Finally, some incentives for purpose-built rental development! After years of detailing the anemic production since the late 1970s – all factually backed by government data – is this 45-year drought over? Unfortunately, no.

From our perspective, purpose built rental is the best choice for housing. It is the most affordable (no down payment, no generational mortgage, etc), most flexible (60 days notice), and offers secure long-term (sometimes lifelong) use as tenure is guaranteed (neither owner’s own use nor vacant possession due to sale). It’s a great housing choice and increasingly attractive to more and more people. But it is also the most undersupplied, despite the ongoing and growing demand.

Will the flurry of newly announced incentives including ‘as-of-right’ zoning, development charge exemptions, property tax discounts, rebates for more bedrooms, increased heights, and others, turn on the taps with gushing new production? Unfortunately, not in a large meaningful way, and certainly not gushing. It could be attractive for some niche homebuilders of ownership housing, but it won’t result in anything that would be considered ‘affordable’ by government standards. From a rental perspective, it’s a step in the right direction, but not big nearly enough.

Why such a grim view? The City of Toronto’s hired consultants took a deep dive on how changes and incentives would provide realistic opportunities for development of new housing. The experts concluded that for rental, even with land at no cost, the construction and operation of small-scale rental apartment buildings was unlikely to meet the return expectations of most rental developers. This financial assessment was for market rental housing, without the expectation of affordable units. When the incentives are tied to requirements – specifically income-based affordable rents – the outcome is often a ‘wash’. When you give with one hand, then take away with the other the net result is essentially status quo. Unfortunately, for purpose built rental, this means ongoing underproduction. The City’s experts noted that increasing height and density have a positive affect, but not enough to make a project financially viable. They recommended that discounted land, FULL DC rebate, and no parkland dedication, as the best ways to generate new rental supply. Another would be to provide a lengthy discount on property taxes.

Hopefully a few GTAA Members will find a way to make the numbers work and bring on some new units. We need lots of new rental supply. GTAA will continue to advocate for more incentives to create it. Send us your recommendations and participate in our ongoing engagement with government officials.

Publisher Nishant Rai

Account Executive

Justin Kreslin

Editorial

Daryl Chong

Creative Director / Designer

Scott Clark

Office Manager

Geeta Lokhram

Published By:

GTAAOnline is published monthly by RHB Inc. on behalf of the Greater Toronto Apartment Association (GTAA) and is distributed online through controlled circulation to the GTAA membership. Please contact the Publisher for advertising dates and rates. Opinions expressed are those of the authors and do not necessarily reflect the views and opinions of the GTAA Board or management. GTAA accepts no liability for information contained herein. Opinions expressed in articles are those of the authors and do not necessarily reflect the views and opinions of the GTAA Board or management. GTAA and RHB Inc. accept no liability for information contained herein. All rights reserved. Contents may not be reproduced without the written permission from the publisher.

P.O. Box 696, Maple, ON L6A 1S7 416-236-7473 All contents copyright © RHB Inc.

Elizabeth Ajadi (216) 273-1580

elizabeth.ajadi@bpapartments. com

Wendy Claure (416) 862-8414 105 wendy@gowanpm.com

Dave Nevins (613) 569-5699 David.nevins@irent.com

Julian Piro (437) 286-6101

julian@forwardlivinggroup.ca

Chris Woronchanka (288) 700-1188 chrisw@hamiltonpropertymanagement.com

Darren Henry (519) 242-4474 dmhenry10@gmail.com www.convertlytics.com

Ronald Tam (416) 482-2525 222 rmt@tamproperties.ca

Euphy Liu (519) 681-1999 euphy@aeoncanada.com aeoncanada.com/

Christian Coldea (647) 390-9545 info@ecobc.ca www.ecobc.ca

Nelan Ambikaipahan (905) 782-6082 nelan@certapro.com certapro.com/markham/

Highrise Restoration Inc.

Kunal Sood (905) 592-2772

info@highriserestoration.ca www.highriserestoration.ca/

Skylon Construction Corp.

Frank Benincasa (647) 829-4997 frank@skylonconstruction.ca skylonconstruction.ca/

Yaz Yadegari (416) 207-9993 111 yaz@kgr.ca www.kgr.ca/

David Pusateri (416) 864-4460 dave@xcelconstruction.ca xcelconstruction.ca

Ron Buffa (905) 660-3334 rbuffa@torque.ca www.torque.ca

Nathan Neyedly (416) 818-1163

nathan@depositrocket.ca rentaldepositsnow.com/

David Himmel (416) 303-4412 david@gowalnut.com www.gowalnut.com

Ocimar Dos Santos (905) 614-1320 3 ocimar@indoorairtech.ca www.indoorairtech.ca/

Boyd Dyer (647) 822-8975 boyd@qmeters.com www.qmeters.com

Asaph Benun (416) 649-1298 5245 abenun@ecosystem-energy.com ecosystem-energy.com/

Kirk Hochrein (905) 624-3479

kirk@kudlak-baird.com kudlak-baird.com/

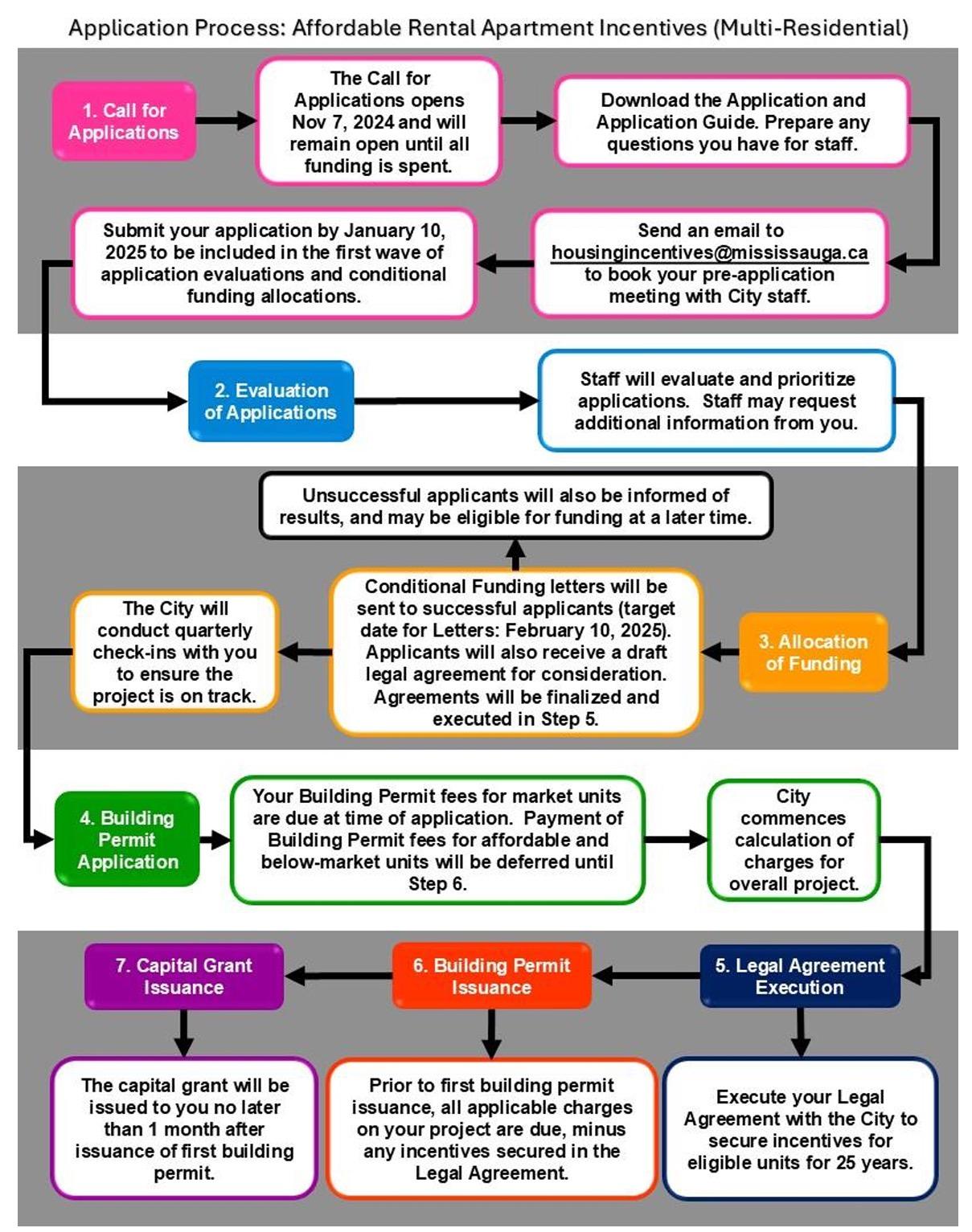

Mississauga’s $44 million affordable rental housing program

Private (and non-profit) developers are encouraged to apply to help get more affordable rental units built. Applications are now being accepted for the City’s affordable rental housing building program. This incentive program is designed to help quickly increase Mississauga’s supply of new affordable and below-market rental units in apartment buildings.

This program will help developers offset some of the costs required to deliver new units at affordable rates. Financial incentives are now available through the City’s Affordable Rental Housing Community Improvement Plan. The program is capped at $44 million in available incentives.

Successful applicants will receive a set capital grant per affordable unit and waivers/grants for certain municipal fees and charges. Non-profit affordable housing providers will also get their planning application fees waived. In Mississauga, “affordable units” must rent at or below 100% average market rent, and are eligible for:

• $130,000 grant per unit

• The City will provide a grant to cover the cost of building permit fees

• These units are also eligible for the provincially legislated exemptions for affordable housing units (City, Region and GO Transit development charges, community benefits charge, and cash-in-lieu of parkland)

In Mississauga, “below-market units” must rent at or below 125% average market rent, and are eligible for:

• $60,000 grant per unit

• The City will provide a grant to cover the cost of building permit fees

• The City will provide a grant to cover the cost of municipal fees (City development charges only, community benefits charge and cash-in-lieu of parkland)

Please review the program webpage for more details: HERE

Maximum monthly rent

Funding is available for private or non-profit rental development projects that create:

• Affordable units with rents at or below 100% average market rent

• Below-market units with rents at or below 125% average market rent

The current maximum monthly rents are identified in the following table. This table will be updated annually in accordance with the Provincial Affordable Residential Units for the Purposes of the Development Charges Act, 1997 Bulletin.

Projects must have at least five affordable or below-market units and maintain a 25-year affordability term.

User Friendly Self Service 24/7 Package Access Eliminates constant staff disruption for deliveries

Officially approved by Canadian Carriers Robust Lockers designed and built in USA

6-8 week delivery timeline

Projects must also meet the minimum unit size requirements to qualify:

• 47 square metres (505 square feet) for 1-bedroom units

• 63 square metres (678 square feet) for 2-bedroom units

• 79 square metres (850 square feet) for 3-bedroom units

How to apply

Applications submitted by January 10, 2025, will be reviewed first. Applications received after this date will be accepted and reviewed only while the Call for Applications remains open and funding is available.

To apply for the program:

1. Read the application guide.

2. Download and review the application form.

3. Book a pre-application meeting by emailing housingincentives@mississauga.ca

4. Complete and submit your application form.

The program has a capped funding amount that must be spent by the end of 2027. Projects will be prioritized on a “first-come, first-served basis” and a building permit is required to secure funding.

If your project meets eligibility requirements, you will receive confirmation from the City within approximately three weeks.

Background

• The affordable rental housing building program is funded through the City’s Affordable Housing Community Improvement Plan (“CIP”). A CIP is a tool under the Ontario Planning Act that allows municipalities to provide incentives such as grants and loans to help encourage development.

• The CIP was developed in consultation with industry stakeholders whose input was instrumental in helping to shape the program. It is designed to work in tandem with funding sources from other levels of government for new market rental and affordable rental construction.

• The focus of this CIP is to increase the supply of rental units affordable for moderate-income renter households earning $54,000 to $96,000 in household income. The CIP is not designed to deliver low-income units. Homes for low-income households are built and operated by the Region of Peel, the City’s municipal housing service manager.

• The Affordable Rental Housing CIP is a key action under Growing Mississauga: An Action Plan for New Housing. The action plan identifies steps the City can take to get more homes built, streamline building approvals and make homes more affordable.

Each year Toronto City Planning produces the Development Pipeline bulletin to provide a detailed analysis of how the city has developed and how it will continue to grow over time. The current report was published in June 2024 and provides an overview of all development projects with approval or construction activity between January 1, 2019 and December 31, 2023 – a five-year window.

The following contains excerpts and charts from the city’s report. Please review it for more information: HERE

Toronto’s Official Plan is the guide for development of the city over the next 30 years. It is regularly updated to reflect Toronto’s changing urban context and to conform with the Provincial Growth Plan for the Greater Golden Horseshoe and the Provincial Policy Statement. The Official Plan’s Urban Structure Map (refer to original report) identifies key geographies for accommodating housing and population growth, including the Downtown and Central Waterfront, and the Centres. The bulletin illustrates how the city has developed and how it will continue to grow over time. It reports on development occurring within growth management areas, as well as at a city-wide level, for the purpose of monitoring the implementation of the Official Plan.

The five-year 2023 Q4 Development Pipeline is comprised of 2,344 development projects. Cumulatively, these projects propose a record 800,889 residential units and 13,958,670 m2 of nonresidential gross floor area (GFA).

New projects were proposed in all areas of the city, however the net number of projects increased exclusively within growth management areas of the Official Plan, which demonstrates the success of the City’s policies in attracting and encouraging development in these areas.

Projects have become larger and more complex. While there are fewer Under Review projects than

there are Active projects, there are considerably more residential units in Under Review projects than there are in Active projects.

The volume of development proposals has historically been influenced by legislative and policy changes, as well as market conditions. Notably, a surge in applications in 2021 was partially triggered by the anticipated implementation of Inclusionary Zoning in 2022.

Source: City of Toronto, City Planning: Land Use Information System II Development projects with activity between January 1, 2019 and December 31, 2023. Built projects are those which became ready for occupancy and/or were completed. Active projects are those which have been approved, for which Building Permits have been applied or have been issued, and/or those which are under construction. Projects under review are those which have not yet been approved or refused and those which are under appeal.

Most of the residential units in the 2023 Pipeline are Under Review (54%) or Active (32%), with the remainder built during the five-year period. The 258,397 units in Active projects represent 90% of units required to achieve the Municipal Housing Target by 2031. Of the residential units within Active projects, 56% (144,351 units) have received at least one Planning approval but have not yet applied for a Building Permit, 17% (42,852 units) have applied for, but not yet been issued, a Building Permit, and 28% (71,194 units) are currently under construction but have not yet been completed.

There are 12,770 built units, 38,316 active units, and 116,424 units under review in All Other Areas. Units under review represent 70% of proposed residential units in All Other Areas, compared to 51% of residential units in Growth Areas. Since the 2020 Pipeline, the number of residential units proposed outside of growth management areas has nearly tripled from 69,276 units, representing an increase of 142% compared to growth of 46% in the growth management areas. About half of this increase is due to the proposed redevelopment of the Downsview Airport lands, which accounts for just over one-quarter of all residential units proposed in All Other Areas. Nevertheless, excluding Downsview, the number of residential units proposed outside of growth management areas has increased by over three-quarters.

Residential projects in growth management areas of the Official Plan are almost twice as large on average than those in the rest of the city. An average of 412 residential units are proposed per project located in a growth management area compared to 208 per project located outside of a growth management area, with the Centres (718 units per project) and Other Mixed Use Areas (645 units per project) containing the greatest number of residential units per project, on average.

Of the 800,889 residential units proposed in the Pipeline, an estimated 71,279 existing units will be demolished, while 40,370 units are proposed to be retained on site for a total of 841,259 units. To calculate new housing supply potential, the estimated number of demolished units are subtracted from the 800,889 proposed new units for a net increase of 729,610 units in the city.

Toronto has approved more than twice the number of residential units than were built over the past five years. An average of 38,428 residential units were approved per year between 2019 and 2023 pertaining only to Official Plan Amendment and Zoning By-law Amendment applications. Over the same period, an average of 17,576 units were built. Projects typically apply for Building Permits once they have received a final Planning approval in the form of a Notice of Approval Conditions (NOAC) or Statement of Approval for a Site Plan Control application. Considering only projects that have received a final Planning approval, the City approved an

of 21,534 residential units per year between 2019 and 2023. This is a surplus of 3,958 units on

built or a total of 123% of the

production through the Pipeline.

the

The City of Toronto has contributed an increasing share of new housing stock in the GTA. CMHC reported that between 1994 and 1998 just 21% of the dwelling completions in the GTA occurred within the City of Toronto. Between 2019 and 2023, Toronto’s share of GTA dwelling completions more than doubled to 49%. This growth occurred through intensification that is increasingly oriented towards high-rise built forms and infill housing. On average between 2019 and 2023, 9% of the units built per year were ground-related, made up of 1,041 single detached houses (6%), 96 semi-detached houses (1%), and 395 row or townhouses (2%) per annum. In contrast, 91% or 15,997 units were apartments and other dwelling types

Source: Canada Mortgage and Housing Corporation, Monthly Housing Now - Greater Toronto Area Reports

A mix of housing options, including rental and ownership tenure, is important for meeting the needs of a diverse city like Toronto. While condominium ownership units continue to be the predominant tenure for proposed residential units in the Pipeline, the number of proposed purpose-built rental units is increasing. The Development Pipeline tracks the intended tenure of projects. The applicant may change the tenure during the development process so the numbers of proposed purpose-built rental units for Active and Under Review development projects are subject to change. The Development Pipeline tracks purpose-built rental units through the City’s development approvals process, but does not capture the secondary rental market. Within the 2023 Q4 Development Pipeline, 539 projects propose to incorporate purpose-built rental units. Purpose-built rental units account for 15% of the total proposed residential units, or 120,301 units.

Three-quarters of purpose-built rental units in the Pipeline are in Growth Management Areas. A greater proportion of proposed rental units are located in the Downtown and Central Waterfront and along the Avenues compared to all proposed units in the overall Pipeline.

Source: City of Toronto, City Planning: Land Use Information System II Development projects with activity between January 1, 2019 and December 31, 2023. Built projects are those which became ready for occupancy and/or were completed. Active projects are those which have been approved, for which Building Permits have been applied or have been issued, and/or those which are under construction. Projects under review are those which have not yet been approved or refused and those which are under appeal.

VANCOUVER

Lance Coulson*** Executive Vice President lance.coulson@cbre.com

604. 662. 5141

VANCOUVER

Greg Ambrose* Vice President greg.ambrose@cbre.com

604. 662. 5178

EDMONTON David Young* Executive Vice President dave.young@cbre.com 780. 917. 4625

EDMONTON Thomas Chibri* Vice President thomas.chibri@cbre.com 780. 424. 5475

CALGARY Richie Bhamra* Executive Vice President richie.bhamra@cbre.com 403. 303. 4569

Chairman david.montressor@cbre.com 416. 815. 2332

LONDON Kevin MacDougall** Vice President kevin.macdougall@cbre.com 519. 286. 2013

The City’s Rental Housing Demolition and Conversion Control By-law protects against the demolition or conversion of rental housing on sites containing six or more rental units. The policies require demolished or converted units to be replaced by the same number of units at a similar rent for the purpose of sustaining Toronto’s rental housing stock.

Using this replacement requirement, the following table estimates the total number of net new rental units by subtracting existing rental units from total rental units, which includes both retained and proposed units.

The Pipeline contains 159,387 purpose-built rental units, of which 48,324 are existing rental units, the majority (81%) of which are intended to be retained and approximately 9,238 proposed to be demolished. If all projects in the 2023 Q4 Pipeline proposing purpose-built rental units were realized, there would be approximately 111,063 net new purpose-built rental units.

This estimate should be cautiously interpreted as the recording of existing units was introduced in 2018, so the number of existing units submitted prior to this date may be inaccurate. In addition, the Pipeline does not capture purpose-built rental units in smaller developments that do not require a Planning application.

Source: City of Toronto, City Planning: Land Use Information System II Development projects with activity between January 1, 2019 and December 31, 2023. Built projects are those which became ready for occupancy and/or were completed. Active projects are those which have been approved, for which Building Permits have been applied or have been issued, and/or those which are under construction. Projects under review are those which have not yet been approved or refused and those which are under appeal.

In 2020, Toronto adopted the “Growing Up Guideline” which encourage private developers to build familyfriendly units defined as large units containing two or more bedrooms. The Guidelines recommend that mid-and high-rise residential buildings should provide a minimum of 25% of its total residential units as large units that are suitable for families; 10% of units should be three bedrooms or greater, and 15% should be two-bedroom units.

Based on information submitted by applicants, the large majority of the proposed units in the pipeline are within mid- and high-rise buildings. The following table provides a breakdown of proposed unit types by number of bedrooms where this information has been provided by the applicants. Of the 668,660 units, most proposed units (61%) are in the form of 1-bedroom or studio apartments, with the remaining 39% having two or more bedrooms.

These proportions are similar to that seen in the entire pipeline, regardless of height. Additionally, there are 100,532 residential units (13% of the total units proposed) for which the breakdown has not been provided by the applicant. Unit breakdowns are, at times, not provided in the early stages of a Planning Application and are provided later as the application progresses through the approvals process.

The total number of family-suitable units proposed within mid- and high-rise buildings suggests that the City is on track to achieving the targets set out by the Growing Up Guidelines.

Ontario’s multi-residential sector remains one of the most resilient segments of commercial real estate capital markets. Notwithstanding market volatility over the last 24 months, investor sentiment for multifamily assets remains strong. As of Q4 2024, values have weathered the impact of higher borrowing costs and are well-positioned in an elevated rate environment due to stable and recurring income growth. Please see below for a summary of recent transactions and active listings within the Greater Toronto Area as of Q4 2024.

For additional info on cap rates, valuations, and market trends in the current investment landscape, please reach out to a member of the CBRE National Apartment Group.

Core-Plus Portfolio, Toronto, ON

346 Suites | $376,301 per Suite

Closed September 2024

$130,200,000

75 & 77 Huron Heights Drive,

110 Suites | $304,091 per Suite

Closed October 2024

$33,450,000

For more information, please contact:

David Montressor * Vice Chairman (416) 815-2332 david.montressor@cbre.com

Tom Schuster * Director (416) 847-3257 tom.schuster@cbre.com * Sales Representative

2, 6, 7 & 8 Park Vista, Toronto, ON

370 Suites | $359,459 per Suite

Closed September 2024

$133,000,000

2 Properties | 416 Suites ACTIVE LISTING

Source: City of Toronto, City Planning: Land Use Information System II

Proposed residential units in development projects with activity between January 1, 2019 and December 31, 2023. Built projects are those which became ready for occupancy and/or were completed. Active projects are those which have been approved, for which Building Permits have been applied or have been issued, and/or those which are under construction. Projects under review are those which have not yet been approved or refused and those which are under appeal.

Note: The number of units only includes units in projects in which the tallest proposed building is five stories or greater, and which the proposed generalized land use is Mixed Use or Residential Apartments, and thus may include units in buildings less than five stories if part of a larger development.

Across the 2,344 projects that are within the 2023 Q4 Pipeline, 1,701 projects propose non-residential GFA totaling 13,958,669 m2, about the equivalent of 51 Yorkdale Malls.

Between the 2021 Pipeline and the 2023 Pipeline, non-residential GFA proposed throughout the city increased slightly, by 8,181 m2, an increase of 0.1%, almost all of which was proposed in areas outside of the growth management areas.

Non-residential development activity is stable but becoming more distributed throughout the city. The Growth Management Areas of the Official Plan have generally maintained their respective shares of proposed nonresidential development since 2021. All the reported areas generally maintained their share of proposed nonresidential development since 2021.

A total of 2,970,854 m² of non-residential GFA was built across the city between 2019 and 2023, one-fifth of the total Pipeline. The majority (62%) of this non-residential GFA was built within the designated Growth Areas.

About 29% of non-residential GFA (1,691,341 m²) in the 2023 Pipeline is within projects that have been issued a Building Permit and thus are assumed to have started construction but that are not yet completed. For every 100 m² of Council-approved non-residential space, 61 m² is under construction.

Similar to proposed residential units, Council approved more non-¬residential GFA than was built over the five years from 2019 to 2023.

Toronto’s Non-Residential Market

Higher interest rates and inflationary pressures in 2023 slowed investment activity in both residential and nonresidential development and across all major markets in Canada. The impact on commercial real estate has varied through the COVID-19 recovery period. While the office sector has experienced negative impacts varying by the class of office space, retail and hotels have seen a positive recovery.

Overall office vacancy in Toronto reached an all-time high at 17% in 2023 Q4 as the market continued to face uncertain market conditions, up from 12% in 2022 Q2 and from 4% in 2019 prior to the start of the pandemic. Not all office space is the same with Class AAA office space and newer office buildings built after 2009 having vacancies of 6% and 8% respectively, while vacancy in older buildings was 18%.

Projects that have already begun construction are likely to continue to proceed through to occupancy, while those still in the planning stages are seeing delays or modifications to proposed non-residential components. The City is currently studying these issues through the Office Space Needs Study.

Industrial uses are about 15% of all proposed non-residential GFA, with about 39% in projects Under Review. Most proposed industrial GFA is located in All Other Areas (88%), mostly within designated Employment Areas. In 2023 Q4, Toronto accounted for 7% of all the industrial GFA currently under construction in the GTA, a decrease of 11% from 18% in 2022 Q4.

Toronto’s Official Plan outlines a strategy for directing intensification (over the next few decades) within this structure and establishes policies for managing change through the integration of land use and transportation. Some areas identified for intensification also need more detailed guidance in the form of Secondary Plans, area studies, and policies to guide local planning and innovative implementation solutions.

The Plan is intended to contribute to a future in which the public and private sectors work together and act as stewards of the city, leading Toronto to be a place where housing choices and economic opportunities are available for all people in their communities.

Within the 2023 Q4 Development Pipeline, 79% of residential units and 55% of non-residential GFA are proposed in areas currently targeted for growth by the City’s Official Plan, specifically Downtown and the Central Waterfront, the Centres, the Avenues, and other Mixed Use Areas.

Mixed Use Areas outside of the Avenues, Centres, and Downtown and Central Waterfront have 165,885 residential units and 1,369,071 m2 of non-residential GFA proposed across 257 projects. This accounts for 11% of the city’s total proposed projects, 21% of residential units and 10% of proposed non-residential GFA. Just over 91% of the proposed residential units in these areas are in projects that are either Under Review or Active. There were 10 projects in Mixed Use Areas proposing 2,500 residential units or more, totaling over 54,300 units

Source: CCity of Toronto, City Planning: Land Use Information System II

Development projects with activity between January 1, 2019 and December 31, 2023. Built projects are those which became ready for occupancy and/or were completed. Active projects are those which have been approved, for which Building Permits have been applied or have been issued, and/or those which are under construction. Projects under review are those which have not yet been approved or refused and those which are under appeal. Gross floor area values are expressed in square metres.

Large-scale residential projects are becoming more common across the city, including in Downtown and the Central Waterfront area. Of the 34 projects proposing 2,500 units or more, four of them are located Downtown and together propose close to 15,000 units. The largest residential project Downtown is 595 Front St W, which proposes to deck over the rail corridor and build five towers including just over 5,750 units, approximately 22,000 m2 of non-¬residential GFA, and on-site parkland.

The four Centres, Etobicoke, North York, Scarborough and Yonge-Eglinton, are focal points of transit infrastructure where jobs, housing, and services are concentrated. The Centres play an important role in managing the city’s growth, as the Official Plan encourages creating concentrations of workers and residents at these locations, resulting in significant centres of economic activity accessible by transit. Each Centre is unique in terms of its local character, its demographics, its potential to grow and its scale. To respect these differences, each Centre has its own Secondary Plan to guide intensification while ensuring the presence of an attractive public realm and necessary amenities.

Five of the 34 largest projects (those containing 2,500 residential units or more) proposed in the Pipeline are located within the Centres. Two are located in Scarborough and two are located in Etobicoke, areas that have experienced slower growth historically compared to Yonge-Eglinton and North York Centres.

The Avenues, as shown in the Official Plan’s Urban Structure Map are corridors along major arterials that are well served by transit and expected to redevelop incrementally over time. They play an important role within Toronto’s urban structure by providing locations for redevelopment outside of the Centres and Downtown.

While the Avenues contain the greatest number of proposed projects compared to the other growth management areas, they are generally smaller in scale. This reflects the implementation of the Avenues and MidRise Buildings Study and compatibility with the built context. The Mid-Rise Buildings Performance Standards are currently under review to provide greater flexibility in the development of mid-rise buildings. The average number of residential units proposed in projects along the Avenues is 295. However, the scale of projects along the Avenues is increasing, with Under Review projects having an average of 402 units, compared to 252 for Active projects and 159 for Built projects.

Similarly, the number of large projects (proposing 2,500 residential units or more) along the Avenues is increasing. Seven of the nine largest projects along the Avenues are under review, proposing a combined total of over 28,800 units, and the two largest Active projects along the Avenues propose close to 9,400 units.

There were 805 development projects proposed outside of the growth management areas, the Downtown and Central Waterfront, the Centres, Avenues, and other Mixed Use Areas, or 34% of the total projects in the city. These areas collectively contain a total of 167,510 residential units (21% of the total units proposed), representing an additional 34,642 units, or an increase of 26%, compared to the 2021 Pipeline. Generally, these projects are infill developments in areas designated as Neighbourhoods or Apartment Neighbourhoods. The majority (70%) of the residential units proposed in All Other Areas are under review. Of the 34 large projects (those proposing 2,500 residential units or more) in the Pipeline, four are located in All Other Areas.

The increasing amount of residential development proposed in All Other Areas signals that development is becoming more dispersed across the city than it has previously been. This trend is likely to continue with Council’s approval to permit townhouses and small-scale apartment buildings of up to six storeys and 60 units as-of-right on properties that are located along Major Streets and designated Neighbourhoods in the Official Plan.

Statistics Canada’s estimate of the Toronto’s population as of July 2021 is 2,917,666, which is about 4% or about 116,300 persons below the revised forecast. Disruptions caused by the COVID-19 pandemic have impacted the short-term growth in population, most notably as a result of more limited international migration which is a large driver of the City’s population growth. It is anticipated that the fundamental growth patterns of the region would reassert themselves in three years’ time. According to Statistics Canada, Toronto’s estimated population as of July 2023 is 3,110,984. This is population growth of almost 200,000 people over the two-year period from 2021.

Toronto’s housing growth is also on track with the household forecasts supporting A Place to Grow as amended in 2020. The forecast anticipates 495,000 households need to be accommodated over the forty-year period from 2011 to 2051.

To accommodate the additional households, more housing must be built. To realize this growth, some existing housing may need to be demolished. Based on an analysis of Demolition Permits over the 16-year period of 2005-2020, the overall average annual demolition rate versus housing units completed over the same period as reported by CMHC was 8.9%. The demolition rate can be applied to the potential housing supply to estimate the net supply.

Just twelve years into the forty-year forecast period, Toronto has built or has had proposed more than enough potential housing less estimated demolitions to accommodate the forecasted growth to 2051. The total potential housing supply of units built, approved and still under review since 2011 is over 900,000 residential units. CMHC reports that 215,206 units were completed between May 2011 and December 31, 2023 for a net total of 196,053 units. The Development Pipeline contains 258,397 units in projects with at least their first Planning approval but not yet built. If realized, the estimated new supply after accounting for demolitions would be 235,400 units. Together this is 87% of the net units required to accommodate the forecasted growth over forty years. A further 436,421 units are in development projects still under review for an estimated added net new supply of 397,580 units or a further 80% of the forecasted growth. Together this represents 167% of the units required to accommodate the forecasted household growth to 2051.

Not all submitted proposals are approved, and not all approved projects are built. Further, the City does not have any influence on the timing of when an applicant advances a Planning approval by submitting Building Permit applications or advancing construction. However, given these trends, there is more than enough supply in the Pipeline to accommodate the forecasted growth, and Toronto is well on its way to housing the population forecasted by A Place to Grow.

The full “Development Pipeline” report contains considerable data, and generally draws to the conclusion that Toronto will have more than enough housing to accommodate population growth forecasts. That is a generally fair assumption. However, the ongoing chronic undersupply of new purpose-built rental is not discussed, beyond a brief mention. And the report ignores the accumulated deficit of four plus decades of stagnant growth of primary rental housing. There is an over emphasis, without full acknowledgement, that almost all of Toronto’s recent and foreseeable housing will be provided by individual investors of condominium units. Many/most will not provide long term housing, and we continue to kick the can down the road and say everything’s rosy.

Explore money saving contract-pricing and time-saving business tools that help you operate efficiently, control costs, and keep your staff and those you serve safe.

HD SUPPLY OFFERS a wide variety of essential and innovative products for all of your facility maintenance needs, including:

• Appliances

Appliance Repair Parts

• Electrical

• Fabrication

• Hardware

• Health & Safety

• Housekeeping

HD Supply Brand Exclusives

• HVAC

• Janitorial

• Lighting

• Paint & Sundries

• PPE Plumbing and Commercial Plumbing Products

• Seasonal Products

• Textiles

• Tools

We also offer a dedicated Special Orders Department to help with those hard-find-products.

Take advantage of the various services we offer to help you manage your orders, improve your property, and make your job easier.

Take advantage of flexible credit limits, no third party provider and 30-day net terms by opening a credit account with HD Supply Canada, Inc.

Keep your property compliant with our procurement tools.

Direct ship and job site delivery options available. Enjoy free next-day delivery on stocked products to most locations.

Hassle-free, coast-to-coast and offers delivery, appliance placing, uncrating and move/ haul away services.

Whether it’s window coverings, flooring, PTAC units, appliances, cabinet refacing, or countertop replacement, we’ve got you covered from start to finish.

We will build a custom catalogue for an easy way to help limit your spend to pre-selected products for consistency and maximum savings.

Contact your Account Manager or call 1.800.782.0775 to get started

In May 2024, Toronto approved a city-wide permission for townhouses and small-scale apartment buildings up to 60 units and 6-storeys (19m), to be built on properties designated Neighbourhoods and in the Residential Zone category along the major streets.

Toronto Planning’s report, tabled at the Planning & Housing Committee, covered several items. The preamble stated that more than 700,000 new residents are expected by 2051. Toronto needs a diverse range of housing options to continue to thrive. That both current and future residents will need homes that accommodate the diversity of household sizes and compositions across the city.

Toronto’s recent housing growth has mostly been in mid- and high-rise buildings concentrated in densely populated areas like the Downtown, Centres, and Avenues, while the supply of low-rise housing, such as townhouses and small-scale apartment buildings, has not kept up with demand. Toronto’s low-rise Neighbourhoods are changing, but much of this change has come through expanding and rebuilding single-detached homes, through refreshing the existing housing with larger homes. The addition of secondary suites, laneway suites, and garden suites has occurred, but slowly. Recent new permissions for Multiplexes have enabled buildings with up to four units across the city.

Permissions for townhouses and small-scale apartment buildings will allow Neighbourhoods to add more housing that complements existing neighbourhood housing while creating a more intensive edge to the neighbourhoods along the major streets.

Townhouses and small-scale apartment buildings have been providing housing in many Toronto neighbourhoods for generations. Expanding permissions for this type of housing creates the opportunity for a range of ground-related/low-rise housing options.

Toronto’s Official Plan recognizes that major streets provide opportunities for additional density along the boundaries of the neighbourhoods. Permissions for townhouses and small-scale apartment buildings will provide a degree of height and density transition from growth areas to the interior of the Neighbourhoods.

With these approved “as-of-right” zoning permissions, this type of housing can be delivered relatively quickly as owners will only be required to obtain a building permit (and Site Plan Approval, when applicable) rather than official plan or zoning by-law approvals. Once enabled, it will remain the choice of the individual property owner whether to exercise these permissions.

The addition of townhouse and small-scale apartment buildings along the edges of Neighbourhoods throughout the city, will provide more diversity of housing, and support neighbourhood facilities and access to amenities. New residents in Toronto’s neighbourhoods can help stabilize declining populations, make better use of existing infrastructure, and support local retail establishments and services. These additional built form permissions introduce housing forms that are already present in many parts of the city into neighbourhoods that have historically been zoned to restrict housing types, helping the city distribute growth more evenly and to accommodate the needs of Toronto’s diverse population.

The original 30 unit cap for small-scale apartment buildings was considered by Planning and Housing Committee and was increased to 60 units by Council. The increase in density (to 60 units) will permit more variability of dwelling unit sizes, increasing the financial viability of these building types. The higher unit cap will permit increased variability in unit sizes, design and opportunities to utilize the available building envelope, particularly in situations where a proponent has assembled more than two lots.

The new permissions for small-scale apartment buildings on major streets are a transitional building type, complemented by other EHON permissions for multiplex dwellings and townhouses.

Providing Expertise in Building Science and Structural Restoration

Garage & Balcony Assessment & Restoration

Building Cladding Design, Assessment & Remediation

Roofing System Design, Assessment & Remediation

Building Condition Assessments

Capital Planning

Building Renewal

Energy Audits and Modelling

Toronto Planning will report back within two years, or following the issuance of the 200th building permit, to review the new policy and determine if changes are necessary.

Note that the Zoning By-law Amendment (ZBLA) stipulates requirements and criteria for many items in addition to unit count and height, such as, but not limited to, building length and depth, setbacks, separations distances, parking, driveways, amenities, water and wastewater servicing, etc. Please contact Toronto Planning for details.

The permissions open up over 31,000 lots to further potential for housing along major streets in Neighbourhoods. Providing permission for building types that have been common in the Former City of Toronto to enable intensification to be more equitably spread across the city, will contribute to increasing the variety and availability of housing for current and future residents of Toronto. Smoothing residential growth patterns through the introduction of townhouses and small-scale apartment buildings will make room for people to move into the neighbourhoods of their choice where existing land, infrastructure and services can be used more efficiently, local neighbourhood retail can be supported, and community vitality is sustained.

Will this work?

Toronto Planning commissioned Parcel Economics in 2023 to a review the financial feasibility of developing the proposed built forms to provide information as to whether the proposed zoning changes would provide realistic opportunities for development of new housing options.

The 2023 Financial Feasibility report tested the recommended small-scale apartment building and provided a series of outcomes based on case studies. Apartment buildings were analyzed assuming an assembly of two lots with development of up to 30 units in five storeys, with a parking ratio of 0.7 residential parking spaces per unit. Small-scale apartment buildings showed strong returns in Etobicoke and Scarborough.

When the cap was raised to 60 units, the Financial Feasibility study was updated. The resulting analysis was based on small-scale apartment buildings with smaller dwelling units, and additional constructed gross floor area due to inclusion of the permitted 6th storey. The analysis assumed a dwelling unit split of 50% 1-bedroom, 37% 2-bedroom, and 10% 3-bedroom units. The analysis indicated that a higher unit cap would result in more dwelling units (41 rather than 30) and higher profits. To achieve 60 units within

the contemplated building envelopes, the unit mix would need to include only studios and 1-bedroom units. Increasing the gross floor area beyond the contemplated building envelopes would allow for some 2 and 3-bedroom units, however, buildings would need to be taller than 6 storeys or have a larger floor plate requiring the costly assembly of additional adjacent lots. The improvement in feasibility is evident across all small-scale apartment buildings analyzed. However, note that this was for ownership condominium units … not purpose-built rental.

The 2023 analysis showed a challenge when considering development of these apartments as purpose built rental. However, in the context tested as part of the 2024 analysis, when these buildings are predominantly made up of studios and 1-bedroom units, the units tend to rent at a higher rent per square feet, essentially resulting in more revenue compared to larger units. This increase may result in this building type to be of potential interest to a broader range of developers, including those who may prefer to build for rental, whether non-profit or for-profit.

Similarly, the ability of small-scale apartment buildings to include affordable units was thought to be more likely with increased densities. Overall, both analyses showed financial feasibility for the recommended building types across Toronto, with the increase in

permitted density resulting in increased profits for small-scale apartment buildings.

The Expanding Housing Options in Neighbourhoods initiative is primarily a market housing initiative, focusing on the expansion of housing options, in a range of formats, within the City’s Neighbourhoods. EHON initiatives represent one portion of the City’s Housing Action Plan, which also includes a range of efforts to address housing access and affordability in Toronto. While the recommended expansion of land use permissions for townhouses and small-scale apartment buildings along major streets will not, in itself, result in the creation of affordable housing; instead, new permissions will enable housing forms that support residents with a broader range of incomes and household compositions at various life stages.

Parcel Economics was commissioned for both he 2023 and revised (60 unit) 2024 Financial Feasibility Studies. The report included a separate analysis for Purpose-Built Rental. In the original 2023 study, Parcel stated,

Rental feasibility is improving with recent government rebates, but at this scale it is still challenged. Even with land at no cost ($0), building and operating a rental stacked townhome or a small-scale rental

apartment building in Etobicoke, North York or Scarborough is unlikely to meet the return expectations of most build-to-hold rental developers.

In all areas the development of new rental buildings will require upfront savings and grants AND/OR operational savings over at least 10 years to justify the purchase of two lots at current land values

A small-scale rental apartment requires more than the assumed 10-year hold period to repay the initial equity investment and is heavily reliant on the future sale for investment returns.

With an increase to 60 units, Parcel Economics revised feasibility showed,

“a rental building of 60 studios and 1-bedrooms would achieve improved returns, however, upon completion it is still likely to yield less than a low-risk government bond and remains heavily reliant on the sale of the building some 15 years into the future to generate more than 87% of future cash flows. That said, some patient, long-term investors may be interested in undertaking such a project as yield is likely to increase over time and the potential for steady, positive cash flow exists.”

“To make rental work at these higher yields still requires costs savings, such as: discounted land; full DC rebate; and/or no parkland dedication.”

Although increase to height and density do positively affect rental yield, it is not enough to reach the targeted investment returns (e.g., above 10— year bond rates). For example, a 12-storey rental apartment building on the typical lots found in Scarborough has the potential to yield just over 3% (i.e., below current 10-yr bond rates).

To increase yield, revenues need to increase, costs decrease, or a combination of both. The City has more opportunity to effect costs. For example, a Development Charges Rebate AND no Parkland Requirement on the 5-storey Scarborough rental apartment has the potential for the same yield as the 12-storey building above, while achieving a higher IRR and EMx.

Parcel’s analysis of Affordability, they stated,

“A small-scale condo building comprised exclusively of smaller units has the potential to deliver 25% as affordable ownership and still deliver attractive returns.

But clearly acknowledged that for purpose-built rental,

“Affordable rental units remain challenging to deliver at this scale.”

Parcel concluded,

“Purpose-built rental feasibility has improved with the recent announcement of GST & PST rebates; however, it likely requires further subsidies or savings to be financially viable.”

So, will this work? It should initiate some ownership condominium projects, with lots of small units – which is counter to the city’s goal of larger, family sized units. Unfortunately, it is unlikely to create lots of new purpose-built rental units unless additional financial incentives are provided. GTAA will continue to advocate for incentives to create new rental supply.

More than 300 members of the Greater Toronto Apartment Association with their guests, friends and family gathered at our Annual Night at the Races at Woodbine Racetrack on July 11, 2024. It was five years’ since our last event (July 19, 2019) which was followed by the pandemic and an extended absence of private functions at the venue.

We returned to the Trackside Clubhouse, to enjoy the expansive patio area for a perfect afternoon and evening to be outdoors. The highlight summer social event of the year.

Events like this only happen with the generous support of our sponsors. Please join all of us in thanking the following sponsors for making this year’s event a huge success.

We’re already working on next year’s event. Watch for announcements in the coming months. Ready, set, go!

GTAA and our Members proudly support the academic advancement of our young residents. Best wishes to the winners, and all the applicants, in their studies and careers. We’re glad we were able to help.

Congratulations to Erjona , Rajeswari , Reayah , and Tristan – each received a $5,000 GTAA Scholarship!

Residents of GTAA Member buildings entering their first year of post-secondary education or training may be eligible for this scholarship next year. Watch for the details in May 2025!

Best wishes to the winners and all the applicants

GTAA Members continue to generously prepare meals and sort non-perishable food items at Scott Mission’s new HUB Kitchen and Distribution Centre.

The Scott Mission provides hot meals to the homeless 7 days a week, along with clothing, childcare services, a variety of other programs, and provides food banks.

The contribution of your time to those in greatly appreciated, and worthy of recognition. Thanks

In July 2024, Toronto adopted support for building code changes related to single means of egress in residential buildings between four and six storeys.

The report preamble provided a succinct outline:

“Exits are a fundamental and essential component of a building’s fire and life safety system. Some designers and others have advocated that the Ontario Building Code threshold for requiring a second exit stair in small multi-unit residential buildings is too high compared to other jurisdictions in North America, Europe and around the world. They suggest that a single exit staircase would support innovation in the design and construction of higher density small multi-unit buildings on constrained sites in higher density urban areas resulting in more missing middle housing.”

Toronto hired a third-party Building Code Consultant with expertise in fire protection engineering to undertake a technical feasibility study.

Note that the United States generally allows buildings of up to three storeys to have one staircase, but many municipal governments have their own codes, like in Manhattan and Seattle, where buildings can be up to six storeys (meeting local conditions). In Europe the height varies with Germany’s limit of 60m (approximately 20 storeys), and the United Kingdom’s limit of 18m (approximately seven) storeys.

Ontario’s Building Code (“Code”) is a regulation made under the Building Code Act (“Act”). The Code sets out province-wide technical and administrative requirements for the construction, renovation, change of use and demolition of buildings in Ontario. The Act and the Code are developed and administered by the Ministry of Municipal Affairs. Canadian provinces are in the process of harmonizing requirements with the National Construction Codes.

Ontario municipalities are responsible for enforcing the Code within their boundaries and are not permitted by the Act from passing by-laws which conflict with the Code, such as setting standards for building construction, or exceeding the Code requirements. In the absence of an Ontario Building Code amendment to allow for single exits in small multi-unit buildings, permit applications must propose an “alternative solution” under the Ontario Building Code.

The report concluded that an alternative solution is feasible, the innovation would be required to demonstrate to provide the same level of fire protection and life safety. To achieve this performance

and mitigate the risk associated with a single exit stair, the report provides potential mitigating features for an alternative solution to include, such as:

• Sprinklered building

• Restrictions on the number of suites per floor that are served by a single exit

• Maximum area of suites

• Travel distance limitations

• Maximum occupant load

• Limits on occupancy types served by a single exit

• Increased exit stair width

• Additional provisions/enhancements for fire protection and life safety systems

Toronto approved the development of a public-facing guideline for building permit applicants to access the feasibility report, thereby making it easier for developers and architects to craft their alternative solutions for single staircase designs in their building plans and making it easier for the City to evaluate an application that an architect may be making.

Each case will still need to be individually vetted by the Chief Building Official and a team of fire protection engineers, which is essentially the system that already exists.

Toronto’s adopted report will be forwarded to the Minister of Municipal Affairs and Housing and the Secretary of the Canadian Board for Harmonized Construction Codes to inform the development of any specific Ontario Building Code or National Building Code of Canada proposals on this topic.

In September 2024, the British Columbia Provincial Government updated the British Columbia Building Code (“BCBC”) to remove the code requirement for a second egress, or exit, stairwell per floor in buildings up to six storeys. This change will make it possible to build housing projects on smaller lots and in different configurations, while allowing more flexibility for multi-bedroom apartments, more density within areas of transit-oriented developments and the potential to improve energy efficiency in buildings. Previously, the BCBC called for at least two egress stairwells in buildings three storeys and higher.

GTAA will continue to advocate for this change in Toronto and Ontario, and provide updates as they become available.

As a property manager, you know the importance of keeping costs low while maintaining a comfortable living environment for your residents. Now, with the Affordable Housing Multi-Residential Program, you can receive financial incentives of up to $200,000 to upgrade your building’s energy systems. Plus, get free upgrades and expert assistance every step of the way.

• Reduce energy, maintenance and operating costs.‡

• Improve the energy efficiency of your building.

• Enhance resident comfort, health and well-being. Why upgrade now?

• Control costs more effectively with automated systems.

• Building automation controls

• Variable frequency drives

• Water heaters • Hybrid heat pumps • Ventilation technologies

Is your building eligible? This program is for: • Eligible private market-rate multi-residential buildings† • Shelters and co-ops • Social, municipal and nonprofit housing providers