution of 73 cases, including 11 in the Supreme Court, 31 in the CAT, and others in various High Courts. However, he emphasized that a significant portion of the litigation backlog—567 cases involving Rs 74 billion in penalties—remains a pressing issue. With 200 cases pending in the Supreme Court, 179 in the CAT, 46 in the Sindh High Court, 43 in the Lahore High Court, and six in the Islamabad High Court, the volume of litigation continues to pose a major hurdle to effective enforcement.

A critical impediment remains the constitutional legitimacy of the Competition Act. Several companies have challenged the federal government’s authority to enforce competition laws across provinces, leading to a legal deadlock. The Lahore High Court has reserved its judgment on this matter since 2017, and successive hearings have yet to yield a definitive ruling. As a result, all companies penalized by the CCP have successfully obtained injunctions against its orders, further obstructing its enforcement powers. Without an operational Competition Appellate Tribunal and more efficient court processes, companies could possibly continue to exploit the system, undermining the CCP’s authority and weakening fair competition.

The need for reform is evident. Strengthening the CCP’s legal standing, ensuring the CAT’s functionality, and streamlining judicial procedures are crucial steps to uphold competition laws. Without these reforms, the persistent abuse of legal maneuvers will continue to shield corporations from accountability, harming consumers and distorting market competition in Pakistan. n

IIn Pakistan’s high-end hairstyling business, a not-so-new player makes a move

For 16 years, the Lebanese hairstylist Michael Kanaan has been running a small, secretive, super-selective, luxury salon. Why is he expanding to Lahore now?

By Nisma Riaz

n 2005, Michael Kanaan had just arrived in Pakistan. For a Lebanese hairstylist, it was more than just far away from home. It was a place he never would have expected to find himself.

That year, the Cedar Revolution was raging in his home country of Lebanon, where Syrian Occupation Forces had controlled the small Levantine state for nearly three decades.

At the time, Kanaan was working in the United Arab Emirates. Even in 2005, the UAE was a uniquely positioned market. Up and coming, Dubai in particular was the testing ground for a lot of individuals that wanted to make it big in the world of high-end fashion. For Kanaan, and many other designers and stylists like him from developing countries, the dream destination was New York, Paris, and Milan.

So what on earth brought him to Pakistan? Well, it was a bit of a coincidence. His work was noticed by a prominent person in the Hashoo Group, which owns Pearl Continental Hotels in Pakistan. At the time, the group was looking for someone to enter a partnership with them to run their in-house hair salon. The biggest competition to PC was Avari, particularly in Lahore and Karachi. Avari was also home

to Tariq Amin, one of Pakistan’s premier hair stylists. So when Michel was told he would be leading the way for a large five-star hotel chain in Pakistan, it was an offer he took up.

But the job was not exactly what he was expecting. The high-end salon industry in Pakistan was not exactly ‘with it’ at the time. On top of this, there were disagreements with the Hashoo Group itself. In particular Kanaan wanted to run his salon his own way, but the Hashoo Group seemed to see it less as a partnership of equals. After a three-year stint running salons at PC and Hotel One, Kanaan left. But he did not leave Pakistan. Why? According to him, he saw potential in the Pakistani market because it had a large population, an upper-class willing to spend on how they look, and a clear dearth of modern styling.

Just how true has this proven to be? Two-decades on and Kanaan is still very much in Pakistan. He has operated from Islamabad, shirking expansion, and focusing instead on providing high-end and high-margin services at fewer locations. That is until now. Kanaan, whose salon goes by the name Michael K, has opened an outlet in Lahore, stepping outside of its domain for the first time. But what does this mean for the very small and intense world of high-end salons in Pakistan?

Industry overview

Pakistan’s beauty and personal care industry has been experiencing significant growth, with projections indicating that the market will generate approximately $5.09 billion in revenue by 2025, reflecting an annual growth rate of 2.19% from 2025 to 2029. This expansion is driven by a burgeoning middle class, increased disposable incomes, and a rising number of women entering the workforce. Of course, these are numbers for the entire beauty industry, which includes makeup, skincare, and other products and services of this nature.

Getting an accurate estimate of the hair salon business and its scope is nearly impossible, unless you sit at beauty parlours all day and count the number of people walking in, note what services they avail and how much they pay for it. Still, your estimate would be inaccurate, considering that there are peak seasons, like Decemberistan, Eid and well another Eid, when the influx of customers is at a record high, and then there are slump seasons.

It is no secret that the beauty salon sector remains largely unregulated. As of 2017, only 40 beauty salons were registered with the Securities and Exchange Commission of Pa-

kistan (SECP), and approximately 287 salons were taxpayers in Punjab province, contributing about Rs 30 - 40 lakhs monthly. However, these figures likely underestimate the actual number of salons, as many small enterprises avoid registration to evade taxation.

In Lahore, between 2013 and 2015, only 100 beauty salons were registered, highlighting the challenges in obtaining accurate data due to the informal nature of many establishments. The lack of regulation has also led to labor issues, with reports of employees being overworked, underpaid, and denied basic rights.

Geographically, Punjab province hosts the majority of beauty parlors, accounting for 65.5% of the total, followed by Sindh with 20.06%, and Khyber Pakhtunkhwa with 6.06%.

Profit reached out to some of the most popular high-end salons in Lahore and Islamabad to get an estimate of the size of their clientele, only to be turned away.

The path less traveled

Kanaan established Michael K Salon in Islamabad in 2009. It would quickly come to be regarded as expensive, exclusive, and a bit of a secret. That is exactly as it was intended to be.

When Kanaan first arrived in Pakistan in 2005, the country’s high-end salon industry was still in its nascent stages and many of his peers were uncertain about the move.

“People were still using highlighting caps that had been outdated since 1975,” Kanaan recalled, highlighting the gap in the market for international-standard hair services. Kanaan was a young man when he first arrived in Pakistan. Speaking to Profit, he now sports a full head of silver hair. His voice is still full of vigour and passion for his craft.

In Pakistan, the path to making it in this business is pretty simple. You build your reputation through fashion week collaborations and celebrity clientele. Kanaan chose a different path. “We recently started being active on Instagram, but usually it’s only been word of mouth, just like a private club - someone has to refer you to come in,” he explained. This exclusive approach has helped maintain the salon’s high-end positioning and intimate atmosphere.

Quality over quantity?

While popular names like Tony&Guy and Nabila’s Salon have rapidly expanded, having multiple locations in Karachi and Lahore, Michael K Salon’s business model challenges the conventional wisdom of rapid expansion and high-volume services. With just 19 employees at its Islamabad location, the salon serves approximately 1,200 clients during peak months - a number that larger salons in the city might handle in

a single week. This deliberate limitation on volume allows for the personalised service that has become the salon’s hallmark.