6 minute read

Colliers Property Focus

INDUSTRIAL & LOGISTICS PRICING OUTLOOK

In this month’s column, Colliers provides MHD with an in-depth analysis of the pricing of industrial real estate assets.

Around the globe, several key economic thematics have emerged that have the potential to impact the pricing of real estate assets. Australia’s industrial and logistics sector is not immune to these risks as inflationary pressure and a higher interest rate environment have the potential to impact asset pricing and investment decisions going forward.

Over the past quarter, the industrial yield compression cycle has slowed; however, the good news for the sector is that income growth is at its highest level in decades, supporting asset pricing and will drive asset performance over the next five years.

Real 10-year Bonds vs. National Prime Industrial Yield

Headline inflation has increased sharply over the past six months, reaching 5.1 per cent year on year to March 2022 – the fastest pace of annual inflation since the introduction of the GST in 2000. Supply chain disruptions have been a critical cog in this upward movement, and given these disruptions are expected to persist for at least the next 12 months given the backlog at key ports, further pressure on inflation is expected and could exceed 7.0 per cent by Q3 2022.

Off the back of this, interest rates which provide a crucial backdrop to real estate pricing have begun to increase, and the view is that they will reach 1.5 per cent or higher by Christmas. Borrowing costs were already heading north before the Reserve Bank of Australia’s (RBA) recent decision and commercial loan rates now range between 2.5 per cent and 4.5 per cent, while the weighted average cost of debt for the REIT sector measured 3.1 per cent in December 2021. Given the outlook for further rate rises, commercial loan rates are expected to follow a similar path.

Nominal bond yields have also shifted higher off the back of higher rate expectations from the RBA with the 10-year Government bond yield more than tripling from the low point of 0.82 per cent in October 2020 to its current ~3.5 per cent. Notwithstanding this, the real risk-free rate (Government bonds adjusted for inflation) remains low at close to 0.0 per cent, and while the spread to industrial yields is lower than historical averages, industrial and logistics assets have been re-priced given the strong macro tailwinds recorded in recent years and historical averages are no longer relevant. Nonetheless, the rise in bond yields and interest rates will undoubtedly limit further yield compression within the sector.

WHAT DOES THIS MEAN FOR INDUSTRIAL AND LOGISTICS YIELDS?

Concerns surrounding rising interest rates are causing investors to assess their underwriting, particularly for core investments in the $100 million or above price bracket due to the higher

prevalence of financing. As a result, we expect the impacts on industrial and logistics yields will be two-tiered, with sharper pricing expected for assets with shorter lease expiry profiles, providing the ability for investors to capture imminent rental growth upside.

With both interest rates and borrowing costs increasing, the yield compression cycle appears to be over and there are likely to be cases and markets where some cap rate expansion may occur. However, we do not anticipate a blowout of yields but rather a 25-50 basis point softening in most cases and markets while selected markets are likely to see greater yield reversion where the depth of capital is more limited. The reality is that there remains a significant volume of unsatisfied capital in the order of $50 billion looking to be placed in the sector, which will support asset pricing well below historical averages.

While rising debt costs are now front and centre of investors’ investment strategies, the impacts on pricing will also be mitigated to some extent given low gearing levels through conservative debt management, including highinterest cover ratios. Generally, gearing levels within the listed sector now average ~30.0 per cent, which is well below the 50 per cent or more gearing levels recorded pre-GFC. Similarly, with higher interest rates impacting levered returns, cash-focused buyers are expected to be active and competitive in transactions.

SHORT WALE ASSETS TO BE FAVOURED

While demand for long WALE assets is expected to remain strong from longer-term investors (including super funds), there has been a noticeable shift in demand for industrial and logistics assets with a shorter lease expiry profile, given the ability to drive rents and capture positive rental reversions sooner.

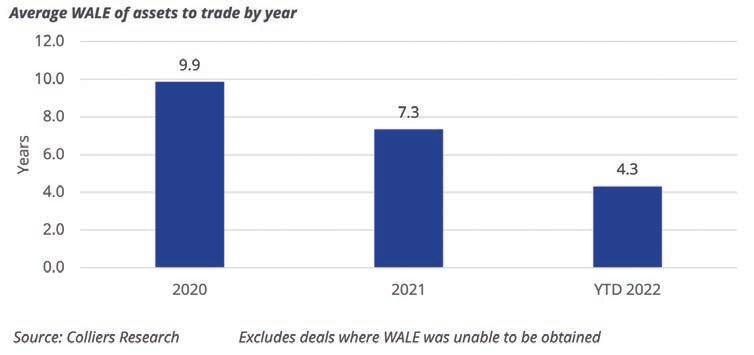

To highlight the shift in demand, we have analysed the average WALE of transactions since 2020. In 2020 and 2021, the average WALE for assets to trade was 9.9 years and 7.3 years, respectively and reflected demand for longer WALE assets at the time, given the security of income they provided in a period of economic uncertainty. Alternatively, of the transactions to occur so far in 2022, the average WALE measured just 4.3 years.

For shorter WALE assets, prospective purchasers will be willing to pay a low initial yield given the immediate upside in rents and subsequently, some modest compression in yields could occur for these assets.

Average WALE of assets to trade by year

Fundamentals within the occupier market remain favourable and income growth is expected to be the primary driver behind asset performance over the next five years. Investors recognise the income potential and are offsetting increased capital costs and inflation risk by underwriting rental growth of 7.0 per cent or more in most markets. In the 12 months to Q1 2022, prime rents grew by almost 10.0 per cent at a national level and similar rates of rental growth are forecast over the next two years.

History suggests that rental growth tends to accelerate during times of high inflation. This is the case given that most rental agreements are tied to inflation and carry an inbuilt hedge. While industrial rental data is not available for the 1970s and 1980s when inflation averaged 8.0 per cent (reaching a high of 17.7 per cent in March 1975), CBD office data highlights the impacts on rents through this period. Between 1970 and 1990, net face rents for Sydney CBD office assets increased by 10.9 per cent per annum on average while through the early to mid-1980s, rental growth in excess of 25 per cent was recorded for some years. Rental growth for the Melbourne CBD was even more pronounced at 12.2 per cent per annum over the same period.

In summary, our view is that rising interest rates will have modest impacts on industrial and logistics values in 2022 through a modest softening of cap rates. However, the pick-up in rents is expected to offset this and asset values are expected to be preserved. Our analysis shows that if yields were to soften by 25 basis points, a ~7.0 per cent increase in rents would be needed to preserve asset values which are well under the forecast rental increases in most markets in 2022. Well-capitalized buyers with strong lending relationships who can get aggressive debt pricing will have an advantage in this rising interest rate environment. ■