12 minute read

LEAD PRICE ANALYSIS: CRU

A restart of Germany’s Stolberg lead plant under new owner Trafigura could be delayed by Europe’s energy crisis, but when it does reopen, CRU lead analyst Neil Hawkes says a key decision will be whether to drip-feed lead into the European market or feed more to the US.

European smelter deal set to have global impact

Trafigura ended months of speculation about the future of the German lead production plant, Stolberg, when the multinational announced early in July it was buying the facility from Ecobat, in a deal that should be completed in the third-quarter of this year.

Once the acquisition of Ecobat Resources Stolberg (which owns the Stolberg multi-metals processing plant) is finalized, Stolberg will be operated by Trafigura’s multi-metals mining and smelting subsidiary Nyrstar — which has to date declined to be drawn on its ambitions for the site.

Nyrstar told Batteries Ingternational exclusively on July 21 that there would be a “continuous assessment” of the potential for future investment in the site, which has been out of action since declaring force majeure in July 2021 after the devasting floods in Europe.

When Nyrstar does formally take up control, its “first priority will be the execution of the current business strategy for the Stolberg business”.

Nyrstar did not say what that strategy entails, but CRU lead analyst Neil Hawkes says Ecobat has clearly had to invest a great deal of money, time and effort into getting the smelter back to the point where it can be restarted.

“My understanding is they’ve completely relined the furnace, so when it does restart the going should be quite smooth,” says Hawkes.

“As I understand it, Stolberg was going to be ready for a restart by the end of July 2022, but it’s unlikely the restart of the smelter will happen before the acquisition is finalized.”

One interesting thing about Trafigura buying Stolberg is that they are first and foremost a trader that happens to produces metal rather than a producer that trades metal, says Hawkes.

Asset disposal plans

Trafigura already has three zinc smelters through Nyrstar in Europe, plus the Port Pirie lead smelter in Australia, so the group is no stranger to the sector.

But what prompted Ecobat to sell?

Hawkes reckons that: “Stolberg was the easiest to sell first in any broader asset disposal plans of Ecobat’s private equity group owners, Golden Tree Asset Management, because it is the only primary smelter they have and is pretty much a standalone asset.

“It does not integrate too much with their other secondary lead operations around Europe, although my understanding is it did treat some of the battery paste from some of their dedicated secondary smelters.”

However, the ‘twist’ in the deal for Trafigura could be that Stolberg can treat some of the residues and slag that come from the group’s zinc smelters in Europe.

“In that sense, it’s a good fit for Trafigura because they can integrate the Stolberg smelter more closely with their three zinc smelters,” says Hawkes.

Later down the line, this could see Trafigura become as much of a silver refiner as a lead refiner, basically treating complex mined lead/silver concentrates and looking to improve the recoveries of silver at the expense of lead.

Hawkes also points out that refined lead production at Stolberg had been in decline even before the plant was knocked out by the floods.

The nominal lead capacity at Stolberg is 140,000-150,000 tonnes a year, but Hawkes says that’s nominal capacity — “which they’ve not been anywhere near to for many years”.

CRU’s estimation is a lot closer to around 100,000-110,000 tonnes a year.

‘Smelters need energy too’

Nevertheless, he says “it’s still a big number and still one of the main reasons why the European lead market has been so tight over the last year”.

But with industry commentators hearing that Trafigura itself has been short in lead supply in Europe, why keep Stolberg in mothballs for any longer than necessary?

“As they’re also a trader, they’ve probably got half an eye on contract negotiations for the next year and trying to maintain some healthy premium,” Hawkes says.

“On top of that, energy prices are high and will probably rise even more during the autumn and winter in Europe as a result of the war in Ukraine.”

And while Stolberg is not as big a

Nyrstar Port Pirie smelting operation

gas guzzler as a zinc or aluminium smelter, lead smelters need energy too — and the Russia-Ukraine hostilities have already set alarm bells ringing over stability of energy supplies across Europe.

“Germany has already moved to level two on the so-called ‘alert level’ of its emergency gas supply planning, so there is concern that if the government asks industrial users to start rationing it could all get incredibly messy,” says Hawkes.

“So, there is an argument — and I’m not saying it’s my view — that Trafigura might keep Stolberg shut for the rest of this year in the hope that the spike in energy prices starts to fall in the spring. But that’s a big assumption, because the view now is that the Ukraine war is entrenched and no one sees an end to it anytime soon.

“Even if some political solution emerges, Western sanctions are likely to remain in place for a long time.”

Meanwhile, Hawkes says the European market has grown accustomed to the cut-off in Russian lead supplies which have virtually dried up as a result of sanctions.

In 2021, about 50% of Russian refined lead exports went to Europe — around 55,000 tonnes last year according to CRU data — and a third of the remainder went to Asian

Stolberg site photo from Ecobat

countries, which Hawkes says raises the question of whether more Russian lead is now heading east to Asia.

Key questions for Trafigura

Does that imply batteries made with Russian lead could eventually find their way into the European and other Western markets, thereby skirting around EU sanctions?

“For sure that remains a possibility,” says Hawkes. “Once the lead has gone over the Russian border to China and countries in the Middle East or wherever, it could be converted into batteries and come in that way. Russia’s lead supply can’t be traced like that.

“We keep hearing that the Asian lead market is quite weak, flat and demand is not strong, so certainly Asia (including China) does not need to hang on to any more lead from Russia as those countries have plenty themselves.”

Meanwhile Europe, which did export some lead batteries to Russia before the invasion, is not doing that now — which frees up more batteries for the internal market.

Hawkes says: “In the future the key questions for Europe are when will Stolberg reopen and what will Trafigura do with the lead? Will they drip feed it into the European market and not impact premiums too much? Or will they feed more of it to the US market, where there is a much stronger need for more lead and where Trafigura also has a presence?

“The other big question for Europe is what happens to lead and battery demand while the path we are set on today seems to be leading to slower economic growth, if not outright recession in many parts of Europe? That will clearly have an impact on sentiment and the broader metals markets.”

In terms of lead, Hawkes’ view is that we could see some impact in the OE battery automotive and industrial lead battery sectors as consumers cut back on spending and steer away from investing in new cars.

However, this means demand in the replacement battery market should hold up quite nicely as consumers continue using existing vehicles and simply replace lead batteries when required.

“That of course creates scrap, which goes into the secondary chain and does not drive new demand, but it certainly helps support lead in a way other metals are not supported — and that is why other metals industries are starting to really worry about the impact on demand of a recession and high energy prices in Europe.”

And if energy prices do spike through the autumn or winter, that might turn attention back to zinc smelters and maybe associated lead smelters, Hawkes says.

Ecobat recently announced it was extending the traditional summer shutdowns of its two Italian secondary lead smelters from two weeks to the whole of August.

The company said this was because of the energy crises and other inflationary raw material costs. Hawkes believes low LME lead prices also influenced Ecobat’s decision.

Global lead outlook

The company will now decide about whether the Italian plants will return to operation in September at the end of August. Hawkes thinks they will be back in operation in September but says there is no 100% guarantee.

“Italy tends to have higher energy costs and higher scrap prices than other parts of Europe, so that combination may also have influenced Ecobat’s decision, as well as making a statement to the wider market to the effect of ‘lead smelters are suffering too — it’s not just about zinc and aluminium smelters’.”

On the global picture, the International Lead and Zinc Study Group said in April that world supply of refined lead metal exceeded demand last year — but Hawkes questions whether that will continue during this year.

“We are crunching our numbers now, so I can’t give an exact figure, but generally the surplus has shrunk globally this year because there was a strong rebound outside China which had big issues with Covid and further lockdowns in the second quarter of this year. These came on the back of the already weak picture there.”

This year’s refined lead market is therefore more finely balanced because of the surplus in China/Asia and shortages in the US and Europe, so the rest of the world has become very reliant on Chinese exports as we’ve gone through this year, Hawkes says.

Nevertheless, he says lead has a strong story to tell in terms of its availability, recyclability and environmental credentials.

“All of the scrap that is available to the market is getting recycled and secondary lead accounts for two-thirds or so of global refined lead production, so it’s a continuing green supply success story for lead.”

Lithium, by contrast, is not a very green story despite the hype over‘clean mobility, says Hawkes.

“The lithium battery is supposed to be part of the green story, yet they still need to keep digging up the ground for fresh raw materials to feed the huge surge in lithium battery demand, with battery recycling in its infancy.

“Lead battery recycling tends to go under investors’ radars as it quietly just meets a battery industry need for lead in a long established and efficient closed loop cycle.”

Dr Thomas Pham and Dr James Chern, of Volta Materials Technology, present the results of research into using the company’s reactive polymer technology for explosion-proof lithium-ion batteries with high energy density.

Polymer technology rises to Li-battery safety challenge

Volta Materials Technology’s (VMT) reactive polymers, which are LISA (lithium-ion battery safety assured), can be easily coated on to cathode active material pellets for explosion-free lithium-ion batteries (LIBs) with desirable high capacity and energy density.

LISA polymer possesses residual reactive functional groups for secondary polymerization initiated by the high temperature environment during the thermal runaway process in LIBs. This will reinforce the crosslinked network structure of the polymer coating on the cathode active material particle surface — in turn greatly reducing the probability of thermal runaway.

In this work, two series of pouch cells comprise NCM 622 and graphite as the major materials in the cathode and anode respectively.

The first series (5 cells) had a capacity of 32.44+ –0.15 Ah and an energy density of 229.34+ –0.16 Wh/kg.

The second series (6 cells) had a capacity of 34.61+ –0.11 Ah and an energy density of 231.24+ –0.24 Wh/kg.

Among these cells, one cell (34.57 Ah, 231.00 Wh/kg) and another cell (34.65 Ah, 231.20 Wh/kg) were stored at room temperature for periods of one month and two months, respectively, before undergoing nail punch testing.

In addition, one cell (34.65 Ah, 231.40 Wh/kg) was assembled using electrodes aged for one month and exposed to the atmosphere for one three-hour period during storage.

Before the nail punch test, the cells were fully charged from 2.8 to 4.3 V (state of charge = 100%) at 0.2C-rate. Note that the pass rate for all 11 cells was 100%.

For example, the cell (34.67 Ah, 231.30 Wh/kg) passed the nail punch test (see top left of image shown below), evidenced by very stable temperature on the cell surface and voltage vs. time profiles during the test (bottom left of image).

However, the reference LIB that did not contain the LISA polymer (9.00 Ah, 229.2 Wh/kg) instantly caught fire and exploded while undergoing the nail punch test (top right of image).

Based on our experience, it is extremely difficult to impart satisfactory safety to NCM 622-based cells with energy density exceeding 230 Wh/kg without detriment to the cell cycle life.

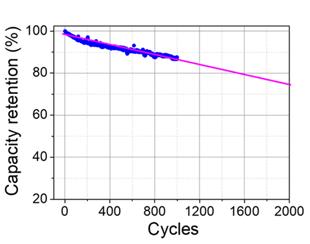

For cycling performance at room temperature, the discharge capacity retention decreases slowly with increasing number of cycles, and it is 87.6% at the 1,000th cycle (bottom right of image).

The cell is expected to maintain a capacity retention close to 80% at the 2,000th cycle by extrapolation. This result strongly suggests that the LISA technology is capable of imparting high safety to NCM 622-based LIBs with an energy density around 230 Wh/kg, while maintaining satisfactory cycling performance at room temperature.

We therefore believe that VMT’s LISA technology is a promising candidate to ensure the highest safety for energy storage systems and electric vehicles, where high energy density is greatly in demand.

For further information about VMT please visit www.vmt.com.tw or email to jim@vmt.com.tw