Earthquakes have literally shaken up our world recently. We still cannot predict them, so how best to model the financial risks? Working on a fault line in Greece, Alexandros Zimbidis and Emmanouil Louloudis have come up with a new method.

While highly volatile from year to year, economic losses from natural catastrophes (natcats) have been increasing in OECD countries since 2000 – at a slightly faster rate than GDP. The risks include floods, hurricanes, wildfires, earthquakes, tsunamis, pandemics – basically any unexpected event capable of causing extreme losses. Financial management of these risks is a key challenge for governments, insurers, banks and other institutions and is particularly important such risks and have limited capacity to manage the financial hit they cause. The importance of urgently addressing this challenge is increasingly being recognized. For example, the European Central Bank, through a report it published in December, underlined the necessity of incorporating the impact of environmental risk into the banking system using climate stress-testing exercises. The OECD has also published reports regarding flood and seismic risk. According to the seismic European hazard map provided by EFEHR (European Facilities for Earthquake Hazard and Risk), Greece is highly exposed to seismic risk. Other countries in this category include Italy, Romania and Turkey. In light of the 7.8 magnitude earthquake that hit southern Turkey and north-western Syria on 6 February this year, and the unusually strong aftershock that occurred nine hours later, it has become evident that buildings in high-risk areas need to be sturdy and have sufficient quake resistance and be constructed according to the very latest seismic codes – as well as having insurance contracts in place to protect them.

EARTHQUAKE ESSENTIALS

• Earthquakes take place along geological fault lines, where tectonic plates in the Earth’s crust lie close together

• Energy from the Earth’s core generates currents (seismic waves) in the Earth’s crust. This causes friction between plates, which then rub, scrape or bump together

• Earthquakes are more frequent than we imagine, with thousands

taking place every day. They are unnoticed because they’re small and take place far below the Earth’s surface, or deep in the seabed. The number of quakes noticeable without instruments is around 50,000 each year

• Earthquakes are measured in many different ways and on different scales. Magnitude (more correctly, the ‘moment magnitude scale’, denoted Mw) measures the strength and duration of seismic waves. Anything over 7Mw is a major event

• In 1935, the American seismologist Charles F Richter published the Richter scale: the logarithm to base 10 of the maximum seismic wave amplitude (in thousandths of a millimetre) recorded on a standard seismograph 100km from the epicentre

• About 80% of earthquakes happen along the rim of the Pacific Ocean, the Circum-Pacific Belt – also known as the Ring of Fire because of its large number of volcanoes

• About 15% of earthquakes take place along the Alpide Belt, running east from the Mediterranean through Asia and linking to the Circum-Pacific Belt

• There’s no known formula as to why earthquakes happen, so predicting them isn’t yet possible. Seismologists can look for changes in Earth elements (eg radon gas, electromagnetism, geology, geochemistry) but it’s still uncertain. This is why historical records, often sketchy and inexact, are also analysed

• Earthquakes would cause less damage if humans didn’t inhabit fault lines, invested in proper precautions and thought more

long-term about risk. It may be argued that it wouldn’t be beneficial to be able to predict them, as this would make us complacent about mitigation measures.

Declustering

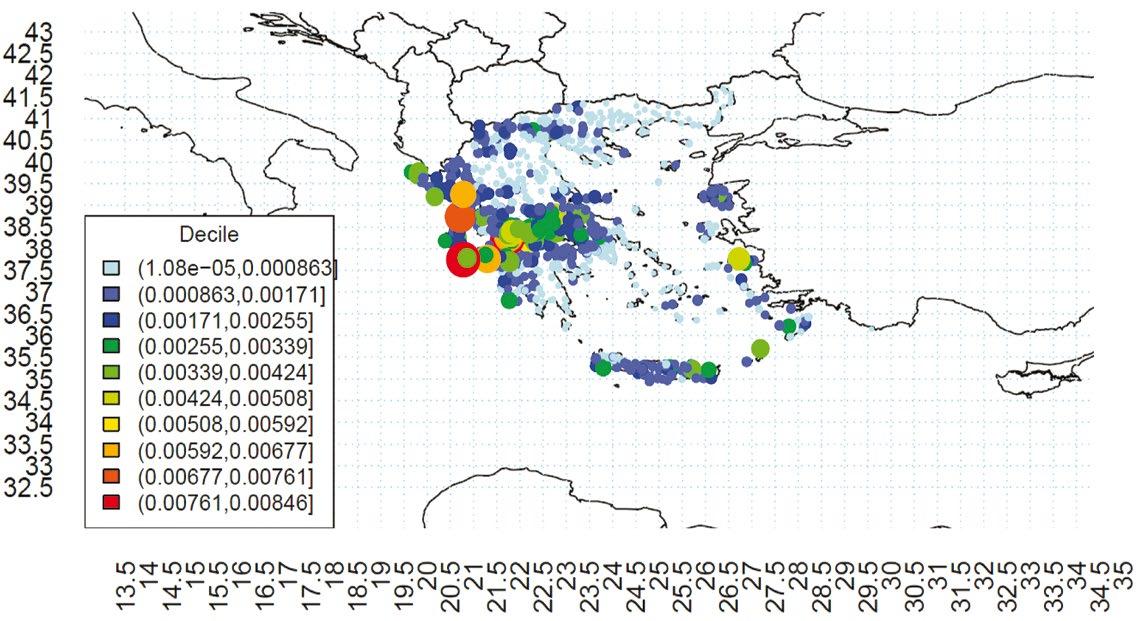

All of this makes it clear that a robust methodology for evaluating the premium rates and capital requirements associated with natcat risk is more essential than ever. As available data for historical quake events along with their associated financial consequences

EACH YEAR, 2014–23*

sufficiently modelled under a Poisson process, offering a longterm inference of each region. There are several declustering methods available. For example, an introductory algorithm was presented by Gardner and Knopoff in 1974. More complicated methods include branching processes such as the Epidemic Type Aftershock Sequence model. According to this, the background events behave as a stationary in time Poisson process, while each event – background or triggered – generates further events along a non-stationary Poisson process.