We would like to acknowledge and thank all parties who made time to participate in the consultation process: Nissan, Polestar, Renault, Tesla Motors, Hyundai, Mitsubishi, Ford, The Australian Energy Regulator, Energy Consumers Australia, ,Monash University, Electric Vehicle Council, Australian EV Association, Electric Future, Jetcharge, Net Zero Engineering Solutions, JLL, EVSE Australia, Ambibox, Sigenergy, Fermata Energy, StarCharge, Next-Dimension, IEA Task 53, Australian National University, California Energy Commission, University of Technology Sydney, ACT Government, Amber Electric, German Ministry for Economic Affairs and Climate Action, Evergen, Kaluza, SwitchDin, AGL, Combined Energy Technologies, Reposit, The Mobility House, ActewAGL, Australian Energy Market Operator, CharIN, CSIRO, Dekra, NewVolt, Weavegrid, Delta, Team Global Express, US Department of Energy, Synergy, QLD Government, Smart Energy Council, Clean Energy Council, Ausgrid, CitiPower, Powercor & United Energy, Endeavour Energy, Energy Queensland, Essential Energy, Evoenergy, South Australia Power Networks and Western Power

Special thanks go to project delivery partners Endgame Economics, ThinkPlace, Watture and Vehicle-Grid Integration Council.

Disclaimer

This paper was commissioned by the Australian Renewable Energy Agency (ARENA) and RACE for 2030 (RACE). The report presents the findings of enX research and consultations in support of the National Roadmap for Bidirectional EV Charging

The paper is provided as is, without any guarantee, representation, condition or warranty of any kind, either express, implied or statutory. ARENA, RACE and enX do not assume any liability with respect to any reliance placed on this report by third parties. If a third party relies on the report in any way, that party assumes the entire risk as to the accuracy, currency or completeness of the information contained in the report. To the best of ARENA, RACE and enX’s knowledge, no conflict of interest arose while preparing this report.

This work is copyright, the copyright being owned by the enX Except for the Commonwealth Coat of Arms, the logo of ARENA and RACE and other third-party material protected by intellectual property law, this copyright work is licensed under the Creative Commons Attribution 3.0 Australia Licence. Wherever a third party holds copyright in material presented in this work, the copyright remains with that party. Their permission may be required to use the material.

Except for the Commonwealth Coat of Arms, enX has made all reasonable efforts to: clearly label material where the copyright is owned by a third party; and ensure that the copyright owner has consented to this material being presented in this work. Under this licence you are free to copy, communicate and adapt the work, so long as you attribute the work to enX and abide by the other licence terms. A copy of the licence is available at https://creativecommons.org/licenses/by/3.0/au/. Requests and enquiries concerning rights should be addressed to arena@arena.gov.au

Bidirectional charging (‘bidi’) allows for the two-way flow of electricity between an EV and an external electricity system. This means that EV electricity loads can be shifted in time (unidirectional smart charging), and EVs can also act as a generator that produces power for a home or building and/or, to support the grid.

Types of bidi include:

• Vehicle to grid (V2G) - EVs supply power to a mains electrical circuit that is electrically connected to the grid

• Vehicle to homes and buildings (V2H/B) – EVs supply power to local electrical distribution system that is electrically separated from the grid

• Vehicle to load (V2L) – EVs supply power directly to one or more electrical appliances that are electrically separated from the grid.

Purpose and scope of this paper

This Background Paper provides further detail in support of the separate National Roadmap for Bidirectional EV Charging. It consolidates the outcomes of a desktop review of current bidirectional charging studies and trials in key markets and extensive supply chain and stakeholder engagement.

This project seeks to define the critical paths, enablers, and barriers to achieve the following Market Objective:

Bidirectional charging is readily available to provide high value services across the Australian economy by 2030, with several products available by 2027.

The interviews and workshops held as part of this project have validated this objective as achievable for residential bidi applications. However, this outcome is not a given and it is contingent on various conditions which are set out in the National Roadmap for Bidirectional EV Charging. While other bidi use-cases (i.e. outside residential applications) may have additional barriers and complexities, stakeholders considered they will closely follow and be somewhat contingent on the residential uptake as that will contribute to community familiarity, a competitive supply of vehicles and EV supply equipment (EVSE) and required grid connection and market participation incentives frameworks.

Market context

Many (possibly all) EV automakers are currently in the process of developing bidirectional charging products. Over the past 24 months, stakeholders have reported a shift in focus from technology demonstrations to preparing early-stage mass-market products, especially V2G for residential customers (with a greater focus on V2H in the US)

Without explicit policy support, bidi availability in Australia can be expected to lag major international markets such as the US and Europe. This is primarily due to Australia being a

relatively small market and that international automakers will prioritise home markets for bidi productisation and product homologation. There was a consistent view among stakeholders that Australia’s leadership on solar and battery uptake could be replicated with bidi, subject to Australia presenting a compelling market offering, and that a competitive supply of bidirectional EV charging products and services could be bought forward.

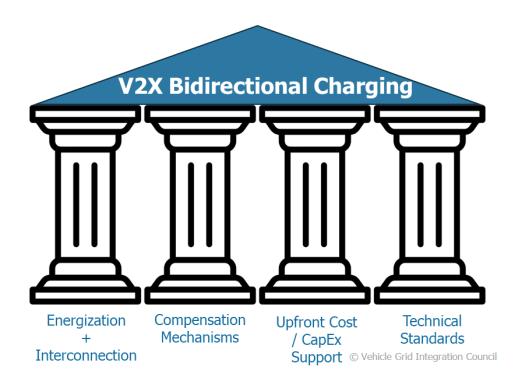

Overall, the timely supply of both bidirectional EV and EVSE products to Australia is thought to be most influenced by four factors:

1. Government policy and incentives

2. Australia’s addressable market size including our customer value proposition

3. The transparency, accessibility, stability and efficiency of standards and regulatory approval frameworks

4. The availability of capable vehicles and EVSE, which will be influenced by the three factors above.

Opportunities by transport sector

The residential sector was universally considered the most scalable opportunity for bidi. This would leverage prior CER and electricity network investments and Australia’s world-beating customer interest in rooftop solar. The overwhelming view of stakeholders was that broadbased incentives can accelerate market commitments by vehicle OEMs and that further studies and demonstration projects were not required to accelerate uptake in this sector Over the past two decades, Australians have installed over 3.8 million rooftop solar systems and there is no apparent reason, based on expected EV uptake rates, why similar V2G uptake levels could not be achieved over the coming decades.

Commercial fleets were generally not seen as an immediate priority due to the need to focus on, and overcome, present barriers to unidirectional charging uptake. However, there are signs of early interest in V2G integration by some fleet owners which may accelerate once vehicles in relevant classes become more available.

Europe has seen car-sharing as an early, successful use-case for bidi and there was a view that the market opportunity for car-sharing and bidi could be mutually reinforcing, with bidi offering a revenue stream that could readily fit into a car-sharing business model.

Several stakeholders commented that it was important to ensure public charging equipment can support bidi. However, it is currently difficult to make an investment case without a better understanding of how this would align with a positive consumer public charging experience. The size of this opportunity is also thought to be relatively minor.

Heavy vehicles are an important area for future growth. Rigid trucks and buses were considered most favourably due to often shorter runs and duty cycles which typically allow for longer overnight recharging periods. Vehicle availability was seen a critical constraint ahead of 2030 during which time targeted demonstrations could be explored to firm up the commercial case for fleet operators. Articulated trucks with high utilisation and longer haulages were not seen as an opportunity in the near term outside of niche applications (e.g., primary frequency control service delivery). Several stakeholders noted the benefits of further studies to identify specific opportunities for bidi across commercial fleets and heavy vehicles.

Table 1 – A summary of the relative size of the opportunity in 2030 and the relative importance of specific conditions that contribute to the Market Objective

The relative importance of conditions that can contribute to the Market Objective

The availability of V2G-enabled vehicles (as opposed to V2L/V2H) as a foundational condition

Clear national policy direction to support international supply chain engagement and investment

Permissive vehicle warranty conditions that are aligned with highest-value customer use-cases

Financial incentives to support early adopters overcome initial high upfront cost and complexity

Trials and case studies that demonstrate commercial benefits and act to derisk investment decisions

The availability of supportive (cost reflective) retail tariffs and dynamic (network support) incentives

Reduction in the FCAS minimum bid size

Coordinated public messaging to address customer concerns and build awareness, understanding and trust

Minimum standards for 'behind the meter' interoperability to support local device orchestration

Permissive and nationally consistent network connection requirements and grid codes to support EV and EVSE homologation

Transparency about future smart grid architecture direction to support increased EV and EVSE supplies

Industry convergence on ISO 18118-20 to support plug & play interoperability between vehicles and chargers

Engagement to ensure Australia’s requirements are a represented in international standards processes

Support for local product homologation for EVSE and automaker OEMs

Chapter summaries

1. Background – This chapter provides context for the project and defines different types of bidi and AC/DC technology configurations. A key message is that the term ‘V2G’ covers any bidi application that is grid-connected, including where the system is export-limited and used only for self-consumption. While V2G has the greatest value, it has greater hurdles to clear related to local grid code compliance. V2H/B relates only to off-grid or backup supply applications but has a faster potential path to market

2. Technology and commercial readiness – This chapter looks at the commercial readiness of different aspect of the bidi technology stack including standards and protocols and provides a state of the market summary. It identifies vehicle availability as the critical barrier to market development and ISO 15118-20 as an enabler (and barrier) to plug and play interoperability between cars and chargers. It describes the different challenges associated with AC & DC bidi applications and the potential to support OEMS homologating products in our market. All the major challenges are software (rather than hardware) related.

3. Exploring bidirectional charging value streams – This chapter explores the potential value streams associated with back-up power and V2G applications such as energy arbitrage, network support and frequency control. It identifies more cost reflective network tariffs as a key enabler of efficient value transfer to consumers. Intraday energy arbitrage and network support are considered the most valuable and scalable services and frequency control may have a role in some heavy vehicle applications.

4. Consumer appetite and readiness – This chapter explores the learning from local smart charging trials and stakeholder perspectives and international V2G demonstrations which demonstrate the potential for consumers to engage in new energy management services. A range of potential consumer motivations are identified with financial returns being the most effective driver of purchasing decisions and long-term consumer behaviour change. We explore the role of early technology adopters and trusted information sources in supporting positive outcomes for consumers. Minimum interoperability and access standards are identified as foundational to efficient value transfer, consumer choice and competitive market operation.

5. The economic value case for bidirectional charging – This chapter summarises local and international electricity market modelling and potential consumer savings estimates. While it is difficult to cross-compare estimates, there is a generally consistent finding that bidi offers consumer and long-term economic value. Further analysis is provided in the separate V2G Energy Market Modelling Report

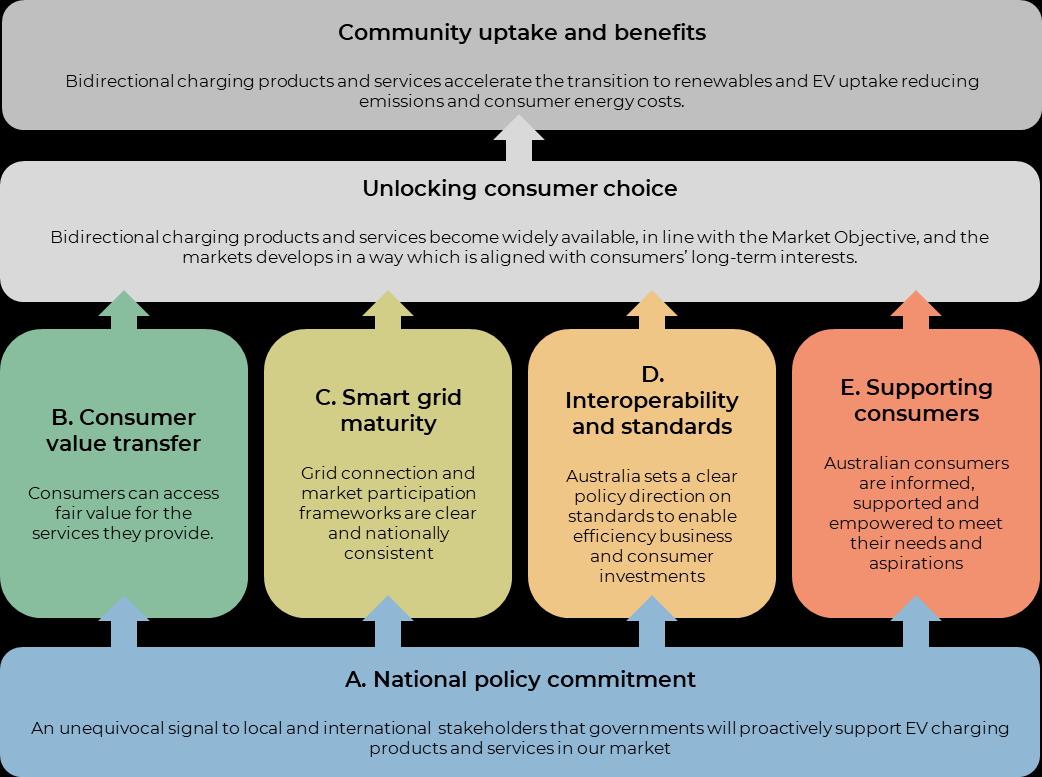

6. Potential roadmap directions – With national policy leadership and support from state and territory governments, there was a consistent view among stakeholders that Australia could bring forward bidi product availability delivering material benefits for Australian consumers and accelerating and supporting our transition to renewables. This leadership should take the form of:

• A strong national policy narrative that signals a clear alignment of bidirectional charging proliferation with Australia’s national interests

• Implementation of concrete actions to advance this interest.

The chapter sets out a range of potential policy and strategy action considered by participants at the National Roadmap for Bidirectional EV Changing Codesign Workshop. These are arranged as per the five coloured boxes the figure below.

ES Figure 1 – Conceptual framework for categorising potential roadmap directions

Glossary of terms

AC Alternating Current

AS/NZ 4777.1:2024

AS/NZ 4777.2:2020

Australia’s installation standard for grid-connected inverters

Australia’s product standard for grid-connected inverters

BESS Battery energy storage system

Bidi Bidirectional EV charging

BPT Bidirectional power transfer

AEMO Australian Energy Market Operator

ARENA The Australian Renewable Energy Agency

BMS Battery Management System

CCS Combined Charging System (for AC and DC charging)

CER, DER Consumer Energy Resource, Distributed Energy Resource

CHAdeMO A standard for EV-EVSE connection and interoperability origination from Japan

CharIN A global association promoting standards for EV charging systems

CPO Charge Point Operator (responsible for charge session management)

CSIP-AUS Common Smart Inverter Profile – Australia, used to communicate dynamic operating envelopes and related information between Australian electricity distribution networks and customer devices. Based on IEEE 2030.5

CSMS Charging Station Management System

DC Direct Current

DOE Dynamic operating envelopes

DSO/DNSP Distribution System Operator / Distribution Network Service Provider (same thing)

EMS, HEMS Energy Management System, Home Energy Management Systems

EV, BEV, PHEV Electric vehicle, Battery Electric Vehicle, Plug-in Hybrid Electric Vehicle

EVSE Electric Vehicle Supply Equipment

IEEE 2030.5 A protocol that standardises communications between utilities and customer devices. In Australia, this has been adapted as CSIP-AUS

FCAS Frequency Control Ancillary Services

ICE Internal combustion engine

ISO International Standards Organisation

ISO 15118

An international set of standards defining EV-EVSE communications

MCS Megawatt Charging Standard (a CCS derivative)

NEM National Electricity Market (consisting of 5 jurisdictional markets: QLD, NSW, VIC, TAS, SA)

NER National Electricity Rules

OBC On-board charger. In the context of this report, it can infer a bidirectional combined inverter-charger, though is still referred throughout as an ‘OBC’.

OCPP Open Charge Point Protocol

PKI Public Key Infrastructure

SoC EV battery state of charge (% of rated capacity)

ToU Time-of-use (tariffs)

V2G Vehicle-to-Grid (a form of bidirectional EV charging)

V2H/B

V2L

V2X

Vehicle-to-Home or Vehicle-to-Building (a form of bidirectional EV charging)

Vehicle-to-Load (a form of bidirectional EV charging)

Vehicle-to-Everything (covering all forms of bidirectional EV charging)

VGI Vehicle-grid integration

VGIC Vehicle Grid Integration Council (US)

1. Background

1.1. Purpose of this paper

On 19 July 2024, the Energy and Climate Change Ministerial Council agreed the Australian Renewable Energy Agency (ARENA) would lead the development of a national strategy for bidirectional electric vehicle (EV) charging.1 This reflects a recognition by all Australian governments that bidirectional EV charging can be an important enabler in our transition to a lower cost and low emissions power system.

ARENA has partnered with the RACE for 2030 Cooperative Research Centre (RACE) who have jointly commissioned enX Consulting to facilitate the development of a roadmap of activities to form the basis for a national strategy (National Roadmap for Bidirectional EV Charging).

This background paper is an output from the process. It focuses on defining and validating the most prospective applications of bidirectional EV charging within the Australian context and identifying potential directions for national strategy development based on:

1. A desktop review of the current directions for bidirectional charging in key markets

2. Supply chain and stakeholder engagement (through interviews and an in-person codesign workshop) to identify critical paths, enablers and barriers

3. Long-run energy market modelling to determine the potential value of bidirectional charging in Australia’s energy transition

4. A national industry codesign workshop held in Canberra in 12-13 November 2024.

1.2. The Market Objective

The following Market Objective has been defined for this project and is the focus for much of the analysis in this paper:

Market Objective: Bidirectional charging is readily available to provide high value services across the Australian economy by 2030, with several products available by 2027.

The objective of the roadmap process is to identify the actions that government and industry can implement to achieve the Market Objective

1.3. Smart and bidirectional charging

Australia is in the early stages of a broad-scale transition to electric mobility (e-mobility) across all road transport sectors. This transition is driven both by comparative technology advantages and the urgent need to reduce greenhouse gas emissions . Our e-mobility transition presents a long-term structural change for Australia’s energy systems.

1 DCCEEW (2024) Energy Ministers agree to the National Consumer Energy Resources (CER) Roadmap | energy.gov.au

An important dimension to this transition is an increasing coupling of the transport sector with our systems of electricity supply. The Australian Energy Market Operator (AEMO) forecasts annual electricity consumption to double from 2024 to 2050, with most of this associated with vehicle electrification.2 AEMO also notes that future electricity customers may be more flexible in the timing of their electricity demand, shifting electricity usage, such as EV charging to take advantage of lower costs and when electricity supply is in surplus.

Bidirectional EV charging

Smart charging is an evolving suite of technologies and strategies which, in established use, can shift EV charging or discharging to opportune times such as periods of low power prices, low grid demand and/or renewable energy abundance. Smart charging requires digital technologies to manage charging sessions and digital coupling with vehicle communications, ‘off-board’ energy management systems and systems used by electricity grid operators to ensure the reliability, security and efficient operation of our power systems. This is underpinned by digital communications infrastructure and interoperability standards and protocols that facilitate the transfer of information, and computational resources within and outside vehicles.

Bidirectional charging allows not only for EV electricity loads to be shifted in time, but also for EVs to act as a generator that produces power for a home or building and/or, to support the grid. Over the coming decades, bidirectional charging is widely expected by stakeholders to become an increasingly available high-value service that can generate benefits for the EV owner as well as the power system and the economy more broadly. It takes advantage of the fact that the capacity of EV batteries will be surplus to most drivers’ needs, most of the time.

Bidirectional EV charging has been developing as a concept since the late 1990’s with around 150 trials conducted internationally to demonstrate its technical and commercial potential.3

Types of bidirectional charging include:

• Vehicle to grid (V2G) - EVs supply power to a mains electrical circuit that is electrically connected to the grid. In this configuration, the bidirectional charging system synchronises with the power system’s AC frequency V2G allows for power to be exported to the grid for a variety of purposes (including energy and services market participation) but can also include export-limited applications such as solar selfconsumption or peak demand mitigation.4

• Vehicle to homes and buildings (V2H/B) – EVs supply power to local electrical distribution that is electrically separated from the grid. In this configuration, the vehicle and off-board charging equipment are grid-forming (i.e. creates its own 50hz AC frequency).

• Vehicle to load (V2L) – EVs supply power directly to one or more electrical appliances that are electrically separated from the grid In this configuration, the vehicle and offboard charging equipment do not need to synchronise with the frequency of the grid

2 AEMO (2024) Integrated System Plan (p.26)

3 See for example V2G hub for a summary of key projects

4 Export-limited V2G is sometimes referred to as V2H, but this definition is not generally accepted by industry.

While these definitions make it easy to discriminate bidirectional charging systems as electrical configurations, innovations in end-use applications can blur these boundaries. For example: V2H capability can also be used to provide peak demand reduction services by switching load temporarily to an offline power supply. V2G can be export-limited e.g., configured such that electricity stored in an EV is only intended for consumption by a customer’s premises.

Bidirectional charging implementations are separated into alternating current (AC) and direct current (DC) configurations:

• AC – DC energy in the battery is converted to AC within the vehicle by an on-board charger (i.e., bidirectional OBC having inverter capability). The EV discharges AC power.

• DC – The EV discharges DC power which is converted outside of the vehicle by an offboard inverter (like a battery inverter).

A high-level taxonomy of bidirectional EV charging configurations is provided in Figure 1 Potential bidi use cases are explored further in the next chapter.

Figure 1 – High-level taxonomy of bidirectional EV charging applications

Grid isolated

Grid synchronised

Off-board power conversion DC V2H/B DC V2G

On-board power conversion

AC V2H/B & V2L AC V2G

This paper focusses on V2H/B & V2G applications rather than V2L which is considered commercially mature and not requiring specific government or stakeholder actions. However, V2L is explored in several cases where the boundary between V2L and V2H/B becomes blurred, such as when V2L is temporarily reticulated through an isolated building circuit.

Grid

code compliance

V2G is subject to the same grid code requirements that apply to all inverter-based generating systems. In Australia, these requirements are set out in the recently updated AS/NZ 4777.1:2024 (installation requirements) and AS/NZ 4777.2:2020 (inverter equipment requirements).

One advantage of DC bidirectional charging is that grid code compliance can be achieved via an off-board power converter as opposed to within the vehicle’s OBC. This means vehicles may cost less to design and build and they can be bidirectional in a range of different markets largely irrespective of local grid code requirements. From a grid code compliance perspective, DC bidirectional charging is considered to have a potentially faster path to market, especially in secondary markets such as Australia that do not have a native automotive industry.

Proposed changes to EU grid connection codes may alter this dynamic by requiring fuller grid code compliance for unidirectional charging 5 This increases the production costs of AC unidirectional power conversion equipment, whether on-board or off-board, and therefore

5 These changes to the EU Demand Connection Code have been reported by supply chain stakeholders, rather than assessed directly by enX.

reduces the incremental grid code compliance costs for V2G It is also possible that vehicle OEMs may take the opportunity presented by unidirectional OBC redesign to introduce AC V2G capabilities. Conversely, this may provide an incentive for some automakers to remove OBCs in some applications and rely instead on offboard DC chargers for uni & bidirectional grid code compliance.

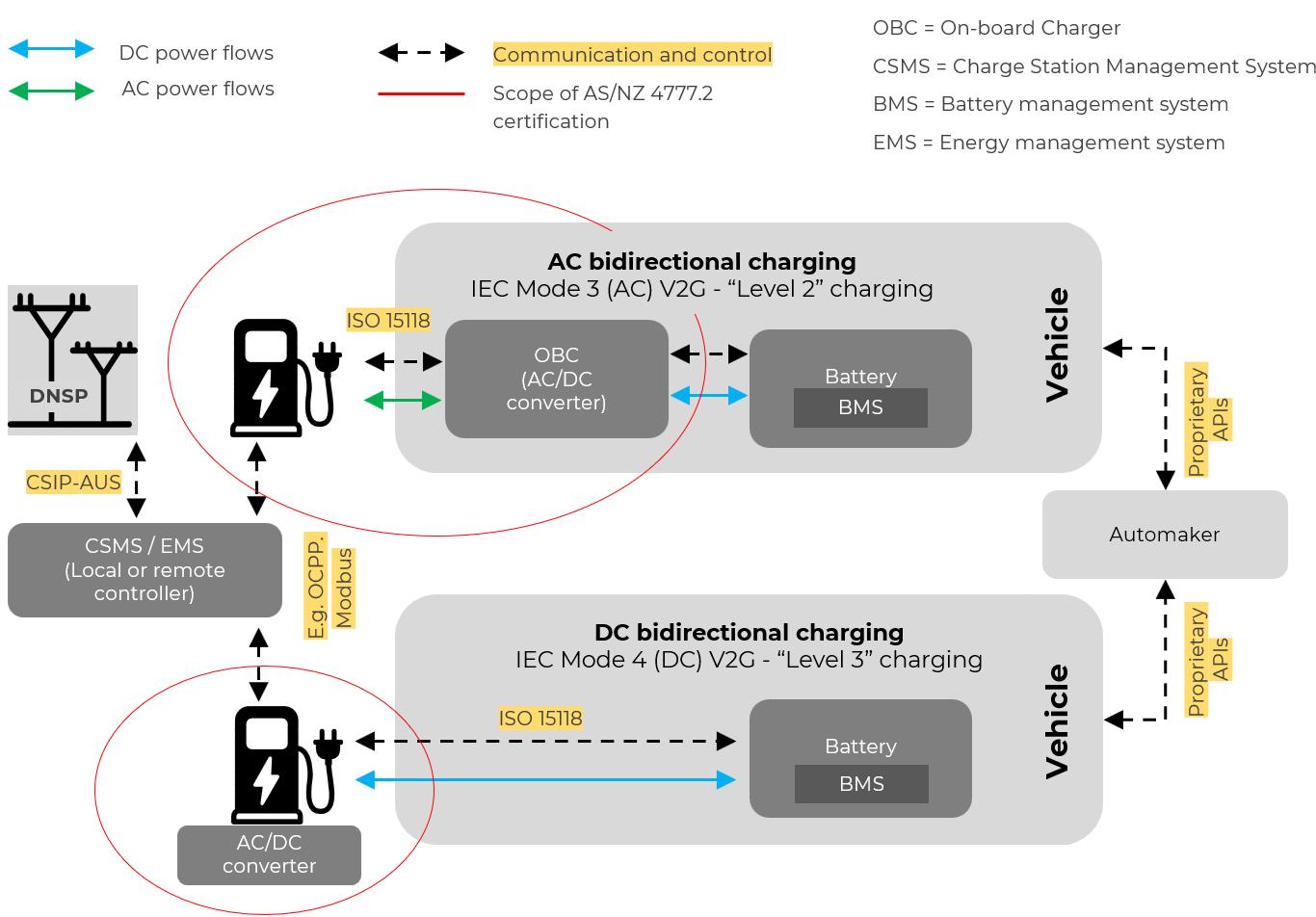

Overall, stakeholders consider that the recent updates to AS/NZ 4777.2:2020 provide a clear (but untested) pathway for grid code certification for both AC and DC bidirectional charging solutions. While for AC, both the charger and the vehicle will need to be certified as a pair, for DC, only the charger will need to be certified. This is illustrated in Figure 2

Figure 2 – Diagram illustrating AC vs DC bidi configurations and the applicability of relevant standards

Summary of relevant standards

Table 1 (below) provides a summary of relevant technical standards and their current status. Implications for these standards and their impact on the Market Objective are explored further in chapter 2.3 Critical path assessment for standards readiness

Table 1 – Summary of relevant technical standards appliable to bidirectional charging

CCS The Combined Charging System (CCS) is the standards framework for charging connectors and EV<>EVSE communications. CCS and its derivative Megawatt Charging System (MCS) is the apparent market direction in Australia. CHAdeMO is a functioning alternative but represents a shrinking market share.

ISO 15118 ISO 15118 is the communication standards for EV-EVSE interoperability. ISO 15118-20 is required for interoperable CCS-based V2G. Whilst production-ready for DC bidi, significant revisions are underway to standardise AC bidi. Early bidi products may be based on custom extensions to the older ISO 15118-2 standard.

OCPP The Open Charge Point Protocol (OCPP) is the communication standard for remote operation of EVSE. Version 2.1 is required for standardised V2G interoperability. Version 2.1 will be backwards-compatible with 2.0.1 (collectively ‘2x’), but not with 1.6 which is used widely today. OCCP 2x is still at an early stage of adoption.

CSIP-AUS Australia is adopting CSIP-AUS, based on IEEE 2030.5, as the national profile for communicating dynamic operating envelopes from distribution network businesses to customer premises. These will typically be received by a proxy or site gateway device with local communication to the EVSE via OCPP or Modbus. IEEE 2030.5 is not widely used outside of Australia and supply chain participants are generally unaware or unclear on how this will impact product development.

AS/NZ 4777.2

AS/NZ 4777.2 is Australia’s product standard for grid connected inverter-based generating systems. Recent updates to AS/NZ 4777.2:2020 provide a clear (yet untested) pathway to EV and EVSE grid code certification. Several DC EVSE OEMs are currently progressing down this path. No network connection delays are expected for equipment listed on the Clean Energy Council’s approved product list.

AS/NZ 4777.1:2024 supply type definitions

Australia’s new national installation standard for inverter energy systems (AS/NZ 4777.1:2024) has introduced ‘supply type definitions’ which apply to bidirectional charging:

1. Normal supply – the default power supply source at a premises, such as from the main grid or the primary generator in an off-grid context (i.e. no bidirectional charging)

2. Supplementary supply – bidirectional charging is coupling with and operating alongside supply from the grid (i.e. V2G) and cannot operate independently

3. Alternative supply – Bidirectional charging offers a backup power source, such as during grid outages (i.e. V2G with back-up power capability or V2H/B)

4. Independent supply – Bidirectional charging provides a ‘stand-alone’ power supply (not grid coupled), but charging can occur from the grid

5. Substitute supply – A relatively niche application where bidirectional charging provides an AC power via the inlet of a secondary inverter-based back-up generator (i.e. V2H/B)

1.4. Transport sector context definitions

Bidirectional EV charging is relevant in different transport sector contexts. The following transport context definitions are used in this report:

• Residential – Vehicles used for private purposes, typically charged at a standalone residential dwelling, extending to more multi-occupancy dwellings in the future

• Commercial – Vehicles used for business purposes, typically charged at a commercial building or depot and sometimes at an employee premises

• Rental fleets – Vehicles are owned by a rental car or car-sharing company, typically charged at a public or destination charging location

• Public charging – Any vehicle while using a public charging station

• Heavy vehicles – Principally trucks and buses typically charged at a depot or a specialised public charging station

1.5. Protecting the power system while electrifying transport

A previous report on EV Technical Standards for Grid Operation for AEMO identified a range of grid-management risks associated with high penetrations of EVs. The highest rated risks included:

• Diversity destruction - Price responsive EV chargers switch on/off or change charge direction simultaneously in aggregate, and the power system experiences an extreme Rate of Change of Frequency (RoCoF) and/or frequency excursion

• Cyber Security – CPO, OEM or Aggregator IT infrastructure is compromised, and the power system experiences a very large load step, leading to insecure power system operation and potential widespread power loss

• Software management – A flawed EV charger software patch is deployed, resulting in an error that causes very large load step down and the activation of protection systems

• Communications loss – The loss of communications for EVSE in a region means smart charging reverts to offline control mode(s) resulting in a large load step up. 6

In this report, enX recommended a range of measures which encapsulate the broader power system risks associated with bidirectional EV charging and the report’s recommendations provide a potential template for future action. This paper therefore focusses on items that are additional to the scope of that report

1.6. State of the market summary

Many (potentially all) EV automakers are currently in the process of developing and trialling bidirectional charging products. Over the past 24 months, stakeholders have reported a shift in focus from technology demonstrations to preparing early-stage mass-market products. Overall, the fundamental technical capabilities and potential use cases for bidirectional charging are considered by supply chain participants to be well demonstrated and/or understood.

6 enX (2023) EV Technical Standards for Grid Operation

The central challenges for automakers are:

• Productisation – developing bidirectional EV charging capabilities into marketable services for consumers, including building trusted supply chain partnerships and establishing battery usage and warranty conditions, and

• Homologation – getting core technologies ready for, and tested against, regulatory requirements in key end markets.

Much of this work is happening by industry, without direct visibility by government and consumers. This fuels an impression of bidirectional EV charging as being in a perpetual nascent state – something that has bene on the cards for years but is yet to be committed to in a substantive way. This perception has been accompanied by wide-ranging speculation about if, and when these products will become available and in what form they will take.

Based on semi-structured interviews with over 50 local and international stakeholders and supply chain participants, including seven automakers, upstream supply chain participants overwhelmingly consider the Market Objective is achievable and desirable. On balance, it was seen as neither over nor under ambitious but contingent on national-level policy support

Outside of supply chains, some stakeholder scepticism has been fed by a legacy of unrealised hype and several false starts. For context, the concept of bidirectional EV charging (as V2G) first originated in the 1990’s7 followed by the first experiments 2001.8 The Nissan ‘LEAF-to-Home’ power supply system was released in 2012 and all Nissan LEAFs since the model year 2013 have been delivered with bidirectional charging capability. However, until 2023, Nissan and Mitsubishi had the only passenger vehicle marketed with bidirectional charging capability outside of trials or closed commercial partnerships.9 This is starting to change.

Nissan and Mitsubishi bidirectional charging capability have used the CHAdeMO charging standard which is being phased out in markets such as the US, EU and Australia. The CHAdeMO standard brought V2G initially to Japan in 2012 as a government-directed imperative following the Tohoku Earthquake (2011), which led to a proliferation of compliant EV and EVSE products which, 12 years later, allow CHAdeMO to be considered mature with respect to being a standard supporting V2G.

The Combined Charging System (CCS) was launched in 2012 by a consortium of EU and US automakers and adopted ISO 15118 for high-level communications after finalisation of the firstgeneration ISO 15118-2 standard in 2014.10

ISO 15118-2 does not explicitly support V2G (ISO 15118-20 does) however depending how the standard is implemented and leveraged some V2G capability has been demonstrated successfully. Compared to CHAdeMO, market pressures did not historically require CCS to support V2G. CCS is now however considerably more feature-rich and flexible than CHAdeMO and accordingly represents the bulk of market adoption in whole or part via regulation or

7 The origins of V2G is generally attributed to Kempton & Letendre (1997) Electric vehicles as a new power source for electric utilities

8 IEEE (2023) False Starts: The Story of Vehicle-to-Grid Power

9 Appendix A provides a summary of major bidirectional charging trials to date.

10 It originally adopted the precedent DIN 70121 standard, which supports unidirectional charging only.

market-led directions. Accordingly, V2G uptake is entering a ‘second wave’ under CCS standards, as the standard is finalised, supported and grown.

Similarly, industry is still in the early stages of transitioning to the 2022 version of the Open Charge Point Protocol (OCPP) 2.0.1 which standardises communication between the EVSE and Charging System Management Software (CSMS). OCPP operates independently of CCS, CHAdeMO or other charging systems. It is the de-facto global standard for EVSE management.11 The transition to 2.0.1 is hampered by reliance of older versions (1.6), legacy systems and infrastructure.

A further version (OCPP 2.1) has been developed in part to standardise bidirectional charging communication and was released in draft form for public review in August 2024 It is expected to be published around the end of 2024.

CharIN, a global association promoting the CCS framework, published a bidirectional charging roadmap in 2019 which identified 2025 as the global ‘go live’ year for V2H & V2G.12 It is logical that in 2024, that we should see a quickening of standards publications and industry preparations for the release of mass-market bidirectional charging products. In 2025 and 2026 we expect mainstream bidirectional charging offering start to enter the mix of product features available to consumers in the US and EU. This will feed into broader competitive auto industry market dynamics which may drive a further proliferation of market offerings in subsequent years.

11 On October 20th, the IEC published the approval of OCPP 2.0.1 as an IEC International Standard (IEC 63584). See OCA (2024) OCPP Achieves International Standard Status

12 Electric (2019) CharIN: Bidirectional CCS charging by 2025

2. Technology and commercial readiness

2.1. Critical path assessment for EV and EVSE supply

This chapter explores the technology and commercial maturity of different elements of bidirectional charging solutions and identifies the risks they present to achieving the Market Objective. It identifies vehicle availability as the critical barrier to market development and ISO 15118-20 as an enabler (and barrier) to plug & play interoperability between vehicles and chargers. It describes the different challenges associated with AC & DC bidi applications and the potential to support OEMS homologating products in our market. All the major challenges are commercial in nature or related to software interoperability.

The impact of EV and EVSE availability on the Market Objective is summarised in Table 2 and discussed in the remainer of this section 2.1

Table 2 – The impact on equipment availability on the Market Objective

Constraint Description Risk

Bidirectional EV availability

Bidirectional EVSE availability

EV readiness

While there is strong potential for a competitive field (e.g. greater than 10 models) of bidirectional EVs in Australia by 2030, this is not assured. Australia is likely to lag overseas markets until such time as we offer a competitive policy & market proposition encompassing standards maturity and incentives for adoption.

Automakers will need compatible EVSE available in each market, presenting a ‘chicken and egg’ dilemma. Importantly, the initial high pricing of DC EVSE is seen as a barrier to productisation by both EV and EVSE OEMs. This suggests that product/installation rebates, and support for product homologation, could be effective in catalysing additional market offerings of both EVs and EVSEs.

Internationally, we have identified 33 models (excluding model variants) that have ‘current’, ‘announced’ or ‘demonstrated’ bidirectional charging capability. These models are listed in Appendix B (p.71) and summarised by OEM & vehicle platform in Table 3

Of these models, only the Nissan LEAF, Ford F-150 Lightning, Tesla Cybertruck and Mitsubishi Outlander and three GM vehicles currently have capability in production. Renault is currently launching bidirectional charging for the Renault 5 E-Tech Electric in France13 The Ford F-150 Lightning is the only CCS-based vehicle to openly support bidirectional charging in Australia, but its initial custom-import release pricing (>$160,000) puts it out of reach for most Australians.

Nissan has announced CCS-based bidirectional charging from 2026. It says, “Under the banner of Nissan Energy, the company’s aim is to roll-out V2G technology in the UK first, followed by

13 Sibley (2024) Major car makers are rolling out V2G plans this year. Is Australia ready?

other markets in Europe, empowering consumers with either AC or DC-based V2G solutions, in alignment with local infrastructure and regulatory requirements” 14

Table 3 – Vehicles with current, announced or demonstrated bidirectional charging capabilities

Overall, we can say that the vast majority of EVs already sold in the Australian market have the hardware capability to support DC bidirectional charging, but this is yet to be approved, enabled or productised for local mass-market adoption

EVSE readiness

EVSE manufacturing for bidirectional charging combines a range of conventional technologies found in unidirectional charging, and bidirectional power converters such as those used in battery energy storage systems (BESS).

While stakeholders identified no critical hardware challenges to supplying either AC or DC bidirectional EVSE, significant challenges do exist with software development and integration testing required to achieve ‘plug & play’ interoperability between different EV and EVSE models. Many EVSE OEMs are developing, or have developed, the capability to be interoperable, however they are largely waiting for matching EV product offerings. A few significant EV-EVSE integrations are underway but these are typically obscured by commercial confidentiality.

14 Nissan (2024) Nissan to launch affordable vehicle-to-grid technology in 2026

EVSE OEMs (like automakers) are generally prioritising home markets and additional certification, and testing is required to homologate products for alternative markets such as Australia. These issues are explored further below but overall, the timely supply of product to Australia will be most influenced by four factors:

1. Government policy and incentives

2. Australia’s addressable market size including the customer value proposition

3. The accessibility, stability and efficiency of standards and regulatory approval frameworks

4. The availability of capable vehicles (greater numbers will reinforces both EV and EVSE proliferation).

Internationally we have identified over 21 EVSE OEMs offering or developing 26 CCS2 bidirectional EVSEs. These are predominantly designed for DC charging and so include a power inverter (one salient exception to this is the Mobilize Powerbox which supports 3-phase AC bidirectional power transfers up to 22 kW). While four of the 26 charging stations (all public chargers) also have a CHAdeMO connector, among the stakeholders canvassed, this option is not offered on any residential/destination charger (though they are known to exist in CHAdeMO’s Japanese home market)

Automakers and CER installers consider the high cost of DC bidirectional EVSE will present a barrier to mainstream uptake in the near-term as markets for these products do not yet support scale production. While residential DC EVSE products may currently (where available) cost in the order of A$8,000 to A$12,000 initially (installed), the consensus among stakeholders was that this could drop to below A$5,000 by 2030 reflecting a target Bill of Materials (BoM) cost of approximately USD$500-550 The cost is less if you consider the A$1500 to A$2500 cost of installing a unidirectional wallbox charger as the baseline (the cost of bidirectional charging can be considered an incremental increase).

In addition to creating opportunities to consolidate revenue, the relatively high installed cost of DC EVSE is understood to be part of the reason why Renault and Nissan are planning mainstream products based on AC V2G configurations. One of the key advantages of AC bidirectional charging is the ability to leverage vehicle scale-production to drive down unit costs. Installation costs and complexity are also reduced to achieve those similar to a conventional AC wallbox. It is stressed that some unique technical challenges exist in developing suitable, scale-production of bidirectional OBC. For example, volumetric and thermal performance enveloped are more stringent than for outboard power conversion and product life is expected to be consistent with engineered vehicle life (e.g., 20 years). Whilst these challenges exceed those of typical DC V2G solutions, it is noted that vehicle OEMs may leverage cost savings in other vehicle systems to present consumers with a net marginal cost that is more favourable than for DC V2G.

There is also a strong engineering design case for combining power conversion from solar, stational batteries and DC charging in a single unit and this would greatly reduce the marginal cost of bidirectional charging for many customers. This may be most relevant to ‘greenfield’ installations or for customers looking to replace existing inverter technologies at their premises. DC bidirectional charging can be more efficient when recharging from a local DC power source such as solar PV. This can reduce power conversion losses by 20% or more as the

electricity does not need to be converted to AC then back to DC again before it reached the vehicle’s battery.

While several EVSE OEMs and adjacent industry participants are developing integrated home energy management system (HEMS) solutions, the extent of integration and feature offerings are not yet clear in most cases.

2.2. Critical path assessment for power transfer limitations

The potential impact of bidirectional power transfer constraints on achieving the Market Objective are summarised in Table 4 Overall, we consider bidirectional charging constraints to have a moderate impact on the Market Objectives for both 2027 and 2030. Issues are discussed in the remainder of this section 2.2

Table 4 – The potential risk of bidirectional charging constraints on the Market Objective

Constraint Description Risk

BMS BMS are generally considered permissive to DC bidirectional charge operation as they are designed to facilitate large power transfers during driving.

OBC physical constraints

Warranty restrictions

While OBC AC output capacity ranges for V2L vary widely, AC V2H and V2G products are likely to support most consumer use cases.

Automakers will impose EV battery warranty conditions in the context of competitive market dynamics and product technology limitations. This may constitute a risk to consumers where they threaten consumer return on investment. Once we have multiple EV offerings in our market, competition pressures can support warranty conditions becoming more permissive

Low load limits OBC and off-board power conversion equipment can have minimum load requirements that can impact specific use-cases such as V2H and back-up power applications, and low power conversion efficiencies in low-load applications. These will vary in different technology configurations with some OBC efficiencies dropping below 75% (unidirectional) at under 1 kW load15

EV battery bidirectional power transfer potential

The operation of EV batteries is inherently bidirectional, discharging power to drive the vehicle’s motor(s) and importing power from the grid to recharge Peak DC discharge power transfer capability varies widely depending on the nature of power delivery (whether instantaneous or constant) and a variety of internal and external factors (e.g., thermal considerations) – from 71 kW (Hyundai Inster) to 760 kW for a Tesla Model X Plaid or Porche Taycan Turbo GT.16 While these levels can be achieved only for short durations (such as during rapid acceleration) they demonstrate that the DC power transfer capabilities of EV batteries are well in excess of all potential residential, and many commercial applications. While planned residential bidirectional EVSE are typically rated to around 11 or 22 kW, commercial and public charging bidirectional EVSE can be rated more than 100 kW.17

15 Sevradi et al (2003) Experimental validation of onboard electric vehicle chargers to improve the efficiency of smart charging operation

16 These are self-reported ratings as published at ev-database.org

17 E.g., Borg Warner’s RES-DCVC125-480-V2G, or Nuvve’s RES-HD125-V2G

The Battery Management System (BMS) in an EV ensures the battery operates safely, efficiently, and reliably. It provides real-time dynamic constraints to ensure that bidirectional charge operation stays within the battery’s operating specifications. In any bidirectional charging session, the BMS will provide dynamic limits that override any external requests via the EVSE or vehicle telematics.

AC bidirectional power transfer capabilities are primarily limited by the power rating of OBCs. Each of the vehicle brands that have announced AC bidirectional charging capability (Renault, Kia, Volvo & Polestar) have limited AC exports to 11kW. To put this in context, a single-phase residential customer in Australia typically draws in the range of 1 – 10 kW and has a 23 kW grid connection limit. Current V2L AC output range from 2.2 kW (e.g., for the MG 4), to 11 kW (e.g., for the Volvo EX90). Given the technical requirements of bidirectional power transfer need to be packaged within the vehicle, in most passenger vehicles higher power bidirectional solutions necessitate greater cost, volume and thermal payload (however in some cases – e.g., heavy vehicles – these issues can be small relative to total vehicle costs).

Battery health management

Stakeholders had a diversity of view on how battery health considerations would impact bidirectional charging uptake and operation. It was universally viewed that customers would need to be assured about battery degradation. It was noted that customers are likely to draw on their experience of mobile phones (rather than stationary batteries) and their knowledge that there is a direct utility impact from reduced battery health. Customer concerns about driving range and potential battery replacement costs are likely to be amplified by any perceptions that bidirectional charging will contribute to battery degradation.

Various strategies are being pursued to address battery health impacts of bidirectional charging:

• Managed charging – There is a growing body of evidence that bidirectional charging can be managed to diminish its impact on battery health, and it can improve it in some instances.18 Overall, in most cases bidirectional charging is likely to have a lesser impact than other consumer driving and charging behaviours.

• Better batteries – Continuing advances in battery chemistry, cell design and thermal management systems are greatly extending vehicle range and battery lifetimes For example, CATL claims its new EV battery can last 1.5 million km 19 Such innovations will enable more permissive battery warranty conditions and assuage customer concerns It is important to note that most studies to date have been based older EV energy storage systems, and compared to modern products, they will generally overstate the problem

• Warranty restrictions – There were different views as to how vehicle warranty conditions may restrict the use of vehicle batteries. While Nissan has generally had no special restrictions on V2G use, Volkswagen has outlined initial warranty conditions for

18 E.g., Wong et al (2024) Quantifying the impact of V2X operation on electric vehicle battery degradation: An experimental evaluation, Loiselle-Lapointe (2023) Effects of Bi-directional Charging on the Battery Energy Capacity and Range of a 2018 Model Year Battery Electric Vehicle

19 Electrek (2024) CATL launches ultra-high-energy-density EV bus battery that lasts nearly 1 million miles,

its V2G offering of 2 MWh and 800 hours of discharge per year.20 Stakeholders had mixed views around whether such terms can be considered a material barrier to consumer value realisation.

• Battery replacement – Automakers are exploring ways to make EV batteries easier and cheaper to replace at the end of their life

• Making it appealing – A central strategy to overcoming consumer concerns about battery degradation is to make bidirectional charging worth their while. Further discussion on consumer attitudes to this issue is discussed in the section Consumer appetite and readiness from p.41

While battery health concerns were not considered a hard barrier to bidirectional charging being productised in Australia, there was a sense that the above strategies would need to be more fully realised for bidirectional charging to achieve mainstream acceptance In a worstcase scenario, this may be a multi-decadal process to fully resolve.

Heavy vehicles

The Megawatt Charging System (MCS) is derivative of CCS. It is DC-only and natively supports bidi up to 3.75 MW DC for heavy road, rail and vehicles and water vessels. MCS underwent initial testing in 2020 with a v1.0 specification whitepaper released in 2022. MCS’ bidirectional capabilities are expected to have vehicles in this class contribute readily to ancillary services markets given that power magnitudes from individual vehicles can exceed frequency market bidding increments (e.g. 1 MW in Australia).

20 Sibley (2024) Major car makers are rolling out V2G plans this year. Is Australia ready?

2.3. Critical path assessment for standards readiness

The potential impact of standards readiness on achieving the Market Objective are summarised in Table 5 below. Overall, stakeholders considered standards-related issues to have a moderate impact on the Market Objective for 2030. This is primarily associated with the lack of clarity over our market direction for smart grid integration and minimum standards for behind-the-meter interoperability. These issues are discussed in this section and summarised in Table 5

Table 5 – The potential risk of standards maturity on the Market Objective

Standard Description

AS/NZ 4777.2: 2020 There is a clear (albeit untested) path for EV and EVSE OEMs to get certified to a national grid code. AC bidi EV-EVSE certification faces the most uncertain path.

ISO 15118 Incomplete development of support for AC bidirectional charging means that these products are likely to be highly bespoke initially. DC bidi has the fastest path to market although early products may be based on custom 15118-2 integrations.

OCPP Limited industry adoption of OCPP 2.x to date means that other protocols (including earlier OCPP adaptations) may be relied on for remote communications.

CSIP-AUS CSIP-AUS integration, as a critical requirement in the medium term, will be a new consideration for most EV and EVSE OEMS supplying our market. This may require additional development work, commercial partnerships but overall, towards a positive end. OEMs may opt for static export limits in the near-term reducing customer value from V2G. Some work is required to understand best ways to integrate EV charging with dynamic operating envelop (CSIP-AUS) intent in functionally consistent, lowest-cost ways.

Behind-themeter

interoperability

Risk

The lack of minimum standards for interoperability between EVSE, solar and battery inverters and other customer devices is likely to add significantly to customer costs and risks, especially in light of CSIP-AUS requirements that multiple generating devices be orchestrated to achieve export limits at a site-level.

AS/NZ 4777.2:2020

Updates to AS/NZ 4777.2:2020 are considered to provide a clear but untested pathway to grid connection for AC and DC bidirectional charging technologies. Most DNSPs surveyed for this project (covering >90% of the Australian population) indicated they will be ready to connect a bidirectional EV charging system within 3 months (i.e., ahead of any products being certified) and that they intended to rely on the Clean Energy Council Approved Inverter21 listing process unless that presented a barrier to deployment.

The Clean Energy Council (CEC) has advised that bidirectional EVSE will be categorised similarly to stationary battery inverters. Applicants will submit applications via the CEC's normal product listing process. CEC listing for bi-directional EVSE requires AS/NZS 4777-2:2020 (with amendments) and IEC 62477-1. If the device includes PV ports, additional standards such

21 CEC Approved Inverter List

as IEC 62109-1 and IEC 62109-2 will apply. The CEC is currently in the process of making changes to relevant documents and form fields.

Local and international stakeholders considered the use of a single national grid code and certified product listing process as critically important given Australia’s relatively small market size. Local stakeholders also noted the critical importance of timely and efficient CEC listing processes.

Standards compliance concerns

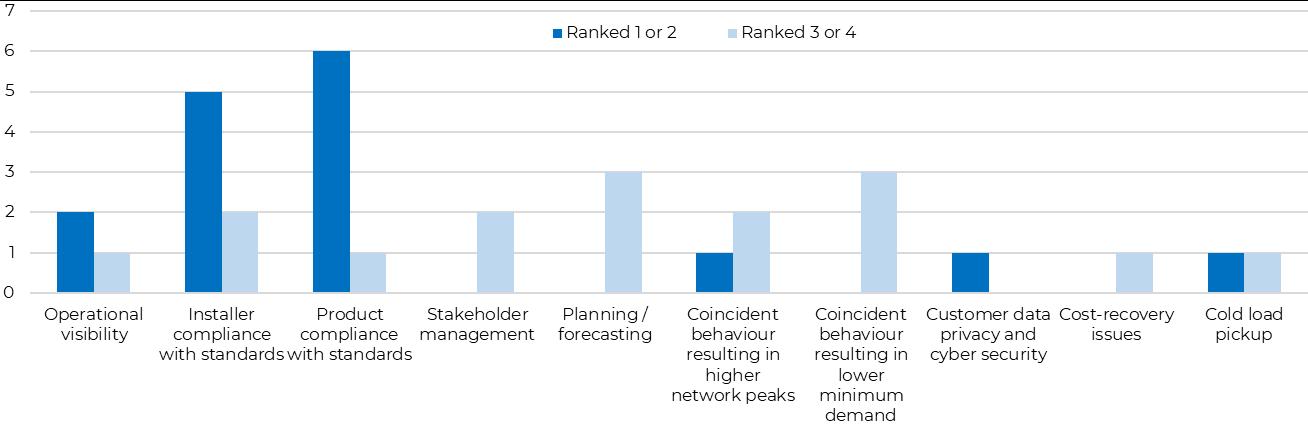

As shown in Figure 4, DNSPs overwhelmingly ranked standards compliance as their greatest concern with bidirectional charging on their networks. This related to AS/NZ 4777.2:2020 (product standard), followed closely by AS/NZ 4777.1:2024 (installation standard). Consumer Energy Resource (CER) standards compliance and enforcement has been a key issue in recent years and bidirectional charging is expected to suffer the same challenges as current technical regulatory frameworks. The Energy Ministers’ CER Roadmap has committed to addressing this 22

Figure 3 – DNSP timeframes and certification process for bidirectional EV charging systems

Figure 4 – DNSP concerns with bidirectional EV charging

ISO 15118-20

ISO 15118 defines high-level communications between a vehicle and an EV charger in a CCS or MCS charging session. The second generation of the standard, ISO-15118-20:2022 (-20) explicitly supports interoperable bidirectional charging communication in addition to many features applicable to advanced smart charging (e.g. communicating SoC information in an AC charging session). Industry stakeholders almost universally supported ISO 15118-20 as an ultimate direction, with some legacy interest in (the US-indigenous) SAE J3068.

The ISO 15118 communications specifications (-2 and -20) can work in parallel. On initiating a charging session both EV and EVSE share which standards and versions they can communicate in order of priority, and the session is initiated at the highest mutually intelligible protocol. Many contemporary CCS bidirectional charging product development processes were initiated prior to -20 being finalised and are based on custom extensions to the older version (ISO 15118-2). This has led to proprietary EV and EVSE integrations (albeit based on open standards) that are effectively not interoperable with other OEM’s products. By consequence, early products to market will involve tight commercial and technical integration between EV and EVSE products.

The following are examples of exclusive EV <> ESVE pairing arrangements that have implemented internationally:

• BMW (Germany) <> Kostal

• Volkswagen (Germany) <> E3DC

• Renault (EU & UK) <> Mobilise

• Nissan (US) <> Fermata

• Ford (US) <> Sunrun

• GM (US) <> GM

ISO 15118-20 is not backward compatible with -2 due to different messaging structures and cybersecurity features As with the shift from CHAdeMO to CCS, the transition from -2 to -20 versions of ISO 15118 involves considerable ‘technology debt’ Moving to -20 can also require hardware upgrades due to higher computation resources associated with data encryption. 15118-20 requires Transport Layer Security (1.3) for all data, ensuring robust cybersecurity

Stakeholders had different understandings of the completeness of ISO 15118-20 and its readiness to support ‘plug & play’ interoperability. In was generally considered that while -20 can support interoperable DC bidirectional charging, it may be several years before all AC usecases are fully standardised. Various international initiatives are underway to resolve outstanding issues within the standard (e.g., in revisions led by ISO) and with its adoption in local regulatory contexts (e.g., by IEA Task 53). MCS (a CSS derivative) is based on ISO 15118-20 and is considered natively bidirectional.

ISO 15118-21 establishes conformance testing against -20 and has so far only been published in draft form.23 Stakeholders indicated that formal conformance testing would be an important requirement for EV and EVSE in the future, underpinning plug & play interoperability between

23 ISO (2024) ISO/DIS 15118-21 - Common 2nd generation network layer and application layer requirements conformance test plan

products and OEMs, and that this should not impede continued innovation and productisation of -20 based products

The Open Charge Point Protocol (OCPP)

Open Charge Point Protocol (OCPP) is a communication framework for EV charging infrastructure and relevant management systems. It is maintained by the non-profit Open Charge Alliance (OCA) and enables interoperability between charging stations and Charge Station Management Systems (CSMSs) from different vendors While designed originally for remote communication, it can also operate locally or work alongside local IoT protocols intended for high-speed local communication (e.g. Modbus, Zigbee, EEBus, MQTT, Thread, Matter etc.)

As is possible with a software framework, OCPP has been customised in a range of projects (e.g., to manage measurement and verification data flows for primary frequency response ancillary service delivery using EVs) or to test pre-production features (e.g., for bidi trials). OCPP has been adopted as a de-facto standard globally and is a requirement in many markets.

Markets globally are currently transitioning from OCPP 1.6 (published initially in 2015) to OCPP 2.0.1 (published initially in 2020), with formal test tools and certification processes released this year). 2.0.1 is not backwards compatible but allows for richer communications and a wider range of applications. OCPP 2.1 - an incremental and backwards-compatible development on 2.0.1 - is still being finalised and is the first version to formally support bidirectional as formal feature.

While stakeholders overwhelmingly considered OCPP 2.x as a cornerstone for remote bidirectional charge management, remote management is not essential in all charging scenarios. As discussed in the next section, Australia’s emerging smart grid architecture implies that customers with multiple generation devices will require some level of local orchestration meaning that local communication protocols may be more relevant in many cases.

CSIP-AUS

The Common Smart Inverter Profile – Australia (CSIP-AUS), is the protocol that facilitates communication between customer CER and grid operators in Australia. It is intended to ensure that CER (especially distributed generation) can communicate with grid operators in a standardised way to manage power flows. It is based on the US Standard IEEE 2030.5.

CSIP-AUS has four current and potential near-term use-cases, as described below.

1. Flexible export limits

Distribution networks have limited export hosting capacity that has traditionally been allocated using static export limits (e.g. 5 kW for a single-phase connection). As more solar systems connect, some areas of the grid are facing export congestion and per-customer static limits are being ratcheted down to 1.5 kW or even 0 kW. An alternative to static export limits is flexible export limits that are derived from actual network conditions and communicated to customer devices in near real-time. This generally means that customers can export more power (e.g. up to 10 kW), more of the time.

Flexible exports are currently offered in SA, WA and Qld and this will extend to all mainland jurisdictions in the next few years. They are especially valuable for bidirectional EV charging as price incentives for exports will mostly align with periods of peak demand (i.e., when export capacity limits are most permissive). Flexible exports will also increase solar curtailment during very sunny days, allowing connected EVs to self-consume solar at zero (or negative) cost.

Fall-back behaviour requirements are included in CSIP-AUS to ensure that CER can continue to operate safely and effectively even when communication with the utility or proxy server is lost:

• Default operating mode – In the event of a communication failure, CER must revert to a default operating mode that ensures grid stability and safety.

• Predefined settings – CER should follow predefined settings for voltage and frequency regulation to maintain grid support during communication outages.

• Local control – CER must be capable of local control to manage their output and protect themselves and the grid from adverse conditions.

• Reconnection protocols – Once communication is restored, CER should follow specific protocols to reconnect and resume normal operations without causing grid disturbances

2. Emergency backstop

Australia’s world-beating rates of rooftop solar uptake is resulting in increasingly low minimum demand on transmission networks (i.e., ‘duck curves’) and this can impact power system security. A requirement that new solar systems can be curtailed during critical minimum demand events is a mandatory requirement in SA, WA and Vic, and this is likely to extend to all mainland jurisdictions in the next few years. While emergency backstop schemes only apply to solar systems, system implementation architectures imply that only one CSIP-AUS client will be provided for at each customer premises. This means that where a customer has emergency backstop requirement for solar, and flexible exports for solar and bidi, these systems will need to be integrated through a local energy management system (EMS)

3. Dynamic load control

The Queensland Electricity Connection Manual24 requires that all EVSE >20A (i.e. hardwired) must participate in a network load management scheme. These include ripple control and DRM remote disconnection schemes, but also via CSIP-AUS which allow for more fine grain control (called ‘dynamic EVSE management’). enX understands that other jurisdictions are considering trailing similar requirements in the next few years. The main implication of dynamic load control schemes is that the EVSE must operate behind a single CSIP-AUS client, requiring an EMS able to coordinate multiple CER in the event of a loss of communications.

4. Dynamic pricing

The Distributed Energy Resource Integration Application Interface Technical Working Group (DERIAPIWG) is currently working on a pricing module extension for CSIP-AUS which would allow for pricing to be communicated from electricity networks and/or retailers directly to

agents appointed by customers to manage their CER. This will allow for more dynamic, and locationally specific prices to be published such that CER operation can be better aligned with customer’s interests. Dynamic pricing is recognised internationally as achieving efficient grid integration and system-value transfer to consumers.

The need for market guidance

Australia’s use of CSIP-AUS is considered favourably by international supply chain stakeholders once it is understood. However, information resources on these topics are diffuse and stakeholders are generally unclear how our approaches form a coherent smart grid architecture. There is a ready opportunity to address this issue through trustable national guidance on Australia’s emerging smart grid architecture models.

Similarly, Australia lacks clear direction on future standards requirements. This is considered salient in the context of behind-the-meter interoperability given our likely future reliance on local communication protocols to enable compliance with CSIP-AUS requirements and to ensure customers can interoperate CER devices to achieve the most value from their investments.

Support for local market homologation

Aligning international technology, standards, and framework development with local needs was also considered by stakeholders to lead to investment efficiencies, benefiting both product vendors and consumers.

Australia is adapting a range of globally common smart grid frameworks (including IEEE 2030.5) to address issues in distribution and transmission networks associated with CER and EV proliferation. Currently, IEEE 2030.5 firmware stacks are not widely used in developing EVSE solutions. These solutions mainly focus on creating a gateway for communication between EV, EVSE, and CSMS. Many CSMS vendors can support IEEE 2030.5 client functionality, as its commands are often replicated in Open Charge Point Protocol (OCPP) development (specifically in OCPP 2.x). This setup works well when the site only has EVSEs, but it doesn't when there are diverse types of CER at the site that need to be controlled under a single IEEE 2030.5 client. An on-site EMS can manage this, and in the future, a virtualised EMS in the cloud might do the same if permitted by the DNSP authorising the CER connection

Various stakeholders noted that policy and funding support processes for local market homologation could be directed to providing greater clarity on local market homologation needs to solution vendors, most of whom are based outside Australia. This could be supported by facilitating informal pre-certification testing with capable laboratories and events such as ‘testivals’ that have been highly successful in supporting industry development in other markets.25 This would help attract vendors to the Australian market ultimately benefiting Australian consumers with greater choice and lower prices

25 For example, the Open Charge Alliance runs regular ‘Plugfests’ in Europe

2.4. Summary of preconditions for mass-market bidi deployment

In summary, stakeholders consulted for this study indicate that the key preconditions for mass-market bidirectional charging product availability in Australia include:

Global conditions

• Commercial decisions on EV feature prioritisation by global automakers

• A competitive supply of charging equipment (AC & DC)

• Frameworks to manage concerns over vehicle battery health related to bidirectional charge operation

• Integration testing for EV<>EVSE communication (via ISO 15118)

Key end-market conditions

• Clear and supportive government policy

• OEM confidence in a compelling consumer value proposition

• Large addressable market relative to market entry costs

• Consumer understanding and willingness to engage

• Permissive national grid connection codes and market participation frameworks

• Clear and efficient processes for product homologation

3.

Exploring bidirectional charging value streams

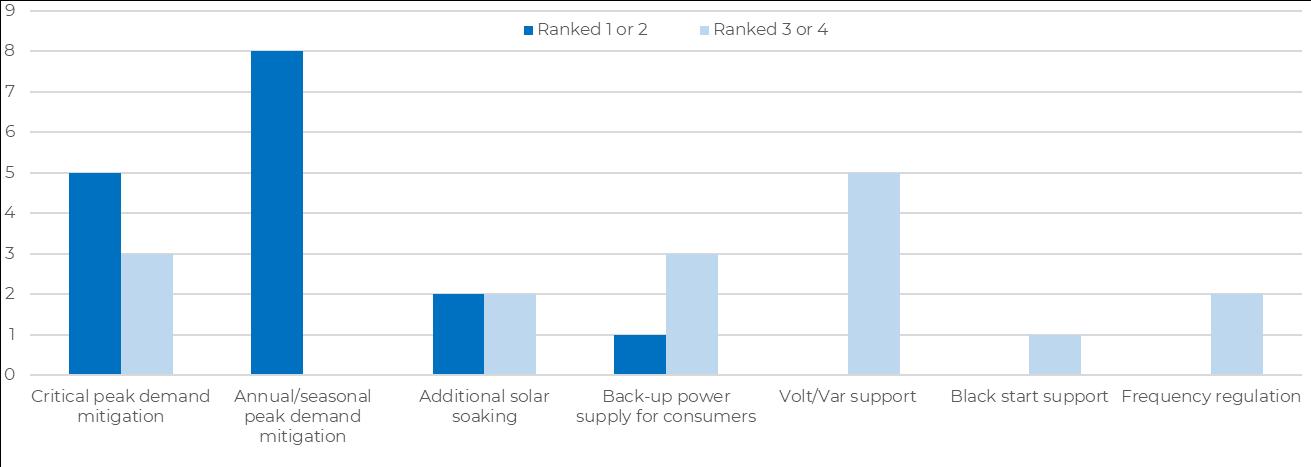

This chapter explores the potential consumer value streams associated with bidirectional EV charging internationally and in an Australian market context. Energy arbitrate (retail or wholesale) is identified as the largest potential source of value. Providing support to local networks is also highly valuable but more dynamic tariffs are required to facilitate efficient value transfer to consumers. While backup power will be highly valued by some consumers, it may be less of a driver of consumer interest in Australia compared to markets with less reliable power systems.

The long-term future for bidirectional changing remains open-ended and we may not fully grasp all the ways in which it can be used. In this section, we will explore six potential bidirectional EV charging value streams that emerged from our literature review and stakeholder discussions:

1. Backup power supply – The vehicle can provide a back-up or mobile power supply

2. Energy arbitrage – The vehicle battery can be charged and discharged to arbitrage electricity prices or increase renewable energy utilisation

3. Network support - The vehicle battery can be discharged to mitigate local peak demand constraints

4. Frequency response – The vehicle battery can be discharged to mitigate underfrequency conditions in a power system (frequency raise). While vehicles can similarly be made to charge or cease exporting to support lowering power system frequency (frequency lower) this does not require V2G

5. Load balancing – The vehicle battery can be discharged to mitigate a local behind the meter power constraint such as a grid connection limit

6. System restart – The vehicle can be coordinated to provide power generation restart services to a system operator in the event of a wide-spread power outage (‘system black’).

3.1. Critical path assessment for bidirectional charging value streams

For each value stream we examine technology preconditions and commercial maturity in Australia the US and Europe. Risks to the market objective are as summarised in Table 6

Table 6 – The potential risk of value stream constraints on the Market Objective

Constraint Description Risk

Access to dynamic electricity tariffs

Access to network support value

Minimum bid size for FCAS

Residential and commercial customers currently have access to spot price passthrough tariffs which effectively value bidi market participation. VPP models are also readily able to be redesigned for customers opting for lower risk / lower value returns.

Solar soak tariff arrangements are emerging that would support bidi operation however dynamic tariffs (or network service contracting) are needed to ensure optimal operation. There are limited incentives for DNSPs to expedite dynamic tariffs and the regulatory pathway under the current pricing rules.

FCAS could be a complementary value stream for some commercial fleets and particularly, heavy vehicles. Overall, FCAS is considered by stakeholders as a secondary (and diminishing) source of value. AEMO’s 1 MW minimum bid increment requirement will provide a barrier to market entry for many small fleets and vehicle classes and provide a barrier to early scaling

3.2. Back-up power supply

Bidirectional charging can provide an alternative power source when the customer is unable to access power from the grid. This can include the vehicle acting as a mobile generator to power a worksite or campsite (V2L), or as a backup generator feeding a home or building circuit (V2H/B) during a power outage. Defining features of this use-case include:

• The AC output of either the vehicle (AC V2G) or bidirectional charging station (DC V2G) is ‘grid-forming’ and electrically separated from the power grid26

• The EV and EVSE do not need to be grid code (AS 4777.2:2020) compliant.

Stakeholder considered that the ability to access an alternative power source is likely to be highly valued by some consumers. Further, not requiring grid code compliance can reduce hardware and installation costs and using EVs as energy storage only for backup purposes implies a relatively low duty cycle minimising battery health concerns. For these reasons, the alternative power supply use-case has been early to market, with 72 models in the European market offering V2L capability27 and several products now offering V2H in the US

Stakeholders consider the addressable market size for V2L is very large, and that it will increasingly be a standard feature on new EV models. This extends across all residential, commercial and rental vehicles and some heavy vehicles. Trucks using MCS are typically DC only, meaning that additional costs would be associated with integrating an OBC for V2L purposes (which are likely small given the relative cost of commercial vehicles).

26 Grid forming in this context means the inverter can maintain 50hz frequency without reference to the grid 27 enX analysis of www.ev-database.org Accessed August 2024

Stakeholders had different views as to the long-term customer utility of V2H/B for back-up power supplies in Australia outside of off-grid situations. While V2H/B has been an early focus particularly in the US, Australia generally has more reliable power supplies which translates into a lower benefit for customers. This issue is compounded by the relatively high capital and installation costs of back-up power relative to the reduced benefits. Additional equipment and labour costs are required to install switching devices. It was considered likely however that this would appeal to a subset of engaged customers until such time as grid-connected (V2G) applications, that are also able to provide back-up power supplies, become more prevalent and lower cost.

A survey of 40 installers undertaken by enX and the Smart Energy Council found that 85% considered back-up power was likely to be a popular use case for bidirectional charging. The most popular use case was export-enabled V2G with backup power capability, providing both revenue and energy security benefits for the customer.

Case study 1 – AC backup power

Several Australian websites promote solutions to power residential circuits using on-board power conversion. Options include coupling via the auxiliary input on a hybrid inverter, allowing the invertersupplied load to be switched alternately from the grid or a V2L power supply. In one instance, an IONIQ 5 was configured to supply 3.6 kW to a home backup power circuit.28

In the US, Tesla’s Powershare Home Backup equipment, available with Cybertruck, can detect a grid outage and provide back-up power up to within 1 minute. The power capacity is large (11.5kW offering up to 123 kWh) which could power an average Australian home under most conditions for several days. This solution implements a Tesla-specific charging station and gateway to detect grid outages and switch between EV and grid sources in a ‘break-before-make’ manner.

3.3. Energy arbitrage

Case study 2 – DC backup power supply

In the US, Ford is offering an early V2H product that allows a home to run off the Ford Lighting F150 in grid islanded mode

The EVSE is electrically connected to, and communicates with, a supplied 'Home Integration System' comprising a bidirectional inverter. The inverter is not grid synchronised and only operates when the mains power is not connected Switching from mains to backup power is automatic and managed by the Home Integration System.

The backup power capacity is large (9.6kW, and up to 151 kWh) which could power an average Australian home under most conditions for a week.