12 minute read

IFR presenta il rapporto World Robotics 2021

L’industria dei robot cresce ancora

I

Il rapporto Industrial Robots mostra un record di 3 milioni di robot industriali che operano nelle fabbriche di tutto il mondo, con un aumento del 10%. Le vendite di nuovi robot sono cresciute leggermente dello 0,5% nonostante la pandemia globale, con 384.000 unità spedite a livello globale nel 2020. Questa tendenza è stata dominata dagli sviluppi positivi del mercato cinese, che ha compensato le contrazioni di altri mercati. Il 2021 è il terzo anno record nella storia dell’industria della robotica, dopo i successi del 2018 e il 2017.“Le economie del Nord America, dell’Asia e dell’Europa non hanno vissuto contemporaneamente il punto più basso del Covid-19”, afferma Milton Guerry, presidente della Federazione internazionale di robotica. “L’assunzione di ordini e la produzione nell’industria manifatturiera cinese hanno iniziato a crescere nel secondo trimestre del 2020. L’economia nordamericana ha iniziato a riprendersi nella seconda metà del 2020 e l’Europa ha seguito l’esempio un po’ più tardi”. “Si prevede che, a livello globale, le installazioni di robot riprenderanno fortemente e cresceranno a 435.000 unità nel 2021, superando così il livello record raggiunto nel 2018”, riferisce Milton Guerry. “Inoltre le installazioni in Nord America aumenteranno del 17% a quasi 43.000 unità. Le installazioni in Europa dovrebbero crescere dell’8% a quasi 73.000 unità. Per l’Asia è previsto il superamento della soglia delle 300.000 unità che aggiungerannao il 15% al risultato dell’anno precedente. Quasi tutti i mercati del sud-est asiatico cresceranno con tassi a due cifre nel 2021”.

Asia, Europa e Americhe

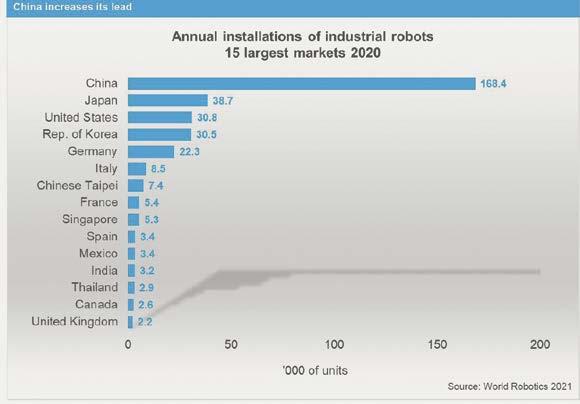

L’Asia rimane il più grande mercato al mondo per i robot industriali. Il 71% di tutti i robot di nuova implementazione nel 2020 è stato installato in Asia (2019: 67%). La Cina, il più grande utilizzatore della regione, ha avuto una crescita del 20% con 168.400 unità spedite. Questo è il valore

ENGLISH TEXT

IFR presents World Robotics 2021 reports

“Robot Sales Rise Again”

The World Robotics 2021 Industrial Robots report shows a record of 3 million industrial robots operating in factories around the world – an increase of 10%. Sales of new robots grew slightly at 0.5% despite the global pandemic, with 384,000 units shipped globally in 2020. This trend was dominated by the positive market developments in China, compensating the contractions of other markets. This is the third most successful year in history for the robotics industry, following 2018 and 2017. “The economies in North America, Asia and Europe did not experience their Covid-19 low point at the same time,” says Milton Guerry, President of the International Federation of Robotics. “Order intake and production in the Chinese manufacturing industry began surging in the second quarter of 2020. The North American economy started to recover in the second half of 2020, and Europe followed suit a little later.” “Global robot installations are expected to rebound strongly and grow by 13% to 435,000 units in 2021, thus exceeding the record level achieved in 2018,” reports Milton Guerry. “Installations in North America are expected to increase by 17% to almost 43,000 units. Installations in Europe are expected to grow by 8% to almost 73,000 units. Robot installations in Asia are expected to exceed the 300,000-unit mark and add 15% to the previous year’s result. Almost all Southeast Asian markets are expected to grow by double-digit rates in 2021.”

Asia, Europe and the Americas - overview

Asia remains the world’s largest market for industrial robots. 71% of all newly deployed robots in 2020 were installed in Asia (2019: 67%). Installations for the region´s largest adopter China grew strongly by 20% with 168,400 units shipped. This is the highest value ever recorded for a single country. The operational stock reached 943,223 units (+21%). The 1-million-unit mark will be broken in 2021. This high growth rate indicates the rapid speed of robotization in China. Japan remained second to China as the largest market for industrial robots, though the Japanese economy was hit hard by the Covid-19 pandemic: Sales declined by 23% in 2020 with 38,653 units installed. This was the second year of decline following a peak value of 55,240 units in 2018. In contrast to China, demand from the electronics industry and the automotive industry in Japan was weak. Japan’s operational stock was 374,000 units (+5%) in 2020. The outlook for the fiscal year 2021 is positive with an expected GDP growth rate of 3.7%. The Japanese robotics market is expected to grow by 7% in 2021 and continue to do so by 5% in 2022. Independent of the domestic market for robotics, the major export destinations will secure demand for Japanese robotics. Even though a major share of production today takes place directly in China, 36% of the Japanese exports of robotics and automation technology were destined for China. Another 22% of the exports were shipped to the United States. The Republic of Korea was the fourth largest robot

più alto mai registrato per un singolo paese. Lo stock operativo ha raggiunto le 943.223 unità (+21%). Il traguardo di 1 milione di unità verrà superato nel 2021. Questo alto tasso di crescita indica la rapida velocità della robotizzazione in Cina. Il Giappone è rimasto secondo alla Cina come il più grande mercato per i robot industriali, anche se l’economia giapponese è stata duramente colpita dalla: le vendite sono diminuite del 23% nel 2020 con 38.653 unità installate. Questo è stato il secondo anno di calo dopo un valore di picco di 55.240 unità nel 2018. A differenza della Cina, la domanda dell’industria elettronica e dell’industria automobilistica in Giappone è stata debole. Lo stock operativo del Giappone era di 374.000 unità (+5%) nel 2020. Le prospettive per l’anno fiscale 2021 sono comunque positive, con un tasso di crescita del PIL del 3,7%. Si prevede che il mercato della robotica giapponese crescerà del 7% nel 2021 e continuerà a farlo del 5% nel 2022. Indipendentemente dal mercato interno della robotica, le principali destinazioni di esportazione garantiranno la domanda di robotica giapponese. Anche se oggi una quota importante della produzione avviene direttamente in Cina, il 36% delle esportazioni giapponesi di robotica e tecnologia di automazione era destinato alla Cina. Un altro 22% delle esportazioni è stato spedito negli Stati Uniti. La Repubblica di Corea era il quarto mercato di robot in termini di installazioni annuali, dopo Giappone, Cina e Stati Uniti, ma c’è stata una diminuzione del 7% nel 2020. Lo stock operativo di robot oggi è stato calcolato a 342.983 unità (+6%). Finora l’economia orientata all’esportazione ha affrontato la pandemia in modo eccezionale. Nel 2020 il PIL è diminuito solo dell’1% e per il 2021 e si prevede una forte crescita del PIL del +4% e +3% per il 2022. L’industria elettronica e l’industria dei semiconduttori, in particolare, stanno investendo molto. Un programma di sostegno agli investimenti lanciato nel maggio 2021 aumenterà ulteriormente gli investimenti in macchinari e attrezzature. La domanda di robot sia da parte dell’industria elettronica che dai fornitori automobilistici, dovrebbe crescere sostanzialmente dell’11% nel 2021 e dell’8% annuo in media nei prossimi anni.

Europa

Le installazioni di robot industriali in Europa sono diminuite dell’8% a 67.700 unità nel 2020. Questo è stato il secondo anno di calo, dopo il picco di 75.560 unità nel 2018. La domanda dall’industria automobilistica è diminuita di un altro 20%, mentre la domanda dall’industria generale è cresciuta del 14%. La Germania, che appartiene ai cinque maggiori mercati mondiali di robot (Cina, Giappone, USA, Corea, Germania) e ha una quota del 33% del totale delle installazioni in Europa. Seguono l’Italia con il 13% e la Francia con l’8%. Il numero di robot installati in Germania è rimasto invariato a circa 22.300 unità nel 2020. Questo è il terzo numero di installazioni più alto di sempre, un risultato notevole data la situazione pandemica che ha dominato il 2020. L’industria della robotica tedesca si sta riprendendo, trainata da una forte attività all’estero. Si prevede che la domanda di robot in Germania crescerà lentamente, principalmente sostenuta dalla domanda di robot a basso costo nell’industria generale e al di fuori della produzione. Nel Regno Unito, le installazioni di robot industriali sono aumentate dell’8% a 2.205 unità. L’industria automobilistica è aumentata del 16% a 875 unità, rappresentando il 40% delle installazioni nel Regno Unito. L’industria alimentare e delle bevande ha quasi raddoppiato le proprie installazioni da 155 unità nel 2019 a 304 unità nel 2020 (+96%), anche perché sta affrontando una massiccia carenza di manodopera. Con le continue restrizioni di viaggio legate al Covid-19 e la Brexit, si prevede che la domanda di robot nel Regno Unito crescerà fortemente. In un’ottica di “modernizzazione” del Regno Unito l’in-

dustria manifatturiera sarà aiutata in questi investimenti da un massiccio incentivo fiscale. Le 2.205 unità appena installate nel Regno Unito sono circa dieci volte meno di quelle spedite in Germania (22.302 unità), circa quattro volte meno che in Italia (8.525 unità) e meno della metà in Francia (5.368 unità).

Nord America

Gli Stati Uniti sono il più grande utilizzatore di robot industriali nelle Americhe, con una quota del 79% delle installazioni totali della regione. Seguono il Messico con il 9% e il Canada con il 7%. Le nuove installazioni negli Stati Uniti hanno rallentato dell’8% nel 2020. Questo è stato il secondo anno di calo dopo otto anni di crescita. Mentre l’industria automobilistica ha richiesto un numero sostanzialmente inferiore di robot nel 2020 (10.494 unità, -19%), le installazioni nell’industria elettrica/elettronica sono cresciute del 7% a 3.710 unità. Lo stock operativo negli Stati Uniti è aumentato del 6% CAGR dal 2015. Le aspettative complessive per il mercato nordamericano sono molto positive. È attualmente in corso una forte ripresa e per il 2021 è previsto il ritorno ai livelli pre-crisi delle installazioni di robot industriali. Le installazioni di robot dovrebbero crescere del +17% nel 2021. Un boom post-crisi creerà un’ulteriore crescita.

Previsioni

Il “boom post-crisi” dovrebbe svanire leggermente nel 2022 su scala globale. Dal 2021 al 2024 sono previsti tassi di crescita medi annui nella fascia media a una cifra. Nel 2024 si prevede di raggiungere il notevole traguardo di 500.000 unità installate all’anno in tutto il mondo. Per scaricare il rapporto completo visitare il sito di IFR

ENGLISH TEXT

market in terms of annual installations, following Japan, China and the US. Robot installations decreased by 7% to 30,506 units in 2020. The operational stock of robots was computed at 342,983 units (+6%). The export-oriented economy has coped with the pandemic remarkably well so far. In 2020, GDP was down by just 1%, and for 2021 and 2022 strong GDP growth of +4% and +3% is expected. The electronics industry and the semiconductor industry, in particular, are investing heavily. An investment support program launched in May 2021, will further boost investment in machinery and equipment. The demand for robots both from the electronics industry as well as from the automotive suppliers is expected to grow substantially by 11% in 2021 and by 8% annually on average in the next years following.

Europe

Industrial robot installations in Europe were down by 8% to 67,700 units in 2020. This was the second year of decline, following a peak of 75,560 units in 2018. Demand from the automotive industry dropped by another 20%, while demand from the general industry was up by 14%. Germany, which belongs to the five major robot markets in the world (China, Japan, USA, Korea, Germany) had a share of 33% of the total installations in Europe. Italy followed with 13% and France with 8%. The number of installed robots in Germany remained at about 22,300 units in 2020. This is the third highest installation count ever - a remarkable result given the pandemic situation that dominated 2020. The German robotics industry is recovering, driven by strong overseas business. Robot demand in Germany is expected to grow slowly, mainly supported by demand for low-cost robots in the general industry and outside of manufacturing. In the United Kingdom, industrial robot installations were up by 8% to 2,205 units. The automotive industry rose by 16% to 875 units - representing 40% of the installations in the UK. The food and beverage industry almost doubled their installations from 155 units in 2019 to 304 units in 2020 (+96%). The food and beverage industry had a high share of foreign workers, often from Eastern Europe, is facing a massive labor shortage. With continued Covid19-related travel restrictions as one reason and Brexit another, the demand for robots in the United Kingdom is expected to grow strongly at two-digit percentage rates in 2021 and 2022. [struggling to connect] The modernization of the UK manufacturing industry will be boosted by a massive tax incentive. The newly installed 2,205 units in the UK are about ten times less than the shipments in Germany (22,302 units), about four times less than in Italy (8,525 units) and less than half the number in France (5,368 units).

North America

The USA is the largest industrial robot user in the Americas, with a share of 79% of the region´s total installations. It is followed by Mexico with 9% and Canada with 7%.New installations in the United States slowed down by 8% in 2020. This was the second year of decline following eight years of growth. While the automotive industry demanded substantially fewer robots in 2020 (10,494 units, -19%), installations in the electrical/electronics industry grew by 7% to 3,710 units. The operational stock in the United States increased by 6% CAGR since 2015. The overall expectations for the North American market are very positive. A strong recovery is currently in progress and the return to pre-crisis levels of industrial robot installations can be expected for 2021. Robot installations are expected to grow by +17% in 2021. A post-crisis boom will create additional growth at low double-digit rates 2022 and beyond.

Outlook

The “boom after crisis” is expected to fade slightly in 2022 on a global scale. From 2021 to 2024, average annual growth rates in the medium single-digit range are expected. Minor contractions may occur as a statistical effect, ‘catch-up’ occurs in 2022 or 2023. If this anomaly takes place, it will not break the overall growth trend. The notable mark of 500,000 units installed per year worldwide is expected to be reached in 2024. For more information visit IFR web site