20

CHAPTER : TAX INVOICE VIS-À-VIS E-INVOICE

1

4

12

CHAPTER : RECEIPT, REFUND AND PAYMENT VOUCHER

250

CHAPTER : E-INVOICING - BACKGROUND & CONCEPT - CAPSULES

CODE 261 ANNEXURES ANNEXURE 1 : RELEVANT SECTIONS & RULES 291 ANNEXURE 2 : RELEVANT NOTIFICATIONS 309 ANNEXURE 3 : CONCEPT NOTE ON E-INVOICE MESSAGING FLOW 313 ANNEXURE 4 : FAQs ON SIGNED QR CODE 327 ANNEXURE 5 : SIGNED QR CODE IN E-INVOICING SYSTEM 329 I-5

CHAPTER 9 : BILL OF SUPPLY VIS-À-VIS E-BILL OF SUPPLY

207

8

7

CHAPTER : E-INVOICE CREATION & IT IMPLEMENTATION

222

CHAPTER : DEBIT-CREDIT NOTE VIS-À-VIS E-DEBIT-CREDIT NOTE

11

CHAPTER : QUICK RESPONSE (QR)

Chapter-heads

5

1

246

PAGE

51

DOCUMENTS 253

13

CHAPTER 6 : E-INVOICING SCHEMA/API - THE CHANGE IN IT SYSTEM

CHAPTER : ISD INVOICE AND MISCELLANEOUS

3

CHAPTER : NEED OF E-INVOICING

28

CHAPTER : TIME & MANNER OF ISSUANCE - INVOICE VIS-À-VIS E-INVOICE

85

241

2

10

CHAPTER : MECHANISM OF E-INVOICING

CHAPTER : AMENDMENT, CANCELLATION & MISCELLANEOUS TOPICS OF E-INVOICING

72

1 E-INVOICING - BACKGROUND & CONCEPT - CAPSULES 1.1 1 1.2 1 1.3 3 1.4 3 1.5 4 1.6 4 1.7 5 1.8 7 1.9 7 1.10 11 2 NEED OF E-INVOICING 2.1 20 2.2 20 2.3 25 2.4 27 I-7 Contents

3 MECHANISM OF E-INVOICING 3.1 28 3.2 30 3.3 33 3.4 34 3.5 35 4 E-INVOICE CREATION & IT IMPLEMENTATION 4.1 51 4.2 68 4.3 69 4.4 70 5 AMENDMENT, CANCELLATION & MISCELLANEOUS TOPICS OF E-INVOICING 5.1 72 5.2 72 5.3 73 5.4 75 5.5 75 5.6 78 5.7 82 6 E-INVOICING SCHEMA/APITHE CHANGE IN IT SYSTEM 6.1 85 I-8

6.2 85 6.3 86 6.4 86 6.5 86 6.6 86 6.7 87 6.8 87 6.9 87 6.10 87 6.11 87 6.12 87 6.13 88 6.14 97 6.15 102 6.16 129 7 TIME & MANNER OF ISSUANCEINVOICE VIS-A-VIS E-INVOICE 7.1 207 7.2 209 7.3 213 7.4 213 8 TAX INVOICE VIS-A-VIS E-INVOICE 8.1 222 8.2 223 8.3 227 8.4 228 I-9

8.5 230 8.6 230 8.7 231 8.8 235 8.9 236 8.10 vis-a-vis 236 8.11 238 8.12 238 8.13 240 8.14 240 9 BILL OF SUPPLY VIS-A-VIS E-BILL OF SUPPLY 9.1 241 10 DEBIT-CREDIT NOTE VIS-A-VIS E-DEBIT-CREDIT NOTE 10.1 246 10.2 vis-a-vis 248 11 RECEIPT, REFUND AND PAYMENT VOUCHER 11.1 250 11.2 251 11.3 252 I-10

12 ISD INVOICE AND MISCELLANEOUS DOCUMENTS 12.1 253 12.2 254 12.3 255 12.4 255 12.5 256 12.6 257 12.7 258 12.8 259 13 QUICK RESPONSE (QR) CODE 13.1 261 13.2 261 13.3 262 13.4 264 13.5 265 13.6 267 13.7 278 13.8 278 13.9 278 13.10 281 13.11 281 13.12 282 I-11

Annexure 3 313

ANNEXURES

Annexure 4 327

Annexure 2 309

I-12

Annexure 5 329

13.14 v. 285

13.13 284

Annexure 1 291

4.1 CREATION OF AN E-INVOICEba E-INVOICE CREATION & IT IMPLEMENTATION 4 CHAPTER 51

Part A: Flow from known as seller) to IRP

Supplier (commonly

STEP

1: DoesSituation:thetaxpayer needs to mention the “mandatory parameters” as stated in the e-invoice schema/standards/APIs? Solution: Notification No. 60/2020-Central Tax dated 30th July, 2020. Para 4.1 52

` 53 Para 4.1

HowSituation:small taxpayers will adopt the e-invoicing in case they do not have the accounting software?

Solution:

STEPwww.gstn.org.in2:Thisisan optional step “Proposed e-invoicing System” dated 12th February, 2020 CanSituation:thetaxpayer generate the IRN by his own and print the invoice? Solution: Para 4.1 54

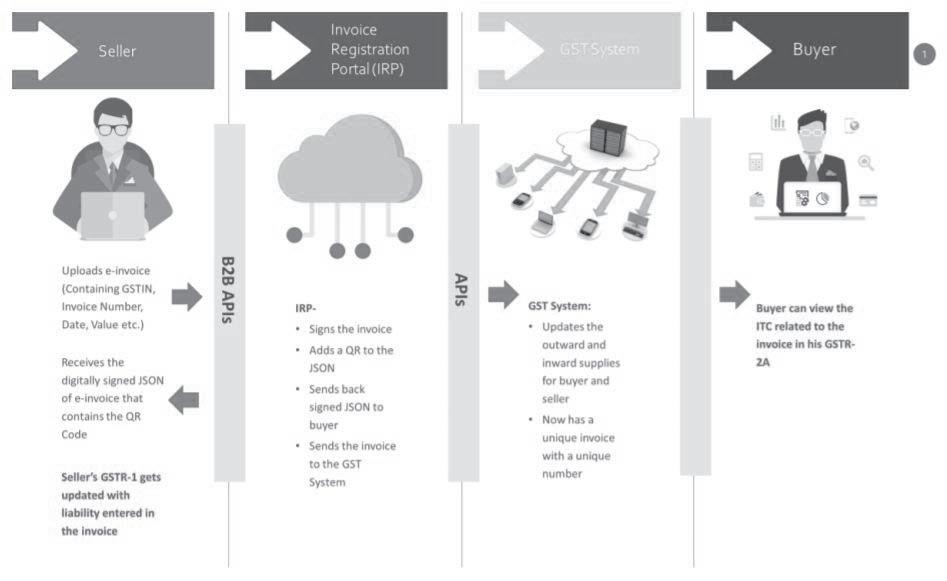

Note: It is important to note that the proposed New GST Returns has been scrapped and the existing returns mechanism is modified. Accord ingly, the above flow of communication to the extent of auto-population in GST ANX-1 may get changed to GSTR 1 and buyer can view the ITC related to the e-invoice in his GSTR 2A/2B instead of GST ANX-2. The aforesaid view on account of modified GST return has been duly answered in the updated image as shown below which is available on

For example: SHA-256 hash of ‘abc’ would be: ba7816bf8f01cfea414140de5dae2223b00361a396177a9cb410ff 61f20015ad.

MeaningSituation:of hash generation algorithm e.g. SHA256

“Proposed e-invoicing System” dated 12th February, 2020

Hashing function or cryptographically secure hashing function

DoesSituation:the3 parameters set the uniqueness of the IRN sufficient or does it require any other parameter to set in?

55 Para 4.1

not make the invoice valid

Solution:

Unique Invoice Reference Number [IRN], also known as HASH: legal invoice

Solution: cryptographic hashSHA-256

FAQ E-invoice Roll-out by GSTN released on 26th December,“Proposed2019e-invoicing System” dated 12th February, 2020

API Based:

STEP 3:

Taxpayers with Aggregate Turnover of < Rs. 500 Crores: Through E-Way Bill APIs –GSPs –

GST Suvidha Providers/ERPs No.Sl. GSP/ERP Name Contact E-mail-Id Para 4.1 56

Solution:

HowSituation:conversion of invoice details will happen in JSON format that needs to be uploaded on the IRP.

Through

57 Para 4.1

No.Sl.

GSP / ERP Name Contact E-mail-Id

No.Sl.

GSP / ERP Name Contact E-mail-Id

Para 4.1 58

GSP / ERP Name Contact E-mail-Id

Through Entities having direct Access to APIs – e.g

No.Sl.

59 Para 4.1

Through ERPs or Billing/Accounting Software Service Providers –

60

Taxpayers with Aggregate Turnover of > Rs. 500 Crores:

“Proposed e-invoicing System” dated 12th February, 2020

STEP 4:

Web based: GST e-invoice system FAQ version 1.4 dated 31-3-2021

GST e-invoice system FAQ version 1.4 dated 31-3-2021

The hash computed by IRP will become the IRN (Invoice Reference Number) of the e-invoice.

SMS based:

“Proposed e-invoicing System” dated 12th February, 2020

Offline Utility Based:

Mobile App based:

Para 4.1

Direct Access to API–

WhatSituation:isthe use of QR Code? How QR Code can be used to verify the details of invoices? Can the user print the e-invoice using the QR Code? Solution: central portal

Facts about IRN

The QR code will enable quick view, validation and access of the invoices from the GST system from hand held devices

Offline App 61 Para 4.1

GST e-invoice SystemFAQs - Version 1.4 Dt. 30-3-2021

Para 4.1 62

Q81. What is dynamic QR Code? Does it have any relevance for B2B e-invoicing?

GST e-invoice/IRN System Frequently Asked Questions (Version 1.4 Dt. 30-03-2021)

An offline app e- view the e-invoice buyers on the GST system/eway bill system

h.d.b.a.c.e.f.g.i.

The facility of e-invoice verification is planned to be made available only through the GST System and not the IRP. This is because the IRP will not have the mandate to store invoices for more than 24 hours. In order to achieve speed and efficiency, the IRP will be a lean and focused portal for providing invoice registration and verification service, IRN and the QR codes. Hence, storing of the invoices will not be a feature of the IRP.

The seller will be returned a signed JSON with all details including a QR Code.

]

AUTHOR e-Invoicing NOW

: Aditya Singhania PUBLISHER : TAXMANN DATE OF PUBLICATION : August 2022 EDITION : 3rd Edition ISBN NO : 9789356223806 NO. OF PAGES : 344 BINDING TYPE : PAPERBACK GST

Description

This book serves as a ready referencer for all tax professionals, technical experts, and the project-in-charge in handling the execution of the e-Invoicing module in the existing accounting

GST

at appropriate places [Pictorial Representations] have been made for a better understanding [Impact on other Verticals of the Business] has been incorporated [Process Flow along-with Validations] done at IRP portal is also given

Publication is the 3rd Edition, amended up to 20th August 2022. This book is authored by Aditya Singhania with the following noteworthy features:

ORDER

Thesoftware.Present

USD : 39

[Tabular Presentation] has

This book is a comprehensive guide on e-Invoicing. It assists the reader in understanding the following with respect to e-Invoicing

IssuesConceptsBackground

GST

Explanation in complete sync with current features available at the following e-Invoicing Portal e-Invoice API Portal Common Portal all Key Changes that have occurred from time to time along with relevant e-schema, etc. been made for of been given

[Ascertain

GST

ascertaining the responsibility

Rs. : 795 |

annexures, FAQs,

each stakeholder involved [Situations & Solutions] have