INTELLIGENT RISK knowledge for the PRMIA community

©2022 - All Rights Reserved Professional Risk Managers’ International Association November // 2022

PROFESSIONAL RISK MANAGERS’ INTERNATIONAL ASSOCIATION FIND US ON prmia.org/irisk @prmia INSIDE THIS ISSUE Thanks to our sponsors, the exclusive content of Intelligent Risk is freely distributed worldwide. If you would like more information about sponsorship opportunities contact sponsorship@prmia.org Intelligent Risk - November 2022 002 CONTENT EDITORS Steve Lindo Principal, SRL Advisory Services and Lecturer at Columbia University Carl Densem Risk Manager, Community Savings Credit Union SPECIAL THANKS 003 Editor introduction 048 Conduct risk - by Shuvajit Chakraborty 012 Assessing cryptocurrency risk for institutional investors by Thomas J. Blackburn, Dan diBartolomeo & William Zieff 043 Risk dynamics of cryptocurrencies - by Peter Gross 036 Potential role of insurance sector in mitigating climate risk by Sonjai Kumar 024 Becoming cyber resilient in a new threat landscape by Michael Balfiore & Sara Downey 052 The climate (ESG) risk management & net-zero wave: the non-financial corporate perspective - by Peter Plochan 039 Operational resilience maturity: How you can reach ‘sophistication’ by 2025 - by Gary Lynam 004 Measuring systematic risk exposures by Barbara C. Matthews 028 The climate risk impact on corporate default rates by Francesca Bell & Gary van Vuuren 059 Build digital infrastructure for operational risk management by Peter Ding 019 Inflation and its drivers by Aleksei Kirilov & Valeriy Kirilov 032 Normalising US interest rates: the Fed can move beyond taming inflation - by Divyansh Awasthi 009 The here and now: ESG through the lens of the war in Ukraine - by Elisabeth A. Wilson 062 ESG, sustainability and non-financial risks a call for action 046 Canadian Risk Forum – Executive Leader Session

editor introduction

Steve Lindo Editor, PRMIA Carl Densem Editor, PRMIA

Steve Lindo Editor, PRMIA Carl Densem Editor, PRMIA

This issue marks a new chapter for PRMIA’s quarterly Intelligent Risk publication, which was first published more than ten years ago. In keeping with PRMIA’s mission to promote, develop and share professional risk management practices globally, the topics now featured in Intelligent Risk are aligned with those currently identified as the highest priority by industry leaders, and the articles hand-picked from an impressive array of contributions from risk practitioners around the world. Most notably, this issue is capped by an article from Barbara Matthews, whose groundbreaking work in measuring public policy volatility and systematic risk follows a distinguished career in the global banking industry and US government financial policy roles.

Recognizing that the topics covered in this issue are dynamically evolving and the subject of ongoing debate, PRMIA has created an Intelligent Risk Community, where readers can exchange views on the topics featured in current and past issues with authors, editors and other PRMIA members on an ongoing basis. We encourage you to add your own comments to this Community and follow the comments of your peers.

Lastly, we would greatly value your feedback on Intelligent Risk’s new style, format, style, and content, which you can send to iriskeditors@prmia.org. We hope that you enjoy reading this issue’s contributions as much as we did editing them!

our sponsor

Dell creates technologies that drive human progress. Today, Dell Technologies is instrumental in changing the digital landscape the world over. We are among the world’s leading technology companies helping to transform people’s lives with extraordinary capabilities. From hybrid cloud solutions to high-performance computing to ambitious social impact and sustainability initiatives, what we do impacts everyone, everywhere.

003 Intelligent Risk - November 2022

Synopsis

Conventional wisdom holds that public policy risks are systematic in nature, which means they cannot be measured or hedged. That is changing, as advanced technology and data analytics are being used to quantify public policy language, allowing risk professionals to chart public policy volatility and quantify systematic risk.

measuring systematic risk exposures

by Barbara C. Matthews

by Barbara C. Matthews

Conventional wisdom holds that risks related to public policy shifts are systematic in nature. They cannot be measured or managed quantitatively because they constitute random, exogenous variables. Historical data provides only limited guidance on risk exposures for risks which have no precedence. According to this convention, policy-related systematic risk exposures cannot be hedged.

Systematic risks undoubtedly exist. Public policy risks present primarily in verbal form, which makes them difficult to quantify. Paradigm shifts in the public policy context generate horizontal, systematic impacts across industry sectors and asset classes, which makes these risks systematic in nature. However, the ongoing technology and data revolutions continue to provide risk managers with the capacity to measure risks that previously were deemed impossible to quantify. Public policy risks are now within the scope of risks which can be measured and managed proactively, objectively, and quantitatively.

moving the efficient frontier

Consider credit risk. During the 1990s, conventional wisdom held that credit risks could not be measured and modeled on a par with market risks because deteriorations in credit quality demonstrated different path dependencies relative to market risks. In addition, observable data regarding credit risk was difficult to obtain in the absence of a traded market in credit risk.

Conventional wisdom was turned on its head in 1999, when Duffie, Singleton, and Pan published their seminal paper on jump diffusion processes1 that provided a paradigm for pricing credit risk using an intensity-based default model.

1 / Transform Analysis and Asset Pricing for Affine Jump-Diffusions, Darrell Diffie, Jun Pan, Kenneth Singleton, NBER Working Paper 7105 (April 1999). A version of this paper was subsequently presented at a Bank of England research conference in November 2000 and in Econometrica, Vol 68, No. 6 (Nov. 2000).

Intelligent

-

004

Risk

November 2022

The new approach permitted financial engineers and risk managers to apply multi-factor models for the purpose of pricing credit risks.2

A new technological and data revolution beckons decades later. This article covers three inter-related topics for consideration:

• A high-level description of systematic risk;

• A discussion of why public policy risks are commonly considered to be systematic in nature;

• How the data revolution chips away at the boundary between the efficient frontier and systematic risk.

Increasingly, data-driven decisions are possible regarding policy-related systematic risk.

systematic risks – the basics

Systematic risks present in four main silos: market risk, interest rate risk, exchange rate risk, and inflation risk

3. They are profoundly momentum-driven. Policymakers attempt to constrain volatility related to those dynamics using tools familiar to most market participants:

• Market Risk: trading halts/circuit breakers; central bank asset purchases.

• Interest Rate Risk and Inflation Risk: Monetary policy.

• Exchange Rate Risk: Trade policy and geopolitical positioning play an outsized role in triggering exchange rate volatility.

Investment analysts and strategists allocate considerable time to assessing how individual firms may be exposed to a broad range of risks 4 in order to identify appropriate mitigation strategies. The ability to trade volatility through the VIX specifically provides opportunities to hedge exposures to systematic risks both directly and through related derivative products.5

The framework for assessing exposure to systematic risks is thus well understood within financial markets even if full insulation from those risks through hedging strategies may not be available. But until recently it has not been possible to measure exposure to systematic risks related to shifts in public policy, much less a broader range of public policy risks that drive market volatility (e.g., cryptocurrency regulation, climaterelated policy risks, energy policy, monetary policy) through discontinuous price movements triggered by headlines.

2

/ The hazards associated with racing towards tradeable credit risks before the credit process had been fully digitized and before a broader universe of analysts and consumers understood the implications of trading credit risk were noted at the time. Regulatory Use of Credit Ratings: Implications for Banks, Supervisors, and Markets, Barbara C. Matthews, Credit Rating: Methodologies, Rationale and Default Risk (Chapter 12), Dr. Michael Ong editor (RISK Books: 2002).

3 / Systematic Risk - Learn How to Identify and Calculate Systematic Risk (corporatefinanceinstitute.com)

4

/ The Essentials of Risk Management, Second Edition, By Michel Crouhy, Dan Galai, Robert Mark (2013) The Essentials of Risk ManagementThe Essentials of Risk Management Digital Handbook (prmia.org)

5

/ The VIX index and volatility-based global indexes and trading instruments: A Guide to Investment and Trading Features, CFA Research Foundation (2020) https://www.cfainstitute.org/-/media/documents/article/rf-brief/rfbr-moran-vix-volatility.ashx

005 Intelligent Risk - November 2022

The reaction function between public policy and markets is well known, driving financial firms to be early adopters of advanced technology that accelerates their access to news. The reaction function has a name: headline risk.6 It encompasses a broad range of media coverage, including corporate announcements and litigation announcements.7 Unsurprisingly, high correlations exist between media coverage and market volatility.8

The high correlation between headline risk and market volatility intensifies the perception that public policy risk is a random exogenous variable, because media attention to public policy developments can be discontinuous over time. Media coverage tends to arise during key inflection points at seemingly random intervals which do not line up with key market timelines (e,g. the opening of trading, options expiration dates, quarterly report filing deadlines).

In addition, public policy volatility is expressed in words while markets must measure volatility quantitatively.

The net impact leads markets and risk professionals to conclude that public policy decisions are random. The inability to measure the informational content (not the definition, not the sentiment) from public policy processes has left the risk discipline flying blind, unable to spot a signal or path dependencies. The inability to access objective historical data regarding the language of public policy has also left the risk discipline unable to apply jump diffusion or other risk estimation processes.

The data revolution changes everything.

The capacity to quantify public policy language provides risk professionals with the first opportunity to begin charting public policy volatility, identify the path towards decisions, and anticipate related market reaction functions.

Consider the technical and macro risks featured in this edition of iRisk. Few, if any, are easily subject to objective quantification using traditional mechanisms. Risks and volatility that impact asset pricing for most if not all of these issues materialize first in the form of words, making it difficult for financial engineers and traders to incorporate these risks into their pricing algorithms. New advances in automated text analytics bring language-related public policy risks within the reach of risk measurement.

6 / Notable accelerants over the last century have included: the telegraph, the tickertape, the teletype, the telephone, the Bloomberg Terminal, Blackberries, cable news, program/algorithmic trading, server co-location, automated headline-reading bots that accelerate trading signal extraction from the news cycle, machine-readable institutional news feeds, and social media.

7

/ Headline risk is formally defined as: “the possibility that a news story will adversely affect the price of an investment, such as a stock or commodity. Headline risk can also impact the performance of a specific sector or the entire stock market.” Headline Risk (investopedia.com).

8 / Policy News and Stock Market Volatility, by Scott R. Baker, Nicholas Bloom, Steven J. Davis and Kyle Kost (25 March 2019), available at: https://www.policyuncertainty.com/media/Policy%20News%20and%20Stock%20Market%20Volatility.pdf

how text analytics extend the efficient frontier

why markets define public policy as a type of systematic risk

006 Intelligent Risk - November 2022

Financial firms and central banks increasingly use text analytics to improve the performance of their nowcasting models.9 Researchers are exploring how a broad range of alternative data derived from language can generate insight into market volatility and firm-specific risks. Input sources so far have included transcripts from quarterly corporate earnings calls10, Google search term data,11 Google/Factiva sentiment ratings, 12 and business leader surveys.13

Given the role that the Federal Reserve’s monetary policy decisions play in driving market dynamics, sentiment analysis of the Federal Open Market Committee minutes has delivered a rich source for new insight regarding public policy trajectories.14 The findings are consistent: the language used to communicate monetary policy is more important than the underlying data. Even the Federal Reserve15 and the Bank for International Settlements16 17 18 created language-based indices illustrating the point.

Converting words into numbers holds value beyond monetary policy, from financial stability reports to other non-monetary policy central bank communications.20 21 22

Backtests of our own PolicyScope data show that volume data generated by our patented process provide advance notice of market volatility by as much as 10 days to 22 days across a broad range of issue areas that far exceed monetary policy, such as digital currency policy, trade policy, and the LIBOR transmission.23

The research arises just as policymakers themselves recognize that public policy shifts create unique risks for markets and economies. For example, public policy shifts are increasingly recognized as a source of macroeconomic risks in relation to climate change. Consider the risk landscape featured in a recent United Nations report 24:

9 / Nowcasting euro area GDP with news sentiment; a tale of two crises, ECB Working Paper 821 (2021).

10 / Firm-level Political Risk: Measurement and Effects, NBER Working Paper No. 24029 (2017)

11 / Predicting the Present with Google Trends, Economic Record 88 (2012)

12 / Measuring Central Bank Communication: An Automated Approach with Application to FOMC Statements, NBR Working Paper 15367 (2009).

13 / Enrichment of the Banque de France’s Monthly Business Survey: Lessons from Textual Analysis of Business Leaders’ Comments, Banque de France Working Paper 821 (2021).

14 / Transparency and Deliberation Within the FOMC: A Computational Linguistics Approach, The Quarterly Journal of Economics (2017).

15 / Words Speak as Loudly as Actions: Central Bank Communication and the Response of Equity Prices to Macroeconomic Announcements, Finance and Economics Discussion Series FEDS Notes 2021-074, Board of Governors of the Federal Reserve System (2021).

16 / Seeing the Forest for the Trees: Using hLDA Models to Evaluate Communication in Banco Central do Brasil, BIS Working Papers No 1021 (2022).

17 / Effects of Banco de la Republica’s Communication on the Yield Curve, BIS Working Papers No. 1022 (2022).

18 / Monetary Policy Press Releases: An International Comparison, BIS Working Papers No. 1023 (2022). “Much of the co-movement between the sentiment index and monetary policy rates may simply reflect the economic data discussed in the press releases and used in the termination of monetary policy. So, if we want to analyze if there is additional information in the monetary policy documents, it is necessary to filter this common information.”

19 / Central Bank Communication on Financial Stability Economic Journal (2014).

20 / Global Spillovers of the Fed Information Effect, Bank of England Staff Working Paper no. 952 944 (2021).

21 / The Narrative About the Economy as a Shadow Forecast: An Analysis Using Banco de Espana Quarterly Reports, Banco de Espana Working Paper 2042 (2020) (observing that “a ‘sophisticated’ reader could infer GDP growth projections based on the text of the reports, somewhat beyond what is told in just the numbers.” They did not specify whether the ‘sophisticated’ reader they had in mind at the time was a machine or a human).

22 / Fed Communication on Financial Stability Concerns and Monetary Policy Decisions: Revelations from Speeches, Banco de Espana Working Paper 2110 (2021) “A higher speaking time (topic proportion) or a higher negative tone on Financial Conditions, Financial Stability and Supervision and Regulation correlate with a more accommodative monetary policy stance while communication on House with a tighter policy stance….speeches by Fed presidents seem to convey timely and strong information for financial-related concerns and the likely direction of monetary policy.”)

23 / PolicyScope Data: Backtest Results, BCMstrategy, Inc. (September 2021).

24 / Economic Impacts of Climate Change: Exploring short-term climate related shocks for financial actors with macroeconomic models, United Nations Environment Program (2022).

007 Intelligent Risk - November 2022

What is true for climate-related policy is true for other arenas as well. What policymakers say matters. Advanced technology for the first time delivers to risk professionals the capacity to measure momentum embedded within the words as well as the sentiment conveyed by those words. Firms that start measuring and pricing these macro-policy risks effectively can ride the innovation wave, extending the efficient frontier. Using text analytics, a small portion of systematic risk can now be measured, managed, hedged, and anticipated.

Barbara C. Matthews

Barbara C.

Inc., a data company

helps

market volatility from public policy risks. She has served in various senior positions in the global banking industry as well as the U.S. government, including service as the first U.S. Treasury Attache to the European Union with the Senate-confirmed diplomatic rank of Minister-Counselor. She was also the first Regulatory Counsel to the Institute of International Finance, where she worked directly with Chief Risk Officers and Chief Executive Officers of the world’s largest banks. She holds advanced degrees in

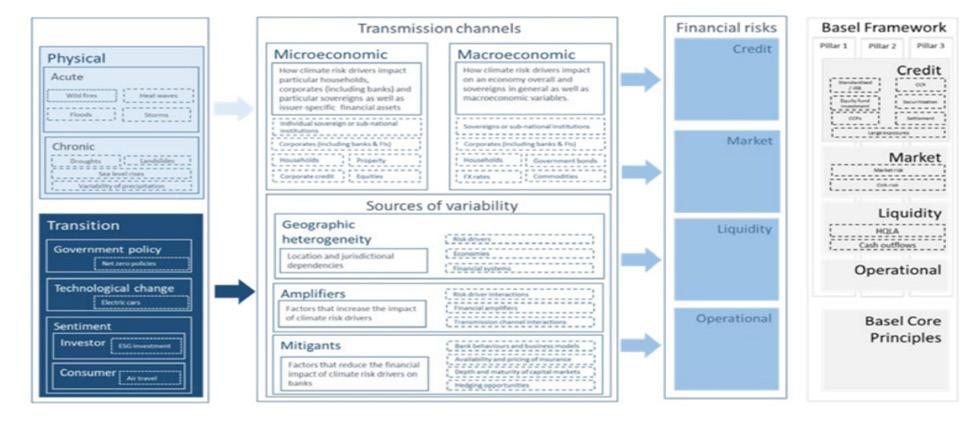

Figure: Macroeconomic transmission channels for climate risks

Steve Lindo

Matthews is Founder and CEO of BCMstrategy,

that

portfolio managers and strategic analysts anticipate

international relations (Georgetown University) and two law degrees (Duke Law School).

Founder and CEO of BCMstrategy, Inc

Figure: Macroeconomic transmission channels for climate risks

Steve Lindo

Matthews is Founder and CEO of BCMstrategy,

that

portfolio managers and strategic analysts anticipate

international relations (Georgetown University) and two law degrees (Duke Law School).

Founder and CEO of BCMstrategy, Inc

author 008 Intelligent Risk - November 2022

peer reviewer

Synopsis

The war in Ukraine places new emphasis on the ESG lens already gaining traction in the financial services industry and with regulatory bodies. The author’s discussion of each pillar, E, S and G, in the context of the conflict offer each new significance and explanatory power, while outlining the needs for formal reporting and potential challenges to this shift.

the here and now: ESG through the lens of the war in Ukraine

by Elisabeth A. Wilson

A recent onslaught of proposed climate change-related financial disclosure regulatory guidance has only served to fuel the meteoric rise of Environmental, Social and Governance (ESG). Business leaders and risk practitioners are scratching their heads trying to determine where and how to start the long journey that will entail ESG compliance—and more importantly, win the consumer seal of approval. However, regulatory requirements are still in the (albeit probably not-so-distant) future and may be inhibited by legal interventions.1

Then there is the ongoing war in Ukraine, which is raising the ESG stakes even higher. Suddenly, every element across the E, S and G pillars has been brought into sharper focus by the tragedy unfolding in Europe. While conflict, unlike anything seen since World War II, continues the impetus on ESG across the financial industry is only growing.

environmental

The economy and inflation have taken a substantial hit due to the United States’2 and Europe’s 3 decision to ban Russian oil imports. It is apparent that the pain the average consumer is facing as a result will not abate any time soon. With nuclear weapons always on the table, Western powers have leveraged Russia’s economy as their alternate weapon of choice, with the goal of exacting maximum damage and slashing Russia’s war chest. In response, Russia has sparked concern over retaliatory moves to cut Finland’s electrical power4 and to stop essential gas supplies to Europe 5

As the West releases oil reserves in response to subsequent supply chain constrictions, controversy over the potential impacts this may have on climate change is fueling greater angst.

Intelligent Risk - November 2022

009

More importantly, the war in Ukraine has highlighted, more than ever, the financial and political benefits of transitioning to a net zero economy. The introduction of clean energy in every sense—both green and oligarch-free—would further isolate Russia’s economy and destabilize its expansionist goals. Beyond the implications of climate change, now there is a need to reduce the United States’ and Europe’s reliance on increasingly volatile countries and regions for its energy supplies. Focus on the E in ESG has taken on new impetus and is evolving into a mechanism necessary to maintaining political, economic, financial, natural and moral balance.

At the outset of the war in Ukraine, a Yale professor published a spreadsheet listing all the foreign companies that continued to do business in Russia. Due to the resulting consumer response, companies that previously had been silent rapidly began making definitive statements and promoting their business strategies to wind down operations and close stores. Companies began leaving Russia in a mass exodus—forfeiting revenue along the way—because they were unwilling to face public displeasure and consumer boycotts that, in the long run, would do far more to degrade profits and tarnish their brands.

The S In ESG has been heavily promoted by shareholders, investors and consumers who want to align themselves with companies that embody their values. These same advocates of sustainable and ethical business practices, these champions of Diversity, Equity and Inclusion, have galvanized the financial industry in the last two years, turning ESG into a veritable grassroots movement. As a result, it is not so surprising that consumers—standing up to Russian aggression on an individual basis—made the impact they did while the world was reeling at the onslaught on Ukraine. It is also a clear reminder to financial institutions still on the fence about ESG that consumers can—and will—hold a company in check if its practices do not line up with a more en vogue world view.

social governance

Wave after wave of economic sanctions against Russia, its political figures and its citizens have placed an additional onus on financial institutions. Compliance and Information Security departments already stand on the front lines in the fight against global terrorism, but now the former must stay abreast of increasingly labyrinthine updated agency guidance while ensuring policies, practices and teammates remain robust and effective.

Knock on wood, significant retaliatory cyber-attacks led by Russia against Western powers providing aid to Ukraine have not materialized as previously feared, but that does not change the fact that the financial industry is still on tenterhooks. Data privacy and cybersecurity play a prominent role in ESG and can align back and forth with either the S or G pillars. When it comes to the potential damage Russia could exert on the financial industry and the world economy—not to mention individual institutions, their shareholders and customers— Information Security teams are sorely aware that the balance has tipped toward governance. The stakes are substantial if system vulnerabilities remain unchecked or employee training efforts to drive recognition of suspicious activity fall short. 010 Intelligent Risk - November 2022

ESG as a whole

ESG is interwoven in the very fabric of our financial industry and economy. These are key concepts and practices that make up our world as a whole. It is why ESG has come to prominence in a world fatigued after a pandemic, unprecedented social unrest and economic instability. Now the world and the financial industry must grapple with a war in Europe, a concept we thought had passed away. When one part of the world behaves in a chillingly provocative manner and the rest bears the brunt—whether directly in the line of fire or by experiencing economic and supply chain constrictions across the globe—, the resulting imbalance highlights the need for consolidation and change.

The financial industry is already equipped to facilitate proactive movement on the ESG front, however there is still a lot to hash out when it comes to appropriate policy and reporting in a way that can satisfy regulators, consumers and an already heavily-burdened financial industry.

ESG is not a new concept. In the last two years, foundations have been laid by financial practitioners, foundations that will serve not only shareholders, investors and consumers, but will help promote global stability going forward.

Disclaimer: All views expressed in this article are my own and do not represent the opinions of any entity that I may be associated with.

peer reviewer

Steve Lindo

Elisabeth A. Wilson

Elisabeth A. Wilson has worked for over 14 years in the financial industry. She was recruited to Atlantic Union Bank’s Enterprise Risk Management Department in 2016 to support development of the company’s then-burgeoning risk management framework. Recently charged with crafting the Bank’s Environmental, Social and Governance (ESG) Risk Framework, Elisabeth continues to build, implement, and manage key risk programs, driving regulatory alignment and promoting bank-wide engagement while simultaneously supporting business line risk oversight. She has also contributed to the ABA Banking Journal, The RMA Journal, and Risk Management Magazine. Elisabeth is based in Richmond, Virginia.

author 011 Intelligent Risk - November 2022

Synopsis

Already volatile crypto coins have come under new pressures in 2022, most dropping severely as investors flee risky assets, but recognition of their utility is also growing as more institutions take serious looks at their possibilities. The authors propose an analytical process for crypto risk related to current practices for commodities and frontier currencies, allowing easier integration with risk models for other asset classes.

assessing cryptocurrency risk for institutional investors

by Thomas J. Blackburn, Dan diBartolomeo & William Zieff

introduction

Recently the value of most cryptocurrencies has declined significantly with Bitcoin now trading at less than 40% of its all-time high value. A major cryptocurrency exchange, Coinbase, has disclosed operating losses of nearly $500 million dollars in the first quarter and $1 billion in the second1, respectively, and raised the possibility that investor crypto deposited with the exchange might be lost if they are forced into bankruptcy. In addition, Terra and Luna cryptos have become basically worthless. The related stable coin TerraUSD has traded for as low as $0.08, a massive failure for an asset purportedly pegged to be worth $1.00 dollar.

Since the circulation of the original Bitcoin white paper in 2008, the value of all cryptocurrencies has risen to now exceed one percent of all traded wealth. There have been large variations in the values of major cryptocurrencies like Bitcoin and Ethereum, in addition to frequent massive shifts in the values of lesser known cryptos. The institutional landscape continues to evolve rapidly with firms like Goldman Sachs and Fidelity setting up trading facilities, while other organizations like HSBC have steadfastly advised clients to keep away from crypto. A useful overview of the current state of play appears in Horne (Journal of Performance Measurement, Summer 2021). Irrespective of intrinsic or extrinsic value, we expect that such items will be present in institutional investor portfolios from time to time. As such it is necessary to have methods in place to assess the risk of holding cryptocurrencies and the incremental impact of crypto holdings on overall institutional portfolios.

Intelligent Risk - November 2022 012

1 / https://investor.coinbase.com/financials/quarterly-results/default.aspx

The main portion of our proposal focuses on key building blocks for understanding the risk of cryptocurrencies and what magnitude of return expectations would justify those risks for a typical investor. Our process involves both historical and forward-looking information, as well as several nuances in the statistical estimation of a covariance matrix (within crypto and between crypto and other assets).

An additional feature is a means to incorporate “tail risk” as might arise from geopolitical events (being outlawed or severely regulated) and operational risks (e.g. theft, loss of private keys) based on use of mixture distributions and the method of Cornish and Fisher (Review of the International Statistics Institute, 1938). This relevance of tail risk is motivated by real world events such as the aggressive regulation of crypto activities by China and other countries, and the persistent occurrence of large hacks (e.g. Poly Networks in August 2021) wherein losses of a half billion dollars or more are almost ordinary.

While the emergence of cryptocurrencies has led to numerous working papers within the academic community, we draw attention to Alexander and Imeraj (SSRN, 2019) which addressed the empirical volatility of major cryptos as being on the order of 80% annualized. Schwenkler and Zheng (SSRN, 2020) identify pairwise covariance structures in the behavior of cryptocurrencies which they ascribe to news coverage. The classic work of Hotelling (Economic Journal, 1929) also offers a relevant foundation given that a major purported benefit of cryptocurrencies is their built-in limitation of a finite supply (at least for each individual cryptocurrency).

analytical method for market risk

Our coverage of cryptocurrencies is closely related to the methods we routinely use for commodities and fiat currencies of frontier market countries. For fiat currencies, we create groups of currencies based on geographic proximity, trade relations, and cultural similarity. A similar grouping concept is used for cryptos. The grouping scheme allows us to build principal component factor exposures for crypto currencies, which are then mapped onto existing risk model factors for non-crypto assets.

The first step is to use a principal component analysis (PCA) of one or more groups of crypto assets to estimate statistical factors that are common drivers of observed returns. These factors may be difficult to identify and may change over time. PCA is a traditional way to deal with such situations which generates factors based on the covariance matrix of the asset returns themselves. In the usual manner of a statistical risk model, we keep the statistical factors which contribute the most to variance and dismiss smaller ones as representing noise. A useful model for drawing the line between PCA factors and noise is presented in Bouchard, Cizeau, Laloux, and Potters (World Scientific, 1999).

Once the statistical factors for a sample period have been identified, the second step maps the statistical factors onto existing factors in other models to determine the correlations between a crypto asset and traditional assets. A general discussion of factor modeling methods is diBartolomeo (chapter in Oxford Handbook of Quantitative Asset Management, 2014). 013 Intelligent Risk - November 2022

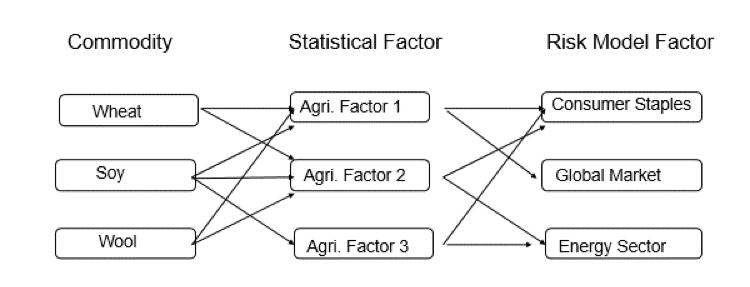

To keep the model parsimonious and to try to avoid overfitting, the number of identified factors on to which each statistical factor is mapped should be limited. One does not know the nature of statistical factors, hence one does not know which risk model factors are most likely to be relevant to it. To select among traditional risk model factors in a systematic fashion, a cross validated LASSO regression is used. This procedure automatically drops factors which do not add to the explanatory power of the model for cryptocurrencies, while simultaneously shrinking remaining risk factor loadings towards zero to combat overfitting. An illustration of the same process applied to commodities is presented in Figure 1.

Figure 1: A conceputual diagram illustrating the stages of our modelling process.

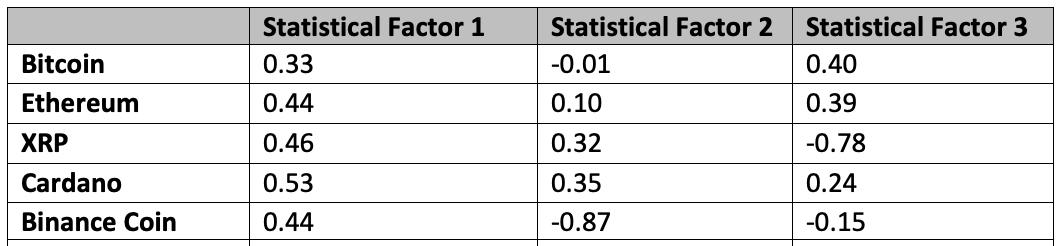

Preliminary results show that PCA in this case picks up a crypto “market” factor which loads positively on all the major cryptocurrencies. Subsequent statistical factors tend to reflect the movement of cryptocurrencies around this market factor. These statistical factors can then be mapped onto our risk model with the LASSO regression. Some unique challenges are presented in this case by the very short history of most cryptocurrencies. One simple approach is to take Bitcoin as an indication of the crypto market and use traditional regressions to estimate “beta” to Bitcoin as a metric of risk for small cryptos that cannot be included in the original PCA cohort.

Figure 2: An example result for five cryptocurrency loadings on statistical factors for a single time period

014 Intelligent Risk - November 2022

Besides defining the cohort set, the statistical process for cryptocurrency must account for several uncommon features. The first is a very large departure from our usual independent and identically distributed (IID) return assumptions. Cryptocurrencies have exhibited high degrees of skew, kurtosis, and serial correlation in their returns. These behaviors may arise from speculative interest from retail investors, the erratic nature of interest from major financial institutions, or fear of cryptocurrencies being severely hampered by regulation (as seen recently in China).

With respect to non-IID behavior we employ four analytical nuances to improve the transformation from purely historical observation to forward looking risk forecasts. The first is the use of “root mean square” (RMS) rather than standard deviation as the measure of dispersion of factor returns. We are treating factor return time series as if markets are relatively efficient so mean returns to a factor should be close to zero, rather than whatever time series mean is observed. For example, a return time series that goes up 10% per month every month for two years (as was roughly observed with Internet stocks in the late 1990s) would have a standard deviation of zero but a significant value for root mean square.

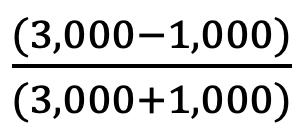

The second technique is the idea of “range based” volatility measures, also replacing the usual definition of standard deviation of returns. One way to think about the volatility of an asset is to consider the percentage distance between the highest and lowest prices observed during a particular period (e.g. day, month, year). If the high and low prices are close together, the asset has low volatility. If the high and low prices are far apart, the asset is volatile. Several papers starting with Parkinson (Journal of Business, 1980) have shown that if returns are IID, there is a direct algebraic transformation between traditional return volatility and range-based measures. A very simplified range-based measure of volatility would just be : . For example, if we observe that a cryptocurrency had a low price of $1,000 and a high price of $3,000 over the past month, we get a volatility of =50% per month.

The third proposed input to ex-ante currency risk estimation is the availability of a “carry trade” wherein bank deposits denominated in a particular currency offer higher interest rates than in major currencies. As cryptocurrency deposit accounts do not carry any form of government deposit insurance the risk of counterparty failure is substantial. At the current time retail “Bitcoin savings accounts” are available with yields over 8% annually, as compared to close to zero for ordinary bank accounts in the US.

Our final key input is the concept of “convenience yield”. The anonymity and ease of global transactions has material economic value to certain market participants (criminals, tax evaders, investors in countries with capital controls). While this effect is hard to quantify directly there is a long history of low or negative interest rates in countries with strong banking secrecy laws. In the 1980s Swiss banks routinely offered negative interest rates on deposit accounts while US banks were offering a rate of around 5% (the maximum allowable under Federal Reserve Regulation Q until 1986).

At present, the combination of convenience yield and interest premium is probably around 12-13% which implies a volatility equivalent (i.e. inclusive of higher moments) of 70-80% annually for major cryptos. For a derivation of this relationship see Estimating an Investor’s Volatility/Return Tradeoff: The Answer is Always Six which is an extension of Rubinstein (Journal of Finance, 1976) and Wilcox (Journal of Portfolio Management, 2000 & 2003). There is also a thinly traded Bitcoin Volatility Index (BVOL) whose value has ranged from a low of around 19% to a high of 188% annualized. As of May 2022, the BVOL value was 79.3%.

015 Intelligent Risk - November 2022

In addition to large scale thefts and the possibility of being outlawed in some countries, there have been many cases of lost computer files, passwords known only to a decedent, and other situations where cryptocurrencies are inaccessible to the rightful owners. There have been successes by law enforcement or quasi self-regulation in recovering significant amounts of stolen crypto as in the Colonial Pipeline case and the recent seizure of purportedly stolen crypto valued at $3.6 billion by the US Department of Justice. Perversely this trend may decrease the acceptability of cryptocurrencies among participants seeking anonymity, decreasing the “convenience yield” premium in crypto valuation. On the other hand, East Caribbean Currency Union is the first central bank to issue a blockchain-based, central bank digital currency (CBDC), and other countries are exploring or have launched pilots. El Salvador has recently recognized Bitcoin as legal tender.

The disclosure of financial problems at Coinbase adds yet another potential operational risk for crypto participants. Unlike securities exchanges and brokerages which are highly regulated by the SEC “net capital rule” 15c3-1 (a 300 page set of rules and reporting requirements) in terms of their financial reserves, crypto exchanges are essentially unregulated. The Coinbase disclosures came about because they are a US public company not because they are a cryptocurrency exchange.

To provide a framework for modeling such event risks, we propose a simple two state model. In one state, there is an event risk incident with probability P and an expected return (loss) L with standard deviation S0. In the other state, there is no operational risk incident with probability (1-P), but there is market risk with expected return E and volatility S. We combine the two states into a single distribution using a “mixture of normal distributions” process. See Robertson and Fryer (Skand Aktuarietidskr, 1969). The resultant combined distribution will have four moments with negative skew and positive excess kurtosis. We then use the aforementioned method of Cornish and Fisher to convert to the closest fit normal distribution.

As an example, we can assume our “regular state” has 0.999 probability per day with a daily volatility of 5% and an expected arithmetic return of 0.1% per trading day. The “incident” state has a probability of 0.001 per day (P). We assume that in the event of an incident, the expected loss is 80% (L) with a standard error of 3% (S0). Including both market risk and “event” risk we get a combined equivalent daily volatility of 9.08%. Annualizing under IID assumptions we get 144% per annum. It should be noted that if we cut the incident probability to 0.0001 we get a volatility of 5.07% per trading day, just a tiny bit higher than with a zero probability of an incident.

modelling event risk stable coins

A sidelight to the cryptocurrency discussion is the matter of stable coins like Tether where a coin issuer functions like an 18th century bank issuing its own currency. Commercial banks in Hong Kong and Scotland still routinely issue their own bank notes.

016 Intelligent Risk - November 2022

To stabilize the value of cryptocurrencies at a relatively fixed value in US$ (like a pegged currency) the “custodian” holds financial reserves that purportedly assure that the stable coins have a claim on assets that can be converted to conventional currency.

However, experts including Gary Gorton of Yale, have questioned the validity of the collateral in these structures: Yale Economist Gorton Questions the Stability of Stablecoins. Lacking complete confidence in the collateral, we can treat this concern as we would counterparty risk in an OTC derivative acting in reliance on a clearing organization for sound collateral management, or a recognized credit rating for the counterparty. This view seems well justified given recent developments with TerraUSD.

On an annualized basis the return volatility of cryptocurrencies looks enormous (80% for the majors, far higher for many of the lesser known). Investors are depending on high liquidity to allow them to exit an asset quickly to limit losses. Under typical IID assumptions, 80% per annum is about 5% per trading day, so a three standard deviation event is a 15% loss per trading day. Even if we “fatten the tails” consistent with a T-5 distribution we end up around a 20% loss.

However, it should be noted that liquidity is not infinite for any asset. On October 19, 1987, the US stock market lost $1 trillion in capitalization (a roughly 22% decline) when the NYSE DOT execution system was overwhelmed. This massive decline was the result of only $15 Billion in trading volume. While the core blockchain capacity for Ethereum was significantly upgraded in 2021, crypto transactions done on “Decentralized Finance” peer-to-peer networks are highly vulnerable to disruption which could lead to extreme cases of “jump diffusion” in prices.

conclusions

Our proposed analytical process for crypto risk is closely related to our current practices for commodities and frontier currencies. This process makes for relatively simple integration with risk models for other asset classes.

The assessment of volatility and market risk is highly dependent on a nuanced understanding of the extent of non-IID returns with unstable means. If we include operational risk, the resultant volatility estimates are extremely sensitive to the probability of an “incident”. Even seemingly low probabilities like 1 in 1,000 create a profound increase in volatility equivalence and joint measures of market and operational risk (e.g. Value at Risk).

liquidity as the risk mitigation method

017 Intelligent Risk - November 2022

Carl Densem peer reviewer

authors

Thomas (T.J.) Blackburn

Thomas (T.J.) Blackburn has worked in the finance industry since 2014, after receiving his PhD. in physics in 2013. After an internship at Northfield Information Services, he worked at BNY Mellon and then State Street from 2015-2019. He has since returned to a Northfield as a senior risk analyst.

Dan diBartolomeo

Dan diBartolomeo is President and founder of Northfield Information Services, Inc. which develops quantitative models of financial markets. He has prominent roles in numerous industry organizations including PRMIA, IAQF, and CQA. He is a director and past president of the Boston Economic Club. His publication record includes more than fifty books, book chapters, and peer-review journal articles. In addition, Dan spent several years as a Visiting Professor at Brunel University. He has been admitted as an expert witness in litigation matters regarding investment management practices and derivatives in both US Federal and state courts. He became an editor in chief of the Journal of Asset Management at the start of 2019.

William Zieff

William Zieff is Director at Northfield Information Services. Bill has extensive experience in quantitative investing. Prior to Northfield, he was Chief Investment Officer of Global Strategic Products, Wells Fargo Asset Management; Partner and Co-Chief Investment Officer of Global Asset Allocation, Putnam Investments; and Director of Asset Allocation, Grantham, Mayo, Van Otterloo. Bill has taught master’s and undergraduate courses in quantitative finance. Bill holds an A.B. degree in Economics and Mathematics from Brown University and MBA from Harvard Business School.

018 Intelligent Risk - November 2022

The Federal Reserve’s efforts to manage inflation depend on its use of two main policy instruments. This article examines the impact of each of these instruments on inflation and how they are currently being used by the Fed to combat the recent surge in inflation.

by Aleksei Kirilov & Valeriy Kirilov

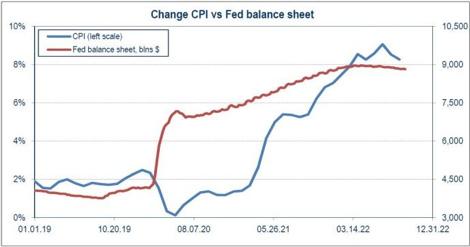

Everyone has been talking about inflation lately: housewives, businesspeople, investors, officials. Indeed, the Americans have not seen such inflation for decades, see Figure 1. That is why the Fed says that the fight against inflation is its main task. In its analysis, the Fed uses the Consumer Price Index (CPI) as a measure of inflation. This indicator is calculated every month by the Bureau of Labor Statistics. A percentage value is usually used, showing how the index has changed compared to the same month a year ago. But no less representative is the absolute value of the index. Figure 1 shows both the absolute and relative values of the index since 1995.

Figure 1 Figure 2

Source: https://www.bls.gov/cpi/

inflation and its drivers Intelligent Risk

A noticeable acceleration of inflation began around March last year, and then this growth became more and more strong, see Figure 2. Recall that back in July 2021, we wrote that the Fed needs to immediately complete the quantitative easing program to prevent further inflation growth1. And that otherwise the economy will inevitably face a strong surge in inflation. However, the Fed began to take real steps to combat inflation only in March of this year. First the Fed raised the rate by 0.25% and then, a month later, began to reduce its balance sheet.

November

019

-

2022

Synopsis 1 / Aleksei Kirilov, Valeriy Kirilov. U.S. Economic Recovery Mirrored in the Stock Market. Intelligent Risk (PRMIA), July 2021, https://issuu.com/prmia/docs/intelligent_risk-july_2021-issuu

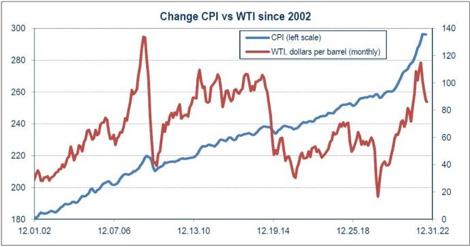

In discussions about the reasons for such a sharp increase in inflation, the assumption of the dominant role of commodity prices and, above all, the price of oil is often expressed. Indeed, if we compare the change in CPI with the price of WTI over the past few years, then such an assumption seems quite appropriate, see Figure 3. The correlation coefficient of these two parameters over a relatively short interval of about 5 years was 74%. The figure shows data from Crude Oil Prices: West Texas Intermediate (WTI) - Cushing, Oklahoma, Dollars per Barrel, Monthly, Not Seasonally Adjusted.

Figure 3

Source: : https://fred.stlouisfed.org/series/MCOILWTICO

Figure 4

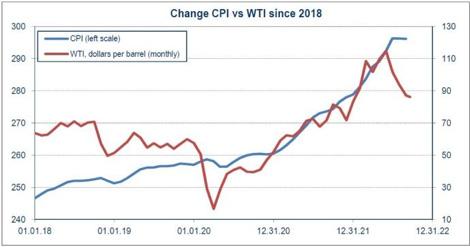

If we look at the dynamics of changes in parameters over a longer period of time, then such a conclusion seems rather controversial. Figure 4 shows data on changes in CPI and WTI prices over the past 20 years. At this time interval, the correlation coefficient of CPI and WTI is only 21%. Of course, macroeconomic conditions have changed a lot over the past 20 years. Perhaps the prices of commodities are not the main reason for the recent surge in inflation.

Recall that during the pandemic and even after it ended, as part of the quantitative easing program, the Fed added a huge amount of liquidity to the market by buying Treasury and mortgage bonds, greatly increasing its balance sheet. This caused the sharp growth in the M2 money supply. In addition, huge funds have been allocated by the government, with the approval of Congress, to help households and businesses. This led to even greater growth in the M2 money supply. To put this in perspective: from February 2020 to April 2022, the Fed’s balance sheet increased by $4,806.8 billion. According to the Fed, M2 increased by $6,477.2 billion over the same time.

Figure 5

Source: : https://fred.stlouisfed.org/series/WALCL

Figure 6

Source: https://fred.stlouisfed.org/series/M2NS

020 Intelligent Risk - November 2022

The change in the balance of the Fed and M2 over the past 20 years is shown in Figure 5. Of course, the supply of huge monetary liquidity in the market was bound to lead to higher prices. And this includes the rise in prices for oil and other commodities. Undoubtedly, disruptions in supply chains have also contributed to price increases, but the increase in the money supply was probably the decisive factor. Figure 5 clearly shows that starting from February 2020, there has been explosive growth in the Fed’s balance sheet and the M2 money supply.

Changing M2 is very similar to changing CPI. This is clearly seen in Figure 6, on which both parameters are plotted. On a twenty-year interval, the correlation coefficient of CPI and M2 is 96%. See Appendix for the statistical tests performed, confirming our assumption that the current surge in inflation is largely due to an increase in the money supply.

Figure 7 Figure 8

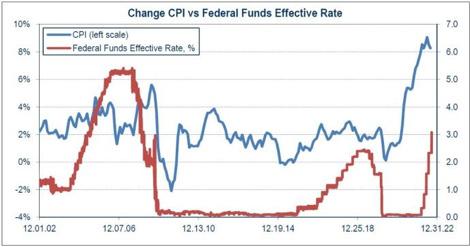

In an effort to reduce inflation, the Fed is aggressively raising interest rates, see Figure 7. However, as can be seen, until this approach has brought the desired results, inflation remains unacceptably high. Of course, by continuing such a policy –increasing the cost of money– in the end it will be possible to achieve a reduction in inflation to an acceptable level. According to our estimates, the Fed will have to raise the rate above 6% for this. Which, given current policy, could take many months.

Perhaps a more effective decision would be for the Fed to reduce its balance sheet more quickly, see Figure 8. Moreover, inflation is caused to a large extent, as we have shown, by a disproportionately large money supply. So far the Fed is not implementing its own plans to reduce the balance sheet.

It should be noted that the belated measures taken by the Fed to combat inflation led to extremely negative consequences for the stock market. First to the bubble in the market towards the end of last year. And then to a sharp decline in the stock market this year, which is probably far from over. So far, the Fed has been able to prevent the market from collapsing, but a further strong increase in interest rates and a simultaneous sharp decrease in the balance sheet may at some point lead to a panic sale, triggering margin calls and a series of bankruptcies of large financial companies. To prevent such a scenario, the Fed should probably choose only one of their available instruments: either a further increase in interest rates or a sharp decrease in the balance sheet. Judging by previous actions, the Fed intends to choose the first option. 021 Intelligent Risk - November 2022

However, such a decision threatens to have serious negative consequences for the economy due to the long-term persistence of inflation and interest rates at extremely high levels. According to our estimates, if the Fed’s current policy is maintained, inflation could remain above 6% for at least another 12 months.

appendix: testing the relationship between CPI and M2

Note that both time series, CPI(t) and M2(t), are non-stationary so spurious regression is possible. This is tested for using the Durbin-Watson statistic, which, in this case, is 0.022, indicating positive autocorrelation.

Therefore, it is necessary to additionally check whether the dependence of CPI(t) on M2(t) is statistically significant. At this first stage, we check the data on the Sims test for Granger causality. To do this, we build regressions of CPI(t) from past, current and future values of M2(t). The entire time interval is divided into three equal segments of 82 months. The results are as follows: regressions from past and current values of M2(t) are not significant based on both t-statistics for the coefficients and F statistic for the equations. For the regression of CPI(t) from future values of M2(t), significant results were obtained:

• the coefficients are 0.81543 and -0.00061, respectively

• the t-statistics for the coefficients are 4.57 and -6.78, respectively, which is much higher than the critical value of 1.99. Therefore, the obtained values of the coefficients are significant

• the F statistic is 45.93, well above the critical value of 3.96

Thus, the Sims test for Granger causality is positive.

Second, an additional test for cointegration is carried out. As can be seen in Figure 6, both time series show clear trends. Using the least squares method, the trend components were identified in the form of a linear dependence:

Then, for each of the series under consideration, the residuals CPI - Trend(CPI) and M2 - Trend(M2) were calculated. A regression was built for the residuals CPI - Trend(CPI) from M2 - Trend(M2) over the last ten years:

The t-statistics for the coefficients are 8.52 and -2.45, respectively, which is higher than the critical value of 1.98. Therefore, the obtained values of the coefficients are significant. The F statistic is 72.7, well above the critical value of 3.92. Therefore, the obtained regression equation is significant.

That is, CPI - Trend(CPI) can be represented as a linear dependence on M2 - Trend(M2) plus the remainder of the next order of smallness. Thus, CPI - Trend(CPI) and M2 - Trend(M2) are cointegrated. This means that there is a statistically significant relationship between CPI(t) and M2(t).

022 Intelligent Risk - November 2022

peer reviewer

Dan diBartolomeo

authors

Aleksei Kirilov

Conflate is a Russian management consulting company specialized in strategy, risk management, asset management and venture investment. As the partner of Conflate, Aleksei is responsible for asset management and venture investment. He specializes in the US stock and debt markets. Aleksei has more than 15 years of experience in financial services including development of financial strategy and financial KPI, liquidity management; controlling system, allocation of expense on business unit, financial modeling and debt finance. He has cross industries experience: banks, oil & gas manufacturing, real estate.

Aleksei has an MBA from Duke University (Fuqua School of Business), a financial degree from Russian Plekhanov Economic Academy and an engineering degree from Moscow Engineering Physics Institute.

Valeriy Kirilov

Valeriy is the General Manager at Conflate LLC. He has 15+ years’ experience in risk management and management consulting (BDO, Technoserv, then at Conflate). Besides he previously worked in the nuclear power industry (safety of Nuclear Power Plants).

Valeriy has an MBA from London Metropolitan University as well as a financial degree from Moscow International Higher Business School MIRBIS and an engineering degree from Moscow Engineering Physics Institute. He holds the PRM and FRM certifications and the certificate of Federal Commission for Securities Market of series 1.0. Valeriy was a member of the Supervisory board of the Russian Risk Management Society in 2009 – 2010.

Partner, Conflate LLC General Manager at Conflate LLC

023 Intelligent Risk - November 2022

Synopsis

Industry experts share their opinions on the cyber security challenges posed by the explosion of technology devices and data.

becoming cyber resilient in a new threat landscape

by Michael Balfiore & Sara Downey

by Michael Balfiore & Sara Downey

Experts discuss how to safeguard data amidst heightened vulnerability, a privacy conundrum and an AI paradox.

Will quantum computing break cybersecurity? How much responsibility should individuals have for safeguarding their data? How can organizations foster a culture of security? In May 2022, cybersecurity experts convened on a panel at Dell Technologies World to answer these questions and more.

Participants included data scientist Chris Wylie, best known as the Cambridge Analytica whistleblower, Bhavani Thuraisingham, founding executive director of the Cyber Security Institute at the University of Texas at Dallas, and Vivek Tiwari, vice president of Product Assurance and Security at Intel. Their conversation was moderated by John Scimone, president and chief security officer at Dell Technologies. He asked the panelists to weigh in on what they see as today’s gravest security challenges—given that, as Scimone mentioned frankly, cyber threats are getting worse each quarter, by every measure.

the data threat

We are living in the data age. On the one hand, we have never created and captured so much data. On the other, there are gaps in our data sharing. Companies are still reluctant to share their attack data. As Thuraisingham notes, this is problematic. We need this intelligence to identify groups of threats that behave similarly and use these discoveries to predict an attacker’s next step.

There was general agreement that the proliferation of data represents a double-edged sword. Wylie cited the weaponization of information as a significant threat. “If you radicalize people, and those people then go on to commit harm, you’ve created a weapon,” he said.

Intelligent

- November

Risk

2022

024

Scimone called out the mushrooming of data created by the ever-expanding internet of things as another challenge to security. “The explosion of technology devices creates exponentially more potential to do really good things,” he said, “but also really nefarious things.”

Thuraisingham agreed. “We’ve got data arriving continuously, so machine learning models have to change,” she said. “We [have to] come up with dynamically changing models,” she said of artificial intelligence (AI) designed to fend off attacks.

When it comes to AI, the panel noted an interesting paradox. Tiwari talked about “AI for security” and “security for AI.”

AI—the very technology that can help threat detection solutions find anomalies in the network and act as a co-pilot in secure development, secure coding and secure assurance—can also be wielded by cybercriminals. The same technology that protects companies could also be used by hackers to inflict unrelenting, automated attacks that any human would struggle to combat, as well as represent a new set of “attack surface” that hackers can manipulate and exploit to cause the AI systems to have unintended effects.

As a path forward, Tiwari talked about protecting the models and data that are integral to AI algorithms, using confidential computing, secure enclaves and trusted domains. He cautioned that these measures need to be built into every product as every product now has AI.

While secure product development is foundational, the insider threat is also a cogent factor. Scimone noted that he found the stat in Dell’s recent Breakthrough study, showing more than half (52%) of workers have not meaningfully improved their security awareness/behavior after hearing about high profile cyberattacks “a little disheartening.”

the AI paradox whose responsibility is it?

” When it comes to the general population, I think it’s actually unfair to expect that people should become more security conscious.”

025 Intelligent Risk - November 2022

Chris Wylie, social researcher and data scientist

According to Tiwari, businesses can move the needle by building a culture of security. This culture starts with leaders clearly articulating the security strategy, vision and principles. Then you need to provide processes to enable employees to implement these. For instance, with secure development lifecycle. Of course, you need a robust training program which is tied into the company’s recognition system metrics to gauge your security culture’s effectiveness.

Tiwari emphasized that security is the responsibility of everyone in an organization. Wylie disagreed.

“When it comes to the general population, I think it’s actually unfair to expect that people should become more security conscious,” Wylie said. Instead, Wylie essentially argues that safety standards should be built into digital technologies just as they are with physical products.

the privacy conundrum

Noting that Dell Technologies World 2022 took place in Las Vegas, a city known for extensive video surveillance in its casinos, Scimone asked the panelists for their opinions on how to weigh security concerns against the need for privacy.

For Tiwari, it comes down to clear, transparent and enforceable policies. “I think as long as you work within those principles and guardrails, you can find the right technological solutions to address those things,” he said of balancing privacy and security. “And be ready to have that engagement with government agencies, with policy bodies, because you have to do this openly.”

Thuraisingham returned to AI’s prevalence as a reason why trustworthy AI is so important. If it’s in most products and making decisions based on the data it collects, it needs to be secure, private and fair.

Wylie noted that a vital element getting lost in most privacy discussions is the idea of human agency. “When we’re creating systems that constantly are collecting data, and then using that data to start to alter information in front of you,” he said, “those are starting to scratch at fundamental things about who you want to be as a person, how you want to interface with society.” In other words, people using such systems risk losing their autonomy. “How do you grow as a person when you’ve got an information system that is constantly deciding things for you?” he asked.

10 years from now

Looking ahead at the next five to 10 years of cybersecurity, Tiwari said he expected challenges to include physical security, supply chain attacks and weaponized AI. Even so, he sees the threat landscape improving for businesses and individuals thanks to dedicated efforts to combat attacks.

026 Intelligent Risk - November 2022

Thuraisingham worries about quantum computing in the hands of future attackers. “I dread to think what’s going to happen to cybersecurity—although it’s going to help with ransomware.” That’s because the brute force computing power promised by quantum computers threatens to smash all existing encryption schemes.

Thuraisingham is encouraged by ongoing work on post-quantum encryption but considers getting more talent into the field, including women and people of color, as vital to success.

“It’s a very monolithic industry,” Scimone agreed. “In five or 10 years, we should look very different and have a lot more horsepower on our side.”

Carl Densem peer reviewer

authors 027 Intelligent Risk - November 2022

Contributor Thought leadership, Dell Technologies

Michael Balfiore Sara Downey

Synopsis

This article explores how potentially complex physical and transition climate risk outcomes regarding obligor creditworthiness can be assessed and predicted via modelling scenarios. The examples provided by the authors regarding resultant probability of default provide a useful and comprehensive guide on how these methodologies can be extended to IFRS 9 accounting reporting, regulatory credit risk measurement, and forecasting.

the climate risk impact on corporate default rates

by Francesca Bell & Gary van Vuuren

The effects of climate risk drivers on financial risks are complex and interrelated. Although current research practices have embraced a wide spectrum of methodologies for how these risks may be examined, much focus has been on the impact of climate change on macroeconomic systems rather than on corporates. Borrowing from bank-focused research by the Basel Committee on Banking Supervision (BCBS, 2021) on the ways in which climate risk drivers foment financial risks, this work synthesises contemporary approaches to create a single, entwined methodology based on several research strands. The framework demonstrates how climate-related changes may be incorporated into corporate financial risks, such as PDs (and potentially both LGDs and EADs as well).

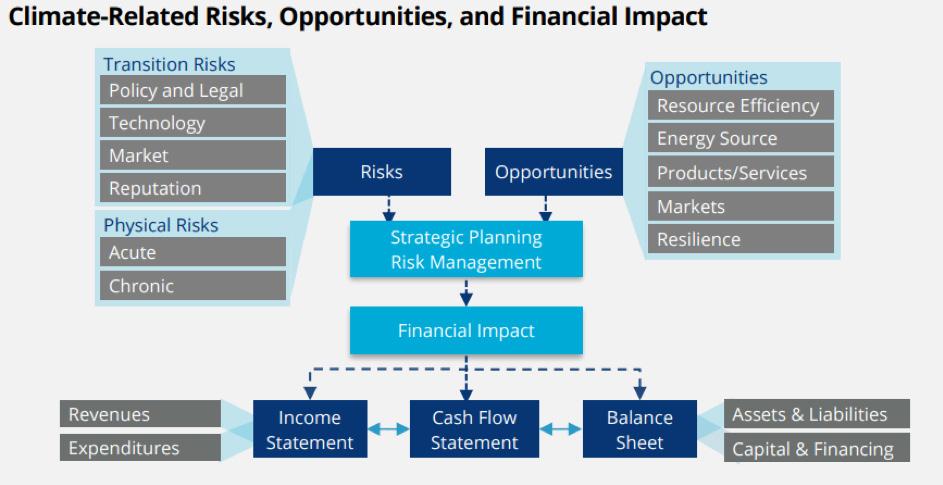

Environmental, social, and governance (ESG) issues are an important contemporary part of corporate evaluations (Ahmad, Mobarek, & Roni, 2021). Climate risk drivers (‘E’ in ESG) are classified as physical or transition risk. Physical risk arises from the physical effects of climate change on corporate operations such as the workforce, infrastructure, raw materials, markets, and assets. Acute physical risks are severe weather-driven events such as floods and fires; chronic physical risks involve longer-term climatic shifts which may result in precipitation/temperature changes or elevated sea levels. Transition risk represents societal changes (such as progress toward affordability of existing technologies and changes in public sector policies) arising from the transition to a low-carbon economy.

We assessed the impact of transition and physical climate risk on obligor creditworthiness using two well-known financial tools: geometric Brownian motion (GBM) to simulate share prices and return volatilities, and the KMV model to estimate probabilities of default (PDs). This evaluation may be translated into a measure of default probability, which may be used in IFRS 9 accounting reporting, regulatory credit risk measurement, and forecasting.

Intelligent Risk - November 2022 028

The recipe is:

1. Simulate share prices using realistic parameter inputs, such as volatility and drift, using GBM

2. Introduce realistic shocks at relevant frequencies and severities

3. Record resulting average asset values (via share prices) and equity volatilities at selected time intervals after the introduction of the shock(s)

4. Input these asset values and equity volatilities into the KMV model to estimate the distance to default (DD)— and hence the change from unshocked DDs.

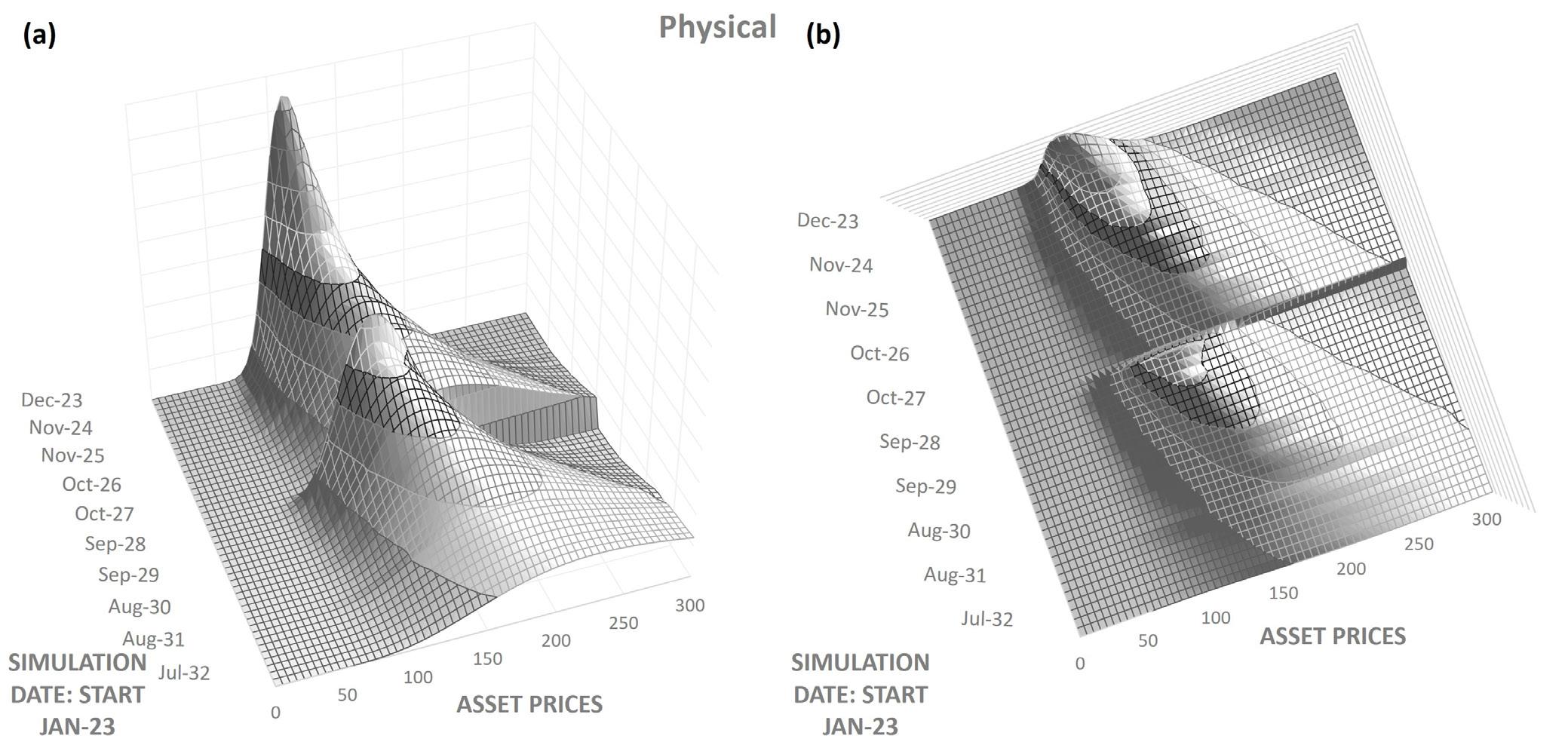

Simulated data were used as loss data are sensitive and proprietary. The evolution of corporate asset and liability values was processed using a GBM approach with a range of stylistic annual volatility and drift values to simulate ten years of weekly share prices. Shocks were introduced at different times with varying severity as a percentage of the stock price at the time of the shock. Frequency and severity of shocks may be selected by the user.

Outputs from the GBM analysis become inputs for the KMV model (similar to Baarsch & Schaeffer’s [2019] approach), and here again, simulated, realistic parameters for liability levels, risk-free rates, etc., are used.

Figure 1 shows a 3D view of the results of our simulations. At each timestep, the mean and standard deviation of the distribution of possible share prices are used to plot the log-normal distribution of outcomes. A shock (in this example a -40% share price shock) is then introduced at time t (in this example halfway through the 10-year simulation). Prices after physical shocks have increased volatilities while those for transition shocks do not.

Figure 1: Simulated log-normal distributions (side and plan view) of share prices for a 40% share price shock occurring halfway through a ten-year simulation cycle, due to (a) a physical climate risk event and (b) a transition climate risk event.

029 Intelligent Risk - November 2022

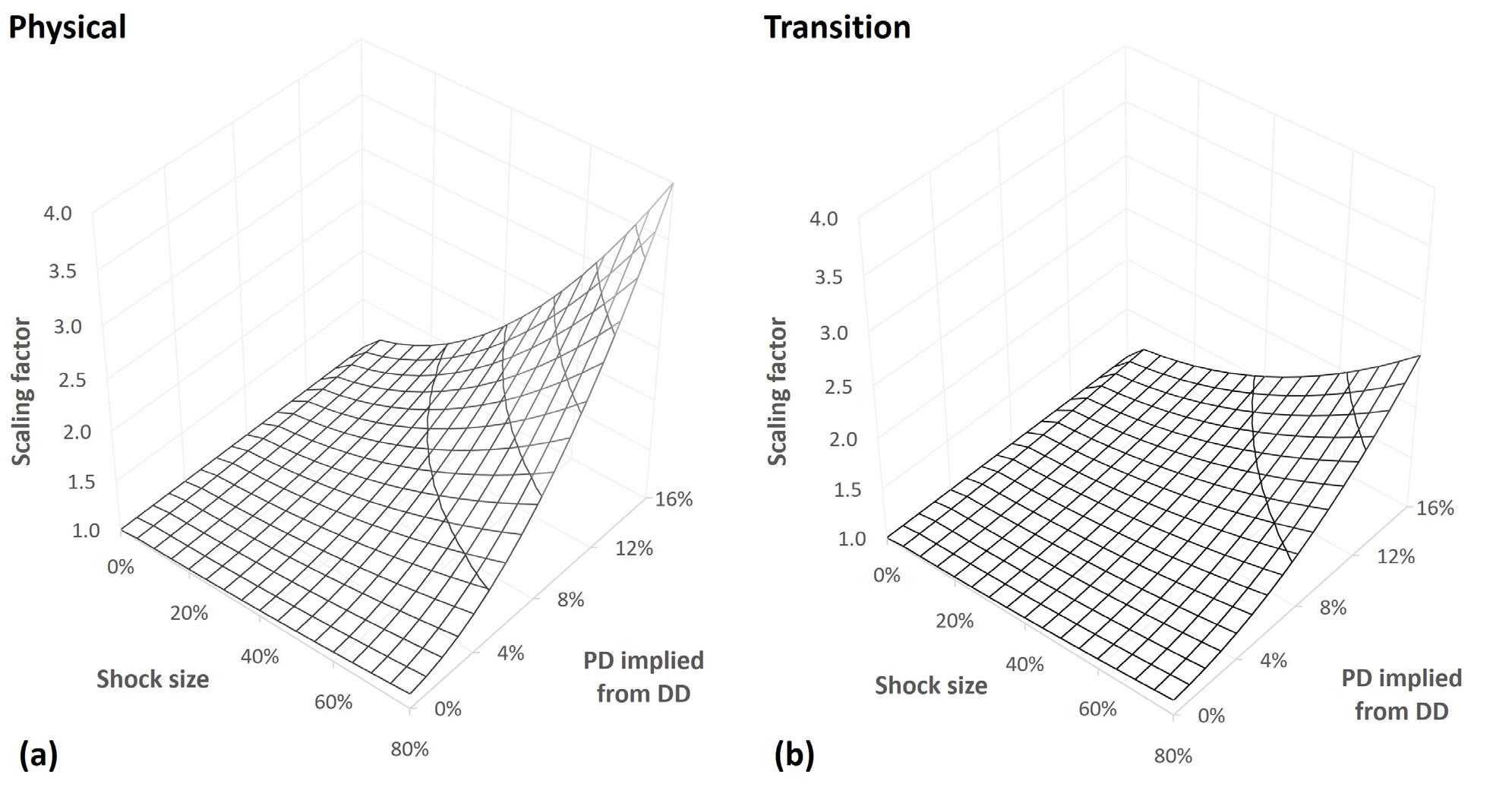

The outcome of the analysis is shown in Figure 2. The scaling factor, applied to unshocked PDs (z-axis) has been plotted as a function of shock size and original PD to which the climate-related shock has been applied. As expected, the scaling factor increases as a function of both parameters (shock severity and original, unshocked PD) for both physical and transition climate events. Such a calibration can be applied to a firm’s obligors to assess forward looking PDs, dependent on climate shocks.

Figure 2: Scaling factor to be applied to unshocked obligor PDs for (a) physical and (b) transition related climate events as a function of shock size and unshocked PD. Again, note the same vertical scale for comparison.

A way to quantify and calibrate climate related impacts on corporate PD levels – whether of physical or transition origin – has been demonstrated. Inputs are subjective and user-determined; obligors have unique price drifts and volatilities, and shock scenarios vary by type, severity, and frequency. However, this provides considerable flexibility. As more climate related events are added to the literature and global databases, specific climate events will eventually be linked to specific shock sizes. These results will benefit IFRS-9 compliant market participants (for forward-looking scenarios of obligor credit quality) but also for loan pricing which uses obligor PDs and regulatory capital calculations (which require knowledge of PDs at multiple maturities, not just one-year).

Bibliography

Ahmad, N., Mobarek, A. and Roni, N. N. 2021. Revisiting the impact of ESG on financial performance of FTSE350 UK firms: Static and dynamic panel data analysis. Cogent Business & Management, 8(1): 1 – 18.

Baarsch, F. and Schaeffer, M. 2019. Climate change impacts on Africa’s economic growth. United Nations Economic

030 Intelligent Risk - November 2022

Commission for Africa report, African Development Bank Group. Available from: https://www.afdb.org/sites/default/files/documents/publications/afdb-economics_of_climate_change_in_africa.pdf, accessed 13 Feb 22.

BCBS, 2021. Climate-related risk drivers and their transmission channels. Available from: https://www.bis.org/bcbs/publ/d517.pdf, accessed 17 Apr 22.

IPCC, 2018. Intergovernmental panel on climate change special report: global warming of 1.5°C. Available from: https://www.ipcc.ch/sr15/, accessed 16 Apr 22.

Mapchart. 2022. Available from https://www.mapchart.net/africa.html, accessed 17 Apr 22.

UNCTAD, 2022. UN list of least developed countries. Available from: https://unctad.org/topic/least-developed-countries/list. accessed 16 Apr 22.

Elisabeth Wilson peer reviewer

authors

Francesca Bell

Francesca Bell is a quantitative financial analyst working at the boutique consultancy RiskWorx in Johannesburg, South Africa. She underwent her undergraduate education at the University of Cape Town. Now a postgraduate student, she is currently about to complete her PhD in finance and economics at the University of the Witwatersrand specializing in the connection between environmental, social, and governance (ESG)-related issues and finance. Her first published article for the degree covered ESG-efficient frontiers: investment strategies which embrace and encourage ethical, socially responsible, climate-friendly asset allocation.

Gary van Vuuren

Although Gary van Vuuren started his career in astro and nuclear physics, he is now a professor of quantitative finance and statistics at the University of the Witwatersrand, South Africa and the Centre for Business Mathematics and Informatics, North-West University in Potchefstroom.

He is a freelance risk management advisor, working for RiskWorx, EY Johannesburg and other niche finance consultancies. He has supervised dozens of postgraduate students’ research. He is Francesca’s Masters supervisor and co-author on the ESG frontier paper.

031 Intelligent Risk - November 2022

Synopsis

While all central banks walk a precarious line in taming inflation, the Fed has an unprecedented chance to tamp down prices and buy itself valuable breathing room to use rate cuts in the future, when necessary. Returning to ‘normal’ rate territory sooner will balance the Fed’s competing priorities and challenges.

normalising US interest rates: the Fed can move beyond taming inflation by

Divyansh Awasthi

The pace of inflation growth has come as a rude shock to monetary policymakers this year. The rise has been sharp enough to have woken them from their slumber.

Central banks around the world, with the exception of those in China and Japan, have adopted a generally hawkish tone on inflation. But among the largest central banks, one finds itself in a situation which can allow it to normalize policy rates and not just tame inflation.

This is not to say that the task of the US Federal Reserve – or specifically the Federal Open Market Committee (FOMC) – is easy. But among advanced economies, it finds itself in a spot where it can think of normal interest rates as a larger aim than just controlling inflation.

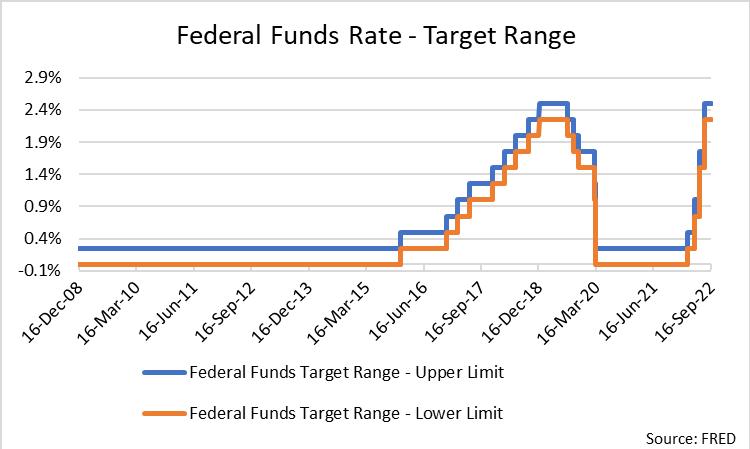

Figure 1: US Fed Funds Rate

Source: https://fred.stlouisfed.org/series/FEDFUNDS

Intelligent

- November

032

Risk

2022

normalized

monetary policy rates

Let us first look at what normalized interest rates mean.

During recessionary times, a central bank of a nation may reduce interest rates as a way to stimulate economic activity. A reduced policy rate induces commercial banks to reduce their lending and deposit rates. This incentivizes consumers to deposit less with banks and spend more, because of cheaper loans, and thus attempts to stoke economic growth.

Once the economy is out of recession and is considered to be on stable ground, the central bank increases its policy rate back to where it was before the downturn to a level which is considered ‘normal.’

This is one of the steps the FOMC took, first to support the economy out of the global financial crisis (GFC) of 2007-08 and then in the aftermath of COVID-19.

Prior to effecting a stimulative monetary policy during GFC, the effective federal fund rate (EFFR) stood at around 5.25%. Then, from December 2008 until the rate hike in December 2015, this rate remained in the 0.07% to 0.23% range.

Though the rate increased thereafter –returning to 2.43% in April 2019–, the FOMC effected stimulative policy again later that year because of stagnating growth, and then decreased it sharply in response to the disruption in economic activity caused by COVID-19. This led the rate to fall down again. Even after several rate hikes in 2022, the EFFR stood at 3.08% in early October.

monetary policy rates and inflation

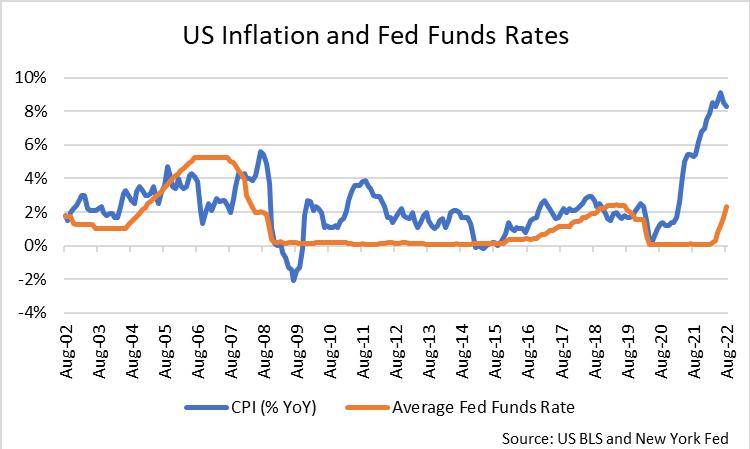

Though it may seem that the EFFR is on the right track, we need to look at the rate in light of prevailing inflation, shown in Figure 2 below:

Figure 2: CPI and the Fed Funds Rate

Source: https://fred.stlouisfed.org

033 Intelligent Risk - November 2022

This graph provides a lens into the aforementioned information on the fed funds rate with the perspective of prevailing sharp increase in prices.

As can be seen, not only is the EFFR nowhere close to its pre-GFC level of 5.25%, it is woefully short of where it should be given decades-high inflation in the US. At the current rate of inflation, the EFFR should be close to the 5.50% mark.

Though this may seem quite high compared to its level at the time of writing, the EFFR had been over the 7% level in June 2000. For reference, during that month in history, CPI inflation had risen at 3.70% yearover-year compared to 8.25% in August 2022. Also, the labor market was not as tight with unemployment at 4% as compared to 3.50% in September 2022.

In an interview on Bloomberg Television in early September 2022, former New York Fed President Bill Dudley observed that the then prevailing EFFR of 2.33% was “well, well below what you would consider to be neutral in this current inflation environment.”1

So, a level of EFFR in the 5%-5.50% range for even a short amount of time does not seem as unthinkable as it may have been at the beginning of 2022, not just because of the level of prevailing inflation but because of the factors which seem to be causing it.

Though the FOMC has tried normalizing the fed funds rate in the past as can be seen in Figure 2, global events like the GFC have prevented it from doing so. At other times, the Fed has been hesitant to raise rates for fear of hurting economic activity.

But the current conditions, as challenging as they are, provide a great opportunity for the FOMC to normalize at least the fed funds rate part of its monetary policy toolkit.

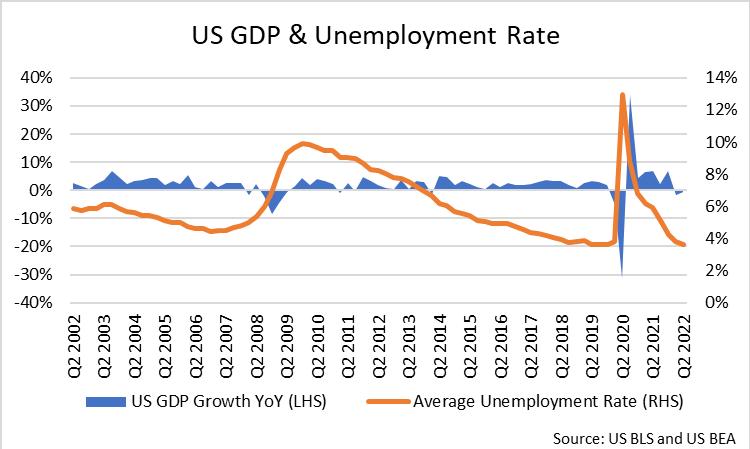

Figure 3: US GDP and average unemployment

Source: https://fred.stlouisfed.org

opportunity to normalise policy rates

/

034 Intelligent Risk - November 2022

1

https://www.bloomberg.com/news/articles/2022-09-09/fed-to-keep-rates-tighter-for-longer-than-expected-dudley-says

The labor market is tight, as seen by the low rate of unemployment in Figure 3 above, and economic growth, though experiencing a slight decline, is in reasonable shape with consumer spending holding up.

Further, unlike most other developed economies, especially those in Europe, the US is not facing a severe energy crisis or conflict. Unlike China, it is not facing a deteriorating property market and military tensions with immediate neighbours.