8 minute read

THE GREEN BEAN PRICE ROLLER-COASTER

THE ICO LOOKS AT GREEN COFFEE’S WILD PRICE RIDE, THE UNDERLYING FACTORS RESPONSIBLE FOR THE LOW-PRICE TREND REVERSAL AND JUST HOW LONG RISING PRICES WILL PREVAIL.

The International Coffee Organization (ICO) has collected, processed, and disseminated coffee statistics and prices for nearly 60 years, serving all coffee stakeholders in a neutral and professional manner. We have recorded and predicted ups and downs, significant volatility, and impact on farmers, exporting countries earnings, industry, and consumers. Now, what is happening in 2021 when we are all still fighting the vicious COVID-19 pandemic and growing weather-related shocks due to overall climate change?

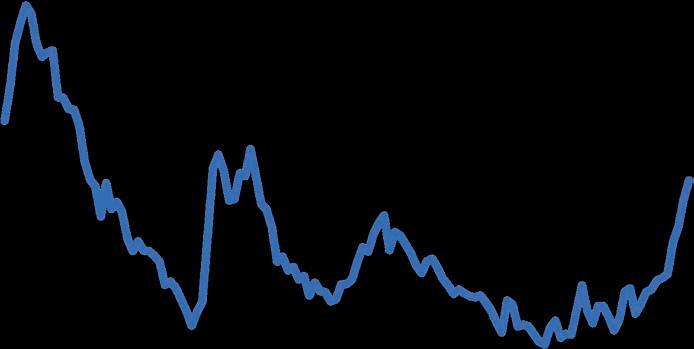

Over the last 10 months, coffee prices have shown signs of recovery after experiencing four years of low levels, as shown by the ICO composite indicator price standing at 160.14 US cents per pound in August 2021, which represents an increase of 51.3 per cent over October 2020, the beginning of the current coffee year. The monthly average of the ICO composite indicator in August 2021 is the highest level since 162.17 US cents per pound recorded in November 2014.

The prices of both types of coffee, Arabica, and Robusta have increased, although gains have been less marked in the case of Robusta coffee. The prices of the two washed Arabica groups (Colombian Milds and Other Milds) increased by 46.1 per cent and 42.2 per cent respectively, with respect to their levels recorded in October 2020. For Colombian Milds, the price of 225.40 US cents per pound reached in August 2021 is the highest since the mark of 244.14 US cents per pound registered in February 2012.

The price of Brazilian Naturals (unwashed Arabica) increased by 74.2 per cent from 100.37 US cents per pound in October 2020 to 174.89 US cents per pound in August 2021, representing the highest level since 181.43 US cents per pound registered in November 2014. The Robusta price in August 2021 increased by 39.2 per cent to 95.18 US cents per pound from the monthly average of 68.36 US cents per pound in October 2020, and is also the highest monthly average since 98.39 US cents per pound recorded in October 2017. These upward trends have also been observed in New York futures exchange, which reflects the market for Arabica, and in London futures exchange for Robusta.

Price movements since the start of coffee year October 2020 to September 2021 seem to mark an end to the low-price levels that had worsened the dire leaving conditions of millions of coffee growers worldwide over the past four years. But what are the factors underlying this trend reversal? And how long will these rising prices prevail?

260

ICO Composite Indicator Price since October 2010

240

220

200

180

US cents/lb

160

140

120

100

80

60

Oct-10 Oct-11 Oct-12 Oct-13 Oct-14 Oct-15 Oct-16 Oct-17 Oct-18 Oct-19 Oct-20

In 2021, the ICO composite indicator reached its highest point since November 2014.

Great profiles are even easier to develop when you can add artificial intelligence to your roast machine!

“I like the idea, similar to curve prediction, that this feature keeps future events front of mind for the roaster. Reminding us that we are working towards time and temperature goals. For training someone I would use the feature, to keep the subject of first crack planning front of mind.” - Paul Arnephy, Cafe Lomi

FIRST CRACK PREDICTION IS HERE

350

300

250

200

150 ICO Group Indicator Prices - Monthly average since October 2010

100

50

Oct-10 Nov-11 Dec-12 Jan-14 Feb-15 Mar-16 Apr-17 May-18 Jun-19 Jul-20 Aug-21

Colombian Milds Other Milds Brazilian naturals Robusta

The sharpest upturn in coffee prices can be observed in Arabica coffees: Brazilian naturals, Colombian Milds, and Other Milds, with Robusta experiencing less significant gains.

SUPPLY/DEMAND DYNAMICS

As in the case of most agricultural commodities, the main factors responsible for the movements of coffee prices are related to supply and demand, particularly production and consumption. However, less fundamental factors, such as US dollar exchange rate movements and futures markets affect trading activities and superimpose themselves on the underlying fundamentals to influence coffee price behaviour and volatility. In coffee year 2020/21, total production is projected at 169.6 million 60-kilogram bags while world consumption for the same period is estimated at 167 million bags, resulting to an excess production of 2.6 million bags over consumption. However, this surplus has been considerably reduced compared to its level in coffee year 2019/20. Nevertheless, in statistical terms the dynamics of the supply/demand ratio alone cannot explain price movements over the past 30 years.

The factors underlying the recent upward movement of coffee prices are mainly weatherrelated shocks that have increased concerns over supply while consumption is beginning to grow again. The weather-related shocks started with a drought in Brazil from late 2020 to mid-2021. In November 2020, hurricanes Eta and Iota hit Central America, with severe impacts in Honduras and Nicaragua. And more recently, in July 2021, many Arabica-growing areas in Brazil were hit by one of the most intense frosts in living memory, with serious damage expected to affect Brazilian output for several years. Brazilian production for crop year 2021/22, which started last April 2021, had already been expected to fall significantly, since this is the off year in the production cycle of Arabica coffee. Moreover, the concentration of origins has fed a widespread concern over the availability of quality coffee, triggering price volatility. For coffee year 2020/21, out of 56 coffee-producing countries in the world, just three countries – Brazil, Vietnam, and Colombia – account for 63 per cent of the world production. When the next three largest producing countries are considered – Indonesia, Ethiopia, and Honduras – these six countries represent more than 78 per cent of world coffee output.

In regional terms, Brazil and Colombia in South America represent 45.9 per cent of world production. Vietnam and Indonesia representing Asia and Oceania produced 24.2 per cent, Africa, Ethiopia and Uganda represent 7.7 per cent world production, while Mexico and Honduras for Central America and Mexico region represented 5.9 per cent. Altogether, the two countries selected in each region (eight countries in total) represented 83.7 per cent of the world production in crop year 2020/21.

PANDEMIC FACTOR

Another important stress factor in the current price trends is the COVID-19 pandemic as supply chains have experienced disruptions due to lockdowns and restriction measures, leading to delays in shipments, lack of containers, and rising freight costs. The spread of the virus in coffee-exporting countries has disrupted local economies, restricted supply of labour for harvesting and affected production by reducing farm maintenance.

For instance, recent stricter lockdown measures are expected to slow down Vietnam’s production and export in the next few months. The ICO has launched its second online survey to monitor the impact of COVID-19 in member countries. The objective of the survey is to assist ICO Members and the global coffee community by assessing the short and long-term impacts on the coffee sector and to identify migration measures available and needed resources.

WILL THE CURRENT TREND CONTINUE?

Looking ahead, these price swings are likely to continue, particularly since climate factors increase the probability of shortterm supply shocks. There are too many variables in the supply/demand equation to be more specific. However, it should be noted that supply is still on the tight side while demand is returning to the level that prevailed before the pandemic. Moreover, with the easing of pandemic restrictions and subsequent prospects of economic recovery, world consumption is expected to continue growing.

If consumption continues to grow at the average rate of 2 per cent per year that has prevailed since 1990, it will exceed 184 million bags in the next five years. World production may not be able to grow at the same rate, since major climatic or environmental disasters can never be ruled out with such a high concentration of origins.

Such an event would force prices up further. Although current price levels are encouraging for coffee growers, escalating costs due to rising prices of inputs, reduction in the availability of labour for farm activities in certain producing countries and decreasing availability of land due to global warming are important limiting factors to production. Coffee is a labour-intensive crop, with little mechanisation in many producing countries, and global urban wages are generally increasing.

Moreover, the increased cost of fertilisers is likely to erode the gains from current high price levels. In coffee farming, the nutrients most widely needed to enrich soils and improve yields are nitrogen, potassium, and phosphates. Nitrogen plays a key role in the healthy growth of the coffee tree, and the formation of new branches and leaves. Potassium is necessary for fruit and seed formation, while phosphate fertilisers contribute to the development of roots, flowering, and fructification. The costs of these fertilisers, already at high levels, are expected to increase further in 2022.

Finally, there is another important market factor that can also influence markets and complicate forecasting: the significant resources available to non-commercial positions in commodity futures markets. These funds are often managed by operators who may not have inherent attachment to a specific commodity and little experience of it. Often, their positions are not based on the traditional fundamentals of the market but on external considerations or even guided by decision of software packages.

The history of coffee is one of price booms and busts, in which the former almost invariably ushers in the latter. The current situation is no exception. With increasing concentration of origins in fewer countries, weather will remain the key driver of the coffee market. Consequently, any concerns over supply from these origins, unless substantial gains in productivity would be achieved quickly and effectively, will intensify price volatility. GCR

ABOUT US

This article was written by Denis Seudieu, Chief Economist of the International Coffee Organization (ICO). In April 1996, Seudieu was appointed Chief Economist at the ICO in London, heading the economic and projects section. He has contributed to the elaboration, monitoring and evaluation of many development projects benefitting coffee sector in producing countries. Over the past 25 years, Seudieu has participated, as speaker to various seminars and conferences. The ICO is the main intergovernmental organisation for coffee, bringing together exporting and importing governments to tackle the challenges facing the world coffee sector through international cooperation. For more information, visit www.ico.org