Part I: Assessing Housing Needs and Policy Tools in New Jersey

A. Current Housing Needs in New Jersey

Housing affordability is shrinking in New Jersey. Although the state’s median income is in the top ten nationwide, there is significant income inequality and racial segregation.3 In 2017, nearly one in five New Jersey households spent at least half of their income on housing costs.4 That same year, New Jersey had the highest foreclosure rate in the country.5 Additionally, with 565 municipalities and an emphasis on “home rule” (i.e., local autonomy of municipalities) New Jersey has prolific and difficult-to-navigate zoning requirements that reduce available affordable housing stock. The Mount Laurel Doctrine, established by the New Jersey Supreme Court in the 1970s and 1980s, requires each municipality to provide for its “fair share” of the regional affordable housing need.6 But political opposition rendered the state Council on Affordable Housing ineffective beginning in the early 2000s, and unmet affordable housing need grew. In 2018, a New Jersey Superior Court trial judge declared unmet fair housing needs to be greater than 150,000 homes for the period 1999–2025.7

Quick Facts on Housing Cost Burden in New Jersey (2018 data):

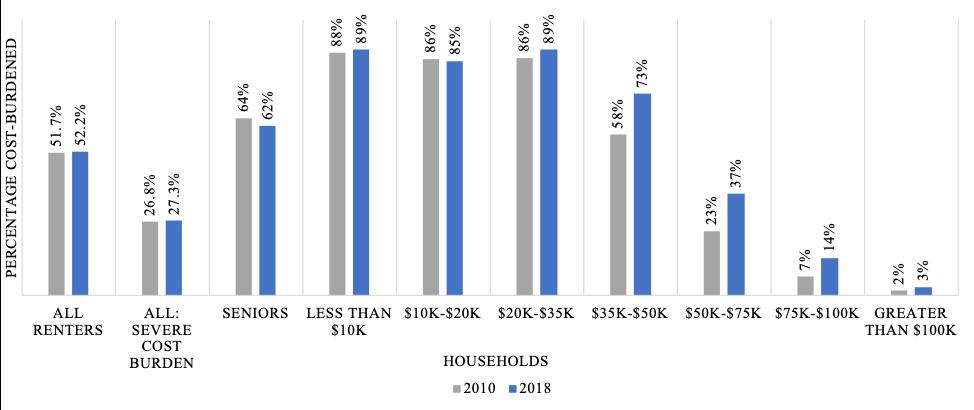

• Half of all renters in New Jersey are cost-burdened. Nearly three in ten renters spend more than half of their income on housing (i.e., are severely cost-burdened).

• 84% of New Jersey renters earning less than $50,000 per year are cost-burdened.

• The portion of renters who are cost-burdened rose by 0.5 percentage points since 2010 in New Jersey even as it fell by 0.7 percentage points across the USA.

Despite the economic expansion after the Great Recession, the rising cost of housing and other basic expenses has outpaced wage growth.8 States like New Jersey suffer from two key problems: first, wage stagnation makes housing less affordable for households. Second, housing costs are rising quickly because there are not enough homes to meet diverse housing needs across different income levels. Barriers to housing construction include, but are not limited to, rising cost of construction material, limited supply of land, and restrictive zoning laws.

Data Source: US Census Bureau, “2014-2018 ACS 5-Year Estimates”.

Figure 1: What Qualifies as Lower Income for a Family of Four in New Jersey?

The National Low Income Housing Coalition ranked New Jersey as the fifth most unaffordable state for renters in 2019. The average renter in New Jersey earned $18.68 per hour, which is enough to afford an apartment with a $971 monthly rent. But the Fair Market Rent for a two-bedroom apartment was $1,501, which would be affordable only for a worker earning an hourly wage of $28.86 or greater.9 Moreover, in 2017, 573,000 renter households and 699,000 owner households were cost-burdened.10

A close look at the data on cost burden levels reveals a greater need to prioritize NJHMFA’s resources to serve very low-income (VLI) and low-income households. Figure 1 shows various income levels of New Jersey households earning less than 80% of the area median income (AMI).

Data Source: U.S. Department of Housing and Urban Development

9

% of AMI 2019 2018 Moderate Income 80% $80,400 $76,100 Low Income 50% $50,250 $47,550 Very Low Income (VLI) 30% $30,150 $28,550

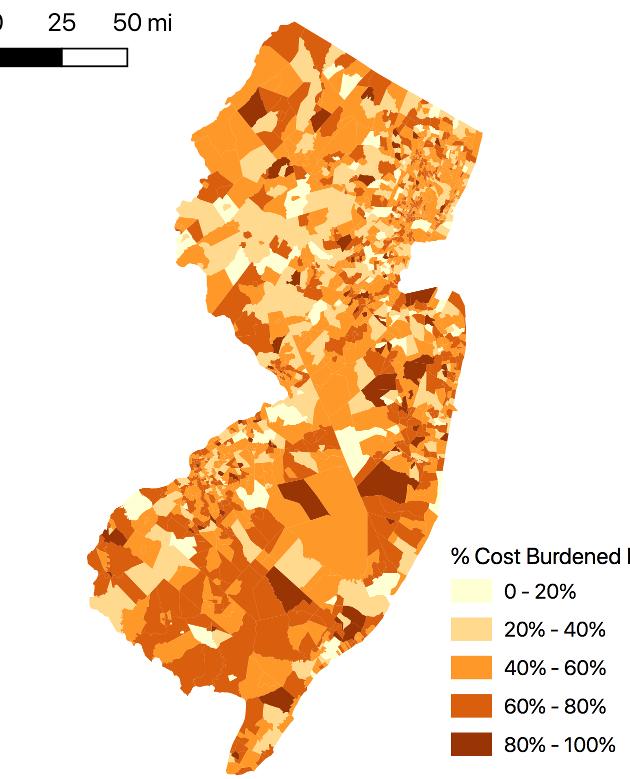

As Figure 2 shows, many more lower-income households are cost-burdened than are higher-income households, and cost burden will have detrimental impacts on these households now and in the future. VLI and low-income households are more likely to spend a greater portion of their incomes on housing and other necessities compared to higher-income groups.11 Therefore, among housing cost-burdened VLI and low-income households, an economic shock—e.g., a job loss or a large health-related expense—is more likely to force these families to cut spending on necessities or to risk eviction. This is particularly relevant with some economists predicting another recession within the next two years.12 Government intervention may be needed to prevent a vicious cycle that can lead to homelessness and displacement.

Figure 2: Cost Burden Share Across Renter Households in 2010 and 2018

Data Source: U.S. Census Bureau, 2006-2010 American Community Survey 5-year Estimates; 2014-2018 American Community Survey 5-year Estimates.

Note: excludes households whose cost burden data could not be calculated, which is about 5% of the renter population in New Jersey. The dollar figures are based on household income.

Housing needs among seniors are also dire, but NJHMFA’s targeted efforts to serve this population seem to be working. Three in five renters over the age of 65 are cost-burdened. However, as Figure 2 shows, the portion of senior renters who are cost-burdened fell since 2010 (from 64.1% to 61.7%), even as it barely moved in the country (from 61.1% to 61.0%). In New Jersey, the number of senior renters increased by 20% from 2010 to 2018 while the number of cost-burdened senior renters increased by 16%. Meanwhile, both the number of senior renters and the number of cost-burdened senior renters increased by 30% over the same time period in the country.

The improvements in New Jersey may be attributable in part to NJHMFA’s programs that fund housing for seniors. Since 2010, the Agency has funded with LIHTC approximately 2,500 senior units across the state. Moreover, the share of LIHTC units allocated for seniors rose from 24% in 2013 to 45% in 2017.13 The QAP’s strategic allocation of LIHTC to seniors may explain some of the change in cost burden rates among seniors.

The need for affordable housing in New Jersey is particularly acute among those who qualify for supportive housing. Supportive housing provides affordable rents and voluntary onsite services to assist those whose life experiences or health conditions impose barriers to securing and maintaining stable housing. In New Jersey, individuals who are experiencing homelessness, are living with a disability, have previously been incarcerated, have aged out of foster care, are in treatment for a substance use disorder, or are living with HIV/AIDS are among those eligible for supportive housing.14

The number of individuals in New Jersey who may qualify for supportive housing is staggering. Presently, 142,750 people with limited resources and living with a disability receive Supplemental Security Income (SSI) in New Jersey.15 The state has 18,514 veterans living in poverty.16 It has a homeless population of 9,398, a number which is likely underestimated.17 There are presently 34,820 incarcerated people, and exiting the criminal justice system leaves some homeless.18 New Jersey has 10,916 children in the foster care system, and

10

Data source: U.S. Census Bureau, 2014-2018 American Community Survey 5-year Estimates. For interactive versions of the maps in this report, visit: http://bit.ly/WWS-NJHMFA-Storymap

18% of this population is age 14 or older.19 Upon turning 18, these children will age out of the system, which leaves an estimated one in five youth homeless.20 New Jersey also has a particularly large population of individuals facing substance use issues. For every 100,000 people in the state, there are 352 opioid use-related hospitalizations and 21.5 opioid-related deaths, a significantly higher rate than the national average of 14.2 deaths per 100,000 people.21 The Corporation for Supportive Housing estimates New Jersey’s supportive housing need at 17,987 units, excluding seniors.22 Since 2010, NJHMFA has allocated LIHTC credits for nearly 1,700 affordable supportive housing units.23 As with New Jersey’s affordable housing stock, there are simply not enough supportive housing units to meet the underlying need. It is crucial that state agencies work to meet the supportive housing needs of the most vulnerable New Jerseyans, whose circumstances compound the challenge of securing safe, secure, and decent housing.

B. Projected Trends in Housing Needs in New Jersey

Population shifts must inform housing needs assessments. The state’s growth depends upon its ability to retain young people, maintain a thriving labor force, meet the needs of children and seniors, and maintain housing affordability while keeping up with demand. Understanding population projections can help NJHMFA prepare for the housing needs of a future New Jersey with a residential makeup different than today’s.

Population and labor force projections from the New Jersey Department of Labor and Workforce Development (NJDOLWD) show that by 2034, the average age of New Jersey’s residents will dramatically shift. NJDOLWD expects the senior population to increase by 63% by 2030, making seniors nearly 20% of the total

11

Figure 3: Cost Burdened Households by Census Tract in 2018

Among housing cost-burdened low-income households, an economic shock— e.g., a job loss or a large health-related expense— is more likely to force these families to cut spending on necessities or to risk eviction.

population.24 Meanwhile, the population of children in middle school and younger (age 14 and below) is not expected to grow significantly by 2034. In eight counties, this population is expected to decrease by 2034. These age trends may have a significant impact on labor force participation rates, as the share of working age residents between the ages of 18–64 years old is expected to decline.

The importance of the housing market for seniors will intensify, and the housing preferences and growth patterns from decades ago will have important modern-day implications for seniors in the state. As seniors age in place, they find themselves in suburban, car-dependent neighborhoods. Given the housing stock of the state, many seniors will be living in single-family homes without easy access to neighborhood amenities, increasing their risk of social isolation.25

Access to affordable housing is critical for seniors, particularly as incomes tend to decrease with age. Across metropolitan areas in New Jersey, the proportion of households headed by those age 65 and older who are cost-burdened ranges from 25% to 46%. Trenton, Newark, and Jersey City all have some of the highest rates in the nation of cost-burdened homeowners age 65 and older.26

Population shifts and changes in housing demand and value will also be impacted by climate change, which should be considered as part of the state’s population projections, smart growth strategies, and planning. With high sea level rises, an estimated 79,000 New Jerseyans would see their homes “chronically inundated” by floods (defined as 26 floods per year) by 2045, and the homes of an additional 375,727 people would be chronically inundated by 2100.27 Currently, mortgage lenders and other financial entities critical to the housing market, including NJHMFA, do not consider climate change projections beyond whether a property is located in a 100-year flood plain, and 30-year home mortgages may not be available in areas with predicted flooding as the market gets more sophisticated in risk analysis.28 In light of New Jersey’s coastal geography, NJHMFA should include anticipated displacement and destabilization caused by climate change in its future forecasting and planning.

C. Opportunity and Smart Growth in New Jersey

Addressing housing needs requires creating enough units, ensuring they are affordable, and building them in the “right” locations. Selecting the “right” locations for affordable housing often centers on whether the location provides a household with access to economic opportunity and high-performing schools as well as on whether building in the location follows “smart growth” principles. Understanding the qualities of high-opportunity areas and smart growth areas helps shed light on where and how NJHMFA presently incentivizes affordable housing development and how it should do so in the future.

Incentivizing development in high-opportunity areas creates potential benefits stretching across generations. Simply put, where you live matters. Location determines access to well-paying jobs, high-performing schools, and ample food options. In the context of affordable housing development, there is no single accepted definition of opportunity. That has not stopped policymakers from attempting to pinpoint opportunity and incentivize it. An analysis conducted by the National Housing Trust found that all states attempt to promote building in opportunity-rich neighborhoods in some manner through their QAPs.29 How and to what extent opportunity is incentivized varies greatly.

In New Jersey, smart growth policies currently play a key role in how the state defines opportunity and shapes its planning efforts. New Jersey’s brief definition of smart growth is found in the New Jersey State Development and Redevelopment Plan, which was adopted in 2001. NJHMFA’s definition of smart growth reads:

“Smart growth areas” means areas that promote growth in compact forms and protect the character of existing stable communities. A compact form of development combines an efficient use of land, natural resources, and public services. An area shall be considered to be a smart growth area if it is within Planning Area 1 [metropolitan], Planning Area 2 [suburban], or within a Designated Center on the State Plan Policy Map. In the Pinelands Area, an area shall be considered to be a smart growth area if it is within a Regional Growth Area, a Pinelands Village, or a Pinelands Town.30

12

Though not included in NJHMFA’s definition of smart growth, key features of smart growth policies also include walkable communities, mixed-use centers, a variety of housing and transportation choices, increased land-use density, and environmental conservation. Smart growth increases residents’ freedom to choose where they live, work, and play by engaging community members in development decisions, pursuing environmentally sustainable development, preserving open space and agriculture, making the most of existing infrastructure, and maximizing options for where a family can live and how they can get around.31 These considerations are especially important in the Garden State. New Jersey is coastal, has the densest population in the country, and is squeezed between New York City and Philadelphia at the center of the East Coast megalopolis. These factors present planners with acute challenges related to the environment, economic development, and infrastructure.

According to the Smart Growth Network, the basic principles of smart growth encourage municipalities to:

• Mix land uses

• Take advantage of compact building design

• Create a range of housing opportunities and choices

• Create walkable neighborhoods

• Foster distinctive, attractive communities with a strong sense of place

• Preserve open space, farmland, natural beauty, and critical environmental areas

• Strengthen and direct development towards existing communities

• Provide a variety of transportation choices

• Make development decisions predictable, fair, and cost effective

• Encourage community and stakeholder collaboration in development decisions

Source: The Smart Growth Network, “What Is Smart Growth?,” March 16, 2015.

D. Responsibilities and Roles of NJHMFA and Other State Stakeholders

Promoting a variety and choice of housing opportunities in New Jersey is a team effort that requires political will and coordination. Responsibility for affordable housing programs is divided among several State agencies, particularly NJHMFA and the Department of Community Affairs (DCA). NJHMFA is “established under, but is not a part of” DCA, though the Commissioner of the Department of Community Affairs—currently Lieutenant Governor Sheila Oliver—is ex officio chair of NJHMFA.32

Programs administered by NJHMFA include LIHTC, Section 811 Rental Subsidy for development of supportive housing for people living with disabilities, preservation financing, and the Special Needs Housing Trust Fund. It also administers single-family homeownership programs such as the Down Payment Assistance Program for first-time homebuyers. NJHMFA has relatively few sources of “soft funds” directly under its control—i.e., grants and other funding to fill financing gaps and ensure projects are feasible. To secure gap financing to complete the capital stack for an affordable housing project, a developer may seek out financing from other government agencies in addition to NJHMFA, as well as from private or nonprofit sources.

In New Jersey, DCA administers U.S. Department of Housing and Urban Development (HUD) programs, such as Section 8 Housing Choice Vouchers, the National Housing Trust Fund (NHTF), Community Development Block Grants (CDBG), and the HOME Investment Partnerships block grants. It also oversees the state-level

13

State Rental Assistance Program (SRAP), the Neighborhood Revitalization Tax Credit (NRTC), and Neighborhood Preservation Balanced Housing funds, also known as the New Jersey Affordable Housing Trust Fund (AHTF). In some other states, housing finance agencies administer these kinds of programs. Two other state-level agencies—the New Jersey Economic Development Authority (NJEDA) and the New Jersey Redevelopment Authority (NJRA)—provide some funding for projects that include affordable housing components, although these agencies’ primary functions are related to economic development and business growth. Additionally, the Office of Planning Advocacy (OPA) oversees the New Jersey State Development and Redevelopment Plan, which guides statewide development, and the Department of Human Services (DHS) has a role in supportive housing. Other levels of government also have responsibility for affordable housing financing. For example, in addition to DCA, 27 New Jersey counties and municipalities administer HUD HOME funding. Additionally, following a 2009 state law, counties are permitted to charge a document fee to establish county-level Homeless Trust Funds, and at least 11 such funds have been created.33 Figure 4 summarizes how responsibility for several key affordable housing programs and related programmatic areas is divided among various agencies in New Jersey.

Figure 4: Responsibility for Key New Jersey Affordable Housing Programs, Financing, and Planning

14

NJHMFA DCA NJEDA NJRA DHS OPA Courts County & Local Gvt Federal LIHTC X HUD ConPlan programs X HOME X X CDBG and CDBG-DR X (DR) X Housing Choice vouchers X Housing Trust Fund X Section 811 Rental Subsidy X State Bond financing X X X X AHTF X SRAP X State Plan X Economic development tax credits X X NRTC X Special Needs Housing Trust Fund X Supportive housing funding (various sources) X X X Fair share housing plans X X Homelessness funding (various sources) X X X

The construction of affordable homes is generally completed by either for-profit or nonprofit developers. Both types of developers access financing from NJHMFA and other agencies. For-profit developers are more likely to complete the kinds of large-scale projects supported by financing tools such as LIHTC, while nonprofit community development corporations tend to complete smaller projects in targeted regions. New Jersey has many active nonprofit community development corporations; however, their productivity has declined in recent years due to sustained cuts to statewide affordable housing funding.34

Part II: Analysis and Recommendations for NJHMFA

As the analysis in Part I indicates, New Jersey needs to build significantly more affordable housing, and need for affordable housing is especially great among low-income and VLI households, seniors, and special needs populations. Part II identifies ways NJHMFA should address these needs using its most powerful financing and policy tools. It focuses on areas where the Agency has the greatest opportunity to maximize housing production and to advance other affordability and smart growth objectives, drawing on best practices from other states.

The following recommendations are addressed to NJHMFA, recognizing the constraints of a housing finance agency while also taking into account how the state as a whole can best allocate its resources to increase affordable housing supply.

A. Update the Qualified Allocation Plan to Address Identified Areas of Need

A QAP is a state’s plan for LIHTC allocation. In states like New Jersey where LIHTC allocation is a highly competitive process, the QAP functions as a tool to score developers’ applications for these tax credits. NJHMFA maintains New Jersey’s QAP and allocates the state’s share of LIHTC. Policy goals are embedded within the QAP; for example, QAPs may allocate points based on characteristics such as a project’s location, proximity to community resources, or energy efficiency.35 The QAP can encourage developers to meet the needs of underserved populations by awarding extra points for projects that set aside units for special populations or keep units affordable for long periods of time. The QAP is a powerful tool, allowing states to encourage or discourage development in certain areas. For instance, in New Jersey, the QAP allocates points for “ready to grow areas,” Opportunity Zones, and Targeted Urban Municipalities (TUMs).

Given the ability of the QAP to advance policy goals, we recommend several revisions to the QAP to help address New Jersey’s affordable housing needs. Some of these QAP recommendations are designed to incentivize lower development costs, while other recommendations may increase development costs by incentivizing services for populations with greater needs, by promoting deeper or longer affordability, or by encouraging more expensive features of design or location. The former group of recommendations would allow NJHMFA to expand quantity—i.e., to build more affordable housing. The latter group would result in better quality of affordable housing and help address areas of high need, but it could result in fewer units of affordable housing overall. When implementing reforms, the Agency should incorporate an evaluation process to review this tradeoff and to measure the outcomes of new incentives.

1. Increase access to high-opportunity areas.

While changes to New Jersey’s QAP over the years have successfully decreased the number of LIHTC properties sited in high-poverty areas, there is less conclusive evidence that they have otherwise meaningfully increased residents’ access to opportunity. A number of studies have demonstrated NJHMFA’s success in deconcentrating poverty. For example, analysis conducted by New Jersey Future found NJHMFA’s 2013 QAP changes reduced the number of LIHTC projects sited in neighborhoods with concentrated poverty by 29.8

15

percentage points.36 However, as john a. powell, head of the Haas Institute for a Fair and Inclusive Society at the University of California, Berkeley notes, poverty is more than just a measure of the poverty rate; it must be considered within a web of opportunity.37 A variety of factors make up that web, from education and healthcare to steady and well-paid employment.

The National Housing Trust identifies five overarching themes prevalent in state QAP definitions of opportunity:

1. Access to Education: Does the QAP prioritize neighborhoods with access to schools and/or universities?

2. Economic Jobs/Growth: Does the QAP prioritize access to jobs and/or low unemployment rates within a community?

3. Income Levels: Does the QAP prioritize areas with high income levels and/or low poverty rates?

4. Access to Health Care: Does the QAP prioritize hospitals, doctors and/or health services in close proximity?

5. Access to Transportation: Does the QAP prioritize access to public transportation and/or shorter commute times?

Source: National Housing Trust & Freddie Mac Multifamily, “Opportunity Incentives in LIHTC Qualified Allocation Plans,” 2018.

Currently, NJHMFA addresses these broader aspects of opportunity through point incentives for proximity to “positive land uses.” The list of positive land uses includes items with a logical connection to opportunity (e.g., high-performing schools, daycare centers, and full-service supermarkets), but it also includes items with a more tenuous connection to opportunity (e.g., post offices, county court houses, and department stores).38 Notably, in contrast to the majority of states, NJHMFA does not maintain an explicit definition of what constitutes a high-opportunity area in its QAP. More than half of all states use an explicit definition in their QAP, and 59% have a definition that is mappable or is already mapped statewide.39 NJHMFA does, however, use the Municipal Revitalization Index (MRI) created by DCA to identify and map TUMs. These are cities with high levels of distress that NJHMFA prioritizes for investment through an allocation set-aside. NJHMFA has the expertise to monitor and map geographic quality. Currently, however, this expertise is used to drive investment to distressed areas without a corresponding analysis of access to opportunity.

An explicit, mappable definition of opportunity provides a host of benefits. Most importantly, it offers a more nuanced and cohesive picture of the factors that affect outcomes for families. A composite measure acknowledges that it is not proximity to any single land use, but rather a confluence of many factors, that determines the level of opportunity in a neighborhood.

When incentivizing transit-oriented development (TOD), NJHMFA should consider the

following:

1. Service Type: Distinguish between hard rail, light rail, and bus rapid transit, as well as the service type (e.g., commuter rail vs. daily service).

2. Service Frequency: Prioritize more frequent service. The generally accepted standard for high frequency transit is service every 15 minutes, but NJ should identify it’s own parameters.

3. Transit Access: Take into consideration pedestrian access to transit. Projects that have a connected sidewalk to a transit station are much more valuable than a project close to a station but on the other side of the highway.

4. Population Density: Consider areas that have the necessary population density or potential zoning to support high frequency transit.

16

A precise, mappable definition of opportunity also sends a much clearer signal to developers about areas they should consider siting projects. Indeed, one complaint that arose in interviews with affordable housing developers in New Jersey is the difficulty in adhering to arbitrary proximity measures to things such as transit stops. As it is currently constructed, the QAP’s point allocation for positive land-use does not necessarily reflect conditions of the overall neighborhood nor whether those land-uses generate meaningful opportunities for households. Identifying opportunity at the neighborhood or regional level could simplify this process and reduce the gamesmanship it encourages. It can also spur positive changes within the Agency itself.

Housing finance agencies interviewed for this report that have incorporated an opportunity map into their QAPs acknowledged it made them more likely to track and evaluate the effectiveness of their policies over time. It should be noted, however, that the purpose of the LIHTC program is not solely to maximize access to opportunity. The program was originally designed also to spur investment in distressed, lower-income communities, with the hope of revitalizing underinvested neighborhoods. As NJHMFA considers how to better incentivize opportunity, it should be mindful of this dual purpose of the program as well as the systemic racism that has driven racial segregation and racist housing policies, depriving some majority-minority communities of resources and leading neighborhoods to be designated as “low opportunity.” Figure 5 visualizes one possible opportunity index for the state of New Jersey.

A very high opportunity tract has:

(a) a low unemployment rate

(b) a high median household income

(c) a low rate of adults with less than a high school degree

(d) a low rate of severely cost-burdened renters

(e) a low child poverty rate

(f) a rate of individuals without health insurance

Z-scores were calculated for each indicator and averaged across census tracts. The results were then broken into quintiles, with equal numbers of tracts in each bin.

Data source: U.S. Census Bureau, 2013-2017 American Community Survey 5-year Estimates; NJHMFA-provided data on LIHTC allocations. For interactive versions of the maps in this report, visit: http://bit.ly WWS-NJHMFA-Storymap

The map displays a relative comparison of New Jersey census tracts based on a composite index of opportunity measures. The index is modeled after the one used by the Ohio Housing Finance Agency, using the methodology developed by the Kirwan Institute at the Ohio State University.40 This index is intended as a proof of concept. The index uses normalized census tract level data for six indicators across education, health and

17

Opportunity

Very Low Low Moderate High Very High Legend

9% LIHTC Allocations 2010-18

Census Tracts

Mapping Opportunity in New Jersey Figure 5: New Jersey Opportunity Map

the economy. For example, a very high-opportunity tract has: (a) a low unemployment rate, (b) a high median household income, (c) a low rate of adults with less than a high school degree, (d) a low rate of severely cost-burdened renters, (e) a low child poverty rate, and (f) a low rate of individuals without health insurance. Each census tract is assigned a composite score and then broken into quantiles (i.e., the top 20% of scores are designated “very high” opportunity, the next 20% “high opportunity” and so on). Using this measure, only 29% of 9% LIHTC-funded properties between 2010 and 2018 were located in census tracts designated as high- or very high-opportunity areas. The indicators in this measure overlap with those included in the MRI. Median household income and the unemployment rate are included in both, as are measures of educational attainment and poverty. If used to prioritize cities with a low rank, the MRI could function as the basis of an opportunity index. It should be noted, however, that the MRI was constructed fundamentally as a measure of distress, not opportunity. As such, it does not currently include measures related to criteria like health or transportation that a curated opportunity index might consider and which also determine the relative opportunity of a place.

NJHMFA deserves credit for success in deconcentrating poverty. This success shows the Agency already has the tools to proactively promote opportunity. To this end, we recommend that NJHMFA implement the following policy changes.

a. Create an explicit definition of opportunity and use it to identify and map regions for tax credit allocation priority.

The index mapped in this report provides a place to start, but we recommend NJHMFA work with other state agencies (e.g., DCA, Department of Health) to refine the measures that represent opportunity in the New Jersey context. This could be achieved by creating a new opportunity index or by expanding the measures included in the MRI to more broadly encompass the factors contributing to opportunity.

NJHMFA should also conduct a survey or otherwise gather feedback from LIHTC project residents to better understand residents’ perceptions of opportunity. Research demonstrates that resident perceptions of opportunity often differ from what statistics can capture.41 Therefore, NJHMFA’s definition of opportunity would benefit from being informed by, and evaluated based on, the lived experience of households and perceptions of their own opportunity and wellbeing.42

An opportunity index could be piloted with a set-aside allocation of tax credits for a project in a high-opportunity area in a future funding round. Using a map or index does not mean that existing incentives, like proximity to high performing schools, need to be eliminated. The opportunity map could be layered on top of existing incentives or set-asides (to preserve the urban/suburban split, for example). Ohio began its opportunity map as a pilot for a few select counties before expanding statewide. We recommend a similar pilot phase to test the measures in the index that best capture opportunity in the New Jersey context, measured against economic, health, and resident satisfaction outcomes.

b. Make it easier for affordable housing developers to build in high-opportunity areas.

This recommendation addresses two aspirations: to make it easier for developers to build in high-opportunity areas, and at the same time ensure that low-income and very low-income renters can afford rents in these new buildings. Developments in high-opportunity areas tend to have higher-than-average total development costs due to constraints such as higher construction costs, a lack of buildable parcels, and greater zoning and regulatory barriers. These costs reduce the likelihood of affordable housing being built in high-opportunity neighborhoods. To offset this effect, NJHMFA could award 30% basis boosts to projects seeking to build in designated high opportunity areas. The power to award such basis boosts at their discretion was granted to HFAs under the Housing and Economic Recovery Act of 2008. The Texas HFA incorporated a 30% basis boost for high opportunity areas in 2010 and saw a significant increase in the number of units built in those areas.43

As NJHMFA makes it easier to build in higher opportunity areas, the Agency must also ensure units are accessible to those most in need. Because LIHTC rents are pegged to AMI, buildings in higher-opportunity areas tend to command higher rents. In some cases, even subsidized LIHTC rents are too high for very

18

low-income renters to afford without additional subsidies because regular operation and maintenance costs alone can be prohibitively high for very low-income renters.44 Therefore, to ensure buildings in high opportunity areas also serve very low-income renters, NJHMFA could pair the 30% basis boost with a required unit set-aside for individuals making 0% to 30% of AMI. Michigan, for example, offers a 20% basis boost to projects restricting 20% of their total units to 30% AMI or less.45 This set-aside requirement would be independent of the income-averaging incentives discussed in the next section.

2. Extend affordability of LIHTC units.

NJHMFA can leverage existing funds to increase future affordable housing supply by extending the life of affordable units. LIHTC projects that reach the end of their affordability periods are at risk of conversion to market-rate units. Unlike in some states where a greater share of LIHTC allocations go to nonprofit development organizations with indefinite affordability baked into their missions, the majority of sponsors utilizing LIHTC credits in New Jersey are for-profit developers. The pro forma revenue projections of these for-profit developers reflect an expectation of market-rate conversions. NJHMFA can create new points or a set-aside of tax credits to incentivize developers to commit to affordability periods beyond even 45 years. Since there is a strong competition for the 9% credits, developers are likely to extend the affordability of their projects to maximize their points on the QAP.

For example, Oregon’s QAP requires 60 years of affordability on all 9% projects.46 Even with this requirement, Oregon’s 9% credits have been consistently oversubscribed.47 The City of Portland has gone a step further and added a 99-year affordability requirement in its Inclusionary Housing program.48

It is important to note that longer affordability requirements will effectively commit the state, municipalities, and developers to refinancing of the affordable project regardless of how the real estate market may change after 30 years. While planning for long-term affordability may make sense in hot real estate markets, requiring more than 30 years of affordability in some municipalities also creates the risk that affordable housing projects will be located in places where a longer subsidy would not help NJHMFA achieve its mission. Moreover, total development cost can be higher with longer affordability requirements because the developer needs to set aside a greater capital reserve for significant expenses occurring after 30 years. As such, while we expect for-profit developers would adapt to this change, we do not anticipate they would do so eagerly.

To extend affordability, NJHMFA can also incorporate a “right of first refusal” for all 9% credit projects. This would give the state or mission-driven nonprofit organizations the first opportunity to acquire LIHTC projects at the end of their affordability periods. In order to ensure the projects are available at a reasonable price, NJHMFA should also set price restrictions on the resale price of a project at the end of the affordability period when a right of first refusal is exercised. Specifically, NJHMFA can tie the maximum resale price to the federally-determined AMI to ensure the state or other sponsor has a reasonable opportunity to acquire the building. For example, a building occupied by residents with incomes at 50% of AMI should be priced such that the new sponsor can continue renting to residents with similar levels of income. In essence, the resale value of an affordable housing project should move in proportion with the changes in AMI. This contractual arrangement would give NJHMFA future flexibility to preserve affordable units, and thus reduce displacement, without committing itself to the financing of a specific building and its surrounding real estate market after the end of the initial affordability period.

Washington State’s Department of Revenue has published a Low-Income Housing Valuation Guide49 to help calculate an appropriate sale price of LIHTC projects. A series of formulas is used to set a maximum sales price. One of the valuation methods generates two estimates: a Restricted Leased Fee Value using

19

Photo credit: NJHMFA 2019

income-limited rents and an Unrestricted Market Value using market rents. The final value of the project is set in between the two estimates and depends on the discount rate that is used. This guide can be a template from which NJHMFA establishes its own methodology.

NJHMFA can also extend affordability by limiting use of qualified contracts. This can be accomplished by either requiring or incentivizing that they be waived in the QAP. Currently, LIHTC property owners are allowed to sell properties after 15 years by requesting a “qualified contract” from the Agency. If NJHMFA cannot find a buyer for the qualified contract within a year after the owner has declared their intent to sell, then the owner is released from all LIHTC restrictions. This process threatens rent affordability for all developments in the extended use period, but it can be prevented if the owner has waived their right to seek a qualified contract.

To address this, many states have introduced point incentives or requirements in their QAPs for waiving the right to request a qualified contract. South Carolina awards five points for waiving the right and Tennessee awards four to ten points for deferring requests for qualified contracts.50 In 2019, Oregon and Virginia changed their QAPs to require the waiver for all future LIHTC projects.51 While it is unclear whether an outright restriction on qualified contracts is more appropriate than point incentives, NJHMFA should choose one of these two options to prevent loss of rent affordability after the fifteenth year.

3. Encourage deeper affordability.

Trends in housing affordability indicate a greater need to focus LIHTC allocations toward households earning less than 50% of AMI. To participate in the LIHTC program, a development must meet one of the following conditions: at least 20% of its units are affordable for households at or below 50% AMI, or at least 40% of the units must have an average affordability equal to or below 60% AMI (with the maximum allowable rent being affordable to households at 80% AMI). Although deeper affordability is technically permitted, as both options allow for underwriting rents below the AMI thresholds, for-profit developers are financially incentivized to maximize revenues by setting rents as high as possible while still remaining LIHTC-eligible. Additionally, designating “the least amount of tax credit per tax unit” as a tiebreaker for project funding in the QAP discourages deep affordability, since these developments often require more tax credits per unit. Indeed, the share of LIHTC units targeted at households earning less than 50% of AMI has been trending downward in New Jersey, from 59% in 2013 to 45% in 2017.52

NJHMFA currently encourages deeper affordability in its QAP by offering one bonus point to applications that underwrite 20% of units (not including those with other rental assistance) for rents affordable to households earning 30% AMI or below.53 However, developers can also claim the same bonus point by setting aside at least 20% of their units for market-rate tenants or by using NJHMFA’s traditional multifamily pooled permanent bond financing, so it’s unclear whether this incentive impacts affordability. Because of the relative lack of supply of units affordable below 50% AMI, NJHMFA should adjust its QAP to incentivize the development of housing affordable to New Jersey households with incomes below 50% of AMI using one or several of the recommendations below.

a. Introduce sliding-scale incentives for income averaging and non-tax credit leverage.

NJHMFA should consider a sliding-scale incentive that awards more points to applications proposing to serve lower average income levels. A sliding-scale incentive provides a progressively larger point award as performance on a desired metric improves. In this case, as the average rent (corresponding to a certain income level measured as a percentage of AMI) falls for a proposed development, its application will receive more points, up to a specified maximum. Maryland and Washington State currently have versions of sliding scales for deeper affordability, and South Carolina has proposed adding one for its 2020 QAP.54 By itself, however, a sliding-scale income-averaging incentive may not be wise at a time when NJHMFA is trying to maintain its level of financing support while all federal Superstorm Sandy disaster recovery funding has been committed by the Agency. Without complementary cost-containment incentives in the QAP, winning projects will likely require a greater per-unit tax credit subsidy. Since the tiebreaker—the main reward for developments with a smaller per-unit LIHTC subsidy—would be rendered less meaningful by a sliding scale, an income-averaging sliding scale should also be paired with a sliding scale incentive to limit the per-unit LIHTC subsidy. As the

20

percentage of non-state financing per unit increases, an application will receive more points, up to a specified maximum. Care must be taken to specifically define “non-state financing” to meet NJHMFA goals. As an example, Maryland includes Community Development Block Grant funds and other rental housing resources administered by its HFA in its definition of state financing, while allowing Multifamily Bond Program proceeds, basis boost equity, and demolition funds to count toward the “leveraged” amount.55

Taken together, these point incentives are likely to be more effective than requirements to set aside a certain percentage of units at a lower income level. The combination of these two incentives obliges developers to

Maryland’s Department of Housing and Community Development (DHCD) prioritizes serving lower income households with its 9% tax credit allocation, awarding up to 10 points (out of 200) for pricing rents affordable from an average household income of 55.5% AMI down to 32% AMI. The award increases from zero points at 55.5% AMI by a half-point for every 1.5-point drop in the target AMI household income band.

Source: Maryland Department of Housing & Community Development, “Multifamily Rental Financing Program Guide: Attachment to Maryland Qualified Allocation Plan for the Allocation of Federal Low Income Housing Tax Credits,” February 14, 2019.

trade off points between the two scales to reach the lowest average AMI in the most efficient way possible. The sliding scales should be designed such that it is difficult to achieve perfect scores simultaneously on both scales. For example, NJHMFA might consider awarding up to three points for developments proposing to price rents down to an average of 40% or 45% of AMI across the development, which likely would be challenging to achieve without a large amount of LIHTC financing per unit.

Use of sliding scales for income averaging and tax credit leveraging would provide NJHMFA with the added benefit of making perfect scores and ties much less likely. Ties have been common in prior NJHFMA funding rounds, and the tiebreaker has been the lowest tax credit cost per unit. When ties are commonplace, the tiebreaker necessarily becomes the decisive criterion determining which projects are funded. By reducing the frequency of ties, sliding scales would give NJHMFA more flexibility to differentiate along several measures in awarding credits rather than relying so heavily on the cost containment criteria.

When used to promote deeper affordability, sliding-scale point incentives have consequences NJHMFA must anticipate. First, as described, the tiebreaker incentive will become less relevant. Second, it is possible that these incentives will inadvertently advantage projects in higher-income areas. Because rents are set as a percentage of AMI, a project in a higher income area will generate greater rental revenues, and thus more operating income, than an equivalent project in a lower-income area. If deeper affordability is rewarded through the QAP, developers may find it increasingly difficult for projects in lower-income areas to both be competitive and to be financially feasible. For this reason, some states like Washington have bifurcated their sliding-scale incentives so that projects in lower-income areas receive more points for the same average AMI.56 Note that NJHMFA may find one or both of these consequences to be beneficial.

b. Adjust the caps on tax credit allocations and per-unit total developments costs for the Supportive Housing Cycle.

Affordability could also be incentivized within a specific cycle, and the Supportive Housing Cycle would be a good candidate. Supportive housing is one of the most difficult forms of affordable housing to make financially feasible, due to high operating costs for ongoing supportive services combined with rent caps to ensure its affordability for tenants with special needs. Currently, the QAP places a cap on tax credit allocations per project ($1.4 million for the Supportive Housing Cycle and the Senior Cycle, $1.75 million for Family Cycle) and per-unit total development costs from $275,000 to $325,000, depending on the number of stories in the building.57 Adjusting the values such that the Supportive Housing Cycle has a higher maximum per-unit total development cost than the Family or Senior Cycles could help supportive housing developers assemble a larger capital stack, providing additional financial bandwidth to serve lower AMI households.

21

4. Improve targeting of special needs populations.

Supportive housing can take a variety of forms, but generally it is affordable, permanent, income-restricted housing that offers voluntary social and/or health services for individuals with special needs. These units are typically designed for residents with incomes below 50% AMI who pay no more than 30% of their income towards rent. Permanent Supportive Housing (PSH)—where residents have leases in their own names and full tenant rights, regardless of whether they participate in support services—originally started as a solution to chronic homelessness, and has since become the gold standard of supportive housing across populations who are vulnerable to homelessness and/or institutionalization.58

NJHMFA prioritizes production of supportive housing for twelve categories of individuals with special needs, both through its Supportive Housing Cycle and by incentivizing unit set-asides in the Family Cycle. New Jersey deserves celebration as one of only six states to set aside a designated portion of its LIHTC allocation for supportive housing.59 Yet because the need for supportive housing is greater than the volume produced annually, we recommend NJHMFA be more targeted and intentional about the types and quality (including fidelity to the PSH model) of its supportive housing projects.

The twelve populations with special housing needs, as outlined by NJHMFA are:

• Individuals with mental illness

• Individuals with developmental disabilities

• Ex-offenders and youth offenders

• Runaway and homeless youth

• Disabled and homeless veterans

• Individuals in treatment for substance abuse

• Individuals with physical disabilities

• Victims of domestic violence

• Youth aging out of foster care

• Individuals and families who are homeless

• Individuals with HIV/AIDS

• Individuals in other emerging special needs groups identified by State agencies

Source: NJHMFA, “Proposed 2019-20 Qualified Allocation Plan (QAP),” November 19, 2018.

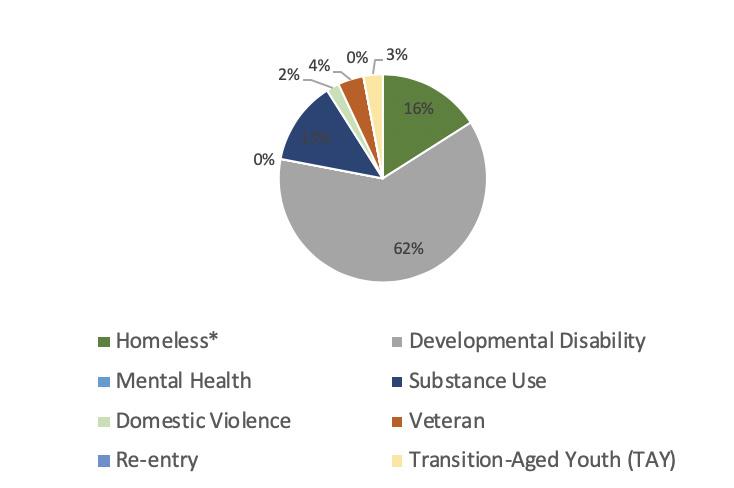

Currently, QAP applicants choose their project’s population without explicit guidance from the state. As such, these populations are not prioritized based on trends in New Jersey’s special needs population. A review of projects funded by NJHMFA in the 2013–2019 Supportive Housing Cycles shows nearly six of ten beds created for a special needs population went to tenants with a physical, mental, or intellectual disability who were registered with the Division of Developmental Disabilities, part of the New Jersey Department of Human Services.

Data sources: NJHMFA-provided data on LIHTC allocations along with NJHMFA press releases and independent analysis of individual project type and population served.

*Percentage calculated from total number of beds created, including those for which the population served is unknown

*Includes homeless sub-population designations (i.e., homeless women with children; homeless youth; homeless individuals with coexisting mental health needs)

22

Figure 6: Percentage of New Beds Funded through the Supportive Housing Cycles (2013-2019), by Special Needs Population

Figure 7: Beds and Units Created for the 12 Special Needs Populations Designated by NJHMFA through the LIHTC Supportive Housing Cycle (2013 – 2019)

Data Sources: NJHMFA-provided data on LIHTC allocations along with NJHMFA press releases and independent analysis of individual project type and population served.

A Special needs beds created for each special needs population using 9% LIHTCs is indicated in the chart above. Note this is the number of beds, not the number of units

B Includes homeless sub-population designations (i.e., homeless women with children; homeless youth; homeless individuals with coexisting mental health needs)

C Defined as a physical or intellectual disability - which were often not distinguished in NJHMFA’s tracking data

D Percentage calculated from beds and units where special needs population data is available

Of the 561 supportive housing beds for which we have complete data, only 24 were PSH beds for people living with substance use disorder (the remaining are temporary beds) and zero were for formerly incarcerated New Jerseyans, despite formerly incarcerated New Jerseyans comprising 25% of the need estimated by the Corporation for Supportive Housing. Currently, NJHMFA does not actively track the populations being served through the Family Cycle 5% / five-unit set-aside point category.

While this breakdown may indeed reflect underlying population needs, it is not informed by a comprehensive statewide review of needed units. NJHMFA reports a key factor in choice of special needs population is the availability of housing vouchers and/or service provider funding. While this does reflect available resources, an important consideration, it does not necessarily reflect underlying need. In this spirit, NJHMFA should conduct an analysis of statewide need for each of the special needs populations and provide guidance from this analysis to developers. Without such an analysis, it is not clear whether the current allocation of tax credits is best serving the needs of New Jersey’s most housing insecure residents. One potential consequence of such an analysis would be a real or perceived competition between special needs populations for LIHTC allocation. However, a comprehensive analysis of statewide supportive housing opportunities and gaps could generate political and public support for greater overall investment in supportive housing.

23

Special Needs Beds CreatedA 2013 2014 2015 2016 2017 2018 2019 Total % of TotalD HomelessB 30 14 0 27 11 4 0 86 16% DisabilityC 60 82 64 28 40 34 20 328 62% Mental Health 0 0 0 0 0 0 0 0 0% Substance Use 40 24 0 0 0 0 0 64 13% Domestic Violence 0 12 0 0 0 0 0 12 2% Veteran 0 0 14 0 6 0 0 20 4% Re-Entry 0 0 0 0 0 0 0 0 0% TransitionAged Youth 0 0 0 0 0 16 0 16 3% Person Living with HIV/AIDS 0 0 0 0 0 0 0 0 0% Unknown 35 10 N/A N/A N/A N/A N/A 45 Total 165 142 78 55 57 54 20 571

following steps:

a. Track robustly the quantity and durability of special needs units funded through the Family and Supportive Housing funding cycles.

As stated, NJHMFA does not actively track which special needs populations are selected for set-aside units in its Family Cycle. NJHMFA also does not track or monitor the status of supportive units over time—for example, whether they continue to be rented to the special needs population designated in the application or to any special needs residents at all. Without this information, the Agency will have difficulty evaluating its effectiveness at meeting population needs. We recommend thorough and ongoing tracking as a first and vital step in an ongoing evaluation.

b. Prioritize special needs population(s) identified as having the highest unmet housing needs in the Supportive Housing Cycle through point allocations in the QAP. Under the current Supportive Housing Cycle, developers will serve the populations for whom it is easiest to secure funding, to gain municipal support, and to provide services. Given the clear commitment of the Agency to supportive housing, it is a missed opportunity for NJHMFA to not actively incentivize developers to use the tax credits for New Jersey residents most in need by awarding points for serving these populations in the Supportive Housing Cycle of the QAP. NJHMFA should take a more active role to ensure credits in the Supportive Housing Cycle go to the populations most in need, to track the allocation of credits by special needs population, and to set explicit goals for housing production targeted for specific populations. The designated targeted populations should be based on the results of a statewide supportive housing needs assessment and should be revised on a regular basis with the QAP revision.

As one potential model, NJHMFA can look to the Indiana Housing and Community Development Finance Agency. In 2017, Indiana began proactively selecting populations of focus for its supportive housing LIHTC allocations. Applicants are required to participate in a Supportive Housing Institute, and expectations for what high-quality “support” looks like are established in the application and further clarified through technical assistance throughout the Institute.60

Washington State takes a different approach. Given the scope of need and the availability of local and state funding to address homelessness, Washington State prioritizes projects with significant supportive housing components within its 9% LIHTC allocation. Projects can receive up to 35 points (out of a total of about 130) for setting aside between 50–75% of units as PSH. Of the 1,020 new units funded through Washington State’s 2019 cycle, 602 were PSH units and all projects included at least some PSH units for people experiencing homelessness, ranging from 13 to 75 units for people experiencing homelessness per project.61

24

To ensure supportive housing development is aligned with population need, NJHMFA should take the

Photo credit: NJHMFA 2019

c. Require developers to work with their local Continuums of Care when designing and leasing-up supportive housing projects and multifamily set-aside units for individuals and households experiencing homelessness.

Currently, New Jersey’s QAP recommends that projects with units for homeless individuals or families have a letter of support from their local Continuum of Care. New Jersey’s sixteen Continuums of Care (CoCs) are designed to access and address homelessness within their respective regions, and some maintain by-name lists of people experiencing homelessness, as well as their special needs and vulnerabilities.62 Consequently, CoCs are well positioned to help NJHMFA better align the projects it funds with local needs. NJHMFA should require, rather than recommend, that developers housing families and individuals experiencing homelessness secure a letter of support from their local Continuum of Care indicating how they will collaborate.

NJHMFA should also require that projects with units for people experiencing homelessness maintain updated records through the Homeless Management Information System (HMIS), currently managed by the Agency. HMIS supports statewide homeless response coordination and monitoring of supportive housing quality.63 Currently, the QAP offers two points to supportive housing developers that give each resident a lease in their own name and full tenant rights. This is what makes supportive housing “permanent,” as housing is not conditional on participating in available supports nor time-limited to the length of a social service or health program.64 To monitor permanency, Indiana is beginning to require HMIS use by all supportive housing units for individuals experiencing homelessness, which in turn will enable the state to investigate if they notice an unusual number of evictions, which could be symptomatic of poor fidelity to Permanent Supportive Housing principles.65 We suggest NJHMFA adopt this monitoring practice for developments serving individuals experiencing homelessness.

d. Expand the QAP definition of “in treatment for substance abuse.”

There is no single treatment universally recommended for substance use disorder, and New Jerseyans may not be actively enrolled in existing treatment programs for many reasons. We encourage NJHMFA to have a more expansive definition of what “treatment” entails. Currently, the QAP defines “individuals in treatment for substance abuse” as “any individual who is a client of programs funded and/or licensed by the New Jersey Department of Human Services, Division of Mental Health and Addiction Services.” We suggest NJHMFA coordinate with the Department of Human Services, along with the New Jersey Department of Health and the newly-created Office of Homelessness Prevention at DCA, to update this definition so that it does not require active participation in a treatment program. For example, a collaboratively-created definition could include participation at one of the state’s Harm Reduction Centers, allow for referrals from case managers at the state’s substance use treatment hotline, or prioritize those identified in HMIS as experiencing a substance use disorder or chaotic substance use. Expanding this definition would create the opportunity for projects that deploy a Housing First model, which does not require abstinence or participation in a treatment program, to be funded through the Supportive Housing Cycle.

e. Incentivize projects that use universal design architecture in all funding cycles.

Projects that practice universal design are those “usable by all people, to the greatest extent possible, without the need for adaptation” and that “meet the broadest spectrum of abilities regardless of age, ability or life status.”66 By promoting a universal standard of accessibility, NJHMFA can increase the quantity of affordable accessible housing that is appropriate for New Jerseyans with a wide range of abilities—for example, those with special needs who do not require supportive housing or those whose needs change over time due to age, accident, or illness. Universal design not only benefits New Jerseyans today by increasing variety and choice for those living with a disability, it’s also smart design because it prepares for a future when population needs may be quite different than they are today. As of 2017, six states included incentives for universal design in their QAPs.67 While universal design could increase development costs, housing stock that can adapt to population needs and that is inclusive of tenants with a wide range of abilities also offers long-term benefits that will accrue over time. In New York City, prohibitively expensive renovations have caused developers to struggle with renovating units for an aging population. Developing according to universal design principles would help ensure that all populations can access the units and avoid high renovation costs in the future.

25

5. Incentivize long-term rental assistance from non-governmental sources in the Supportive Housing Cycle.

NJHMFA should amend the QAP to award two points to supportive housing projects with project based rental assistance from non-governmental sources. These points would complement the two points NJHMFA already awards to supportive housing projects with project-based rental assistance from government sources.

This recommendation is based on the Flexible Housing Subsidy Pool in Los Angeles County. The Flexible Housing Subsidy Pool is distributed by the County Department of Health Services for the housing and service needs of individuals experiencing homelessness in LA County, including housing based supportive services, rental agreements, and both project and tenant based rental assistance. For everyone dollar spent on housing for this population a study by RAND found a net savings directly to the LA County health care system of $1.20.

While this program is not a non-governmental source of rental assistance incentivized through a QAP, the Flexible Housing Subsidy Pool does provide a model for leveraging non-governmental funding in affordable housing for special needs populations. The funding for the Flexible Housing Subsidy Pool is provided by foundations, primarily the Hilton Foundation, L.A. Cares (one of two Managed Care Organizations in Los Angeles County), the Los Angeles County Department of Health Services, and other governmental agencies including the local office of diversion and re-entry. The program launched in February 2014 with an initial contribution of $14 million from Los Angeles County and $4 million from the Conrad N. Hilton Foundation.

This would incentivize developers to work with non-government stakeholders who have helped fund supportive housing development in other states, such as hospitals, managed care organizations, and foundations (as highlighted in section II-C-3 of this report, “Expand partnerships with healthcare institutions”). These stakeholders have provided critical soft funds in addition to capital and in-kind land donations.

In Los Angeles and Chicago, for example, they have provided rental assistance and social service funding for some of the “hardest to serve” special needs populations like individuals experiencing homelessness, acute mental health substance abuse disorder needs, justice involvement, or medical frailty.68 Typically, these funds are used to provide rental or social service supports for the non-governmental parties’ population of interest in supportive or affordable housing.

To ensure this funding provides long-term benefits, the QAP should include explicit guidelines for what qualifies as non-governmental rental assistance and require the assistance to, at minimum, mirror the structure of Section 8 project-based financing. Almost all state QAPs incentivize federal vouchers, and many also incentivize state and local rental assistance. A few states—including Utah, Hawaii, Indiana, New Hampshire, and New Mexico—allow non-governmental sources of rental assistance, subject to state standards for qualifying rental assistance and approval by the entity allocating tax credits in the state.69 New Jersey should follow their lead. This change would complement the Agency’s active effort to engage other stakeholders in housing financing, as in its innovative hospital partnership, and provide a flexible tool for partnerships to come.

Source: Los Angeles County Department of Health Services, “Housing for Health-Highlights”.

B. Leverage Other Financing Tools to Produce Variety and Choice of Housing

NJHMFA receives no direct funding from the State of New Jersey and only small amounts from the federal government for various programs. It is crucial that the Agency find innovative ways to continue to finance affordable housing given its financial constraints. Other government-subsidized funding streams, such as tax-exempt bonds and tax credits, are some of the best ways to produce much-needed rental housing in

26

New Jersey. However, New Jersey often maximizes the use of its federally-allocated annual tax-exempt bond volume cap (currently about $935 million, of which roughly 50% is allocated by the State Treasurer to NJHMFA every year). Faced with similar constraints, other states have found creative ways to better leverage their allocations of tax-exempt bonds and tax credits to increase affordable housing production, as explained in two examples below. The Agency should consider implementing these policies.

1. Use bond recycling and bifurcated financing to reuse and preserve limited bond volume cap.

Authorized in the Housing and Economic Recovery Act of 2008, bond recycling involves refunding some of a state’s unused tax-exempt bonds for use in future affordable housing projects. As the New York University Furman Center for Real Estate and Urban Policy explains, “Recycling allows for reuse of tax-exempt bonds that are only needed for a few years, far short of the potential years of tax-exempt financing possible with private activity bonds.”70 Prior to 2008, short-term bonds and longer-maturity bonds both counted against a state’s volume cap. The relationship between 4% credits and bonds requires that “an initial level of bond financing will no longer be needed once a project has completed construction or been placed in service.”71 As bond-financed projects reach this stage, volume cap that was previously used by the project where the loan has been prepaid can be used again for future multi-family housing. This allows the bonds to be reused, or recycled, without allocating additional volume cap.

The State of New York used this method to generate nearly $2 billion in recycled tax-exempt bond financing, which in turn helped finance almost 70,000 affordable housing units from 2009–2017.72 New York City has been effective at using recycled bond revenues for middle-income housing.

The law does not allow New York to “double-dip”—that is, to use recycled bonds with new 4% tax credits since they had originally been paired with 4% credits in the first project. Instead, the City has used the bonds for middle-income housing, as this requires less subsidy- and gap-financing due to relatively higher rents. In cities and states with tight housing markets, bond recycling can be a source of extra funds for middle income housing without decreasing tax-credit financing available to projects with deeper affordability.

New York City also successfully preserved more of its bond cap allocation by bifurcating financing for mixed income projects. When using 4% tax credits and bonds to finance affordable housing, bonds must be used to cover 50% of total development costs (TDC). As the law stands now, if the project is less than 100% affordable, the bond proceeds still need to cover 50% of TDC. Through bifurcated financing, the 50% test would only apply to the tax credit (i.e., the affordable) portion of the development, rather than the whole project with potential market rate units. This would free up bonds to be used for other affordable developments.73 There is great potential in New Jersey for bond recycling and bifurcated financing.

As cities across the state look to build more mixed-income projects, NJHMFA needs to leverage its bond cap allocation as much as possible to maximize rental unit production. NJHMFA should reach out to the New York City Housing Development Corporation for specific financial records showing how bonds are recycled from one deal to the next and the legal frameworks used to comply with the Housing and Economic Recovery Act.

27

The state of New York generated nearly $2 billion in recycled bonds to help finance roughly 70,000 units from 2009-2017.

Recently proposed federal legislation would make bond recycling easier by extending the length of time in which recycled bonds must be used.74 Representatives from both sides of the aisle in large and small states support the measure, indicating broad support for expanding bond recycling.

2. Explore and encourage separate ownership of tax credit deals to maximize eligible basis and to produce larger projects with more affordable units.

Several states, including Virginia, Maryland, and California, have encouraged split ownership of tax credit deals in what they call “twinning”, “hybrid deals”, or “stretching the 9s,” to maximize the use of their scarce 9% credits. This is made possible by allowing a development to be divided into two discrete deals with separate ownership structures. One deal is constructed using 9% credits and the other with 4% credits, which stretches the limited 9% credits to maximize their efficiency.

This structure allows states to build denser projects with more units by “monetizing” the unused “eligible basis,” or cap on tax credits.75 States often put a lower cap than that required by the IRS on the amount of tax credits a developer or project can receive in every allocation cycle, which spreads 9% tax credits across more projects. The New Jersey 2019–2020 Qualified Allocation Plan (QAP) places a $1.75 million cap on tax credits for Family Cycle projects and $1.4 million cap for Senior and Supportive Housing Cycle projects. By creating a split-ownership structure with 9% and 4% credits, projects can reach the cap of 9% tax credits laid out in the QAP for the 9% “owner one” deal while utilizing the remaining eligible basis for 4% credits and bonds in the “owner two” deal.

This allows developers to produce more units on the same site, increasing density. In some cases, this frees up enough 9% credits for a state to allocate for an additional affordable project.76 The Virginia Housing Development Authority (VHDA) proposed a first-of-its-kind incentive in their QAP for this twinning model and has seen great success. Developers who blended the 9% and 4% tax credits were awarded more points for their projects. In 2015, the first year the incentive was implemented, VHDA produced 707 units of affordable housing through these hybrid deals. In 2018, 2,368 units were built in fourteen developments in hybrid deals, underscoring the popularity and success of the incentive. Ultimately, Virginia has been able to fund at minimum an additional project of approximately 70 units each year using 9% credits that were not used because of the proliferation of hybrid deals.77 Maryland has already added an incentive in its QAP for developers to use leveraged funds gained through such hybrid deals.

New Jersey should incentivize hybrid deals and the additional affordable units they can produce in future QAPs. They can do this by awarding more points to projects that use this structure, depending on the Agency’s anticipated bond volume cap utilization.

For states that have not hit their volume cap, splitting the deals to use more 4% credits and bonds instead of 9% credits allows the 9% credits to be leveraged further for additional projects, as seen in Virginia. For years in which New Jersey does not anticipate using its full volume cap, incentivizing this structure in the QAP could free up 9% credits to use for more projects. However, there are still benefits if the Agency anticipates hitting its volume cap.

By monetizing unused eligible basis, this ownership structure has the potential to increase density by creating more units on a single site. NJHMFA should keep in mind that these deals tend to be more complex and work

28

Virginia used hybrid deals in fourteen developments to produce 2,368 units in 2018. The Virginia Housing Development Authority estimates that an additional, medium sized 70-unit project can be built each year as a result of its program.

best in areas with potential for increased density and soft funding. Since the deals are more complicated and require strict adherence to rules surrounding 9% and 4% credits, bond counsels, developers, and HFAs refer to “brain damage,” or added mental strain, accompanying hybrid deals. However, New Jersey can benefit from attorneys and developers in others states who already navigated this process and acquired expertise.

C. Strengthen Partnerships and Collaboration to Efficiently Allocate Resources

NJHMFA has powerful financing and policy tools at its disposal. But the Agency’s ability to use these tools most efficiently depends on its working in close partnership with other state agencies and other stakeholders. By implementing the following recommendations, NJHMFA can better leverage statewide resources to address New Jersey’s affordable housing needs.

1. Establish a consolidated financing application.

NJHMFA should lead an interagency effort to create a consolidated housing financing application. Currently, NJHMFA provides a “Unified Application for NJHMFA Multifamily Rental Housing Production Programs,” which lists the various financing sources offered by NJHMFA—but not funds available from other agencies that also help developers complete their capital stacks, such as HUD and state programs administered by DCA.78 A consolidated financing application would help NJHMFA and partner agencies better leverage existing financing for housing development, would reduce duplicative efforts among agencies, and would offer developers a more streamlined process.

Several states offer models for implementing a consolidated financing application. Minnesota Housing, the state’s HFA, has established a Consolidated Request for Proposals (RFP) in partnership with several state and regional entities. Developers of multifamily rental housing can apply for and receive 9% LIHTC, amortizing mortgages, deferred loans, and project-based rental assistance via one application.79

As another example, Washington State offers a “Combined Funders Application” in conjunction with state, county, regional, and local government partners.80 This process simplifies work for developers by providing a common application for use across various funders; however, unlike the Minnesota application, applicants still respond separately to different agencies’ individual Solicitation for Applications or Notices of Funding Availability (NOFA). There are some combined NOFAs within these jurisdictions. Connecticut has a third approach, with only two partners in its Consolidated Application, the Connecticut Housing Finance Authority and the Connecticut Department of Housing.81 Connecticut’s process involves a series of deadlines for applicants seeking various combinations of financing.

Key partners for a consolidated financing application in New Jersey include state agencies such as DCA, NJRA, and EDA. Other levels of government should also be involved if possible, including participating jurisdictions for HOME funding, Continuums of Care, and counties with Homeless Trust Funds.

Challenges to developing a consolidated financing application include securing buy-in from all stakeholders. Also, some funding programs may operate on different timelines, which may necessitate changing deadlines, creating several rounds of applications, or limiting the number of funding opportunities offered through the consolidated application.

These challenges should be weighed against the benefits. First, a consolidated application provides an easier process for developers by removing a regulatory barrier. Second, a consolidated application can help agencies better achieve their missions of increasing the supply of affordable housing with intention and focus. As an administrator of the Minnesota program noted, “it gives funders more than one way to approve an application. For example, a development that might not otherwise happen due to the fierce competition for 9% tax credits might be supported for funding using 4% credits or other sources.”82

29

2. Launch a supportive housing partnership with the New Jersey Department of Health.

While Permanent Supportive Housing (PSH) and Housing First—which does not require sobriety or adherence to any medical or social service treatment program as a condition of housing—are recognized best practices in supporting people living with chronic health conditions, including substance use disorder, multiple state housing finance agencies reported that uptake of these best practices has been slow among providers. Several stakeholders interviewed for this report suggested housing providers are hesitant to commit to these models because of longstanding ideas about which tenants are and are not “housing ready” and the ongoing cultural shift within homeless services from transitional to permanent housing. To support and equip providers, Oregon’s HFA launched a Supportive Housing Institute in which a cohort of developers and nonprofits work together to design Housing First projects. The Institute is cohosted with the state health department, and trainings and technical assistance are provided by the Corporation for Supportive Housing; $5 million in funding is given to projects that are successfully created through the Institute. Oregon’s initiative is modeled on Indiana’s Supportive Housing Institute, which has increased both the quality and the strategic focus of the state’s supportive housing developments.