09 Ufone’s troubles are indeed the government’s problem

Interloop’s road ahead

16 The rise of Pakistan’s tech services exports

23 What is Tania Aidrus’ Dbank up to now?

28 Disrupt.com announces $100mn investment to fuel startups globally

29 Pakistan’s cashback startup Savyour to completely shutter operations

32 With interest dwindling, does Pakistan have a climate funding plan?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Ufone’s troubles are indeed the government’s problem

As the state-owned telecom operator hemorrhages money, the government deliberately looks away

By Ahtasam Ahmad and Hamza Aurangzeb

At the heart of sound corporate governance lies a fundamental principle: a company’s management bears a fiduciary responsibility to act in the best interests of its shareholders. But what happens when those shareholders appear indifferent to massive financial losses?

This troubling scenario is unfolding with Ufone, Pakistan’s state owned telecom operator. Earlier this month, headlines quoted the IT Minister claiming that “Ufone losses are not the government’s concern.” Her rationale? Management control of Pakistan Telecommunication Limited (PTCL) and its subsidiary Ufone rests with Etisalat (now rebranded as E&), absolving the government of responsibility for the mounting losses.

This position seems strikingly at odds with financial reality. The government remains PTCL Group’s majority shareholder with approximately 62% ownership. Far from being insulated, public finances have absorbed significant damage. The Group’s losses, primarily driven by Ufone, have resulted in negative cash flows of approximately Rs. 15 billion over the past two fiscal years, according to the latest State Owned Enterprises (SOE) report from the Ministry of Finance.

To understand this apparent contradiction between ownership and accountability, we must examine the complex story of Pakistan’s state-owned mobile operator in detail.

A brief history of Ufone

After more than a decade of inception of the mobile industry in Pakistan and the success of Mobilink, PTCL decided to enter the sphere in 2001 by launching its brand, Pakistan Telecommunications Mobile Ltd.

(PTML), popularly known as Ufone. It began operations by capturing market share at an unprecedented rate, so much so that by 2006, it controlled 21.7% of cellular subscribers and 17.9% of the industry’s revenue, merely five years after its launch.

As the telecom market expanded further, more players emerged. During the era from 2004 to 2008, three more companies launched their operations in the country, which included Telenor, a Norwegian telecom corporation; Warid, a nascent telecom company established by Abu Dhabi’s ruling Nahyan family, and Zong that was backed by the China Mobile group based out of Beijing, China. This marked the beginning of an era of cutthroat competition in the telecom industry which lasted for a decade. The period witnessed five companies competing with another to cement their place in the market. However, despite intense competition, Ufone managed to remain in the middle of the lot, swaying between the second or the third spot throughout the era.

Ufone’s downfall and role of 4G spectrum auction

Throughout its existence, Ufone has displayed mixed financial performance. From 2003 to 2011, despite the entrance of new telecom companies, it held its ground and posted robust financial results. At its peak in 2011, Ufone had a market share of 21% of the industry’s revenue, where its revenue grew from 2.7 billion in 2003 to 60.5 billion in 2011 at a CAGR of 47.5%. The company’s topline grew at a much faster pace than the overall size of the cellular market, which grew from 19.8 billion in 2003 to 263 billion in 2011 at a rate of 38.2% annually. However, Ufone’s revenues stagnated afterwards and the company never witnessed a major boost in its revenues until 2023. The topline expanded at a sluggish rate of 0.9% per annum between 2011 and 2022, while the

industry as a whole grew at a rate of 6.0% per annum. As of 2024, Ufone’s market share has gone down to 13.5% from its peak of 21% in 2011.

So what exactly happened? Well, the competition eventually got the better of Ufone, it started to falter after 2011 but the situation exacerbated post 2014, when the government decided to auction four 3G and two 4G licenses to telecommunication companies. Initially, it was believed that the four mobile companies would just opt for the basic 3G license, except Warid for whom it was not financially feasible. However, Zong caught the whole telecom industry by surprise, when it acquired the 4G license in addition to the 3G license by spending a mammoth $517 million, while Telenor, Mobilink, and Ufone only secured 3G licences.

Since Zong was effectively the only mobile company with a 4G license, it devised a strategy of offering cost-effective packages to customers, which although resulted in a lower ARPU than peers but allowed it to gain greater market share albeit by compromising on profit margins. Warid followed suit and launched its own 3G and 4G services with the help of its technology neutral license, however, it was no match to Zong.

This ushered in a new era for Zong, where it racked up market share, coercing other major players like Mobilink and Telenor to obtain 4G licences the next time the government auctioned them in 2016. Nevertheless, Ufone remained the only company, which refused to transition to the 4G technology and it cost the company big time. Imagine, Zong snatched revenue of Rs. 8.9 billion from its competitors in 2015, Rs. 6 billion of that came from the books of Ufone.

Ufone became the only company to not offer 4G services until 2019. It only launched its 4G services in August 2019 with the approval of the government but without formally acquiring a 4G license. However, this initiative proved to be too little too late as the damage had already been done when Zong rampaged the entire telecom industry and shrunk market

shares of its peers.

The era of high leverage and the current state of financials

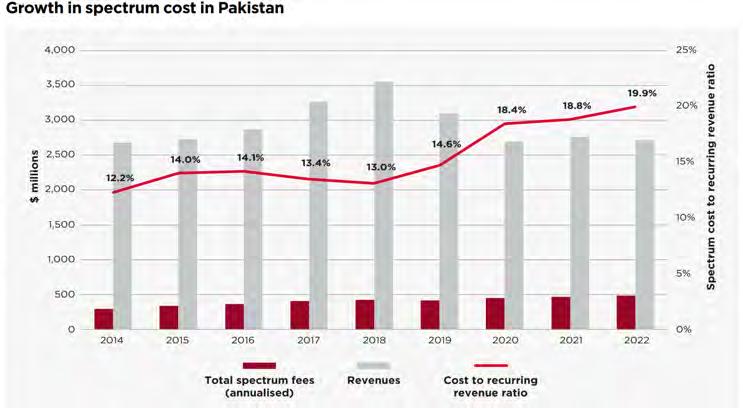

In 2021, Ufone made a bold strategic pivot, securing its largest syndicated loan to expand 4G offerings and acquire spectrum for $279 million. However, this debt-heavy approach coincided with Pakistan’s unexpected interest rate spiral, which saw policy rates peak in 2023 at 22% for nearly a year.

This timing proved financially devastating for the operator. According to GSMA analysis, spectrum costs as a proportion of recurring revenue for Pakistani mobile operators nearly doubled, rising from 11% in 2014 to 20% in 2022. This escalating cost structure has become increasingly unsustainable, threatening the future development of mobile services across the industry. As operator revenue per MHz continues to decline, the bandwidth required to meet customer demand keeps growing.

For Ufone specifically, these challenges converged simultaneously. Despite successfully

shifting its revenue mix between 2021 and 2024 (data revenue increased from 28% to 46%, while voice revenue decreased from 53% to 34%), operational costs outpaced this growth. Combined with the crushing burden of financing costs, this revenue transformation failed to translate into profitability, leaving the company facing a prolonged path to financial recovery.

Further analysis reveals Ufone’s troubled financial position, with parent company PTCL injecting approximately Rs. 60 billion in equity between 2020 and 2023 primarily financed through debt on PTCL’s own books.

The state-owned cellular operator’s leverage problems have become critical. According to Ufone’s latest credit rating report, its gearing and leverage ratios have deteriorated dramatically due to persistent losses that continue to erode equity despite frequent parent company injections. By the end of 2023, gearing reached 10.95x while leverage climbed to 31.4x. More alarmingly, by mid-2024, these ratios skyrocketed to 68.6x and 206.2x respectively, indicating a rapidly worsening financial position.

The severity of these losses prompted the Ministry of Finance to address the issue specifically in its latest SOE report. The analysis highlighted how PTCL Group’s struggles

(primarily driven by Ufone) stem from a significant debt burden and resulting high finance costs that consume substantial cash flow.

This financial strain severely limits the company’s ability to invest in operational improvements, fund essential infrastructure upgrades, remain competitive, and build financial reserves. This dangerous cycle increases Ufone’s vulnerability in an already competitive and economically volatile telecommunications environment, as customers increasingly migrate to providers offering more advanced technology and superior services.

The Telenor acquisition, a necessity in the face of adversity

Despite current financial challenges, Ufone may have a transformative opportunity on the horizon. The pending Telenor acquisition, though still awaiting regulatory approval, could dramatically reverse Ufone’s fortunes through substantial operational synergies.

Telenor’s financial performance has been remarkable, generating approximately Rs. 24 billion in operating profit on a Rs. 100 billion revenue base in 2024. With an impressive 18% return on capital.

PTCL has negotiated the acquisition at roughly $400 million (Rs. 108 billion), a multiple of just 4.5x earnings that market analysts widely consider a bargain.

The value proposition becomes even more compelling when compared to recent industry benchmarks. Consider the recent Engro acquisition of Deodar (Jazz’s tower business): $565 million for 10,500 towers, establishing a market rate of $53,590 per tower. Applying this valuation standard to Telenor’s infrastructure of approximately 7,500 towers yields an estimated tower asset value of $402 million.

This comparison reveals the extraordinary nature of PTCL’s deal: they’ve secured Telenor’s entire operation including spectrum, customer base, brand equity, and operational infrastructure for essentially the same price as its tower assets alone. This remarkable valuation appears to stem primarily from Telenor’s strategic urgency to exit the Pakistani market, potentially positioning Ufone for a significant upside if regulators greenlight the acquisition.

However, significant risk persists as the acquisition relies on additional dollar-denominated debt from the International Finance Corporation (IFC). This precarious financing structure leaves the group vulnerable, where any substantial interest rate spikes or currency devaluation could prove catastrophic. n

Source: GSMA

Interloop’s road ahead

As the economy sees stability, there can be choppy waters ahead for the hosiery behemoth

By Zain Naeem

Apiece of barren land. Sand, dust and grit gently blowing over. Lack of moisture and rain has made it immune and incapable of growing or supporting life. Is it the fault of the land that it has become that way or does the blame lie with the conditions that surround it? Welcome to the corporate dessert. With a lack of infrastructure and development

opportunities, it is the skill and talent alone that is able to produce giants that dot Pakistan’s corporate ecosystem.

In a world of Tatas, Ambanis and Adanis, there is a perception that the entrepreneurial spirit in Pakistan is something that has failed to materialize. This perception is wrong. With names like Syed Babar Ali and Mian Mansha, there is a failure to recognize business acumen and genius when it is present in the country. If the nationalization disaster of the 1970s had not been carried out, there

might have been more names that could have matched the achievements of their Indian counterparts.

Still, the spirit lives on. It might come as a surprise to some that one of the biggest hosiery manufacturers in the world had its humble beginnings in Faisalabad. Read that again. One of the largest hosiery manufacturers in the world is from this country.

What started out as a brainchild of Musadaq Zulqarnain and Navid Fazil now counts international giants like Nike, Adidas

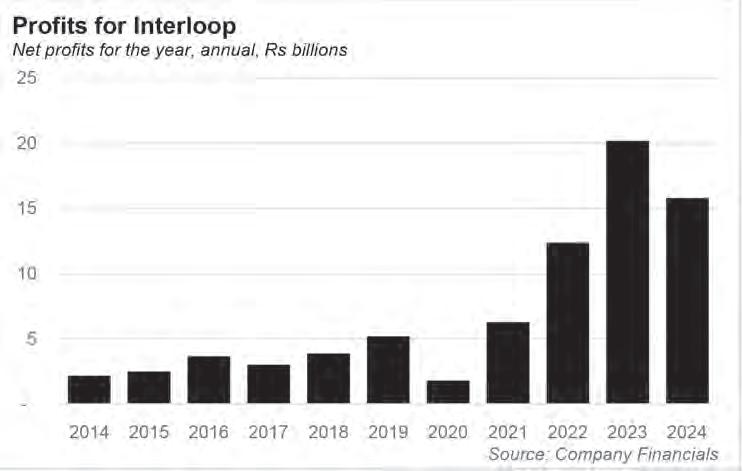

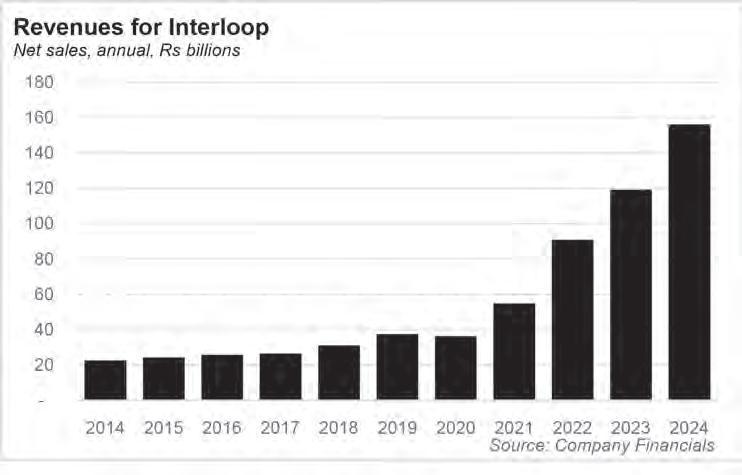

and Puma as their clients in just the active wear space. Once Wilson, Levi’s, Amazon, Uniqlo, H&M and Target are added to this list, the size and scope of the company starts to become apparent. With sales of more than Rs 156 billion in 2024 and profits of Rs 16 billion, the company has come a long way in a period of just 33 years. But now it seems that Interloop has hit a hitch.

There is an old saying that one man’s trash is the next man’s treasure. What is considered good for one is bad for another. The corporate world also falls prey to the same idiom. Pakistan has gone from being on the precipice of default to now seeing a prolonged period of stability.

A stable rupee, falling interest rates and a healthy foreign reserve shows that things are looking up for the country. Many in the corporate world are delighted that economic metrics are turning in their favour. As the economy tries to get back on its feet, companies are seeing expanding profitability and revenues.

On the other hand, companies like Interloop are seeing a downturn in their performance. The lifeblood of these companies is dependent on exports and sales being carried out in foreign markets. As the rupee was depreciating in the past, Interloop was able to see their bottom line expand while the manufacturer was able to sell the goods at a cheaper price in the US. With the rupee depreciating, the sales kept growing and the revenues were being translated into better profits.

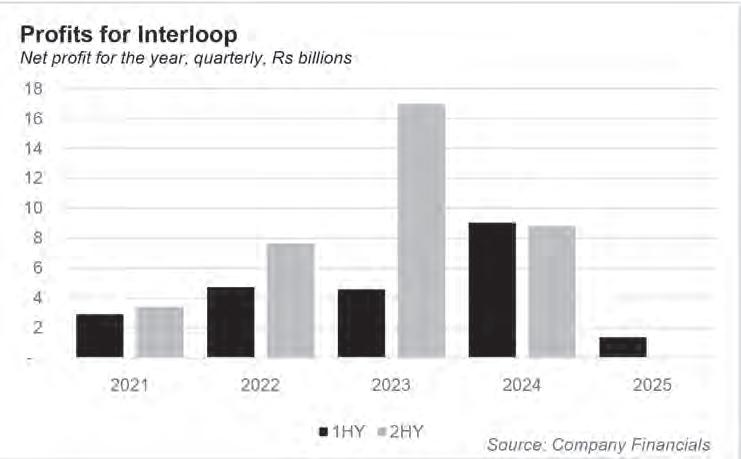

Now it seems that the music has finally stopped and the company might be in for some hard times going into the future. Last year, Interloop earned profits of Rs 9 billion for the 6 months ended in December of 2023 on sales of around Rs 74 billion. Even though sales increased to Rs 84 billion for the current half

year of 2025, profits have shrunk to only Rs 1.4 billion.

Earnings per share of Rs 6.44 last year have decreased to Rs 0.98 for the current year. As the third quarter nears its end, it can be expected that things will get worse before they start to get better. This is the tale of dichotomy at Interloop. When the country does better, the company does worse.

History of the company

It is 1992. The country is riding high on the euphoria of winning the cricket world cup. This was the year Interloop established its first unit on Jaranwala road in Faisalabad and from that point on, the company has not looked back. The first unit had

10 knitting machines and was able to grow its client base due to its commitment to quality in terms of product and service. By 2019, the company had more than 4,500 knitting machines which could produce more than 500 million pairs of socks annually.

As the company expanded, it established production facilities in Faisalabad and Lahore before crossing borders into Bangladesh. The company has also developed strategic alliances with companies in North America, Switzerland and Holland. These alliances provide logistical, warehousing and marketing support to Interloop by developing its footprint in these countries. There is also an integration between Interloop offices in China which allows for seamless provision of dyes, yarns and other raw materials in the manufacturing of socks.

On the back of its operational and financial success, the company went for its Initial Public Offer (IPO) in 2019. Investors were given an opportunity to invest in a company which was expanding its revenues year on year. From 2014 to 2019, the sales of the company went from Rs 23 billion to Rs 31 billion. The growth in sales was complemented by the growth in its gross profit margin which stood at 24% in 2014 and increased to 29% by 2018. Lastly, these gains continued down to the net profits which also increased from 9.6% in 2014 to 12.5% in 2018.

The will and drive to keep expanding was evident by the fact that the owners did not rest on their laurels. They were constantly looking to expand into the denim market in order to diversify its revenue streams. Interloop also has a focus towards research and product development as it established a state of the art aVertical sampling facility in Faisalabad. The goal of this facility is to take note of

the requirements of the clients and to develop its products based on these specifications and requirements.

After the book building was carried out, Interloop received a resounding response as it was able to get a price of Rs 46.1 which was higher than its intended price of Rs 45. The company ended up raising more than Rs 5 billion from the IPO which was the highest ever for a private company in the history of the country. The issue also meant that it became one of the top 50 companies that were listed on the Stock Exchange based on its market capitalization.

The purpose of carrying out the public offer was to raise additional funds for the company which would be used to finance the expansion of Interloop further. The funds would be used to expand the hosiery segment in Faisalabad and setting up a denim facility in Lahore. The funds raised from the IPO would be supplemented by debt financing in order to raise an amount of around Rs 11.3 billion which would be used to fund its letter of credit and the machinery that was going to be imported.

In return for the investment, the shareholders were going to get ownership in one of the biggest knitting facilities in the country. In terms of dividend, the company had a healthy track record of giving out cash and bonus dividends which was expected to continue based on the healthy profitability of Interloop.

Post IPO financial performance

The period from 2019 onwards was more of the same old same old.

Revenues for the company had reached Rs 37 billion by 2019 which

increased to Rs 156 billion by 2024. The only year sales saw a dip was in 2020 due to the pandemic, however, the revenue growth from 2020 onwards only reiterated the fact that the fundamental growth at the company was strong. Sales had fallen to Rs 36 billion in 2020 but then increased by 50% to settle at Rs 55 billion in 2021.

If 2021 was a good year, 2022 ended up being a great year as Interloop was able to increase sales by 65% to register around Rs 91 billion in 2022. Even though the growth slowed down, the revenues still grew to Rs 119 billion in 2023. This was a growth of 31% which would be exceptional by itself. The year from 2023 to 2024 again saw growth of around 31% yet again,

As sales saw growth, the gross profit and net profit margin showed tremendous growth in line with the revenues. In 2019 gross profit margin was 32% which increased to 33% by 2023. Similarly, net profit margin stood at 14%

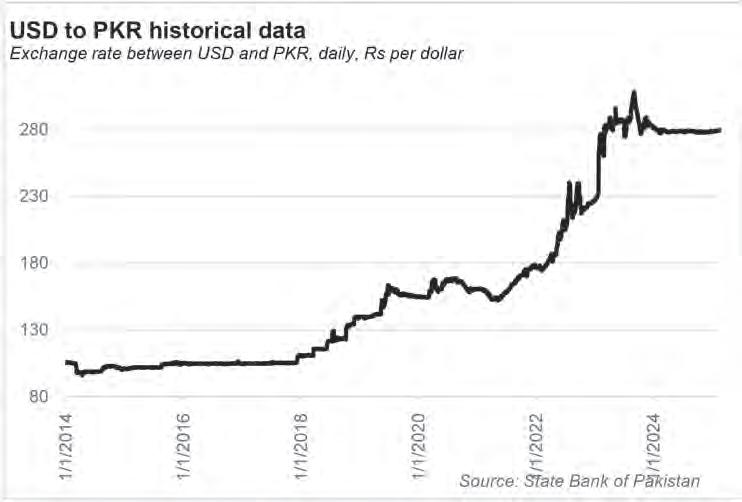

in 2019 and also jumped to 17% in 2023. The improvement in these metrics can be attributed simply to the value of rupee. From 2019 to 2023, the rupee had depreciated from Rs 140/ dollar to Rs 282/dollar. As the value of the local currency depleted by 100%, the impact was seen on the financial statements of interloop as well.

Earnings per share stood at Rs 3.7 per share in 2019 which hit a high of Rs 14.39 in 2023. Due to the increasing profits, Interloop gave out healthy dividends of Rs 16.5 for the 5 years combined.

The reason behind the increase is hidden in the concept of exchange gain. Suppose Interloop sold a pair of socks to Nike in 2019 for $1. Based on the currency rate, Interloop ended up earning Rs 140 for the sale of that sock. In 2023, the same pair of socks was sold to Nike again which cost the sportswear company only $1, however, the depreciation meant that now Interloop earned Rs 280 for the same sale which had been half of that before. The same product being sold in the same market led to an increase in sales by 100%.

Things take a turn for the worse

In the times of depreciating rupee, Interloop was able to enjoy substantial profits as 90% of its sales were attributed to exports. As the rupee started to stabilize, this strength started to turn into a weakness as it had a direct impact on its profitability. The prospectus of the company released in 2019 foreshadowed this possibility as the company recognized that any unfavorable movement in the value of rupee was going to be detrimental to the profits.

The impact of the stable rupee started to show their effect on the accounts in the third and fourth quarter of 2024 itself. Breaking down the financial performance for 2024 and 2025 represents the effect that was seen on

the results. In the period from July 2022 to December 2022, Interloop was able to earn profits of Rs 4.6 billion in the half year ended December 2022. For the same period, it saw profits of Rs 9 billion for the half year ended December 2023. In terms of earning per share, this translated into a profit per share of Rs 6.44 in 2023 which had only been Rs 3.27 a year ago.

The average exchange rate for the period for these periods explains the jump in the profits. For the same period in 2022, the exchange rate was trading at around Rs 215 while in 2023, this rate increased to around Rs 280. The depreciation seen was able to contribute to the increase in the profits.

Things started to turn later in the year. The second half of 2023 saw the exchange rate stabilizing at Rs 280. For the remaining year, the company was able to earn an additional Rs 7 billion by end of June 2024 where they had earned Rs 15 billion in the same period last year. To put things into perspective, the company should have seen a 3 times increase in its profits and should have closed out the year at Rs 36 billion compared to where it actually ended up earning only Rs 16 billion.

With the exchange rate becoming rigid and fixed to some extent, the same pattern has repeated for the 6 months period ending in December of 2024 as well. In the last two quarters, the performance of the company has further deteriorated as the reality is slowly setting in. In the recent half year accounts, Interloop has shown profits of only Rs 1.4 billion which had been Rs 9 billion last year. The earning per share has fallen by more than six folds as it has decreased to Rs 0.98 from Rs 6.44 seen last year.

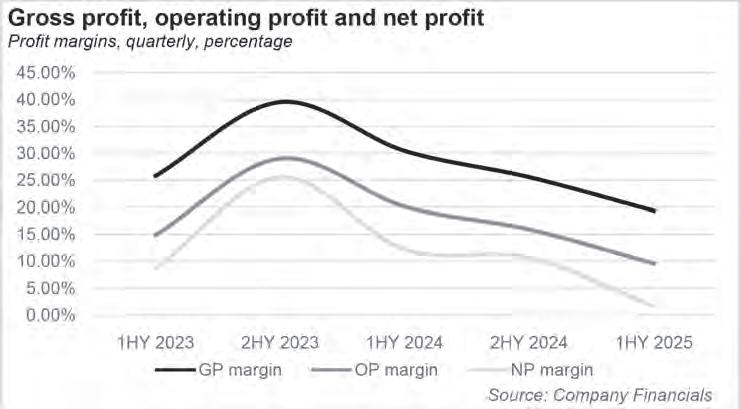

The performance deterioration can be seen in terms of the profits margins of the company. Gross profit margin touched a record high of 33.5% in 2023. This could be broken down to a ratio of 25.8% in the first half and almost 40% in the second half of financial year 2023. The first half of 2024 saw the ratio fall to 30% and then decrease further to 26% in the second half. The average for the year settled at around 27.9% for 2024. The first half of FY 2025 has seen erosion to such an extent that the gross profit margin has fallen below the 20% threshold as well. This is the lowest margin the company has seen since it was listed.

The same pattern is seen in terms of other margins as well. The operating margin was 15% for the first half of FY 2023 which further doubled to nearly 29% in the second half. Due to this, the average margin came at around 22.7%. For the first half of FY 2024, the ratio was 20.1% and with a further decrease to 15.9% in the second half averaged to 17.9% for financial year 2024. The latest half year has

shown a further decrease to less than 10%.

Net profit margin has gone through a similar trend. Net margin touched a high in 2023 of 17% buoyed by the second half margin of 26%. Due to the depreciation, the margin fell to around 10% for FY 2024 as profits started to shrink. The latest half year shows that the margin has fallen to 1.6% as the company fights to show profits for the year.

The treatment of exchange gains

The fall in the gross profit margin usually points towards two things. Either sales are falling or costs are increasing. To some extent, Interloop did see rising costs as its raw materials were proving to be more costly leading to the margin shrinking. Exchange gain is considered to be a gain that is earned by the company from a source which is not considered central to the company. Gross margins are related to the operations while exchange gains are seen as other income further down the income statement.

This is where Interloop diverts from convention. In the financial statements, the company considers exchange gain or loss as part of the sales and adds any income earned due to depreciating currency as sales. When exchange gain is earned, the company records higher sales with the same costs and sees its gross margin grow. In periods of stable or appreciating currency, the margin shrinks.

To get an understanding of this, it was seen that exchange gain was around Rs 89 crore in 2018 which increased to Rs 2.3 billion in 2019. Due to the pandemic and decrease in sales, the gains fell to Rs 20 crores in 2020 and became an exchange loss in 2021 of Rs 68 crores. In 2022 and 2023, the exchange gains

rebounded to Rs 5.3 billion and Rs 8.4 billion respectively.

With the currency stabilizing in 2024, the exchange gains again went into the red as Interloop registered exchange losses of Rs 74 crores. Due to the treatment of the exchange gain and losses, it can be seen that the volatility of the exchange rate impacts the gross margin of the company directly.

The general trend from 2019 to 2024 mostly saw the currency depreciating which meant that exchange gains were far greater than the losses that were seen in the periods of low movement in the currency. In 2019, total profits were of Rs 5.2 billion from which nearly half were attributable to exchange gains. In 2022 and 2023, profits earned were of Rs 12.4 billion and Rs 20 billion respectively from which nearly 40% of the gains could be credited to exchange gains alone. With such a huge reliance on exchange gains as part of its profits, it is no wonder that the company suffers low profits in periods of stability and appreciation.

The third and fourth quarter results of the company will be vital to observe as they will show whether Interloop has resigned themselves to their fate or are actively looking to turn the ship around. With exports being a major part of its revenues, the company might have to look towards solutions other than exchange rate which is out of its control. One thing going for the company is that it has reserves it can burn into the future and has a client base which will stay loyal to the brand through its lean period. With the recent announcement of a current account deficit, there can be an expectation of a depreciation in the currency being on the cards.

With little in the way of influence, Interloop can hope more than expect things to turn in their favour. n

The rise of Pakistan’s tech services exports

It is low-value, far smaller an industry than that in India, and is actively being strangled by the government. But Pakistan’s white collar techies and tech-enabled services exporters may hold the key to the country’s macroeconomic salvation

By Farooq Tirmizi

In 2020, the world economy hit an interesting inflection point: India exported more software and tech-enabled outsourced services than Saudi Arabia exported oil. Now, 2020 was a global pandemic year, and many things about it were very different, so it was a point easy to ignore. But when it happened again in 2023, it was starting to become clear: the nature of what was valuable, and what allowed a nation to generate income, was changing.

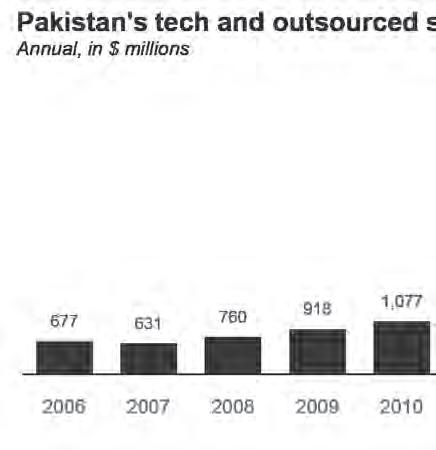

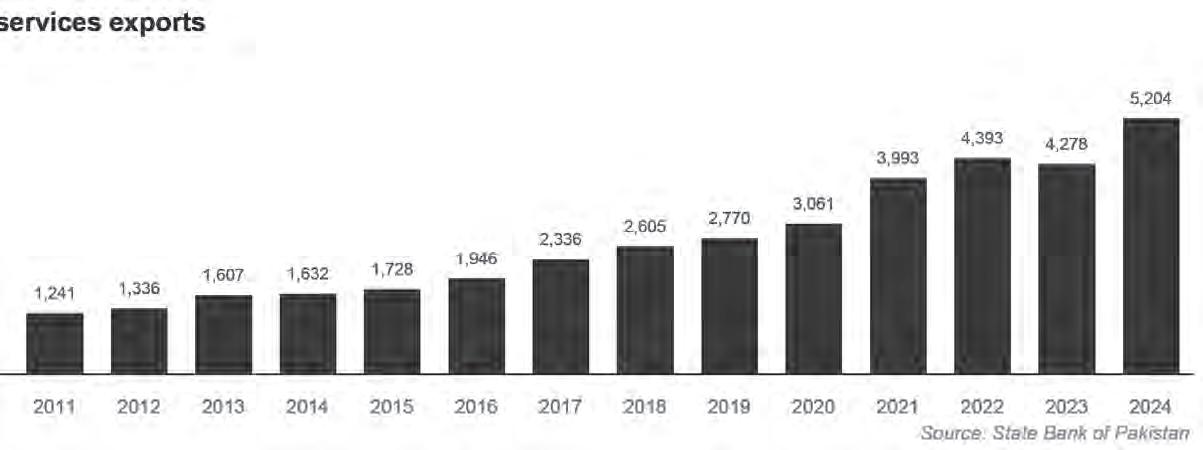

Pakistan’s software and tech-enabled outsourced services business is laughably behind that of India, and we do not think a comparison is particularly helpful. Indeed, we will lay out the numbers up front just so that the lack of comparison can be laid to rest. In 2023, India exports $250 billion worth of these services. Pakistan exported $4.3 billion.

So perhaps Pakistan’s tech and outsourced services industry will not be quite as globally significant as to eclipse Saudi Arabia’s oil exports. But a smaller goal – and one that would make all our lives a lot better – is more within reach: having Pakistan’s tech and outsourced services exports exceed Pakistan’s own imports of oil and gas.

Pakistan’s goods exports have been growing highly anemically, at a measly average of 3.6% per year in between calendar years 2006 and 2024, according to data from the State Bank of Pakistan. During that same period, Pakistan’s tech and tech-enabled outsourced services industry’s exports grew by 12% per year.

And they did it without being crybabies about it, unlike the textile exporters who cannot get out of bed in the morning without asking for a government subsidy.

This is the story of how an industry spent decades trying to get a foot in the door of a market dominated by its next door neighbour, one whose growth was – and is – mostly being strangled by the government, but one that, if left alone, can help the country achieve macroeconomic stability like no other industry can. We will then also explore ways that individuals could help expand the industry’s scope.

Origins of Pakistan’s tech industry

The first computer arrived in Pakistan in 1964: an IBM 1620 mainframe, intended for use by the Pakistan Atomic Energy Commission (PAEC). It was initially meant to be used at the Lahore office of the PAEC, but since the only Pakistani citizen at the time who could operate it was a native of Dhaka, it was moved to the Dhaka office.

Following that first computer, several

other government organizations were able to procure computers, and eventually, by the 1970s, many banks in Pakistan had them, and an initial computer industry started taking off in the country.

By the 1980s, a handful of upper middle class households in Pakistan started being able to afford desktop computers, which some used as the opportunity to learn more about software development. Famously, the world’s first computer virus was developed in Lahore in 1986 by the brothers Amjad and Basit Alvi, who developed it mainly out of intellectual curiosity, and naively put their names, address (in Allama Iqbal Town) and telephone number on the virus.

As a mass industry, information technology began to take shape in the early years of the Musharraf era, starting in 2000 when the then-Science and Technology Minister Dr Ataur Rehman began encouraging universities all over Pakistan to start offering degrees in computer science and software development. By then, news of the success of the Indian outsourcing industry was widely known in Pakistan, and hence emulating it was seen as something worth trying.

This was also the era when the government began investing heavily in higher education in general, both by opening new universities, as well as expanding the campuses and teaching capacity of existing universities. Among the things the government pursued during this era was ensuring that every university was equipped with a world-class computer infrastructure.

This resulted in every university in Pakistan being connected to global repositories of journals, having well functioning computer labs with – shockingly at the time for Pakistan – fully licensed software that the government actually purchased (at discounted prices) from the world’s leading software companies, most notably Microsoft.

(This purchase from Microsoft explains why Pakistani government and bank websites work best when you open them in Microsoft browsers rather than Google Chrome or any other browser.)

And while primary and secondary education are areas the government has neglected, the rise of higher education – especially in computer science – really did happen largely due to the public sector’s efforts. The private Lahore University of Management Sciences (LUMS) may have Pakistan’s best computer science department, but the vast majority of Pakistan’s software developers who have college degrees got them at public universities.

Despite the concerted effort and significant investment, the strategy did not have much success initially. By the end of Musharraf’s time in office in 2008, when India’s industry was doing $73 billion in software

and outsourced services exports, Pakistan barely cracked $760 million.

Strangling the golden goose

In the years that followed, the federal government largely ignored the technology and outsourced services sector, though it did continue the efforts to expand higher education, which often meant expanding the opportunities for students to study computer science.

During the immediate post-Musharraf era, the government did make one massive blunder: despite interest and financial capacity in the Pakistani mobile telecommunications industry, it refused to auction off 3G and 4G spectrum in 2010 and 2011. Allegedly, the Zardari Administration was seeking large amounts of bribes for the spectrum, which the companies were not willing to pay.

The auctions did not happen until 2014 for 3G and 2016 for 4G spectrum, after the Zardari Administration had left office and the Nawaz Administration had come in. This decision meant that mass adoption of the internet in Pakistan was set back by about half a decade compared to India and other parts of the world, and so was the development of the country’s tech sector.

When it was dependent on just dialup or broadband internet access in people’s homes, internet penetration rates in Pakistan grew at anemic rates. When mobile broadband internet finally did become available, it became the mainstay of how Pakistanis began to access the internet, and by extension, marked the beginning of when the country as a whole went online.

Meanwhile, there was the government’s

– especially the military establishment’s – attempts to censor the internet, which was done in such a ham-fisted manner as to render the entire internet functionally unusable for much of the country. Indeed, on February 24, 2008, the whole world lost access to YouTube for 24 hours because the government of Pakistan was trying to censor it in the country but managed to effectively block it for the whole world for almost a full day.

Wikipedia, Facebook, and many other websites have been blocked in Pakistan periodically. Ironically, there is now a whole Wikipedia page about the censorship of the internet in Pakistan. YouTube was banned for a full four years from 2012 through 2016. Twitter, now known as X, is blocked now.

But worst of all, the government of Pakistan has a habit of rendering the internet so slow as to make it impossible for anyone who needs to access it for their work to be able to effectively work, sometimes for days and weeks on end. This makes it difficult for Pakistani tech business and outsourced services businesses to deliver projects on time for foreign clients, which in turn, makes them less willing to hire a Pakistani service provider instead of someone from another country.

Since it is our view that all Pakistanis should assume that the utter stupidity and incompetence of the government of Pakistan as a fact of life, we will not belabour this point and move on.

There is one other government policy – implemented at the provincial level by the Pakistan Muslim League Nawaz (PML-N) in Punjab and the Pakistan Tehrik-e-Insaf (PTI) – that did help move the industry forward: the program that gave high performing high school students laptops for free.

While the precise percentage of people

who received those laptops who then went on to develop an early interest in tech and now have careers in it is not published, the government-issued laptops are frequently seen at technical interviews at software companies in Pakistan, brought in by young candidates who still use that laptop as their primary device.

The boom hits

So for the decade after the Musharraf era ended, the Pakistani outsourcing and tech industry was growing respectably even though it was being strangled by the federal government’s policies, though somewhat helped by two of the provincial governments. Making a mark on the world stage, however, was not quite on the cards.

Then came Covid.

In 2020, with worldwide lockdowns, demand for remote work skyrocketed, which in turn got many companies in developed economies used to the idea of working with people not in the same physical location, in turn increasing the demand for outsourced services. While some of the outsourcing champions –India, in particular – captured a large share of this increase in demand, some of it ended up coming to Pakistan, with the nascent industry finally able to capture some market share.

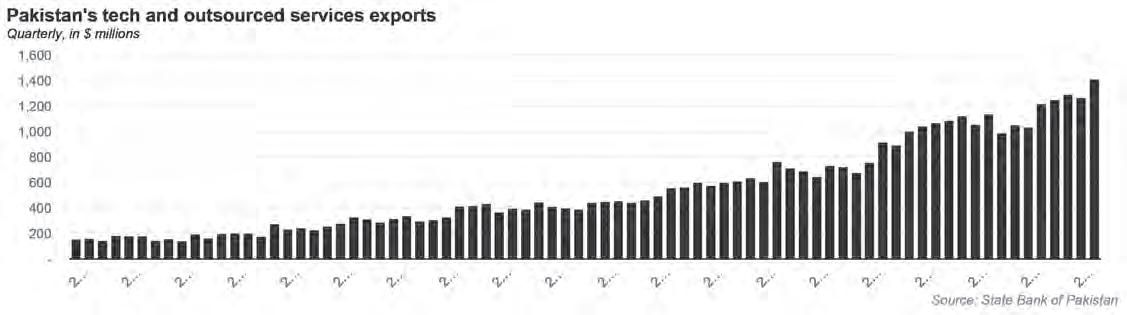

As of 2020, the Pakistani tech and tech-enabled services industry was exporting about $3 billion a year. The next year, in 2021, it exported about $4 billion, a 30% increase in just one year.

More encouragingly, however, this appears largely to not have been a fluke. The industry has mostly kept growing, and closed the calendar year 2024 having exported $5.2 billion worth of services.

Of this, the bulk is software and related services, which brought in $3 billion in 2024.

This is also among the fastest growing part of the sector, having grown by an average 22.6% per year since 2006, when it was just $71 million a year in exports. Over the past five years, the amount of software exported from Pakistan has tripled. At the end of 2019, the amount of software exported from Pakistan had not yet cracked $1 billion.

Call centers are the slowest growing portion of the industry, bringing in $552 million in 2024 and growing at just 5.7% per year between 2006 and 2024. Various forms of tech-enabled services – including professional services – constituted the remaining $1.6 billion in exports.

That tech-enabled services piece refers to the Pakistanis who are not software engineers but otherwise offer their services over the internet. It includes graphic designers, copywriters, accountants, lawyers, financial analysts, digital marketers, Quran teachers, and all manner of service providers who provide their services to companies and individuals outside the country.

The opportunity

One of the fundamental problems in Pakistan’s macroeconomy is that it imports far too much and produces relatively little of what the world would want to buy from us. This is despite years of doling out subsidies by the billions to industries that have struggled to grow their export base and keep coming back wailing and asking for more handouts every time they encounter the slightest inconvenience in the market.

We now, at last, appear to have an industry that has grown with relatively little government help and – far from wanting subsidies – largely wants to be left alone. But

if current growth trajectories are able to continue even for about a decade, which is not out of the realm of possibility, Pakistan’s software exports could increase to a point where the country’s macroeconomic default would be a current account surplus instead of a current account deficit.

Let us get concrete with what we mean. The largest current account deficit on record in Pakistan was the $19 billion deficit encountered in 2018. That precipitated a currency crisis so deep that it ended up taking about five years to full play out. If Pakistan’s software industry were to quadruple in size – which is very likely to happen over the next decade based on current growth trends in the industry – it would be large enough to cover even a record-breaking current account deficit like that.

Of course, that was the deficit in 2018 and a decade from now, both the Pakistani economy and the potential size of its deficits will be higher, but the broader point stands: the country has a gap in its earnings from its exports of goods and people (remittances) that it may soon have the ability to fill using exports of services by people who remain in Pakistan but offer their talents to customers outside the country.

In fairness to the government, it seems to at least understand this basic concept and is now undertaking policies that – in its own misguided way – it thinks will help grow the industry. There is, for example, the thoroughly unnecessary tax break for income earned through services exports equal to just 1% of total income, compared to a top rate of 35% for income earned within Pakistan.

And it is trying to induce more of the freelancers and software export companies to repatriate the dollars they earn from clients abroad by making the banks create accounts for freelancers. Those accounts have special dispensation to allow account holders to pay expenses in US dollars through debit cards and wire transfers (this is allowed in theory, but highly restricted in practice).

But, of course, it refuses to give them the one thing they actually need: an unrestricted internet. Instead we have a vapid IT minister

who represents the very worst of nepotistic incompetence in Pakistani politics and goes around denying that the government is throttling internet speeds as an act of political repression. “Don’t believe your lying eyes” is apparently the government motto these days.

The good news is that the industry will likely continue to expand, despite the government’s level best to destroy it.

Where to go next

In last week’s cover story, we explored how Pakistan’s workforce is increasing its education levels at relatively rapid rates, with the number of college graduates increasing at three times the rate of population growth. We also talked about how the advent of artificial intelligence (AI) is not likely to be a long term barrier to the income growth potential of Pakistanis who export their services to markets around the world.

What we want to explore in this issue is areas of growth: what services can Pakistanis offer the world next? After all, while software is the obvious service that many Pakistanis are currently exporting already, not everyone is a software developer, and hence that option is not open to them.

The key to understanding the spectrum of opportunity is to understand the end markets one is serving. The largest – and most lucrative – of these is the United States, though other countries will also have some characteristics similar to those of the US.

In the US and Europe, there is a significant demographic shift occurring with large numbers of professionals retiring and not nearly enough younger professionals stepping in to take their place. This is especially true in industries where there is a considerable amount of regulation.

One industry where this is playing out rather dramatically is for accountants in the United States: The American Institute of CPAs reported that 75% of today’s public accounting CPAs will retire within the next 15 years, since more than two-thirds of them are already over the age of 60.

If, for example, you are a Chartered Ac-

countant or have an ACCA degree, you could enroll in a masters in accounting program recognized by US accounting bodies (the one at LUMS qualifies), register to take the US Certified Public Accountant (CPA) exams (Prometric test centers, which administer the test, exist in Lahore, Karachi, and Islamabad), and become a fully licensed US CPA and begin serving the US market.

Financial analysts who are willing to sit for US regulatory exams may find themselves qualified to work as outsourced analysts for investment banks or other investment firms in the United States. Lawyers with Pakistani law degrees can take the New York State Bar Exam without any US degrees and, if they pass, can serve US clients based in New York.

Beyond these regulated industries is a whole plethora of other services where demand for outsourced services continues to grow.

Most specifically, there are many companies that require research where their find that AI creates a “last mile problem”: the AI produces results that are fast, but a human needs to sift through the results to verify them for accuracy, something that a person in a lower cost location like Pakistan can do at a rate that is attractive for the Pakistani professional but cost effective for the person in the foreign location.

The prospects for Pakistani professionals offering their services to markets outside the country are only beginning to open up, and young professionals looking at their career options are increasingly viewing themselves as global professionals, even when they are not making plans about immigration.

Indeed, one could argue that a freelancing contract or a remote job is likely to be a better career choice in the long run than those masters programs in Germany and other countries from where graduates often struggle to find meaningful jobs.

This is not to suggest that emigration is not the right option for some people, but merely to point out that, given the way the global economy is shifting, the best place for a Pakistani professional may be to stay in Pakistan while working for a global market. n

What is Tania Aidrus’ Dbank up to now?

After a pivot, the only VC backed contender for SBP’s digital banking licence is solving the same problems with a different approach

By Nisma Riaz and Taimoor Hassan

On 13 January 2023, after a wait of nine months, the State Bank of Pakistan (SBP) finally unveiled the five successful applicants authorised to establish long-awaited digital banks. The list of applicants shortlisted for a digital banking licence included Easy Paisa DB, Hugo Bank, KT Bank, Mashreq Bank and Raqami.

However, something did not sound right. To many onlookers’ shock, the application of the most prominent venture capital-backed contender in the race Dbank’s name was nowhere to be found in the list. Former special assistant to the prime minister (SAPM) Tania Aidrus and her cofounder Khurram Jamali’s Dbank, backed by prominent Silicon Valley VC firms Kleiner Perkins and Sequoia, had seemingly been one of the top contenders for the licence. Why would the SBP reject them? Silence echoed at Dbank’s headquarters in Islamabad.

To understand how we got to this point, let us start from the beginning. Specifically, one woman’s beginning: Tania Aidrus.

Tania Aidrus’ vision

After working for 10 years at Google, first as the Country Manager for South Asia Emerging Markets and then as the Director of Product and Payments for Next Billion Users, Tania Aidrus returned to her home country in 2019 with a mission – to digitise Pakistan. She planned to achieve this goal through a collaboration with the government, so she joined as an SAPM in the then prime minister Imran Khan’s office, under the PM’s Digital Pakistan Initiative in February 2020. In her efforts to digitise Pakistan, she popularised the infamous slogan ‘Roti, Kapra, Makan aur Internet’.

Unfortunately, Aidrus’s plans to digitise Pakistan did not pan out as she expected. Problems had started soon after Jehangir Tareen, who arranged the first meeting between Aidrus and Khan, was ousted from Khan’s political party Pakistan Tehreek-e-Insaf (PTI) due to the sugar crisis probe. In July 2020, Aidrus gave up her position as the SAPM. The reason cited for the resignation, according to Aidrus, was criticism regarding her dual nationality, explaining that it was overshadowing the goals of Digital Pakistan.

So, Aidrus gave up on roti, kapra and

makan, zeroing her focus on just the internet. In December 2020, she co-founded a technology advisory and investment company called the Rayn Group. She had also set off to achieve a new dream – democratising access to financial services and enabling financial inclusion in Pakistan with technology. She was going to do this through a digital bank. Aidrus and her former colleague at Google Khurram Jamali co-founded a digital bank called Dbank. Around the same time, the State Bank of Pakistan (SBP) announced that it would be granting five digital banking licences of two different types; a digital retail bank licence (DRB) and a digital full bank licence. Dbank became one of the first contenders in the race to get an early digital retail bank licence by the SBP.

The newly formed fintech startup had a great beginning, bagging seasoned international venture capital firms, including the likes of Kleiner Perkins and Sequoia, along with others such as Brazil-based Nubank, RTP Global, Rayn and Askari Bank. They raised $17.6 million in their seed round. Aidrus also became a regular on State Bank-organised panels of digital banking, making her mark in Pakistan and becoming a prominent proponent of not just technological advancement but also

financial inclusion.

So, now we had a fintech company, backed by seasoned venture capitalists and owned by former Google employees, who also happened to be closely working with the SBP, and gunning for a coveted licence that the SBP was to grant. They would at least get the license, right? Apparently not.

Everyone was convinced that Dbank would soon be granted a DRB licence, not only because of their promising model and bluechip investors, but also what appeared to be a cordial working relationship with the State Bank.

Fast forward to January 2023, the State Bank announced names of companies that had been chosen for the licence. Dbank did not make the cut.

Banking licence and beyond

In 2022, a team with a strong conviction set out to solve a pervasive problem: financial inclusion and access to credit in Pakistan. The ambition was not just about launching another digital bank — it was about creating an ecosystem that could uplift millions by addressing a fundamental issue in the financial landscape.

“The mission was not about having a digital bank,” Aidrus told Profit in a recent interview. “The mission was to solve the financial inclusion problem. A digital bank was merely a tool to achieve that.”

The foundation of the team’s ambition lay in a crucial insight: when it comes to lending, the lower the cost of capital, the easier it is to scale a lending business. In banking, the lowest cost of capital is found in consumer deposits. And as any banker knows, this makes the digital bank model a highly scalable approach to lending. To strengthen this vision, they attracted investors with relevant technical know-how, including the world’s largest digital bank, Brazil’s Nubank, whose backing added both credibility and confidence to the team at DBank.

Despite these strategic moves, the team at DBank was aware of the challenges ahead. As digital banking licenses were announced in 2022, everyone thought that DBank was well-positioned. After all, with the resources they had raised, the partnerships they had established, and the expertise at their disposal, it seemed like the perfect combination of capital and technical expertise to bring their vision to life.

“We thought we had everything in place. We were prepared. We had the right investors, the right team, and the right strategy. We even began building the bank’s infrastructure and software,” Aidrus explained. “When the announcement came and we didn’t get the

license, we were as shocked as everyone else.”

The application process for a digital banking license was highly competitive, and the team was fully committed to submitting a stellar proposal. They had invested heavily in their infrastructure and were confident that their plan could transform Pakistan’s banking landscape.

“We believed our application was strong. The presentation went well, and we had already raised the necessary funds. We had everything the regulator could want — a clear path, experienced investors, and a solid framework,” they said.

However, despite their best efforts, the regulatory authorities did not grant them the license. The disappointment was palpable, but Tania quickly accepted the reality.

“I don’t believe in crying over spilled milk. It was a setback, sure, but my focus is always on the future. I want to know that I did my best today, and I want to do the same tomorrow.”

Instead of dwelling on the disappointment, they pivoted, leveraging the software they had already developed to offer a B2B solution instead. By shifting their focus, they hoped to deliver the same benefits they originally sought for the consumer market but through a different avenue.

“Pivoting is common in the financial world, especially when you are navigating regulatory challenges,” they explained. “Digital banking was just one way to solve the problem. Now, we’re taking what we’ve built and turning it into a B2B offering.”

It would be fair to ask: why was Dbank passed over for the digital banking licence? Well, only the committee at the SBP responsible for the decision can answer this question. That being said, there are several theories afloat.

A source shared with Profit that the State Bank is a conservative and largely archaic organisation. As much as they claim to be interested in digitising finance and moving towards a technology backed system, they could not bet on something so unfamiliar as a startup. Unlike the tech and startup ecosystem, old school entities, such as, the SBP are quite risk averse, who would be taking a gamble had they granted a DRB licence to Dbank.

In addition to their application, DBank had strategically partnered with Askari Bank, a regulated entity, to bolster their proposal. This partnership was designed to show the regulator that they had a credible, regulated partner in place — a bank that would add legitimacy to their venture.

“We believed that having Askari Bank involved in the application would demonstrate that we weren’t just a group of people trying to start something without proper

structure. We had the support of an established, regulated entity,” they said. “They were never meant to invest large amounts of capital, but they were a crucial partner to show that we had a solid foundation.”

However, the outcome raised questions: Did the partnership with a bank work against them? Could it have played a role in the decision not to grant the license because the State Bank was reluctant and in fact did not give a license to any bank that had applied? The team does not know for sure, and they are reluctant to speculate. What they do know, however, is that they presented a strong case and met all the requirements laid out by the regulators.

“I have no idea why we weren’t selected. The decision-making process was beyond our control. At the end of the day, the regulator has to play the long game. I can’t focus on things that are outside my control,” they said, emphasizing that their focus remained on their mission, not on external factors.

“Our goal has always been to democratise financial services and we went for the licence because it was happening at that time and we felt like we had raised from stellar investors and have been in the space for quite long as well, so might as well put our best foot forward.”

Aidrus optimistically highlighted that there is not just one single route to reach the north star and not getting the licence was not the end of the world for Dbank.

Is there light at the end of the pivot?

So what is the pivot that DBank engaged in after not getting the license? The company had already invested heavily in building a flexible, scalable tech stack. The initial vision was clear: they were creating a platform not just for themselves, but with an understanding that the future of banking would be digital at its core. It was a stack designed to be adaptable, capable of serving millions, and engineered to handle the complexities of modern financial services.

“We weren’t building for traditional banking. We were building for the future of banking — a digital-first platform,” the co-founder explained. “The idea was that you should be able to launch new products, test them, and scale them effortlessly. For instance, if you have 100,000 users and need to test something on 10,000, that’s a difficult task for a traditional bank.”

With this forward-thinking approach, the team’s tech stack had become the foundation of a new company. In a meeting with the board, the team laid out the current situation and their next steps. Their investors — a group of seasoned veterans who had backed

the company’s vision — reaffirmed their confidence in the team and the problem they were trying to solve.

“They took a bet on us because they believed in the mission. This wasn’t a situation where we had to abandon our core vision; we just had to evolve,” the co-founder noted. And evolve they did. The result was the creation of DCore — a flexible, modular core banking platform designed to serve any organization providing financial services, whether a small business or a large fintech company.

At its heart, DCore was built to be a universal solution — a platform that could serve everything from a wallet provider to an institution managing complex credit and debit ledgers. DCore’s modular nature meant that businesses could plug and play the services they needed, making it adaptable for different types of organizations and different sizes of operations.

Once the platform was fully developed, the team set their sights on global expansion. As of now DCore is engaging in Request for Proposal (RFP) processes, having serious conversations with global organizations. The company anticipates that their first client would be an international digital financial services company.

“What we’re building now is a system that can compete globally. We’re thinking of this not just as a regional solution, but as a product with global potential,” said the co-founder.

The core banking system is often called the ‘engine’ of a bank, the underlying technology that drives all transactions, manages ledgers, and supports lending and treasury systems. Traditional banks spend millions of dollars on these platforms, and once they’ve built on them, they rarely change. New digital banks need to buy these systems from scratch, while older banks often look to upgrade outdated legacy systems. This is where DCore steps in.

“We’re positioning DCore as a cloud-agnostic solution. This opens up markets where the traditional core banking platforms haven’t been able to penetrate, either due to cost or regulation,” the co-founder explained.

Most traditional banking platforms are built on legacy technology that requires immense investment to maintain. These platforms are often inflexible, expensive, and difficult to scale. For many new banks, particularly in emerging markets, the costs associated with these platforms are simply prohibitive. DCore, however, offers a cost-effective alternative.

“We saw a gap in the market where new banks couldn’t enter because the regulatory frameworks were prohibitive, or the cost of using traditional banking systems was far too high,” the co-founder said. “We’ve built DCore

with flexibility in mind, allowing it to be used in a wide range of contexts and markets.”

This adaptability makes DCore particularly attractive to countries with emerging financial systems, where outdated technology or prohibitive costs might stifle innovation. DCore’s cloud-agnostic nature ensures it can be deployed across various markets, providing both new and old financial institutions with a versatile and cost-effective solution.

Profit asked Shahzad Ishaq, the Group Head of Digital Banking and Chief Digital Officer at MCB Bank Limited, to explain whether a traditional bank looking to digitise their services would be interested in a software like Dcore. He responded positively: “One of the credentials of any organisation looking for a digital transformation is that you will not develop everything yourself, but you will also be buying things off the shelf. If someone has already invented a software that you can outsource and they have the technology, the expertise and the credentials to offer a good product, there is no point in spending more time and money trying to build something inhouse from scratch.”

Jamali shared that even at the time of their funding round, they had pitched a global product to their investors and Dbank had always been a small part of their larger mission. “The idea was never to just stick to Pakistan. We are doing it here because we are passionate about Pakistan but we also have a global footprint and our own relationships with people around the world, so our product would also not just be limited to Pakistan,” Jamali said.

Waseela

Core banking software is not all the DBank team started working on. They went to work to solve the actual problem they had envisioned to solve when they applied for a digital bank license: financial inclusion. And in financial inclusion, they decided to solve for access to credit for Pakistan’s underserved small farmers. With limited digital financial services available, particularly in rural areas, the newly created initiative Waseela sought to create an ecosystem that would empower farmers not only through lending, but through a holistic approach that included access to the right agricultural inputs, mechanization, and market knowledge.

In Pakistan, a majority of farmers remain outside the formal financial system, particularly those with small landholdings, Tania says. The challenge is not just about getting loans; it is about understanding the farmer’s true financial situation. In a country where only 1-2 million people have access to fully digital financial services, traditional methods

of assessing creditworthiness — such as using transaction history — are simply not applicable for many farmers.

Agriculture is the backbone of Pakistan’s economy, employing around 36% of the labor force. Yet, the sector remains woefully underserved. Small and medium-sized enterprises (SMEs), including those in agriculture, struggle to access the credit they need to grow their businesses — such as expanding farms, buying equipment, or opening new retail outlets. Similarly, farmers face numerous challenges, including lack of access to financial services, inputs at the right prices, and the knowledge to optimize their yields.

“Lending requires confidence — both in the ability and willingness to repay,” says the co-founder. However, assessing that ability and willingness is no simple task, especially when collateral is almost nonexistent in rural areas. The key, they realized, was to understand the entire value chain of agriculture.

For example, to support small farmers working in agriculture, Waseela needed to track who owned land, whether they were producing milk or other goods, and how they were generating income. With a comprehensive understanding of each farmer’s profile, Waseela could begin making informed lending decisions without relying on traditional collateral.

Thus, Waseela focuses on building a strong understanding of rural Pakistan, with the ultimate goal of improving financial inclusion in the agricultural sector. With a presence in Central Punjab, Waseela began to understand the core issues facing farmers and developing solutions that met their specific needs.

In June 2023, Waseela was born. With a newly acquired Non-Banking Financial Company (NBFC) license, the company charted a course that was not focused on lending first. Instead, Waseela decided to take an ecosystem approach — positioning themselves to deeply understand the challenges faced by small farmers before offering financial solutions.

The platform initially focused on providing unadulterated agricultural inputs at transparent prices, giving farmers access to essential resources they needed to succeed. Beyond that, they began offering mechanization services, helping farmers access machines they might not be able to afford on their own.

“We’re not just a lending business,” says Tania. “Lending is embedded in what we do, but we’re offering much more. We’re building a platform that helps farmers access the tools, inputs, and knowledge they need to succeed.”

While Waseela’s long-term vision involves leveraging technology to its fullest potential, they are mindful of the fact that rural Pakistan is not yet ready for a fully digital solution. “Forty percent of farmers still use fea-

ture phones,” the co-founder notes, “and most have access only to 2G connectivity.”

Given this reality, Waseela’s approach combines use of technology and a physical presence. While the company collects data and uses it to inform decisions, this tech operates mostly behind the scenes, with physical agents engaging directly with farmers on the ground. They’ve set up physical outlets called “Kisaan,” where farmers can access unadulterated products and transparent pricing. In the future, they envision using technology to further enhance their ability to provide these services, but for now, trust-building is paramount.

One of the biggest challenges facing Waseela is trust — both from the farmers and from the financial institutions involved. Many farmers are skeptical about financial institutions, having seen predatory lending practices in the past. To overcome this, Waseela began by offering products and services at fair prices and establishing themselves as a reliable and transparent partner.

Farmers who become members of the platform can access agricultural inputs at the manufacturer’s price, which is a significant benefit in an environment where fair pricing is often elusive. Furthermore, Waseela offers more than just products: it provides a network of support and services that farmers can trust.

“We’re building trust with the customer,” says the co-founder. “It’s not just about lending. It’s about showing farmers that we’re here to empower them, not exploit them.”

“We are in a growth phase,” says the co-founder. “Our business model is not just about having a store. It’s about building an ecosystem, and each part of that ecosystem is a business line on its own. We have milk collection centers, agricultural input stores, and mechanization services. All of this adds value to the farmer and creates an efficient marketplace.”

As Waseela continues to grow, the founders are cautious about relying too heavily on venture capital (VC) funding. Pakistan’s startup ecosystem has yet to develop an open and consistent VC tap, and the founders are focused on building a sustainable business model.

“We’ve had a good run with VC funding, but that’s not going to last forever,” says the co-founder. “The future will require better business practices. We need to create solid businesses with real, scalable models.”

This pragmatic mindset is evident in how they operate across all aspects of the business, from hiring practices to their focus on both digital and physical solutions for farmers. Waseela is building for the long term, with an eye on creating a platform that can empower millions of farmers and small businesses to thrive.

Trouble in paradise?

It has been more than a year since DCore’s seed funding round, where they raised $17.6 million. It has also almost been over a year since Dbank was looked over for a digital banking licence, and the company shifted its direction.

It would be fair to ask: are DCore’s investors becoming impatient? Have they lost hope in the founders’ ability to put their money to good use? Well, there is one particular founder who might have expressed the desire to leave this party.

Earlier this year, Sequoia decided to split into three different VC firms, breaking into Sequoia US and Europe, Sequoia China, which is now called HongShan and Sequoia India and Southeast Asia, now known as Peak XV Partners.

A source told Profit that ever since the split, Peak XV Partners was sceptical to invest in Pakistan. By default, their desire to leave this market also meant that they did not wish to continue with their investment in Dbank especially after the pivot to DCore.

According to the source, DCore convinced the investors to continue their partnership on the basis of the argument that it is not just a Pakistani startup, but one with a global outlook. The company plans to take its services and products to international markets, as well and this became the reason why DCore was able to convince Peak XV Partners to stay.

The source speculates this to be a stopgap solution for now and the fund’s reluctance to invest in Pakistan can be expected to become an issue again later.

Profit spoke to Aman Nasir, partner at venture capital firm Sarmayacar, to understand VC’s general sentiments towards pivots. He informed us, “It depends on the reasoning and the type of pivot - VCs would like start ups to be adaptable and open to change based on data insights and market feedback. However, they are generally cautious as significant pivots can take time to execute and there needs to be open communication.”

Another venture capitalist Kulsoom Lakhani, who is a partner at i2i Ventures, had a slightly differing opinion on the matter.

Lakhani told Profit, “I have seen a number of pivots in our own portfolio. There are a lot of external factors that can make a company pivot, especially considering our macro economic condition. Ultimately, you are investing in the founders more so than in the business, at least for the most part and especially with early investments, such as a seed round. So, oftentimes the pivots are related to making the business better and founders are usually transparent with their decision, and keep VCs in the loop with any new decisions or direction they plan to take.”

Lakhani believes that pivots are actually quite healthy, especially in premature businesses because at an early stage one goes in with an assumption, the likelihood of which getting refuted is high.

When asked about VCs general expectations after investment, Nasir said, “VCs expect only a small number of start ups in their diversified portfolio to deliver outsized returns. In a country like Pakistan, VCs acknowledge there are heightened external challenges and often help to navigate some of the challenges, including potential pivots or providing support to survive a difficult temporary period. In some cases, a promising start up may not survive due to factors beyond their control - it’s important to maintain open, transparent communication with investors in such situations.”

What Nasir and Lakhani’s comments have in common is open communication and transparency, arguing that keeping investors in the loop while making decisions pivotal to the business holds immense importance.

It can be said that investors as large as Sequoia and Kleiner Perkins are probably smart enough not to invest in an idea that is contingent upon a banking licence or any regulatory decision. Therefore, it is probably fair to assume that they have faith in the founders, who they invested in.

It is also fair to assume that seasoned investors such as Sequoia would not be ones to have a knee jerk reaction to every hiccup, in fact most investors are aware of the risks beforehand, especially when backing seed rounds.

However, the problem here was never the licence or the pivot. The issue was simply the market that DCore operates in, which the newly split fund was disinterested in.

The co-founders of DCore completely denied the notion of Sequoia having second thoughts.

Aidrus told Profit that, “We are incredibly grateful to have the support of all stakeholders who believe in our mission. While obtaining a digital banking licence is one approach to achieving our goal, we collectively recognize that it’s not the only solution.”

She added that, “What we are trying to achieve will take several years and it is a long way ahead. Digital transformation takes years to materialise fully and the good thing for us is that we have investors who understand the stakes. Good experienced VCs are not looking for short-term gains and quick returns. They knew we had applied for the licence and when that did not work out they asked us to think of another route to achieving our initial goal.”

How successful DGlobal is and how capable the founders truly are is yet to be seen. All the questions will perhaps stop once the software launch finally happens. n

announces $100mn investment to fuel startups globally

By Taimoor Hassan

Disrupt.com, a UAE-based venture builder founded by three Pakistanis, Aaqib Gadit, Uzair Gadit, and Umair Gadit, has announced a $100 million investment commitment to support technology ventures worldwide.

The ambitious move underscores the firm’s focus on fostering innovation in technology-driven sectors like AI, cybersecurity, Web 3.0, automotive technology, and retail innovation. The investment also positions Disrupt.com as a key player in the emerging global technology ecosystem, with a particular emphasis on underserved markets such as MENA and Pakistan.

Amid a global venture capital slowdown, with MENA VC investments falling 29% in 2024, Disrupt.com’s approach aims to counter the trend, providing funding, strategic guidance, and operational support to early-stage startups. The firm is determined to empower entrepreneurs in regions that typically face challenges in accessing growth capital, especially in the wake of funding declines in places like the UAE, where investments decreased by 8%.

Disrupt.com’s founders, originally from Pakistan, have a deep-rooted entrepreneurial background. They first made their mark in the technology space through Gaditek, which they founded in Karachi in 2008. In 2022, they sold Cloudways, a Malta-based cloud hosting platform, to US-listed Digital Ocean Holdings for $350 million, marking one of the biggest exits in Pakistan.

Cloudways’ acquisition by DigitalOcean marked a significant milestone for the Gadit family, and also allowed them to reinvest their capital and experience into their next venture: Disrupt.com. Since its inception, Disrupt.com has already deployed over $40 million into a diverse range of startups in key technology sectors, including cybersecurity, AI, and Web 3.0, according to the company.

Aaqib Gadit, co-founder and CEO of Disrupt.com, reflected on the success of Cloudways, noting, “SMBs love simplicity, performance, predictability, affordability, and great support. Together with DigitalOcean, we turbocharged Cloudways’ mission of helping SMBs grow through cloud offerings. Now, with Disrupt.com, we aim to support a broader range of entrepreneurs and tech ventures globally.”

The $100 million commitment from Disrupt.com will target early-stage startups that focus on AI, cybersecurity, Web 3.0, automotive technology, and retail innovation. The firm is particularly interested in businesses at the pre-seed to Series A stage that show strong organic growth potential and clear paths to profitability. This aligns with the company’s mission to help create sustainable businesses that will drive the next wave of innovation in these industries.

“We are doubling down on building the next wave of startups that will define the future of the world,” said Aaqib Gadit. “Web 3.0 is in its early stages, and AI is revolutionizing industries. The opportunity to solve real-world problems and create businesses that align with how people live and work is vast, and we believe MENA and Pakistan will play an integral role in this transformation.”

Disrupt.com is not only committed to providing funding but also to fostering a supportive ecosystem that helps startups thrive. With a network of over 650 professionals globally, including many in Pakistan, the firm offers entrepreneurs access to a wealth of expertise across business strategy, technology development, and marketing.

By leveraging experience and the lessons learned from previous ventures, Disrupt.com founders aim to create a powerful ecosystem for founders. “Our network brings the experience of all the mistakes we’ve made ourselves in the past,” added Uzair Gadit, co-founder of Disrupt.com. “We are here to help entrepreneurs avoid these pitfalls and accelerate their growth.”

Despite relocating its headquarters to Dubai, Disrupt.com maintains strong ties with Pakistan and other underserved markets. The founders’ commitment to empowering entrepreneurs in these regions is integral to the firm’s mission. Aaqib Gadit emphasized the firm’s belief in the untapped potential of MENA and Pakistan, stating, “There are incredible entrepreneurs in this region, but they often lack the resources to bring their ideas to life. We are here to bridge that gap and help them build world-class businesses.”

This focus on MENA and Pakistan comes at a critical time when venture capital funding in the region is declining. According to data from Magnitt, MENA VC investments dropped by 29% in 2024, and early-stage investments in the UAE decreased by 8%. Disrupt.com’s commitment to these regions provides a vital lifeline for entrepreneurs who otherwise might not have access to the necessary funding and support to scale their businesses.

Pakistan’s cashback startup Savyour to completely shutter operations

The startup, which distributed more than Rs400mn in cashback rewards to 4 million customers, said that it decided to shut down 12 months ago

By Taimoor Hassan

Savyour, Pakistan’s only cashback fintech startup, has announced the closure of its operations, a decision confirmed by one of the company’s co-founders.

The company did not disclose any reason for the shutdown and only said that the decision was taken 12 months ago. “Over the past year, the team has been diligently working on this transition, ensuring a smooth and well-managed wind-down,” the company said.

“Today, after a period of internal restructuring and ideation, Savyour announces its decision to close, marking the end of one chapter and the beginning of another phase of strategic growth.” his marks the conclusion of an ambitious journey that began in August 2020 when the company set out to transform the country’s e-commerce ecosystem with its innovative cashback model. At its core, Savyour introduced a unique approach to Pakistan’s market, where cashback models were virtually unheard of.

The startup created an app and a payper-sale affiliate marketing network, enabling customers to earn cashback by purchasing from popular e-commerce brands like Daraz, foodpanda, and Bata. Acting as an intermediary marketing service, Savyour earned commissions