09 Panadol costs more now. What has this meant for the pharma industry?

12 Nearly a trillion rupees have disappeared from the books of the Punjab Govt

18 What is the banking industry thinking?

22 Are coworking spaces a viable asset class in Pakistan?

27 Three pivots later, how will agritech startup Tazah deal with the international e-commerce business?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Haleon has benefited from the new drug pricing policy introduced by DRAP and it shows in its financial results

By Zain Naeem

An airconditioned room. A bureaucrat babu sits behind the desk covered with official and important looking papers.

Just outside his office, he has a personal assistant who answers to his every whim and request. In the lot outside glints a government provided car which shines brightly as the driver polishes it for the umpteenth time. A low ring of a phone in the distance makes it look as if the babu is the centre of the universe.

He can be likened to an ant trying to haul a large piece of food back to its anthill. The illusion turns to delusion as he thinks the world cannot function without him. Even though, in reality, he is an insignificant part of an obsolete system which is rotting from the inside.

In such a world, the policy makers and the bureaucrats feel that they have the solution for every ill and problem in the country. Due to this position, it is their honour, nay, duty, to make sure they are looking out for the little man. It makes them feel as if they are the messiah to the downtrodden and they can end

up being heroes of the poor. Sadly, they are all mistaken. Rather than helping the poor man out, they end up creating new problems and issues which would not exist in the first place.

Case in point, the price capping policies that governed drug prices in Pakistan for the longest time. It was thought that there was a need for the bureaucrats to look after the quality of medicine being sold in the country while also looking to have a price controlling mechanism. For the manufacturers, this meant that the regulator was able to control the price of the medicine being sold.

The motive for any manufacturer is to maximise the profits he is earning by charging a set price and minimizing his costs. In the scenario of the pharmaceutical companies, manufacturers are at the mercy of the regulator if and when they feel they need to increase their prices. While the quality mandate falls by the wayside, focus is centred around the fact that prices cannot be allowed to change or increase upwards.

The intention behind this motive is pure in nature. Any increase in the price of medicine will hit the wallet of the poor people buying them. Medicine and healthcare should be

something that is affordable and within reach. However, the policy fails to take into account the profit motive of the manufacturer.

The result of such a policy was that the manufacturer would see rising costs with little control over the price they could charge. Seeing their margins shrink, the only option that was left for them was to reduce the quality of raw material in order to reduce cost. The last resort was to stop supply altogether as selling at a lower cost would only increase the losses on their books.

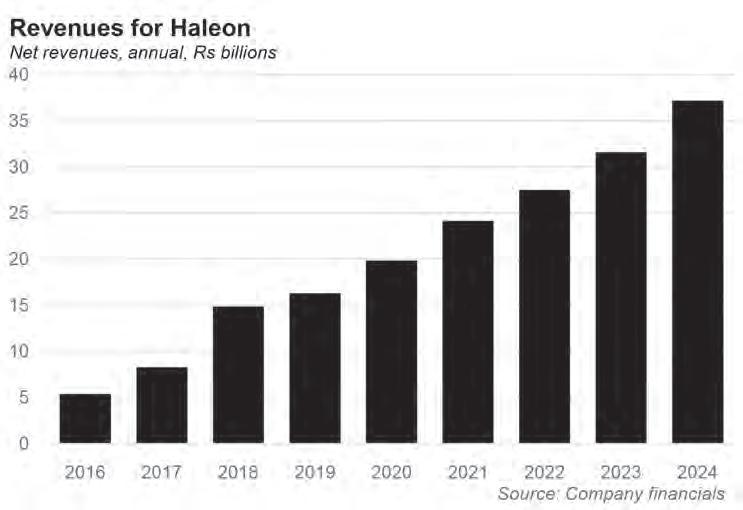

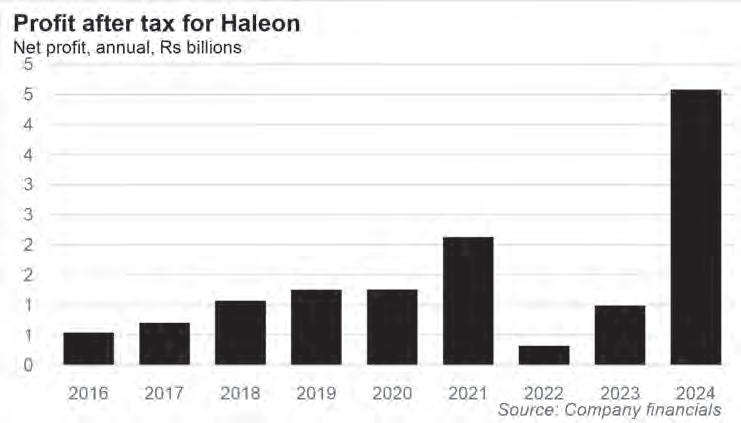

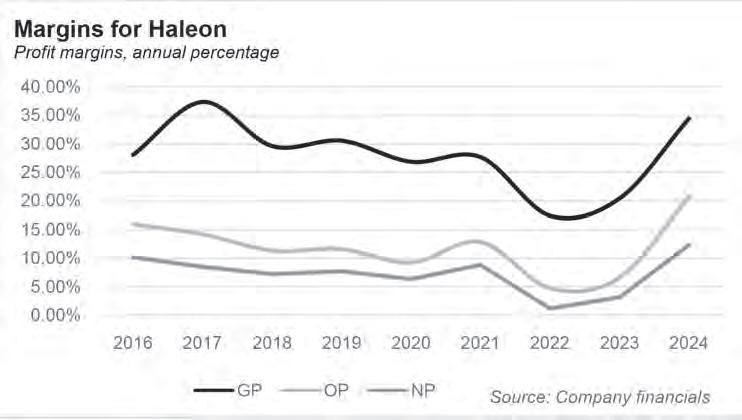

In February 2024, this policy was changed and drug prices were deregulated. With the policy finally being revised, the impact is clear to see on the financial statements of pharmaceutical companies. Haleon Pakistan closed out 2024 with a record high profit of Rs 4.6 billion. This is equal to the profits it earned for the previous 4 years combined. Announcing dividends of Rs 20 per share, it is clear to see that the policy shift has been taken as a positive step by the company and the industry on a whole. How was the previous policy affecting the company and how have the ratios improved in the latest year?

Profit sifts through the numbers to give

a detailed analysis, and tells the full story through one simple drug that has become a household name: Panadol.

If you haven’t heard of Haleon in recent years, it is not your fault. The company is the latest iteration of GlaxoSmithKline (GSK) Pakistan. In 2015, GSK Pakistan demerged its consumer business wing as a separate entity. In 2016, the company started to operate as an independent company and by 2017 it was listed on the stock exchange. By 2018, GSK OTC (Private) Limited was merged with this endeavor and by 2020 this company had the rights to market Panadol in the country. Panadol is considered the flagship product of GSK since the company entered the Pakistani market.

In 2022, Haleon Netherlands took over the consumer healthcare businesses of GSK, Novartis and Pfizer. Due to the merging of these businesses on the international stage, GSK customer health care also went through a change as it was renamed to Haleon Pakistan. Currently, Haleon owns the brand names of Panadol, Voltral, Centrum, Paradontax, Eno and Actified. Panadol alone sold Rs 15 billion worth of sales for the company in 2024.

The performance of Haleon can be broken down into three distinct periods. From 2015 to 2021, from 2022 to 2023 and the last part looking at 2024 by itself. For this analysis, the performance of Haleon in its previous avatars will be merged with the performance of Haleon in 2024 to make the comparison easier to understand.

From 2016 to 2021, Haleon saw its performance grow. After the demerger, the company saw revenues of Rs 5.3 billion in 2016 which grew to Rs 24

billion by the end of 2021. The quadrupling of sales revenue was due to the marketing efforts of its management which was able to grow its topline. The growth in revenues was translated into increase in gross profits which went from Rs 1.5 billion to Rs 6.7 billion in the same period. The same impact was seen on the operating profits and net profits which grew inline with the revenues.

In terms of the gross profit margins, 2016 saw margins of 28%. From then, the margin fluctuated between 37% and 27% before settling in at 28% in 2021. Due to a need for expansion, Haleon saw its operating profit margin fall as it looked to spend a higher amount on marketing and advertising in order to expand its revenue potential. Operating profit margin was 16% in 2016 which had a spread of 13% with gross margin. By 2017, this spread had widened to 23% before coming down to 15% in 2021. Operating margin came

to around 13% in 2021. A similar trend was followed by net profit margin which was at 10% in 2016 before falling to 6.4% in 2020 and ending at 8.8% in 2021.

The profit margins show two trends taking place at the same time. Gross profit margin jumped in the initial years before it came down to the same levels that were being seen in 2016. On the other hand, Haleon started to focus on carrying out additional expenses which meant that operating and net profit margins fell in initial years before coming back to previous levels.

Things started to turn sour starting from 2022. From 2021 to 2022, sales revenue kept going on the upward trajectory as sales increased from Rs 19.8 billion to Rs 24.1 billion. This was a growth of 20%, however, gross profits decreased for the first time in the history of the company. Gross profits actually fell from Rs 6.7 billion a year ago to only Rs 4.8 billion in 2022. A similar fall was seen in operating profit which decreased from Rs 3.1 billion to Rs 1. 3 billion and net profit which decreased from Rs 2.1 billion to Rs 32 crores only.

The ratios also showed how the profitability had decreased. In 2021, gross margins were at 28% which fell to only 17% in 2022. Operating margin fell from 13% to 4.7% and net margin nearly disappeared from 8.8% to 1.2%.

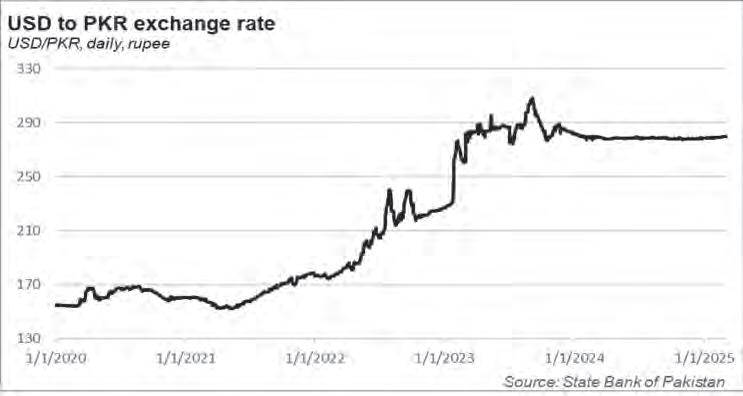

The reason behind the fall in profitability can be attributed to two major reasons. The first reason was that manufacturers were facing higher costs as the rupee depreciated

considerably during this period. Most of the raw material used in the production and manufacturing of medicines has to be imported before it is used in local processing. As the rupee depreciates, imports become more expensive leading to higher cost of sales.

On 1st of January 2021, the exchange rate stood at Rs 160/dollar which had fallen to only Rs 176 by the end of the year. In 2022, however, the exchange rate depreciated to Rs 234/dollar. The rupee depreciated by 33%.

Usually, manufacturers can transfer some of this cost increase by increasing the price of their goods.This makes sure that the margin earned on the product does not fall by the same magnitude as some of the cost increase can be added to the price. In the case of pharmaceuticals, this is not possible. As manufacturers have little control over the price, they have to keep producing seeing their profitability suffer.

In 2022, Pakistan actually saw a shortage of Panadol being available in the market as it would have meant that Haleon would have to take on higher losses if they had kept producing at the prices they had to sell at. Haleon cried over the fact that they could not keep producing in order to decrease losses. On the other hand, the Sindh government launched an anti-hoarding drive against the company alleging that they were keeping a low supply in the market to get a higher price. While both sides kept making accusations against each other, the company saw its financial performance suffer. In 2023, revenues again increased by 15% as the Rs 30 billion threshold was crossed for the first time. During 2023, the rupee further depreciated to Rs 278/dollar which was another depreciation of 19%. The second half of the year finally saw some stability as the rate hovered around the Rs 280/dollar mark. With no change allowed in the price, the gross profit margin slightly improved to 20.4%. Operating and net profit

margins also saw a slight increase to 6.6% and 3% respectively.

The implementation of the new policy could not have come at a better time. In February of 2024, the caretaker government deregulated drug pricing policy with its foot almost out the door and the effect of the change is nothing short of remarkable. The change starts from the revenues of Haleon which again increased by only 17% from Rs 31.6 billion to Rs 37 billion. The real change was seen in gross profits which jumped from Rs 6.4 billion to Rs 12.8 billion. In terms of margins, the ratio jumped from 20% in 2023 to 34% in 2024.

The credit for the huge jump lies with the fact that there was stability in the exchange rate for most of the year which meant that the costs were mostly constant. With the costs being stable, Haleon had the opportunity to increase its prices after the deregulation went into effect. With an increase in price and

a decrease in costs, the margin increased by almost 100% for Haleon. As costs were coming under control, operating profits also increased from Rs 2.1 billion to Rs 7.7 billion while the margin almost tripled from 6.6% to 20.7%.

Lastly, the bottom line also saw an increase from Rs 99 crores to Rs 4.6 billion. The net margin for the company leapt from 3% to 12% in a span of a year. The Earning per share was Rs 8.5 in 2023 and clocked in at Rs 39 in 2024. In order to reward the shareholders, the company also gave out a dividend per share of Rs 20 for the year.

To get a glimpse of how price deregulation actually impacted the company, the price of a humble pill of Panadol can be seen. In November of 2022, one pill had the price of Rs 2.35. By February of 2024, the price was increased to Rs 2.67 per pill. After the deregulation came into effect, the price of Panadol in March of 2025 is being quoted at Rs 3.52 per pill. In a space of less than 3 years, the price has increased by 50%. With little change in cost, most of this was converted into profits. When policies are made in the halls of the bureaucracy, they give little thought to all the stakeholders who would be influenced by these policies. The proverb of path to hell being built on good intentions seems to apply here. When the policy of price regulation was being thought up, the opinion of the manufacturers was never considered. Now that this policy has been thrown out, it is clear to see that the manufacturers are rejoicing.

The regulator has decided to take a back seat in terms of pricing. The responsibility of Drug Regulatory Authority of Pakistan (DRAP) is now to make sure that any price hikes and changes are justified and that no advantage is taken by the manufacturers. DRAP can look to make sure the quality of the product, exorbitant hikes in prices and availability of medicines is assured in the market. n

By Abdullah Niazi

The misappropriation of funds meant for local governments indicates that the bureaucrats running the finance division and successive administrations have either been woefully unaware of constitutional requirements or have remained willfully ignorant

Nearly a trillion rupees are missing from the books of the Punjab government. The money, which has been misappropriated over the course of eight years and six chief ministers, was constitutionally supposed to be handed over by the provincial government to the 229 local governments that exist in Punjab.

These local governments, such as Municipal Committees and Municipal Corporations provide vital services to the people in their jurisdiction and are supposed to be the third constitutional tier of democracy in Pakistan. However, the absence of these funds have brought many of these local governments to the point of bankruptcy. An investigation conducted by Profit revealed a number of local governments do not have the money to pay their utility bills, and the electricity connection for streetlights in their jurisdiction have been cut. In other areas, sanitation workers have gone on strike while employees of these local governments are not receiving their salaries.

So where did this money come from, why was it owed to local governments, and how has the government managed to get away with not paying them their due?

The money, which amounts to at least Rs 828 billion, is part of the Interim Provincial Finance Commission. This was established in Punjab in 2017 as a temporary body pending legislation regarding local governments in Punjab. The PFC acts much as the National Finance Commission (NFC) does. The NFC is supposed to pool taxes collected by Islamabad into a fund and divide it every year between the provinces. The provinces are then supposed to set up PFCs which collect the NFC award, add provincial revenues to this pool, and then allocate a certain portion of these funds to local governments.

Since 2017, the Punjab Government has paid Rs 281.37 billion to local governments in lieu of this money. However, the amount due according to the formula for the division of money created by the Punjab Government itself comes out to almost Rs 1.1 trillion.

The money owed to these LGs has gone largely unnoticed because of the conspicuous lack of elected local governments all over the country. Since the 18th amendment, it has been the responsibility of provincial governments to establish empowered and elected local governments, which all four provinces have failed to do. In Punjab, the disregard for this constitutional requirement has come to a point where the amount due to the 229 local governments spread across the province has just not been released.

The only reason the misappropriation of funds has come to light now is because of the deplorable state many of these local governments

find themselves in, and their inability to keep up with expenses.

Behind this misappropriation of funds is the callous attitude of the Punjab Finance Department and the career bureaucrats that run the economy of Pakistan’s largest province. The finance department’s handling of the PFC award shows an utter disregard for constitutional requirements. At best, it comes from being criminally unaware of the role local governments play in Pakistan’s already ailing democracy. At worst, it is a case of wilful ignorance. This callous attitude was on display only recently, on the 27th of February during a meeting of the Punjab Assembly’s Public Accounts Committee. This also happened to be the meeting from which Profit gained access to some of the raw data that has led us to the misappropriated Rs 828 billion.

Members of the Punjab Assembly are famously not fans of very long meetings. It was apparent at a recent session of the assembly’s Public Accounts Committee (PAC), where despite the provision of tea and sandwiches, the committee adjourned without ripping into

a presentation by the Punjab Finance Division as they should have.

After all, there was more than enough material in there that deserved to be torn to shreds.

The PAC meeting was held after the local governments department complained that the finance division was not disbursing funds from the Provincial Finance Commission that were supposed to go to local governments. It was an issue that never should have come up, largely because it is dictated by a very simple process.

More than a decade ago, the Government of Punjab passed the Punjab Local Governments Act 2013. This piece of legislation set out to establish local bodies in Punjab and empower them as the country’s third tier of democracy, as enshrined in the constitution. Since then, a number of other local government acts have been introduced and passed in the assembly, some of which have helped derail local governments.

There was one in 2019 during the Buzdar administration which resulted in 58,000 elected representatives being told to pack up and go home. Another act introduced in 2022 during the brief ministry of Hamza Shehbaz. While the story of local governments in Punjab

has been shaky (and surprisingly progressive as far the legislation is concerned), the 2013 Act did establish an Interim Provincial Finance Commission (PFC) which came into effect in 2017. The act was passed at the beginning of Shehbaz Sharif’s third stint as Chief Minister of Punjab, and the commission came into effect near the end of it.

As mentioned earlier, the PFC is supposed to disburse a set amount of funds to local governments. A lot of these funds come from Islamabad because taxation is centralised in Pakistan. The Federal Board of Revenue (FBR) still collects many taxes that are supposed to be collected either by provincial or local governments, where it would also be more efficient to collect them. Property tax, for example, is constitutionally a subject of local government. What the federal government does is collect all of these taxes, pool them into the NFC Award, and distribute the funds to the province.

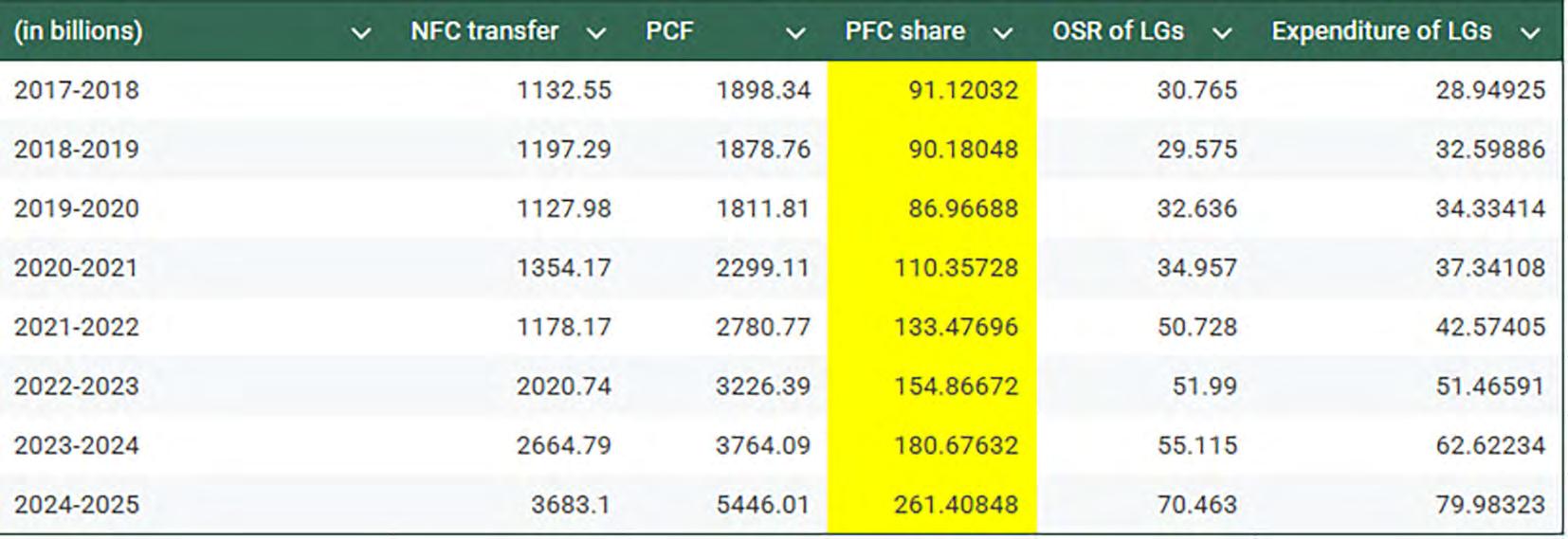

In 2017-18, when the PFC was first established, Punjab’s share of the NFC award was Rs 1.13 trillion. On top of this, the provincial government had its own sources of revenue. The provincial government has non-tax revenues, it also takes on debt by borrowing from banks

and international lenders, as well as provincial taxes. All of this money is pooled together in the Provincial Consolidated Fund (PCF) — essentially a big pool of revenue that the provincial government gets. In 2017-18, this fund was Rs 1.89 trillion. Out of this Rs 1.89 trillion, the Punjab Assembly decided that the provincial government would retain 62.5% while the remaining 37.5% would be distributed.

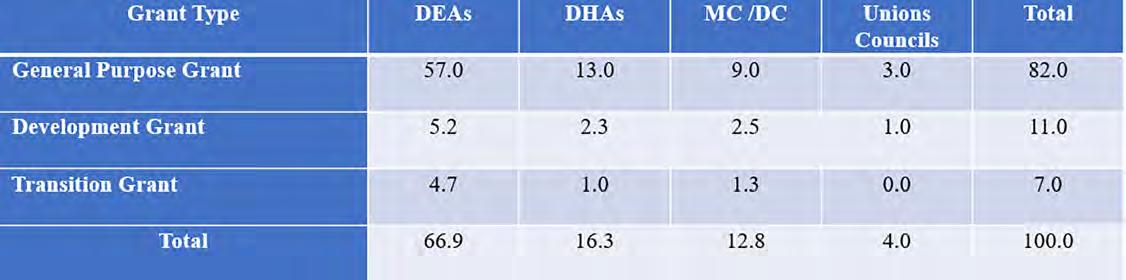

Where would this money be distributed? Well, a big chunk of it would go to District Education Authorities and District Health Authorities, with both of these two major functions receiving 66.9% and 16.3 % respectively. While some might have raised concerns regarding this, it made sense since health and education were both new provincial subjects after the 18th amendment. As part of this formula devised by the Punjab Government itself, out of this money, around 12.8% was also allocated for local governments. Out of the Rs 1.89 trillion consolidated fund, this was a very small chunk of Rs 90 billion. This money is then to be distributed amongst different local governments which can spend them at their discretion.

Up until now, it is a pretty simple equation. Which is why when the local governments department made their presentation in front of the Public Accounts Committee on the 27th of February, the discrepancy in numbers caught some of the members off guard. In 201718, when the share of the local governments was Rs 90 billion, only Rs 36.82 billion were disbursed by the finance division.

That is only the tip of the iceberg. In the years since, local governments have been given around the same amount of money. In fact, every successive year since 2017-18, local governments actually got less money from the PFC than they did that first year. The disbursements have hovered between Rs 32.85 billion to Rs 36.82 billion. This year the amount has increased, with the PFC claiming Rs 46.67 billion will be disbursed to local governments. These are details that can be seen in the table below:

The catch here is that throughout all these years these amounts should have been increasing. The share of local governments in

the PFC award is proportional. That means every year when the NFC payment increases and other provincial revenues increase, so does the Provincial Consolidated Fund. As a result, the amount of money owed also increases for local governments (or it could even decrease) depending upon what the PCF stands at. The same goes for the disbursements that are supposed to go to District Health and Education Authorities.

Unfortunately, the data from these DHAs and DEAs is not available because it has not been shared by either the finance ministry, or the health and education ministries despite multiple requests by Profit. However, during the PAC meeting, the local governments department did share that in 2023-24, the amount of money they received from the PFC was Rs 35.5 billion. However, they claimed that the amount they should have received under the Punjab Government’s own formula for disbursements was Rs 180.67 billion — a gap of nearly Rs 150 billion. The details of this are given in the table below:

These gaps have only increased every year. As we began with, since 2017 the share of local governments in the Provincial Consolidated Fund amounts to Rs 1.1 trillion, out of which they have only received Rs 281.37 billion, leaving a gap of Rs 828 billion in between.

There are many details within this, of course. Some were shared by the local governments department. For example, out of the 12.8% that local governments are supposed to receive, general purpose grants account for nearly 75%, however there are other development grants and the like which are also included in this. The exact distribution is given in the table below:

Within this distribution, taken from the finance ministry’s presentation, union councils are at this point not counted amongst the local governments. On top of this, in the 89 months since September 2017, the outstanding amount owed from just development grants is over Rs 50 billion for these local governments.

During the meeting of the PAC, it was clear that the local government department was feeling the heat from the MCs and DCs they are responsible for coordinating with. It was a fact felt by the members as well. The meeting was chaired by Ahmad Iqbal, the member from Narowal who has been a great advocate for local governments throughout his career. He was also accompanied by the provincial finance minister, Mian Shuja ur Rehman, who directed the finance division’s bureaucrats to redo their math on the subject. Samiullah Khan was another vocal voice.

What was most surprising was the lack of understanding in the presentation of the finance division. Without acknowledging the discrepancy in fund distribution, the finance division’s representatives lumped in development grants and special grants amounting to Rs 140 billion into the money to the local governments. However, their own presentation pointed towards the fact that even out of the money that the government was supposed to disburse to local governments, at least Rs 90 billion had yet to be disbursed. Essentially, the government is giving less money to local governments as it is and they aren’t even giving

them the complete reduced amount.

At one point, when the finance department was under pressure from the members questioning them, one of its representatives brought up the fact that when it came to certain special grants, they were giving the LGs more than their share, and they would like to know what happened with this excess amount. To this point, they were rebuked by the committee’s Chairperson, Ahmad Iqbal, who stressed that the PFC share for local governments was a constitutional issue.

“There seems to be some confusion regarding this issue, but the money owed to local governments is constitutional theirs. We cannot as the provincial government ask them what they are doing with this money,” he said. The meeting ended with Mr Iqbal assigning some homework to the department to go redo some of their mathematics and figure out how much money they owe to the local governments. No updates have been received publicly since then, but the calculations are quite simple.

This is what it comes down to: there is a shocking lack of understanding regarding local governments in Pakistan, even amongst high ranking government functionaries. Local governments are a pillar of the constitution and Pakistan’s already frail democracy can never be complete without elected local representatives.

If the current situation was an indicator of anything, the bureaucrats of the finance division will go back and figure out ways to make two and two equal five. Perhaps they will claim the disbursements were lower because of common expenditures or because of a lack of clarity regarding the formula. What remains is the fact that if elected local representatives had been empowered and functioning in the way the constitution prescribes, they also would have been able to fight for what is owed to them.

For now, Rs 828 billion have been spent elsewhere by the Punjab Government. This is not to blame any party or government in particular. The PFC was established during the end of Shehbaz Sharif’s time as CM of Punjab. It saw over three years of Usman Buzdar, and then the tenures of Hamza Shehbaz, Pervez Elahi, Mohsin Naqvi as caretaker (even though his term lasted longer than Pervez Elahi and Hamza Shehbaz’s terms combined — perhaps an even bigger indicator of the state of democracy in the country than the disregard for local representation), and now finally the tenure of Maryam Nawaz. It is entirely likely that the provincial government spent this money on

good causes, but that is not the point. What matters is what was supposed to happen with these funds. As our readers might have seen in the tables above, the operating expenses of LGs have far exceeded the money they are getting from the Provincial Consolidated Fund. As a result, an already tired and adulterated arm of democracy is left completely hapless.

What makes this worse is the potential of local government. By all accounts, local overnment makes sense. We are not speaking here specifically of any local government acts that have been passed in Pakistan, but generally of a third tier of democracy as a concept. It is a more efficient administrative system and adds another tier to the democratic process, making accountability and access to said administrators a less arduous process than it currently is. It also allows communities to look out for and administer themselves in accordance with their own best interests, and leave legislators in the assemblies to the more important task of actually legislating instead of being caught up in gali mohalla riff raff.

But more than just being a third tier of democracy, having a local bodies system means having a new economic process. In essence, it is not just a new administrative stratification, but also involves the dispensation and spending of money. Things such as education and health that people automatically look towards the provincial government for would now be handled by local representatives. Perhaps most crucially, the ability of local governments to collect taxes and release their own schedule of taxation allows them to make their own money and spend it on themselves rather than waiting for the benevolence of the provincial or federal government.

Currently in Pakistan, the system that operates rather than local body governments is a bloated, vain, and self-contradictory bureaucracy where rather than elected representatives controlling local issues, the district is in essence the fief of a government appointed district commissioner (DC). This not just centralises authority, but means locals with a better understanding of the area’s politics and requirements are not in charge of decision making.

Punjab in particular has a solid history of legislation regarding local government as well. The problem has been that provincial governments fail to let go of the reins and empower these local governments. In 2013, the PML-N passed the PLGA 2013 making the first move to implement local governments in the province. Members were also elected, but these governments were far from empowered. District councils worked on a project to project basis, did not get regular funding, and were heavily dependent not only on the Deputy Commis-

sioner (DC) of the district, but also how well connected they were to the local MNAs and MPAs.

In 2019 there were improvements to this law. The PTI government bulldozed the Local Government Act, 2019, and the Village Panchayat and Neighbourhood Councils (VPNC) Act, 2019 through the provincial assembly on the direct instruction of then prime minister Imran Khan. The Act was progressive, ambitious, and took the issues head on. While he was criticised for dismissing more than 58,000 sitting local government representatives, the Act itself was largely seen as a step in the right direction even by his opponents.

Yet over the three years that his party was in power in Punjab, rather than the Act being implemented and local body elections taking place, Khan’s men in the Punjab rolled back on it, with policies such as the Punjab Spatial Strategy (PSS) and the Punjab Local Government Ordinance 2021, which undermined not just the spirit of the constitution, but the 2019 Act that had been passed by the same government.

In 2022, during the brief Hamza Shehbaz government in the Punjab, another act that improved on the 2019 Act was introduced. The act was one of the first and few things on that government’s legislative agenda, and it went further than any previous act by stripping the chief minister of their discretionary power to dissolve local councils, placing land development authorities under the jurisdiction of Municipal Councils, placing organisations like WASA and TEPA as well as local taxation under the control of the mayors of each district, and forming the Punjab Local Government Commission.

Once again, the implementation of this law in spirit remains. This is the crux of the issue. Even when we talk about nearly a trillion rupees being missing, the problem is it is taken for granted. There is not necessarily any malicious intent behind this, just a callous and frankly dull-minded disregard for local governments.

It is unlikely that the money owed to these local governments will ever make its way to them. What we can hope for is that these LGs are at least given their due in the future, and that the government takes care to remember they are not giving them this money out of the goodness of their heart but because it belongs to them. More than that even, as with every government, now is the time for a choice. Empowering local governments could very well be a lasting legacy for Maryam Nawaz as Chief Minister. It is long overdue, and with the legislative precedent in place, she can make a place in Pakistan’s constitutional history. Only time will tell if flickering streetlamps and pending salaries will spur her into action. n

PBA holds the first Banking Summit, what does it mean for the banking industry and the broader economy?

By Hamza Aurangzeb

Banking in Pakistan is at a crossroads. For too long, the industry has been entrenched in inefficiency, with sluggish adoption of digital tools, crippling regulatory hurdles, and a persistent reliance on outdated financial systems. The economy’s dependency on banks as the primary avenue for growth has only compounded these issues. The reality is stark: Pakistan’s financial infrastructure is far from ready to compete in an increasingly digital, competitive, and globalized marketplace.

But it seems the industry is self-aware of its problems. The question is, are they going to do anything about it? The signs are positive.

On February 24-25, 2025, the Pakistan Banks Association (PBA) convened the first-ever Banking Summit in Karachi. It was billed as a milestone for the country’s banking sector—a rare chance for industry leaders to meet face-to-face with policymakers, discuss the future of finance, and confront the urgent challenges facing Pakistan’s economic health. However, as speakers lined up to extol the virtues of a sector long seen as a lifeline for the country, the true tone of the event was anything but celebratory.

The reality of Pakistan’s banking system was laid bare. Panelists, government officials, and financial experts did not mince words: Pakistan’s banking sector is suffering. Growth has stagnated, financial inclusion remains a challenge, and the economy is burdened by unsustainable debt. The question looming over the summit was clear: can the banking industry find a way to modernize, adapt, and lead Pakistan into a new economic order?

The summit opened with a sobering assessment from Mr. Zafar Masud, Chairman of the Pakistan Banks Association. He highlighted a disconcerting reality: while the banking sector has indeed become the largest tax-paying industry in the country, contributing an estimated Rs. 700 billion in taxes this year, the financial system’s capacity to stimulate real growth is severely limited. Banks are funding the majority of the government’s budget deficit, but this is not a sustainable model. More concerning was Masud’s admission that 74% of private sector lending in Pakistan goes to large corporations, while just 5% flows to small- and medium-sized enterprises (SMEs), which are the lifeblood of any economy.

Moreover, while Pakistan’s banks employ around 200,000 people, Masud’s acknowledgment that the sector must become

more inclusive and serve the wider economy was a tacit admission of its failings. The industry has failed to reach the vast majority of Pakistan’s population, particularly those in rural areas or from lower-income backgrounds. As the country’s population grows, so does the disconnect between financial services and the people who need them the most.

As the summit progressed, it became clear that digital banking is the key to bridging this gap. Yet, even here, Pakistan lags behind. Only 20% of transactions in the country are digital—an embarrassing statistic compared to regional neighbors. Despite the rise of mobile banking during the COVID-19 pandemic, the cash-on-delivery (COD) culture and an estimated Rs. 9.5 trillion in cash circulation continue to hold back progress. The summit participants, however, offered little more than optimistic projections. There was talk of expanding e-KYC (electronic Know Your Customer) systems, digitizing more services, and pushing for greater financial inclusion. But it was evident: these were not the revolutionary ideas the banking sector so desperately needs.

The global economic landscape is shifting. The summit’s international speakers, many of them experts from the US, Europe, and emerging markets, were unanimous in their assessment: the old order, driven by trade, efficiency, and competitive advantage, is collapsing. The new order, dominated by nationalism, protectionism, and an emphasis on state power, is already taking shape. Pakistan, historically a passive participant in global trade, has a unique opportunity to carve out a niche for itself in this emerging era. But only if it can overhaul its financial sector and align itself with the new geopolitical and economic realities.

The United States has already begun turning inward, a trend that began with Pres-

ident Trump’s tariffs on China and has only deepened since. Europe is also recalibrating, with nations looking to shield themselves from the economic power struggles between the US and China. This rising nationalism is leading to a fragmentation of the global economy—and Pakistan must adapt quickly or risk being left behind.

While Pakistan may never have been a key player in the global economic order, it could position itself as an important regional actor. The question is: can Pakistan’s financial institutions rise to the occasion? Can they create financial ecosystems that not only serve local needs but also position the country as a leader in the South Asian region?

One of the most pressing themes of the summit was Pakistan’s staggering fiscal and current account deficits. The country’s reliance on borrowing to fund its operations has resulted in a debt crisis that shows no signs of abating. With roughly 40% of national income spent on servicing debt—one of the highest ratios in the world—Pakistan is shackled by its financial obligations. The banking sector has played a central role in this, with a significant portion of loans issued to fund government deficits. Yet, the country’s banking system lacks the necessary tools to foster innovation and growth in sectors that can drive longterm development.

Experts at the summit pointed out the need for a radical shift in policy to reverse this trend. Pakistan must expand its tax base, privatize state-owned enterprises, and overhaul its energy sector. The banking industry, they argued, must step up by focusing on productive lending to high-potential sectors like agriculture, SMEs, and housing—areas that have been largely neglected in favor of lending to large corporations.

Moreover, the country’s outdated fiscal

Banking is the largest taxpayer sector in the country. In this year alone, we are expecting a contributing of around Rs. 700 billion in taxes,”

Zaffar Masud, Chairman PBA

Technology and climate-resilient financing is reshaping Pakistan’s financial sector. Since technology-enabled financial services are rapidly altering business models and risk profiles of customers, the State Bank is prioritizing digital innovation to enhance financial efficiency and inclusion

Jameel Ahmad, Governor SBP

policy needs an overhaul. Panelists emphasized the need for Pakistan to cut its dependency on foreign borrowing and improve the efficiency of its power sector. Without these structural reforms, Pakistan’s financial system will remain bogged down by unsustainable debt and stagnant growth.

The summit’s focus on digital banking revealed another key issue: technology is not just a nice-to-have, it’s a must-have. If Pakistan’s banking sector is to have any hope of modernizing, it must embrace artificial intelligence (AI), machine learning, and predictive analytics. These tools, speakers argued, have the potential to radically transform the industry, driving down costs, improving customer service, and creating new avenues for growth.

AI can be used for everything from automating customer onboarding to streamlining loan approval processes. Predictive analytics can help banks better assess risk, while machine learning can optimize lending practices. Yet, for this transformation to take place, there must be a cohesive digital strategy—and this is where Pakistan has faltered. While banks like Habib Bank and UBL are leading the charge in

digital innovation, many others are still stuck in the past, with archaic systems and outdated approaches to customer engagement.

The key to success lies in collaboration. The government, regulators, and banks must work together to create a digital ecosystem that benefits all stakeholders. The State Bank of Pakistan (SBP) has already made strides in this direction, with initiatives like e-KYC and policies aimed at improving financial inclusion. However, these efforts will only bear fruit if the banking sector is willing to adopt new technologies and modernize its operations.

As the summit drew to a close, a final, crucial issue emerged: the role of climate-resilient finance. Governor of the State Bank of Pakistan, Jameel Ahmed, addressed this head-on. He pointed to the disastrous floods of 2022 as a reminder of the economic vulnerabilities Pakistan faces in the face of climate change. Banks, he said, must start considering climate-related risks in their financial models, from lending practices to risk assessments.

SBP’s Vision 2028 focuses on integrating climate change into Pakistan’s financial strategy. The introduction of green taxono-

mies, climate risk assessments, and a renewed emphasis on sustainable investments are key components of this vision. While these steps are a positive start, they are just that—a start. The banking sector needs to embrace sustainability not just as a regulatory obligation, but as a core business strategy. The shift to climate-resilient finance will not be easy, but it is necessary for the long-term survival of the banking industry.

The PBA’s Banking Summit was a wake-up call for the financial sector. Pakistan’s banks are at a critical juncture. If they continue down the same path—sticking to outdated models, failing to innovate, and neglecting key sectors of the economy—the country’s financial system will continue to stagnate. But if the banking sector can adapt, embrace digital transformation, and work collaboratively with policymakers to implement structural reforms, it has the potential to lead Pakistan toward a more sustainable, inclusive, and resilient future.

The stakes are high. The world is changing, and Pakistan’s financial system must change with it. There is no time to waste. n

The banking sector needs to focus on productive lending, while the government needs to promote deregulation and minimize red tape. In addition to that the government also needs to focus on fiscal prudence by differentiating between bad costs and good costs

Muhammad Aurangzeb, Finance Minister

By Hamza Aurangzeb

Coworking spaces as we know them today first emerged in the United States around the mid 2000s to deal with the growing demand for shared spaces driven by the rapidly expanding freelance economy and the need for flexible work environments.The first official coworking space, San Francisco Coworking Space, was founded in 2005 by Brad Neuberg. The space provided a collaborative environment, where individuals from the same field could exchange ideas and learn best practices to enhance their products and services. However, the concept goes back further, where hackerspaces like C-base, deemed to be precursors of coworking spaces, were founded as early as 1995 in Berlin.

The idea of Neuberg made coworking spaces popular across the globe, particularly in developed markets like Europe and North America, where such spaces started springing up to cater to this niche demand. Over the years several coworking spaces have emerged that have transformed into major global players like WeWork, Regus (IWG), and Industrious.

When it comes to Pakistan, the country caught on to the trend a little late. Although international chains like Regus were already operating coworking facilities in the country in 2009, it was the year 2016 when the sphere of coworking spaces started gaining momentum in the country. This was the case due to the inception of a nascent gig economy and fledgling startup ecosystem, both of which were evolving quickly due to the launch of high speed 3G and 4G internet in the country a couple of years ago. During this era several local players emerged onto the scene.

However, an unprecedented upsurge in the establishment of commercial real estate for coworking spaces has been observed post COVID-19, where numerous coworking facilities have mushroomed across the country. But why is that the case, have coworking spaces emerged as a successful model within commercial real estate? In this story, Profit explores the evolution of the coworking space industry and its future trajectory.

Coworking spaces provide office space at affordable rates, particularly to small and early stage ventures for whom it is financially infeasible to make a massive upfront investment on infrastructure. This includes lease commitments, administrative overheads, utility payments, maintenance costs, refreshments, printing

facilities, security, IT support, and other expenses. These spaces enable companies to scale efficiently in accordance with their budget and plan. Companies can expand or roll back their operations seamlessly, as additional customized space is available on demand and the ownership of company’s fixed assets is minimal.

Apart from that, these spaces also provide small companies with a sense of community, where they can expand their network by interacting with a diverse range of companies and individuals, enabling the exchange of ideas, the latest market developments, and new skills. It is very much possible that companies might find investment for their next funding round or discover a lucrative business opportunity from within their coworking space community. Additionally, many coworking spaces host roundtable conferences, workshops, and mentorship programs, which further foster innovation and collaboration.

These spaces are strategically located around major business districts, which allows small companies to enhance their brand value by flaunting a posh business address and makes their prospective client base of companies much more accessible that plays a crucial role in business generation.

According to estimates, there are around 449 coworking spaces operational across Pakistan. However, there are five major players in the coworking space industry, where Regus is the only international brand, while four local players include Kickstart, Daftarkhwan, COLABS, and the Hive. Three of them, Kickstart, Daftarkhwan, and the HIVE were founded in 2016, while COLABS was founded in 2019.

Regus, the only international chain of coworking spaces in Pakistan, was founded by Mark Dixon, a Monaco based English billionaire. The company started their operations in the country in 2009 with a single branch at Bahria Complex III, MT Khan Road.

On the other hand, Kickstart was established by three founders, Saad Riaz, Khawaja Raza, and Hassan Shahid. The three founders struggled to find an affordable and flexible working space, which inspired them to find the coworking space. They funded initial operations of the company through their own capital. Similarly, Daftarkhwan was the brainchild of Saad Idrees and Ahmad Habib who wanted to promote entrepreneurial culture in the country through providing premium coworking spaces. The venture Daftarkhwan is backed by investors such as Dubizzle, Walled City Co, and Dot Edu Ventures.

The Hive, another major player, was founded by Owais Zaidi, who established the venture to provide customizable and flexible office solutions for businesses of all sizes. Mr. Zaidi bootstrapped the company by starting out from a single location in Islamabad but today the Hive has a footprint across three major cities. Lastly, COLABS was founded by two brothers Omar Shah and Ali Shah. The founders raised capital from VCs like Indus Valley Capital, Zayn Capital, and Fatima Gobi Ventures to redefine the workspace experience for all segments of the corporate sector in Pakistan through COLABS.

All of these major players are present in almost all three major business centers of Pakistan, Karachi, Lahore, and Islamabad, except COLABS which does not have a branch in Islamabad and Daftarkhwan which does not have a facility in Karachi but is present in Rawalpindi instead. If we had to rank these players by number of locations, then at first place would be Regus, which has 12 coworking spaces, Kickstart will grab the second spot with 10 coworking facilities, Daftarkhwan would be third with 9 branches, fourth will be the Hive with 8 spaces and COLABS will be at last spot with 6 locations.

Since these companies provide premium quality coworking services, they charge higher rents from the rest of the competition. In this segment of premium coworking spaces, the rent for a desk starts from Rs.25,000 per month and goes up to Rs.70,000 per month depending on location and facilities. The total capacity of these coworking spaces range from 4,200 to 5,400 desks, where all of them are operating at an overall occupancy rate of more than 80%, while some at even 97%.

During the outset of the coworking spaces culture in Pakistan in 2016, the general notion was that the coworking spaces are for startups and freelancers, which were given a boost by the evolving entrepreneurial ecosystem and the surging gig economy. While startups and freelancers did use these spaces, they were not the core customer base. Instead, a new segment, initially not on the radar of the coworking spaces emerged as the star category: service export driven SMEs and back-end offices of foreign companies. The SMEs exported services related to accounting, design, consulting, and IT services, but the majority of them exported IT services. This makes complete sense, as IT services companies generally have small to medium sized teams and stable cash flows, making coworking spaces an ideal choice for

their business. No wonder we have witnessed a monumental rise in Pakistan’s IT exports.

This trend continued until Pakistan was hit by the COVID-19 pandemic, which halted the national economy, but there was a silver lining, it expedited technological innovation and adoption in the country. It provided impetus to the local startup ecosystem, enthralling foreign investors who invested mammoth sums of capital, leading to a startup boom in the country post 2020.

During the years 2021 and 2022, almost all startups that had raised funding decided to work through coworking spaces. This meant that the concentration of startups in the customer base of coworking spaces increased significantly. This allowed the coworking spaces to thrive and expand as the startups they catered to were growing at a brisk pace.

Nevertheless, this startup frenzy ended towards the end of 2022, when we saw skyrocketing inflation and huge interest rates spikes in the developed world. It dried up funding for startups particularly in frontier economies like Pakistan, instigating a startup winter that lasts till date. This dry spell for startups has adversely affected coworking spaces to say the least. However, over the past two to three years, the industry has found a new customer segment, large corporations and multinational companies, which have become increasingly interested in its services. Why is it the case?

The world is entering a new global order of multipolarism, characterized by protectionism, as it transitions from a unipolar order dominated by globalization. This has led to an increase in the frequency of black swan events around the globe, as oxymoronic as it may sound, fueling skepticism among countries regarding each other. Hence, large corporations have recalibrated their strategy with regards to capital expenditure, they don’t want to own fixed assets particularly in countries that have precarious economic and political climates.

However, it’s not just that, corporations across many industries are motivated to minimize their capital expenditure and ownership of fixed assets, particularly the ones which are not involved in producing value for the company directly. This strategy allows companies to shrink costs and focus on core business operations, while remaining agile, where it could scale up or down in any market in case of a disruption.

Initially, when the coworking spaces came onto the scene, most of the major operators followed a location based model, where they would pool in capital from multiple investors for establishing a

coworking space at a certain location. These operators would lease property from a landlord using the collective funds and then develop a coworking space on it, where the maintenance, branding, and management were the responsibility of the operator. Since the concept was new and untested, investors demanded high returns from operators, which squeezed margins for operators themselves. The situation exacerbated for the operators during COVID-19, when businesses shut down and many companies terminated their contracts with coworking space operators, however, landlords demanded full rent despite economic slowdown.

The situation obliged operators to redesign their strategy and come up with a new asset-light model. In this model, coworking space operators identify a strategic location and landlord. Afterwards, they launch a coworking space with the landlord as a joint venture, where the landlord spends his own capital for development of the space but it is managed by the operator. As far as the rents are concerned they are distributed between both the landlord and the operator. This model has proven to be highly successful for coworking space operators as it saves them massive upfront costs and enables them to share risk with the landlord appropriately. Nevertheless, the landlord takes on more risk in this model because he bears all the cost for setting up a coworking space. So what’s the catch?

Well, the landlords earn a higher rental yield by participating in this model. They are able to split the gains with the operator obtained through managing a coworking space, which would not have been possible through a vanilla rental agreement with the operator or any other lessee. As per the coworking space operators, the average rental yield for a commercial property is 5% but with this model of coworking spaces, landlords can uplift their yields to about 7.5% to 8%.

Today, most of the operators utilize both models but they prefer the second one. However, there is a third model as well, the franchise model, but it has not been widely adopted by the market, thus far. In this model, operators who have an established brand (franchisor) partner with independent operators (franchisees) in order to expand. The franchisee invests in setting up and running the space, while benefiting from the franchisor’s brand, business model, and support in marketing and operations. In return, it pays franchise fees and royalties to the franchisor. This model enables rapid expansion with lower risk for the franchisor and provides franchisees with a proven framework to attract members and generate revenue.

The coworking space market in Pakistan has gone through multiple highs and lows over the years due to varying economic activity, swaying business models, and concentration of customer base in certain segments such as startups. Nevertheless, major coworking space operators are increasingly inclined towards developing a diversified customer portfolio, including startups, SMEs, freelancers, and large corporations. However, in recent times, operators have been striving tirelessly to onboard large corporations in particular, as they have stable cash flows and large capital reserves, which would provide them recurring revenue and assist them in establishing a truly diversified portfolio.

Apart from that, major operators are also exploring the market for coworking spaces in tier 2 cities like Faisalabad, Multan, Gujranwala, and Peshawar. The demand for coworking spaces and flexible work environments is surging in these cities due to a growing base of businesses and freelancers. Although some local players have emerged in these cities, we are barely scratching the surface. Expansion into these regions would allow operators to tap into a burgeoning demand for flexible workspaces, while benefiting from lower real estate costs compared to major cities. The growing traction for remote work and hybrid models in these regions, present an opportunity for coworking brands to establish early dominance and cater to local entrepreneurs, business outsourcing firms, and regional corporate offices.

Lastly, one major gap that exists in the market is the absence of a centralized marketplace for coworking spaces. There is a need for a dedicated platform that allows customers to compare different coworking spaces based on pricing plans, locations, and amenities. Such a platform will not only augment the accessibility and visibility of coworking spaces but also enhance decision-making for businesses and individuals. We feel that if such an aggregator for coworking spaces is developed, it would redefine how businesses discover and book office spaces.

The advent of coworking spaces has certainly provided the much needed innovation for commercial real estate in Pakistan, where it has raised rental yields for investors, fostered entrepreneurial culture in the country, and served as a focal point for networking and exchanging groundbreaking ideas. Nevertheless, the major operators in the sphere need to ponder how they could further develop this industry. Here’s a hint: they could consider integrating VR/AR technology into their spaces. n

Tazah’s $6.5m preseed funding is fueling a strategic third pivot from agritech to cross-border e-commerce

By Nisma Riaz and Taimoor Hassan

If you’re a startup in Pakistan, you need the superpower of shapeshifting; quick reflexes, a sharp eye for opportunity, and the ability to regear in an entirely new direction if the need presents.

Tazah Technologies knows this reality all too well. Originally launched as an agritech marketplace with ambitions to streamline Pakistan’s fresh produce supply chain, the company has now pivoted into cross-border e-commerce.

Why?

Because in a market where operational hurdles can stall even the most well-funded ventures, adaptability isn’t just a strength, it’s survival. By leveraging its logistical expertise and tech-driven approach, Tazah is now tapping into global trade, proving that sometimes, the best way forward is a completely new path.

This story maps out the journey of how Tazah Technologies navigated a challenging economic landscape, the rationale behind its pivot, and how Zambeel is positioning itself in the highly competitive world of international e-commerce.

Founded in 2021 by former Careem executives Abrar Bajwa and Mohsin Zaka, Tazah embarked on a mission to digitise Pakistan’s agricultural

supply chain. This was a promising company, considering that even though Pakistan is an agricultural economy, the sector accounts for only 23% of the GDP but together with agrobased products fetches 80% of the country’s total export earnings. Yet, the sector remains difficult and the entire supply chain network requires technological advancement to match global standards.

Tazah technologies aimed to revolutionise the movement of produce from farms to retailers, enhancing efficiency and price transparency. Initially, Tazah’s vision was to address the inefficiencies in Pakistan’s agriculture sector. The sector is plagued by fragmented supply chains, leading to inflated prices and significant food wastage. To combat these issues, Tazah developed a B2B marketplace connecting farmers directly with retailers, aiming to streamline operations, reduce post-harvest losses, and ensure that retailers receive high-quality products while farmers gain better market access and fair compensation. Their efforts garnered substantial support, with a $2 million pre-seed funding round in October 2021 led by Global Founders Capital and Zayn Capital, followed by an additional $4.5 million in December 2021, bringing the total pre-seed funding to $6.5 million.

Seven months into business, Tazah realised that something wasn’t right. Despite early successes, including a remarkable 1000% growth shortly after launch, Tazah encountered significant operational challenges. The high costs associated with scaling in a cash-in-

tensive industry, coupled with a tightening venture capital environment, necessitated a reevaluation of their business model. Agritech companies around the world function on a high cash burn model and Tazah realised that it had missed the narrow window of opportunity when this business model would reap high returns. However, they also realised that they had two thirds of the capital still lying around and they had time to switch gears.

Recognising the need for a more sustainable approach, the founders decided to pivot towards a lower cash burn model and started financing the sale and purchase of maize and rice in March 2022.

This model improved margins while reducing burn rates. The company had the advantage of significant remaining capital of around $4 million which provided room to maneuver and Tazah 2.0 was born.

Abrar Bajwa, co-founder of Tazah, told Profit, “This new model was working out for us and we could have even raised an additional $2 million had we kept at it but there was an issue.”

Soon after the pivot from fresh produce to just maize and rice, the company ran into a problem the entire startup ecosystem and other business sectors all know too well.

The macroeconomic conditions of Pakistan became extremely turbulent and lending became increasingly expensive, considering the soaring interest rates. Since Tazah functioned on credit lending and the interest rates were squeezing credit markets, the company found

We made an attempt to sell the same SaaS internationally for about two to three months, but it wasn’t very successful. As we began marketing the product, particularly in the Middle East, we quickly realised that the SaaS infrastructure globally, especially in that region, was far more advanced than what we had built in Pakistan. Closing that gap would have required an additional six to eight months of development just to meet market standards. Ultimately, we decided that investing that much time and effort wasn’t the best path forward

Abrar Bajwa, founder Tazah

itself vulnerable to payment delays and defaults in a low-margin business.

Then, in the third quarter of 2022, came the third pivot and something all startups do when they are desperately clawing at straws, trying not to go under.

Can you guess what?

Well, of course, they started building a software as a service (SaaS) product for agriculture manufacturing, aiming to target another aspect within the agricultural space.

Let’s call it Tazah 3.0, the SaaS chapter.

This product was directed towards digitising and automating the distribution of pesticide and seed manufacturers.

Bajwa recalled, “The traction was such that we had to implement it fully to prove it. Some basic product was developed, after which we took it to the market and started discussions about how much it would sell for - $500 per month, $1000 per month, and what format it would take, etc.”

Continuing, he added, “Then another change happened at the macro level. Imports in Pakistan were completely restricted by the government, remember? Our agriculture industry, especially the pesticide industry, relies on Chinese imports. The precursors they use to mix and create pesticides here- they said their own survival was at stake. “ We don’t even have the raw materials to manufacture what we can sell here. We’ll look at your subscription later.”

Despite the traction Tazah achieved with its revised model, it became clear that external factors were making it increasingly difficult to sustain long-term growth in the agricultural sector.

And there went Tazah’s second pivot down the drain.

The founders had lost all hope in Pakistan by this point. The market was so unreli-

able and always at the mercy of the country’s everchanging macroeconomic conditions that they decided to give up on not just the agriculture sector, but also the country all together.

Bajwa shared, “After these two or three things, where I got some experience, I became somewhat disheartened with Pakistan because things were deteriorating so aggressively at a macroeconomic level that whenever we started something, one problem would lead to another.”

“We made an attempt to sell the same SaaS internationally for about two to three months, but it wasn’t very successful. As we began marketing the product, particularly in the Middle East, we quickly realised that the SaaS infrastructure globally, especially in that region, was far more advanced than what we had built in Pakistan. Closing that gap would have required an additional six to eight months of development just to meet market standards. Ultimately, we decided that investing that much time and effort wasn’t the best path forward.”

When asked whether repurposing their tech stack was necessary for them, Bajwa answered, “My perspective is that a startup’s core business should generate revenue. Simply selling the technology you’ve built isn’t a reliable model for long-term success. While many startups try to pivot by monetising their tech as we did, in most cases, it’s not a sustainable or profitable approach. Instead, the focus should always be on building a business that stands on its own and creates real economic value.”

So, they did what any dedicated team would do; they went back to the drawing board. Again.

They, rather belatedly, realised that Pakistan and culture weren’t the primary considerations. What truly mattered was

building something meaningful that solved a problem for a large number of people. So, they started with a clean slate, this time determined to make it work.

“We started throwing ideas and determining which market made the most sense to target. The closest and most viable option was the UAE,” said Bajwa.

And that is when Tazah was out the window for good. So was the Pakistani market. But one thing they still held strongly was agricultural produce.

Finally, the founders decided that cross-border e-commerce was their calling.

This move would allow them to capitalise on global markets while mitigating domestic operational hurdles.

This strategic shift led to the creation of Tazah Global, a platform designed to connect international food and agriculture buyers with Pakistani produce. By facilitating cross-border trade, Tazah Global aimed to bridge the gap between local suppliers and global demand, opening new revenue streams for Pakistani farmers and businesses. This move positioned Pakistan as a key player in the global agricultural market.

But they knew the sector was volatile and decided to diversify Tazah’s portfolio.

The company expanded its reach through MyZambeel.com, a fully owned subsidiary focused on empowering entrepreneurs via cross-border e-commerce, dedicated to providing efficient warehousing, fulfillment, and logistics services.

MyZambeel sources high-demand products directly from manufacturers in countries like China, India, Pakistan, and the UAE, offering them at OEM prices to resellers in the UAE and Saudi Arabia. This model enabled small and medium-sized enterprises to access quality products competitively, increasing

their income potential.

By building a robust on-ground team, Zambeel ensured seamless operations for SMEs, corporates, and e-commerce companies aiming to enter the MENA region, regardless of their location. This infrastructure reduces operational costs and enhances service quality, making cross-border transactions more accessible and reliable.

When asked whether it is possible for a startup within the agricultural sector to succeed, since all three of Tazah’s attempts failed, Bajwa replied, “There’s definitely potential to build a business in agriculture, but unless you’re working on something highly scientific, like developing new seed technology, it can be incredibly challenging. The main issue is that venture capital thrives on consistent, scalable growth, whereas agriculture is inherently seasonal and influenced by numerous external factors.”

For a VC-backed business, growth is expected to follow a steady upward trajectory, but in agriculture, growth fluctuates due to seasonal cycles and unpredictable market conditions. This mismatch makes agriculture and venture capital a difficult combination.

“What we realized was that many aspects of the agriculture business operate like clockwork, certain products are cheaper at specific times of the year, and there are opportunities to buy and sell strategically. However, when it comes to scaling a pure technology-driven business in agriculture under the VC model, it simply doesn’t align well.”

Launched in August 2023, Zambeel marked a strategic departure from the original vision of Tazah, yet retained the underlying philosophy of leveraging technology to solve inefficiencies in supply chains. And this time not just within the agri sector.

We asked Bajwa why he and his co-founder decided to call this new venture Zambeel.

He explained that the name “Zambeel” has an interesting origin.

“If you go back to folklore, you might remember the legendary character Umro Ayyar. One of his defining traits was his magical bag, in which he could store anything he wanted. In Arabic, zambeel means “bag,” and this mythical sack could hold an endless number of items, making it a fitting inspiration for our platform.”

He shared that the name Zambeel actually predates even Tazah. “Before launching Tazah, Mohsin and I were working on another startup, and Zambeel was a name we had considered back then. When we eventually decided to build this new venture, we

thought, “Why not bring back that name?” So, we revived Zambeel and built it into what it is today.”

But what exactly is Zambeel Logistics and how does it work?

Zambeel operates as a hybrid between a dropshipping supplier and a fulfillment provider. The platform allows small businesses and individual sellers to list products at a retail price while Zambeel manages fulfillment, warehousing, and last-mile delivery.

Bajwa explained, “When users sign up on our platform, they essentially tap into our inventory. Our products are listed at wholesale prices, and sellers pick them up, not physically, but by listing them on their own online stores.”

Continuing, he elaborated, “For example, they create a store on Easy Order, set their own retail prices, and handle digital marketing to generate sales. Once an order comes in, we take care of fulfillment. Let’s say a product is listed at 20 dirhams wholesale, and the delivery cost is another 20 dirhams. The seller might price it at 100 dirhams for their customers. When they receive an order, we handle the delivery for 40 dirhams in total, ensuring a seamless transaction. That’s the core structure of the model.”

Zambeel’s inventory spans electronics, household goods, and kitchenware, marking a complete departure from Tazah’s original focus on agricultural produce.

The new venture’s expansion strategy has been aggressive yet calculated, according to Bajwa. The company initially set up operations in the UAE, recognizing its role as a key international trading hub. Within months, it began attracting sign-ups from India, Bangladesh, Saudi Arabia, and the United States. It then expanded into Saudi Arabia and Kuwait, leveraging its growing expertise in cross-border logistics.

“We started with e-commerce, aiming to help businesses in low-income countries access high-income markets and launch successfully. Our first step was establishing a 3PL business focused on warehousing and fulfillment,” Bajwa explained.

He added, “More recently, we moved into dropshipping, recognizing the demand for this model. Dropshipping has been around for nearly two decades, with major players like CJ Drop Shipping in China generating $20-25 million in monthly revenue. By entering this space, we positioned ourselves as a faster, more efficient alternative, particularly for businesses in the Middle East and South Asia.”

Zambeel has evolved into a multi-faceted business, offering services beyond dropshipping. Customers can purchase inventory, use Zambeel as a logistics partner, or leverage its shipping solutions. While the company initially considered selling its SaaS model externally, it realized the true value lies in the capabilities

it has built internally, which continue to drive growth.

With further regional expansion on the horizon, Bajwa reflected on how their perspective has shifted, “Where we once celebrated launching in new cities within Pakistan, we now scale across entire countries at a much faster pace.”

Today, Zambeel operates multiple business models, from dropshipping and individual sourcing to last-mile delivery and brand partnerships. By diversifying its offerings and expanding into new markets, the company has positioned itself as a key player in the global e-commerce ecosystem.

With this final pivot, the company has not only entered uncharted waters, but also one invested with sharks much bigger than Zambeel.

In the fast-paced world of e-commerce, Zambeel competes with global giants like AliExpress, which has its own B2B dropshipping arm. However, what sets Zambeel apart is its ability to deliver products faster, especially within the Middle East and South Asia, giving it a crucial edge over international players that struggle with long shipping times and complex logistics.

While AliExpress dominates globally, the real competition in this region comes from companies like Tiger, an e-commerce firm that recently secured $55 million in funding, along with a few Moroccan startups optimizing similar models for regional sustainability. Despite these competitors, Zambeel differentiates itself by maintaining a lean, high-efficiency model that ensures profitability on each transaction. This approach, shaped by lessons from Tazah’s earlier challenges, allows the company to scale without high burn rates, a stark contrast to many venture-backed startups that prioritize rapid expansion over financial sustainability.

Expanding across multiple markets presents significant challenges, particularly in navigating diverse regulatory landscapes, trade laws, and tax structures.

The Zambeel team tackled these hurdles through a trial-and-error approach, entering new markets, learning from setbacks, and adapting quickly.

“We had never operated outside Pakistan before,” Bajwa admitted. “Everything we did was based on trust and learning from experience.”

“Each country demands a tailored logistics strategy, shipping cosmetics from China differs from moving fasteners or chips from the UAE to Saudi Arabia. Optimising land and air routes while managing customs regulations in Kuwait, Saudi Arabia, and beyond remains an

ongoing challenge,” he finished explaining.

Zambeel’s expansion has been a continuous learning process. With limited knowledge at the UAE launch, the team adapted on the go. By the time they entered Saudi Arabia, they had refined operations, and when expanding into Kuwait, they leveraged key lessons from previous experiences.

Operating across multiple geographies requires agility. Regulations and market conditions evolve constantly, making flexibility and continuous improvement essential. Zambeel’s ability to embrace change and navigate complexities has been crucial in building a scalable cross-border model.

When asked whether Zambeel is sustainable, Bajwa said, “For Zambeel, sustainability means financial stability, and we have effectively eliminated the “life-or-death” question that plagues many startups. Unlike high-burn models, Zambeel generates profit on every transaction, ensuring a self-sustaining business. With a nine-year runway and minimal burn, we are in a strong financial position.”

As the burn rate decreases, the runway expands exponentially. In fact, Zambeel reached breakeven within just two months, meaning it not only covered costs but even generated a small profit early on. With significant capital reserves, the company can comfortably manage fixed costs while investing in future expansion.

Scaling into new markets naturally comes with additional expenses; hiring teams, acquiring trade licenses, setting up warehouses, and maintaining inventory. These upfront costs are necessary for long-term growth, which is why Zambeel prioritises strategic investments over short-term profitability.

While the company could already generate substantial profits, it operates close to a break-even burn rate to maximize runway and ensure long-term scalability. This approach positions Zambeel for sustainable growth while

maintaining financial flexibility to expand into new regions.

By focusing on operational efficiency, market adaptability, and a sustainable financial model, Zambeel has positioned itself as a formidable competitor in the regional and global e-commerce landscape.

Throughout its pivoting journey, the company managed its $6.5 million in funding strategically.

Bajwa explained, “As we transitioned through different models, we kept our investors informed. When we decided to shut down our initial model, we were upfront about our reasoning—we still had capital, but we didn’t believe it was best deployed in that approach, so we had to pivot. Some investors were initially skeptical, but as market conditions continued to shift, they understood our decision.”

From there, the company moved to a second model and later a third, maintaining transparency at every stage.

“When we pivoted to Zambeel, we once again walked our investors through the challenges of operating in Pakistan, particularly the risks of being a PKR-denominated business. We had raised capital when the exchange rate was around PKR 160 per USD, and within a year, rapid currency devaluation reinforced the need for a more globally resilient model. Our vision remained the same—to build something meaningful and scalable—but the strategy had to evolve,” Bajwa shared.