It gives me immense pleasure to place before esteemed readers, the ninth edition of my book “GST & Customs Law”. The book is designed as per B. Com. (Hons.) syllabus of Delhi University and equivalent courses of other universities.

After the roll out of GST in India with effect from 1st July, 2017, there have been many changes in the GST laws. July 1, 2022 marked the completion of five years of this India’s ambitious law. Till date, the GST Council held 48 meetings to discuss the anomalies, approval of amendments, budget proposals and other practical issues in the implementation of GST laws. The latest GST Council’s 48th meeting was held on 17th December, 2022 virtually from New Delhi, under the chairmanship of the Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman.

The Finance Act, 2022 has amended and substituted many sections of CGST Act. The law relating to ITC and Returns have been changed significantly. Those amendments which are covered in syllabus have been incorporated in the present edition at relevant places. The chapter on “Returns” has been revised thoroughly. Other changes have also been made, keeping in view the suggestions received from the colleagues and teaching fraternity. The practical illustrations have further been added and simplified.

I am thankful to dear students who have shared their problems with me through E-mail, which really helped me towards making the book more student-friendly. My thanks are due to the publishers and the editorial team of Taxmann publications with special thanks to Mr. Mitra Pal Yadav and Mr. Sumit Dwivedi.

I am grateful to CA Raj Chawla, member-Central Council (ICAI) for disseminating the practical aspects of the law. I am also thankful to my wife. My apologies are due to my lovely kids “Vatsla and Varad” as I have spent their ‘precious time of togetherness’ in writing this book, which cannot be compensated.

I am thankful for the comments and suggestions made by the colleagues from Delhi University and other professional institutes for the improvement of the book. Further comments and suggestions for improving the quality of the book are welcome and

will be gratefully acknowledged. In case of any query, I may be reached through e-mail given below.

Dated: CA. (Dr.) K.M. Bansal

1st January, 2023 kmbansaldu@gmail.com

B.COM. (HONS.) : SEMESTER VI

PAPER BCH 6.2 : GOODS & SERVICES TAX (GST) AND CUSTOMS LAW

COURSE OBJECTIVE

Course Learning Outcomes

COURSE CONTENTS

Unit 1: Introduction

Unit 2: Levy and collection of GST

Unit 3: Input Tax Credit

Unit 4: Procedures and Special Provisions under GST

Unit 5: Customs Law

Note:

PAPER BC 5.2 (b): GOODS & SERVICES TAX (GST) AND

COURSE CONTENTS

Unit I: Introduction -

Unit II: Levy and collection of GST

Unit III: Input Tax Credit -

Unit IV: Procedures and Special Provisions under GST

Unit V: Customs Law

Note:

After studying this chapter, you shall be able to understand the following:

10.3

Burden of Proof for claiming ITC

10.4 LEGAL FRAMEWORK OF ITC

Section 16

Section 17

Section 18

Section 19

Section 41

Section 42

CGST RULES, 2017 RELATING TO ITC

Rule 36:

Rule 37:

Rule 38:

Rule 39:

Rule 40: Rule 41: Rule 42: Rule 43: Rule 44: Rule 44A: Rule 45: Utilisation of ITC

Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of business and the said amount shall be credited to the electronic credit ledger of such person

1. Registered Person:

Exception: -

2. In the course of or in furtherance of business: -

Explanation:

‘Intention to use’ implies

3. Credit Ledger:

4. Manner of Utilisation

5. Rules under CGST Rules, 2017

10.6 CONDITIONS TO BE SATISFIED FOR AVAILING ITC [SECTION 16(2)]

(a) Possession of Invoice:

Rule 36: Documentary requirements and conditions for claiming input tax credit 36(1)

(b) Furnishing and communication of details:

Author’s Comment

(

c) The ITC is not restricted:

(

d) Receipt of Goods or Services or both:

Now, in this example

When goods/Services are deemed to have been received: Statutory Provisions:

the Central GST (Amendment) Act, 2018

b for the purpose of this clause, it shall be deemed that the registered person has received the goods or, as the case may be, services— (

Analysis of the Provisions:

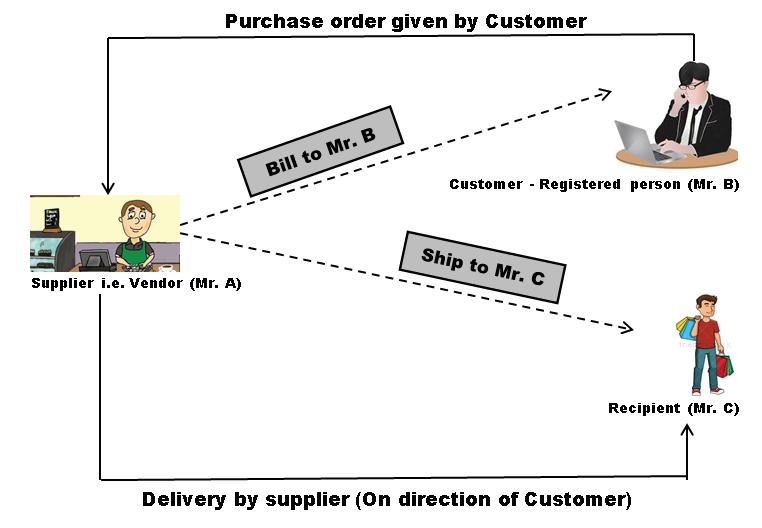

Bill to Ship to Model -

Example 10.3 [Deemed Receipt of goods]

Example 10.4 [Deemed Receipt of services]

(e) Payment of Tax to the Government

(f) Filing of valid Return: d

Solution:

Computation of admissible ITC to Nishant Limited for the month of July, 2018

Total admissible ITC for the month of July 2018 34,000

Working Notes:

When Goods are received in instalments

It has been discussed in detail in Chapter 11 under Para 11.10.

(1) ITC availed to be paid along with Interest [Second Proviso to Section 16(2)]:within 180 days

Related provisions as prescribed under Rule 37 of CGST Rules, 2017

As per Rule 37(1),

When supply is made without consideration:

As per Rule 37(2),

Please refer example 10.7 for computation of interest in case of reversal of ITC.

(2) Re-Entitlement when payment is made subsequently:

Related provisions as prescribed under Rule 37(4) of CGST Rules, 2017

10.11

(3) Exceptions to the Limitation Period of 180 days:

10.8 NO ITC IF DEPRECIATION IS CLAIMED ON TAX COMPONENT [SECTION 16(3)]

Example 10.11 [No ITC if Depreciation is claimed on tax component]

10.9 TIME LIMIT FOR AVAILING THE INPUT TAX CREDIT [SECTION 16(4)]

30th November furnishing of the relevant annual return, earlier

Earlier of Example 10.12:

Solution: Particulars CASE I CASE II

Last date by which ITC can be claimed (Earlier of the above two dates) 30-11-2023

Additional points as regards the time limits for claiming ITC

1. Relevant Date for Debit Note

2. No time limit for reclaiming ITC reversed due to non-payment within 180 days: As per rule 37 t

3. One Year from the date of Invoice in special cases: For

CGST Act, 2017

(1) Where goods or services are used partly for business purposes and partly for other purposes [Section 17(1)]

(2) Where goods or services are used partly for effecting taxable supply including zero rated supply and partly for exempted supply [Section 17(2)]

(3) Items included in exempted supplies [Section 17(3)

(4) Optional method for Banks for taking ITC [Section 17(4)]

(5) Blocked Credits [Section 17(5)]

CGST Rules, 2017

(1) ITC by a banking company or a financial institution [Rule 38]

(

2) Manner of determination of ITC in respect of Inputs or input services and reversal [Rule 42]

(3) Manner of determination of ITC in respect of Capital Goods and Reversal [Rule 43]

10.10.1 Where goods or services are used partly for business purposes and partly for other purposes [Section 17(1)]

1 “Where the goods and/or services are used by the registered person partly for the

purposes of any business and partly for other purposes, the amount of credit shall be restricted to so much of the input tax as is attributable to the purposes of his business.”

For Example:

10.10.2 Where goods or services are used partly for effecting taxable supply including zero rated supply and partly for exempted supply [Section 17(2)]

Solution: Calculation of Taxable Supplies

Total Taxable Supplies 24,00,000

Total Supplies during the month `

Calculation of Taxable Supplies as a Percentage of total supplies = Taxable Supplies Total Supplies × 100 = 24,00,000 30,00,000 × 100 = 80%

ITC Available ` ` Rule 42 and Rule 43 of CGST Rules, 2017 [Apportionment of Common Credit]

10.10.3 Items included in exempted supplies [Section 17(3)]

Taxable supplies 108

Exempted supplies:

The Central GST (Amendment) Act, 2018

For the purposes of section 17 3 , the expression “Value of Exempt Supply” shall not include the value of activities or transactions specified in Schedule III, except those specified in paragraph 5 of the said Schedule.”

(1) Availability of 50% of total ITC:

(2) Availability of 100% of total credit:

(3) Non-Availability of ITC for Non-Business use and of Blocked Credits:

(4) Option applicable for Financial Year:

Example 10.17 [Comparison of section 17(2) and 17(4)]

Particulars Input Tax (`) (CGST & SGST

Alternative 1

Alternative 2

Solution:

Alternative 1: When the bank has opted section 17(2)

Total Supplies = `

Total ITC = ` `

Net ITC Available

CGST Available = Taxable Supplies Total Supplies × = 8,00,000 20,00,000 × ` `

SGST Available = `

Alternative 2: When the bank has opted section 17(4)

Total ITC Available = ( )

CGST Available = ` `

SGST Available = ` `

ITC [Section 17(5)]

The section 17(5) of CGST Act, 2017 has listed down specific goods and services, in respect of which ITC is not available, irrespective of their use in business. These are termed as Blocked Credits

(a) Motor vehicles

[As substituted by CGST (Amendment) Act, 2018]

(A)

(B)

(C)

except

Remarks on amendment made by CGST (Amendment) Act, 2018:

(1) vehicles for transportation of persons capacity 13 persons not allowed

(2) vehicles for transportation of persons capacity > 13 persons allowed

(3)

Examples: Where ITC is not allowed [ITC is blocked]

Examples: Where ITC is allowed [Exception to Section 17(5)(a)]

(aa) Vessels and Aircraft except

Remarks on amendment made by CGST (Amendment) Act, 2018:

Examples: 1. allowed 2. not allowed

(ab) Specific Services relating to Motor vehicles, Vessels and Aircraft

Provided

Author’s Remarks on above provision:

not allowed

allowed

Examples:

(b) Specific Supply of Goods or services or both

Author’s Remarks on above provision:

1. Food and beverages……: is allowed

2. Membership of club…..Travel benefits……: is allowed

Examples:

1.

2.

(ITC allowed)

3. (ITC Not allowed) 4. ` (ITC Not allowed) 5.

Explanation:

PUBLISHER : TAXMANN

DATE OF PUBLICATION : JANUARY 2023

EDITION : 9th Edition

ISBN NO : 9789356226401

NO.OF PAGES : 640

BINDING TYPE : PAPERBACK

Rs. 895 USD 45

Taxmann's flagship publication on GST & Customs Law aims to fulfil the requirement of students of undergraduate courses in commerce and management, particularly the following:

• Choice-Based Credit System

• B.Com. (Hons.) Semester VI: Paper BCH 6.2: Goods and Services Tax (GST) and Customs Law

• B.Com. Semester V: Paper BC 5.2(b): Goods & Services Tax (GST) and Customs Law

• Non-Collegiate Women's Education Board

• School of Open Learning of the University of Delhi

• Various Central Universities throughout India. This book aims to minimize the need to consult multiple books while preparing for the exam and give the students a step-by-step guide for learning the subject.

This book is written in simple language, explaining the provision of the law in a step-by-step manner with the help of suitable illustrations, without resorting to paraphrasing of sections and legal jargons. This book helps bridge the gap between theory and application of the subject matter.