8 minute read

Is Gold Losing Its Lustre? Or Are We Just

iS iS gOlDgOlD lOSiNg iTSlOSiNg iTS luSTRE? ORluSTRE? OR aRE WEaRE wE JuST ShORT-SighTED?JuST ShORT-SighTED?

“You have to choose between trusting to the natural stability of “You have to choose between trusting to the natural stability of gold and the natural stability of the honesty and intelligence of gold and the natural stability of the honesty and intelligence of the members of the government. And, with due respect to these the members of the government. And, with due respect to these gentlemen, I advise you, as long as the capitalist system lasts, to gentlemen, I advise you, as long as the capitalist system lasts, to vote for gold.” —George Bernard Shaw vote for gold.” —George Bernard Shaw

Much is being made of gold’s recent price performance, with many questioning whether the yellow metal can still fulfill its traditional role as a safe-haven asset in turbulent times, as well as a hedge against skyrocketing inflation. After all, shouldn’t developments over the past couple of years – a global pandemic, unprecedented government spending, European war, global uncertainty, and rampaging inflation - provide the perfect springboard for gold to thrive? The fact that questions are being asked about gold’s relevance is not at all a new phenomenon. Indeed, over recent decades with the advent of newfangled financial instruments and the emergence of cryptocurrencies, some speculators have become captivated by these shiny new financial market trinkets - to the detriment of gold. But does this necessarily mean that gold is losing out in terms of performance? Gold’s relevance is typically measured and interpreted on the basis of its US dollar price performance - but this should not be viewed in perfect isolation - as gold’s performance must also be viewed in the context of how it has performed in terms of other currencies, and also against other asset classes. Let’s begin with an examination of how gold has performed so far in 2022. Although gold is down for

Much is being made of gold’s recent price performance, with many questioning whether the yellow metal can still fulfill its traditional the year in US$ terms below $1700, it is nevertheless outperforming most major asset classes - including Treasury bonds, U.S. corporate bonds, the S&P role as a safe-haven asset in turbulent times, as 500 and tech stocks. Gold has therefore effectively well as a hedge against skyrocketing inflation. After fulfilled its role as an insurance policy, by helping all, shouldn’t developments over the past couple of investors mitigate losses in other areas of their years – a global pandemic, unprecedented govern- portfolio. ment spending, European war, global uncertainty, and rampaging inflation - provide the perfect springboard for gold to thrive? The fact that questions are being asked about gold’s relevance is not at all a new phenomenon. Indeed, over recent decades with the advent of newfangled financial instruments and the emergence of cryptocurrencies, some speculators have become captivated by these shiny new financial market trinkets - to the detriment of gold. But does this necessarily mean that gold is losing out in terms of performance? Gold’s relevance is typically measured and interpreted on the basis of its US dollar price performance - but this should not be viewed in perfect isolation - as gold’s performance must also be viewed in the context of how it Furthermore, the latest report by the World Gold has performed in terms of other currencies, and also Council (WGC) also makes the case that gold can against other asset classes. typically be a powerful investment in the face of a potential economic recession. The London-based Let’s begin with an examination of how gold has group has compared the performance of a number performed so far in 2022. Although gold is down for of asset classes during the course of the past seven

the year in US$ terms below $1700, it is nevertheless outperforming most major asset classes - including Treasury bonds, U.S. corporate bonds, the S&P 500 and tech stocks. Gold has therefore effectively fulfilled its role as an insurance policy, by helping investors mitigate losses in other areas of their portfolio. Furthermore, the latest report by the World Gold Council (WGC) also makes the case that gold can typically be a powerful investment in the face of a potential economic recession. The London-based group has compared the performance of a number of asset classes during the course of the past seven U.S. recessions going back to 1971, and it has found that gold performed the best on average aside from government and corporate bonds. The bottom-line therefore is that gold’s performance must not be viewed simply in terms of its US$ price performance in isolation, but it must also be viewed within the context of how well it has stacked up against other asset classes. On this basis, gold’s performance stacks up very well indeed. What we know about gold so far in 2022 is that it has struggled in US$ price terms since April, due to the combined strength of a rampaging US dollar that is at fresh 20-year highs, along with the relentless march of the US Federal Reserve’s rate hike

Figure 1: gold versus other major asset classes over a 2-year period.

U.S. recessions going back to 1971, and it has found that gold performed the best on average aside from government and corporate bonds.

Figure 2: gold versus other major asset classes during seven recessionary periods since 1971.

Figure 3: gold price Performance Since March 2022. Figure 4: gold versus the uS dollar index over the past 12 months.

Figure 5: gold versus the uS dollar index over the past five years.

The bottom-line therefore is that gold’s performance must not be viewed simply in terms of its US$ price performance in isolation, but it must also be viewed within the context of how well it has stacked up against other asset classes. On this basis, gold’s performance stacks up very well indeed.

What we know about gold so far in 2022 is that it has struggled in US$ price terms since April, due to the combined strength of a rampaging US dollar that is at fresh 20-year highs, along with the relentless march of the US Federal Reserve’s rate hike program, which shows no signs of easing any time soon. In fact, markets are anticipating an even more aggressive tone from the Fed. This has seen US$ gold fall below $1700 per ounce.

Whilst gold is traditionally seen as a hedge against inflation, rapidly escalating interest rates nevertheless mean that investors weigh up the opportunity cost of holding gold bullion/futures - as neither generate any interest income. So a rising dollar can be somewhat of a drain on gold’s appeal.

However, it’s also important to look more closely at the performance of gold versus the US dollar over different timeframes. If we look at a chart of gold versus the US currency over the past 12 months, as represented by Figure 4 below, we see clearly that the dollar has outperformed, whilst gold has underperformed.

However, if we examine the respective performances over a broader five-year period, we see that gold has actually outperformed the US dollar, as shown in Figure 5 below.

We can even examine the relative performances over an even longer period, as shown in Figure 6 below, which represents a +20-year timeframe.

So, the bottom-line is that to formulate a view on

Figure 6: gold versus the uS dollar index over the past 20 years.

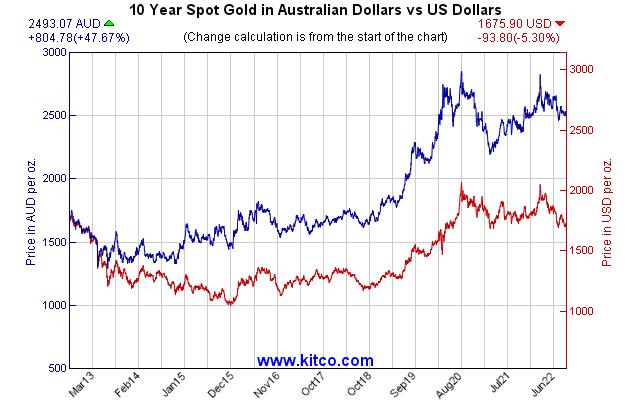

Figure 7: gold priced in yen, a$, euro and Brazilian real, compared with uS dollar price, over the past 10 years.

gold’s underlying performance and relevance, we need to view it over meaningful timeframes, and also against other asset classes.

It’s also worthwhile comparing the yellow metal’s performance not just within the context of the US dollar price alone, but in terms of other major world currencies. This way, we can analyse gold’s performance away from the influence of the US dollar, which as we know is trading at a 20-year high, thus hampering gold’s performance in terms of this metric.

Below we have four graphics that compare the respective performances of gold priced in four different currencies – the Japanese yen, Australian dollar, the Euro and the Brazilian real.

In all of the four examples above, gold priced in these currencies outperformed the US dollar price of gold over the past 10-year period, to varying degrees.

CONCLUSION

Gavin is based in Sydney, Australia and has followed the fortunes of international resource markets for the past 25 years, covering both equities and commodities, as a research analyst. He believes that the most interesting resource opportunities are typically found at the smaller end of the market, which is his exclusive area of focus.

The resource sector is on an inexorable growth path, driven by an ever-increasing world population and modernization of living standards in emerging economies, as well as a significant shift in how we generate energy. This will provide enormous growth in the demand for commodities of all types.

Gavin is the Head of Mining & Metals with research group Independent Investment Research (IIR) and he is the Founding Director and Senior Resource Analyst with MineLife.

Whilst many might question gold’s relevance based on an apparent underperformance in US dollar price terms, it is important to fully comprehend the bigger picture. It is apparent that when we look past gold’s price performance solely within the context of the US currency, we see that the yellow metal has performed strongly against other major asset classes, it has performed strongly when priced in terms of other major world currencies, and it has even performed strongly in US$ terms.

Gold then appears not to have lost its lustre – rather, it is sections of the market that appear to have become short-sighted.