Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Fauji Foods had its best year to date. Could it have been better?

The FMCG company earned its highest profits in 2024, but a deep dive shows the true nuances of these numbers

By Profit report

Less than a decade ago, the parent company of Nurpur Pakistan was taken over by Fauji Foundation and turned into Fauji Foods. What should have proven to be an easy turnaround turned into a long slog that needed to be bailed out and funded over and over again to stay afloat. After nearly a decade, it seems Fauji Foods is finally living up to its true potential. The last time the company saw a profit was when it was called Noon Pakistan and the logo was a rendition of the Hebrew letter for alif.

Just two years ago, the company registered a loss of Rs 2.2 billion and saw its accumulated losses reach Rs 18.5 billion. From those lows, Fauji Foods seems to have taken a turn for the better with two consecutive years of profits.

2023 closed out with profits of Rs 61 crores which was improved in 2024 to Rs 66 crores. With such a momentous change, it is clear to see that the company is on a path to recovery. But is this all there is to it? A detailed analysis of quarterly performance shows that the profits could have been better if it had continued on the path it was on back in September 2024. A spoiled opportunity, an impact of the boycott against the company or just luck. Whatever the reason maybe, the numbers show that the company could have had it so much better.

Noon Pakistan to Fauji Foods

In 1966, Noon Pakistan was set up by Manzoor Hayat Noon who developed the company under the brand name of Nurpur Pakistan. Over its history, the company was able to build on its product portfolio and profitability as it expanded into milk, butter, cheese, cream, and ghee. Even though the net profit margin for the company hovered between 1% to 3%, stable profits were being earned which kept accumulating the unappropriated profits for the company. However, things changed in 2013

when losses were seen of Rs. 13 crores. The company had crossed into the red before as well but this time the losses were here to stay. This was followed by a period of continued losses as the company tried to stabilize in tumultuous times. This was the situation in which Fauji Foundation acquired the company which had started to struggle. The management felt that they could turnaround the loss-making endeavour and bring back the days of its past back to the company. Initially, Fauji Fertilizer Bin Qasim and Fauji Foundation together bought around 70% of Noon Pakistan in order to take control of it. As soon as the acquisition was carried out, a need was felt that the operating efficiency of the company could be improved to lower input costs and boost production. Balancing, modernization and replacement (BMR) of Rs 7 billion was carried out which ended in 2018. Different financial initiatives were also carried out by injecting equity into the company which was used to support working capital needs. As the losses persisted, Fauji Bin Qasim put their money where their mouth was and in 2018 provided an additional Rs 3 billion to meet contractual obligations that were pending on Fauji Foods. Talks were being carried out with Inner Mongolia Yili Industrial Group, a Chinese company, which was interested in buying 51% shareholding from Bin Qasim.

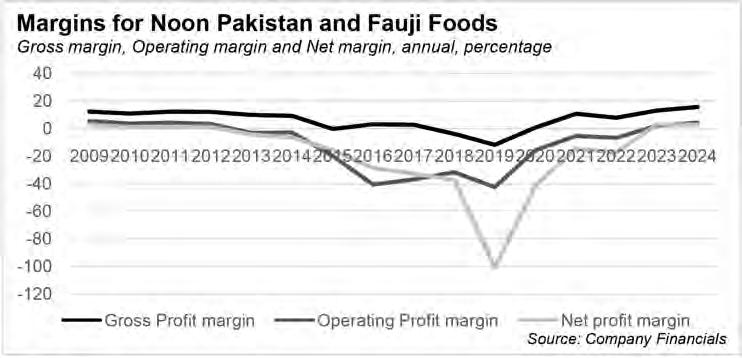

Much of these efforts failed to materialize in profits as the net profit margin fell from -6.5% in 2015 to 35.2% by the end of 2018. Accumulated profits had already turned to losses while Noon Pakistan existed in 2014 and by 2018 they were valued at Rs 6.5 billion under Fauji Foods. With no deal materializing between Inner Mongolia, the only solution to the problem was to keep throwing more money hoping that things would bounce back. By 2020, Bin Qasim pledged more support by providing Rs 3.5 billion to the company and an additional Rs 6 billion to the financial institutions to guarantee that Fauji Foods will come good on their loans. In terms of its financial performance, 2019 proved to be annus horribilis as the company saw a net profit margin of negative 100% which meant that the amount of sales was equal to the amount of net loss made. Even the gross profit margin was negative 12% which showed that the cost of sales was higher than the revenues earned by the company as well. Increasing losses also proved to be a cause of concern for many of the banks who approached the company to clear their liabilities as they saw the financial standing of the company deteriorating. A restructuring deal was negotiated between the syndicate of banks as Bin Qasim started to take a bigger role in terms of supporting Fauji Foods. Back in 2018, a line of Rs 6 billion was provided

by Bin Qasim which was given to meet working capital requirement needs. By 2020, almost all of these facilities had been used.

By 2022, the gross profit margin had gone back to the positive zone but Fauji Foods was still hemorrhaging money as it kept making losses. In 2022, a net profit of Rs 2.1 billion was made which brought accumulated losses to Rs 18.5 billion. Bin Qasim kept trying to prop up Fauji Foods as it pledged further equity injection of Rs 12 billion to allow the company to meet its borrowing needs, capital requirements, and commitment to financial institutions. Based on the loans given by the parent, much of these amounts were being turned into share capital to decrease the burden of liabilities and increase the ownership and control of Bin Qasim. There was a constant promise being made by the parent that they were looking to weather the storm.

Finally, the company turns profitable

The commitment of the parent finally seems to be coming off as Fauji recorded its first profits in more than a decade when it posted a profit of Rs 61 crores. All metrics of the company saw an improvement as the management was able to capitalize on expertise and experience to change its fate. After 2022, the company embarked on the philosophy that private sector enterprises need to be headed and run by individuals who have know-how in the field and can better execute the task at hand. Marketing, sales, and operational management were changed which was able to carry out a revolution within the company in a matter of one year.

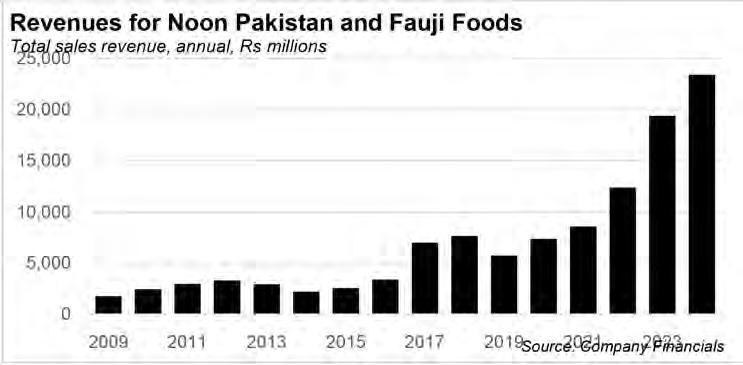

The new management was able to start by increasing sales from Rs 12 billion to Rs 20 billion from 2022 to 2023. While sales increased by 60%, the company saw its costs only increase by 48% leading to its gross profit margin almost doubling from 7.8% to 15% by 2023. While sales increased, its marketing and distribution expenses remained the same, and administrative expenses increased slightly. The impact of this was that what had been an operational loss of Rs 81 crore a year ago became an operational profit of Rs 94 crore in 2023.

The profitability saw an increase for 2023 even though the company created a provision of Rs 44 crore for sales tax levied on tea whiteners. Much of this provision was negated by the fact that the company was able to reduce its finance cost for long-term loans and short-term loans which decreased its finance cost from Rs 1.3 billion to Rs 32 crores in 2023.

The net results of all these elements was that the company saw a net profit of Rs 61 crores in 2023 which had been a loss of Rs 2.2 billion in 2022. The gross profit margin for the company has finally broken into positive double figures and it has registered a positive net

margin of 3% in more than 10 years. One of the biggest contributors to the profitability was the fact that Fauji got Rs 55 crores as a tax rebate for the losses that it had endured in the previous years. Fauji was able to use these losses and get these losses back which increased its profit before taxes from Rs 6 crores to Rs 61 crores.

Continued momentum

With the recent release of its 2024 financial results, it can be seen that the company is growing from strength to strength. In the past, the company was sliding downwards after seeing losses for consecutive years but now it seems that the slide has finally halted with 2024 being closed out with a profit of Rs 66 crores. For the first time in its history, Fauji Foods has registered sales revenue of more than Rs 23 billion. It seems like a far cry from the Rs 3.3 billion it registered in its first full year in 2016.

Sales have increased by around 20% year on year while its costs of sales have increased by only 17% in comparison. Due to this, the gross profit margin of the company has further improved to 15.74% from where it was 13.13% in 2023. Profit from operations have also seen a boost as the company has reduced its expected credit losses from Rs 9 crores to Rs 2 crores this year. Due to inflationary pressures, the marketing, distribution and administrative expenses have increased. Still, the company has been able to increase its profit from operations from Rs 41 crores in 2023 to Rs 1 billion in 2024. Due to all these contributions, the company made a profit before tax of Rs 1.1 billion in 2024 which had been Rs 6 crores in 2023. In 2024, the company also ended up giving income tax of Rs 41 crores which had been a tax rebate of Rs 55 crores in 2023. After considering tax, profit after tax of Rs 66 crores was earned in 2024 which had been Rs 61 crores in 2023. On the face of it, this is an amazing achievement considering that in 2022, losses of Rs 2.2 billion were being earned. It can be seen that the

management of the company has been able to carry out a revolution which has helped Fauji get back on its feet. Two consecutive years of profits show that the measures being put into place have started to work and reap benefits and that profits are slowly returning.

But could these results have been much better?

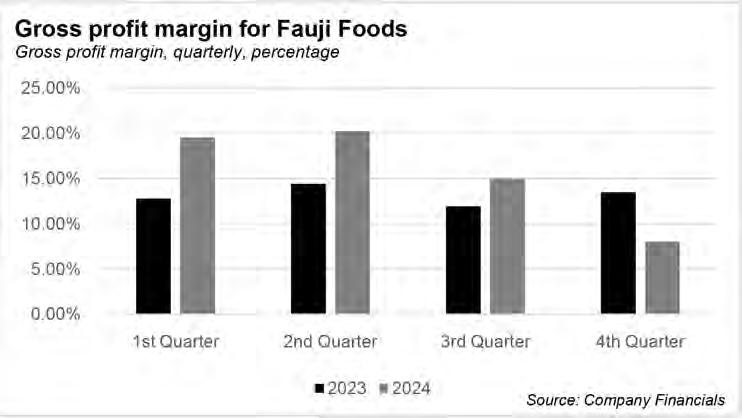

Breaking down the performance of the company quarter by quarter shows that Fauji was on a better trajectory back in September and results have gotten worse in the last quarter which have dampened the annual results to some extent. From January to September of 2023, the 9-month period saw sales of almost Rs 15 billion. For the same period in 2024, the company registered sales of Rs 18 billion. This shows that if sales had increased at the same rate of 20%, the yearly sales should have registered at Rs 23 billion which did take place. Things seem to be fine in that regard. The problems start to emerge when the gross profit margin is considered. For the 4 quarters of 2023, it was seen that gross profit margin fluctuated between 12% and 13.5% ending the year at 13% average on an annual basis.

In comparison to this, the gross profit margin for the three quarters of 2024 was 19.6%, 20%, 15%. The last quarter saw the margin fall to 8%. The sudden fall in the last quarter decreased the average of the whole year down to 16%. In the last quarter, sales of Rs 5.6 billion were made which cost the company Rs 5.1 billion leading to a gross profit of Rs 45 crores. The sudden fall in the gross profit margin can either be a sharp increase in the costs or a huge decrease in the price of the products. The question then becomes what happened in this period? Did cost increase to such a degree that it halved the gross profit margin in a matter of months?

It can be difficult to determine what took place in regards to the cost as companies do not release quarter-wise data on their volume

of sales. Volume and sales data for each quarter will allow a better analysis in terms of seeing whether the cost per unit increased during the quarter or whether the price per unit was cut. Companies operating in the same industry are namely Nestle, Prema, and FreislandCampina, and seeing their performance for the same quarter can show whether they saw a sudden increase between the last two quarters.

Another trend that was seen in this quarter was the boycott carried out of Fauji products with social media inundated with images of Fauji products being sold at discounted prices. Videos and images have flooded different social media platforms where stores and shops display the products being sold at lower prices compared to its competitors. This can also prove to be a contributing factor as a cut in selling price could lead to a lower gross profit margin being earned.

As gross profit margins fall, this is translated down the income statement as well. During 2023, the operating profit margin was between 1.4% and 3.8% for the company. The average margin closed at 2.11% at the end of the year. This year, the operating profit margin touched

8.3% and 9.7% in the first two quarters. In the 3rd quarter, it plummeted to 3.9% before becoming negative in the 4th quarter at -4.4%. The average for the year was still registered at 4.4%.

In terms of the net profit margin, the starting point in the first quarter of 2023 saw a net profit margin of -3.3% as the company was recovering from -5.2% in the last quarter of 2022. Over time net profit margin started to increase and closed out the last quarter at 17.9% bringing the average margin to 3%.

Throughout 2024, the net profit margin stayed positive and closed out at 2.8% at the end of the period. One of the sources of the profit in 2024 is coming from other income it has earned as markup for its investment in TDR and bank deposits. If that income is stripped away, it can be seen that net margin for 2023 falls from 3% to 1.9%. When the same is done for 2024, it is seen that the last quarter saw a negative net margin of -1.9%. Due to this decrease, net profit margin for the year goes from 2.8% with this income to 0.5% without this income being used to supplement the net profit.

The real reason behind this sudden fall in gross profit in the last two quarters and specifically the last quarter of 2024 needs to be understood. Whether it is the impact of the boycott being reflected in the accounts or it is the sharp rise in direct costs, the real reason needs to be identified and addressed.

Similar companies like Prema, Nestle, and FrieslandCampina can only be studied once their 4th quarter results are announced to see whether the cost of the whole industry has increased in lockstep with Fauji Foods as well. In case no such increase has been seen, the evidence will point towards the fact that the price of the product has been decreased which is eating into the gross margin. Results from the first quarter of 2025 will also give further credence to the boycott hypothesis once these are released as well. n

Smuggled vapes from China are poisoning Pakistan

Since BAT pulled their vaping product, Vuse, from the market, nearly all of the vapes being sold in Pakistan are illegally smuggled. With a criminally unregulated market to play around in, just how big is this business?

By Abdullah Niazi

On the weekend of February 7th, Lahore was hosting its annual Book Expo. Major publishers, bookstores, and importers had set up elaborate stalls at the Expo Centre in Johar Town. The largescale event is an annual mainstay for the city. But right next door, in halls 1 and 2 of the Expo Centre, a much larger exhibition was taking place.

This was the Vape Expo Pakistan 2025.

The scale of the event would have been more alarming if it had not been so comically caricaturish. Outside, long lines of men (many barely out of their teens) shuffled about to get inside, restlessly tapping their feet and fiddling with their phones. Inside, the air was thick with clouds of candy-scented vapor, pulsating neon lights, and the bass-heavy thump of a live concert. The hall floor was dotted with massive stalls from international vape brands. Some were offering free samples. Others were showcasing disposable vapes that double as a cellphone and a speaker. While virtually the entire crowd was men, all of the stalls were manned by young women in their early-twenties smartly dressed in brand attire. Many were university students trying to make some money on the side.

It was a spectacle of indulgence, a carnival of consumption, and a stark reminder of Pakistan’s unlikely status as a vaping haven.

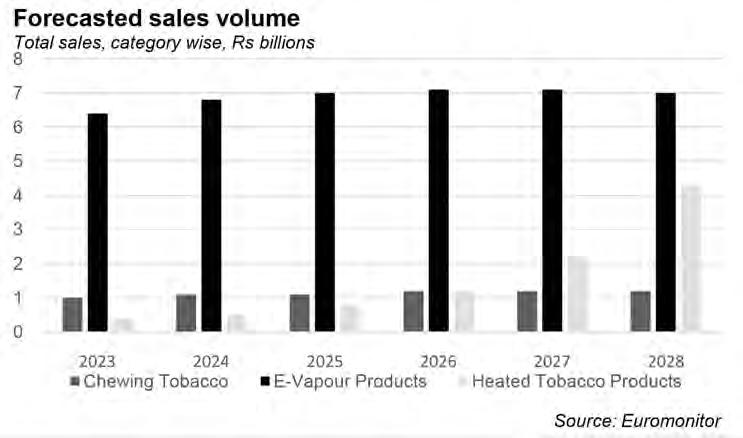

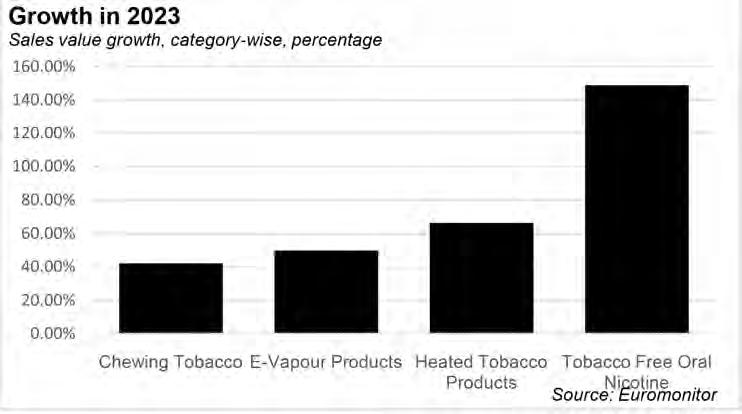

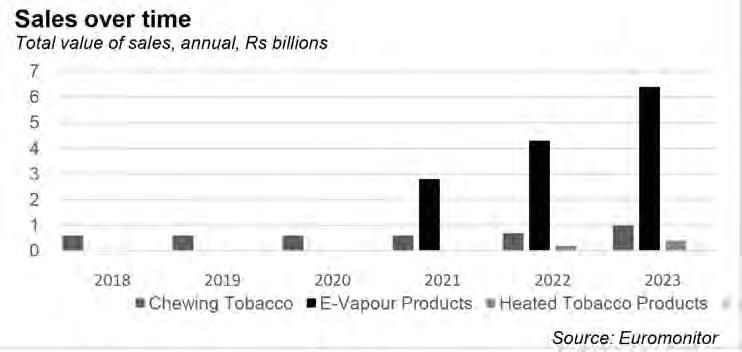

The sale of e-vapour products is a high-margin, high-volume business that has been growing fast. In the span of just three years, the sales of e-vapour products has more than doubled in Pakistan, growing from Rs 2.8 billion in retail sales in 2021, to over Rs 6.4 billion in 2023, which is when the latest data is available from.

Pakistan is a market that checks all of the boxes for the vape industry. It has a young population, a laissez-faire approach towards health regulations, and bribeable customs officials. Perhaps most importantly, the country shares a border and very strong trade ties with China, which is the global leader in vape manufacturing, making more than 90% of the world’s e-cigarettes and e-vapour products.

It is a fact that was painfully obvious at the Vape Expo in Lahore. The event venue was surrounded by sharply dressed police commandos of the Punjab Police’s Elite Force. Nearly all of the stalls had Chinese nationals present, and as per government regulations, all of them needed a police escort.

As the world grapples with the health implications of vaping, Pakistan has emerged as an unlikely haven for an industry under siege. From the United States to Europe, and even in China—where the majority of these devices are produced—governments are moving to ban or heavily regulate vaping, citing its appeal to youth and uncertain long-term health effects. Yet, in Pakistan, the vape industry is flourishing, unimpeded by the kind of oversight that has become commonplace elsewhere.

This raises a pressing question: Why has Pakistan, a country already burdened by public health challenges, become a fertile ground for an industry that much of the world is rushing to control? The answer, it seems, lies in a regulatory vacuum—one that has allowed vaping to thrive even as its risks remain poorly understood.

But beyond the lack of health regulations, something more insidious is happening in Pakistan’s vaping industry. As of 2024, virtually all of the vapes that are being sold in Pakistan have been illegally smuggled into the country free of taxes. It is a fact manufacturers, distributors, and retailers alike admitted with surprising candour at the event. It was painfully clear that the absence of regulation is not just an oversight; it is an invitation. And for an industry facing increasing scrutiny elsewhere, that invitation is too lucrative to ignore. The clouds of vapor may seem harmless, but the stakes are anything but.

Understanding the business

John Moriarty has been in the vape industry for more than 15 years. A big burly Englishman with a thick accent and an easy way about him, Moriarty was manning possibly the only stall at the Vape Expo in Lahore that was not directly selling vapes or other e-vapour products. Mr Moriarty works for Chubby Gorilla, a California based company with a presence in the Netherlands and manufacturing facilities in China’s Zhejiang province, where they produce patented plastic containers for nicotine pouches and e-vapour liquid.

Chubby Gorilla’s business model is simple. They have patented products that have special child safety features embedded in them. They sell their plastic bottles to vape manufacturers which package their products in these bottles and sell them all over the world. Vapes, or e-cigarettes, were invented in China by a pharmacist in 2003. The structure of a vape is very simple. There is a device with a battery, a coil, and space for an oily liquid that contains nicotine. The battery heats up the coil which turns the liquid into vapour which is then inhaled. Originally designed as a product to help people quit smoking, vapes have become a distinct category in and of themselves over time.

With options for fruity flavours and scents, vapes have become popular globally amongst younger audiences, giving them an alternative entry into the addictive nature of nicotine. Vaping devices can either be disposable, which means you buy them, use them and throw them away, or one can buy a device and keep refilling it with vape ‘juice’. Mr Moriarty’s company produces the bottles for this juice. According to him, Pakistan is a market that is currently an open playing field.

“The best thing about Pakistan for my business is that vaping is completely legal. We manufacture in China and sell directly to vape producers there. My goal for being here is to show consumers our safety logo so they buy vapes that are packaged in our bottles,” he

explains. Moriarty feels that the market has developed enough in Pakistan that consumers are becoming more conscious of what kind of products they prefer. “All over the world demand for vapes has fallen because of restrictions. There is no such thing in Pakistan. You can market your product, sell it, or open a retail store. It is beautiful for business. The only problem is Pakistani Customs because you have to pay them off every time.”

This was an overarching topic of conversation at the expo. Beyond the sensory overload of plumes of sickeningly sweet vapour and the resonance of the concert, serious business was taking place. Behind the main hall guarded by heavy security and characterised by neon lights, a small passageway leads to another hall, nearly as large as the first one but not nearly as loud. In fact, the voices here were hushed. Instead of elaborate stalls, small meeting rooms and sitting spaces were crafted here. There were also cabins that had been erected to create closed off rooms. This is where distributors, importers, retailers, and manufacturers were making deals — and the conversations were breathtakingly shocking.

The market is bigger than anyone thinks (or knows)

“Demand has been increasing, which is why we want to diversify with the number of brands we import, not just keep increasing the quantity of the brands we are already bringing in,” says Sunny. Middle-aged, dressed in a sports coat, slacks, and funky socks he smiles genially at us through his square framed glasses. He does not look like he imports and distributes vapes all over Pakistan. He also does not look like a Sunny — that is just the nickname he asks us to use

for him.

“Some people that have been working with me for years know Sunny is a family nickname. I do not want to be identified by my own name, but the people in the industry will recognise me by this name.” When asked whether he is afraid people from the industry will recognise him and confront him about it he laughs. “They have no interest in revealing my identity to other people, or the authorities, or anyone else because they are involved in the same things I am involved in. This is just how business is done.”

As he leans back in a chair at the event’s business lounge, he has a pack of cigarettes right in front of him on the table next to his phone, wallet, and keys. “I don’t really get the hype about vaping. I have been a smoker for most of my life and nothing really changes that but vapes are good for business, and the market has been growing.”

Sunny is a distributor in Pakistan’s e-vapour supply chain. He has relationships with manufacturers in China where he places orders for vapes which are then purchased directly from China and brought into Pakistan. He then sells these vapes to the countless vape shops dotted all over major cities in the country, at khokhas, and at stores and petrol pump convenience stores. It is a rapidly growing market, and distributors are having a hard time keeping up with the massive demand.

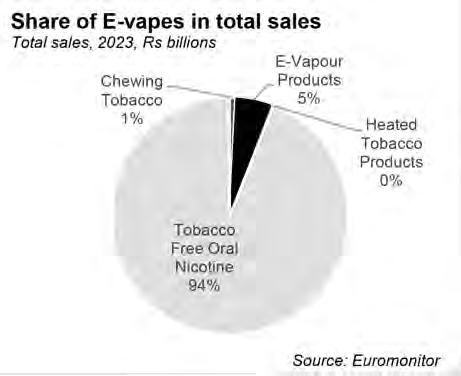

According to a report by Euromonitor, retail sales of e-vapour products, including kits, liquids, and disposable devices, had retail sales worth Rs 6.4 billion by the end of 2023. This was up 50% from 2022 when it was Rs 4.3 billion. The year before that total sales were worth Rs 2.8 billion. In terms of volume, the growth has not been as large, indicating that the rise in revenue might have to do more with rising prices and inflation. However, volumes did grow from 1.5 million units to nearly 2.5 million units according to the Euromonitor re-

port. What is perhaps more significant is that rechargeable closed vaping systems, what are known in the market as ‘pods’ saw a volume increase of more than 60%.

In terms of more anecdotal evidence, there has been a very clear proliferation of vape stores in major cities. In Model Town Lahore, a small residential area, their central C-Block market that spans a radius of barely 200 meters has seven different vape retail stores. The more surprising thing is that these stores sell only vapes, not even cigarettes, whilst most tobacco stores have started selling vapes as well. Similarly, you can even find vapes at traditional khokhas now.

All of this indicates vaping habits are fast growing in Pakistan, since pods are used by regular vapers compared to disposable or single use devices. On top of this, these numbers are vastly under reported. One individual in the tobacco industry, not the vaping industry but with some important insights available, told Profit there were a lot more vapes coming into Pakistan than recorded, and that most of them were smuggled into the country.

It is a fact corroborated by Sunny as well as a number of manufacturers and importers. As of 2023, the biggest brand of vapes coming into Pakistan is VGOD Inc, which is based out of Shenzhen and has a retail share of 20%. Other brands such as Acme, RELX, and more than four other companies with Shenzhen in their names making a wide range of brand names make up most of the rest of this pie. One major Pakistani retailer is Artisan Vapor, which has a 1.5% share in the market and imports their own products as well. At the Vape Expo, there were many new brands present looking to enter the Pakistani market because of its WildWest attitude towards regulating this growing industry.

Yalla, a UAE based company, is selling vapes with Middle Eastern branding. They have introduced hookah and paan flavours as well as Oudh smelling vapes. Angel and Ghost, brands based in the UK, are also trying to introduce a vast range of products. Asmodus

and Silvaper are some of the new brands from China trying to bring flashy products such as vapes that double as speakers and cellphones. Other names include Vome, Romio, and Geekbar. All of these brands have their unique marketing styles, but they are all produced in China, almost exclusively in the Shenzhen province. It does not really matter whether a company is British, Middle Eastern, or from somewhere else — they are getting their products from China 90% of the time. Since Chinese vapes are cheap, all of the ones coming into Pakistan are Chinese in origin.

“We do not care particularly what retail price you set eventually, we just want someone that can buy the product from us and take care of customs” says a representative for one of these brands in a meeting with Sunny that this correspondent sat in on. This kind of concern was a common theme from vape brands. Some have in the past attempted to import these products directly into Pakistan but have found taxation is high and customs is corrupt. “All I know is I am selling products to you, and it is your job to get it to the market and sell it at a profit.” E-Vapour products are currently the subject of both sales tax and Federal Excise Duty (FED). The FED on vapes is around Rs 10,000 per kilogram of products, or 65% of the retail price — whichever one is higher. This FED is steep. Vapes are already an expensive product. Cigarettes are very cheap, the only reason they have become unaffordable in Pakistan is taxation, and if the same taxation applies to vapes, they are definitely not a cost effective replacement for cigarettes.

“If you look at the prices of vape liquids, they are often cheaper than cigarettes. I smoke imported brands for example, and a pack costs me Rs 800. Now, I smoke a pack a day. Meanwhile, for a user like me, a vape liquid bottle can last me 3-5

days depending on my use, sometimes even a week. If this costs Rs 3500, I might in certain weeks be better off vaping” explains Sunny. But the prices for vaping products are this cheap mostly because they do not include tax.

“This is just part of the business. Many of the people in the industry consider smuggling halal because they believe in the free trade of goods. Most people import some portions legally to have receipts, and larger quantities are brought in illegally,” explains Sunny. “Of course I import legally,” he says with a chuckle. All of the people at the expo Profit spoke to were tight-lipped about how they did this, even though the fact of the smuggling was an open secret. This correspondent even posed as a potential buyer in front of some manufacturers and importers, but they did not divulge any details. The general impression, however, was that most of these vapes are brought into Pakistan by bribing government officials. Back in 2023, a major raid on a warehouse in Karachi by Pakistan Customs had seized Rs 9 crore in smuggled vapes. While Customs has been trying to curb this smuggling, there are clearly chinks in place that allow the continued import and sale of smuggled vapes. Perhaps nothing is more indicative of this than the fact that these brands from China have managed to beat back one of the largest and most well-known companies in the world: British American Tobacco (BAT).

Big enough to beat Goliath

One name missing at the Pakistan Vape Expo was Vuse. They had no stall, no representative, and no presence at all. This was surprising considering Vuse is the global vaping brand operated by British American Tobacco (BAT), which is the second largest tobacco company in the world and one of the largest companies in the world. In Pakistan, BAT is the owner of

the Pakistan Tobacco Company (PTC), which launched Vuse brand vapes in Pakistan in late 2023. Vuse, which has its main production facility in Malaysia, was entering Pakistan as the first major vape brand from outside China. It was a stark admission on the part of the tobacco industry that vaping was a growing market, and they would have to address demand for alternative nicotine products. It is also when they introduced Velo, and eventually Zyn was also introduced by Philip Morris Pakistan.

When it first came out, Vuse made quite a splash. PTC marketed the product, used its wide distribution network to spread it everywhere, and introduced a number of different kinds of products, pricing them low compared to some of the products already available in the market. However, PTC was in for a run for its money.

Large companies like PTC are obliged to pay tax. In fact, the disproportionate amount of tax they pay is a major bone of contention in the tobacco industry. According to one individual well placed in the tobacco industry, nearly 78 billion sticks of cigarettes are sold in Pakistan annually, and revenues for 2023-24 were close to Rs 300 billion. However, a large part of this market is illicit. According to some estimates, the legitimate market of recorded and taxed cigarettes is around 48%, and the remaining is around 52%. Large tobacco companies like PTC and Philip Morris claim that despite not having that big of a market share, they pay nearly all of the tax. This is because local cigarette manufacturers, particularly based in KP, grow their own tobacco, make their own products, and sell them at cheaper rates without paying taxes. This issue has continued to grow as taxation has risen.

During the financial year 2022/2023, excise rates saw an unprecedented increase of more than 200% in both tiers. The market share of the legitimate sector dropped from 63% in 2022 to 42% in 2024 and is expected to decline further if the situation remains unchanged. During the same period, illicit share increased from 37% to 58%.

Of course, the cigarette market is unique from the vape segment. However, the issue of taxation remains the same. There is no regulation governing vapes in Pakistan. In fact, most vape shops and vape producers do not sell to anyone under the age of 18. Even at the Vape Expo, there were stringent identity checks to make sure no one underage managed to get into the exp. However, other than in KP where there is a law dictating a minimum age to buy vapes, companies do not sell to minors voluntarily and out of fear that if they do, their activities will come out into the open.

In the 2024-25 budget, FED was imposed on vapes at the rate of Rs 10,000 per kilogram or Rs 6500 per unit, whichever is higher. This was a big problem for Vuse. Since they were

a large multinational, PTC had to make sure their tax receipts were clean and paid. It is the same issue they face with the cigarette market. Over time Vuse could not compete with Chinese vapes. These were cheaper, came in higher volumes, and because of smuggling they were cheaper given they were not paying the correct FED, or were only paying a small portion of the FED compared to the volume of e-vapour products they were bringing in.

As a result, PTC had to discontinue its Vuse line of vapes. For all intents and purposes, a sea of cheap Chinese vapes, most of them smuggled, manage to run one of the largest tobacco companies in the world out of the Pakistani market.

“Currently there is no law in place to regulate new category products. Voluntary Modern Oral and Vapour E-Liquid standards have been issued by the Pakistan Standards and Quality Control Authority (PSQCA). FED also exists on vapour e-liquids however a majority of the products available are not paying the correct excise duties,” says our source in the tobacco industry, summing up the issue.

When it comes to cigarettes, multinationals have faced the same problem in Pakistan. Their products are more expensive because they are taxed. These companies actually devote quite a lot of resources towards encouraging taxation and compliance, especially through track-and-trace. In the case of cigarettes, at least, these companies had an early mover advantage and have been mainstays in Pakistan’s tobacco industry. In the case of vapes, Chinese companies were early movers and are the bigger players. In front of them and with the burden of taxation, they were really no match to the flood of vapes coming into Pakistan from China.

Regulatory winter

There are bigger problems than taxation. The recent vape expo in Lahore was a flashy affair, a sign of an industry ready to explode. Companies

from around the world descended on the city, eager to tap into Pakistan’s unregulated and rapidly growing market. But behind the sleek designs and flavored vapor lies a troubling reality: the global vape industry is under fire, and Pakistan is walking into the storm without a plan.

Most of the world’s vapes are made in China, but even they’ve hit the brakes. Flavors—cherry, mango, cotton candy—are banned, seen as a gateway for kids. Online sales are restricted. Other countries, from India to Brazil, have gone further, outlawing vapes entirely. The reason? Health. Vaping isn’t the harmless alternative it’s often sold as. It’s packed with nicotine, formaldehyde, and other toxins linked to lung damage, heart issues, and addiction. The World Health Organization has sounded the alarm, but in Pakistan, the market is booming, fueled by smuggled products and a lack of rules.

Here’s the problem: Pakistan has no regulations for vaping. None. Taxes exist, but they’re easily dodged. Vapes are everywhere—in shops, online, even in the hands of teenagers. And while the industry sees dollar signs, the health risks are being ignored. Vaping isn’t just a trend; it’s a public health gamble. The long-term effects are still unknown, but the early signs are worrying. Respiratory problems, addiction, and a new generation hooked on nicotine are just the beginning. The global response has been clear: regulate or ban. Pakistan needs to decide. Do we wait for a full-blown health crisis, or do we act now? Banning flavors, restricting sales to minors, and enforcing strict import controls would be a start. But more than that, we need research. How is vaping affecting Pakistanis? What’s in the products being sold here? These are questions that can’t be answered by glossy expo booths or clever marketing. The vape industry sees Pakistan as a golden opportunity. But without regulation, that opportunity could come at a steep cost. The smoke is rising, and it’s time to clear the air. n

The economics of skimpy clothes in Pakistan

The target audience of Landa bazaars is evolving, thanks to culturally deviant consumer demands that the formal sector fails to fulfill

By Nisma Riaz

The landa bazaar, or as we call it here in Karachi, Sunday bazaar, is not for the faint of heart. If you can’t weaponize your elbows to make your way into the market, you will be left behind panting and hyperventilating. But amidst this chaos, overwhelming enough to make a grown man cry, is a sea of tables, stalls and sections scattered with all things imaginable to man, from clothes, shoes, jewelry and makeup to

curtains, rugs, crockery and even appliances.

On the other side of Clifton, near Teen Talwar, a similar commotion is seen outside small shops displaying mini dresses, skirts, sparkly party tops, swimsuits, bralettes and all manner of other clothes. This is Karachi Playhouse, a market of preloved clothes and accessories and the ultimate goldmine for a party girl’s dream wardrobe.

And somewhere in the middle of these two markets, hovering above the sea and the city, stands Dolmen Mall Clifton. Exactly 23 steps into the mall and you’re greeted by Lama,

a high-street, multi-fashion brand that claims to combine functional design with popular fashion: a Zara inspired outlet that has grown significantly over most major cities in the country. A smaller but quite similar group of women are seen strolling through the store, lazily sifting through the racks, sometimes stopping to feel the soft linen fabric between three fingers and turning over collars to eye the price tags dangling by a black thread.

And those who aren’t seen at any of these scenes, are sitting at home, scrolling incessantly on their phones, jumping from one online

thrift shop to another Instagram thrift page.

But who are these women, hurriedly making their way through these markets, unstoppable unless something catches their keen eye? These are women, who otherwise wouldn’t be caught dead walking on the streets of Karachi, out in search of new clothes and determined to crush anyone who comes in their way. These same women are also master hagglers, trained by none other than their expert haggler mothers.

This is a story about buying a particular kind of clothing in Pakistan. We are talking about Western clothing, particularly for women. Over time, especially over the past decade, locally manufactured western clothing options for women have grown in Pakistan. They have grown because the demand for them has increased ever since women have become a larger part of the workforce. But the outlets manufacturing these clothes have restrictions. By their own accounts, they often have to self-censor the kind of clothes they produce and put on sale out of the fear of moral outrage. Yes, many players try to push boundaries, but they are aware of the delicate disposition of most mobs. That means while they do not make tube tops, and tank tops, and halter tops, and shorts, and mini bodycon dresses, and miniskirts, and the list goes on.

That does not mean you cannot find them in Pakistan. Despite the vague restrictions on women’s clothing in Pakistan, there is still an appetite for Western fashion; even the so-called “haram”, “skimpy” and “inappropriate” kind.

Against all odds, the landa bazaar has become the major hub for these clothes. More importantly, there is a growing trend of young, enterprising women with a keen eye for clothes going to the landa, finding the best products there, bringing them home and selling them at a profit on Instagram. These women often wash, model, photograph, market, and ship these clothes themselves out of college dorm rooms. Pages specialise in all kinds of things from clothes, to shoes, to intimates, to t-shirts, accessories, and yes, clothes you would not otherwise find in a store in Pakistan. Access to all kinds of clothing has never been easier. It means you no longer have to go on a trip or beg your cousin in the UK to bring you these things.

Whether these clothes are being worn at a party, to work, at home, or on a trip abroad they are inching their way into the mainstream. What was once reserved for the underground is now creeping into the public eye, challenging sartorial boundaries one crop top at a time.

With global fast fashion giants like Zara, H&M, and Forever 21, considered budget-friendly abroad, remain out of reach

for most Pakistanis, thanks to punishing exchange rates and a lack of local stores, and local brands trying to balance what is and isn’t socially permissible, this alternative ecosystem is thriving.

Profit explores Pakistan’s evolving fashion landscape, mapping out the formal and informal sectors shaping the industry. From locally produced ‘quiet luxury’ pieces to the underground thrift market keeping rebellious wardrobes alive, we take a closer look at where the demand for Western and ‘immodest’ fashion is coming from and just how far brands are willing to push the envelope before hitting a cultural wall.

Who is going to wear it?

If you have ever gone shopping with your mother, you have probably heard the phrase, “Who wears this?!” followed by, “Where would you even wear that to?” and finally, “Taubah, itna behuda. Isse behtar kuch na hi pehno!”

But who wears these clothes?

The potential market for western clothing in Pakistan can be primarily traced through the country’s urban, educated, and professionally active female population. Not the entirety of this population of course, but still a significant fraction of it.

According to the Pakistan Bureau of Statistics’ 2023 Labor Force Survey, women’s labor force participation in urban areas stood at 11.9%, representing approximately 32 lakh women in the formal workforce across major cities. Educational institutions, particularly universities, serve as significant drivers of changing fashion trends. Higher Education Commission data shows that female enrollment in tertiary education has reached 46% of total enrollment, with about 2.1 million women pursuing higher education in urban areas. Cities like Karachi, Lahore, and Islamabad host the highest concentrations, with women comprising over 50% of the student body in many private universities.

The target demographic becomes clearer when examining income brackets. The Pakistan Social and Living Standards Measurement Survey indicates that approximately 22% of urban households fall into the middle and upper-middle-income brackets (monthly household income exceeding PKR 150,000). Within this segment, women aged 18-35 from these households, particularly those employed in corporate sectors or pursuing higher education, form the core market for western clothing.

Key urban centers reveal distinct patterns. Karachi, the country’s largest city, has an estimated 1.2 million women in the workforce, with 35% employed in the services sector where western business attire is increasingly

accepted. The city’s universities host approximately 4 lakh female students.

Lahore follows with roughly 8 lakh working women, with a notable concentration in its growing IT and creative industries. The city’s educational institutions enroll about 3.5 lakh female students, with private universities showing particular openness to contemporary fashion.

Islamabad-Rawalpindi, despite its smaller size, shows the highest per capita representation of working women in modern sectors, with approximately 4 lakh women in government, diplomatic, and corporate roles where western attire is common.

Secondary cities like Faisalabad, Peshawar, and Multan collectively account for another 8 lakh working women and roughly 4.5 lakh female students in higher education, though cultural constraints may be stronger in these regions.

This data suggests a core market of approximately 25 lakh urban women who regularly participate in settings where western clothing is acceptable or even required, with an additional 30 lakh who might occasionally seek such clothing for specific events or purposes. The market potential grows further when considering the multiplier effect of social media influence and changing cultural norms among the younger generation.

However, it’s crucial to note that this market remains sensitive to both economic and social factors. While the demand exists, accessibility is often constrained by both pricing, due to import costs and currency devaluation, and social acceptability, leading to the rise of alternative channels like thrift markets and local adaptations of western styles.

The economics of Landa Bazaars

The demand is clearly there. So whatever your purpose might be, the clothes are available. You just need to find them.

Inside a road facing shop at Playhouse, with all sorts of ‘inappropriate’ clothes displayed for passersby and those driving by to see, we picked out a mesh top. No sleeves or waist or anything. Just a piece of see through net fabric, cutout in the shape of a toddler’s shirt. When asked whether anyone would buy it, the shopkeeper who maintained their anonymity told Profit, Of course it would sell. If it comes to Pakistan, it will be sold in Pakistan and some will surely wear it.”

He revealed that they get ‘all sorts of stock’ in Western wear and it all clears out. “We get all categories of customers too.”

When asked if he has ever seen anyone wear the skimpy clothes he sells and where he saw them, he said without even a hint

of judgement, “Our job is to source and sell clothes. It is not our business as to why or where women wear these clothes, that is their private matter. But obviously we see people wearing shorts and bras at the beach and in other places in Pakistan.”

If you want to buy a cute crocheted crop top and a pair of light linen shorts for your friend’s laid back intimate birthday party at French beach, you can’t just walk into a shop at Dolmen and find it. You need to turn the entire landa bazaar inside out to find that little knitted top some white girl in America thought she was donating to the needy. And if you do not want to go through the hassle, you scroll through the many online thrift stores on Instagram.

The landa bazaar is an interesting place.

It offers a peek into the global fashion arbitrage, where one man’s discarded Ralph Lauren shirt becomes another’s prized possession. These markets, thriving on second-hand clothing from the West, operate through a complex international supply chain that begins in the donation bins of developed nations and ends in the wardrobes of Pakistani consumers.

The journey begins in countries like the United States, England, Australia, Japan, and South Korea, where charitable organisations collect donated clothing. Consider a scenario where the Goodwill Foundation receives a brand-new Burberry shirt during a clothes drive in Boston. While donors might assume their contributions will be shipped directly to those in need, the reality is quite different. Charitable organizations, overwhelmed by the volume of donations, sell these clothes in bulk at minimal prices, often just a few dollars per kilogram.

After being sold by weight, these thrifted clothes retailers sift through the clothes, and separate torn or useless items. are recycled and used again as things like insulation materials, and soiled garments end up in landfill or incinerated. The more in-shape items end up going to flea markets within the home country, but the vast majority of the entire bulk is exported to sub-Saharan Africa and Asia, where they dominate local market stalls.

The supply chain operates with remarkable efficiency. Pakistani expats in countries like the UK operate warehouses where they execute a methodical sorting process. First, they categorise items by type; pants, shirts, shoes, etc. Then, each category is further sorted by quality and brand. The premium items are sold to local thrift stores in those countries, while the rest are fumigated, which causes the notorious ‘landa smell’ you notice immediately at Sunday Bazaar. These donated clothes are then bundled, and shipped to countries like Pakistan. The scale is massive, Britain alone exports 351 million kilograms of clothes annually, equivalent to 2.9 billion T-shirts, with Pakistan being among the top five destinations

alongside Poland, Ghana, Ukraine, and Benin.

The market for this is massive. An earlier mentioned report in The Guardian estimated that globally the wholesale used clothing trade is valued at more than £2.8 billion. It is a textbook example of arbitrage, an economic concept in which an asset is bought in one market where its value is lower, and sold in another market where the value of that product is higher without any value addition. Donated clothes are sold dirt cheap in developed countries, but since they are not readily available to low-income families in the third world, their value is higher in that market. Arbitrage is essentially a risk-free way of making money by exploiting the difference between the price of a given good on two different markets.

An earlier Profit article cracked the economics of the landa bazaar and the results are staggering. A Ralph Lauren shirt that originally retailed for $110 (approximately Rs 31,000) in the US might end up in a Lahore flea market for Rs 1,000-1,500 ($4-5). This dramatic price differential forms the backbone of the landa bazaar economy. According to the Pakistan Bureau of Statistics, the country’s appetite for used clothing is substantial. During fiscal year 2020-21, imports surged by 90% to $309.56 million, weighing in at 732,623 metric tonnes. The following year saw even more growth, with Pakistan importing 186,299 metric tonnes of pre-used garments just in the first two months of FY 2021-22, marking a 283% increase over the same period the previous year. According to a report by the Pakistan Business Council (PBC), despite a sharp decline in textile imports, Pakistan imported 277,721 metric tonnes of worn clothing between July to September of fiscal year 2024-25.

The business model is particularly intriguing at the local level. Bulk importers bring containers worth millions of dollars to Pakistan. Local merchants then purchase these containers sight unseen, a gamble that almost always pays off due to the extremely low acquisition costs. As Shams Khan, a veteran landa dealer from Peshawar, explains, “Be it an importer of pre-used clothes, a wholesaler, a shopkeeper or a wheelbarrow, no one has ever lost in this business.”

The mathematics is compelling. A 60-kilogram bundle of ‘B category’ clothes costs around Rs 36,000 at Rs 500-600 per kilogram. For t-shirts, this translates to approximately 1,200-1,800 pieces, as it takes 18-20 t-shirts to make one kilogram. After sorting, about 500-600 shirts might be in near-new condition, selling for Rs 300-500 each. Even selling these premium pieces at wholesale rates of Rs 150 per shirt generates Rs 75,000, while the remaining lower-quality items can fetch another Rs 50,000 when sold to smaller vendors. However, 2023 brought a significant

shift with the government imposing a 300% import duty on used clothing. As Usman Farooqui, General Secretary of Pakistan Second Hand Merchants Association, explains, “A container of Landa clothes that previously cost Rs 700,000 now costs Rs 2.7 million.” This change has disrupted the traditional export patterns. Pakistan typically re-exports high-quality pieces to countries like Turkey, Afghanistan, and India. According to Faisal Memon, a Karachi-based import-export manager with two decades of experience, many importers delayed clearing their containers, hoping for tax reductions, leading to supply shortages.

Despite these blocks, landa bazaars are thriving. Not just due to the rising demand for worn designer clothing, but also the rise of Instagram landas.

The landa bazaar ecosystem exemplifies the perfect intersection of global charity, international trade, and local enterprise. It’s a system that transforms Western excess into affordable fashion for Pakistan’s masses while creating business opportunities at every level. Despite recent regulatory challenges, the market continues to evolve, finding new channels and customers, proving that in the world of fashion arbitrage, one person’s castoff truly is another’s treasure.

The landa goes online

There used to be a time when not everyone was privy to the wonders of thrifting. Then came young entrepreneurs, particularly women students from institutions like IBA, who decided to revolutionise the landa business model. They navigate the flea markets, select premium branded items, clean and photograph them professionally, and market them as ‘pre-loved’ or ‘rescued’ fashion on social media. This approach particularly appeals to college students who want designer labels but can’t afford retail prices, as well as middle and upper-middle-class consumers who desire branded clothing but either lacked the patience to sift through piles or were simply too shy to be seen at a traditional landa bazaars.

As the market for second-hand clothing evolves, one group stands to benefit the most; Instagram thrift stores. While importers, shopkeepers, and budget-conscious shoppers brace for rising prices, savvy entrepreneurs have found a way to turn landa fashion into a thriving business. It is hard to say whether they are a part of the formal or informal retail sector, we can say with surety that they are largely unregulated. Therefore, getting away with selling clothes that local brands would shy away from. Once the go-to for low-income buyers and students on a budget, landa markets have recently attracted a new customer base: young, fashion-forward individuals who

see value in branded, second-hand clothes. These thrift-savvy buyers, mostly women, have transformed bargain hunting into a business model, sourcing clothes in bulk, sprucing them up, and reselling them online under the guise of sustainable fashion.

For students at elite universities, where designer labels serve as status symbols, thrifted Western wear provides an affordable alternative. While middle and upper-middle-class buyers may balk at the idea of scouring a crowded flea market, they have no problem purchasing “pre-loved” finds from a well-curated Instagram store, especially when the clothes are styled and photographed to perfection.

The economics of it are simple. A crop top that lands in the flea market for Rs 200 may sell for Rs 500 on-site, but an Instagram thrift store can flip the same item for Rs 2,000, sometimes within minutes. As prices continue to climb in the landa, shoppers will likely opt for a Rs 2,000 branded thrift store piece over an Rs 800 off-the-rack find.

Today, we see thrift pages and Instagram accounts dedicated to second hand commodities, categorised into shoes, bags and clothes, displaying labels as big as Prada, Coach, Kate Spade, Micheal Kors and even Gucci.

With their understanding of demand, branding, and pricing, Instagram thrift store owners are perfectly positioned to capitalise on the growing market for second-hand fashion. And with new containers of imported clothes soon to hit the landa, this could be their biggest year yet.

However, there is a catch. For those who shop at landa bazaars not particularly to find Western ‘immodest’ clothes, but for its affordability are suffering. Sellers at landa, taking note of Instagram sellers, who buy from them and sell the same items at a markup have driven landa sellers to spike their prices.

A designer’s dilemma

What other options does a girl have?

Well, there is a formal sector of fashion retail, working endlessly to give consumers what they want.

Of course, with international fast fashion giants like Shein, AliExpress and Temu taking over the world, thrift markets are not the only place to find cheap, trendy clothes. But you have to stay patient. If you can’t wait for two months for your Shein packages to arrive, or you’re too preppy to set foot into a flea market, but can’t afford to travel abroad and shop at Forever 21, you will have to settle for our local brands.

But will you find a sparkly bralette to go with your silk shirt at a local Western wear brand?

Most probably, not.

Local fashion brands in Pakistan face a unique conundrum. Balancing the growing demand for Western wear with the rigid expectations of a conservative society. While there is a clear market for tank tops, short dresses, and body-hugging silhouettes, brands must constantly navigate the fine line between pushing boundaries and avoiding backlash.

“There’s multiple facets to that,” explained Wasay Hasan, Director at Lulusar and Koyo . “There’s one in the design element, there’s one in the marketing aspect, then your physical presence and your digital presence. These are all factors we have to consider.”

Unlike Instagram thrift stores, which operate in a gray area with minimal oversight, formal brands are under constant scrutiny. “We try not to hold ourselves back just because we are in Pakistan,” Hasan said, adding. “At the end of the day, there are so many brands over here making clothes for international markets, yet within Pakistan, we still have to be careful about what we put on display.”

Despite wanting to cater to the consumers’ demands, when asked whether cultural norms dictate the creative process of designing clothes, Hasan admitted that they do face a certain degree of self-censoring. “Yeah, I won’t lie, it’s tough. It’s not easy. But my personality is such that I try my best not to care about what people say. As long as I believe something is ethically and morally right, then no one should have the power to dictate what I can or can’t do.”

Regardless, businesses remain cautious, with designs that flirt with inappropriateness (by Pakistani standards) but just modest enough to avoid backlash.

On occasions when their designs were a bit too daring for the supposed Pakistani market, Hasan recalls receiving backlash, “It’s a mix of both perspectives. It’s definitely not for the faint-hearted. You get messages, some unpleasant things, but at the end of the day, if you’re reasonable and educated, you can remind yourself that what you’re doing isn’t what others may assume. I understand that we’re an Islamic state but if people don’t see the bigger picture, they may not recognise that, as a company, we’re trying to shed light on an industry with immense potential here,” adding, “Beyond that, there’s also a clear demand for it.”

One way brands manage this is through strategic modifications, such as adding sleeves to a tank top or adjusting hemlines. Even so, some designs remain controversial. “We had these bralettes we came up with, and I wasn’t going to tell the designers not to do it because it’s not accepted here. The demand is there. People want it.” The only reason Hasan would want to say no to a design would be because it was ugly, rather than being dictated by what’s considered to be acceptable or not.

The problem, however, isn’t just societal backlash, it’s also economic. While

international buyers may pay a premium for high-quality fashion made in Pakistan, local consumers often balk at similar prices for homegrown brands. “If I am a buyer, I go to Dubai and I see all these stores, I would be willing to pay. When a local brand tries to offer the same thing, I personally, the same buyer, would hate that price tag,” a responded and self-diagnosed shopaholic, who wishes to remain anonymous, told Profit, unknowing that even her frilly Zara top was probably stitched somewhere in a Pakistani factory. This discrepancy forces brands to find a middle ground. Some position themselves as premium yet attainable, mimicking the pricing of high-street brands like Massimo Dutti or COS. Others rely on limited releases, ensuring exclusivity while justifying a higher price point. “We strategically place ourselves in the middle,” explained Hasan. “Why? Because technically we’re trying to enter a gray area that no one entered.”

Despite these efforts, cultural resistance remains a hurdle. Brands receive backlash not only from conservative consumers but also from authorities who may deem certain designs inappropriate for public retail. “You get messages, you get all sorts of stuff that isn’t pleasant,” Hasan said. “But at the end of the day, if you know within reason that what you’re doing is not what people think you’re doing, then that’s for them to worry about.”

We asked Hasan whether brands like Koyo consider the informal clothing market to be their competitors, he said, “No, we actually encourage it. Why? Because at the end of the day, if it proves there’s a market for such clothes and people are willing to pay that price, it only reinforces that the demand is real. Whether you scale it up or down, the market exists.” Hinting, how businesses can innovate, according to consumer demands, even when they are made apparent in an informal sector such as the landa bazaar.

“That aligns with our perspective that Western is still in an experimental phase. Or, you could say that with more brands entering the space, it’s becoming increasingly accepted by the people,” he concluded.

As Gen Z gains purchasing power and social norms shift, the landscape is expected to change. “The young Gen Zs have now come to fruit, and I think they’re more dominant in the population,” Hasan observed. “They’re going to get their way at one point.” But until then, the formal sector must continue its tightrope walk, adapting just enough to cater to demand, without tipping over into controversy.

Will there ever be a day, when local brands can proudly display outfits that look like lingerie, the way thrift market and online resellers do? Perhaps. But will there ever be a day when brands can compete with thrifting prices? Perhaps, not. n

How is KTrade redefining investment in the capital markets of Pakistan

Fintech technologies, a fresh set of strategies, and the legacy of reverence for the investment powerhouse

KASB

Securities, all coming together to expand

Pakistan’s capital markets

Partner Content

The Pakistan Stock Exchange (PSX) achieved an impressive return of 86% in dollar terms during 2024, yet it remains critically underutilized. With only 357,419 registered accounts, a mere 0.3% of the population over 20 has a trading account—a stark reflection of the market's limited penetration.

This low investor participation stems from multiple barriers: widespread financial illiteracy, deep-rooted distrust in financial intermediaries, and limited market accessibility. Enter KTrade, a potential solution to these systemic challenges.

KTrade was launched in April 2018 under the leadership of Ali Farid Khwaja and Mahmood Bukhari, where it aimed to democratize capital markets by empowering retail investors and serve as a conduit between global investors and growth companies in Pakistan. The enterprise has since emerged as one of Pakistan's fastest-growing brokerage firms, rapidly expanding its account base and challenging traditional market dynamics.

However, KTrade's meteoric rise

prompts a critical question: How did this fintech startup transform the investment landscape where others have struggled?

The origins of KTrade (formerly KASB Securities)

The younger generation of professionals became familiar with KTrade during the VC funding boom of 2021–22 in Pakistan when the company raised $5 million from leading venture capital firms. Investors included HOF Capital and Mentors Fund from the US, as well as angel investors such as TTB Partners from Hong Kong, Shorooq Partners from the UAE, Zayn VC from Pakistan, and Dragonstone Capital from China. Several prominent individuals also participated in the round, including Waleed Saigol, the management of Careem, Haider Chaudhry, Simon Chisholm, David Mortlock, Sardar Durrani, and Omar Shah (co-founder of COLABS). However, KTrade’s roots trace back decades to 1952, when Khadim Ali Shah Bukhari founded KASB Securities. Despite being a novice in the trade at the time, Mr. Bukhari rapidly

grew the company by building a strong and loyal customer base, serving both individual and institutional investors. His sharp business acumen and exceptional relationship-building skills helped KASB Securities gain prominence. By the 1970s, both Bukhari and the firm had become household names in Pakistan’s brokerage industry, earning widespread respect from key stakeholders.

In the 1980s, when Nasir, Mr. Bukhari’s son, overtook the business, he pushed the company towards modernization by transitioning from a sole proprietorship to a public company, while in the 1990s, he publicly listed the company and established a partnership with Merrill Lynch. The company also became one of the pioneers to introduce electronic trading in the country, ushering in a new era for the brokerage industry in Pakistan.

KASB Securities emerged as a pioneer in digital brokerage, introducing online trading platforms that allowed retail investors to execute trades through websites, desktop software, and eventually mobile apps. This innovative approach propelled KASB to become the largest retail brokerage in Pakistan, leading in both investor numbers and trading volume. However, the company's trajectory took a

dramatic turn when its parent company, KASB Bank, was auctioned to Bank Islami Pakistan Limited by the State Bank due to capitalization issues, resulting in its merger and rebranding as BIPL Securities in 2014. Prior to the merger, KASB had built an impressive customer base of 22,000 and controlled a 15% share of overall

trading on the Karachi Stock Exchange.

The merger marked the beginning of a decline. BIPL Securities struggled to maintain the operational excellence that had defined KASB, failing to replicate its predecessor's market approach. Consequently, thousands of customers abandoned the firm, and those who remained

significantly reduced their trading volumes. This demand gap meant that there was an opportunity up for grabs. Ali Farid Khwaja, along with the youngest generation of the Bukhari family, latched onto this opportunity to relaunch KTrade, drawing inspiration from the heaps of wisdom embedded within the rich

legacy of KASB Securities.

KTrade, darling of the retail segment

KTrade has developed a forte in extending equity research and brokerage services through leveraging financial technology. However, the company also offers services related to domains like corporate finance. Moreover, it has established divisions for money market and commodity futures trading as well. The head office of KTrade, situated in Karachi, serves as its nerve center; however, it has several branches spread across cities like Lahore, Islamabad, and Multan.

Although KTrade, ever since its rebirth in 2018, has managed to claw its way back into both retail and institutional customer segments, its primary focus remains the retail segment.

If we consider the retail investors in Pakistan, they are apprehensive of investing in the stock market due to their diabolical experiences with prop trading and substandard services of brokerage institutions. Furthermore, there is a dearth of financial awareness among the majority of the population in Pakistan, which compels them to invest in asset classes like real estate and savings accounts,

exacerbating the situation overall.

However, KTrade realized the significance of the participation of retail investors in the growth of the stock market and capital markets overall.

Hence, KTrade has developed a chic app equipped with a sleek user interface that can be comprehended intuitively and used effortlessly, creating a seamless experience for users. The app has been downloaded more than a million times, with a 4.2 out of 5 rating on Google Play Store—the highest rating and most downloads for a capital markets-related app in Pakistan.

The growing footprint of KTrade among institutions

Nevertheless, the success story of KTrade isn’t restricted to retail investors as it has had a profound impact in the arena of institutional clients as well. KTrade has assisted several venerated companies like Mughal Steel in raising capital and facilitated IPOs of upcoming companies like Big Bird. Moreover, the company has another six IPO deals lined up, which will be disclosed by the management in due time. KTrade also has a strategic equity

trading partner in the form of Jefferies Group, one of the veterans of the investment banking industry in the US.

KTrade’s Strategic Initiatives and Recognition

KTrade is a mission-driven company rather than merely profit-driven. Hence, it reinvests the majority of its profits to realize its goals. It believes that bountiful profits will follow once it fulfills its ambition of ensuring widespread participation in financial markets from retail investors and serving as a bridge between global investors in search of alpha (α) and growth companies in Pakistan, promoting robust and sustainable growth in the country.

KTrade as a financial entity has expanded beyond the domain of a traditional brokerage institution, delving into an eclectic set of spheres to spread financial literacy and augment the common man’s access to capital markets. Its future plans entail offering a comprehensive suite of investment products including ETFs, mutual funds, and personalized portfolio management through robo-advisory platforms, solidifying KTrade as the paragon of ingenuity revolutionizing investment in Pakistan's capital markets. n

Driven by upper middle class recovery, auto sales surge 61%

Larger vehicles appear to have recovered sales numbers faster than smaller ones, suggesting the economic recovery has hit the well off and upper middle class first

Profit Report

Pakistan’s automobile industry is witnessing a rebound in sales, with a marked shift in consumer preference toward larger, more premium vehicles. The robust growth in auto sales, particularly in the upper middle-class segment, signals not only a recovering economy but also changing lifestyles and rising consumer confidence among the more affluent segments of society.

Recent figures reveal that automobile sales in January 2025 reached approximately 17,010 units—a staggering 61% year-on-year (YoY) increase and an even more impressive 73% month-on-month (MoM) surge. This upswing, which mirrors the performance last seen in December 2022, has been attributed to a confluence of factors including the new year

buying effect, a decline in interest rates that has rendered auto financing more accessible, and a reduction in inflation, which has bolstered consumer purchasing power across the board.

What is particularly striking about the latest data is the growing appetite for larger vehicles—a trend that underscores the economic resurgence among Pakistan’s upper middle class. Larger vehicles such as the Toyota Fortuner, Toyota Hilux, and Toyota Corolla Cross are not only commanding impressive sales numbers but are also indicative of shifting consumer priorities. Buyers are now prioritizing enhanced safety, advanced features, and superior comfort, factors that are often associated with larger and more expensive models. This shift is a stark contrast to the previously dominant trend of smaller, more

economical cars that catered primarily to the lower and middle-income groups.

Analysts at Arif Habib Ltd, including Muhammad Abrar and Menka Kirpalani, have noted that the strong performance in larger segments is a clear signal that the benefits of the country’s economic recovery are being felt more acutely by those higher up the income spectrum.

Indus Motors Company Ltd (INDU) reported an impressive 102% MoM increase in volumetric sales in January 2025. This surge was largely driven by a significant 86% MoM increase in sales of models such as the Toyota Corolla, Yaris, and the increasingly popular Corolla Cross. Notably, sales of the Toyota Fortuner and Hilux surged by 138% MoM, underscoring the growing demand for larger, high-end vehicles. These models, renowned

for their performance, durability, and premium features, have resonated well with buyers who are looking for both style and substance.

Similarly, Honda Atlas Cars (HCAR) showcased robust performance with overall sales in January 2025 increasing by 99% MoM, culminating in 2,210 units sold. The iconic Honda Civic and City models were particularly popular, experiencing a 105% MoM rise in sales, with 1,985 units sold. Additionally, Honda’s HRV/BRV segment saw a 61% MoM increase, reaching 225 units in sales. The rising demand for these vehicles is reflective of a broader trend where consumers are gravitating toward models that offer a blend of performance, comfort, and advanced technology.

Pak Suzuki Motor Company (PSMC) also contributed significantly to the market’s buoyant performance, with a 32% MoM increase in overall sales, maintaining a robust figure of 7,794 units. Particularly noteworthy was the exceptional performance of the PSMC Every, which recorded a fourfold increase in sales compared to the previous month. Moreover, other popular models in the Suzuki lineup, including the Swift, Cultus, Alto, Bolan, and Wagon R, experienced healthy MoM growth rates of 59%, 48%, 22%, 18%, and 10% respectively.

The latest report also highlights that Sazgar Engineering Works Ltd (SAZEW) reported total sales of 1,995 units for its Haval models over December 2024 and January 2025. Although these figures reflect combined data from two months, they are indicative of a growing appetite for newer variants and innovative models in the market.

Several macroeconomic factors have converged to create a favorable environment for auto sales in Pakistan. One of the most significant influences has been the decline in interest rates, which has made auto financing considerably more accessible to consumers. Lower borrowing costs have effectively broadened the pool of potential buyers, enabling even those who were previously hesitant to take on substantial loans to consider purchasing a vehicle. This development has been a critical catalyst for the overall sales increase observed in January 2025.

In addition to lower interest rates, the easing of inflationary pressures has also played a pivotal role in bolstering consumer confidence. With the cost of living stabilizing, households now have more disposable income to allocate toward major purchases such as automobiles. This newfound financial flexibility has spurred a wave of buying activity, particularly among the upper middle class, who are now in a position to upgrade to larger, more feature-rich vehicles.

The new year buying effect—a phe-

nomenon where consumers rush to complete purchases before the year’s end or take advantage of special New Year offers—has also contributed to the spike in sales. This trend is particularly evident in the January figures, where the low base effect of December sales combined with pent-up demand has resulted in a dramatic month-on-month increase.

One of the most compelling narratives emerging from the latest sales data is the pronounced preference for larger vehicles. Historically, the Pakistani market has been characterized by a predominance of smaller, budget-friendly cars designed for mass-market consumption. However, recent trends indicate a significant shift in consumer behavior, with an increasing number of buyers opting for larger models that offer enhanced performance, greater comfort, and a suite of advanced technological features.

For instance, the Toyota Fortuner—a model that has long been associated with luxury and performance—has experienced a phenomenal 138% MoM increase in sales. This SUV, known for its spacious interior, robust engine, and off-road capabilities, has become a symbol of status and affluence among Pakistan’s rising upper middle class. Similarly, the Toyota Hilux, a rugged pickup truck favored for its durability and reliability, has also recorded a significant surge in sales. These models are no longer seen merely as transportation solutions; they have evolved into lifestyle statements, reflecting the aspirations of a growing demographic that values quality and prestige.

The growing preference for larger vehicles can also be seen in the performance of models from other manufacturers. Honda’s Civic and City, while traditionally positioned as compact sedans, have been updated with more luxurious interiors and advanced safety features, making them attractive to a higher-income clientele. The HRV/BRV variants, with their elevated driving position and additional space, further cater to the needs of families and professionals who demand both comfort and functionality in their vehicles.

The impressive sales figures for larger vehicles have not only lifted the overall performance of the auto industry but have also had a ripple effect on related segments. For instance, the two-wheeler segment recorded a 13% MoM increase in January 2025, with Atlas Honda achieving sales of 115,557 units—a 15% MoM increase. Although two-wheelers have traditionally been an entry point for many consumers, the concurrent rise in larger vehicle sales underscores the broader economic recovery and the diversification of consumer preferences.

Conversely, the tractor segment experienced a notable decline, with sales plunging

by 61% MoM to 2,761 units. The drop was primarily due to a significant 50% MoM decline in sales from MTL and an 82% MoM decrease for AGTL, attributed to the high base effect and the distribution of tractors under the Punjab government's Green Tractor Scheme in the previous month. This divergence in performance between different segments of the automotive industry highlights the varied impact of macroeconomic factors on consumer purchasing behavior.