SACCO REVIEW Website: www.saccoreview.co.ke THE LEADING NEWSPAPER FOR THE CO-OPERATIVE MOVEMENT IN KENYA : Sacco Review Newspaper Large Co-ops to be federations in new era KSHS 50 ISSUE 79 DECEMBER 17,2022 - JANUARY 17, 2023 » STORY PAGE 8 » Page 18 » Page 7 » Page 25 Govt’s grand plan to revive coffee sector Afya Sacco holds members’ trainings, rebrands products » Pages 16 & 17 Patrick Kilemi, PS Cooperatives & MSMEs Simon Chelugui,

David Obonyo, Commissioner for Cooperatives Think beyond salaried staff, Coop boss tells Saccos Saccos to reap from Hustler Fund in February Divided opinion on who should audit Saccos

CS Cooperatives and Micro, Small and Medium Enterprises (MSMEs)

Mercy Njeru, KUSCCO

Advocacy Manager

Evans Sichangi, Trans-National Times Sacco chairman

Charles Kaba, Qwetu Sacco CEO Daniel Marete, Solution Sacco CEO

» Page 2

population of Kenyans in formal employment is less than five per cent and depending on it translates to serving only a small percentage of the Kenyan population.

Isedorius Agola, chairman KAFOSA

The

Major milestones for Co-op sector in 2022

By Azael Masese

As the curve of the Covid-19 pandemic tipped down in 2021, the cooperative sector roared back to reclaim its glorious spot as a financial solutions favourite among Kenyans.

The resurgence of the resilient sector was typified by the 100th Ushirika Day celebrations that took place mid this year after a two-year hiatus, marking a complete come back to set a new stage replete with purpose and hope.

The sector’s growth has once again been pegged on critical market segments; notably asset base, deposit portfolio, loan book and income.

Albeit with single digit percentage point growths, the positive deviation is the clearest indication of the sector’s spirit that never says die.

To sustain the gains reported, major regulatory and policy shifts have been made in 2022.

Standalone ministry

The creation of a standalone Cooperative and MSME ministry was hailed as a masterstroke, with many stakeholders tipping it as the best bet for a more competitive sector among peers globally.

Inasmuch as Cabinet Secretary (CS) Simon Chelugui noting that cooperatives and MSME have a symbiotic relationship, to many, the creation of the ministry will enhance decision making processes.

With Patrick Kilemi Kiburi taking over from Ali Noor Ismail as Principal Secretary (PS), expectations could never be higher considering the huge steps already taken by his predecessor.

Hustler Fund

Saccos have been identified as key players through which Kenyans will access the Ksh50 billion Hustler Fund; a major plank of President William Ruto’s campaign.

The fund seeks to enable Kenyans access cheaper capital to engage in income generating activities.

Since its launch on November 30, 2022, billions of shillings have already been disbursed to Kenyans.

Sacco Depositors Guarantee Fund

The regulations of this fund were approved this year. For many years,

The cooperative sector has steadily roared back to reclaim its glorious spot as a financial solutions provider. The sector recorded single digit percentage point growths, a clear indication of the sector’s spirit that never says die.

members have reeled in huge losses in the unfortunate event that a Sacco collapses.

However, the situation is set to change as members will be cushioned against any financial calamity visiting their Saccos as they will be guaranteed protection with deposits of up to Ksh100,000.

This will restore public confidence and reassure members of the safety of their investments.

Sacco Central

The creation of the Kenya Sacco Central Liquidity and Shared Services Cooperative Society Ltd (Sacco Central) marked a major milestone in the country’s Sacco sub-sector.

The platform will enable Saccos to shore up resources under one platform besides sharing a common ICT platform.

Pooling resources will address liquidity challenges as those with excess cash can lend to their peers in what is called inter-lending in the banking in-

dustry.

In the technology sphere, Saccos with limited resources can be allowed to use the ICT platform at subsidized rates compared to investing in the same, which is more often expensive.

The platform will allow Saccos' entry into the National Payment Sys-

tem. The same was approved by the Cabinet in May and is awaiting Parliament’s approval.

National Cooperative Policy

The review of the National Cooperative Policy that resulted in Sessional Paper No 4 of 2020 is a boost that will put the cooperatives on a growth trajectory. It is anchored on the theme ‘promoting cooperative societies for industrialization’.

The policy will identify contemporary challenges facing cooperatives and how to address them.

Top on this is to enable cooperatives participate in value addition and manufacturing in the country, partly through rationalizing the role of the national and county governments to ensure harmony in how they address issues affecting the industry.

Spire Bank buyout

Equity Bank acquired troubled Spire Bank owned by Mwalimu National. The acquisition brings to an

end a long torturous journey for the bank that has seen Mwalimu National spend huge resources trying to resuscitate it.

This is also a lesson to Saccos that buying a commercial bank, whose functions are similar to theirs, does not augur well with members’ investment.

For background check, Mwalimu National had topped the charts as the wealthiest Sacco with an asset base of about Ksh60.60 billion by the close of December 2021.

Coffee Bill 2020

The Bill aims at ensuring that coffee factories and societies only take loans with the approval of farmers. Any loans taken in contravention will be statutorily moved into personal loans of the officials of the offending factory or Society.

It seeks the regulation, development and promotion of the coffee sector, besides reintroducing the coffee levies abolished in 2014 and attaching a coffee research levy at no more than 1 per cent of the gross coffee proceeds.

At the height of coffee farming in Kenya, production was at 140,000 metric tonnes, but has since shrunk to about 40,000 metric tonnes. The Bill thus seeks to boost coffee production and ensure it occupies a special place in revitalizing Kenya’s agricultural sector.

Sacco faces in government

Following the 2022 General Elections, notable Sacco top managements and Boards of Directors have been appointed to the new government.

Notable are Stima Sacco Board Chair Rebecca Miano, who was appointed CS for the East African Community, Arid and Semi-Arid Lands and Regional Development.

Miano, who served at KenGen, is one of the few Sacco players to be appointed as top government officials.

Former Eco-Pillar chief executive Fred Lourien was elected West Pokot County Assembly Speaker. Mr Lourien had been at the helm for several years and has been replaced by Linus Likoria.

The Cooperative sector has a membership of more than 14 million and some feel that more should be appointed into the government at the national and county levels.

New KCC upgrade boost to farmers’ livelihoods, cooperative sector

By Azael Masese

Cooperatives and Micro, Small and Medium Enterprises (MSMEs) Cabinet Secretary Simon Chelugui has underscored the role of New Kenya Cooperative Creameries(New KCC) in supporting Kenya’s cooperative movement.

Speaking during a recent visit and tour of the processor’s Dandora plant, Chelugui disclosed that since 2016, the government had pumped Ksh2 billion into New KCC plants countrywide to enable the cooperative mop up excess milk during the rainy season and convert the same into powder to be released during the dry season.

“The investment is very important in ensuring stability of food security and prices,” he said, adding that the modernization programme seeks to upgrade all farmers’ cooperative cooling plants to

minimize post-harvest losses.

Once achieved, this will greatly improve dairy farmers’ earning and their contribution towards cooperative societies and Saccos.

A number of cooperative societies, notably in Mount Kenya and Rift Valley, rely on dairy farming for their contribution to the societies and Saccos.

“The government is working on ensuring dairy farmers get animal feeds which has been a challenge. What dairy farmers are processing is a third of what is being utilized by the milk caucus. We can mop up the amount by modernizing our plants,” he said.

He noted that with more than 120 dairy products on offer, New KCC can command a controlling market share and play a key role across the dairy sector.

He noted with concern that Kenya

has been sourcing for feeds and sunflower from Uganda and Zambia and that it is time we started contractual farming.

New KCC Board Chair Anthony Mutungi noted that coolers will enable dairy farmers to give out their surplus milk to a processor and reduce the amount sold informally.

Former President Uhuru Kenyatta and his then Deputy William Ruto launching the ultra modern UHT production unit in Eldoret in June 2017. File Photo

New KCC

Managing Director Mr. Nixon Sigey said they are targeting to replenish the milk powder during the short rains to stabilize the milk prices.

He regretted that the biggest challenge experienced by dairy farmers is the high cost of animal feeds.

“With the support and intervention by the government, we are putting in

place programmes that will go a long way in addressing the cost of animal feeds so that we are able to be competitive,” he said.

The leaders urged the government to activate the strategic food reserve that has been dormant for two years to mop up excessive milk from the market Revitalisation of the New KCC has been identified as a critical pillar in enhancing the vibrant cooperative sector.

According to the Sacco Supervision Annual Report, 2021, the asset base of dairy sector deposit taking Saccos stood at a paltry KSh8.40 billion by close of 2021.

Any improvement in the sector will greatly improve dairy farmers’ earnings and their contribution to Saccos. This will eventually translate to improved asset base, deposits, loan portfolio and incomes.

SACCO REVIEW | 3 DEC 17, 2022 - JAN 17, 2023

Rebecca Miano, former Stima Sacco chairperson.

Simon Chelugui, CS Cooperatives and Micro, Small and Medium Enterprises (MSMEs) Development, during his swearing in at State House, Nairobi on October 27, 2022.

Ukulima Sacco targets senior members with unique products, services

senior members control substantial amounts of deposits and shares hence the need to guard and preserve their shareholding. Key products and services it seeks to rollout targeting senior members include Fosa savings accounts, long term and short term loans, medical cover, deposit contribution accounts, fixed deposit accounts, estate planning scheme among others.

FOSA Savings Accounts

By Azael Masese

Ukulima Sacco has introduced new products and services to enable senior members meet their unique financial needs.

The senior members, notably those aged 50 years and above, are considered a key pillar of the Sacco and retaining them will sustain and improve on its healthy balance sheet.

By coming up with tailor-made products and services, the Sacco is keen on retaining this critical membership as it seeks to bolster improved capital base and improved profitability, guided by the 2022-2026 Strategic Plan.

Board Chair Dr. Philip Cherono stated that the Sacco has since looked into the demographic composition of its members and used this information to develop responsive financial products and services, unique to the specific needs of the members.

Dr Cherono said that the move is informed by the fact that members approaching retirement and those who have retired have unique needs that may not fully be met by the conventional Sacco products and services.

This, he added, is due to their low borrowing appetite and sometimes may be devoid of a regular source of income to commit to regular savings contributions.

Speaking during the Sacco’s Senior Members’ Engagement Forum, Dr Cherono said that retaining retirees as lifetime members has been Sacco’s biggest challenge.

“The forum is part of members’ education and we deliberately and strategically identified you as a critical category of our membership as we strive to walk with you into your retirement phase,” he said.

He stated that majority of the

To continue patronizing banking services, any member and in particular, the pensioners, are allowed to open or maintain accounts at FOSA.

“Upon retirement, we have established a mechanism in which members can channel their pension through our Front Office Service Activities (FOSAs),” he said.

Members can henceforth channel their pension fund through FOSA and earn an income.

Under FOSA, members can open savings accounts such as FOSA Savings Account, Biz Current Account and Pamoja Current Account.

The FOSA Savings account is suitable for channeling of salaries and pensions through the FOSA bank.

The biz current account works like a Fosa savings account but is suited for members with alternative income generation activities including rental incomes, farming incomes, trading incomes.

This account and the various incomes will support members when seeking credit facilities.

Pamoja current account will enable access to banking services by a registered group or chama as opposed to an individual.

Such groups include self-help groups, welfare associations, welfare societies, investment groups, churches, schools, clubs, primary cooperatives and trading companies.

Deposit contribution accounts

Deposit contribution accounts are also open to pensioners as they will enable them to contribute their savings.

One such account is the ordinary deposit contribution account where pensioners can contribute Ksh500 per month, instead of the minimum Ksh2,800 per month for every member.

Haba na Haba is a voluntary savings account that will enable pensioners to promote a culture of wealth accumulation through capitalisation of annual returns.

Fixed Deposit Account

Members have investment opportunities of fixing lump-sum amounts through the society to earn a return.

One such account is the Hifadhi fixed deposits account and flex fixed deposits account.

Hifadhi Fixed Deposits Account is a savings product targeting pensioners to provide them a financial safeguard for retirement between the date of retirement and receipt of pension. Instead of a member withdrawing from the society fully or accessing

half of their deposits through partial withdrawal, the targeted withdrawal funds are instead transferred to Fosa and accessed by members in phases gradually.

Flex Fixed Deposits Account

This type of fixed deposit account offers very attractive flexibilities to investors. It targets retirees who would wish to earn monthly income on their lump sum savings balances.

Loan products

To encourage retirees engage in income generating activities, the Sacco has a number of long term and short term loan products suitable for retirees.

Long term loans targeting pensioners include development loan, Fosa Daima Loan and Wezesha loan.

It also offers short term loans including emergency and Ukulima advantage loans.

Most importantly, there are selfguaranteed loans, where a member can borrow up to 90 per cent of their deposits without a guarantor. However, a member should not have guaranteed any member for a loan.

There is also the alternative loan security where a member can use other securities such as a title deed or log book to take loan.

Relationship banking

The society allows membership from individuals or corporates who are interested in accessing banking services only as opposed to being active with monthly back office contributions. Such a member is only required to maintain a savings account for FOSA banking services without the requirement of being a regular contributor. This is suitable for pensioners and need to open a transactional account to facilitate access to the associated banking

4 | SACCO REVIEW DEC 17, 2022 - JAN 17, 2023 Advertising Feature

Dr. P.K. Cherono, National Chairman

page...

CPA Richard Nyaanga, CEO

Board of Directors at the high table during the Members’ Engagement Forum Cont. next

The move is informed by the fact that members approaching retirement and those who have retired have unique needs that may not fully be met by the conventional Sacco products and services.

-

Board Chair Dr P.K. Cherono

2022-2026 strategic plan targets membership, deposit portfolio and asset base

services.

Flex fixed deposit account offers very attractive flexibilities to investors, especially retirees who would wish to earn monthly income on their lump sum savings balances.

The Sacco has developed close relationships with the Government’s Pensions Department so as to enable better services to the members.

As a result, pensioners are able to access a number of services out of this relationship.

One such advantage is that pensioners are able to participate in retirement planning training for members who are nearing retirement. Issues highlighted here include retirement planning, financial planning, available Sacco products and services.

It also helps in follow ups with the pensions department to fast track as appropriate the pensions processing for members who have retired and expect to be channeled through Ukulima Fosa bank.

It will also help in following up on the monthly pensions earnings for members to avoid or minimize undue delays.

In most cases, the Sacco pays monthly pension earnings to members in case of delay in remittance of funds from the pensions department. This is done upon liaison with the pension department to avail the pension payment schedule of the month and commit to remit monies soon afterwards.

Medical cover

The introduction of Ukulima Seniors Afya Plan is one such product that will augment the members’ medical expenses.

Board Chair Dr P.K. Cherono noted that with old age comes a myriad of health issues.

This informed the decision to develop unique medical products to cater for medical expenses for recurrent illnesses associated with old age.

“We have witnessed a trend where the majority of retirees usually withdraw their deposits from the Sacco to cater for such expenses, thus we have developed a product that has a medical cover component to augment medical expense,” he said.

The affordable and comprehensible medical cover protects insured persons against valid medical expenses.

Eligible expenses are paid subject to annual benefits limits provided for. In conjunction with CIC Insurance Company, pensioners can buy annual medical covers of their choice to cater for inpatient medical expenses.

It offers a wide range inpatient benefits such as pre-existing and chronic conditions cover, psychiatry/ psychotherapy cover, emergency air evacuations and road ambulance services.

Others include dental surgery, post hospitalization and rehabilitation

expenses, inpatient ophthalmologic, prescribed external aids cover, home nursing and comprehensive geriatric assessment.

The product also offers a last expense cover in the event that the insured person passes on as a result of covered conditions while the cover is in force.

Eligibility for principal member and

spouse is from 60 years to 80 years. Cover allows only one spouse as a dependent of the principal member as child dependents are not eligible under this cover.

Mentoring young generation

Dr Cherono tasked the senior members to become ambassadors and role models for the younger generation

to woo them to join as members.

The young generation, he noted, has been shying away from Sacco membership due to lack of guidance and mentorship by seniors, a role they are expected to play.

Senior members are expected to start by encouraging the children and grandchildren to join.

“There is a need to share with

younger members why they need to enhance their savings contribution and retain their membership in the Sacco for their whole lifetime,” he said.

Ukulima Sacco has also developed a dividend management plan for pensioners and involves making income from dividends earned.

This can cater for the required monthly savings contributions while the balance is distributed into a monthly income scheme.

The fixed amount that remains in the account shall continue to earn interest on a daily basis while a member earns on a monthly basis.

Estate Planning Scheme

The Sacco also seeks to encourage members who have built their deposits and shares over time to pass them on to the younger and future generations.

This would be a means of inculcating the younger generation into a savings culture and instead of withdrawing shares and deposits, these too can be distributed to the younger generation to kick start their membership journey in the society.

This, according to Sacco, is part of the inheriting the senior members’ investment, the same way it is done with land and other properties.

“The proposal would see the beneficiaries enjoy borrowing on behalf of the senior members and should they pass on, the beneficiaries will automatically inherit the retiree’s deposits but with a caveat of not withdrawing the deposits or shares of the deceased but enjoying the monthly incomes.

“Ukulima Sacco will look into the possibility of establishing an estate planning scheme where senior members would be encouraged to nominate any of their preferred beneficiaries or next of kin to join the Sacco as a member whilst they are still alive,” he said.

Strategic Plan 2022-2026

The main driver of this projected growth is the Strategic plan 2022-2026.

Sacco CEO CPA Richard Nyaanga said this is the sixth strategic Plan the Society has developed since it was founded in 1972.

Some of the key highlights of the plan is to grow its membership, deposit portfolio and asset base by 18 per cent annually.

For example, Sacco wants to increase its membership to 102,000 by the end of the plan compared to the current more than 58,000 members. Its deposit portfolio will grow to Ksh22 billion by the end of the strategic plan, compared to Ksh9.7 billion reported by the end of 2021.

It also seeks to grow its loan book by 18 per cent annually to hit the Ksh25 billion mark by the end of the strategic plan. This will be an improvement compared to the Ksh11 billion recorded in 2021.

SACCO REVIEW | 5 DEC 17, 2022 - JAN 17, 2023

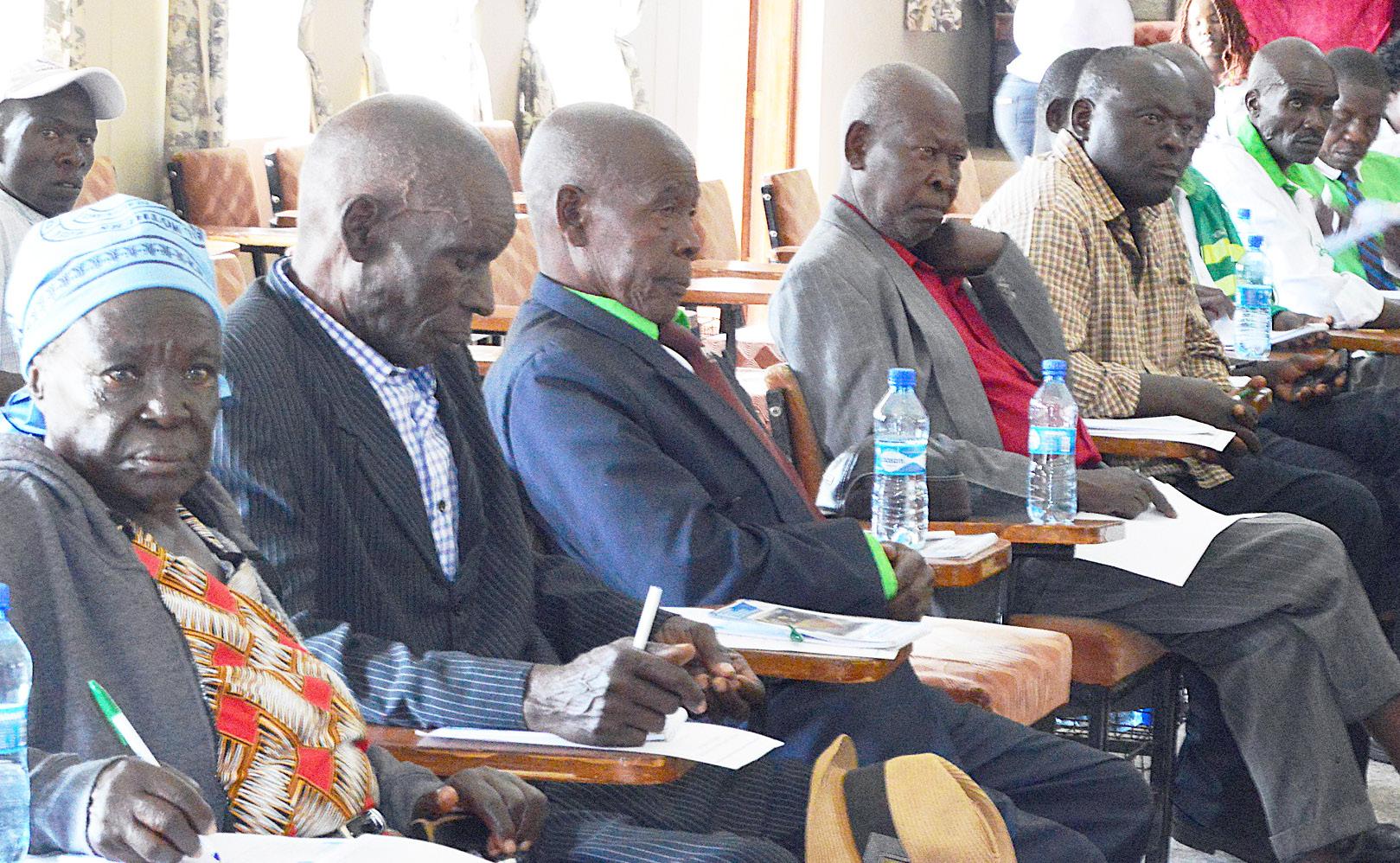

Senior members of Ukulima Sacco keenly follow proceedings during the engagement forum held in Nairobi recently. The Sacco has developed unique products to serve senior members who are approaching retirement

Senior Sacco members during the engagement forum held in Nairobi recently. The Sacco has developed unique products to target senior members who are approaching retirement

Cont. from prev. page...

SENIOR MEMBERS Special Products & Services

OUR SPECIAL PRODUCTS

RELATIONSHIP BANKING

FOSA SAVINGS ACCOUNTS

Fosa Savings Accounts

Biz Current Account

Pamoja Current Account

DEPOSIT CONTRIBUTION ACCOUNTS

Ordinary Deposit Contribution Account

Haba na Haba Deposits Account

FIXED DEPOSITS ACCOUNTS

Fixed Deposits Accounts

Flex Fixed Deposits Accounts

Hifadhi Fixed Deposits Account

LOAN PRODUCTS FOR PENSIONERS

LONG TERM LOANS

Development Loan

Fosa Daima Loan

Wezesha Loan

SHORT TERM LOANS

Emergency Loan Mahitaji Mobile Loan

Ukulima Advantage Loan

Dividend Advance

OTHER LOAN SERVICES

Self-Guaranteed Loans

Alternative Loan Securities are acceptable

Top up Loans

Housing Loans

MEMBERS WELFARE SERVICES

Membership Obligations for Pensioners

Partial Withdrawal Program

Benevolent Fund Program

Ukulima Seniors Afya Plan

CUSTODIAL SERVICES

LINKAGES WITH GOVT PENSION DEPT.

UKULIMA KASH

DEPOSIT TO FOSA A/C USING SACCO PAYBILL

6 | SACCO REVIEW DEC 17, 2022 - JAN 17, 2023 X | SACCO REVIEW DECEMBER, 2022

Are you a member of Ukulima Sacco? Refer a member today and get KES 700 for each referal Talk to us today Become a member today by dialing *882*9# and select option 2 Let’s unite to create wealth... contact@ukulimasacco.coop ukulimasacco.coop 0111035600 @ukulimasacco Ukulima Sacco Ukulima Co-operative House, Haile Selassie Avenue, P.O Box 44071-00100, Nairobi

JAN 17, 2023

By Hezron Roy

A total of 350 Micro, Small and Medium Enterprises (MSMEs) have been linked to the larger East African Community (EAC) market during this year’s 22nd East African Community MSMEs trade exhibition, formerly known as the EAC JuaKali and Nguvu Kazi, which was held December this year in Uganda.

The trade fair, held between December 8 and 18, 2022 at the Kololo Independence Grounds in Kampala, Uganda, under the theme ‘Buy East African to Build East Africa for Resilience and Sustainable Development,’ drew over 1,500 MSMEs from trade, manufacturing, agribusiness and services sectors.

Exhibitors came from the seven EAC partner states to open up new market frontiers for products and bridge knowledge and technology gaps, while at the same time boost regional integration.

Speaking during the launch of the National Organizing Committee for the trade fair on November 25, 2022, the Cabinet Secretary (CS) for Cooperatives and Micro, Small and Medium Enterprises (MSMEs) Development Simon Chelugui noted that the theme resonated well with Kenya’s mantra of ‘Buy Kenya, Build Kenya’.

He added that over the past 5 years, volumes of Kenyan exports to the EAC region has amounted to $1.4 billion (approximately Ksh172.03 billion), and that the National Export Development and Promotion Strategy envisions to increase this by ensuring that 60 per cent of Kenya’s manufactured products will be

By George Otieno

All Cooperatives will in future become federations and subscribe to an apex body, Group Managing Director of the Kenya Union of Savings and Credit Cooperatives (KUSCCO) George Ototo has hinted.

A restructured Cooperative sector will ensure sustainability and viability as it will solely depend on the subscription of the cooperative members.

Ototo revealed this while addressing over 350 delegates during the fifth annual KUSCCO conference in Mombasa converged to dissect Sacco matters, especially issues of sustainability, innovation and inclusion.

“The economic participation of our business model is critical hence the need to establish sustainable Cooperatives,” he said.

He added that it is the responsibility of the cooperators to understand and identify with the Cooperative model, invariably charging that the breach and misunderstanding of the model had led to many cooperatives going astray into unplanned diversification.

The economic development of cooperatives, Ototo added, remained critical despite Saccos being social institutions because as cooperatives, they still had obligations to the government.

The formation and growth of the Cooperative sector, Ototo said, are attributed to the efforts and contributions of early leaders such as the late President Mwai Kibaki and Tom

Micro and Small Enterprises Authority Director General and Chief Executive Officer (CEO) Henry Rithaa, noted that Kenya's continuous involvement in the event is motivated by its ability to provide avenues for MSMEs in various nations to create connections and collaborations that will create market linkages in the region.

According to the Authority, as the global and regional economies emerge from the shocks of the Covid-19 pandemic, the business recovery trajectory must be maintained by way of harnessing local sourcing and deepening the value chain frameworks, among other strategies.

Regional trade fair exposes Kenyan traders to huge EAC market

exported to the regional and global markets.

“This will grow the country’s export target by 25 per cent. It comes at a time that Kenya’s exports are projected to rise by 15 per cent this year compared to the $6.08B recorded in 2021 due to increased sales to new African countries upon the operationalization of the African Continental Free Trade Area (AfCFTA),” said Chelugui.

He added: “The trade fair will further serve to consolidate Kenya’s contribution to the volume of exports in the region, in line with the National Export Development and

Promotion Strategy. The government is also exploring new development plans to improve MSMEs' awareness of digital markets and trade to sustain e-commerce.”

Since its inception, the annual EAC exhibition has brought together MSMEs from the then East Africa's six partner nations (now seven) to expand their reach into new markets, share new technologies, and strengthen regional integration.

About 5,000 Kenyans have benefited from this trade fair, with a majority having established solid presence in the regional market through consistent supplies.

The EAC's expanded market size of 300 million people (as a result of the recent entry of the Democratic Republic of Congo (DRC) into the community) adds significant impetus to the push to increase intra-EAC trade, given that the EAC region now stretches from the Indian Ocean to the Atlantic Ocean.

With a combined GDP of approximately US$250 billion (Ksh30.72 trillion), it has made it competitive and easy to access the larger African Continental Free Trade Area (AfCFTA), hence giving the MSMEs an opportunity to access a bigger export market.

Kenya has taken several steps at the national, regional and global levels to address bottlenecks to trade in the EAC and other trading blocs.

These include integration of MSMEs into value chains, strengthening production linkages to enhance value addition, and expansion of local manufacturing for the export market.

The initiatives are aligned to the National Trade and Policy Framework as contained in Kenya’s Vision 2030, which focuses on export growth through value addition in export-oriented manufacturing and services.

Change beckons as KUSCCO boss hints at co-ops forming federations

well-trained and informed team on compliance, as well as a structured Board and staff training guided by identified needs,” he advised.

The SASRA boss further added that delegates and members need to be trained to ensure legitimate expectations are met, and the institution’s culture and ethical boundaries are understood.

He said cooperatives also need to develop a risk management culture across all cadres, from the Board down to the junior staff as risk management functions are collective.

Part of this is identifying, scoring and reporting high priority risks to enable them capture, aggregate and centralize them based on standards, controls and measures.

Mboya, who aspired to anchor development on cooperatives.

Thus, he encouraged the sector not to see mobile lenders as competitors but instead concentrate on what they were doing differently and adapt.

One such way is investing in production, value addition and marketing.

“In other worlds, the producer cooperatives are stronger than the financial cooperatives since financial cooperatives only provide finances to facilitate production,” he observed.

The managing director added that Saccos should encourage their members to get into production through lending or having value addition loans, advising delegates to create businesses that outlive them.

The Cooperative policy and the Cooperative Bill 2021, Ototo stated, will be implemented by the county governments once passed because it is a devolved function.

SASRA Chief Executive Officer (CEO) Peter Njuguna said that Saccos and cooperatives were a legal creation, thus had to be constantly

aware of new laws to continuously adjust and remain compliant.

He said it was the reason cooperatives established compliance controls and processes, accountability levels and focal points of managerial yardsticks that are accessible to all players.

Njuguna urged Sacco players to engage professionals to help across functional units on aspects such as finance, risk management, legal matters, ICT, operations, among others, to make business better.

“You also need to invest in a

Accurate and timely communication, he emphasized, was another way that cooperatives could use to remain compliant as this enhanced transparency and accountability to members and other stakeholders.

As cooperative institutions, he urged the leaders to embrace consistent communication with members using credible and authoritative platforms to stem misinformation and disinformation. Such effective communication across ranks helps maintain the cooperative ideals.

SACCO REVIEW | 7 DEC 17, 2022

-

Hon. Simon Chelugui (centre), Cabinet Secretary Cooperatives and MSMEs Development, speaking during the commissioning of the National Organizing Committee for the EAC Exhibition

A

Peter Njuguna, SASRA CEO

George

Ototo, KUSCCO Managing Director

restructured

Cooperative

sector

will ensure sustainability and viability as it will solely depend on the

subscription

of

the Cooperative

members.

Cooperatives are a legal creation hence the establishment of compliance controls and processes, accountability levels and focal points of managerial yardsticks.

Saccos challenged to diversify from check-offs to MSME markets Invest in research, innovation to remain relevant, Kilemi urges coops

By George Otieno

Commissioner for Cooperatives David Obonyo has called for a paradigm shift on how Saccos conduct their businesses, warning that relying on the check off systems is no longer tenable.

Most Saccos, Obonyo stated, were employee-based that depend on bank check offs at the end of the month to recover loans, turning their backs on millions in informal employment.

“The population of Kenyans in formal employment is less than five per cent and depending on it translates to serving only a small percentage of the Kenyan population,” he said.

Obonyo said the youth make up more than thirty five per cent of Kenyan earners, hence the need to bring them on board.

He was addressing delegates during the leaders’ forum organised by the Kenya Union of Savings and Credit Cooperatives (KUSCCO) in Mombasa recently.

Majority of Saccos have opened the common bond, allowing the business community to join and enjoy the benefits that come along with membership.

He said that the rebranding and opening of the common bond to accommodate a bigger community was not enough and they need to target where the population is.

“What are we doing to improve the lives and the income of the members that join our Saccos?” He posed.

He reiterated the need for Saccos to come up with prod-

ucts that are SME-oriented and facilitate the growth of business.

He encouraged Saccos that have not yet fully embraced the use of technology to establish mechanisms that will help them transit into modern ways of running businesses or face extinction.

He, however, dissuaded the Cooperative leaders from using technology to embezzle or misuse members’ funds.

Since the ‘Hustler Fund’ is heavily dependent on technology, Obonyo asked Saccos to adequately prepare their systems.

were in the business of changing the lives of the people and not necessarily making money.

“We need to ensure members live in decent homes, are able to meet the cost of education of their children and address their daily needs,” he said.

On the other hand, he pointed out that Sacco leaders should not open branches haphazardly, nor give indiscriminate loans that do not perform, ending up hurting the Saccos. Though it is appropriate to continuously keep looking for new available opportunities, Obonyo reminded Saccos to first carry out due diligence before allowing new members in.

As a devolved function, Obonyo challenged the leaders to take the sector to the next level.

“At the county level, the county government has deployed officers to support the Cooperative functions,” he said.

He challenged them to look beyond region and compete with Europe and the Western economies.

By our reporter

Principal Secretary in the State Department for Cooperatives Patrick Kilemi has challenged cooperatives to come up with new ways of doing business if they are to remain relevant.

In a competitive and challenging market, the PS underscored the need to embrace research and innovation as critical ingredients to sustainably improve performance and profitability.

“You need to invest in strategies that focus on products, services, processes, business models and marketing,” he said.

Besides, he identified technology, marketing and social interaction as other areas cooperatives need to invest in to enable them to serve members effectively and efficiently.

He said this at a conference organized by the Kenya Union of Savings and Credit Cooperatives (KUSCCO) in Mombasa recently.

every single day and by last week more than ten million Kenyans had enrolled on the platform with more than KSh7.5 billion disbursed.

In addition, over 10 million have registered on the platform to enable them to borrow funds.

Speaking at the same event, Taita Taveta Deputy Governor Christine Kilalo underscored the significance of the Hustler Fund in boosting national savings and promoting economic growth through job creation.

Kilalo, who was the chief guest representing the governor Andrew Mwadime, said the fund promotes market interaction by providing access to finances.

She urged the cooperators to take advantage of the fund to promote the growth of micro enterprises.

“We must strive to positively impact the lives of our members who aspire to have homes of their own, making it our responsibility to come up with mortgage products that will enable members to achieve these dreams,” he added.

Cooperatives, he said,

He identified the creation of the standalone Ministry of Cooperative and SME as a critical investment aimed at creating an enabling environment, giving policy direction, legal framework and investment that will enable cooperatives realize their aspirations.

Obonyo said skilled students from TVETs and colleges can be brought together to form a worker cooperative and make it easy for them to acquire jobs in government and other institutions, yet save to build their own Saccoos.

The discussions during the conference, the PS noted, would inform government policies and address the strategies to create an enabling ecosystem for sustainable cooperatives and enhance Kenyans’ social and economic transformation.

“The output of the conference will not only provide information for expansion of the body of knowledge but also highlight challenges and opportunities in the Sacco sector,” he said.

The PS promised that the government was committed to developing the sector and members have the mandate to come together and build the sector.

He said that collaboration of the Union, the government, Saccos and other stakeholders will culminate in a stronger partnership necessary for the development of the

industry.

He applauded KUSCCO organizers for running the annual conference five years in a row, bringing together over three hundred and fifty members drawn from different Saccos to deliberate on issues such as the challenges, opportunities and emerging trends in the industry.

At the same time, he disclosed that the second phase of the Hustler Fund will begin in the middle of January 2023 to enable young people engage in income generating activities.

The figures keep on changing

The Deputy Governor encouraged the industry players to educate themselves on cyber security to prevent loss of funds through hacking and other forms of cybercrime.

Acknowledging the immense role Saccos play in the country, Kilalo said the transformation of the Kenyan economy has been through financial inclusion through savings and affordable credits.

Kilalo noted that the KUSCCO summit provided a pool of knowledge and skills with the ability to continue to spur the growth of the Cooperative sector.

She promised to lobby other elected leaders to support the sector by passing all the pending legislations related to the Sacco sector.

Kenya’s cooperative sector has more than 27,000 registered cooperatives and more than 14 million members.

Its asset base is estimated at Ksh1.5 trillion, savings at Ksh1 trillion and loans in excess of Ksh980 billion.

Coop sector deserves govt support, Kilifi DG says

By George Otieno

By George Otieno

Kilifi County Deputy Governor Flora Mbetsa Chibule has stressed the need to support cooperatives as key enablers of Kenya’s improved social and economic growth.

Cooperatives, she said, cut across all the sectors of the economy, namely agriculture, mining, housing, transport, and manufacturing.

In addition, they are known worldwide as instruments of poverty eradication and wealth creation through mobilization of financial resources for development, hence the need to be given the necessary support.

She was speaking on behalf of her governor Gedion Mung’aro during this year’s KUSCCO annual leaders’ summit held in Mombasa.

“We must commend the government for the good work it has done to ensure that there is a good operating environment for our cooperatives to thrive,” she remarked.

Chibule identified Central Liquidity Facility, Sacco Central, Deposit Guarantee Fund, and Sacco Societies Fraud Investigation Unit as some of the policing

vocacy wing that has been very instrumental in lobbying for good pieces of legislation.

Chibule encouraged industry players to re-double their efforts in order to achieve financial inclusion in the country.

This, she said, can only be achieved by investing in digital transformation as the financial sector was very dynamic and as such, Saccos had to embrace ICT in their operations to remain competitive.

“You need to map all your services and products on digital platforms and come up with innovative products such as internet banking and mobile banking. A robust management system will

not only guarantee safety but also ease recording of transactions and regulatory reporting,” she said.

Chibule underscored the need to entrench good governance practices to boost the growth and survival of institutions.

She identified the cooperative movement as a key partner in the county’s development agenda, promising the government’s full support aimed at promoting and enhancing growth.

These include building institutional capacity for value chain cooperatives to be able to do value addition and processing.

Others are allocation of capacity building funds for training members

and officials of cooperatives, provision of working capital to start up cooperatives through the Kilifi County Micro Finance Fund, and matching grants through agricultural sector programmes, building capacity of the cooperatives directorate through staff training and recruitment, and coming up with relevant legislations to meet specific sector needs

She remained optimistic of a bright future for Saccos, considering the establishment of a fully-fledged ministry. This, she said, called for concerted efforts by the government and development partners to popularize and also support the Sacco business model for the benefit of all.

and regulatory framework aimed at improving member confidence in Saccos.

The incorporation of Kenya Mortgage Refinancing Company to bridge the gaps in mortgage financing is another milestone reported in the Sacco sub-sector.

She applauded KUSCCO for its dedication towards the growth of the Sacco sector through their various programmes and activities such as the ad-

8 | SACCO REVIEW DEC 17, 2022 - JAN 17, 2023

FOCUS ON KUSCCO CONFERENCE

David Obonyo, Commissioner for Cooperatives.

Christine Kilalo, Taita Taveta Deputy Governor.

Patrick Kilemi, PS Cooperative & MSMEs.

Cooperative officials during the KUSCCO Sacco leaders conference in Mombasa recently. Photo /George Otieno

Flora Mbetsa Chibule, Kilifi DG.

Co-op Bank donates Ksh150M to the President’s Drought Response kitty

By staff reporter

Co-operative Bank of Kenya has pledged Ksh 150 million towards President William Ruto’s anti-hunger fundraising appeal.

The contribution, the single largest donation to the kitty so far, will support families affected by the drought that has ravaged various parts of the country.

Speaking during the 37th graduation ceremony of International Leadership University (ILU) on Saturday Nov 19, 2022, Group CEO and Managing Director Dr Gideon Muriuki stated that CSR is one of the three critical pillars that have enabled the bank to become a key financial player in Kenya’s socio-economic development.

The bank serves more than 9 million customers and 15 million cooperative movement members.

Dr Muriuki underlined the importance of having a strong workforce as another critical pillar of success.

“As a leader, I have learnt that investing in people and teams pays the best interest. You are ultimately as strong as the team around you,” he advised.

He noted that through the collective efforts of the employees at Co-op Bank, the bank has revolutionized the banking sector through many initiatives as trailblazers.

“In 2003 we pioneered mobile banking in

Kenya when we made it possible for our customers to access and complete bank transactions, such as making enquiries on bank balances and paying of electricity bills, directly from mobile phones,” he noted.

Dr Muriuki also identified building a transformative culture as another critical investment for the bank.

He stated that Co-op Bank fully embraces and nurtures a transformational culture that guides the way it relates with all its stakeholders.

“We believe that building a transformative culture that is sustainable and inclusive is not in conflict

with our business goals and pursuit of profit, but rather complementary. We are proud to have built a culture that is competitive and highperforming as well as purpose-driven and faith-led,” he said.

Transformative culture encompasses key components such as values, leadership and management, brand, reputation and risk, sustainability and social justice among others. The above mentioned lead to courage, connection, collaboration, common purpose, communication, compassion and curiosity.

On its identity, he said the bonds of loyalty

between stakeholders were tested during the Covid-19 pandemic, when many institutions, especially banks and other listed companies, took a defensive stance and decided not to pay dividends to shareholders.

“However, as Co-op Bank, we are aware that we were indeed ‘created for moments like this’. We defied the trend and paid dividends, knowing very well that our act formed a critical lifeline especially to our Co-operative shareholders,” he said.

In 2020 and 2021, Co-op Bank paid out a total of Ksh11.7 billion in dividends, the bulk of it going to co-operatives as majority shareholders. During the ceremony, Dr Muriuki recognised Police Constable Ann Wanjiku Waigwa for setting the right tone in building honest leadership in the country.

Constable Ann recovered a bag containing Ksh2.4 million and other valuables which a British tourist had misplaced at Wilson Airport. She preserved the items and tracked the owner to ensure he gets back his items.

Dr Gideon Muriuki, flanked by the Chair of the ILU Board of Trustees Hon. Justice Daniel Musinga, awarded Wanjiku a Special Merit Award and a full academic scholarship by ILU.

Hon Justice Musinga is also the President of the Court of Appeal in Kenya.

SACCO REVIEW | 9 DEC 17, 2022 - JAN 17, 2023

020 277 6000 / +254 703 027000 P.O. Box 48231 - 00100, Nairobi https://www.co-opbank.co.ke/ Co-operative House, Haile Selassie Avenue, Nairobi. customerservice@co-opbank.co.ke

Police Constable Ann Wanjiku Waigwa (right) receives a Special Merit Award and full academic scholarship from the International Leadership University (ILU), handed over to her by the Group Managing Director & CEO of the Co-operative Bank Dr Gideon Muriuki who was Chief Guest at the university’s graduation ceremony recently. He’s flanked by the Chair of the ILU Board of Trustees

Hon. Justice Daniel Musinga who is also the President of Kenya’s Court of Appeal. Policewoman

Anne Waigwa was honoured for her remarkable integrity when she recovered a bag containing Ksh 2.4 million in cash and other valuables that a British tourist had misplaced at Wilson Airport, where she proceeded to make every effort to trace the owner and finally handed over the goods.

The contribution, the single largest donation to the kitty so far, will support families affected by the drought that has ravaged various parts of the country.

mandate

The year 2022 will be behind us in a few days. In its place is 2023, with new aspirations that traditionally usher in a new year.

The old will be gone, but the cherished memories will endure to pass the baton of optimism and hope to yet another cycle of human struggle. Our resilience and promise of a better tomorrow is holding out, and we pray once again to put our acts together and become better people and better organizations.

It is true for individuals and partnerships as much as it is for Saccos and cooperative societies; they all celebrate their achievements but do not stay in that mood forever. Sooner, merry will be laid aside to resume the same journey of uncertainty, expectations, dreams and ambitions.

Consequently, 2023 presents the Cooperative Boards and managements the opportunity to improve performance, profitability, and sustainability.

This is easier said than done, yet it is hard when there is little drive to motivate towards higher goals and targets that are invariably set at the onset of every year. There are hits and misses as far as these two pillars are concerned.

Fortunately for the cooperative movement, forbearance and stability have proved to be their standard banner even in the most difficult of times. The Covid-19 test is a good example.

The short unwinding period will suffice to plan better and avoid the common mistakes that cumulatively make it hard to reach our objectives as organizations.

As stakeholders, including government, keep their expectations high, the promise and pressure to deliver compete with our abilities and limitations.

There is no better planning than now, though it is time to measure expectations against realities of our own situations.

Sacco Societies Regulatory Authority (SASRA) CEO Peter Njuguna has always insisted on a constant focus on the impact that Sacco activities have on members.

This is away from the dividends paid every single financial year and closer to the opportunity for saving and borrowing.

The measure of success of a Cooperative may have to be revised as to be aligned to the original purpose for which they were formed.

This way, the growth of the Cooperative sector in Kenya can be seen from the welfare lenses rather than profitability.

When this is done, there might be no need to spend massive resources in the new year on irrelevant product training at the expense of education.

Sacco Review wishes you a merry Christmas and happy new year.

SACCO REVIEW

Website: www.saccoreview.co.ke

Chief Executive Officer: Peter Silsil

Editor: Rosemil Oduor

Revise Editor: Kipkemboi Toroitich

Supplements Editor: Azael Masese

Layout & Design: Gabriel Sankale & Sydney Kimiywi

Distribution: Daniel Maganya

Registered at GPO as a newspaper

Hustler Fund can be incorporated into Sacco business model

The much awaited Hustler Fund aimed at helping small business owners access startup capital is finally out. The fund is also meant to establish a saving culture as well as encourage investments and social security, among other benefits to Kenyans.

The terms and conditions have been greatly simplified to meet the financial needs of every Kenyan. Individuals can access from Ksh500 to Ksh50,000.

The government has expressed interest to work with cooperatives to channel the funds to Kenyans. Should cooperatives accept the offer? Are they ready to channel the fund? If not, what do they need to do?

First and foremost, cooperatives should get in the frontline of supporting this agenda.

They should rise to the occasion and give a positive response to the offer from the government in the best possible way and prove they are the best vehicle to drive the government’s agenda.

The Hustler Fund accessibility involves a very short process and the period between funds application and cash disbursement is greatly minimized. The fund security is very affordable to all as it requires only a guarantor, which is the most common mode of loan securities in our cooperatives.

Through the Hustler Fund, both cooperatives and their members will benefit. Cooperatives will have the best opportunity to increase their businesses and expand their market share while mobilizing fund credits.

To channel the funds, cooperatives should formulate friendly measures and strategies to make the agenda realizable by the target group potential and existing members.

Cooperatives should redesign their policies to accommodate this fund initiative to co-exist normally with other cooperative products and services.

They need to get to work by making the fund more popular and attractive to Kenyans who may consider joining cooperatives with the intention of accessing the funds.

The new marketing language needs to be incorporated with Hustler Fund sensitization messages. The target groups of cooperatives should shift from their common bond members to youth groups, women groups and any other marginalized organized groups targeted to be the greatest beneficiaries of the Hustler Fund.

Cooperatives should be on the ground guiding and educating these target groups on entrepreneurial skills and

financial literacy to ensure the purpose of this initiative is achieved. They should engage all possible avenues including incentives, simplified offers and online recruitment platforms to ensure they disburse majority of the hustler credits.

The hustler fund has been set with attractive features that include reduced turnaround time, simplified procedures to apply, very affordable securities and no discrimination regardless of who applies.

Cooperatives should therefore consider some features that accommodate the fund specifications.

Since it is aimed at solving the problems of frustrated Kenyans who have been queuing for hours and days with loan application forms and several evidence documents in banking halls seeking business startup capital, cooperatives need to embrace new technologies in automation of services.

They need to reduce these traditional processes and come up with quicker methods of disbursing the fund. This calls for effective and fast response to enquiries and operating systems put in place to increase efficiency on all operations.

Cooperatives that wish to channel the Hustler Fund agenda should ensure they are financially sound to ensure their business is continuous. Their commitment in disbursing the funds should match the same efforts in provision of other products and services.

All in all, Cooperatives should stick to their main objectives. The Hustler Fund mobilization is an added advantage to boost their businesses. This should not divert their attention of serving their members or developing more products as per the needs of the existing customers.

10 | SACCO REVIEW DEC 17, 2022 - JAN 17, 2023 EDITORIAL

OPINION

Ndegwa

the

Saccos in the country.

CCOP Dorcas Nyambura

The writer works with one of

thriving

Let’s take Saccos back to their original

Ngrrrrrr! hee! hiii! Why did I even get the Hustler Loan in the first place! It’s all gone due to betting!

President William Samoei

Ruto had a catchy, meticulous and well-executed campaign on the Hustler Fund that drove masses to vote for him during the August general elections.

Through the Fund, the president sought to help the many people involved in informal economy to start or build their businesses.

There have been a lot of arguments on the practicability of the Hustler Fund and in all honesty, their points are valid.

I have been struggling to figure out the difference between the Hustler Fund and other similar funds like the Youth Enterprise Development Fund, Women Enterprise Fund and Uwezo Fund.

The Hustler Fund is a noble idea but its chances of failure are lurking around it. First, if you ask those who have been practically involved in any lending business like banks or Saccos, they’ll tell you that their biggest headache is Non-Performing Loans (NPLs).

The high rate of NPLs is an indicator of a poorly performing economy.

Secondly, it might seem fair enough to give someone between Ksh5,000 to Ksh50,000 to start a business like small barber or salon shops, but in actual sense, it isn’t. Most of these small businesses are duplicates.

The latest reports by reputable in-

Innovation, not Hustler Fund, is the antidote to poverty

stitutions reveal that the rate of attrition of micro to mini businesses in Kenya within the first 3 years is very high (above 50%). By the 5th year, a huge portion (estimated to be above 70%) of these businesses are gone.

The main challenge experienced by these businesses is lack of adequate effective demand. This challenge in the economy can be attested to by poverty levels as well as high rate of unemployment and underemployment.

You won't solve the problem of poverty by simply supplying money in credit. The success stories you see in the media are just one in many other failures unreported. The owners of the few success stories manage to cultivate a market niche or build a cartel to succeed.

The excitement about the Hustler Fund should be measured because it isn’t any different from the other funds we have. Hustler Fund is a good idea but won't do much as probably many expect. The promise of some utopia, which many want to believe in, won’t work. Politicians, magicians, sales people and scammers all work perfectly on

Harrison Mwirigi Ikunda

The Writer is a Political, Economic and Social Analyst and Commentator. He is also the Chief Executive Officer of one of the leading Auto Industry Associations in Kenya. hm.ikunda@gmail.com

Harrison Mwirigi Ikunda @hikunda

Harrison Ikunda

the same principles and strategies.

The solution to fighting poverty is innovation.

Our country’s population is growing rapidly and that’s a blessing as a huge population provides huge labour force, which when utilized well can easily make a country a super power.

History has indeed proven that densely populated countries are always innovative and end up powerful, both economically and military-wise.

What we are missing in the fight against poverty isn’t a supply of money but complete economic reforms, radical thinking and transformation.

Our biggest problem is that our economy is too shaky as a result of corruption and a shaky industrialization journey. Our country has a few industries set up to manufacture products yet we’re shameless importers of even goods we can easily produce and export.

Without successful local industries, the unemployment problem in the country will remain a thorn in our flesh. To add to our misery, we are not also exploiting our potential fully.

The hits and misses of Sacco rebranding

The liberalization of the Cooperative Sector vide Sessional Paper No 6 of 1997 titled Cooperatives in a Liberalized Economic Environment gave Saccos a chance to rebrand to grow and enhance their competitiveness in the liberalized market.

They rebranded by developing strategic plans that prioritize short and long term measures of achieving intended goals. As a result of this, most Saccos’ missions read ‘to be the best Sacco in the country’

What did the Saccos do to rebrand?

i) Changed names. New names were adopted to endear the Saccos to broader catchment areas beyond the traditional common bonds captured in their bylaws. The Saccos hoped such changes could boost their brands in the hitherto controlled environment.

ii) Saccos amended the common bonds and areas of operations in their bylaws. As a result of this, membership grew exponentially that the ‘new members’ outstripped the ‘traditional members’.

iii) In a bid to attract more members, the Saccos developed very attractive short term loan products to keep commercial banks at bay. The high uptake of short term loans progressively eroded the demand for development loans culminating in members becoming net borrowers rather than net savers. This was an affront to the primary objective of forming Saccos: inculcating a savings culture and providing affordable loans to the members.

iv) Saccos developed new logos, chose colours of staff attire, modernized their office premises and also hired qualified staff to manage the anticipated increased workload.

Revitalize coffee production

I have been keenly following Cooperative and MSME Cabinet Secretary Simon Chelugui’s media reports since his appointment.

He is keen to revive the coffee sector in this country. Truth be said, there is no history of Kenya’s cooperative sector without coffee.

Gone are the days when coffee production was the main economic driver in Mt Kenya, Rift Valley and some parts of Nyanza.

Reviving coffee production seems to be an uphill task

but the new CS has stated he is up to the task.

He has severally said that at the height of coffee production, Kenya used to produce 140,000 metric tonnes before it went down to about 40,000 metric tonnes.

How to get there is never an easy task and calls for concerted efforts. However, the Government should not forget the role of other crops such as tea, cotton, and dairy.

- Joseph Kimani, Kiambu

Fred Sitati

What are the hits of rebranding?

a. By and large, all Saccos that rebranded have witnessed exponential growth in business

b. The expansion of branch-

Kudos Ali Noor Ismail

Former State Department for Cooperatives Principal Secretary Ali Noor Ismail served with dedication and commitment and there is every reason to hope that the new PS follows suit.

During his tenure, the sector reported remarkable growth and this has to be surpassed if we are to remain on top of the charts in Africa and the world. We all need to emulate his ethics while he served the country.

-Mary Mwangi, Nairobi

For many years now, comparisons between commercial banks and Saccos have been made. This is meant to sway Kenyans to decide where to invest their money.

While there is every convincing reason on why Saccos look like a better bait, a lot needs to be done.

Recently news of misappropriation of

The tourism industry, a good net for foreign cash inflows or hard currencies income, has undergone too much ups and downs and is barely generating any income. The agriculture sector is still on its knees. Worse still, subdividing land into smaller parcels is a challenge for viable agriculture in the long term, yet we still do it for individual and family security reasons, cultural issues and lack of viable alternatives.

In conclusion, the Hustler Fund is a good and temporary painkiller to soothe the hungry and angry population. We need to create industries that can absorb massive labour. Since we have too much idle labour or under-employed people, let us find ways to use them in a structured and formal way which is properly regulated. If we don’t do that, in another cycle of 5 or 10 years, we will be treated to other painkillers.

We also need to deal with the borrowers’ mentality. So many Kenyans borrow without intending to pay back, arguing that it’s government money after all. People want freebies as our politicians have cultured us to expect them. There are many entrepreneurial and hardworking Kenyans but our cumulative culture is simply rotten. Kenyans do not fear the law any more. You can add millions of layers of laws, fines and jail terms, yet Kenyans simply don't seem to care.

es has improved service delivery and created employment opportunities for many Kenyans

c. Due to the stiff competition amongst the Saccos, to a large extent efficiency has been achieved.

d. The corporate images of these Saccos have been boosted through engagement of qualified Secretariat staff led by Chief Executive Officers (CEOs)

What are the misses of rebranding?

a. Since membership is some Saccos is now 'open', the Saccos risk losing their identity. Some new Sacco names are not easily related to the original names the public were acquainted to

b. As competition among Saccos widened, rates of dividends and interest on deposits became the major determinants of luring new members to join or defect to Saccos perceived to

be better in service delivery. Such rates also determine the re-electability of the retiring board members. Your guess is as good as line as to whether or not the trend is in line with the cooperative identity.

c. Due to the stiff competition among Saccos, some employed unorthodox means like monetary inducements to get new members.

d. In terms of governance, the huge membership dictated the adoption of delegates system. The delegates attend Sacco meetings, a move that has disenfranchised majority of members.

e. Due to the diversity in membership, it became challenging in terms of logistics to organize successful members' education meetings. As a result of this, some Saccos organize delegates’ education programmes purportedly on behalf of ordinary members who are treated as mere customers.

f. Financial implications of rebranding in some Saccos was shrouded in opaqueness and some of the anticipated achievements were, to say the least, hot air!

one of the top Saccos was reported. It does not work well when news of mismanagement of one Saccos gets to the public limelight while there is increased marketing to recruit more members to join Saccos. A simple mistake by Saccos will dent their efforts to recruit more members.

-Peterson Marwa, Migori

As 2022 comes to a close, I am optimistic that 2023 presents another golden opportunity to make the cooperative sector great. This can only work if we improve on a number of areas that make the sector great. Top on this is the savings culture. We all need to embrace a saving culture by putting aside some savings for the rainy season.

No country or individual has been able to build formidable investments without saving for the future. It is from these savings that one can get enough capital to invest in income generating activities and that should be our driving force going forward.

We can make our economy great like other countries have done, such as China by improving on our savings. Let 2023 be the year to improve on our savings.

-Daniel Mutua, Mombasa

SACCO REVIEW | 11 DEC 17, 2022 - JAN 17, 2023 OPINION The Editor welcomes short and precise articles for publishing on this column. Send your observations to; Saccoreview@shrendpublishers.co.ke FEEDBACK COLUMN

The writer is a Co-operative Movement Consultant.

Saccos need to up their game

May 2023 be the year with blessings

About Yetu Sacco

Yetu SACCO is a deposit-taking Sacco licensed under the Societies Act. Its Registration No. is CS. 6366. Over the years Yetu SACCO has established itself as a leading institution playing a central and supportive role in the social and economic development of our country through the provision of the competitively priced financial products. The name Yetu SACCO Society Ltd was adopted in 2010 when the administrative areas of presence moved beyond South Imenti in Meru County. The name “Yetu” is a Swahili word that means ‘ours’; born from members commitment to building their own society.

YOUR SUCCESS, OUR PRIDE

Mission

To grow and empower our membership by adopting innovative market driven services

Vision

To be an inclusive financial institution offering high quality services

Slogan

Your success our pride

Core Values

Professionalism

Equity

Accountability Integrity

Customer Service Teamwork

Concern for community Innovation

TheChairman,BoardofDirectors,delegates,staff andmembersofYetuSaccoheartilycongratulate EGHSimonKipronoCheluguionhisappointment as CS Cooperatives & Micro Small & Medium Enterprises(MSMEs) Development.

12 | SACCO REVIEW DEC 17, 2022 - JAN 17, 2023

Mark Gitonga, Sacco Chairman

Congratulations Congratulations CongratulationsCongratulationsCongratulations

SACCO REVIEW | 13 DEC 17, 2022 - JAN 17, 2023 Head Office, Yetu SACCO House, P.O Box 511-60202,Nkubu. Phone: 0724114444, +254 64 5051399 | Email: info@yetusacco.co.ke, sitsacco@yahoo.com Nkubu Branch +254 (0) 64 5051399 Opp. Methodist Church, Mikumbune Rd, Nkubu Meru Branch +254 (0) 20 200 1119, Sawasawa Uniform building, opp Mutindwa Chemist, Meru Town Kionyo Branch +254 (0) 20 800 6078, Kionyo Market Kinoro Branch +254 (0) 20 2o26143, Kinoro Market Kitengela Branch Eagle house, Nairobi-Namanga highway 0111038000 Nairobi Branch +254 (0) 20 218 1909 Magamano Building, Ground Flr, Lagos Rd Nairobi

BRANCHES:

Housing cooperative members warned against reckless land sales

By Agnes Orang'o

Komarock Housing Cooperative Society members have been urged to avoid unnecessary land sales and instead invest on the lands to secure their future.

Speaking to members during one of the Society’s meetings, chairman Bernard Maembe expressed concern over the increased land sales.

“Most of you inherited your land from your fathers hence you should focus on investing on the land to enable

you create a future for yourself and your children,” he said.

He warned that some members had recklessly sold their land and ended up poor while others are battling land cases in courts of law.

Bernard Mungata, the Society’s lawyer, gladly told members that the dispute with KCB was coming to an end and that they can now develop the 700-acre piece of land.

He hailed former senator Johnson Muthama for helping in the fight to get back their land.

Cooperatives expect radical reforms from new ministry, Vision Sacco Manager says

By Lydia Ngoolo

By Lydia Ngoolo

Vision Sacco Manager Dominic Musyoka has noted that Cooperative members have high expectations that the sector will improve under the leadership of the new CS.

Speaking to Sacco Review from his Wote office, Musyoka expressed satisfaction with the move to have a standalone Cooperatives ministry and Cabinet Secretary.

He noted that Saccos can now smile since they have a ministry which is fighting for and fully minding their interests.

He went on to note that he’s now sure Saccos will easily get government loans.

"We have been recognized after a long time. We hope that things will stabilize now," he concluded.

By Robert Nyagah

Neno Savings and Credits Co-operative Society has embarked on a serious marketing drive to increase membership.

Sacco Chair Peter Manga said the Sacco has blazed its guns on doubling its membership through a ruthless recruitment campaign.

Addressing members during the budget approval meeting, Manga said the Sacco’s marketing team is working on ensuring each member recruits two new members and the 500 members with dormant accounts revive them. This will bring the membership to 2600.

“The marketing team will be adequately funded to traverse all parts of Mt Kenya region,” he said. Manga urged the members to be good ambassadors of the Sacco by telling others about the Sacco’s loan products and proactive management systems.

“The Sacco has attractive loan packages and I would like to encourage members to take loans and elevate their businesses and their standards of living,” he noted. He further urged them to be ready to open up to the management on areas they need to work on.

Sacco treasurer Martin Fundi noted that members approved the budget of Ksh47 million for the year 2023 FY up from Ksh45 million set aside for this year’s budget.

According to the budget,

County promises to improve livelihoods through CEDF

Uasin Gishu Cooperatives and Enterprise Development CECM Martha Cheruto

Neno Sacco embarks on aggressive membership recruitment drive

lion in 2023 compared to Ksh5 million this year. Present economic crisis and the need to ensure that the Saccos staff are well remunerated will see staff salaries rise to Ksh 3.5 million in 2023 from the present Ksh 3 million.

Members approved an increased budget provision for bad debts to Ksh5 million for the year 2023 up from the present Ksh4 million while an extra Ksh400,000 was factored in for taxes for 2023.

Next year Ksh3 million will be spent on committee allowances and other expenses as compared to this year's Ksh2.3 million.

The budget for members’ education, committee and staff will consume Ksh5.3 million.

Management allowances will cost Ksh500,000, professional services Ksh500,000, internet services Ksh250,000 and Corporate Social Responsibility (CSR) Ksh400,000. Funds for Annual and Special General Meetings will cost Ksh1.5 million. ICT maintenance will consume Ksh600,000 while marketing, National Social Security Funds (NSSF) contributions, insurance and consultancy fee payments will each cost Ksh2 million.

By Wasike Elvis

Uasin Gishu County Government has expressed commitment to improve the livelihoods of residents through the County Enterprise Development Fund (CEDF).

Martha Cheruto, County Executive Committee Member (CECM) for Cooperatives and Enterprise Development, said the government aims to ensure that residents are empowered financially through the Fund. She called upon residents to apply for the funds to help them improve and boost their businesses.

“The funds are available and will only be given to those in groups and cooperatives,” she said.

Cheruto said that the administration will continue to provide guidelines and policies that will make CEDF self-sustainable to enable it enhance livelihoods up to the grassroot level for enhanced service delivery.

“The CEDF, which was established in 2014, has so far disbursed

loans amounting to Ksh648,939,999 to 234 Cooperative societies including; 62 marketing cooperatives, 57 investment/value addition cooperatives, 42 Saccos, 17 youth cooperatives, 19 women cooperatives, 11 traders Saccos and 26 other cooperatives on asset financing,” she added.

Cheruto noted that decentralization of services is geared towards enhancing cooperatives revolving fund to enable them access affordable funding, build a robust cooperative movement, optimize CEDF Act 2019 to streamline Fund management, and encourage Cooperative enterprises to borrow funds from the kitty.

Isaac Lagat, Acting Chief Officer for Cooperatives and Enterprise Development, said the departmental strategic plan will help them realize sustainability to enhance repayments, monitoring and evaluation notwithstanding the revival of dormant ones.

Philip Mamet, chairperson CEDF, said the loan repayments are at Ksh221,458,583 and that the Fund has asset-financed a number of cooperative societies including; Tuiyotich FCS(pickup), Tuiyoluk (Lorry), New Progressive (tractor), Olendu (sawmill and tractor) and Kibagenge bodaboda Sacco (motorbikes), among others.

Imarisha Sacco launches tailored products for new members

By Benedict Ng’etich

Imarisha Sacco has launched new tailor-made products to help new members achieve their financial dreams.

Sacco chairman Mathew Ruto noted that the products include the take off loan which caters for newly employed people and does not require one to have deposits. The repayment period is 84 months and the applicant should have minimum share capital.

interest from members’ loans was set at Ksh47 million for 2023 up from Ksh45 million

in the current year.

The cost of management risks will rise to Ksh 6 mil-

Neno Sacco is ranked one of the best managed Saccos in Mt Kenya region. It provides passenger transport and courier services across various parts of Mt Kenya region as well as Nairobi-Mombasa network.

“We have the needs of our newly employed teachers at heart hence we innovated these products to enable them access financial stability,”Ruto said.

The Sacco reviewed the amount of Karibu loan from Ksh 70,000 to Ksh 100,000. The loan doesn’t require shares but a posting letter and casualty from the school.

The superior product has a repayment period of 96 months and can be accessed by all members. One is eli-

gible for 4 times their deposits.

“We developed these products since we’re keen on ensuring that all our members from all walks of life benefit from the variety of products and services. We therefore encourage all our member to patronize the newly developed products.’’ Ruto concluded.

14 | SACCO REVIEW DEC 17, 2022 - JAN 17, 2023 EASTERN

RIFT VALLEY

Bernard Maembe, chairman Komarock Housing Cooperative Society.

Photo/ Agnes Orang’o

The head of Neno Sacco Courier Services Erphy Muriithi explains a point during an interview with the Sacco Review at his office in Embu town.

Photo/ Robert Nyagah

Mathew Ruto, Imarisha Sacco chairman

WAKENYA PAMOJA WAKENYA PAMOJA SACCO SOCIETY LIMITED

You, Our Concern ...

The Chairman, Board of Directors, Delegates, Staff and members of Wakenya Pamoja Sacco extend heartfelt congratulations to EGH Simon Kiprono Chelugui on his appointment as CS Cooperatives & Micro Small & Medium Enterprises(MSMEs) Development To

•